malta and the eu 9 years down the line 1 horizon 3: aviation horizon 1: shipping (since 1973)...

TRANSCRIPT

Malta and the EU9 Years down the line

1

Horizon 3: Aviation

Horizon 1: Shipping

(Since 1973)

Horizon 2: Banking

InsuranceInvestment Services & Funds Multi-nationals

(Since 1994)

… alchemy of growth

9 Years down the lineThe last 8 years have changed our countrydramatically and positively.

The majority of Maltese citizens recognise this

reality, notwithstanding differing politicalaffiliations.

Eurobarometer has recently found that thenumber of Maltese who believe that the EU

hasbeen of benefit to the country exceeds those

whodo not by a ratio of more than two to one.

Eurobarometer Survey

Has Malta benefited from being a member of the EU? (May 2010)

Source: Standard Eurobarometer 73

60%29%

11%

Benefited Not Benefited Don't know

60%

The changes experienced

- Both the government and the private sector conduct their business and take decisions with a greater focus on the longer term

- More emphasis is given to managing the realities before us, and on husbanding our resources, as opposed to the amateurish wishful thinking of the past

The changes experienced

- The massive investment in several sectors coupled with the reduction of bureaucracy and simplification of tax and other rules has led to the development of a vibrant and diversified economy

- Active participation at all levels has enabled us to both defend Malta’s interests and help shape the EU’s future direction on the basis of our national experiences and those of our partners

Malta’s size has not hindered us from attaining our goals

- Changes to budget legislation which worked against us as the most densely populated country in the EU

- The re-shaping of the EU's policy on illegal immigration so that solidarity in this area became part of EU policy. Hosting the European Asylum Support Office in Malta

- Ensuring that the Regulation on the Registration, Evaluation and Authorisation of Chemicals (REACH) had an SME focus

- Negotiating a sixth Maltese seat in the European Parliament

Malta’s Performance as an EU Member State

- Malta’s representatives are described as persons who know their business and put forward strong and persuasive arguments

- We are considered to be a country which - due to our preparedness - normally ‘punches well above its weight’

- This is not just something to be proud of but, given our size, is a necessity if we want to be truly effective

Malta’s Performance as an EU Member State

- The Commission’s bi-annual Internal Market Scoreboard confirmed Malta as leader for the seventh consecutive time in terms of the transposition of internal market Acquis

- Malta has one of the lowest number of open infringements in the Union; this being the case for the past four years

The lessons learnt

- While there is no such thing as ‘mission impossible’, consistency, patience and resolve are essential attributes;

- Master your brief and only spend time on what is truly important to your country

- At all times be constructive, work with others and actively look for solutions not just for your country but also for others

Quote……

“ …in Malta’s case, not only has membership of the European Union been beneficial on multiple levels, but it has permitted the Maltese Government to respond more effectively to national challenges while contributing to addressing European interests and concerns which are today interlinked with the concerns of Maltese citizens. EU membership is a tool and we would not be where we are today without the opportunities provided by this tool and the Maltese Government’s effective use of it.”

Diversification of the Economy

- Malta’s economy has diversified substantially with the emergence of new sectors which were impossible or even unimaginable before EU membership

- These sectors have created many new and better-paid jobs than those lost in the scaled-down sectors

- The use of EU Funds is another way in which Malta has benefited

- Malta benefited from some €1.3 billion EU funds (which equates to over €3,250 per capita) between 2004 and 2013

Economic Performance

- Since membership, Foreign Direct Investment has never gone below 7% of Malta’s GDP, and in June 2011 the stock of FDI in Malta was estimated to total €12.4 billion

- In 2011, Malta brought its deficit below the 3% level being one of just six Eurozone countries to do so

- In February 2012, Malta was among a minority of Member States not needing further in-depth review by the Commission of its macro-economic and fiscal status

Employment and Growth

- Employment growth rate of 2.7% in 2011, the third largest growth rate amongst the EU27

- Unemployment in Malta, stands at 6.5% of the labour force, the fifth lowest in the EU compared to 11.1% unemployment rate in the Eurozone

- Over 93% of Malta’s graduates find employment within three years of their graduation compared to the EU average of 76.5%

- The compounded annual average growth rate of GDP has been a remarkable 4.4% over the period 2003 to 2011

Economic output

source: Eurostat

EUR 6,755,851,000

Malta GDP (2012)

Economic output

source: Eurostat

Malta GDP per capita (2012)

EUR 16,100

Unemployment

Malta (2012) 6.5%

Euro Area (2012) 11.4%

European Union (2012) 10.5%

source: Eurostat

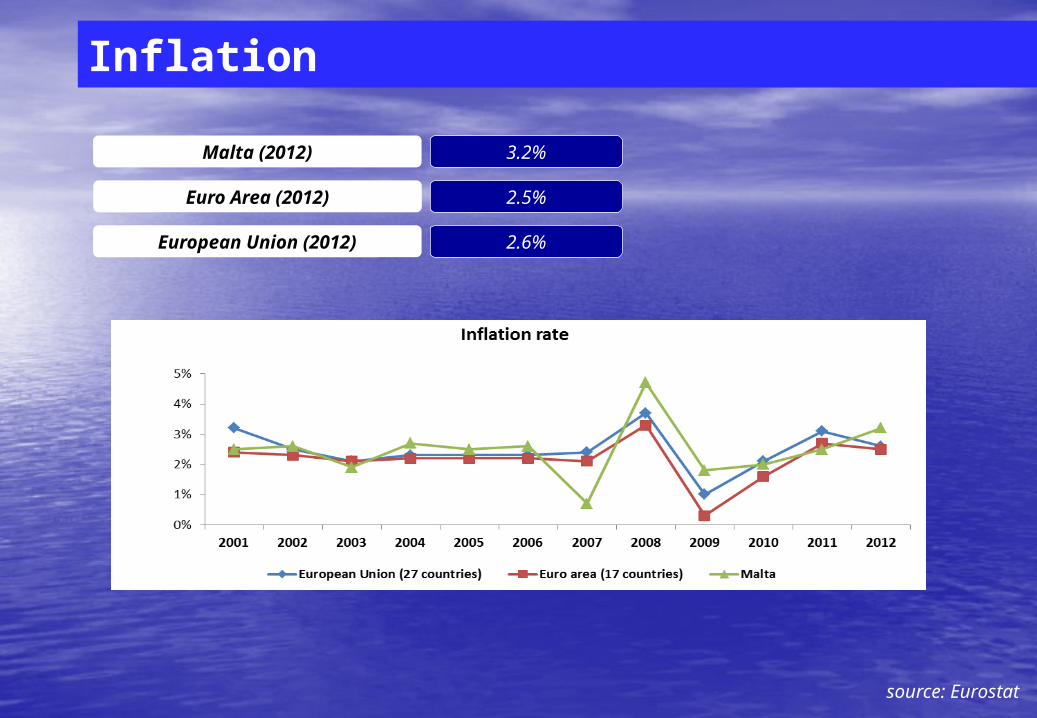

Inflation

Malta (2012) 3.2%

Euro Area (2012) 2.5%

European Union (2012) 2.6%

source: Eurostat

Government Deficit

Malta (2011) -2.7%

Euro Area (2011) -4.1%

European Union (2011) -4.4%

source: Eurostat

2012 data not yet available

Government Gross Debt

Malta (2011) 70.9%

Euro Area (2011) 87.3%

European Union (2011) 82.5%

source: Eurostat

2012 data not yet available

Table SIZE OF MALTESE BANKS

Core domestic banks Non-core domestic banks International banks

Total assets (EUR billions)

12,726.011 3,799.470 23,668.693

Total assets (as % of GDP)

195.8 58.5 364.2

Source: Malta Financial Services Authority

0

10

20

30

40

50

60

70

2006 2007 2008 2009 2010 2011 2012

per

cen

t Solvency ratios

Regulatory capital to risk weighted assets

Regulatory Tier 1 capital to risk weighted assets

MFSACreating a finance centre – the Supervisory Authority

24

MFSA’s Historical timeline

1988 MIBA offshore regime

1989 Set up of Malta Stock Exchange

1994 MFSC onshore regime: Regulation – Transparency - Taxation

1996 Grant of offshore licences stopped

2000 Malta OECD accord FATF co-operative jurisdiction

2002 MFSA set up as Single Regulator Set up of FIAU

2004 Offshore licences stopped/nominee companies phased out Agenda for Maltese Financial Services in Europe Financial Services Consultation Council EU Entry: Regulatory Standards & Single Market

MFSA’s Historical timeline

2007 MFSA Strategic Plan 2007-2009

2010 MFSA move towards Integrated Regulation

2011 MFSA Strategic Plan 2011-2014

2012 Setting up of Enforcement Unit

2013 Introducing Conduct of Business

Primary LegislationBanking ActFinancial Institutions Act Financial Markets ActInsurance Business ActInsurance Intermediaries ActInvestment Services ActRetirement Pensions ActTrusts and Trustees ActMFSA ActCentral Bank of Malta Act

Financial Services LegislationFinancial Services Legislation

27

Supporting Legislation:-

Companies (includes LPs) Act

Netting upon Insolvency Act

Securitisation ActPrevention of FinancialMarkets Abuse ActProfessional Secrecy ActPrevention of MoneyLaundering Act

Regulation

Malta Financial Services Authority (MFSA):-

• Single regulator for financial services• Regulates banking, financial institutions,

insurance companies, investment services companies, securities, recognised investment exchanges and admissibility to listing, trust management companies, pension schemes

• Listing Authority

28

MFSA’s approach to regulation

• Autonomous public institution, self-funded

• Avoidance of Prescriptive Regulation to allow promoters the flexibility to operate

• Risk-based supervision

• Regulation is proportionate to the size and nature of the business

• Direct contact with all license holders

• On-site and off-site supervision

Main Objectives of the MFSA

• to regulate, monitor and supervise financial services in Malta

• to promote the general interests and legitimate expectations of consumers of financial services, and to promote fair competition practices and consumer choice;

• to advise the Government generally on the formulation of policies in the field of financial services, and to make recommendations to Government as to any action which in the opinion of the Authority, it would be expedient to take in relation to matters in respect of which the Authority has such duties;

30

MFSA - Organogram

Board of GovernorsLegal & Int. Affairs Unit

Chairman

Board Secretary

Supervisory CouncilBoard of Management

and Resources

Director General Chief Operations Officer

Company Registry

Registrar of Companies

Enforcement Unit

DirectorCo-ordination Committee

Functions – Board of Governors

• Board of Governors - composed of 7 members including Chairman. Chairman and Governors appointed for a period of up to 5 years and their appointment may be renewed for further periods of 5 years;

• Board of Governors sets policy;

• Legal and International Affairs Unit - Secretary to the Board of Governors and the Co-Ordination Committee.

32

Co-Ordination Committee

33

Director GeneralSupervisory Council

Chief Operations OfficerBoard of Management & Resources

Director / Board SecretaryLegal & International Affairs Unit

Registrar of CompaniesCompany Registry

Chairman Board of

Governors

Act as contact point and principal channel of communication/co-ordination between Board of Governors, Supervisory Council and Board of Mgt & Resources. Co-ordinates the implementation of

policies approved by the Board of Governors.

Co-Ordination Committee

• Responsible for the Co-Ordination of the implementation of the policies of the Authority

• Act as contact point and principal channel of communication/co-ordination between Board of Governors, Supervisory Council and Board of Mgt & Resources

Composition of the Supervisory Council

SUPERVISORY COUNCILDirector General

DirectorBanking Supervi

sion

DirectorInsurance &

Pensions Supervision

DirectorSecurities &

Markets Supervision

Director Regulatory

Development

DirectorAuthorisat

ion

35

Remit of the Supervisory Council

• Art 10. (1) of the MFSA Act states:-

– The Supervisory Council shall be responsible for the approval of and for the issuing of licences and other authorisations, for the processing of applications for such licences and authorisations, and for the monitoring and supervision of persons and other entities licensed or authorised by the Authority in the financial services sector.

36

Tasks (I)

• Authorisation

Insurance Companies

Banks / Financial Institutions (payment services; financial

leasing; venture or risk capital; money broking; e-money issuers)

Collective investment schemes / Investment Services

Licences (asset managers, trustees, custody, stockbroking)

Regulated markets & Central Securities Depositaries

Retirement Schemes and Retirement Funds

Due Diligence exercise carried out prior to licensing

Tasks (II)

• Supervision Compliance with laws and regulations Compliance with licence conditions On-site and off-site supervision Admissibility of Financial Instruments

• Regulation Drafting of legislation, legal notices and regulations Rules and Guidance Notes Issue of Circulars

Board of Management & Resources

MFSA Act Art 11 states

“.....responsible for carrying out the day-to-day management and finances of the Authority, including business development and ancillary services and for the general co-ordination of the Authority’s administrative affairs and shall be composed of the persons responsible for such activities as may be designated by the Board of Governors”

39

Board of Management & ResourcesChief Operations Officer

Information Systems

Administration Finance & Risk Management

Communications & Events

Human Resources & Training

Board of Management & Resources

• Responsible for carrying out the day-to-day management and finances of the Authority, including business development and ancillary services and for the general co-ordination of the Authority’s administrative affairs

• Presided by the Chief Operations Officer as Chairman and Heads of Unit responsible for Communications and Events, Administration, Human Resources and Training, Finance and Risk Management, Information Systems

Remit - Board of Management & Resources

Admin-istration• Upkeep of premises – including cleaning and maintenance• Organisation of transport, • Security

HRD & Training• Internal personnel training• Industry training programmes• HR functions – recruitment, personnel records, staff appraisals• Support Education Council

Information Systems• Systems development, outsource system applications, data security & integrity• Implement new systems & infrastructure, security, support, maintenance• System back-up and business continuity• IT Security

Communic -ations

• Information – website, enquiries, intranet• Public Relations – media, press releases • Events – conferences, seminars, training logistics, conference facilities

Finance & Risk• Finance – Accounting records, internal control, budgets, fees• Procurement• Operational risk management 41

MFSACreating a finance centre – Recognised Investment Exchanges

42

Malta Stock Exchange

European Wholesale Securities Market

43

Recognised Investment Markets

A new regulated market for wholesale fixed income securities, registered and domiciled in Malta in 2012 [Majority Shareholder – Irish Stock Exchange (ISE) Minority shareholder – Malta Stock Exchange (MSE)]

The EWSM is approved as an EU regulated market under MiFID. Dedicated to arrangers and issuers of wholesale [€100,000 denomination] securities under the Prospectus Directive

44

European Wholesale Securities Market - EWSM

Why Malta and Ireland?

• Long standing relationship between ISE and MSE. Combines strengths of two reputable exchanges into one truly European market designed to meet international debt issuer requirements

• Malta is an emerging financial services location with a commitment to develop capital markets

• EU regulatory framework, both jurisdictions form part of the Eurozone

45

EWSM Overview

EWSM

MFSACompetent Authority

Market Supervisor

ISEMarketing,

Infrastructure & Corporate Services

MSE Market Operator Listing Agent

& Annotation Services

46

Infrastructure

• Market Operator & Compliance - MSE• Administration, finance and company

secretarial -ISE• IT market services (announcements, listing

and website management) - ISE• Marketing and promotion - ISE• Corporate knowledge of ISE will be at EWSM’s

disposal

47

Listing Process - Overview

48

Process – Efficiency and Expertise• The EWSM has established Guidelines for Listing and

Trading on the EWSM [www.ewsm.eu]. All regulatory requirements of the MFSA and EWSM are presented in one user friendly document.

• The MFSA approves prospectuses for securities to be admitted to the EWSM under the Prospectus Directive. As Listing Authority, under the Consolidated Admissions and Reporting Directive [CARD], the MFSA approves the admissibility of securities to listing as well as the ongoing requirements of issuers under the Transparency Directive.

• The MFSA adopts a pragmatic market oriented proactive approach to prospectus review and approval including guaranteed review times of 3 business days for initial submission and 2 business days for subsequent drafts of prospectuses.

49

Listing Agent

The appointment of a Listing Agent is a keyelement of the admission process as the

ListingAgent ensures smooth and timely

interactionbetween issuers and arrangers and the

MFSAand EWSM on regulatory requirements.

The Listing Agent reviews the prospectus and

other documentation for compliance with the

EWSM Guidelines prior to submission

50

Listing Agent

A Listing Agent approved by the Listing Authority shall be a body corporate, partnership or firm incorporated or established in the EEA (i.e. either in an EU Member State or an EEA State) and be independent of any Issuer, or related service provider, to which it provides listing agent services.

• have extensive experience in reviewing and preparing listing applications and Prospectuses for debt Issuers and in advising Issuers on the application of the Listing Rules and have adequate resources to fulfil the role expected of a Listing Agent under the Listing Rules;

• Currently only one Listing Agent – ISE Listing Services [ISELS] has been approved by the MFSA [www.isels.ie]

51

Niche Markets

• Insurance Securitisation – Legislation for Incorporated Cell Companies is in place. Each incorporated cell can be an iSPV. Rules are currently being drafted.

• Debt linked to life settlement policies – policies have already been developed by MFSA in this area.

• Environmentally driven finance – debt linked to infrastructure for wind and solar energy. Waste to energy finance etc.

• Intellectual Property based structures• Finance for Transportation Projects – Aircraft Finance

[Malta has developed legislation for Aircraft Registration, Maintenance etc] Shipping Finance [Malta has the third largest shipping register with arounr 7,000 registered shipping companies].

• Project bonds – reflecting the move from loan financing of projects to financing of projects through the capital markets.

• Traditional forms of finance 52

Securitisation Act, 2006

• The aim of the Act is to provide a legal framework for domestic

and cross-border securitisations to take place in and from Malta. . It provides a comprehensive framework for the conversion of receivables or other assets into securities that can be placed and traded in capital markets

• Article 2 of the Act defines Securitisation as a transaction or an arrangement whereby a securitisation vehicle, directly or indirectly:

1. Sale transactions: whereby the originator transfers a pool of assets to the securitisation vehicle;

2. Synthetic transactions: whereby the securitisation vehicle assumes the credit risk of the originator through credit derivatives;

3. Loan transactions: whereby the securitisation vehicle grants secured loans or other secured facilities to the originator. 53

• Establishment of a Joint Financial Stability Board with the Central Bank of Malta

• Introduction of Registration for Corporate Service Providers

• Banking Union

Supervisory Developments

1.Establishment of a Conduct of Business Board

Proposed Composition – Director General; Director Consumer Complaints; Director Enforcement; Director of the Relevant Supervisory Unit

or

2. Establishment of Conduct of Business Unit

Supervisory Developments – Conduct of Business [options]

Enforcement Unit

• Set up in 2012• Responsible for the enforcement aspects

previously carried out by the respective supervisory units’ Reviewing actions and conducting investigations of licence

holders suspected of having committed compliance failures,

serious misconduct, market abuse, breach of listing rules or

any other serious breaches of the law

Investigating persons carrying on financial services activities

without having the necessary licence or authorisation

Financial crime issues

Consumer Affairs Unit

Consumer Education

Consumer Complaints

Support for the Depositor Compensation Scheme, Investor Compensation Scheme and the Protection and

Compensation Fund59

Consumer Affairs Unit

Receives and assesses wide range of issues arising from consumer complaints and queries

Handles all forms of consumer complaints with feedback/interaction from regulatory and admin units

• Member of FIN-NET, the EU’s network for out-of-court financial redress. Contacts with the network beneficial, especially when sharing best practices in resolving common issues arising from complaints

60

Consumer Affairs Unit

61

New web-based Case Management System (CMS) installed 1 Jan 2012.

The CMS, developed by MFSA ICT Unit, meets reporting requirements of the European Commission Recommendation C(2010)3201 on harmonised methodology of consumer complaints reporting (issued 12 May 2010). The legacy CMS software is still in use in regard to those cases received until end 2011.

New system enables Unit to provide better reporting, especially in regard to phone calls received by the Unit.

Fully integrated with online complaints system available on mymoneybox portal .

Weekly participation in TV and radio programmes.

Financial services consumer education portal:

Each month new topics being added/updated. Pages are also being translated into Maltese.

Monthly e-newsletter “My Money Box” + Facebook presence

New insurance comparative tables

Consumer Complaints UnitConsumer Education

62

Membership of International Organisations

• New EU Supervisory Architecture:-

• European Securities & Markets Authority (ESMA)

• European Banking Authority (EBA)

• European Insurance and Occupational Pensions Authority (EIOPA)

• Inter. Association of Insurance Supervisors (IAIS)

• Inter. Organization of Securities Commissions (IOSCO)

• Inter. Organisation of Pensions Supervisors (IOPS)

63

Memoranda of Understanding currently in force

• 27 MoU’s in 23 countries & 2 Letter Agreements• Covering Banking, Insurance, Securities, Trusts, Pension

funds, exchange of information, etc• New MOU with Qatar Financial Centre & Regulatory

Authority, State of Nebraska, National Bank of Slovakia

Bilateral MoU’s and Agreements with

Foreign Regulators

• Office of Fair Competition – exchange of information & assistance

• CBM – exchange of information and payment and securities settlement systems, Joint Financial Stability

Board

Bilateral MoU’s – Local Authorities

• MOF/CBM – co-operation in financial crisis• NSAs/EU Central Banks & EU Finance Ministers on financial

stability• EIOPA – Insurance and Occupational Pensions

• ESM & IOSCO – Securities• IAIS - Insurance

Multilateral MoU’s & Protocols

64

Strategic Plan 2007-2009

MFSA Mission Statement

• Opportune to remind staff on the MFSA Mission Statement:-

“Ensure high standards of conduct and management in

financial services and promote the legitimate

expectations of consumers.”66

MFSA’s Strategic Plan

Enable innovation through Legislative and Regulatory Development

Review of existing Legislation and Regulation

Continuous training at staff and Industry level

Develop strategic partnerships with other regulatory Authorities

Maintain Malta’s reputation as a leading financial services jurisdiction

2002/3: IMF/World Bank Review-FSAP

2005: Internal Audit

2007: Internal Audit

2010: Independent Assessment

2011: Governance of Supervision

2012: Internal Audit - Risk Management

Ongoing Art IV consultation with the IMF

Currently a review of the financial swector under

the EU Alert Mechanism is taking place

68

Assessment of the MFSA

Number of Employees

69

2007 2008 2009 2010 2011 20120

50

100

150

200

250

126135

146161

178

200

3 3 5 7 6 9

Full Time Part Time

Staff

Economists, Mathematicians, Accountants & Statisticians

23%

Lawyers 12%

Banking & Finance 16%

Other Professions 25%

Staff having diploma 14%

Clerical and others 10%

Total MFSA employees Approx. 210

Malta and the EUCreating a finance centre -Results

71

Licenses Issued – CISs

72

2008 2009 2010 2011 2012

PIFs 112 102 102 163 117

UCITS 4 3 5 14 9

Non-UCITS

3 0 0 2 2

Private 0 0 1 0 0

Total 119 105 108 179 128

2008 2009 2010 2011 20120

20

40

60

80

100

120

140

160

180

200

112102 102

163

117

43 5

14

93

2

2

PIFs UCITS Non-UCITS Private

New

funds (

incl. s

ub-f

unds)

Investment Services Licences

73

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Investment Services 75 88 102 109 113

Recognised Fund Administrators 12 13 18 24 26

Total 87 101 120 133 139

Dec-08 Dec-09 Dec-10 Dec-11 Dec-120

20

40

60

80

100

120

140

7588

102 109 113

12

13

18

2426

Investment Services Recognised Fund Administrators

Lic

ences

Licensed Insurance Companies

74

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Non Life 26 30 33 37 42

Life 8 8 8 8 7

Composite 3 3 2 2 2

Reinsurance 4 4 7 7 7

Total 41 45 50 54 58

of which

Domestic origin Insurers 8 8 8 8 8

Affiliated Insurers 6 8 10 10 11

PCCs3

(10 cells)

3 (12

cells)

4 (13

cells)

8 (15

cells)

8 (18

cells)

Foreign Insurers

2 2 2 1 1

Dec-08 Dec-09 Dec-10 Dec-11 Dec-120

10

20

30

40

50

60

2630

3337

42

8

88

8

7

3

32

2

2

4

4

7

7

7

Non Life Life Composite Reinsurance

Insura

nce U

ndert

akin

gs

Insurance Intermediary Licences

75

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Registered Insurance Brokers

67 69 66 71 78

Enrolled Insurance Brokers28 28 28 30 29

Registered Insurance Agents

30 28 27 28 28

Enrolled Insurance Agents21 19 18 19 20

Registered Insurance Mgrs.20 23 22 26 26

Enrolled Insurance Managers

12 13 13 15 15

Tied Insurance Intermediaries

529 500 507 513 506

Credit and Financial Institutions

76

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Credit Institutions 22 23 25 25 27

Financial Institutions 15 15 13 15 23

of which:

Payment Institutions 6 6 7 9 15Electronic Money

Institutions0 0 0 1 4

Dec-08 Dec-09 Dec-10 Dec-11 Dec-120

5

10

15

20

25

30

22 2325 25

27

15 1513

15

23

Credit Institutions Financial Institutions

Lic

ences

Trust and Trustees Authorisations

77

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Nominees 29 24 23 22 20

Trusts Registered - Trust Act, 1988

132 117 117 115 115

Authorised Trustees - Trusts and Trustees Act

98 108 117 123 131

Dec-08 Dec-09 Dec-10 Dec-11 Dec-120

20

40

60

80

100

120

140

98108

117 123131

Authorised Trustees - Trusts and Trustees Act

Retirement Schemes

78

Retirement Schemes

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Asset Managers - - 3 3 3

Retirement Scheme Administrators - - 5 7 9

Retirement Schemes - - 6 13 17

Dec-10 Dec-11 Dec-120

2

4

6

8

10

12

14

16

18

3 3 35

79

6

13

17

Asset Managers Retirement Scheme Administrators Retirement Schemes

Registered Companies

79

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

New registrations 2,818

2,678

3,130

3,458 4,016

Companies on the register

45,975

48,520

51,650

55,150 59,098

Dec-08 Dec-09 Dec-10 Dec-11 Dec-120

1,000

2,000

3,000

4,000

2,818 2,678 3,130 3,4584,016

New Registrations

Dec-08 Dec-09 Dec-10 Dec-11 Dec-120

10,000

20,000

30,000

40,000

50,000

60,000

70,000

45,975 48,520 51,65055,150 59,098

Companies on the reg...

ECB Press Release on Growth of MFIs in 2012

Finland -8.2France -9.2Greece -5.1Hungary 0Ireland -2.9Italy -7.0Latvia 0Lithuania 1.1Luxembourg -22.4

AustriaBelgiumBulgariaCyprusCzech RepGermanyDenmarkEstoniaSpain

-2.8-4.1 0-2.8-9.0-2.0 0-5.4-8.2

MaltaNetherlandsPolandPortugalRumaniaSwedenSloveniaSlovakiaUnited Kingdom

3-1.0-1.00.6-3.6-11.2-3.4-29.50

80

Malta Bucks the Trend – Investment Adviser

Taxation

Malta follows an imputation system of taxation established in 1948. The system was agreed with the EU under State Aid and Code of Conduct for Business Taxation in 2007.

Under the system all companies pay tax at 35% of which 6/7 is imputed to shareholders on declaration of a dividend. Shareholders of holding companies get 7/7 refund and shareholders of companies receiving royalty income get 5/7 refund. In a number of countries, the refund in retaxed separately from the investment income under CFC legislation.

Anti-abuse and exchange of information mechanisms in place

OECD/G20 classifications of tax havens place Malta on the “white list”

82

Securitisation Vehicles: Tax Neutral

• A securitisation vehicle enjoys tax neutral status thereby optimising the investors’ return and the originator’s cost of funding. Although, as a rule, securitisation vehicles are liable to tax in Malta at 35%, substantial deductions are available which effectively eliminate any taxable income in Malta. Specifically enacted tax rules clarify that the following deductions may always be availed of by a securitisation vehicle:

1. Cost of acquisition: Expenses payable to the originator for the acquisition of securitisation assets or the assumption of risk;

2. Finance expenses: Premiums, interest or discounts relating to financial instruments issued, or funds borrowed, to finance the acquisition of securitisation assets or the assumption of risks;

3. Operating expenses: Costs incurred in the day-to-day administration of the securitisation vehicle and the management of the securitisation assets, including the collection of any relevant claims.

83

EWSM Listings - Taxation

The EWSM was on 18th January 2013 granted“Recognised Stock Exchange” within the

meaning of the UK Income Tax Act, 2007.

As such , the Quoted Eurobond Exemption applies for investors.

Non-resident investors do not suffer any tax in Malta.

84

Malta Double Tax Treaties

EU CountriesOther

European

Countries

Rest of the World

AustriaBelgiumBulgariaCyprusCzech Rep.DenmarkEstoniaFinlandFranceGermanyGreeceHungaryIrelandItaly

LatviaLithuaniaLuxembourgNetherlandsPolandPortugalRomaniaSlovakiaSloveniaSpainSwedenUnited Kingdom

AlbaniaCroatiaGeorgiaIcelandIsle of ManJerseyMontenegroNorwaySan MarinoSerbiaSwitzerland

AustraliaBahrainBarbadosCanadaChinaEgyptHong KongIndiaJordanKorea (Rep.)KuwaitLebanonLibyaMalaysiaMorocco

PakistanQatarSaudi ArabiaSingaporeSouth AfricaSyriaTunisiaUnited Arab EmiratesUnited StatesUruguay

85

Malta Double Tax Treaties

Belgium (Protocol)GuernseyIsraelLuxembourg (Protocol)MexicoNorway (new treaty)Russia (being renegotiated)Singapore (Protocol)South Africa (Protocol) Turkey

ArmeniaAzerbaijanBosnia and HerzegovinaIndia (new treaty)MoldovaOmanRussia (new treaty)ThailandUkraine

Double tax agreements: signed but not yet in force; initialled/being negotiated

Signed but not yetIn force

Awaiting Signature or Under Negotiation

86

Malta and the EUCreating a finance centre –Ancillary Services

87

Proposition

• Malta as an emerging financial services location has proved to be successful in the various financial services sectors with responsive communication from the Regulator

• The World Economic Forum Competitiveness Report [2012-2013] places Malta:

1. 15th for Financial Market Development [LU 12th; IE 108th] 2. 12th for the Regulation of Stock Exchanges [LU 4th; IE

76th]3. 13th for the Soundness of the Banks [LU 18th; IE 144th] out of a total of 144 countries.

88

Critical Success Factors

• Well educated/competitive cost pool of labour• Inexpensive and modern office developments

with capacity• Good telecommunications & IT infrastructure• Very competitive tax regime• Flexible legal and regulatory environment• Well trained Professionals• Multilingual community • Comprehensive Double Tax Treaty network

89

Legal Services

• Malta is a civil law jurisdiction – company law is based on English law principles. Interpretation of English text prevails

• Legal framework is therefore flexible, versatile and able to relate to different legal systems.

• Legal community is well established with many practitioners obtaining further training overseas and most firms form part of international legal networks.

90

Accounting Services

• IFRS – International Accounting Standards applicable since 1997

• Major international accountancy firms BDO, Deloitte & Touche, Ernst & Young, Grant Thornton, KPMG, PKF, PricewaterhouseCoopers, Mazars, Ecovis and others operate in Malta

• The World Economic Forum Competitiveness Report [2012-2013] places Malta:16th in Strength of Reporting and Auditing Standards [Luxembourg 15th and Ireland 66th ] out of 144 countries

91

Conclusion

• Business environment: product-driven jurisdiction, established banking, insurance and funds industry, sharp growth in financial intermediation services, easy access to decision makers, ability to adapt fast to changing circumstances.

• Cost structures: cost of human resource, expertise, quality; productivity levels, taxation

• Strategic factors: language, geography, culture, international perception

• Infrastructure: communications and IT, regulation, training structures, tax treaties

92

Our Thinking

We must not think that we are living in some kind of glass structure

94

“

Under the Spotlight

We are being watched:

………there is too much talking going on outside the MFSA......

95

.Thank you!

96