make money do good - ethex · self-directed positive investor – people who ... ‘con panis’ -...

TRANSCRIPT

make money do good

The Ethex Positive InvestmentReport 2014

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

2

Contents

ForewardEd Mayo

Section 1The UK Positive Investment Marketplace

Section 3The Positive Investors

Section 5Conclusions

Section 6Research Methodology

Section 4The Role of Ethex

Section 2The Hotspots

Executive Summary

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

We are seeing the emergence of the self-directed positive investor – people who are more connected to their money, feel in control of it, want to know where it goes, and

recognise that they can make a positive social impact with it.

A movement is emerging, refreshing a spirit of co-operative action that is people-centred and from the ground up. This is a movement that should be supported and encouraged, reflecting it within wider tax policy and with intelligent and proportionate regulation, that recognises the social value and consumer empowerment that positive investing can bring.

The good news is that positive investment is emerging as a proven option for individuals and communities right across the UK. With the right infrastructural support this market has a very exciting future.

3

Foreword

The traditional approach to ethical investing, by screening companies on the stock market, has its place, but at a time when the public are more sceptical than ever that even the best of class fossil fuel companies are going to take on responsibilities around climate change or banks their responsibilities to society, it can also represent a form of ‘ethics lite’.

Instead, we have the rise of a closer connection to money. Investors are moving away from remote, negative screening to positive social impact and local community – they want to see real change.

We now have a report on the number of people that are investing in enterprises that they believe in. It is new and something to celebrate. It is something that fits beautifully with social trends and emerging technology platforms, but in many ways it is also the ‘new old’.

The idea of sharing has always been implicit in economic action, from the early guilds, to the very term ‘company’ whose origin is in the sharing of bread - ‘con panis’ - at table between master and apprentice. It is only in more recent times that business and the markets they operate in are sold as activities

where the winner takes all – and where, if you operate with a positive ethical mission, then you have to distinguish yourself.

The power of positive investing is that it uses the best of modern technology and regulation to offer a way back to a more co-operative, human scale of finance. It is the younger sister of the wider ethical investment movement, but without the periodic dumbing down (‘ethics lite’) and paternalism that has characterised that sector.

The report highlights, for example, the growth of community shares, using co-operative models, that mean that people who put money up are not just investors, but members, with equal rights in the enterprise. We have seen over 40 share offers of this kind in 2014, including PEC Renewables, a member of Co-operatives UK that has worked with Ethex and benefited from the new wave of positive investing.

Ed Mayo Secretary General of Co-operatives United Kingdom

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

Positive investing is self-directed saving and investing by individuals who are taking control of their own finances and choosing to save and invest not only for a financial return but also

to make money do good. It involves saving with or investing directly in positive businesses - charities, co-operative and community organisations and a number of companies and funds set up with the explicit intention of addressing a social or environmental need alongside delivering a financial return.

4

ExecutiveSummary

Our 2014 Positive Investing Report Make Money Do Good highlights the latest trends in this rapidly growing marketplace and its increasing influence on the finance sector. It reveals which geographical areas are now the main hotspots for positive investing in the United Kingdom. It investigates where the UK’s positive investors live, what they invest

in and why, and what can be done to build the positive investing marketplace.

Growth of the marketThe positive investing market has grown significantly since we published our 2013 report and since the launch of Ethex only 18 months ago.

On a like for like basis, the size of the market is up 33% from nearly £1.6 billion to £2.1 billion. However new data that reveals £1.14 billion of savings with Northern Ireland credit unions, available for the first time this year, takes the total market size to £3.25 billion.

In contrast, the green and ethical retail funds market, which has been the mainstay of ethical investing since the early 90s and grew rapidly until 2009, has seen growth slow to under 4% a year over the last 3 years.

Whilst savings in ethical banks and credit unions (excluding Northern Ireland) rose by 29% to £1.86 billion, the fastest growth was to be found in the smaller direct investment sector, which consists of community share issues, bonds issued by charities and bonds and equity in a small number of public companies set up with the intention of delivering social and environmental benefits.

This sector is up from £140 million to £249 million, a staggering 78% increase with large numbers of new people entering the market.

Within the direct investment sector, the most dramatic growth was in communities issuing shares for local projects, up 98% in total value on last year. The phenomenon of charities issuing bonds to the public, almost unknown before 2012, also saw high levels of activity, with one charity even issuing bonds on the London Stock Exchange.

“The size of the market is up 33% and now totals £3.25 billion”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

Executive Summary

5

The HotspotsLast year’s report identified 15 hotspots of positive investing around the UK.

Oxford is the winning hotspot this year, having seen the most active engagement from positive investors, followed by Bristol, Bath, Brighton and South/Central Devon.

This year we found that two in every five UK businesses that has sought to raise funds in the last two years is based within 20 miles of one of these hotspots. This confirms that these hotspots are still the communities leading the trend towards local investment in positive social and environmental change.

A growing movement Ethex’s view is that wider participation in financial markets is now unstoppable. Positive investing is emerging as a broad popular movement and should no longer be considered as a number of isolated investors acting alone. Younger people are investing more, average investment amounts are rising, and individual investors are tending to build a diversified portfolio of investments rather than just taking one single holding.

The investors engaged with Ethex now see positive investing as a core part of their overall investment activity. They welcome

the transparency and connectedness that this form of investment offers. They are coming together to share ideas on how to further their positive investing aspirations a nd to find ways to create a closer connection with their savings and investments.

Barriers to growthYes despite this growth many challenges remain. Ethex has identified three main areas where work still needs to be done.

• Firstly, individuals should be provided with educational tools on how to assess the risks and rewards of investment, so that they can make better investment decisions on their own account. This will ensure that the participation in financial decision making that people are demanding is channelled creatively and effectively and the risk of them making a bad decision is reduced.

• Secondly, greater investment is needed in the financial infrastructure supporting an investment once it has been made. As positive investors become more active and informed, they expect a higher quality of service. Making direct investments is becoming easier, but the aftercare is still weak, particularly when it comes to an investor wanting to sell or value their holding on a secondary market. This lack of infrastructure persists

despite significant resources being injected into the market by charitable foundations and government.

• Thirdly, the Financial Conduct Authority needs to ensure that regulations do not excessively limit access to the market for the less experienced investor. Otherwise we run the risk that finance remains the domain of professionals paid to navigate their way through the regulations. However, in reaction to a rapid proliferation of crowd-funding websites, the FCA has tightened regulation further, making it harder for the investor to understand and engage with the investment journey. Ethex believes that in the long term an emphasis on educating and supporting the investor stands a greater chance of success than limiting access to the market.

The next stepsEthex’s investors are calling for guidance on how they can become more positively invested. In response to this, Ethex is devising positive investing personal action plans for release in 2015 that will enable investors to calculate how positively invested they are, together with recommendations on how to improve. This method can be used by anyone regardless of their actual level of wealth and will serve as a powerful tool for self-education on investment.

“Individuals should be provided with educational tools on how to assess the risks and rewards of investment”

Section One

The UK Positive Investment Marketplace

Barbara Hammond invests in Oxford’s Osney Lock Hydro scheme

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

7

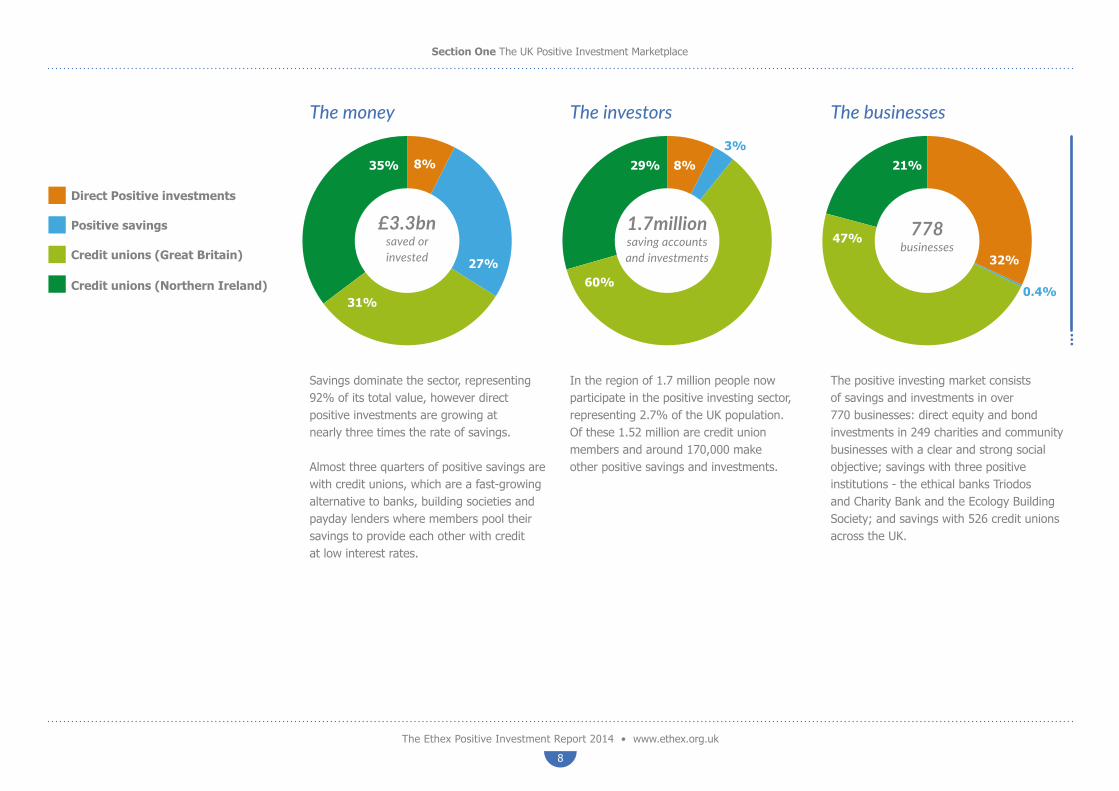

The positive saving and investing market is now worth £3.3 billion, and reaches around 1.7 million people.

The UK positive investing marketplace

Since our 2013 report, a further £417 million has been saved and £109 million invested positively, adding £0.5 billion to the market and taking the total size from £1.6 billion to £2.1 billion, an increase of 33%.

Furthermore, data on £1.14 billion saved with credit unions in Northern Ireland became available for the first time in 2013, taking the overall market size to £3.3 billion – more than double last year’s figure.

Positive vs ethical investingPositive investing is growing into a movement with a wide level of public engagement. In contrast, the green and ethical retail funds

market, which has been the mainstay of ethical investing since the early 90s and grew rapidly until 2009, has seen growth slow to under 4% a year over the last 3 years. This growth can largely be attributed to rises in underlying stock market values, with the FTSE 100 index increasing by 27% over the period, rather than by any wider public participation.

The collective size of the 80 funds that make up the ethical investment marketplace stood at £12.2 billion as of June 2013. At £3.2 billion, and with almost ten times the number of businesses and more people participating, positive investing should now be considered an equally important component of the ethical investing sector.

Credit unions (Northern Ireland)

Credit unions(Great Britain)

Positive savings

Direct Positive investments£140m

£684m

£762m

£1.6bn

£3.3bn

£2.1bn

+33%

£1.1bn

£1.0bn

£862m

£249m

2013Ethex report

2014Ethex report

Size of the positive savingand investing market

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

8

Section One The UK Positive Investment Marketplace

The investors

In the region of 1.7 million people now participate in the positive investing sector, representing 2.7% of the UK population. Of these 1.52 million are credit union members and around 170,000 make other positive savings and investments.

The businesses

The positive investing market consists of savings and investments in over 770 businesses: direct equity and bond investments in 249 charities and community businesses with a clear and strong social objective; savings with three positive institutions - the ethical banks Triodos and Charity Bank and the Ecology Building Society; and savings with 526 credit unions across the UK.

The money

Savings dominate the sector, representing 92% of its total value, however direct positive investments are growing at nearly three times the rate of savings.

Almost three quarters of positive savings are with credit unions, which are a fast-growing alternative to banks, building societies and payday lenders where members pool their savings to provide each other with credit at low interest rates.

£3.3bnsaved orinvested

1.7millionsaving accountsand investments

778businesses

8%

27%

31%

35% 8%

3%

60%

29%

32%

0.4%

47%

21%

Credit unions (Northern Ireland)

Credit unions (Great Britain)

Positive savings

Direct Positive investments

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

9

Section One The UK Positive Investment Marketplace

Growth in the marketThe most marked rate of growth since 2013 was to be found in direct positive investing rather than savings, which grew by 78% to £249 million. This reflects growing interest in a more direct, transparent and accountable way to save and invest.

Growth in direct positive investingDirect positive investing makes up only 8% of the value of the positive investment market but 32% of the businesses. This sector showed the most marked rate of growth, increasing by 78% since our last report to £249 million, as individuals sought out new investment opportunities.

Since our 2013 report, which analysed the market up to early 2012, 164 positive businesses have raised a total of just over £109 million in additional investment. This compares to less than 100 new offers in the whole of the three preceding years from 2009-11.

The three areas of direct investingDirect positive investments can be broken down into: investments in community shares; investments in bonds issued by charities; and investments in bonds and equity issued by companies with a clear social or environmental mission. Community share offers proved the liveliest part of the direct investment market.

Market share8% £249m

Growth rate+78% 2013–2014

£75m

£12m

£53m

2013 2014

Breakdown of the direct positive investment market Number of businesses raisinginvestment 2012–2014

Company equities

Company bonds

Charity bonds

Community shares£122m

£45m

£16m

£66m

£140m

£249m

Total 164

3

2

7

152

+78%

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

10

Section One The UK Positive Investment Marketplace

Community Shares

Of the 164 new offers undertaken since our 2013 report, 152 were for community shares, raising over £47 million of further investment across the UK.

Community shares have been used to finance shops, pubs, renewable energy initiatives, local food schemes, and community buildings, along with a host of other community based ventures. The new offers are highly diverse in the nature of the activity undertaken.

The commonest activity was community-owned renewable energy, where 56 schemes (37% of the total) raised £29 million. These offers qualified for Enterprise Investment Scheme relief, offering investors a tax rebate of 30% of the value of their investment.

Community shops and pubs also proved very popular with 59 offers undertaken with a total value of £6.6 million.

Number of community share offers undertaken in 2014 and sum raised

Total152

56 Renewable energy £29m

34 Community retail £1.9m

25 Pubs and brewing £4.7m

15 Social property and regeneration £2.5m

7 Food and farming £1.4m

4 Sports £730,000

3 Development and fairtrade £5.4m

3 Creative and media £240,000

3 Finance £420,000

1 Telecomms £700,0001 Transport £300,000

PEC Renewables, Plymouth

PEC Renewables

launched its

community share offer in

summer 2013 with the aim

of raising £500,000 to install

solar panels on over 20

schools and community

buildings across Plymouth.

Plymouth City Council provided

a further £500,000 in a low

cost loan to help get the

scheme off the ground.

The panels are installed

for free, and help reduce

school energy bills. Digital

displays installed in reception

show the pupils how

much energy their school

is generating and how much

carbon is saved. The scheme

receives subsidy from the

Feed in Tariff Scheme, and

any surplus energy is sold

to the grid. Profits are used

to give a return to investors,

and to tackle fuel poverty

in Plymouth.

The share offer was

oversubscribed, raising over

£600,000 before it was closed.

All funds came from individual

investors who invested from

£50 to £50,000.

“The share offer was oversubscribed raising over £600,000”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

11

Section One The UK Positive Investment Marketplace

Bonds and equitiesInvesting in positive bonds also proved popular. Just under £50 million was raised in nine offers as a number of charities and companies issued bonds to the public with the support of Triodos Bank, such as Bristol Together, St Mungos and Connexions.

The market was boosted by the first ever issues of positive bonds on the London Stock Exchange: a highly successful bond issue by renewable energy company Good Energy for £15 million following its listing on the AIM stock market; and the launch of Allia’s Retail Charity Bonds platform on the London Stock Exchange, which raised a further £11 million for the charity Golden Lane Housing, a subsidiary of Mencap that provides supported housing forpeople with a learning disability. Around 60% of the sum raised on the LSE by Golden Lane came from individuals rather than institutions.

By comparison, the market for positive investing in companies remained relatively flat, raising an additional £18 million, an increase of 25% but from only three companies, with more than half of the companies in this group raising no further funds at all.

“Around 60% of the sum raised on the LSE by Golden came from individuals rather than institutions”

Bristol Together, Bristol

Bristol Together

is turning rising

property prices to social

advantage – by employing

ex-offenders to renovate

empty properties. The

properties are sold on at

a profit to pay the costs of

the scheme. Out of more

than 60 men employed at

Bristol Together since 2011,

only one has reoffended,

compared to a national

average of 26% who reoffend

within one year of release.

In summer 2012, Bristol

Together raised £1 million

from a bond offering 3%

interest, of which £250,000

came from individual positive

investors. The money is being

used to acquire and renovate

up to 40 empty, run down

homes in Bristol.

The scheme expanded to

the West Midlands in summer

2001, with the launch of a

bond issue for £3 million by

Midlands Together. This time

almost half the finance raised

came from individual investors.

“Only 1 in 60 men employed has since reoffended”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

12

Section One The UK Positive Investment Marketplace

Growth in Savings Savings with Triodos, Charity Bank and Ecology Building Society have increased by £178 million to £862 million, up 26% since our 2013 report, as people continued to switch their accounts away from the big four banks and into the more democratic and transparent alternatives to be found in Triodos Bank, Charity Bank and the Ecology Building Society.

Credit unions in Britain saw growth of 31% and an increase of £240 million to reach £1 billion in deposits. This was fuelled by a growing recognition of the important role credit unions play in addressing the impacts of austerity. The Archbishop of Canterbury’s concerns about the social and emotional burden of debt caused by payday lending, and his call for a modernised and expanded credit union movement helped to bring renewed vigour to the sector. The UK Government also invested in systems modernisation so that credit unions can provide a better level of service.

Our 2013 survey revealed that the number of people in Northern Ireland engaged in direct investment in positive businesses was lower than in any other region of the UK. However we now know that the reverse is true when it comes to savings.

New data released by the FCA in 2013 tells us that engagement of the Northern Irish population in saving with a credit union is far greater than in the rest of the UK. More than one in four people (27%) of the Northern Irish population now hold a credit union account, as compared to 1.6% for the rest of the UK.

Positive savings

Market share27% £862m

Growth rate+26% 2013–2014

Credit Unions (Great Britain)

Market share31% £1.0bn

Growth rate+31% 2013–2014

Credit Unions (Northern Ireland)

Market share35% £1.1bn

Elaine and Geoff

are retired and

live in Southmead, Bristol.

When Elaine ran up debts

of over £4,500 on store cards,

it was Bristol Credit Union

that got her out of trouble.

“The staff sit you down

and talk to you, not like in

a normal bank. They went

through all our income

and out goings and made

suggestions about how

we could get through each

month without going short.”

Elaine managed to transfer

all of her debt to the credit

union by taking out a series

of small loans and ended up

being charged much less

interest. Once she had paid

off her debts, the credit union

lent her the money for her

wedding to Geoff, her long

term partner.

“Geoff and I got married

five years ago and it was

marvellous. The credit

union lent us £6,500 and

it’s all paid off now.”

Bristol Credit Union, Bristol

“They sit you down and talk to you, not like in a normal bank”

Section Two

The Hotspots

Steve Clarke invests in Golden Lane Housing’s provision of housing for people with a learning disability

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

14

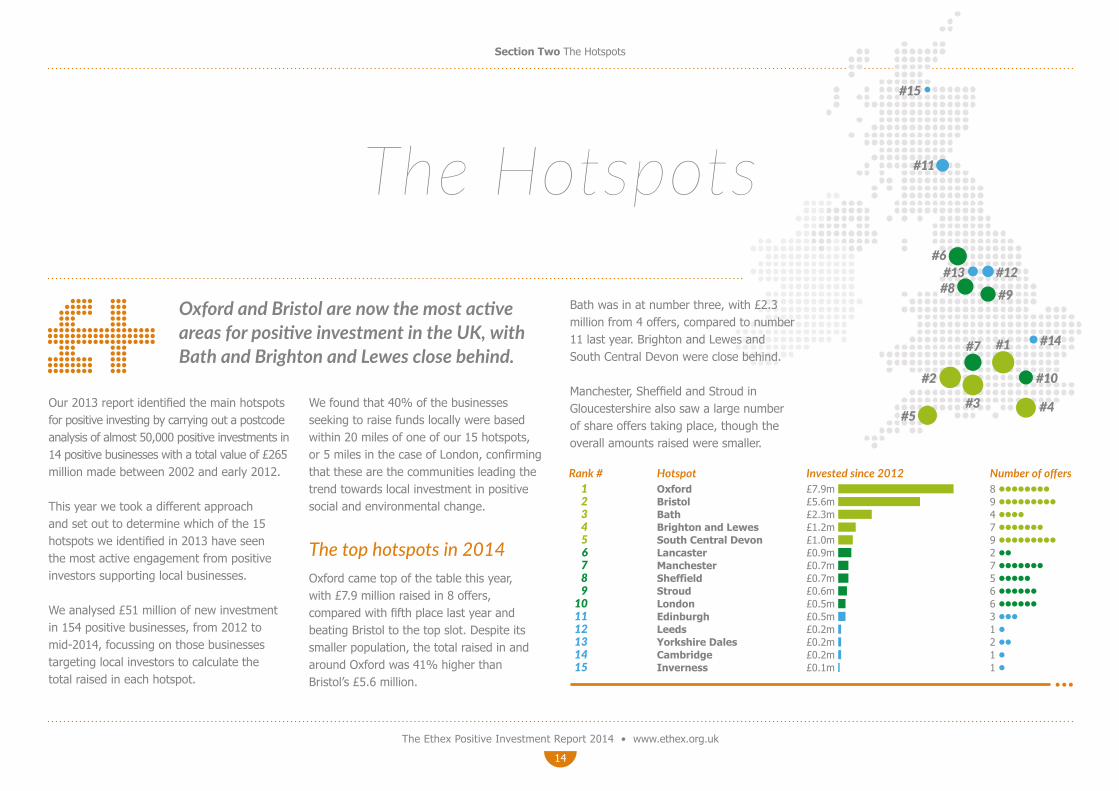

Our 2013 report identified the main hotspots for positive investing by carrying out a postcode analysis of almost 50,000 positive investments in 14 positive businesses with a total value of £265 million made between 2002 and early 2012.

This year we took a different approach and set out to determine which of the 15 hotspots we identified in 2013 have seen the most active engagement from positive investors supporting local businesses.

We analysed £51 million of new investment in 154 positive businesses, from 2012 to mid-2014, focussing on those businesses targeting local investors to calculate the total raised in each hotspot.

We found that 40% of the businesses seeking to raise funds locally were based within 20 miles of one of our 15 hotspots, or 5 miles in the case of London, confirming that these are the communities leading the trend towards local investment in positive social and environmental change.

The top hotspots in 2014Oxford came top of the table this year, with £7.9 million raised in 8 offers, compared with fifth place last year and beating Bristol to the top slot. Despite its smaller population, the total raised in and around Oxford was 41% higher than Bristol’s £5.6 million.

Oxford and Bristol are now the most active areas for positive investment in the UK, with Bath and Brighton and Lewes close behind.

Section Two The Hotspots

The Hotspots

Rank # Hotspot Invested since 2012 Number of offers1 Oxford £7.9m 82 Bristol £5.6m 93 Bath £2.3m 44 Brighton and Lewes £1.2m 75 South Central Devon £1.0m 96 Lancaster £0.9m 27 Manchester £0.7m 78 Sheffield £0.7m 59 Stroud £0.6m 6

10 London £0.5m 611 Edinburgh £0.5m 312 Leeds £0.2m 113 Yorkshire Dales £0.2m 214 Cambridge £0.2m 115 Inverness £0.1m 1

#15

#14

#13 #12

#11

#10

#9#8

#7

#6

#5 #4#3

#2

#1

Bath was in at number three, with £2.3 million from 4 offers, compared to number 11 last year. Brighton and Lewes and South Central Devon were close behind.

Manchester, Sheffield and Stroud in Gloucestershire also saw a large number of share offers taking place, though the overall amounts raised were smaller.

Rank # Hotspot Invested since 2012 Number of offers1 Oxford £7.9m 82 Bristol £5.6m 93 Bath £2.3m 44 Brighton and Lewes £1.2m 75 South Central Devon £1.0m 96 Lancaster £0.9m 27 Manchester £0.7m 78 Sheffield £0.7m 59 Stroud £0.6m 6

10 London £0.5m 611 Edinburgh £0.5m 312 Leeds £0.2m 113 Yorkshire Dales £0.2m 214 Cambridge £0.2m 115 Inverness £0.1m 1

Rank # Hotspot Invested since 2012 Number of offers1 Oxford £7.9m 82 Bristol £5.6m 93 Bath £2.3m 44 Brighton and Lewes £1.2m 75 South Central Devon £1.0m 96 Lancaster £0.9m 27 Manchester £0.7m 78 Sheffield £0.7m 59 Stroud £0.6m 6

10 London £0.5m 6 11 Edinburgh £0.5m 3 12 Leeds £0.2m 1 13 Yorkshire Dales £0.2m 2 14 Cambridge £0.2m 1 15 Inverness £0.1m 1

Rank # Hotspot Invested since 2012 Number of offers 1 Oxford £7.9m 8 2 Bristol £5.6m 9 3 Bath £2.3m 4 4 Brighton and Lewes £1.2m 7 5 South Central Devon £1.0m 9 6 Lancaster £0.9m 2 7 Manchester £0.7m 7 8 Sheffield £0.7m 5 9 Stroud £0.6m 6 10 London £0.5m 6 11 Edinburgh £0.5m 3 12 Leeds £0.2m 1 13 Yorkshire Dales £0.2m 2 14 Cambridge £0.2m 1 15 Inverness £0.1m 1

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

15

The Oxford area is the most active in the nation for community energy. Local investors are showing a strong appetite for new schemes, adding to an already vibrant renewable energy community.

Westmill Solar Co-operative raised £5.8 million back in the summer of 2012 and is still the largest community owned solar park in Europe. Osney Lock Hydro, a scheme to install an Archimedes screw on the River Thames in Oxford, raised its first £500,000 in just 4 weeks. Over 40% of the Osney investment came from within a mile of the project, and 4 out of every

Section Two The Hotspots

OxfordRanking: 1 Total investment: £7.9 millionNumber of Offers: 8

5 investors live in Oxfordshire. Low Carbon Oxford North also equipped two schools with solar panels on their roofs.

Low Carbon Hub, which supported the Osney hydro scheme and installed solar panels on the roof of the Oxford Bus Company in 2013, is continuing the drive to make Oxford self-sustaining in renewable energy. Its share offer for £1.5 million to complete solar panel installations on 21 schools across the county launched in September 14.

Not all Oxford’s offers focused on community energy. The Seven Stars Pub in Nuneham Courtney and the Bull in Great Milton were acquired by the local community; and Cultivate raised funds to supply Oxford with locally grown food.

These new community businesses add to those existing – such as the Turl Street Kitchen, which donates all its profits to Student Hubs, a charity that supports students in engaging in social action; the Ethical Property Company providing affordable office space for charities and campaign groups; and of course Ethex. Oxford’s role in building the social enterprise movement was recently recognised when Oxfordshire was the first county in Britain to be officially named a Social Enterprise Place by Social Enterprise UK.

BBarbara worked at

a senior level on

the government’s renewable

energy programmes until

2010. She is now Chief

Executive of the Low

Carbon Hub and a Director

of Low Carbon Oxford.

“Oxford is a hotspot for

community energy because

it is full of people who

understand the need

to take action. Across

Oxfordshire, over 8,000

people are working in low

carbon industries – that’s

the equivalent of two BMW car

factories. The City Council has

set a great example, cutting

Oxford’s carbon emissions

by 25% over five years.

In September it became

the first local authority in the

UK to pledge to divest from

fossil fuels.”

The Low Carbon Hub has just

launched a share offer on

Ethex to raise £1.5 million to

fund its next wave of projects,

which include 21 solar PV

schemes on local schools

and a number of businesses.

“Community energy puts local

power in the hands of local

people. Collective ownership

helps to engage people in

taking the serious action

that’s needed as part of

their lifestyle.”

The Hub is collaborating

with researchers at Oxford

University on pilot projects

such as local smart grids

that will make community

ownership more possible.

Barbara Hammond, Oxford

“Our aim is that local communities will be able to buy energy directly from the projects they own”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

16

Bristol continues to develop a strong identity as a forward thinking centre for green and community innovation in which positive investing plays an integral role.

Bristol will become European Green Capital in 2015. Led by its independent mayor George Ferguson, there has been a big push to get people out of cars and into buses and bicycles. A community share offer also kept the ferries running along the harbourside to the railway station.

Section Two The Hotspots

BristolRanking: 2Total investment: £5.6 millionNumber of Offers: 9

The launch of the Bristol Pound in 2013 has led to an upsurge of interest in local independent businesses. The Bristol Pound is the UK’s first city wide local currency, the first to have an electronic payment mechanism and to be managed by a regulated financial institution, and the first that can be used to pay local business rates and council tax. The mayor takes all of his salary in Bristol Pounds.

Local community-owned renewable energy schemes have also played their role in making Bristol one of the top hotspots for positive investing. Bristol Energy Co-operative and Bristol Power have installed solar panels on roofs across Bristol, and Wedmore Community Power and Low Carbon Gordano have set up large solar panel arrays in the surrounding countryside.

Bristol is also the home of Triodos Bank. It supported several offers including Bristol Together, which creates full-time jobs for local ex-offenders by bringing empty properties back into use, to raise £1.6 million, and bond issues by charities St Mungos and Connexions.

Steve Clarke, Bristol

Stephen Clarke

was until recently

a partner in a Bristol law firm,

but switched career at 60 to

become one of the founders

of the Bristol pound.

“I grew up in Bristol and find

it such an exciting place to live.

As a city it has a strong identity

and a fiercely independent

spirit. Money plays a key role

that – I want to see Bristol’s

wealth strengthening the

local economy not disappearing

off to some tax haven.”

Steve’s positive investments

include Golden Lane Housing

Bonds and the community

share issue for the local Bristol

harbourside ferry. He explains

what motivates him as a

positive investor:

“I am willing to take a risk

but am more motivated by

the social usefulness of an

investment than by an extra

0.5% interest. All of our pension

is ethically invested, but I have

little confidence in what the big

insurers mean by that.

“I invested in the Golden Lane

Bond because I would like to

support the institution (Mencap)

as well as the cause -

independent housing for people

with learning difficulties - and I

think it is a secure investment

with a reasonable return.”

“I don’t want to see Bristol’s wealth disappearing off to some tax haven”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

17

Bath is one of the most active areas for community energy in the UK. Bath and West Community Energy advised Wiltshire Wildlife Trust on raising £1.2 million for a solar array and assisted Low Carbon Gordano near Bristol to raise £2.2 million, and won the 2014 UK community Energy Organisation of the Year award.

Section Two The Hotspots

BathRanking: 3 Total investment: £2.3 millionNumber of Offers: 4

On September 17th, Bath and West Community Energy launched a new public share offer for £1.6million to build the 2.3MW Wilmington Farm Solar Array just outside Marksbury.

But community investing extends beyond renewable energy. When people heard that The Bell Inn in Walcot Street was to be sold there was great concern that an important live music venue would be lost. In just a few short months the community came together to raise over £700,000 to bring the pub into local ownership with more than 500 customers investing.

BPete Capener

is a trustee of the

Centre for Sustainable Energy

in Bristol as well as a member

of the government’s ministerial

Community Energy Contact

Group and interim chair of

Community Energy England.

He was recently named

Leader of the Year at the 2014

Community Energy Awards

for his work with the group

he co-founded and now chairs,

Bath and West Community

Energy (BWCE).

“Bath has a history of doing

things differently. We are lucky

to have a proactive council,

a history of community

action and a strong Transition

movement. There is a positive

community focus which is

fertile ground for investment

into realistic and dynamic

projects like BWCE’s.”

Like many great ideas, BWCE

was born in 2010 following a

conversation in a pub and in

a relatively short space of time

has grown into a working model

of how community ownership

can offer an alternative way

of doing business.

“By giving local people a

stake in the outcome,

community ownership will

increase the roll out of

onshore renewable energy.

But it also gives us all a

greater awareness of where

our energy comes from and

encourages us to consider

how we use energy in our

own lives.”

BWCE has raised over £6

million from local share offers,

funding the installation of over

3.5 MW of solar PV, enough

to meet the equivalent

annual electricity demand

from nearly 1,000 homes.

BWCE has just launched its

latest share offer, to raise £1.6

million towards the installation

of a new 2.34 MW solar array

at Wilmington Farm in Bath

& North East Somerset.

Pete Capener, Bath

“Community ownership encourages us to consider how we use energy in our own lives”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

18

The seat of Caroline Lucas, the UK’s only Green Party MP, Brighton has a long history of green independent thinking. Nearby Lewes shares the green independent spirit, and was the second town to launch a local currency in 2008, modelled on the first such currency from Totnes in South Devon.

In this hotspot, community energy was again the most popular investment. Ovesco in Lewes, who installed the UK’s first ever community owned 92kW solar power station

Section Two The Hotspots

Brighton and LewesRanking: 4 Total investment: £1.2 millionNumber of Offers: 7

on the roof of the local Harvey’s Brewery in 2011, raised a further £70,000 for new projects. And Brighton Energy raised £630,000 to install solar panels on roofs across the city.

In addition, Lewes’s community-owned football club raised more than £200,000 from local supporters to build an all-weather pitch to provide sporting opportunities for young people, and Exeter Street community hall and the Bevendean Pub in Brighton were acquired by the local community.

Paul Bellack is

a former fund

manager who is now a social

entrepreneur; his current roles

include directorships of the

Ethical Property Company

and OVESCO, the community

renewable energy company.

“As a community, Lewes is

always looking for new and

innovative ways to solve

its problems”.

Paul has been a positive

investor for 15 years, and

his investments include Good

Energy, PEC Renewables,

Low Carbon Gordano, the

Ethical Property Company, and

Communities for Renewables.

“As an entrepreneur I get

excited about supporting social

businesses, and I want to show

that business does not have to

be dirty – it can be ethical and

work well too. It is important

to have a sustainable model

that can produce not only a

social return, but a financial

one as well. “

“I’m passionate about the

environment, and particularly

interested in renewable

energy investments. It make

sense, they’re quite easy

to understand and less

risky, with a relatively

straightforward income. But

I’m also interested in investing

in other business models

that are ethical as well.

“As a fund manager in the

corporate world I was

disconnected from the impact

that my investments might

have. Ethical funds weren’t

really around in those days.

I now want to use my skills

and knowledge in a more

social way.”

Paul Bellack, Brighton and Lewes

PicturePaul Bellack

“As a community, Lewes is always looking for new and innovative ways to solve its problems”

Imag

e co

urte

sy o

f Be

vy P

ub

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

19

Section Two The Hotspots

South DevonIn South Devon, community energy projects raised £600,000 for wind and solar schemes in South Brent and Totnes, but the full range of community share issues included bookshops in Crediton and Dartmouth, shops in Blackawton, Ide, Littlehempston and Otterton and a community facility in Exmouth raising a further £400,000

Manchester, Lancaster and SheffieldIn other areas, Manchester and Sheffield have undertaken 12 offers between them since the start of 2012.

In Manchester, Greater Manchester Treestation makes use of waste wood for joinery and biomass, and the Fair Tax Mark offers recognition to businesses that pay a fair rate of tax. In Sheffield, the focus was on funds raised for renewable energy and the renovation of buidlings as community resources, while in Halton, close to Lancaster, over £850,000 was raised to install a turbine on the river Lune. Sheffield

Ranking: 8 Total investment: £0.7 millionNumber of Offers: 6

South Central DevonRanking: 5Total investment: £1.0 millionNumber of Offers: 9

ManchesterRanking: 7 Total investment: £0.7 millionNumber of Offers: 7

LancasterRanking: 6 Total investment: £0.9 millionNumber of Offers: 2

Imag

e co

urte

sy o

f D

uda

Arra

es

Imag

e co

urte

sy o

f Tr

ee S

tatio

n Im

age

cour

tesy

of

Hal

ton

Turb

ine

Section Three

The Positive InvestorsSam Daws invests in Bath

and West Community Energy

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

21

The Positive Investors

Since Ethex launched in February 2013 more than 1,000 people have opened an account, investing over £6 million in 30 businesses. We analysed this group to map recent shifts in positive investor behaviour. We found that a growing number of people are engaging with the impact of their money and becoming part of the nascent but growing positive investing movement.

Our data indicates an increasingly sophisticated investment strategy and attitude to risk amongst positive investors. More investors are building a diversified

portfolio of multiple investments rather than making one positive investment only; the average age of investors is falling; and the average amount they invest is increasing.

While the 1,000 sample size in the 2014 report is smaller than the 50,000 investments across 14 positive businesses that we analysed in 2013, the 2014 report covers a much shorter period of 18 months only, and the data is more reliable and detailed than previously as it is Ethex’s own. The 2014 data focuses only on direct positive investing and does not include any savings or credit union members

“Since Ethex launched in February 2013 more than 1,000 people have opened an account”

The number ofinvestments forming part of a portfolio has risen from 31% to 49% in the past year

Positive investorsare getting youngerwith 22% of Ethex

investors underthe age of 40, up

from 16% last year

<40

The overall averageamount of direct

positive investmentincreased from

£3,551 to £5,504in the past year

£

The number of investments forming

part of a portfolio has risen from 31%

to 49% in the past year

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

22

Section Three The Positive Investors

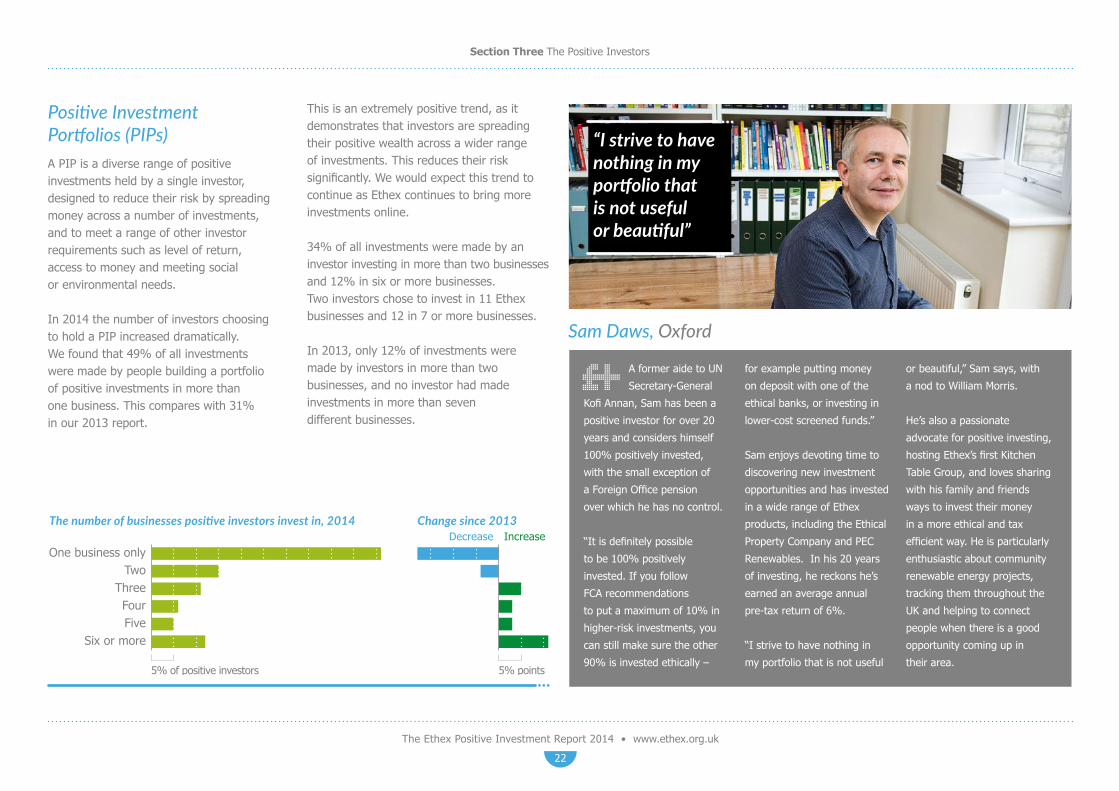

Positive Investment Portfolios (PIPs)A PIP is a diverse range of positive investments held by a single investor, designed to reduce their risk by spreading money across a number of investments, and to meet a range of other investor requirements such as level of return, access to money and meeting social or environmental needs.

In 2014 the number of investors choosing to hold a PIP increased dramatically. We found that 49% of all investments were made by people building a portfolio of positive investments in more than one business. This compares with 31% in our 2013 report.

This is an extremely positive trend, as it demonstrates that investors are spreading their positive wealth across a wider range of investments. This reduces their risk significantly. We would expect this trend to continue as Ethex continues to bring more investments online.

34% of all investments were made by an investor investing in more than two businesses and 12% in six or more businesses. Two investors chose to invest in 11 Ethex businesses and 12 in 7 or more businesses.

In 2013, only 12% of investments were made by investors in more than two businesses, and no investor had made investments in more than seven different businesses.

The number of businesses positive investors invest in, 2014 Change since 2013

One business onlyTwo

ThreeFourFive

Six or more

IncreaseDecrease

5% of positive investors 5% points

A former aide to UN

Secretary-General

Kofi Annan, Sam has been a

positive investor for over 20

years and considers himself

100% positively invested,

with the small exception of

a Foreign Office pension

over which he has no control.

“It is definitely possible

to be 100% positively

invested. If you follow

FCA recommendations

to put a maximum of 10% in

higher-risk investments, you

can still make sure the other

90% is invested ethically –

for example putting money

on deposit with one of the

ethical banks, or investing in

lower-cost screened funds.”

Sam enjoys devoting time to

discovering new investment

opportunities and has invested

in a wide range of Ethex

products, including the Ethical

Property Company and PEC

Renewables. In his 20 years

of investing, he reckons he’s

earned an average annual

pre-tax return of 6%.

“I strive to have nothing in

my portfolio that is not useful

or beautiful,” Sam says, with

a nod to William Morris.

He’s also a passionate

advocate for positive investing,

hosting Ethex’s first Kitchen

Table Group, and loves sharing

with his family and friends

ways to invest their money

in a more ethical and tax

efficient way. He is particularly

enthusiastic about community

renewable energy projects,

tracking them throughout the

UK and helping to connect

people when there is a good

opportunity coming up in

their area.

Sam Daws, Oxford

“I strive to have nothing in my portfolio that is not useful or beautiful”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

23

The age and gender of positive investorsOne of Ethex’s principal recommendations in 2013 was that positive investing needed to be brought to a younger audience. The direct positive investing market has historically been made up of people of 50+ years investing small amounts in one-off share issues. However an examination of Ethex data clearly demonstrates that younger investors are entering the market.

Our 2014 survey found that 33% of Ethex investors are over 60, compared with 42% of positive investors in 2013. Similarly,

Section Three The Positive Investors

20 to 2930 to 3940 to 4950 to 5960 to 6970 to 7980 to 89

90+

5% of positive investors 5% points

IncreaseDecreaseChange since 2013Age distribution of positive investors, 2014

How much positive investors are investing2014

Change since 2013

Sean, 25, has a

degree in Economics

from Bath University and is

now a freelance consultant

and writer in the sustainability

sector. His first positive

investment was £100 in

Stockwood Community Benefit

Society, a community-owned

biodynamic farm enterprise

in Worcestershire, which

launched a successful share

issue on Ethex last year.

“I believe that what you spend

represents your values. Money

is a super-important resource

and how you choose to spend

it is effectively a vote for

something. Like energy, food

is something that’s integral to

our health, eco-system and

society, but which we tend to

take for granted. And I trust

it to work better when owned

by communities rather than

large faceless institutions.”

Sean’s ability to invest

positively is limited by his

disposable income, but he

would like to continue with

Sean Buchan, Bristol

positive investing, perhaps

choosing one project a year

to invest in – and is thinking

about renewable energy next.

However, he still has a current

account with one of the

mainstream banks.

“My behaviour hasn’t changed

as quickly as I wanted,” he

says, “but I believe that by

investing positively early on, my

risk expectation will be easier

to adjust, and eventually I

would like to have 100% of my

savings in positive investments.”

“Money is a super-important resource and how you choose to spend it is effectively a vote for something”

22% of Ethex investors are now under 40 compared with 16% of positive investors in 2013.

Particularly striking was the finding that 9% of Ethex investors are aged 20 to 29, given that this age group made up just 3% of investors in our 2013 study.

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

Gender of positive investors

For the first time, Ethex is able to analyse the gender of its investors. We were surprised to find that two thirds of investors in 2014 were male, and one third female. There were more male than female investors in every age bracket, although with a higher than average number of females being the active investor in the 60 to 80 range. Only in the 70 to 79 range did the proportion of women investors approach 50%.

24

Age distribution of positive investors compared to the UK populationOverall, the age distribution of positive investors on Ethex has moved closer to that of the UK population as a whole. However positive investors tend to be on average older than the population as a whole as older people have more disposable income and are in a better position to make investments. The majority of positive investors are aged 40 to 69.

The average amount each person invests is also related to their age, with people aged 60 to 69 investing the most.

Section Three The Positive Investors

Female Male

5% 10%£1,000

20 to 2930 to 3940 to 4950 to 5960 to 6970 to 7980 to 89

20 to 2930 to 3940 to 4950 to 5960 to 6970 to 7980 to 89

Positive investors by agecompared to UK average

2014 Amount investedby age

Gender split by age

Positive investorsUK population

The Shepherd Family, Oxford

Jane Shepherd

from Oxford runs

Pigeon Organics, an organic

children’s clothing company.

She and her husband made

a small investment of around

£1,000 on behalf of her two

daughters in the Ethical

Property Company back in

2002. The business develops

and runs shared office

centres for non-profit

organisations and social

enterprises, and is based in

Oxford, so Jane had watched

it grow from nothing.

“It looked like a robust

investment and also an

opportunity to support

something worthwhile. As we

were doing it on behalf of our

children it felt more significant

that it was an investment

that would contribute to a

better future. It was an easy

decision to make at the time.”

Over 10 years on and the

girls, Alice (16) and Jess (13),

are now old enough to take

an interest in their investment,

and get excited when the

dividend cheque arrives each

year. Jane says, “Getting a

cheque in the post feels a

bit special, but they also

understand that they own

shares in a company that is

doing useful work.”

Alice adds, “I support fairtrade

and organic, and want a more

sustainable future. This feels

better than investing in just

anything because it’s ethical;

now I’m thinking about

switching to a more ethical

bank as well.”

“I support fairtrade and organic, and want a more sustainable future”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

25

Section Three The Positive Investors

The amounts positive investors investThe amounts that positive investors invest increased significantly in 2014.

In 2013, the commonest investment amount was from £100 to £500. In 2014, this had increased to from £500 to £1,000, with an overall shift to larger amounts across the board.

Furthermore the overall average amount for direct positive investment in our 2013 report was £3,551 but in 2014 was £5,504. This is an increase of 55%.

Guru Singh, Leicestershire

“Guru Singh, 65, is

a semi-retired GP

living near Loughborough.

“I look for an investment

which has green credentials,

is reasonably secure and with

a good return on investment.

It’s also important to me that

the project should help the

local community, so I look at

how it affects other people.”

Having installed solar panels

at home, switched to a green

energy provider, and invested

in double glazing to make his

home more energy efficient,

investing positively to have

an impact on climate change

was a logical next step.

Guru has four community

renewable energy investments

so far - in Triodos Renewables,

in the JCC Woodheat school

biomass project, in Wester

Derry wind turbine in Scotland

and in Calleva’s scheme to

install solar panels on the

rooftops of a business park

in Berkshire. He invests on

average around £2,000 a

time, and expects to earn

a return of 6% to 7% on each

one, more if EIS relief applies.

At some point, Guru explains,

he would like to become

100% positive invested –

however he recognises that

investing through funds and

ISAs is not always transparent,

so for now he focuses

on negatively-screened funds

that exclude unethical

investments.

“I look for an investment which has green credentials, is reasonably secure and with a good return on investment”

£0-£50£50-£100

£100-£500£500-£1k

£1k-£2k

£5k-£10k£10k-£20k£20k-£50k

£50k-£100k£100+

£2k-£5k

5% of positive investors 5% points

IncreaseDecrease

How much positive investors are investing2014

Change since 2013

0.3%

Section Four

The role of Ethex The Shepherd Family invests in The Ethical Property Company

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

27

Ethex is gathering together a growing community of individuals with a strong interest in positive investing. We maintain close dialogue with our investors at all times and are continuously learning what investors are looking for and how to grow the market.

It is the analysis of investments made through Ethex plus the nature of the discussions held with investors that have led to the conclusions reached in this report.

In May 2014 Ethex held its first ever Annual Gathering. Many investment

events focus on presenting the needs of the businesses to the investor – every business makes a short pitch for funds but there is no opportunity for the investors to learn from each other. The aim of the Ethex event was to focus on the needs of the individual investor. How well do they understand the risks and rewards of the positive investing marketplace?

What barriers do they personally face in deciding whether or not to make positive investments? What would it mean to be 100% positively invested, what benefits would that bring to society, and what would be the financial risks?

The Role of Ethex

Ethex launched in February 2013. In its first 18 months, 3,700 people have registered on the site and over 1,000 people have so far invested over £6 million in 30 positive investments.

The Annual Gathering gave rise to our first positive investing Kitchen Table group. A small number of investors came together to discuss how to go deeper. How could they support each other in achieving their positive investing aims?

As Ethex moves forward it will continue to catalyse change in the marketplace and to report on progress in building a positive investing movement that can act as a genuine alternative to the mainstream financial system.

At the request of its investors, Ethex is devising a positive investing personal action plan methodology for release in 2015 that will enable investors to calculate how positively invested they are, together with recommendations on how to improve. This method can be used by anyone regardless of their actual level of wealth and will act as a powerful self-educational tool.

“We maintain close dialogue with our investors at all times”

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

28

Section Four The Role of Ethex

About EthexEthex is a not-for-profit online web portal building a better market in ethical savings and investments. It aims to bring together on one website the full range of positive investments in fair trade, renewable energy, tackling poverty, organic farming, community shops and pubs, sustainable forestry, green transport, organic food and farming and social property.

Ethex makes positive investing easy to understand and easy to do. Anyone can browse, compare and choose investments that meet their personal social, financial and environmental objectives. Ethex also offers the ability to build and track a portfolio of positive investments.

Ethex provides a transparent secondary market for positive investments. This ensures that investors can see what shares are available to buy and sell at any time, and at what prices. As well as helping to discover their true market value, this secondary market provides a continuous investment opportunity for all positive investment products so that positive investors can buy and sell their investments at a fair price at any time. Ethex sees this service as an essential part of supporting people in making and managing their investments.

Through Ethex, positive investors can actively invest in businesses they believe in, and positive businesses can find the investment they need to grow.

“Ethex makes positive investing easy to understand and easy to do”

Sean Buchan invests in Stockwood biodynamic farm

Section Five

Conclusions

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

30

Seven years on from the financial crisis, a popular response to it can now be clearly seen in the growth of the positive investing movement. People want financial institutions

that can be trusted, and that are transparent and accountable. For a growing number of people, that means taking control of their money and making it do good, by making investments that deliver demonstrable benefit to society.

Conclusions

The momentum behind the positive investing movement is great, and the benefits that it stands to bring to society are significant. We describe here the three main ways in which this positive trend can be encouraged and supported.

Until these major barriers are overcome a properly functioning positive investing marketplace cannot become a reality.

Personal education in finance and investmentA broad educational programme focused on supporting people, young or old, in making their own financial decisions is a vital component of a more democratic and accountable financial services industry fit for purpose in the 21st century. The need for this programme is more pressing now

that younger people are entering the market, and overall more people are making investment decisions on their own behalf.

People in less well-off communities also need support on how to avoid the cycle of debt perpetrated by high street payday lenders. Credit Unions are playing a crucial role here in helping people with their financial management, but this could be further supported through personal education.

The Government’s decision to introduce personal finance into the secondary school curriculum from September 2013 is to be welcomed. Martin Lewis, the founder of Money Savings Expert, who has campaigned on the issue for many years has always seen the cycle of financial illiteracy in the UK as one of the main causes of our current

economic crisis and a major contributor to the mis-selling of financial products.

And yet, unless we wish to wait for the young to grow old for the problem to be solved, we need adult education too. Providing this education will help people to make more sophisticated investment decisions, reducing the risk of both bad investment choices and of mis-selling.

Ethex sees it as a central part of its role to educate and inform its investors, and is now devising a Positive Investing Personal Action Plan methodology, giving generic advice on how to improve your positive investing ‘score’, within the context of existing regulations |and conventionally accepted investment management strategies. Similar educational programmes could be offered by other investment sites, ideally with grant support from central government.

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

31

Section Five Conclusions

Greater investment in financial infrastructurePositive investing cannot develop without the infrastructure necessary to support it. An essential part of that infrastructure is a secondary market, in which people can know the true value of their investments, can easily sell them when they need to, and can buy even if there is no share offer running at the time.

Ethex believes that this secondary market will not function properly until there is a change of attitude from both positive investors and businesses.

Investors tend to believe that buying someone else’s shares is less socially useful than providing new capital to the business. There is an underlying suspicion that if someone wants to sell their investments, they must somehow be underperforming. However, this is paradoxical given that every investor will at some point want to sell their shares.

As to the businesses, once they have raised the capital they need, servicing investors tends to become less of a priority than running the business, and some do not take the steps necessary to ensure that investors are well serviced. This attitude is made worse by the use of tax incentives like EIS that mean no one can divest within three years without losing eligibility for the relief.

“Ethex has pioneered the provision of a secondary market for unlisted shares and community investments”

Even though positive investing is for the long term, in Ethex’s experience the demand to sell an investment starts to rise rapidly around five years after issue, and this leaves businesses with a large backlog of sellers if no action is taken. As more and more investments mature, the demand for a secondary market will increase dramatically. Without it, the supply of new capital will eventually dry up, as early investors are not able to realise or recycle their funds.

Ethex has pioneered the provision of a secondary market for unlisted shares and community investments, outside of the main stock exchanges. However these investments are less popular on Ethex than new offers, with only 11% of investment funds raised and 20% of businesses featured being of this type, as opposed to 52% of funds raised being new issues of shares and 28% issues of new bonds.

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

Section Five Conclusions

32

Proportionate and consistent regulationWhile regulation is essential to protect the investor from mis-selling, it is important that it does not become over-controlling and too complex to be readily understood. This is particularly true in the case of positive investments, which are almost exclusively made directly by individuals without the support of a financial professional.

As recently as two years ago, it was extremely hard to find out what positive savings and investments were available without going through a financial firm. But there is now a plethora of crowdfunding sites in the UK offering savings and investments to the general public.

The reaction of the Financial Conduct Authority (FCA) to the rapid expansion of the direct investment marketplace through crowdfunding has been to try to discourage the smaller non-professional investor from investing directly on their own account. In October 2014 it is bringing in new regulations that require people investing in unlisted securities without advice to complete a statement saying that they will not invest more than 10% of their investable wealth in investments of this type.

This is due to an understandable fear that investors might lose their money or be

misled. But while Ethex agrees that the 10% limit is a sensible one, the FCA’s approach runs the risk of being seen as deciding what is best for people rather encouraging them to make decisions on their own behalf.

Community share issues benefit from exemption from some FCA regulations on the promotion of investments to the public. This is on the basis that they are undertaken for social benefit rather than for financial gain, and that the inherently democratic nature of these organisations means that investors already have a greater say. However the FCA is expressing nervousness about the exemptions these organisations are afforded and has taken some steps to tighten them. For example, the FCA is now refusing to register co-operatives who apply

to set up community renewable energy schemes on the basis that they are not of direct benefit to their members. Schemes are required to set up as community benefit societies instead. This has limited the number of community schemes registering and introduced uncertainties for renewable energy co-operatives already set up.

At the same time, government is angling to remove EIS tax relief from community energy schemes. This is in spite of the government’s Community Energy Strategy, published in January, which expresses a desire to grow the community energy sector significantly.

The benefit of this regulatory exemption is that it makes it possible and affordable to offer directly to the public investments that

contribute to a better society at low cost and with a low minimum investment threshold. Many people are motivated to make their first ever investment through this route. These kinds of investment therefore play a vital role in widening access to the financial system as a whole, and in helping people to learn about the risks and rewards of investing through the actual experience of it.

However, it is the duty of those businesses afforded the privilege of this exemption to ensure that it is used responsibly, and exercising that responsibility in a growing market will require a degree of professionalism. This will inevitably come at some additional cost, although costs should remain at a significantly lower base than in the regulated sector.

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

33

Data for this report was drawn from three main sources. We would like to thank The Cooperative Shares Unit in Manchester, for their detailed data on community share issues undertaken

since 2010, and the Association of British Credit Unions, also in Manchester, for their guidance on where to find data on credit unions. The remaining information came from Ethex’s own data bank of positive investments featured on Ethex.

Research Methodology

Size of the marketplaceData on the size of the marketplace was either drawn directly from the reports of the businesses concerned, or from centralised sources. The centralised sources were the Financial Conduct Authority and the Prudential Regulatory Authority for data on credit unions; the Community Shares Unit for data on community shares; and Triodos Bank for share offers supported by them.

Data on the size of the green and ethical funds market was drawn from research undertaken annually by EIRIS (Ethical Research and Information Services).

The number of savers and investorsWhilst precise numbers of savers are available for credit unions and other savings, it has been necessary to estimate

the number of investors on the basis of the average investment size in the 2013 report. It should also be noted that some individuals hold more than one investment, meaning that the total number of people investing will be less than the total number of investments held.

The hotspotsOur 2013 report analysed by postcode almost 50,000 positive savings investments in 14 businesses and with a total value of £265 million, made since 2002 and still current in early 2012, to identify 15 hotspots for positive investing across the United Kingdom.

In 2014 we took a different approach and set out to determine which of the 15 hotspots we identified in 2013 have seen the most active engagement from positive investors supporting local businesses.

The Ethex Positive Investment Report 2014 • www.ethex.org.uk

Section Six Research Methology

34

We analysed all of the new share offersundertaken between the start of 2012 and mid-2014 and the change in amounts saved since the last report to show the growth in the market. We further analysed the 164 share offers undertaken to determine which of our hotspots had shown the highest level of activity over the period.

In order to ensure that the data truly reflects local activity, the three national savings institutions Triodos, Ecology Building Society and Charity Bank and a number of share offers by larger organisations were excluded from the hotspot analysis on the basis that their funds were not predominantly raised from local investors. Data from credit unions was also excluded as sufficiently detailed information was not available.

This left us analysing £51 million of investment in 154 businesses to give a picture of which of our 2013 hotspots have seen the most active engagement from positive investors supporting local businesses over the last two years.

We focused only on businesses within 20 miles of the hotspots identified in last year’s report. In the case of London, this distance was reduced to 5 miles due to the far higher population density and the high degree of variation from area to area.

The positive investorsData analysis was carried out on 1,044 Ethex customers who had opened an account with us since our launch in February 2013. These had all had been through anti-money laundering checks, ensuring that we had full and accurate data on them. Of these 1,044 customers, 622 had placed a total of 938 orders ranging from £10 to £250,000 in value in 30 different businesses.

It should be noted that age data from 2013 included savings accounts opened by adults on behalf of children aged under 20. In 2013, this was 5% of all savers and investors. However because Ethex does not itself handle any positive savings account openings directly, data on accounts opened by adults on behalf of children was not available to Ethex in 2014 and therefore the under 20 age bracket was ignored.

For more information contact

EthexThe Old Music HallCowley RdOxfordOX4 1JE

+44 (0)1865 [email protected]

Written and researched by Jamie Hartzell with the help of the rest of the Ethex team

Design by Greenhatdesign.co.ukInfographics by Lulu Pinney @lulupinney

© Ethex 2014