madalena energy inc. suite 3200, 500 - 4th avenue sw

TRANSCRIPT

Madalena’s PMS-1135(h) Fracture Treatment: Rio Negro, Argentina

Advancing Four Unconventional Resource Plays and Implementing North American Horizontal Technology in Argentina

JUNE 2015

Head Office:

MADALENA ENERGY INC.

Suite 3200, 500 - 4th Avenue SW

Calgary, Alberta, Canada T2P 2V6

Argentina Office:

MADALENA ENERGY S.A.

421 Lola Mora, 13th Floor

Buenos Aires, ARG C1011ABE

www.madalenaenergy.com

MVN (TSX-V)

MDLNF (OTC)

Madalenae n e r g y inc.

READER ADVISORIES

JUNE 2015 2

Forward-Looking Statements or Information

Certain statements contained in this presentation of Madalena Energy Inc. ("Madalena" or the "Corporation") constitute forward-looking statements or information (collectively "forward-looking statements")

within the meaning of the "safe harbour“ provisions of applicable securities legislation. Forward-looking statements are typically identified by words such as "anticipate", "continue", "estimate", "expect",

"forecast", "illustrative", "may", "will", "project", "could", "plan", "intend", "should", "believe", "outlook", "objective", "aim", "potential", "target", "seek", "budget", "predict", "might" and similar words and

derivatives thereof suggesting future events or future performance. All statements other than statements of historical fact may be forward-looking statements. In addition, statements relating to "reserves" or

"resources" are deemed to be forward-looking statements as they involve the implied assessment, based on certain estimates and assumptions, that the reserves or resources described exist in the quantities

predicted or estimated and can be profitably produced in the future. In particular, this document contains, without limitation, forward-looking statements pertaining to the following: all details of, all projections

of future activities related to, and all expectations of our performance and results as a result of executing Madalena's short and long term plans, strategies and goals, and the benefits anticipated to accrue to

Madalena and its securityholders as a result thereof; expected production levels; expected additional oil and gas plays that could provide opportunities to the Corporation; expected product types in the

Corporation's areas in which it holds assets; expected operations to be undertaken by the Corporation in the future and the timing thereof; type-curves for various kinds of wells that are expected by the

Corporation and the assumptions related thereto; growth; the use of funds from production; Madalena's inventory of drilling locations; the expected quality of the Corporation's assets and the

probability of successful operations on such assets; the thickness of zones in Madalena's assets; the quality of infrastructure in the areas in which the Corporation operates; matters pertaining to Madalena’s

reserves and resources; Madalena’s corporate vision; matters pertaining to the 2015 capital budget including the source of funds for the budget; improving netbacks and operating costs; and matters pertaining to

commodity prices and our operating environment.

With respect to forward-looking statements contained in this document, we have made assumptions regarding, among other things: the expected nature of and timing of operational activity; Madalena's ability

to execute on its short and long-term plans as described herein and the impact that the successful execution of such plan will have on Madalena and its shareholders; the laws and regulations that Madalena will

be required to comply with, including laws and regulations relating to taxation, royalty regimes and environmental protection; future capital expenditure levels; future crude oil, natural gas liquids and natural

gas prices and differentials between light, medium and heavy oil prices and Canadian, WTI and world oil prices; future crude oil, natural gas liquids and natural gas production levels; drilling results; future

exchange rates and interest rates; future debt levels; the cost of expanding Madalena's property holdings and growing production; Madalena's ability to obtain equipment in a timely manner to carry out

exploration and development activities and the costs thereof; Madalena's ability to market oil and natural gas successfully to current and new customers; the impact of increasing competition; Madalena's

ability to obtain financing on acceptable terms; and our ability to add production and reserves through Madalena's development and exploitation activities. In addition, many of the forward-looking statements

contained in this document are located proximate to assumptions that are specific to those forward-looking statements, and such assumptions should be taken into account when reading such forward-looking

statements.

Although Madalena believes that the expectations reflected in the forward-looking statements contained in this presentation, and the assumptions on which such forward-looking statements are made, are

reasonable, there can be no assurance that such expectations will prove to be correct. Readers are cautioned not to place undue reliance on forward-looking statements included in this document, as there can

be no assurance that the plans, intentions or expectations upon which the forward-looking statements are based will occur. By their nature, forward-looking statements involve numerous assumptions, known

and unknown risks and uncertainties that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur, which may cause our actual performance

and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward-looking statements. These risks and

uncertainties include, among other things: the possibility that Madalena will not be able to successfully execute its short or long-term plan in part or in full, and the possibility that some or all of the benefits that

Madalena anticipates will accrue to it and its securityholders as a result of the successful execution of such plans do not materialize; the impact of weather conditions on seasonal demand and Madalena's ability

to execute capital programs; risks inherent in oil and natural gas operations; uncertainties associated with estimating reserves and resources; competition for, among other things, capital, acquisitions of reserves,

resources, undeveloped lands and skilled personnel; incorrect assessments of the value of acquisitions; geological, technical, drilling and processing problems; general economic and political conditions in

Canada, the U.S., Argentina and globally, and in particular, the effect that those conditions have on commodity prices and Madalena's access to capital; industry conditions, including fluctuations in the price of

crude oil, natural gas liquids and natural gas, price differentials for crude oil produced in Canada and Argentina, respectively, as compared to other markets, and transportation restrictions; royalties payable in

respect of oil and natural gas production and changes to government royalty frameworks; changes in government regulation of the oil and natural gas industry, including environmental regulation; fluctuations

in foreign exchange or interest rates; unanticipated operating events or environmental events that can reduce production or cause production to be shut-in or delayed (including wild fires and flooding); failure

to obtain regulatory, industry partner and other third-party consents and approvals when required, including for acquisitions, dispositions and mergers; failure to realize the anticipated benefits of dispositions,

acquisitions, joint ventures and partnerships; changes in taxation and other laws and regulations that affect us and our securityholders; the potential failure of counterparties to honour their contractual

obligations; and the other factors described under "Risk Factors" in our Annual Information Form, and described in our public filings available in Canada at www.sedar.com. Readers are cautioned that this list of

risk factors should not be construed as exhaustive.

The forward-looking statements contained in this document speak only as of the date of this document. Except as expressly required by applicable securities laws, we do not undertake any obligation to publicly

update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The forward-looking statements contained in this document are expressly qualified by this

cautionary statement.

JUNE 2015 3

Presentation Outline

� Madalena Overview and Yearly Growth Comparison

� Argentina Commodity Prices

� Summary of Key Properties

� SurubiConventional oil production – “Cash Cow”

� Coiron Amargo

� Conventional base + growth production

� Unconventional Shale Oil upside in Vaca Muerta

• Curamhuele

• High impact exploration in scalable unconventional resource plays

• Lower Agrio Oil, Mulichinco Liquids Rich Gas and Vaca Muerta shale

� Puesto Morales

� Conventional base production

� Loma Montosa oil resource play – scalable development

� Closing Summary

MADALENA ENERGY INC.: Argentina Focused

JUNE 2015 4

� Trading Symbol: TSXV – MVN

� Total Issued and Outstanding Shares ~541 million

� Market Capitalization ($0.37/share) ~$200 million

� March 31, 2015 Positive Working Capital ~$ 3 million

� 2015 Budget Up to $44 million

� 100% of 2015 Budget directed towards Argentina

� Current Base Production ~4,000 Boe/d (~95% from Argentina)

� Additional ~400 Boe/d of Temporarily Shut-in Volumes in Canada

Conventional Assets Provide Solid Platform

� 2014 YE Proved and Probable (“2P”) Reserves ~11.5 MMBoe

� 2014 YE 2P NPV@10% Btax ~$200 MM

Four Unconventional Resource Plays Provide Growth & Strategic Value

MADALENA ENERGY INC.: Overview

UPSTREAM OIL AND GAS COMPANY FOCUSED ON THE DELINEATION OF

SHALE AND UNCONVENTIONAL RESOURCES IN ARGENTINA

5JUNE 2015

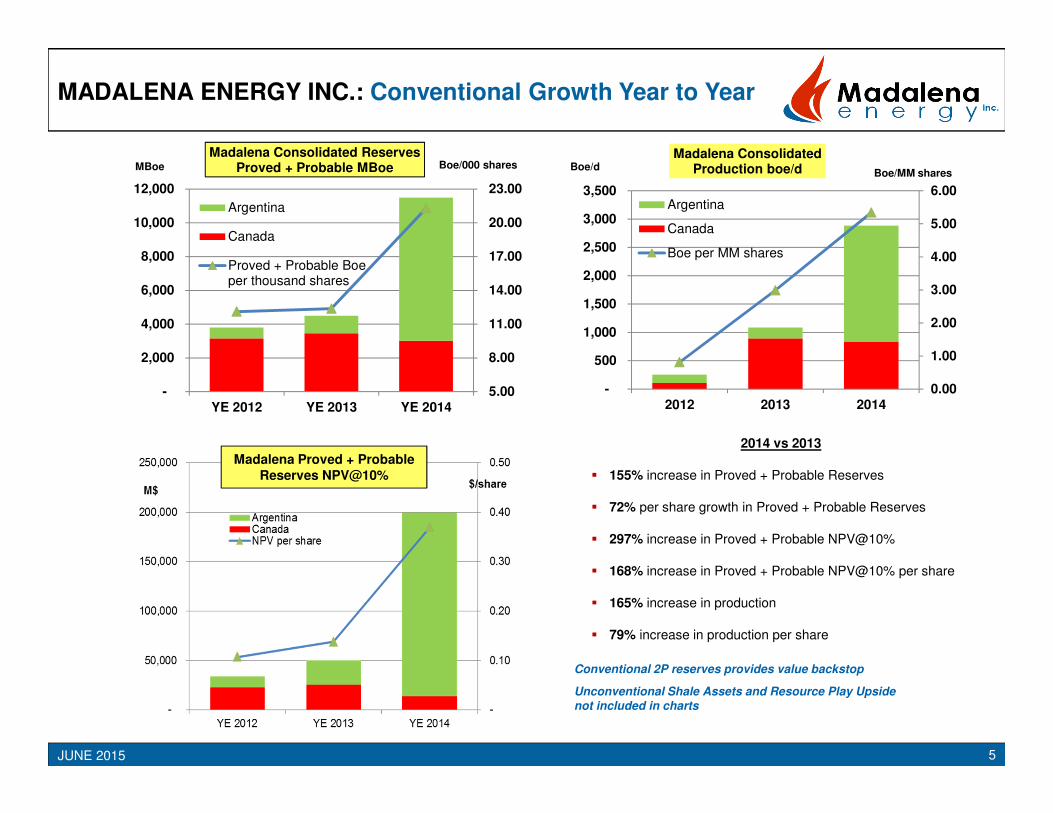

MADALENA ENERGY INC.: Conventional Growth Year to Year

5.00

8.00

11.00

14.00

17.00

20.00

23.00

-

2,000

4,000

6,000

8,000

10,000

12,000

YE 2012 YE 2013 YE 2014

Madalena Consolidated ReservesProved + Probable MBoe

Argentina

Canada

Proved + Probable Boeper thousand shares

MBoe Boe/000 shares

2014 vs 2013

� 155% increase in Proved + Probable Reserves

� 72% per share growth in Proved + Probable Reserves

� 297% increase in Proved + Probable NPV@10%

� 168% increase in Proved + Probable NPV@10% per share

� 165% increase in production

� 79% increase in production per share

Madalena Proved + Probable Reserves NPV@10%

0.00

1.00

2.00

3.00

4.00

5.00

6.00

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2012 2013 2014

Madalena ConsolidatedProduction boe/d

Argentina

Canada

Boe per MM shares

Boe/dBoe/MM shares

Conventional 2P reserves provides value backstop

Unconventional Shale Assets and Resource Play Upside not included in charts

6JUNE 2015

ARGENTINA OIL PRICING: Current Regulated Premium to Brent

� In Argentina, oil prices are set by the government monthly for product sold into the domestic oil market

� Regulators in Argentina set April & May 2015 oil pricing at approximately USD $76 per barrel for Medanito qualitycrude oil which continues to remain well above comparative Brent price and WTI benchmarks

� February 2, 2015 – USD $3.00 / Bbl (royalty free) incentive program above USD $76/Bbl Medanito price

� Madalena Q1 2015 operating netback1 $37.16/Bbl (doesn’t include incentive program at this time)

� Madalena recently entered into a new gas contract at USD $5.30/mmbtu for period May to September 2015

Note: 1Operating netback is a non-GAAP measure calculated as the average per boe of the Company’s oil and gas sales, less royalties and operating costs

40

50

60

70

80

90

100

110

120

130

140

Jan

-11

Ma

r-1

1

Ma

y-1

1

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Ma

r-1

2

Ma

y-1

2

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Ma

r-1

3

Ma

y-1

3

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Ma

r-1

5

Ma

y-1

5

Jul-

15

Historical Oil Price US$/Bbl -Argentina Medanito vs Brent and WTI

Argentina US$/Bbl

WTI US$/Bbl

Brent US$/Bbl

JUNE 2015

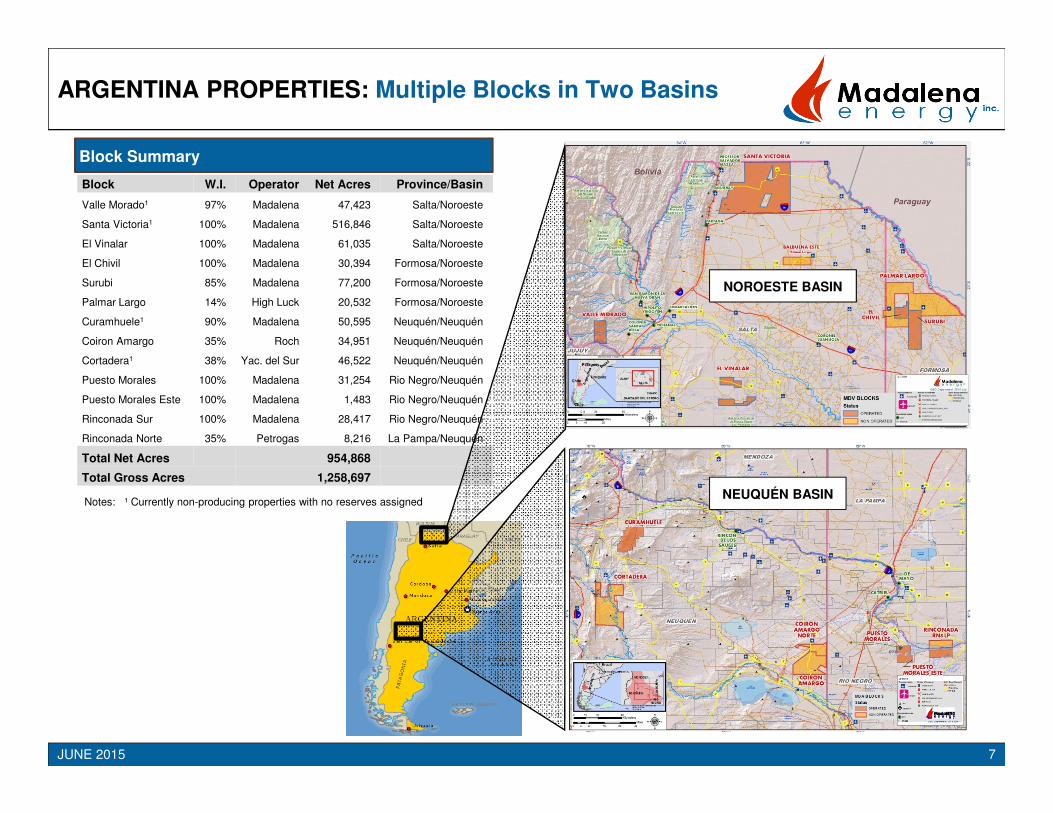

ARGENTINA PROPERTIES: Multiple Blocks in Two Basins

7

Block Summary

Notes: ¹ Currently non-producing properties with no reserves assigned

Block W.I. Operator Net Acres Province/Basin

Valle Morado1 97% Madalena 47,423 Salta/Noroeste

Santa Victoria1 100% Madalena 516,846 Salta/Noroeste

El Vinalar 100% Madalena 61,035 Salta/Noroeste

El Chivil 100% Madalena 30,394 Formosa/Noroeste

Surubi 85% Madalena 77,200 Formosa/Noroeste

Palmar Largo 14% High Luck 20,532 Formosa/Noroeste

Curamhuele1 90% Madalena 50,595 Neuquén/Neuquén

Coiron Amargo 35% Roch 34,951 Neuquén/Neuquén

Cortadera1 38% Yac. del Sur 46,522 Neuquén/Neuquén

Puesto Morales 100% Madalena 31,254 Rio Negro/Neuquén

Puesto Morales Este 100% Madalena 1,483 Rio Negro/Neuquén

Rinconada Sur 100% Madalena 28,417 Rio Negro/Neuquén

Rinconada Norte 35% Petrogas 8,216 La Pampa/Neuquén

Total Net Acres 954,868

Total Gross Acres 1,258,697

NOROESTE BASIN

NEUQUÉN BASIN

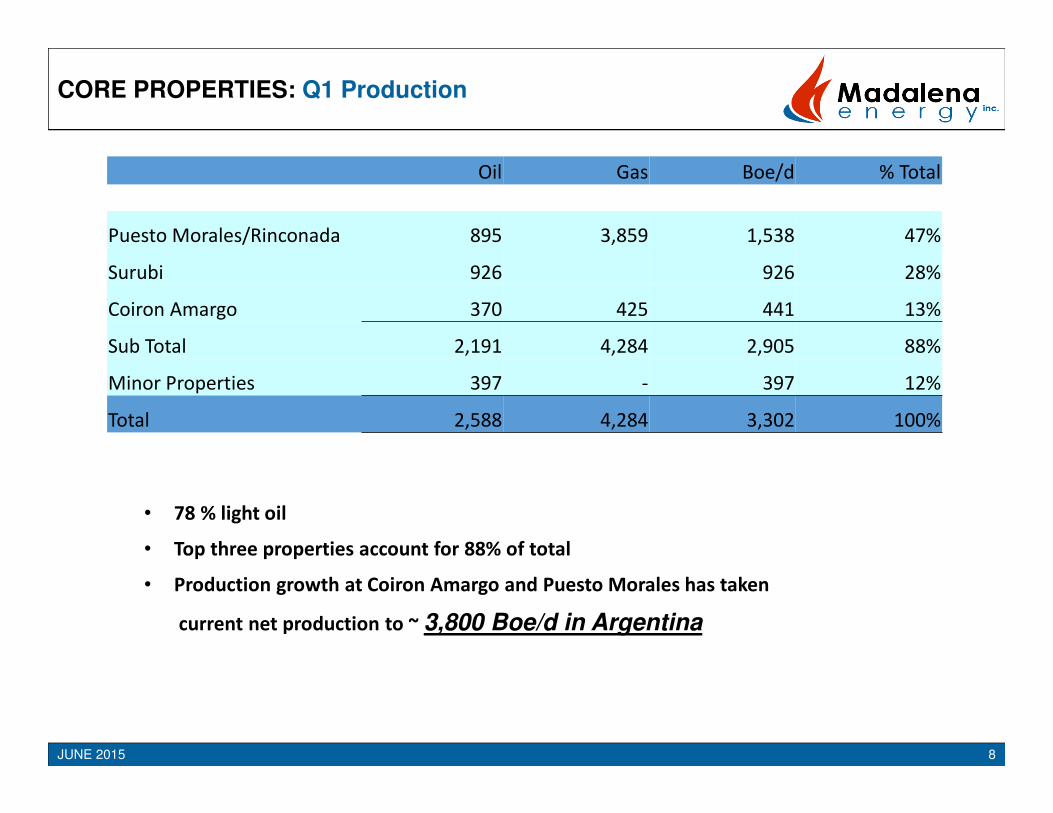

CORE PROPERTIES: Q1 Production

8JUNE 2015

Oil Gas Boe/d % Total

Puesto Morales/Rinconada 895 3,859 1,538 47%

Surubi 926 926 28%

Coiron Amargo 370 425 441 13%

Sub Total 2,191 4,284 2,905 88%

Minor Properties 397 - 397 12%

Total 2,588 4,284 3,302 100%

• 78 % light oil

• Top three properties account for 88% of total

• Production growth at Coiron Amargo and Puesto Morales has taken

current net production to ~ 3,800 Boe/d in Argentina

!(!(!(!!

!!!(

!(!(!(

Buenos Aires

Lima

Quito

Bogota

Caracas

Santiago

Brasilia

Montevideo

Santo Domingo

!!̂

!!̂

!!̂

!!̂

!!̂ !!̂

!!̂

!!̂

!!̂

B R AB R A

A R GA R G

P E RP E R

C O LC O L

B O LB O L

V E NV E N

P R YP R Y

C H LC H L

E C UE C U

U R YU R Y

G U YG U Y

S U RS U RG U FG U F

P A NP A N

D O MD O MJ A MJ A M

A R GA R G

U S AU S A

!

!

!

!

!

!

!

!

!

!

!!

!

!

! !

!

!

!

!

!

!

!

!

!

!

PALMAR LARGOWI: 14%

PALMAR LARGO(BALBUENA ESTE)

WI:14 %

CHIVILWI: 100%

SURUBIWI: 85%

TEUCO

HONDO

EL CHORRO

PILCOMAYO

A r g e n t i n aA r g e n t i n a

P a r a g u a yP a r a g u a yS

ou

th

At

l an

ti c

Oc

ea

n

So

ut

hP

ac

ific

Oc

ea

n

F

Formosa

Province

SaltaP

rovi

nce

Legend

Operated Property

Non-Operated Property

Palmar largo

Field

Surubi

Block

JUNE 2015

Northern Properties: Surubi, Chivil and Palmar Largo

� Surubi –Mature stable production platform

� High volume, lower op costs resulting in the

highest netback (Q1 ~ US$ 53/bbl)

� No interference from PROA-3 to original PROA-2

� Wells currently flowing, opportunity to go to

high volume lift

100

1,000

10,000Surubi Field: PROA Structure Daily Oil (bbls/d)1

1) - Madalena has an 85% WI in Surubi

NOROESTE BASIN: Conventional Light Oil Production with Exploration Upside

JUNE 2015 10

Additional Exploration & Appraisal Blocks

� EL Chivil -1 00% Operated (Producing)

� El Vinalar - 100% Operated (Producing)

� Santa Victoria - 100% Operated

� Valle Morado - 96.6% Operated

� Multiple exploration leads on 2D and 3D seismic

Palmar Largo (14% Non-Op)17 wells have cum. production of > 40 MMBbls

Surubi (85% Operated)Proa-2 well has produced > 1.1MM Bbls in 21 mo.

Palmar Largo(Balbuena Este)

Surubi

Palmar Largo

El Chivil

Palmar Largo

El Vinalar

Valle Morado

Santa Victoria

Bolivia

Paraguay

Argentina125 km

Operated (Exploration)

Non-operated (Exploitation)

Operated (Exploitation)

El Chivil

Palmar Largo

Surubi

11JUNE 2015

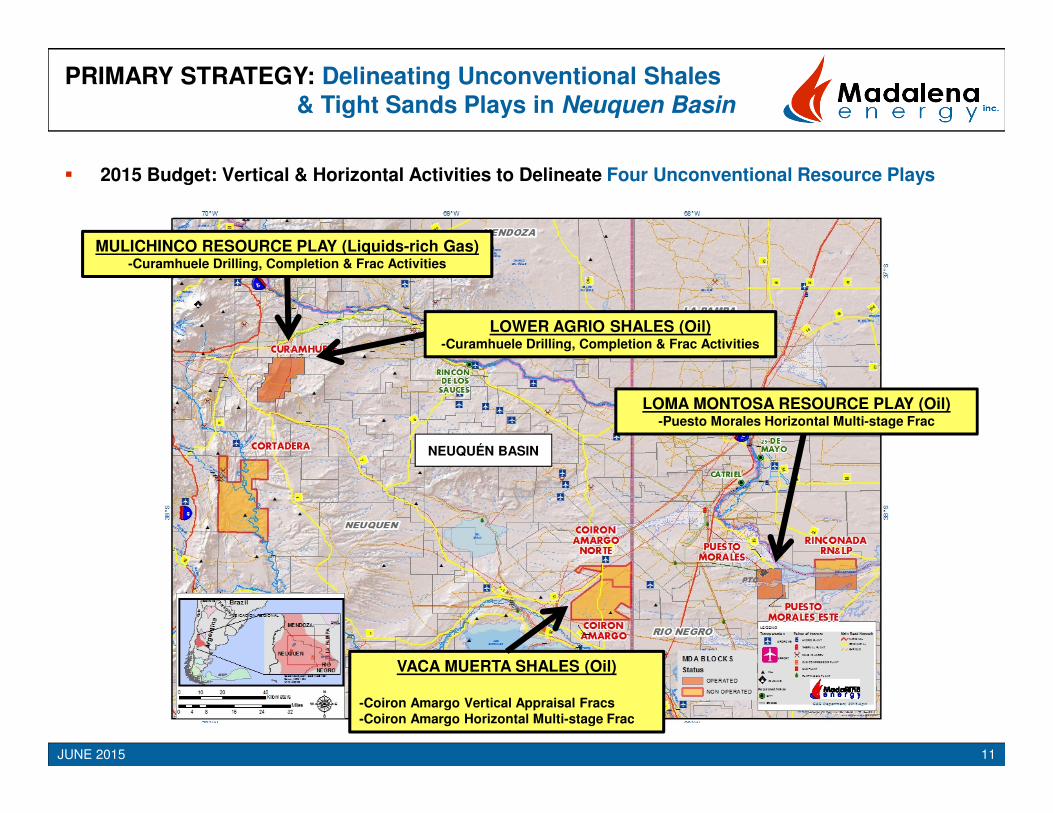

� 2015 Budget: Vertical & Horizontal Activities to Delineate Four Unconventional Resource Plays

PRIMARY STRATEGY: Delineating Unconventional Shales & Tight Sands Plays in Neuquen Basin

LOMA MONTOSA RESOURCE PLAY (Oil)-Puesto Morales Horizontal Multi-stage Frac

MULICHINCO RESOURCE PLAY (Liquids-rich Gas)-Curamhuele Drilling, Completion & Frac Activities

LOWER AGRIO SHALES (Oil)-Curamhuele Drilling, Completion & Frac Activities

VACA MUERTA SHALES (Oil)

-Coiron Amargo Vertical Appraisal Fracs -Coiron Amargo Horizontal Multi-stage Frac

NEUQUÉN BASIN

COIRON AMARGO: Recent Offsetting Vaca Muerta Operations

12JUNE 2015 12

Aguada Federal -Wintershall;

March 16, 2015 (Wintershall website)

-2 vertical VM wells in 2015

-Contingency of 6 horizontal VM wells

La Amarga Chica -Petronas;

May 2014 (YPF Website)

-2015 -4 vertical VM wells

+ 2 horizontal VM wells

Loma Campana -Chevron / YPF;

Jan. 9, 2015 (Petrolnews.net)

-200 VM wells on production

-2015 -120 vertical VM wells

+ 40 horizontal VM wells Cruz de Lorena & Sierras Blancas –Shell;

Dec. 2, 2014 (O&G Journal)

-Plan to invest $250 MM exploring 2 blocks

Dec. 16, 2014 (Shell)

-2015 Operations to include 7 wells in VM

plus 1 vertical well for microseismic

CURAMHUELE: Recent Offsetting Activities Lower Agrio Shale & Vaca Muerta Shale

JUNE 2015 13

Madalena e n e r g y inc.

Development Potential in the Vaca Muerta , Lower Agrio & Mulichinco

� Offsetting activity by internationaloperators including ExxonMobil, YPF, Chevron and Total

Mulichinco to be evaluated in theMadalena Yp.x-1001 vertical well

- Offsetting Yp.x-1st tested at 10 MMcf/d of gas and 500 Bbls/d of 51º condensate after acidizing

Lower Agrio shale to be evaluated in theMadalena Ch.x-1 vertical well

- Originally flowed ~75 Bopd without frac/stimulation

Los Toldos II (ExxonMobil / Americas Petrogas)

LTE.x-1 (Vaca Muerta) -Tested 694 Bbls/d 40⁰ API oil + 618 Mcf/d gas- IP30: 254 Bbls/d 40⁰ API oil + 330 Mcf/d gas

ADA.x-1 (Vaca Muerta) -Tested 260 Bbls/d

Los Toldos I (ExxonMobil / Americas Petrogas)

ALL.x-1 (Vaca Muerta) -Tested 3.2 MMcf/d + 18 Bbls/d of 54-58⁰ condensate

EL TRAPIAL (CHEVRON)

-ET.x-2006 (Vaca Muerta)-Indicated to be capable of significant liquids and gas production- Four Vaca Muerta delineation wells drilled in 2014

August 14, 2014 YPFannounces “very importantoil discovery” in the Agrio

La Invernada (ExxonMobil)

LAL.x-3 (Hz) (Vaca Muerta) -On completion

Loma Del Molle (YPF)

LDMo.x-1 (Vaca Muerta)

Loma Del Molle (YPF)

CLMi.x-1 (Vaca Muerta) –Fraced in 6 stages

YPF

YPF

YPF

Total

YPF

Total Chevron

ExxonMobil

ExxonMobil

ExxonMobil

YPF

Source: Based on mapping by the Gobierno de la Provincia del Neuquén, modified by Madalena Energy Inc.

*** See “Analogous Information” on Slide 30 of this presentation.

14JUNE 2015

Prospective at Coiron Amargo, Curamhuele and Cortadera� Thickness¹ >500m –Progressively deeper & thicker from east to west in the basin

� Thickness¹ >1000m with the inclusion of the overlying Quintuco formation

� Madalena expects that the Vaca Muerta is Oil prone at Coiron Amargo, Gas prone around the Cortadera block and Gas & Liquids prone at Curamhuele

VACA MUERTA SHALE PLAY: Overview

Sources: (Isopach Map) Madalena Energy Inc. mapping; (Thermal Maturity Map) Based on mapping by the Gobierno de la Provincia del Neuquén, modified by Madalena Energy Inc.

Note: ¹ Ryder Scott Company, Petroleum Consultants, May 2013 and Madalena Energy Inc. internal data; Madalena owns a 35% working interest in the Vaca Muerta rights on the Coiron Amargo block, a 90% working interest in the Vaca Muerta rights on the Curamhuele block and a 38% working interest in the Vaca Muerta rights on the Cortadera block in the Neuquen basin of Argentina. Madalena expects the Vaca Muerta to be oil prone at Coiron Amargo, gas prone at Cortadera and gas & liquids prone at Curamhuele. Please see the disclosure at the beginning of this presentation and Madalena’s AIF dated April 16, 2015 for details with respect to the risks and uncertainty associated with Madalena and its business.

*** See “Analogous Information” on Slide 30 of this presentation.

JUNE 2015

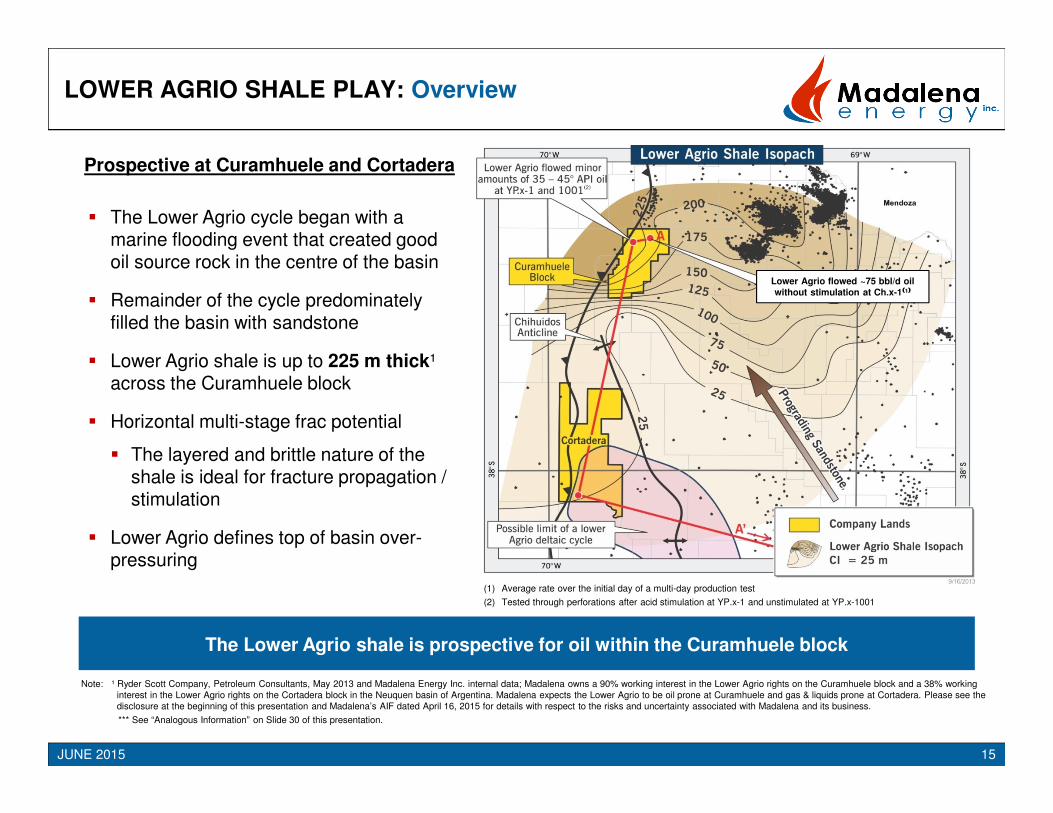

The Lower Agrio shale is prospective for oil within the Curamhuele block

� The Lower Agrio cycle began with a marine flooding event that created good oil source rock in the centre of the basin

� Remainder of the cycle predominately filled the basin with sandstone

� Lower Agrio shale is up to 225 m thick¹ across the Curamhuele block

� Horizontal multi-stage frac potential

� The layered and brittle nature of the shale is ideal for fracture propagation / stimulation

� Lower Agrio defines top of basin over-pressuring

Prospective at Curamhuele and Cortadera

(1) Average rate over the initial day of a multi-day production test

(2) Tested through perforations after acid stimulation at YP.x-1 and unstimulated at YP.x-1001

LOWER AGRIO SHALE PLAY: Overview

Note: ¹ Ryder Scott Company, Petroleum Consultants, May 2013 and Madalena Energy Inc. internal data; Madalena owns a 90% working interest in the Lower Agrio rights on the Curamhuele block and a 38% working interest in the Lower Agrio rights on the Cortadera block in the Neuquen basin of Argentina. Madalena expects the Lower Agrio to be oil prone at Curamhuele and gas & liquids prone at Cortadera. Please see the disclosure at the beginning of this presentation and Madalena’s AIF dated April 16, 2015 for details with respect to the risks and uncertainty associated with Madalena and its business.

*** See “Analogous Information” on Slide 30 of this presentation.

15

Lower Agrio flowed ~75 bbl/d oil without stimulation at Ch.x-1⁽⁽⁽⁽¹⁾⁾⁾⁾

JUNE 2015

The Mulichinco tight sandstones are prospective for gaswithin the Curamhuele and Cortadera blocks

� Liquids-rich gas bearing tight sand play

� Rapid thickening (> 200 m )¹ of the Mulichinco on the Curamhuele and Cortadera blocks

� Significant horizontal development potential in the lowermost and coarser clastic portion of the Mulichinco

− Deposited during an initial low-stand period

� Total S.A. reportedly drilling successful Mulichinco horizontals at Aguada Pichana

� Significant Mulichinco production test on Madalena land at Curamhuele

Prospective at Curamhuele and Cortadera

MULICHINCO LIQUIDS-RICH GAS RESOURCE PLAY: Overview

16

Note: ¹ Ryder Scott Company, Petroleum Consultants, May 2013 and Madalena Energy Inc. internal data; Madalena owns a 35% working interest in the Mulichinco rights on the Coiron Amargo block, a 90% working interest in the Mulichinco rights on the Curamhuele block and a 38% working interest in the Mulichinco rights on the Cortadera block in the Neuquen basin of Argentina. Madalena expects the Mulichinco to be gas prone at Cortadera and gas & liquids prone at Curamhuele. Please see the disclosure at the beginning of this presentation and Madalena’s AIF dated April 16, 2015 for details with respect to the risks and uncertainty associated with Madalena and its business.

*** See “Analogous Information” on Slide 30 of this presentation.

JUNE 2015 17

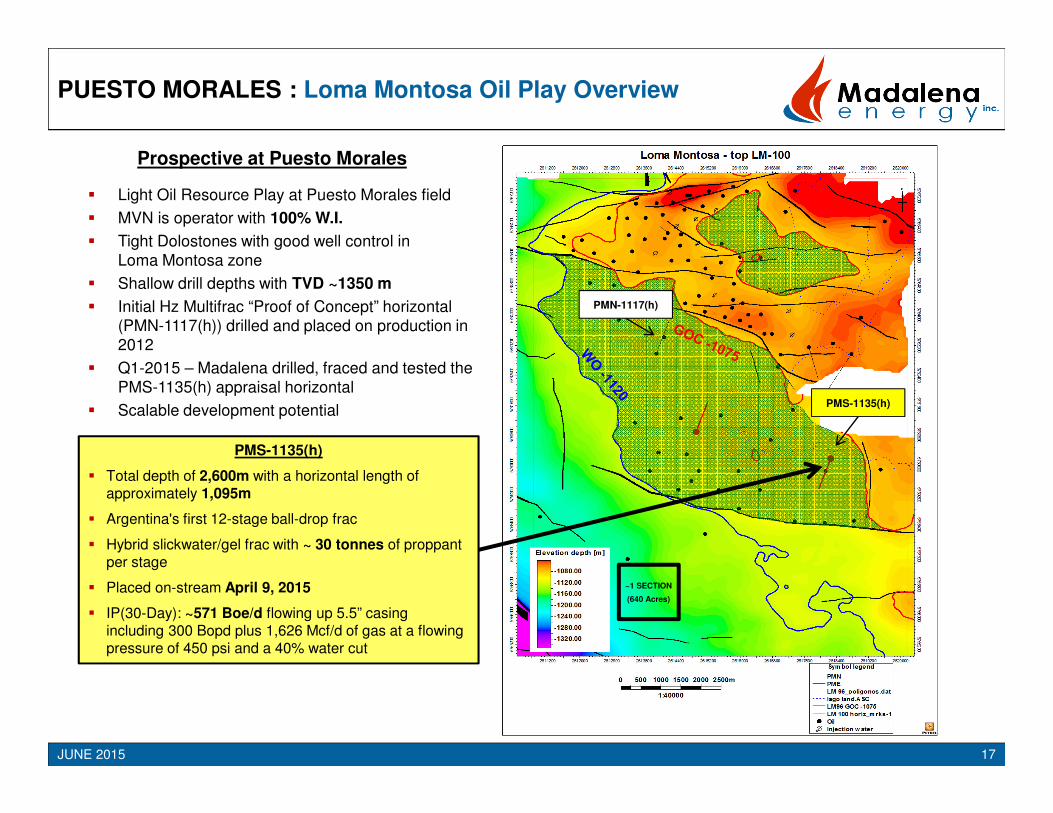

PUESTO MORALES : Loma Montosa Oil Play Overview

Prospective at Puesto Morales

� Light Oil Resource Play at Puesto Morales field

� MVN is operator with 100% W.I.

� Tight Dolostones with good well control in Loma Montosa zone

� Shallow drill depths with TVD ~1350 m

� Initial Hz Multifrac “Proof of Concept” horizontal (PMN-1117(h)) drilled and placed on production in 2012

� Q1-2015 – Madalena drilled, fraced and tested thePMS-1135(h) appraisal horizontal

� Scalable development potential

PMS-1135(h)

� Total depth of 2,600m with a horizontal length of approximately 1,095m

� Argentina's first 12-stage ball-drop frac

� Hybrid slickwater/gel frac with ~ 30 tonnes of proppant per stage

� Placed on-stream April 9, 2015

� IP(30-Day): ~571 Boe/d flowing up 5.5” casingincluding 300 Bopd plus 1,626 Mcf/d of gas at a flowing pressure of 450 psi and a 40% water cut

PMN-1117(h)

PMS-1135(h)

~1 SECTION

(640 Acres)

10

100

1,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

PMS-1135

30 day IP 570 Boe/dBoe/d

LOMA MONTOSA OIL PLAY:Applying N.A Horizontal Technology in Argentina

18JUNE 2015

PMN-1094

Offsetting Vertical

PMN-1117 (Hz)500m Hz with 5 fracsProved-up concept

PMS-1135(h): Longer Hz, More Stages & Bigger Fracs Providing Solid Results To Date

TARGET

300 MBoe Type Curve

LOMA MONTOSA OIL PLAY:Applying N.A Horizontal Technology in Argentina

19JUNE 2015

1011

a-4

Horiz.Well

Be

stR

ese

rvo

ir

PMS-1135 (h)

LM-100

LM-93/96

Net thickness Res3-4-5 thicknessPHIE

Puesto Morales Facilities: Madalena Operated & Controlled

20JUNE 2015

PMN Main Battery

• Q4 Oil

968 bbl/d

• Capacity

~ 12,000 bbls/d

• Q4 Gas

4.1 mmcf/d

• Capacity

~ 7.8 mmcf/d

• Expandable to

~ 15.5 mmcf/d

• Oil Sales Line

~ 12,000 bbls/d

• Gas Sales Line

~ 30 mmcf/d

• Originally cost approximately USD $40 MM to build Plant & Infrastructure

• Room to Grow via Horizontal Development in Loma Montosa Oil Resource Play

21

Applying N.A. Horizontal Technology to Conventional Light Oil Development� Coiron Amargo Norte (108 km2) converted to 25-year exploitation license (MVN 35% W.I. -Non-Op)

� Recently placed CAN-16(h) well on-production

� Additional horizontals planned for 2015

� Inventory of low-risk horizontal development wells

� GLJ 2P approximately 10% Recovery Factor – opportunity for growth

Source: Madalena Energy Inc. mapping

CAN-15(h)CAN-15(h)

CAN.xr-2(h)CAN.xr-2(h)

CAN-18(h)

CAN-16(h)

� Avg. production over the first 60 days was 450 bopd, 670 mcf/d ~564 Boe/d (197 Boe/d WI)

� As of May 16, 2015 the well was flowing 480 bopd, 1000 mcf/d ~ 650 Boe/d (227 Boe/d WI)@ wellhead pressure of 1225 psi and a 19% water cut

COIRON AMARGO NORTH: Sierras Blancas Horizontals

JUNE 2015

465 491

388

330

287 260 248 250

233

195 196

129

178 173 183 174

163 162 153

113 112 105 105 110

216

728 693 662

761

624

547 516 520

451 432 418 408 410

347 353

304

524 490

432

360

255

145 146

170 176 195

158

192

227

149

112

45

169

442 460

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Average Daily Oil Prod Coiron Hz Well v Offset Sierras Blancas Hz

Average of seven LJE wells

CAN.xr-2(h)

CAN-15(h)

CAN-18(h)

CAN-16(h)

CAN-15(h) - now pumping

CAN.xr-2(h) - Cum 254 Mbbls in 17 months

CAN-18(h) now pumping

CAN-16(h) - recently

increased to 650-700 Boe/d

22

COIRON AMARGO NORTH: Sierras Blancas Horizontal Prod

JUNE 2015

MADALENA ENERGY: Argentina Focused Plan

23JUNE 2015

� Entering 2015 with No Debt & Focused Plan

� Active Argentina Focused Drill Program in 2015

2015 / 2016 Plan:

Advance Four Key Resource Plays

�Loma Montosa Oil resource play at Puesto Morales - Initial Success at Puesto Morales

on Scalable Asset

� Lower Agrio Shale oil at Curamhuele

� Mulichinco Liquids-Rich Gas resource play at Curamhuele

� Vaca Muerta Shale at Coiron Amargo

Continue to Implement North American Horizontal (Hz) Technology in Argentina

� Continued horizontal development of multiple Sierras Blancas light oil pools

� Follow-up on Loma Montosa horizontal success with multi-well horizontal program

� Work with partners on design and planning for first Hz multi-frac into the Vaca Muerta shale

� Continue to assess Non-core Asset Sales and Joint Venture Partnerships

JUNE 2015 24

APPENDICES

Kevin Shaw, P. Eng., MBA – President & CEO� Previously Managing Director & Head of Energy Research at a boutique

investment bank; Prior to a Senior E&P Research Analyst and Partner, Wellington West Capital Markets (now National Bank)

� Prior thereto, held various technical, senior management and/or officer roles with ExxonMobil (via Imperial Oil), Trimox Energy Inc. (VP Operations & Engineering), WorleyParsons (BP Alliance Manager).

Thomas Love, CA – VP, Finance & CFO� Previously CFO, Online Energy Inc., CFO, Trimox Energy and Moxie

Exploration and President & CEO, Moxie Petroleum

� Prior thereto with Westward Energy Ltd. and Charterhall Oil Canada, Articled at Clarkson Gordon & Co. (now Ernst & Young LLP)

Steve Dabner, P. Geol. – VP, Exploration� Previously President and CEO, Online Energy Inc., President & CEO,

Trimox Energy and Moxie Exploration and VP Exploration, Moxie Petroleum

� Prior thereto with Cimarron Petroleum Ltd. and Home Oil Company Ltd.

Stephen Kapusta, P. Eng. – Head of Engineering

� Over 30 years of diverse Operations, Reservoir Engineering and Management experience. Actively involved in the planning and execution of complex operations in unconventional reservoirs over the past 15 years;

� Previously with Texaco, Unocal, Star Oil & Gas, Canex Energy and Zargonin senior officer, director, consultant or manager roles.

Ruy Riavitz – Argentina Country Manager

� Previously E&P Manager, Hidenesa Gas SA (now GyP of Neuquen) & Independent Engineering Consultant

� Prior thereto Senior Consultant, PA Consulting, Reservoir Engineer, YPF

Robert Stanton, P. Eng. - VP, Operations� Previously VP, Operations, Online Energy Inc., VP, Engineering and

Operations, Result Energy Inc.

� Prior thereto with Oiltec Resources Ltd., Pinnacle Resources Ltd., Jordan Petroleum Ltd., Transwest Energy Inc., Triton Canada Resources Ltd., Canadian Worldwide Energy Ltd. and Petro-Canada Inc.

Barry Larson

� VP Operations & COO, Parex Resources Inc.(South American producer)

Gus Halas

� Director of Triangle Petroleum Corp. & executive roles at Central Garden a & Pet, T-3 Energy Services, Dresser’s Pump Services & Aquilex Corp

Jay Reid

� Partner, Burnet, Duckworth & Palmer LLP

Keith MacDonald

� President, Bamako Investment Management Ltd; Director of Surge Energy and Bellatrix

Kevin Shaw, P. Eng., MBA

� President & CEO, Madalena Energy Inc

Raymond Smith, P. Eng.

President, CEO & Director, Bellatrix Exploration Ltd.

Steven Sharpe (Chairman)

� Former Chairman of Longview Oil Corp (acquired by Surge Energy) & Advantage Oil & Gas; Former Director of Renegade (acquired by Spartan)

Ving Woo, P. Eng.

� Former VP, Engineering & COO, Bellatrix Exploration Ltd.

MANAGEMENT TEAM BOARD OF DIRECTORS

APPENDIX #1: Experienced Full-Cycle Operating Team

25JUNE 2015

June 2013 – EIA Released Updated World

Shale Oil & Gas Assessment

� Argentina has 4th largest technically

recoverable shale oil resource in the

world

� Behind only Russia, USA & China

� 3X greater than Canada

� Argentina has 2nd largest technically

recoverable shale gas resource in the

world

� Behind only China

� 1.2X greater than USA

� 1.4X greater than Canada

� Three Shale Plays in Argentina:

Vaca Muerta, Agrio, Los Molles

� Neuquén Basin is a the focus of Shale

Resource development by Major E&Ps and

NOCs

APPENDIX #2: Argentina’s World-Class Shale Potential

26JUNE 2015

*** See “Analogous Information” on Slide 30 of this presentation.

27JUNE 2015

APPENDIX #3: Vaca Muerta vs US Shales

The Vaca Muerta shale compares favourably to leading US shale resource plays

0

250

500

750

1,000

m

Shale Thickness

Oil Shales Gas Shales

Shale Comparisons

Vaca Muerta Shale

Madalena’s Coiron

Amargo Area ¹ Eagle Ford ² Bakken ³

Vaca Muerta Shale

Madalena’s Cortadera

Area ¹ Barnett ⁴ Haynesville ⁴ Marcellus ⁴

Thickness (m) 70 - 140 15 - 100 10 - 40 950 - 1350 45 - 75 70 - 90 20 - 45

Depth (m) 2800 - 3200 2200 - 3400 2700 - 3400 3200 - 4500 2300 3700 2100

Porosity (%) 4 - 8 4 - 11 5 - 8 6 - 10 4 - 8 7 - 9 7 - 9

Permeability (nD) 50 - 250 40 - 1300 50K – 500K 30 - 1000 50 - 200 100 - 500 100 - 200

TOC (%) 7 1 - 7 2 - 18 4 4 - 5 3 - 4 4 - 7

Reservoir Pressure (psi) 6300 - 8000 4700 - 7800 3800 – 8400 >11,000 3000 - 3800 7200 - 9100 3500 - 4200

Pressure Gradient (psi/ft) 0.65 – 0.75 0.65 – 0.70 0.43 – 0.75 >0.75 0.4 – 0.5 0.6 – 0.75 0.5 – 0.6

Notes: ¹ Ryder Scott Company, Petroleum Consultants, May 2013 and Madalena Energy Inc. internal data; Madalena owns a 35% working interest in the Vaca Muerta rights on the Coiron Amargo block, a 90% working

interest in the Vaca Muerta rights on the Curamhuele block and a 38% working interest in the Vaca Muerta rights on the Cortadera block in the Neuquen basin of Argentina. Madalena expects the Vaca Muerta to be oil prone at Coiron Amargo, gas prone at Cortadera and gas & liquids prone at Curamhuele. Please see the disclosure at the beginning of this presentation and Madalena’s AIF dated April 16, 2015 for details with respect to the risks and uncertainty associated with Madalena and its business.

² EOG Analyst Conference, April 2010

³ Tudor, Pickering, Holt, “The Bakken Momentum Continues” November 2011, Hart Energy Playbooks 2008 & 2010, Jarvie – AAPG Section Meeting 2008

⁴ Schlumberger, World Shale Summit September 2013 -Gas y Petroleo del Neuquén and YPF

*** See “Analogous Information” on Slide 30 of this presentation.

28JUNE 2015

APPENDIX #4: ARGENTINA VS. CANADAHigher Risk = Larger Rewards

Fiscal Differences

� Regulated oil and gas pricing (May US $ 76/Bbl), future prices set on monthly basis

� Incentive programs for oil and gas pricing set by regulators and usually awarded based on production/reserves criteria

� Restrictions on free movement of funds and currency control measures

� Foreign exchange risk with US$ sales, Argentina PESO expenses and reporting in CDN$

� Block contracts require continual management and negotiations for amendments and/or extensions

� Higher inflation rates in Argentina affects cost structures and local business

� New Hydrocarbon Law has improved regulatory and fiscal understanding between Federal and Provincial Governments

Operational Differences

� Access to services requires more planning and longer lead times

� Unionized workforce provides additional complexities

� Import restrictions & complex regulatory approval system can impact the ability to execute in a timely fashion

Note: For additional information on risks see Company’s YE 2014 MD&A dated April 16, 2015 or the Company’s Annual Information Form (”AIF”) dated April 16, 2015

Potential to unlock much bigger value in Argentina makes the challenges of

operating there worthwhile, but effort and patience are required to achieve success

Greater Paddle River Core Area (>150 Net Sections of Land)

� High Working Interest & Primarily Operated

� Multiple Plays for horizontal multi-stage frac operations:

� Nordegg -Emerging ~139 net sections-Oil & Liquids-rich gas

� Ostracod -Development ~57 net sections-Oil

� Notikewin/Wilrich -Development ~137 net sections-Liquids-rich gas

� Additional opportunities exist in: Viking oil, Rock Creek oil

� Large Inventory of unbooked horizontal drilling locations

� Drill-Ready Program of horizontal development wells

29JUNE 2015

APPENDIX #5: CANADIAN ASSETS - West-Central Alberta

ALBERTA

CALGARY

EDMONTON

READER ADVISORIES

JUNE 2015 30

Barrels of Oil Equivalent

All calculations converting natural gas to barrels of oil equivalent ("boe") have been made using a conversion ratio of six thousand cubic feet (six "Mcf") of natural gas to one barrel of oil, unless otherwise stated. The use of boe may be misleading,

particularly if used in isolation, as the conversion ratio of six Mcf of natural gas to one barrel of oil is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Analogous Information

Certain information in this document may constitute "analogous information" as defined in National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities ("NI 51-101"), including, but not limited to, information relating to areas, wells and

/or operations that are in geographical proximity to or on-trend with prospective lands held by Madalena and production information related to wells that are believed to be on trend with Madalena's properties. Such information has been obtained

from government sources, regulatory agencies or other industry participants. Management of Madalena believes the information may be relevant to help define the reservoir characteristics in which Madalena may hold an interest and such

information has been presented to help demonstrate the basis for Madalena's business plans and strategies.

However, to Madalena’s knowledge, such analogous information has not been prepared in accordance with NI 51-101 and the Canadian Oil and Gas Evaluation Handbook and Madalena is unable to confirm that the analogous information was prepared

by a qualified reserves evaluator or auditor. Madalena has no way of verifying the accuracy of such information. There is no certainty that the results of the analogous information or inferred thereby will be achieved by Madalena and such information

should not be construed as an estimate of future production levels. Such information is also not an estimate of the reserves or resources attributable to lands held or to be held by Madalena and there is no certainty that the reservoir data and economics

information for the lands held or to be held by Madalena will be similar to the information presented herein. The reader is cautioned that the data relied upon by Madalena may be in error and/or may not be analogous to such lands to be held by

Madalena.

Initial Production Rates

Any references in this document to test rates, flow rates, initial and/or final raw test or production rates, early production, test volumes and/or "flush" production rates are useful in confirming the presence of hydrocarbons, however, such rates are not

necessarily indicative of long-term performance or of ultimate recovery. Such rates may also include recovered "load" fluids used in well completion stimulation. Readers are cautioned not to place reliance on such rates in calculating the aggregate

production for Madalena. In addition, the Vaca Muerta shale is an unconventional resource play which may be subject to high initial decline rates. Such rates may be estimated based on other third party estimates or limited data available at this time and

are not determinative of the rates at which such wells will continue production and decline thereafter.

Financial Outlook

Any financial outlook or future oriented financial information in this presentation, as defined by applicable securities legislation, was approved by management of Madalena on January 7, 2015. Such financial outlook or future oriented financial

information is provided for the purpose of providing information about management's current expectations and plans relating to the future. Readers are cautioned that reliance on such information may not be appropriate for other purposes.

Non-GAAP Measures

In this presentation, management uses certain key performance indicators and industry benchmarks such as cash flow and operating netbacks to analyze financial and operating performance. Management feels that these key performance indicators

and benchmarks are key measures of profitability for Madalena and provide investors with information that is commonly used by other oil and gas companies. These key performance indicators and benchmarks as presented do not have any

standardized meaning prescribed by Canadian generally accepted accounting principles and therefore may not be comparable with the calculation of similar measures for other entities. For additional information on the use of these measures please see

Madalena's Management’s Discussion and Analysis at www.sedar.com.

Finding and Development Costs

NI 51-101 specifies how finding and development costs ("F&D costs") should be calculated if they are reported. Essentially NI 51-101 requires that the exploration and

development costs incurred in the year along with the change in estimated Future Development Costs (“FDC”) be aggregated and then divided by the applicable reserve additions. The calculation specifically excludes the effects of acquisitions and

dispositions on both reserves and costs. Since acquisitions can have a significant impact on annual reserve replacement costs, excluding these amounts could result in an inaccurate portrayal of Madalena's cost structure. F&D costs disclosed herein are

based on working interest gross reserves. The aggregate of the exploration and development costs incurred in the most recent financial year and the change during that year in estimated FDC generally will not reflect total F&D costs related to reserve

additions for that year.

Information Regarding Disclosure on Reserves and Resources

The reserve and resource estimates contained herein are estimates only and there is no guarantee that the estimated reserves or resources will be recovered. In relation to the disclosure of estimates for individual properties, companies or business

units, as adjusted, such estimates may not reflect the same confidence level as estimates of reserves or resources and future net revenue for all properties, due to the effects of aggregation.

The estimates of reserves and future net revenue from individual properties or wells may not reflect the same confidence level as estimates of reserves and future net revenue for all properties and wells, due to the effects of aggregation. Where

discussed herein "NPV 10%" represents the net present value (net of capex) of net income discounted at 10%, with net income reflecting the indicated oil, liquids and natural gas prices and IP rate, less internal estimates of operating costs and royalties. It

should not be assumed that the future net revenues estimated by Madalena's independent resource evaluators represent the fair market value of the reserves, nor should it be assumed that Madalena's internally estimated value of its undeveloped land

holdings or any estimates referred to herein from third parties represent the fair market value of the lands.

Drilling Locations

This press release refers to unbooked drilling locations. Unbooked locations are internal estimates based on Madalena's prospective acreage and an assumption as to the number of wells that can be drilled per section based on industry practice and

internal review. Unbooked locations do not have attributed reserves. Unbooked locations have been identified by management as an estimation of our future drilling activities based on evaluation of applicable geologic, seismic, engineering, production

and reserves information. There is no certainty that Madalena will drill all unbooked drilling locations and if drilled there is no certainty that such locations will result in additional oil and gas reserves or production. The drilling locations on which we

actually drill wells will ultimately depend upon the availability of capital, regulatory approvals, access restrictions, oil and natural gas prices, costs, actual drilling results, additional reservoir information that is obtained and other factors. While certain of

the unbooked drilling locations have been derisked by drilling existing wells in relative close proximity to such unbooked drilling locations, some of other unbooked drilling locations are farther away from existing wells where management has less

information about the characteristics of the reservoir and therefore there is more uncertainty whether wells will be drilled in such locations and if drilled there is more uncertainty that such wells will result in additional oil and gas reserves or production.