management accounting in a changing environment chapter fourteen

TRANSCRIPT

Management Accounting in a Changing Environment

Chapter Fourteen

14 - 3

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Outline of Chapter 14Management Accounting in a Changing

Environment

• Integrative Framework • Organizational Innovations and Management Accounting• When Should the Internal Accounting System be Changed?

14 - 4

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Connection to Other Chapters

• Chapter 14 summarizes the concepts developed in the previous chapters and applies them to recent internal accounting system innovations.

• Every chapter mentions the trade-offs between decision management (decision making) and decision control.

• Internal accounting systems continue to evolve in response to changing needs and environments.

14 - 5

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

History of Management Accounting

• As firms evolve, internal accounting systems evolve.• Early 1800s: Multi-process textile mills develop absorption costing.• 1850 - 1910: Multi-location firms create cost controls.• 1915 - 1925: Large corporations decentralize in operating divisions.• 1925 - 1975: External reporting dictates internal accounting design.• Recent: Automation induces redesign of product costing.• Recent: TQM requires more non-financial measures• Recent: JIT producers want to identify non-value-adding

activities.• Recent: The Balanced Scorecard links strategy to key performance

indicators to help determine if the organization is moving in the right direction.

14 - 6

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Organizational Architecture

• See Figure 14-1.• Decision rights partitioning

- Separating decision management and control

• Performance evaluation system- Management accounting system- Nonfinancial measures

• Performance reward and punishment system

14 - 7

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Business Strategy

• Asset structure influences performance measurement.- Some firms can use historical financial accounting.- Publicly-traded firms may use stock market value.

• Customer base influences distribution of specialized knowledge.- May decentralize into many responsibility centers

• Knowledge creation influences partitioning of decision rights.- If knowledge is easy to acquire, more centralization is possible.

14 - 8

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Environmental and Competitive Forces

• Technological change- Changes relative value of investment projects- Changes performance measures and controls

• Global market conditions change- Production sources dispersed internationally- Competitors from other countries

14 - 9

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Quality’s Multiple Meanings

• Different meanings of quality can conflict.• High mean• Low variance• Larger number of options• Meeting customer expectations

• Partitioning decision rights• Who determines quality goals?• Who measures quality?

14 - 10

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

TQM Program Elements

• A firmwide process- communicate up, down, and laterally

• Quality is defined by customer- specialized knowledge of customer needs

• Requires organizational changes- push decision rights down to operating and marketing

• Designed into the product- Reduce defects by redesigning production

14 - 11

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

ISO 9000

• Issued by International Standards Organization, a European community body that sets quality standards.

• Requires written policies, procedures, and quality methods.

• Certifies that policies exist that allow quality products to be manufactured.

14 - 12

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

TQM Quality Costs

• Benefits• Reduce internal failures (before sold)• Reduce external failures (after sold)

• Costs• Prevention (reengineering and training)• Appraisal (inspection and testing before delivery)

• Find optimal balance between benefits and costs.

• See Self-Study Problem 1.

14 - 13

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

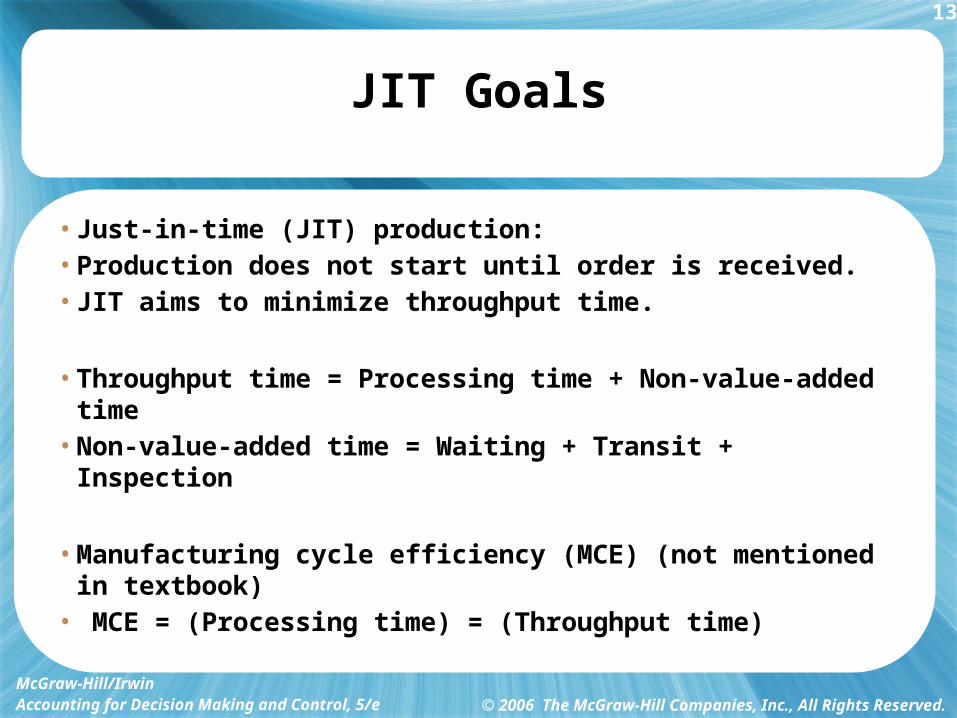

JIT Goals

• Just-in-time (JIT) production:• Production does not start until order is received.• JIT aims to minimize throughput time.

• Throughput time = Processing time + Non-value-added time• Non-value-added time = Waiting + Transit + Inspection

• Manufacturing cycle efficiency (MCE) (not mentioned in textbook)

• MCE = (Processing time) = (Throughput time)

14 - 14

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

JIT Techniques

• Increase quality of material and processes• Reduce setup times• Balance flow rates across manufacturing cells• Coordinate deliveries from suppliers• Improve factory layout to reduce transit time• Change performance measurement and reward system to

focus on reducing throughput time of entire production process rather than individual departments

14 - 15

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

JIT Cost Flows

• See Figure 14-3. Compare to Figure 9-1.

• Raw and In-Process (RIP) combines raw materials and work-in-process.

• Conversion Cost combines direct labor and all manufacturing overhead.

• Backflushing: As work completed, transfer costs to finished goods• from RIP using standard rates or specific identification• from conversion costs using throughput time or other allocation base

• See Self-Study Problem 2.

14 - 16

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

JIT Limitations

• Advantages:• Simpler because no work-in-process accounting• Focus attention on throughput time

• Disadvantages:• Become dependent on suppliers for on-time delivery• Still need periodic physical count of materials inventory• Reorganizing production can be expensive.

14 - 17

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Balanced Scorecard

• Translates the strategy into a plan of action• Identifies specific objectives and performance drivers (key

performance indicators)• Helps determine if the organization is moving in the right

direction

14 - 18

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

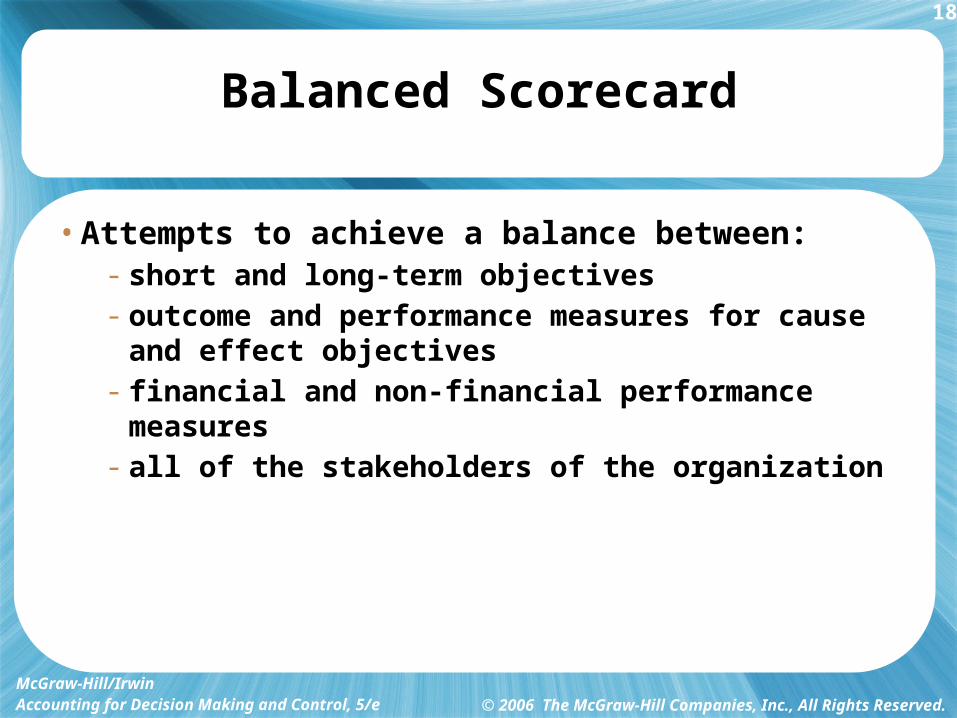

Balanced Scorecard

• Attempts to achieve a balance between:- short and long-term objectives- outcome and performance measures for cause and effect

objectives- financial and non-financial performance measures- all of the stakeholders of the organization

14 - 19

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Balanced Scorecard

• For each objective there are - Driver performance indicators

• measure input activities to achieve the objective- Outcome performance indicators

• Measure if the objective has been realized- Driver and outcome performance indicators reflect the

cause and effect nature of the balanced scorecard.

14 - 20

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

The Balanced Scorecard’s Four Perspectives

Innovation and Learning Perspective

Customer Perspective

STRATEGYFinancial

Perspective

Internal Business Processes

Perspective

14 - 21

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

Example Objectives, Performance Indicators, and Targets

• Review Table 14-1.• Pay particular attention to the specificity of the definition of

each element, particularly the targets.

14 - 22

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

What Makes the Balance Scorecard a Success or a Failure?

• Example 1: Philips Electronics (a success)• Example 2:The U. S. retail banking operations of a leading

international financial services provider (a failure)• Summarize what is needed to achieve success and avoid

failure.

14 - 23

McGraw-Hill/IrwinAccounting for Decision Making and Control, 5/e

© 2006 The McGraw-Hill Companies, Inc., All Rights Reserved.

When Should the Internal Accounting System be Changed?

• Continual evolution (economic Darwinism)• No ideal management accounting system• Respond to changes in technology and markets

• Trade-offs• Decision making vs. Decision control• Opportunity cost vs. Historical cost• Simplicity vs. Comprehensiveness• Internal users vs. External users• Financial measures vs. Nonfinancial measures