macroeconomic analysis series bi board of governor meeting

TRANSCRIPT

MACROECONOMIC ANALYSIS SERIES

BI Board of Governor Meeting December 2019

Macroeconomic & Financial Sector Policy Research Febrio N. Kacaribu, Ph.D. (Head of Research) [email protected]

Syahda Sabrina [email protected]

Nauli A. Desdiani [email protected]

Teuku Riefky [email protected]

Highlights • BI should keep its

policy rates at 5.00% this month.

• Inflation is subdued and stable. Rupiah is stable; partially helped by better CAD in short run.

• BI needs to maintain its macroprudential measures to maintain liquidity for 2020.

he latest picture of inflation confirms that 2019 inflation will remain low. We also see that the 2020 inflation to be within BI’s lower goal of 3.0±1%, given the signs towards no-

significant change in 2020 demand. BI has started its accommodative stance in July 2019 and has cut its policy rates four times. The easing trend needs to take a break for now since BI would like to accumulate more international reserves amid the short-term consolidation in the global financial market. Liquidity in the banking system has increased slightly. However, the business activities have not fully responding as production has not picked up. We could see a slight increase in the credit growth starting from 2020Q3.

On the external side, the reduced easing stance by central banks due to the robust US’s economic figures has caused a slight capital outflow from the emerging countries. Rupiah is still kept stable by BI, maintaining a 3.3% (ytd) appreciation rate by the middle of December. A slight improvement in the picture of trade balance has eased the pressure on CAD for now. It is appropriate for Bank Indonesia to maintain the rate differential for now and attracting more capital inflow and increased liquidity in the banking system. The probability of the crises in the US has somewhat decreased but still at around 30%. We view that Bank Indonesia needs to keep the policy rate until the end of this year while maintaining the liquidity in the banking system.

Subdued Inflation to Follow Weakening Demand

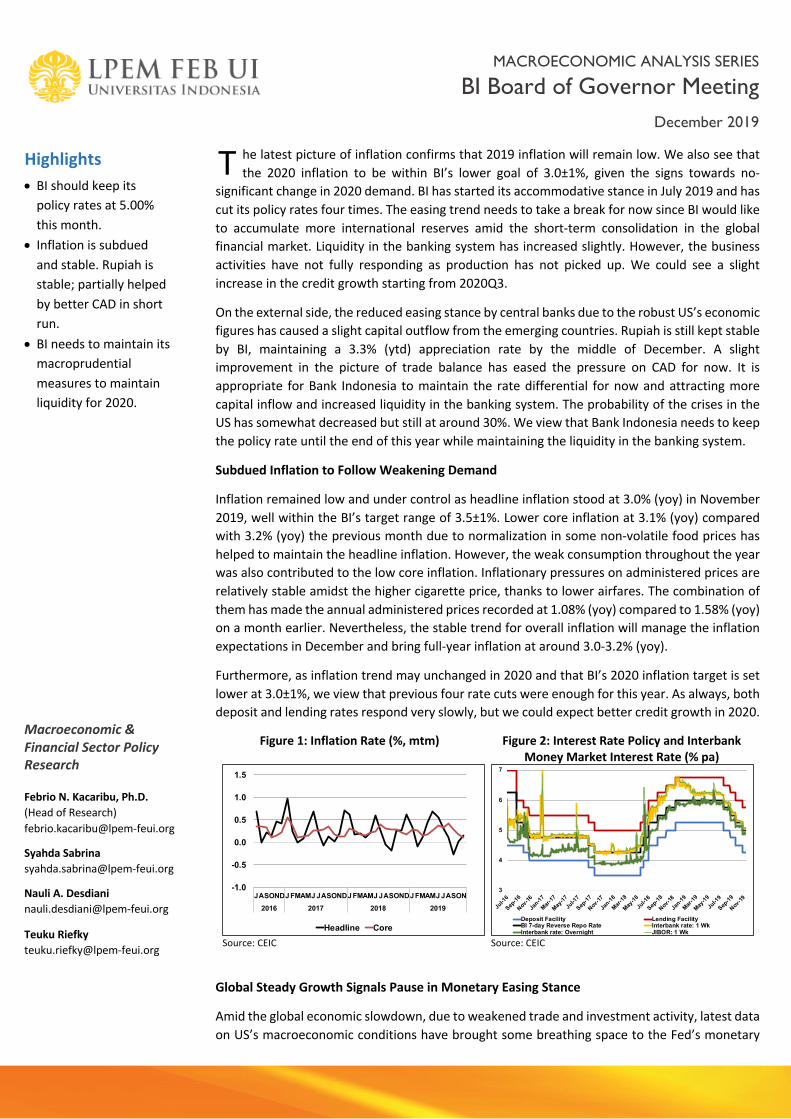

Inflation remained low and under control as headline inflation stood at 3.0% (yoy) in November 2019, well within the BI’s target range of 3.5±1%. Lower core inflation at 3.1% (yoy) compared with 3.2% (yoy) the previous month due to normalization in some non-volatile food prices has helped to maintain the headline inflation. However, the weak consumption throughout the year was also contributed to the low core inflation. Inflationary pressures on administered prices are relatively stable amidst the higher cigarette price, thanks to lower airfares. The combination of them has made the annual administered prices recorded at 1.08% (yoy) compared to 1.58% (yoy) on a month earlier. Nevertheless, the stable trend for overall inflation will manage the inflation expectations in December and bring full-year inflation at around 3.0-3.2% (yoy).

Furthermore, as inflation trend may unchanged in 2020 and that BI’s 2020 inflation target is set lower at 3.0±1%, we view that previous four rate cuts were enough for this year. As always, both deposit and lending rates respond very slowly, but we could expect better credit growth in 2020.

Figure 1: Inflation Rate (%, mtm)

Source: CEIC

Figure 2: Interest Rate Policy and Interbank Money Market Interest Rate (% pa)

Source: CEIC

Global Steady Growth Signals Pause in Monetary Easing Stance

Amid the global economic slowdown, due to weakened trade and investment activity, latest data on US’s macroeconomic conditions have brought some breathing space to the Fed’s monetary

-1.0

-0.5

0.0

0.5

1.0

1.5

JASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASON2016 2017 2018 2019

Headline Core

3

4

5

6

7

Jul-1

6

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-1

7

Sep-17

Nov-17

Jan-18

Mar-18

May-18

Jul-1

8

Sep-18

Nov-18

Jan-19

Mar-19

May-19

Jul-1

9

Sep-19

Nov-19

Deposit Facility Lending FacilityBI 7-day Reverse Repo Rate Interbank rate: 1 WkInterbank rate: Overnight JIBOR: 1 Wk

T

MACROECONOMIC ANALYSIS SERIES

BI Board of Governor Meeting December 2019

Key Figures • BI Repo Rate (7-day, Nov ‘19)

5.00% • GDP Growth (y.o.y, Q3 ‘19)

5.02% • Inflation (y.o.y, Nov ‘19)

3.00% • Core Inflation (y.o.y, Nov ‘19)

3.08% • Inflation (mtm, Nov ‘19)

0.14%% • Core Inflation (mtm, Nov ‘19)

0.11% • FX Reserve (Nov ‘19)

USD126.6 billion

To keep you updated with our monthly and quarterly reports, please subscribe. Scan the QR code below

or go to http://bit.ly/LPEMCommentarySubscription

easing stance. The Fed has been making it clear on pausing their easing stance by leaving rates steady. More robust consumer spending, strong labor market, and the agreement between US-China on phase one deal are among the good news. Meanwhile, ECB also decided to keep the reference rates unchanged, remain at 0%. RBI also announced the unchanged rates as they are considering inflationary pressure and the transmission lag between rate cuts and loanable funds to the economy. Bank Indonesia has also kept its policy rates at 5.00% last month, having already cut it fourth times by a total of 100 bps this year as the pre-emptive move to push economic growth momentum in the future.

Figure 3: IDR/USD and Accumulated Portfolio Capital Inflow (Since Jan-2018)

Source: CEIC

Figure 4: Government Bonds Yield (% pa)

Source: CEIC

The reduced easing stance by central banks in advanced economies has caused a slight capital outflow from the emerging countries. Indonesia enjoyed lower total accumulated capital inflow at USD12.5 billion by mid-December from USD12.7 billion a month earlier. The slight net capital outflow is also reflected in the higher yields of 10-year and 1-year government bonds to 7.3% and 5.5% in December (Figure 4).

However, Rupiah is kept stable and even appreciated at 3.3% (ytd) against the dollar in the middle of December. The better picture of the trade balance data in the short run has eased pressure on the CAD, thus, lessen the risk for Rupiah. The positive impact of trade surplus into Rupiah is also confirmed by the stable figure for the foreign exchange reserves that is recorded at USD126.6 billion in November (Figure 5).

Figure 5: IDR/USD and Official Reserve Assets

Source: CEIC

Figure 6: NFA, Bank IDR Deposit, and Credit (changes year-over-year)

Source: CEIC

Financial Market Deepening Desperately Needed

Despite the robust economic picture in the US and the reduced easing stance by central banks, Bank Indonesia needs to be always vigilant and maintains the yield differential for now. To ensure

13,000

13,500

14,000

14,500

15,000

15,500

-4

-2

0

2

4

6

8

10

12

14

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-1

8Ju

l-18

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

May-19

Jun-1

9Ju

l-19

Aug-19

Sep-19

Oct-19

Nov-19

Dec-19

USD billion

Total Portfolio IDR/USD (RHS)

7.3

5.5

4

5

6

7

8

9

Apr-17

Jun-17

Aug-17Oct-

17

Dec-17

Feb-18

Apr-18

Jun-18

Aug-18Oct-

18

Dec-18

Feb-19

Apr-19

Jun-19

Aug-19Oct-

19

Dec-19

10 Year 1 Year

126.6

14,069

12,000

13,000

14,000

15,000

16,000

100

110

120

130

140

Nov-17 Mar-18 Jul-18 Nov-18 Mar-19 Jul-19 Nov-19

IDR/USDUSD Billion

Official Reserve Assets IDR/USD

-

100

200

300

400

500

600

700

-200

-150

-100

-50

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

IDR trillionIDR trillion

IDR deposit - LHS NFA - LHS Credit - RHS

MACROECONOMIC ANALYSIS SERIES

BI Board of Governor Meeting December 2019

Key Figures • BI Repo Rate (7-day, Nov ‘19)

5.00% • GDP Growth (y.o.y, Q3 ‘19)

5.02% • Inflation (y.o.y, Nov ‘19)

3.00% • Core Inflation (y.o.y, Nov ‘19)

3.08% • Inflation (mtm, Nov ‘19)

0.14%% • Core Inflation (mtm, Nov ‘19)

0.11% • FX Reserve (Nov ‘19)

USD126.6 billion

To keep you updated with our monthly and quarterly reports, please subscribe. Scan the QR code below

or go to http://bit.ly/LPEMCommentarySubscription

that the extra NFA accumulated in 2019 translate into better credit performance in 2020, BI needs the macroprudential measures as the channels in prompting liquidity.

Since 2010, liquidity in the banking system is very dependent upon the NFA. Figure 6 shows that the surplus of foreign funds is always transformed into IDR deposits in banks after some lags in credit creation by the banking system. Whenever possible, BI has always pursued a rather stable exchange rate. In this setting, capital inflow means higher international reserves and vice versa. It also means that BI sterilizes the capital flows, hence the reserves in the banking system is sensitive towards NFA. By extension, this is also true for credit and deposit.

The additional IDR monetary base allows banks to increase their loans. But, the transmission between foreign funds to bank loans in Indonesia is driven by several considerations. Typically, additional foreign inflow takes at least a couple of quarters to show impact. It is confirmed by the lower credit growth in 2019 amidst the fourth times’ rate cuts. The credit growth for FY 2019 is now projected at 8%. The sluggish demand from businesses as reflected from the significant drop in working capital loan growth (Figure 7) contributes to the meagre performance of credit growth in 2019. Wholesale and retail sectors as the most significant contributor to productive loans, show a drop in their growth from 9% in 2018 to around 4% in Q3-2019. Overall, the bank loan slowed down significantly as a result of tight liquidity in 2018 and the monetary policy easing in 2019 will materialize in terms of higher credit growth in 2020.

BI has put efforts in boosting liquidity, starting from lowering the reserve requirement by 50 bps to 5.5% that will be effective early next year, loosened LTV for property and motor vehicle FTV until the invention of RIM as the extension measurement of LDR. These attempts are expected to stimulate bank lending and boost the economy next year. Considering the weak domestic case to cut rates and relatively manageable external condition, we view that Bank Indonesia needs to keep the policy rate until the end of this year while maintaining the liquidity.

Figure 7: Credit Growth (% yoy)

Source: CEIC

Figure 8: Bank Liquidity Performance (%)

Source: BI, OJK, CEIC

Indonesian financial market still desperately waits for a significant reform in the non-bank segments. Corporate bond is still underdeveloped and illiquid, standing at around IDR440 trillion (about 10% of government bonds). At this level, the growth rate of corporate bonds merely depends on the spillover from government bonds market when there is a capital inflow. Much reform needs to be done from the regulatory aspects and the incentive mechanism for the non-bank sectors of the financial market to emerge and give a meaningful additional liquidity for the financing of economic activities in Indonesia and bringing about more stability as well. KSSK needs to be more purposeful in pushing the financial deepening agenda.

5.94

12.84

6.82

3579

111315

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018 2019Working Capital InvestmentsConsumption Total

91.0

94.3

2

4

6

8

10

12

82

86

90

94

98

102

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19

Macroprudential Intermediation Ratio (RIM) - LHSLoan to Deposit Ratio (LDR) - LHSStatutory Reserve Requirement (GWM) - RHS