management accounting 1 syllabus--read this carefully. it is a contract

TRANSCRIPT

Management Accounting 1

Syllabus--Read this carefully. It is a contract.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Professor Daly’s Website

Syllabus, lecture notes, quiz and test grades, etc.

http://kbiz.khu.ac.kr/professor/12.php

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Classroom Conduct

Class starts promptly at:10:30 for sections A0309602

1:30 for sections A0309603

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Classroom Conduct

You are expected to prepare for class: Read the chapter in textbook Write answers to assigned

questions, exercises and problems.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Classroom Conduct

Bring your textbook and a calculator to class.

No computer use during class.Show respect for me and your

classmates by turning off your cell phone prior to class.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Required text: Managerial

Accounting, 13th Edition,Garrison Noreen, and Brewer, International Edition

Connect, online program, access code included on postcard inserted in textbooks sold at university bookstore

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

To Register for Connect

On the worldwide web, go to the online address (URL) for your section of the course.

(Address distributed in class)

Enter the access code, and other items requested

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Connect URL for assistance

http://mpss.mhhe.com/connectlinks.php

This site provides instructions for registration and using Connect

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Connect Assignments

Assignments preceded by a barbell symbol are for Practice.

These may be completed at any time, may be re-worked with different fact patterns, and are ungraded.

Practice with these before attempting the graded assignments.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Connect Assignments

Assignments preceded by a “page” symbol are graded.

Must be completed by the end date indicated in the Availability column---only 1 attempt permitted.

Due by midnight on Friday of the week in which assigned.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Additional Online Learning

For supplemental material such as:

chapter outlines

videos

practice quizzes

www.mhhe.com/garrison13e

Managerial Accounting and the Business Environment

Chapter 1

Managerial Accounting and Financial Accounting

Managerial accountingprovides informationfor managers of anorganization whodirect and control

its operations.

Financial accountingprovides information

to stockholders,creditors and others

who are outsidethe organization.

Expanding Role of Managerial Accounting

Increasing complexity andsize of organizations

Rapid development andimplementation of technology

Regulatoryenvironment

World-widecompetition

Increasedemphasison quality

Factors thatincrease the need for

managerial accountinginformation

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Traditional “Push”Manufacturing Company

Forecast Sales Order components

Produce goods in Anticipation of Sales

Make Sales from Finished Goods

Inventory

Store Inventory

StoreInventory

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Traditional “push”manufacturing

Traditional “Push”Manufacturing Company

Largeinventories

Finishedgoods

Rawmaterials

Work inprocess

Materials waitingto be processed.Materials waitingto be processed.

Completed products awaiting sale.

Completed products awaiting sale.

Partially completed products requiring more work before

they are ready for sale.

Partially completed products requiring more work before

they are ready for sale.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

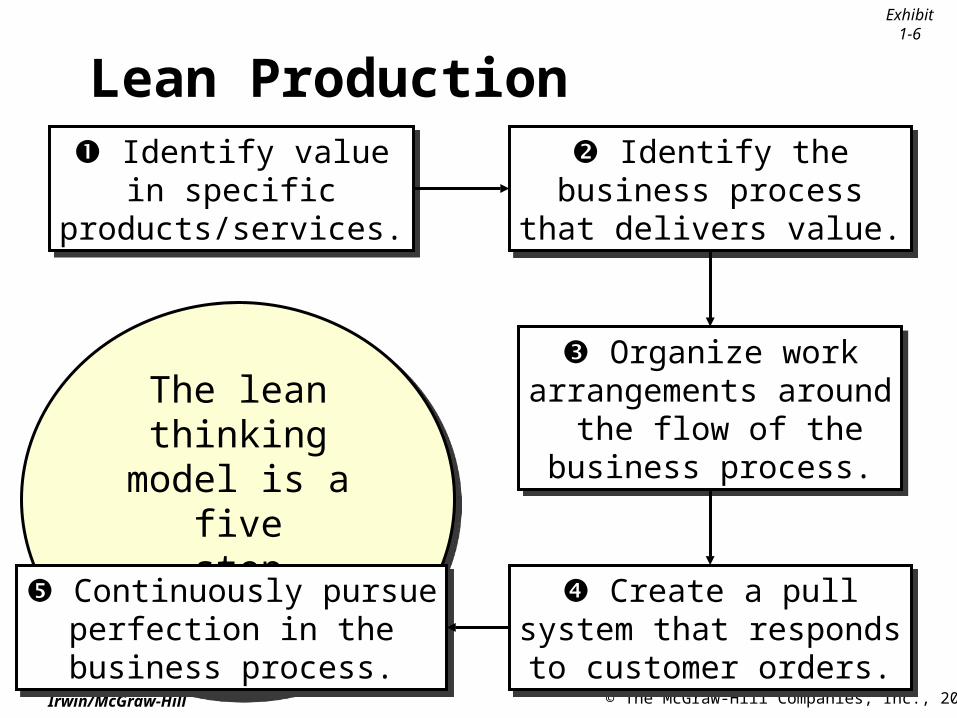

Lean Production

Exhibit1-6

The lean thinkingmodel is a fivestep approach.

The lean thinkingmodel is a fivestep approach.

Identify valuein specific

products/services.

Identify valuein specific

products/services.

Identify thebusiness process

that delivers value.

Identify thebusiness process

that delivers value.

Organize workarrangements around

the flow of thebusiness process.

Organize workarrangements around

the flow of thebusiness process.

Create a pullsystem that respondsto customer orders.

Create a pullsystem that respondsto customer orders.

Continuously pursueperfection in the

business process.

Continuously pursueperfection in the

business process.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

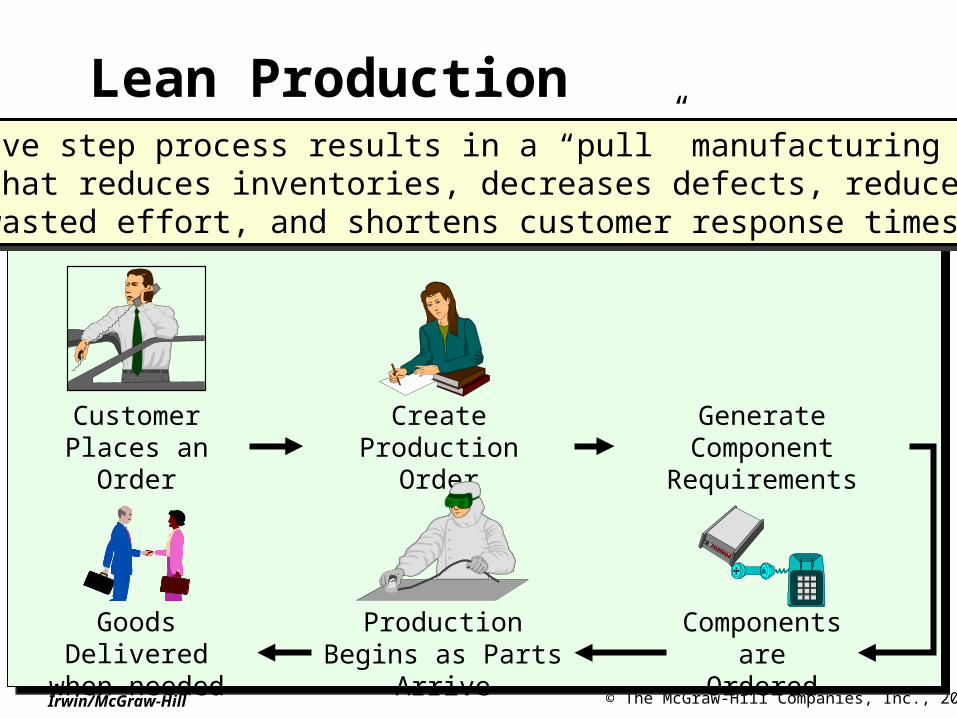

Customer Places an Order

Create Production Order

Generate Component Requirements

Production Begins as Parts Arrive

Goods Delivered when needed

Components are Ordered

Lean ProductionThe five step process results in a “pull” manufacturing system

that reduces inventories, decreases defects, reduceswasted effort, and shortens customer response times.

The five step process results in a “pull” manufacturing systemthat reduces inventories, decreases defects, reduceswasted effort, and shortens customer response times.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

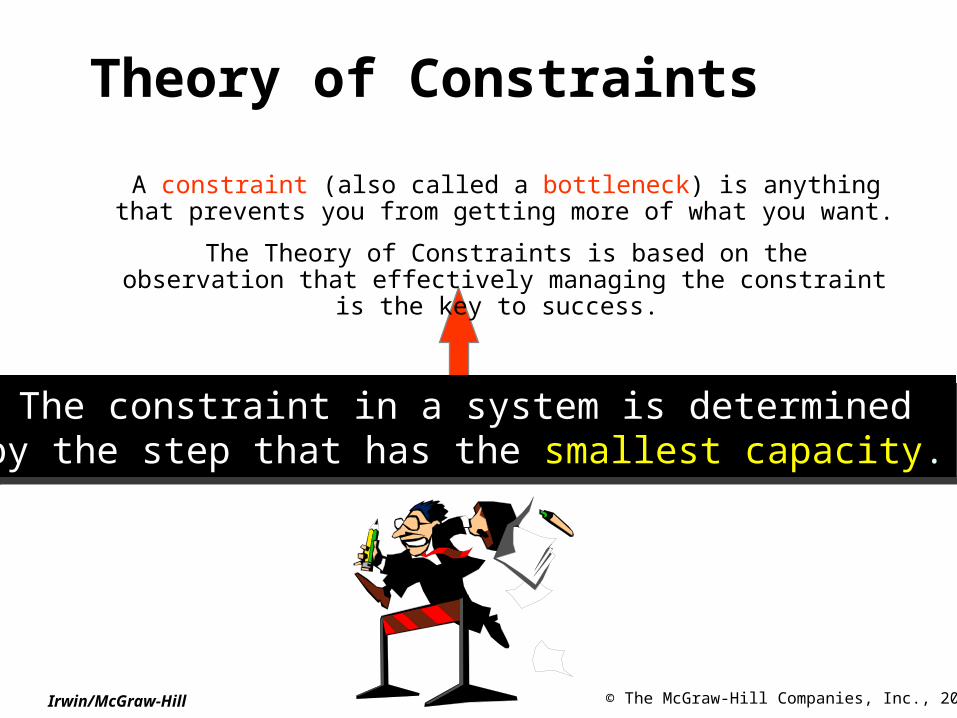

A constraint (also called a bottleneck) is anything that prevents you from getting more of what you want.

The Theory of Constraints is based on the observation that effectively managing the constraint is the key to success.

The constraint in a system is determinedby the step that has the smallest capacity.

The constraint in a system is determinedby the step that has the smallest capacity.

Theory of Constraints

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

4. Recognize that the weakest linkis no longer so.

4. Recognize that the weakest linkis no longer so.

1. Identify the weakest link.

1. Identify the weakest link.

2. Allow the weakest link to set the tempo.

2. Allow the weakest link to set the tempo.

3. Focus on improving

the weakest link.

3. Focus on improving

the weakest link.

Only actions that strengthen the weakest link in the “chain” improve the process.

Theory of Constraints

Importance of Ethicsin Accounting

Ethical accounting practices build trust and promote loyal, productive relationships with users of accounting information.

Many companies and professional organizations, such as the Instituteof Management Accountants (IMA),have written codes of ethics whichserve as guides for employees.

IMA Code of Ethics for Management Accountants

Competence

Confidentiality

Integrity

Credibility

Resolution of Ethical Conflict

Competence

Confidentiality

Integrity

Credibility

Resolution of Ethical Conflict

IMA Code of Ethics for Management Accountants

Follow applicable laws, regulations and

standards.

Prepare complete and clear reports after appropriate

analysis.

Maintain professional

knowledge and skills.

Competence

IMA Code of Ethics for Management Accountants

Do not disclose confidential information unless legally

obligated to do so.

Ensure that subordinates do not disclose confidential

information.

Do not use confidential

information for personal

advantage.

Confidentiality

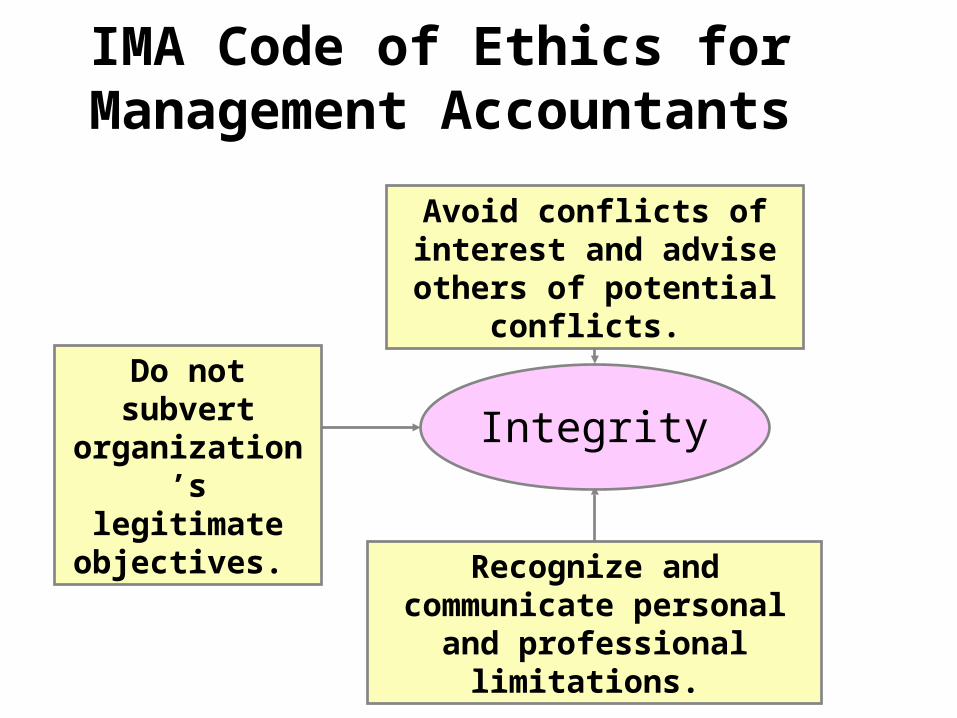

IMA Code of Ethics for Management Accountants

Avoid conflicts of interest and advise others of potential conflicts.

Recognize and communicate personal and

professional limitations.

Do not subvert organization’s

legitimate objectives.

Integrity

IMA Code of Ethics for Management Accountants

Integrity

Avoid activities that could affect your ability to

perform duties.

Communicate unfavorable as well as favorable information.

Refrain from activities that could

discredit the profession.

Refuse gifts or favors

that might influence behavior.

IMA Code of Ethics for Management Accountants

Credibility

Disclose deficiencies or delays

in information, timeliness, or internal controls

IMA Code of Ethics for Management Accountants

Credibility

Communicate information fairly and objectively.

Disclose all information that might be useful to

management.

Resolution of Ethical Conflict

Follow established policies.

For unresolved ethical conflicts:

Discuss the conflict with immediate superior.

If immediate superior is the CEO, consider the board of directors or the audit committee.

Except where legally prescribed, maintain confidentiality.

IMA Code of Ethics for Management Accountants

Resolution of Ethical Conflict

Clarify issues in a confidential discussion withan objective advisor.

Consult an attorney as to legal obligations.

The last resort is to resign.

IMA Code of Ethics for Management Accountants