making 3g work in vietnam presented by: marc daniel einstein senior industry analyst october 5th,...

TRANSCRIPT

Making 3G Work in Vietnam

Presented by:Marc Daniel EinsteinSenior Industry Analyst

October 5th, 2008Hanoi, Vietnam

2

Today’s Agenda

• Section 1: Vietnamese Mobile Market Overview

• Section 2: 3G Market Overview

• Section 3: 3G Services & Applications

• Section 4: Making 3G Work in Vietnam

3

Section 1: Vietnamese Mobile Market Overview

4

Vietnam’s Telecommunications Market in Context

Vietnam’s Mobile Market is at a medium level of maturity for an emerging market.

“The Digital Divide”

Australia

Bangladesh

China

Hong Kong

India

Indonesia

Japan

Malaysia

New Zealand

PakistanPhilippines

Singapore

South Korea

Sri Lanka

Taiwan

Thailand

Vietnam

0%

20%

40%

60%

80%

100%

120%

140%

0% 20% 40% 60% 80% 100%

Household Broadband Penetration Rate (%)

Mo

bile

Pe

ne

tra

tio

n R

ate

(%

)

5

Vietnam Mobile Market Forecast

Vietnam will continue to be one of the fastest growing mobile markets in terms of netsubscriber additions. Vietnam will have 4% of all AP subs by 2013.

0

10

20

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

To

tal

Mo

bil

e S

ub

scri

ber

s (0

00s)

0%

20%

40%

60%

80%

100%

120%

Mo

bil

e P

enet

rati

on

Rat

e (%

)

6

Vietnam Mobile ARPU Evolution

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

$20.00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

AR

PU

(U

S$

)

Voice ARPU (US$) Data ARPU (US$)

As most of Vietnam’s future mobile market growth will come from the rural and youthSegments, we believe that the blended market ARPU will breach the US$3 level by 2013

We predict that the 2013 ARPU will only be 25% of its 2005 value

7

Asia Pacific ARPU vs. EBITDA Margin Comparison

NTT DoCoMo

KDDI

SKT

KTF

SingTel

Optus

Telstra

CHT

SmarTone

M1 Starhub

Taiwan Mobile

Three

SoftBank MobileLG Telecom

China Mobile

China UnicomDTAC

SMARTGlobe Telecom

Bharti Celcom

DigiGrameen Phone

Telkomsel

XL

RelianceAISDialog

TMIB

True Move

Mobilink

0%

10%

20%

30%

40%

50%

60%

70%

$0 $10 $20 $30 $40 $50 $60 $70

ARPU (US$)

EB

ITD

A M

arg

in (

%)

This decline, however, does not necessarily correspond to low profitability, especially foremerging market incumbent operators

Emerging Market Incumbents

Emerging Market Challengers

Developed Market Operators

8

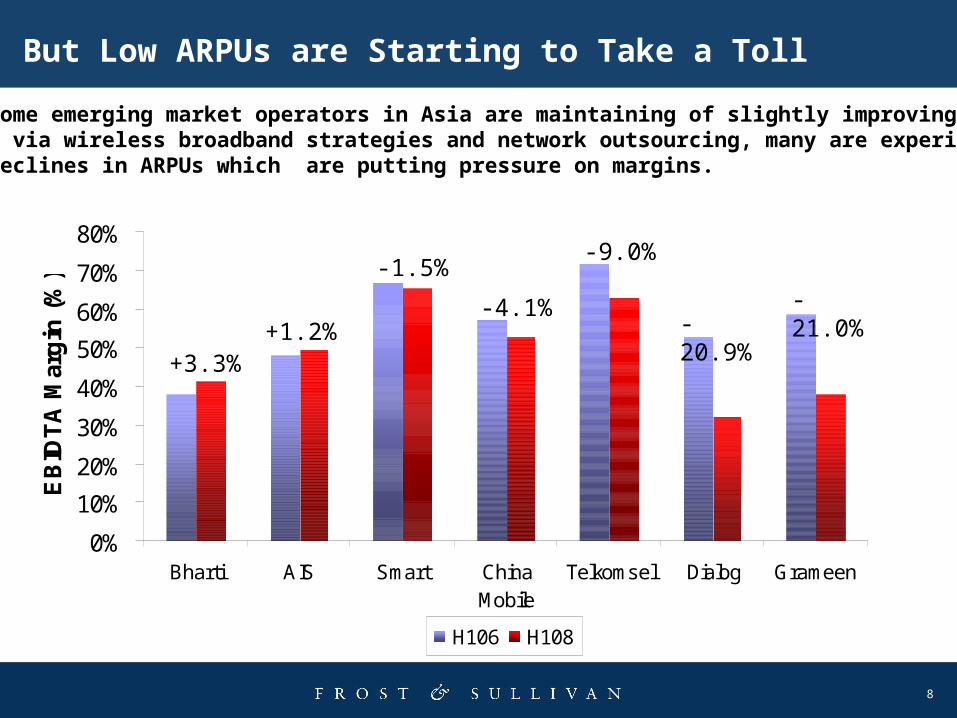

But Low ARPUs are Starting to Take a Toll

While some emerging market operators in Asia are maintaining of slightly improving EBITDAmargins via wireless broadband strategies and network outsourcing, many are experiencinglarge declines in ARPUs which are putting pressure on margins.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Bharti AIS Smart ChinaMobile

Telkomsel Dialog Grameen

EB

IDT

A M

arg

in (

%)

H106 H108

+3.3%+1.2%

-1.5%

-4.1%

-9.0%

-20.9%-21.0%

9

Section 2: 3G Overview

10

KEY CHALLENGES:

High Handset Prices Lack of Subscriber Adoption Large Markets Still Untapped QoS/Indoor Coverage

3G Deployments3G Deployments –Asia Pacific

11

3G Subscriber Update

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2004 2005 2006 2007e

Japan South Korea HK, Aus, Taiwan, Spore Others

Japan & South Korea comprised 80% of the APAC 3G Subscriber Base in 2007

‘000 subscribers

12

3.5G vs. 4G Technology Comparison

LTEHSPA+

LTE will offer significant advantages over 3.5G in terms of data rates, latency, transmission time interval, and is more flexible with spectrum blocks.

Latency

Data Rates

TTI

Spectrum

144/57Mbps DL/UL42/11Mbps DL/UL

10ms50ms

2ms .05ms

5MHz Blocks Flexible

13

LTE Time to Market

LTE is still in the laboratory and early field testing phases as vendors such have publicly demonstrated live LTE handovers. Going forward we expect limited deployments in 2011 with wider-scale launches by 2012.

2008 2009 2010 2011 2012

Lab Testing

Field Testing

Network Deployment

First-Mover Launches

Wide-Scale Deployment

14

Section 3: Making 3G Work in Vietnam

15

APAC Household Penetrations Rates

0%10%

20%30%40%50%

60%70%80%

90%100%

Ba

ng

lad

esh

Pa

kist

an

Ind

on

esi

a

Sri

La

nka

Ind

ia

Vie

tna

m

Ph

ilip

pin

es

Th

aila

nd

Ch

ina

Ma

lays

ia

NZ

Jap

an

Au

stra

lia

Sin

ga

po

re

Ta

iwa

n

Ho

ng

Ko

ng

Ko

rea

Ho

us

eh

old

Bro

ad

ba

nd

Pe

ne

tra

tio

n (

%)

The “Digital Divide”

Low-bandwidth, high ARPU wireline broadband markets are ripe for competition from 4G, even in developed markets.

16

PLDT – Wireless Broadband Strategy

Exhibit: PLDT’s Broadband Service Portfolio

Exhibit: PLDT’s Broadband Subscriber Uptake by Service, 2005-2007

89 113

264122

302

24

13

10

6

0

100

200

300

400

500

600

700

2005 2006 2007

To

tal

Su

bsc

rib

ers

(000

s)

Fixed SmartBro WeRoam

The PLDT has been able to diversify its revenue streams in the broadband market by deploying wireless solutions for last-mile connectivity:

• GPRS/EDGE, HSPA, WiFi and eventually WiMax are all used to compensate for low fixed-line penetration (~4%)

• In 2007 wireless broadband subscribers overtook wired subscribers (only case in the world)

• Product bundling: New subscribers can purchase a laptop with a wireless data card and service plan from the operator

17

Clearwire – Wireline to Wireless Churn

Clearwire, one of the largest WiMAX operators in the world and based in the USA reported that a surprising 59% of its wireless broadband subscriber base actually churned from a fixed-line broadband service, driven by both lower price points and the added feature of mobility.

Cable Modem33%

DSL26%

Other2%

No Internet12%

Dial Up27%

18

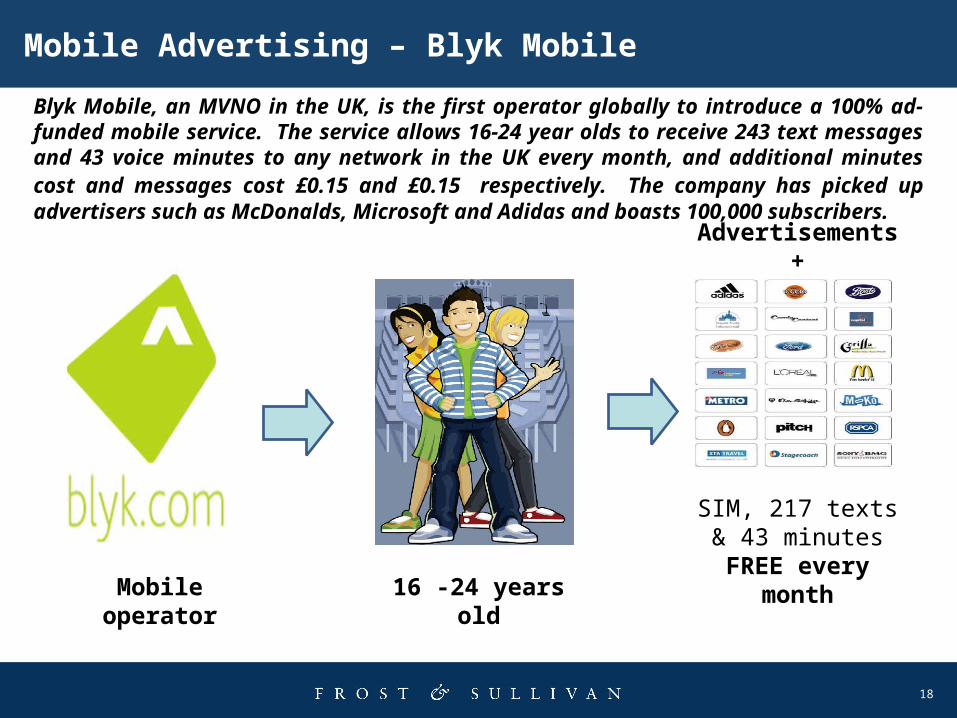

Mobile Advertising – Blyk Mobile

Blyk Mobile, an MVNO in the UK, is the first operator globally to introduce a 100% ad-funded mobile service. The service allows 16-24 year olds to receive 243 text messages and 43 voice minutes to any network in the UK every month, and additional minutes cost and messages cost £0.15 and £0.15 respectively. The company has picked up advertisers such as McDonalds, Microsoft and Adidas and boasts 100,000 subscribers.

SIM, 217 texts & 43 minutes

FREE every month

Advertisements +

16 -24 years oldMobile operator

19

Section 4: Making 3G Work in Vietnam

20

What does 3G Mean for Vietnam?

• Vietnam’s mobile market has rapidly caught up with other emerging markets in Asia but the broadband market still lags behind.

• Emerging market wireless operators are facing pressure on margins which will entice them to aggressively enter the broadband market.

• 3G technology has reached a point where it can adequately compete with wireline service in Vietnam.

• Service offerings should first focus on ACCESS then VAS.

• A higher broadband penetration is crucial to Vietnam’s competitiveness in the global economy and so it is ultimately in the government’s best interest to promote wireless broadband usage.