macquarie capital · macquariecapital page 1 this presentation has been prepared by macquarie...

TRANSCRIPT

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

2016 capital markets insights and 2017 outlook

January 2017

Macquarie Capital

PAGE 1STRICTLY CONFIDENTIAL MacquarieCapital

This presentation has been prepared by Macquarie Capital (Australia) Limited ABN 79 123 199 548 (“Macquarie”) for the sole purpose of providing an overview of the Australian equity and debt markets in 2016, and an outlook for 2017. (“Purpose”). It is provided on a confidential basis, and may not be reproduced in whole or in part, nor may any of its contents be disclosed to any other person, without Macquarie’s prior written consent.

This presentation is provided by Macquarie for general information purposes only, without taking into account any potential investors’ personal objectives, financial situation or needs. It should not be relied upon by the recipient in considering the merits of any particular transaction. It is not an offer to buy or sell, or a solicitation to invest in or refrain from investing in, any securities or other investment product. Nothing in this presentation constitutes investment, legal, tax, accounting or other advice. The recipient should consider its own financial situation, objectives and needs, and conduct its own independent investigation and assessment of the contents of this presentation, including obtaining investment, legal, tax, accounting and such other advice as it considers necessary or appropriate.

This presentation has been prepared on the basis of publicly available information. Macquarie has relied upon and assumed, without independent verification, the accuracy and completeness of all such information. It contains selected information and does not purport to be all-inclusive or to contain all of the information that may be relevant to the Purpose. The recipient acknowledges that circumstances may change and that this presentation may become outdated as a result. Macquarie is under no obligation to update or correct this presentation.

Macquarie, its related bodies corporate and other affiliates, and their respective directors, employees, consultants and agents (“Macquarie Group”) make no representation or warranty as to the accuracy, completeness, timeliness or reliability of the contents of this presentation. To the maximum extent permitted by law, no member of the Macquarie Group accepts any liability (including, without limitation, any liability arising from fault or negligence on the part of any of them) for any loss whatsoever arising from the use of this presentation or its contents or otherwise arising in connection with it. This presentation may contain forward-looking statements, forecasts, estimates and projections (“Forward Statements”). No independent third party has reviewed the reasonableness of any such statements or assumptions. No member of the Macquarie Group represents or warrants that such Forward Statements will be achieved or will prove to be correct. Actual future results and operations could vary materially from the Forward Statements. Similarly, no representation or warranty is made that the assumptions on which the Forward Statements are based may be reasonable. No audit, review or verification has been undertaken by the Macquarie Group or an independent third party of the assumptions, data, results, calculations and forecasts presented or referred to in this presentation.

The recipient acknowledges that neither it nor Macquarie intends that Macquarie act or be responsible as a fiduciary to the recipient, its management, stockholders, creditors or any other person. Each of the recipient and Macquarie, by accepting and providing this presentation respectively, expressly disclaims any fiduciary relationship and agrees that the recipient is responsible for making its own independent judgments with respect to any transaction and any other matters regarding this presentation.

The Macquarie Group may have interests in the securities and other investment products referred to in the presentation, including being directors of, or may have or may in the future act in various roles including as underwriter, dealer, broker, lender or financial advisor to their issuers and may receive fees, brokerage or commission for acting in those capacities. A list of these roles is available on the Macquarie Group’s website at http://www.macquarie.com.au/macsec/equitiesresearch/InstitutionalHomeServlet?nav=disclosure_disc. Further, the Macquarie Group may act as a market maker or buy or sell those securities and other investment products as principal or agent and as such may effect transactions which are not consistent with this information.

None of the entities noted in this presentation are an authorised deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542. Macquarie Bank Limited does not guarantee or otherwise provide assurance in respect of the obligations of these entities.

© Macquarie Group 2017

Important notice and disclaimer

01 Insert divider title 3

A Insert divider title 7

Contents

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

01 2016 equity and debt market performance 4

02 2016 equity and debt issuance review 8

03 2017 equity and debt market outlook 18

A Macquarie capabilities and contact details 21

PAGE 3STRICTLY CONFIDENTIAL MacquarieCapital

Markets pricing in stronger growth outlook

2016 equity and debt market performance

02 0301 Despite a series of tumultuous events, equity

markets closed 2016 at intra-year highsas volatility abated

A backdrop of renewed exuberance around equities emerged thanks to stronger US growth expectations, the prospect of a continuation of relatively low benchmark rates and higher than expectedcommodity prices

Historically low interest rates drove investors to search for yield in other asset classes. Over the course of 2016 credit spreads tightened

2016 equity and debt issuance

A total of $33 billion was raised in equity in 2016 (compared to $64 billion in 2015). Despite political events, the IPO market and secondary issuance market remained active. Secondary issuance was dominated byM&A funding

Debt market issuance was down over the course of 2016 in Australia as lower refinancing volumes and reduced M&A activity affected the market. The sources of funding continued to move away from Australian to Asian lenders and from bank loans to bond markets more generally

Looking ahead to 2017

The domestic economic outlook for 2017 is shaping up to be a tale of two halves with the second half expected to deliver better real growth, driven by stronger private and public investment, increasing export volumes and growth-conducive monetary policy

Macquarie Research forecasts a modest increase of 3.7% in the ASX 200 from December 2016 to December 2017 and expects the equity market to trade above‘fair value’ (~16-18x) as risk-taking behaviour remains supportive for equities over bonds against an outlook for positive earnings momentum (~10% EPS growth)and a broader economic recovery

2016 in retrospect and the outlook for 2017Macquarie Capital Markets team

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

2016 equity and debt market performance

01

PAGE 5STRICTLY CONFIDENTIAL MacquarieCapital

Despite a series of tumultuous events, markets closed 2016 at year highs as volatility subsided

Source: IRESS and FactSet as at 31 December 2016.

…with volatility trending lower despite tumultuous events

The year was marked by a number of significant macro eventsASX 200 at yearly highs and S&P 500 at all time highs…

Australian market driven by macro events

— Weak growth and declining oil prices led to global volatility and weak share price performance at the start of 2016

— Market weakness saw the ASX 200 reach lows in early February 2016

— US expectations of a slower pace of rate hikes spurred a relief rally

— Brexit shocked the markets leading to a spike in volatility and flight to safety

— Fed rate uncertainty pushed volatility higher

— The US Presidential election caused volatility to spike once more, however dropped sharply following Trump’s victory

— Renewed optimism around equities has emerged against a backdrop of stronger US growth expectations, the expectation of a continuation of relatively low benchmark rates and higher than expected commodity prices

85

95

105

115

Jan 16 Mar 16 May 16 Jul 16 Sep 16 Nov 16 Jan 17

Per

form

ance

(reb

ased

to 1

00)

S&P ASX 200 S&P 500

6

14

22

30

Jan 16 Mar 16 May 16 Jul 16 Sep 16 Nov 16 Jan 17

VIX

CBOE Market Volatility Index

+7.0%+9.5%

(22.9)%

21

3

6

5

4

7

1 2

3 45 6

7

7

6

5

4

3

2

1

PAGE 6STRICTLY CONFIDENTIAL MacquarieCapital

(6%)

1%

4%

5%

6%

6%

13%

15%

15%

17%

21%

24%

Financials

Cons. Staples

Telcos

Media

S&P/ASX 200

Energy

Cons. Disc.

Healthcare

Industrials

Utilities

A-REITS

Materials

8%

(0%)

(16%)

(12%)

1%

7%

(4%)

(13%)

(7%)

(3%)

(10%)

12%

60

70

80

90

100

110

120

Jan 16 Mar 16 May 16 Jul 16 Sep 16 Nov 16 Jan 17

Per

form

ance

(reb

ased

to 1

00)

ASX 200 Real Estate ASX 200 Utilities ASX 200 Telcos Aus 10 yr bond yield

Source: IRESS and FactSet as at 31 December 2016.

Defensive sectors underperformed post August as investors rotated into commodity/growth correlated sectors

Rotation from defensives to cyclicals

January to July characterised by a continuation of the yield trade, but as bond yields rose investors rotated to growth stocks

Pre 1 Aug 16 Post 1 Aug 161 August

Marked shift from defensive exposures to cyclical stocks against a backdrop of rising bond yields

2.8%2.8%

- 94 bps + 96 bps

1.8%

A$ 10yr bond yields

PAGE 7STRICTLY CONFIDENTIAL MacquarieCapital

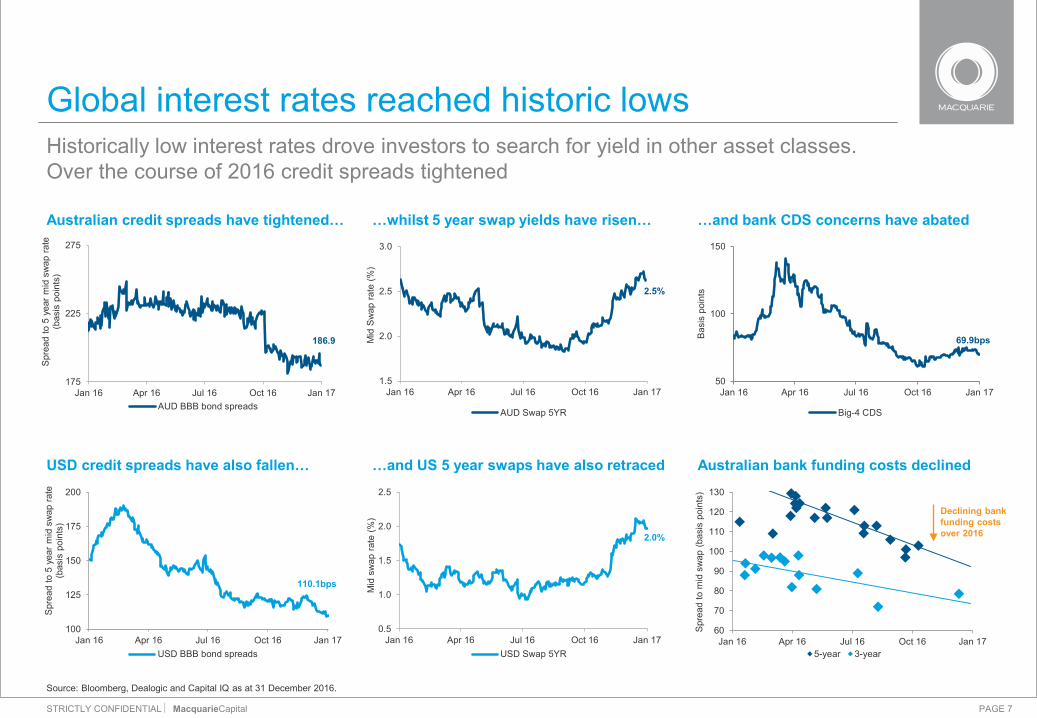

Historically low interest rates drove investors to search for yield in other asset classes.Over the course of 2016 credit spreads tightened

Source: Bloomberg, Dealogic and Capital IQ as at 31 December 2016.

186.9

175

225

275

Jan 16 Apr 16 Jul 16 Oct 16 Jan 17

Spr

ead

to 5

yea

r m

id s

wap

rate

(b

asis

poi

nts)

AUD BBB bond spreads

…whilst 5 year swap yields have risen… …and bank CDS concerns have abated

69.9bps

50

100

150

Jan 16 Apr 16 Jul 16 Oct 16 Jan 17

Bas

is p

oint

s

Big-4 CDS

USD credit spreads have also fallen…

110.1bps

100

125

150

175

200

Jan 16 Apr 16 Jul 16 Oct 16 Jan 17

Spr

ead

to 5

yea

r m

id s

wap

rate

(b

asis

poi

nts)

USD BBB bond spreads

…and US 5 year swaps have also retraced

2.0%

0.5

1.0

1.5

2.0

2.5

Jan 16 Apr 16 Jul 16 Oct 16 Jan 17

Mid

sw

ap ra

te (%

)

USD Swap 5YR

Australian credit spreads have tightened…

Australian bank funding costs declined

60

70

80

90

100

110

120

130

Jan 16 Apr 16 Jul 16 Oct 16 Jan 17

Spr

ead

to m

id s

wap

(bas

is p

oint

s)

5-year 3-year

Global interest rates reached historic lows

2.5%

1.5

2.0

2.5

3.0

Jan 16 Apr 16 Jul 16 Oct 16 Jan 17

Mid

Sw

ap ra

te (%

)

AUD Swap 5YR

Declining bank funding costs over 2016

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

2016 equity and debt issuance review

02

PAGE 9STRICTLY CONFIDENTIAL MacquarieCapital

During 2016 there was a marked reduction in secondary issuance due to an absence of bank recapitalisations seen in 2015

Source: Dealogic as at 31 December 2016. Note 1: All ECM issuance. 2: Follow-on ECM transactions >A$50m.

…with secondary issuance in 2016 dominated by M&A funding2…

…and a marked reduction in large recapitalisations compared to 20152

A total of $33 billion was raised in equity in 20161…

2016 saw ECM volumes moderate

$19.7bn

$30.8bn

$48.0bn

$63.5bn

$33.0bn

-

10

20

30

40

50

60

70

2012 2013 2014 2015 2016

Equ

ity ra

ised

($A

bn)

IPO Block Secondary DRP/SPP Hybrid

$2.7bn$4.5bn

$8.5bn $7.4bn $8.1bn

$8.1bn $8.0bn

$12.6bn

$33.7bn

$13.2bn

-

5

10

15

20

25

30

35

40

2012 2013 2014 2015 2016

Equ

ity ra

ised

($A

bn)

M&A Balance sheet repair Growth

$8.1bn $8.0bn

$12.6bn

$33.7bn

$13.2bn

-

5

10

15

20

25

30

35

40

2012 2013 2014 2015 2016

Equ

ity ra

ised

($A

bn)

Resources Consumer InfrastructureIndustrials Real Estate TechnologyHealthcare Financials

IPO volumes remain robust

PAGE 10STRICTLY CONFIDENTIAL MacquarieCapital

(20)

(15)

(10)

(5)

(0)

0 10 20 30 40 50 60 70 80

Dis

coun

t (%

)

Offer size (% mkt cap)

2016 saw more companies raise capital to fund M&A with a clear trend observable between offer size and discount achieved

Source: Dealogic and company announcements as at 31 December 2016. Note 1: M&A raisings over A$50m. 2: Discount to TERP for rights issues, discount to close for placements. Placements includes Placement with SPP offer structures. Non-renounceable includes Placement with non-renounceable offer structures. Renounceable includes Placement with renounceable offer structures. Excludes deals with an offer size greater than market capitalisation. 3: M&A raisings over A$150m. 4: Entitlement offer. 5: Placement to CPPIB at 2.9% discount to TERP.

M&A raisings dominated activity in 20163

Discounts remained tight for M&A linked equity issuance1,2

Clear correlation between raising discount and offer size1,2

M&A funding featured strongly4.

4%

3.5% 5.

1%

2.1%

\

3.4%

15.5

%

5.9%

11.4

%

5.8%

9.4%

16.3

%

13.3

%

11.5

%

11.5

%

14.8

%

-

5

10

15

20

2012 2013 2014 2015 2016

Dis

coun

t (%

)

Placement average 3.7%

Non-renounceable average 9.6%

Renounceable average 13.5%

Issuer Target Date Size ($m) Structure Discount (%)2

Headwaters Nov-16 2,058 Placement & EO4 (15.1)

Harris CapRock Nov-16 294 Entitlement offer (13.8)

Adshel Oct-16 273 Placement & EO4 (20.1)

The Good Guys Sep-16 394 Entitlement offer (8.1)

Hellaby Sep-16 181 Placement & SPP (5.0)

Ernest Henry Aug-16 404 Entitlement offer (13.4)

Generic product portfolio

Jun-16 888 Placement & EO4 (9.2)

Nextgen Jun-16 652 Placement & EO4 (10.4)

Southern Cross portfolio

Jun-16 260 Placement & EO4 (6.0)

Asciano Mar-16 800 Placement & EO4 (7.0)5

DBP Mar-16 246 Placement & SPP (3.5)

Placement

Non-renounceable rights issues

Renounceable rights issues

APN

MaynePharma

PAGE 11STRICTLY CONFIDENTIAL MacquarieCapital

$5.3bn

$3.8bn $4.0bn

$6.6bn$7.1bn

$12.7bn

$6.4bn

-

1

2

3

4

5

6

-

3

6

9

12

15

18

2010 2011 2012 2013 2014 2015 2016

Ave

rage

dis

coun

t to

last

clo

se (%

)

Blo

ck v

olum

e ($

bn)

Block volume ($bn) (LHS) Average block discount (%) (RHS)

Block trades continue to account for a large portion of ECM activity, although investors experienced mixed returns post selldown

Source: Dealogic and IRESS as at 31 December 2016. Note 1: 2016 blocks above A$125m. 2: Return on offer price as at 31 December 2016.

Block activity was dominated by non-sponsor selldowns1Block trades continue to be executed at tight discounts

Block selldowns experienced mixed results

#

15

3233

39

39

16 23

Date Issuer VendorValue ($m)

Discount (%)

Return (%)2

PE vendor

Dec-16 Archer Daniels Midland 387 (2.1) 12.1

Nov-16 IPH Partners 150 (1.0) 2.4

Sep-16 Gandel Group 396 (7.1) (5.2)

Sep-16 PEP, ICG 872 0.0 (9.7)

Sep-16 Atlas Roads Macquarie Group 282 (4.1) (5.1)

Aug-16 The Carlyle Group 350 0.0 (4.3)

Aug-16 Consolidated Press 448 (5.3) (9.5)

Aug-16 ADIA 254 (1.3) (12.2)

Jun-16 Cheung Kong 252 (3.5) 6.7

Jun-16 NZ Super 292 (2.2) (9.4)

May-16 Spark Infrastructure 306 (5.1) 21.8

Apr-16 PEP, ICG, Macquarie 392 0.5 1.5

Mar-16 Macquarie 130 (8.5) 43.1

Mar-16 Newmont Mining 244 (4.2) 18.3

PAGE 12STRICTLY CONFIDENTIAL MacquarieCapital

4.6

1.5

3.1

8.6

9.7

16.0

8.4

9.8

1.8

2.8

8.2

1.3 1.1

6.7

17.1

8.5

6.8

10.0

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

-

2

4

6

8

10

12

14

16

18

20

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

AS

X 20

0

AS

X IP

O is

suan

ce ($

bn)

QR National

MedibankPrivate

Goodman FielderSpark Infrastructure

SP AusNet

Company Listed Size ($Am) %Δ since listing3 Main Vendor

BRAVURA Nov-16 148 (4.1%) Private Equity

AUTSPORT Nov-16 160 4.6% Founders

ELANOR Nov-16 109 -% Corporate

CHARTER HALL Nov-16 827 0.2% Corporate

INGAHMS Nov-16 596 1.3% Private Equity

ANTOPED Oct-16 313 -% LIC4

QANTM Aug-16 147 (4.1%) Corporate

PROERTYL Aug-16 504 (12.4%) Corporate

VIVA Aug-16 911 9.1% Corporate

SCOT PAC Jul-16 294 (17.2%) Private Equity

AUS UNIT Jun-16 152 0.5% Corporate

GTN Jun-16 188 43.2% Private Equity

May-16 394 4.5% LIC4

TEGEL May-16 NZ299 (6.5%) Private Equity

RWC Apr-16 919 28.0% Founders

WISTECH Apr-16 168 68.7% Founders

Source: Factset, Dealogic and press releases as at 31 December 2016. Note 1: IPOs > A$20m (excludes dual listings). 2: IPOs > $100m in 2016. 3: From listing date to 31 December 2016. 4: Listed investment company.

IPO window remains open for high quality companies1

IPO volumes remained robust Despite political events in 2016, demand for high quality IPOs remained strong, although several deals struggled towards year end resulting in repricing/restructuring or deferrals

IPO

pip

elin

e

IPO window open305 deals, $39bn raised

IPO window open848 deals, $53bn raised

Performance of IPOs during the year was mixed2

PAGE 13STRICTLY CONFIDENTIAL MacquarieCapital

Company Announced Capital returned ($m) Mechanism

AGL Sep-16 596 On-market buy-back

IAG Aug-16 314 Off-market buy-back

INTERP Aug-16 24 Capital return

QANTAS Aug-16 366 On-market buy-back

JAMES HAR Aug-16 1002 On-market buy-back

TELSRTA Aug-16 1,500 On and off-market buy-back

GENW Aug-16 67 Special dividend

SGH Mar-16 71 On-market buy-back

QANT Feb-16 500 On-market buy-back

CALTE Feb-16 270 Off-market buy-back

IAG Feb-16 243 Special dividend

NAVIT Feb-16 135 On-market buy-back

OZMINER Feb-16 60 On-market buy-back

Sources: Dealogic, ASX announcements, annual reports, IRESS, Bloomberg and company announcements as at 31 December 2016. Note 1: Announced capital management initiatives excluding $1.6bn RIO Plc buy-back announced Feb-2015. 2: USD.

Capital management remained strong in 20161 EPS accretion benefits of on-market buy-backs a feature in 2016

Capital management continues to feature

$4.0bn

$17.9bn

$11.1bn

$6.4bn$5.9bn

$7.0bn $7.3bn

-

4

8

12

16

20

2010 2011 2012 2013 2014 2015 2016

Vol

ume

(A$b

n)

Off-market buybacks On-market buybacks Special dividends Capital returns

Many large companies focused on capital management initiatives to enhance shareholder returns against the low growth backdrop

PAGE 14STRICTLY CONFIDENTIAL MacquarieCapital

Despite an increase in the average discount offered in 2H16, DRP participation rates have declined compared to prior years

Source: IRESS as at 31 December 2016 for ASX 200 companies. Note 1: When discount provided. 2: Excludes participation rates > 50% (GOZ). 3: DRP discounts in 2016.

23.2%24.1%

21.9%21.4%

18.8%19.3%

1.5

2.5

3.5

15

20

25

CY1H14 CY2H14 CY1H15 CY2H15 CY1H16 CY2H16

Ave

rage

dis

coun

t1(%

)

Ave

rage

par

ticip

atio

n (%

)

Average participation Average discount

…with 30% of companies neutralising DRPs to avoid dilution

-

2

4

6

8

-

20

40

60

80

CY1H14 CY2H14 CY1H15 CY2H15 CY1H16 CY2H16

Und

erw

ritte

n D

RP

s (#

)

Act

ive

and

neut

ralis

ed D

RP

s (#

)

Active DRPs (LHS) Neutralised DRPs (LHS) Underwritten DRPs (RHS)

Substantial participation observed at 1.5% and 2.0% discounts2… …however majority of DRPs offered with no discount3

69%

4%

10%

7%

7% 3%

0.0%

1.0%

1.5%

2.0%

2.5%

5.0%

Average participation consistent over 2016…

DRP participation rates have declined

-

10

20

30

40

50

- 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

DR

P p

artc

ipat

ion

rate

(%)

Discount (%)Participation rate at given discount Average participation rateAverage participation rate at given discount

PAGE 15STRICTLY CONFIDENTIAL MacquarieCapital

1.2%

1.4%

1.5%

3.4%

3.6%

3.8%

3.0%

2.2%

3.0%

4.3%

4.1%

2.3%

1.4%

1.7%

2.0%

2.8%

2.8%

2.9%

2.9%

3.0%

3.5%

3.7%

4.3%

4.7%

- 1 2 3 4 5

Real Estate

Utilities

Financials

Industrials

Energy

Materials

ASX 200

Health Care

Telcoms

Cons. Disc.

Cons. Staples

IT

Average short position (%)1

Shorting levels for resource and consumer correlated sectors fell in 2016, with investors instead increasing shorts on IT and healthcare names

Source: ASIC short positions as at 31 December 2016. Note 1: Reported as percentage of total product in issue reported as short positions.

…from resources and consumer to IT and health care2016 saw a significant shift in shorted sectors…

Shift in short positions

Short position at beginning of 2016 Short position at conclusion of 2016

2.4

0.2

(0.6)

0.5

0.8

(0.1)

(0.9)

(0.8)

(0.6)

0.5

0.3

0.2

Resource and consumer namesIT and health care names

Largest changes in shorting levels in key sectors

Shorting levels (%)1

Start of 2016 End of 2016 Change

IT0.9% 16.1% 15.2

0.1% 7.8% 7.7

Health care1.4% 8.3% 6.9

2.0% 8.3% 6.3

Consumer Discretionary

19.9% 4.1% (15.8)

12.9% 4.6% (8.3)

Materials13.2% 1.5% (11.7)

14.8% 5.5% (9.3)

Energy9.2% 2.3% (6.9)

9.7% 5.6% (4.1)

PAGE 16STRICTLY CONFIDENTIAL MacquarieCapital

Issuer Type Pricing date Rating Volume (A$m) Tenor (yrs) Margin to Mid-swapBank loan Nov-16 NR 1,725 5 – 7 200 – 225

Bank loan Oct-16 NR 13,000 Various 100 – 175

Bank loan Apr-16 BBB-/Baa3

4,000 3, 5 135, 165

Bank loan Mar-16 BBB/Baa2

1,200 3, 5.5 130, 160

AMTN1 Oct-16 A-/A3 200 10 167

AMTN1 Sep-16 BBB-/Baa3

425 7, 10 258, 280

EMTN2 Sep-16 BBB /Baa1

US550 10.5 227

EMTN2 Apr-16 A/A2 EUR750 10 76

EMTN2 Mar-16 A+/A1 EUR500 7 210

S144a Sep-16 BBB+/Baa1

US600 10 236

S144a Sep-16 A-/Baa1 US800 10 258

S144a Apr-16 BBB/Baa2

US900 10 215

USPP3Oct-16 BBB/NR ~774 US$:10/12/15

A$: 10/15/18 US$: 228/ 230/ 235A$: 223/ 242/ 252

USPP3 Jul-16 A- US500 US$: 10, 12 A$: 10, 15

US$: UST + 125, ~135 A$: Ms + 178,186

USPP3Jul-16 Baa2 756 10, 12.5, 15, 17 160, 170, 185,

ICUR+175

USPP3Mar-16 NR US300 10 ~260

Source: Dealogic and Loanconnector. Note 1: Australian medium term notes. 2: European medium term notes. 3: US private placement

2016 DCM transactions by Australian borrowersBond issuances in Australasia below historical averages

Debt volume affected by market conditionsReduced loan and bond volume has created competition for high quality assets

Loan issuances in Australasia declined for a second year

-

80

160

240

-

20

40

60

2012 2013 2014 2015 2016

Tota

l num

ber o

f iss

ues

Issu

es (U

S$b

n)

Australasia Total number of issues

-

100

200

300

400

-

50

100

150

200

2012 2013 2014 2015 2016

Tota

l num

ber o

f iss

ues

Issu

es (U

S$b

n)

Australasia Total number of issues

US$47bn US$34bn US$26bn US$38bn US$26bn

US$106bn US$136bn US$160bn US$110bn US$96bn

PAGE 17STRICTLY CONFIDENTIAL MacquarieCapital

Chinese banks and institutional investors are increasing lending to the Australian market

Source: Loanconnector and Thomson Reuters.

Chinese participation in the Australian market increased markedly in 2016

Funding landscape for borrowers is evolving

Chinese participation in the Australian market accounted for 10.8% in 2016 (compared to 1.4% in 2014)

The growth in Chinese lenders has been driven by

— Weight of capital in China looking to be deployed into investmentsother than equity

— Capital constraints of other banks including Basel 4 regulations, switching focus of domestic banks and European banks facing stagnant economic growth in home economies

Institutional lenders in Australian market are growing and competitive

1.4% 3.9% 10.8%

-

20%

40%

60%

80%

100%

2014 2015 2016Australian European Japanese Others Chinese

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

2017 equity and debt market outlook

03

PAGE 19STRICTLY CONFIDENTIAL MacquarieCapital

2017 expected to see robust ECM activity

Large 2017 IPO pipeline02 0301

Since the IPO window reopened in 2013, issuance has remained strong despite the deferral of a number of IPOs in the last few months of 2016

Expect the IPO market to remain open in 2017 with the potential for several high profile floats to come to market including the floats of a number of companies who delayed their listing plans in late 2016

Estimated 2017 IPO pipeline of ~$10 billion

M&A activity to continue After a year dominated by M&A issuance,

expectations are for companies to continue to look for accretive M&A opportunities to enhance growth and for investors to support these initiatives

The need for large balance sheet recapitalisations remains subdued

Blocks a likely focus Block trades will continue to account for a

large proportion of ECM activity with several large stakes set to be released from escrow in 2017

Strong estimated 2017 pipeline with >$3.3 billion in blocks coming out of escrow in 2017

Expectations for equity raisings in 2017Macquarie Capital Markets team

PAGE 20STRICTLY CONFIDENTIAL MacquarieCapital

-

1

2

3

RB

A c

ash

rate

(%)

Macquarie Research expects equities to perform positively in 2017 against a steeper yield curve and a stronger growth outlook

Source: Macquarie research, IRESS, Bloomberg and FactSet as at 31 December 2016.

…market does not expect cash rate to fall… …A$ remains a focus…

…resource exports underpin GDP…

2014A 2015A 2016A 2017F 2018F

…the AUD yield curve steepness is…

ASX expected to strengthen in 2017…

… in line with global yields

2017 macro backdrop to improve

1.0%

0.65

0.70

0.75

0.80

0.85

0.90

0.95

2014A 2015A 2016A 2017F 2018F

AU

D /

US

D ($

)

3.1%

2.3%

1.6%

2.4%2.8% 2.9% 3.0% 3.1%

2.9%

-

1

2

3

4

1H16 2H16 1H17 2H17 1H18 2H18 1H19 2H19 1H20

GD

P g

row

th (%

)

Resources GDP growth Other GDP Growth

4700

5000

5300

5600

5900

Jan 16 May 16 Sep 16 Jan 17 May 17 Sep 17 Jan 18

AS

X 20

0

5875(Dec 2017)

Macquarie Research Forecast

0.74

0.75

Increase supported by small improvement in

global growth and broadening recovery in

corporate earnings

A$ will find support from firm commodity prices

but the economy requires it to remain in

the low 70s range

1

2

3

4

1M 6M 2Y 5Y 10Y 20Y

AU

D M

id S

wap

Rat

e (%

)

Jul 16 Dec 16

-

1

2

3

1M 6M 2Y 5Y 10Y 20Y

US

D M

id S

wap

Rat

e (%

)

Jul 16 Dec 16

…however Macquarie Research forecasts cash rate to bottom in Q2 2017 at 1.0%

Market has a ~91% probability of remaining at 1.5% in Q2 2017…

1.0%

1.5% 1.6%

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

APPENDIXMacquarie capabilities and contact details

A

PAGE 22STRICTLY CONFIDENTIAL MacquarieCapital

12.1%11.1% 11.0% 10.9% 10.8%

9.6%

Macquarie UBS CS MS GS Citi

Mar

ket s

hare

(%)

Source: Thomson Reuters and IRESS as at 31 December 2016. Note 1: New issuances exclude block trades. 2: Best proxy for active institutional market share.

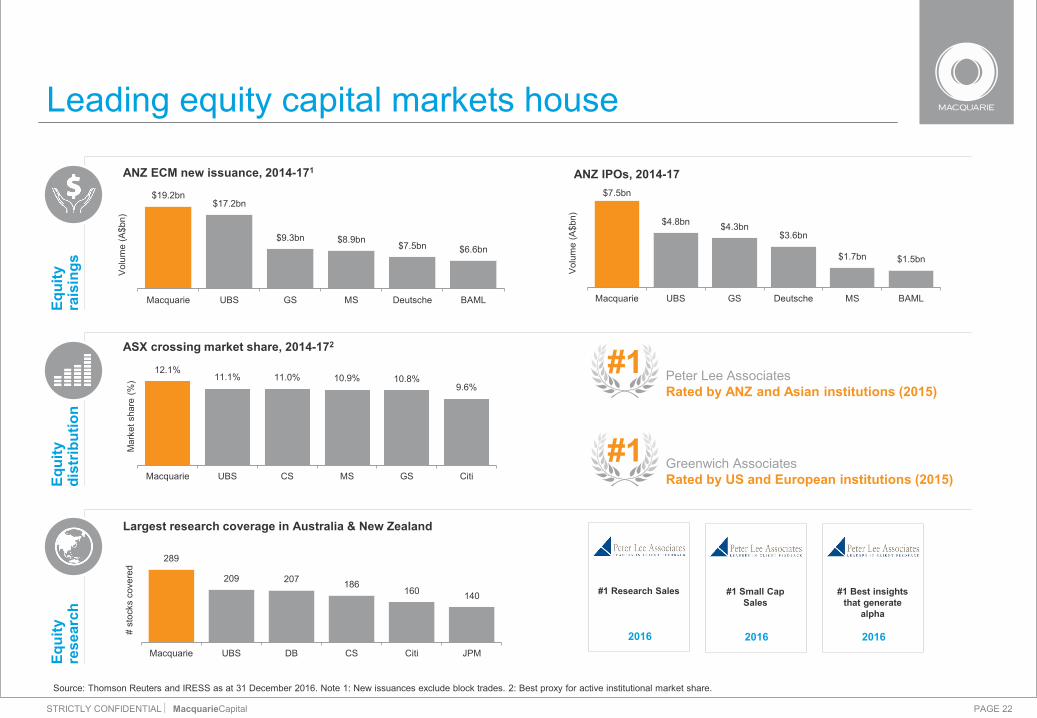

Leading equity capital markets house

ANZ IPOs, 2014-17ANZ ECM new issuance, 2014-171

Equi

ty

rais

ings

ASX crossing market share, 2014-172

Largest research coverage in Australia & New Zealand

Equi

ty

dist

ribut

ion

Equi

ty

rese

arch

$7.5bn

$4.8bn $4.3bn$3.6bn

$1.7bn $1.5bn

Macquarie UBS GS Deutsche MS BAML

Vol

ume

(A$b

n)289

209 207 186160 140

Macquarie UBS DB CS Citi JPM

# st

ocks

cov

ered

#1 Research Sales

2016

#1 Small Cap Sales

2016

#1 Best insights that generate

alpha

2016

$19.2bn$17.2bn

$9.3bn $8.9bn$7.5bn $6.6bn

Macquarie UBS GS MS Deutsche BAML

Vol

ume

(A$b

n)

Peter Lee Associates Rated by ANZ and Asian institutions (2015)

#1

Greenwich AssociatesRated by US and European institutions (2015)

#1

PAGE 23STRICTLY CONFIDENTIAL MacquarieCapital

$19.2bn

$17.2bn

$9.3bn$8.9bn

$7.5bn

$6.6bn

$5.3bn

$4.4bn

Macquarie UBS GS MS Deutsche BAML Citi CS

Vol

ume

(A$b

n)

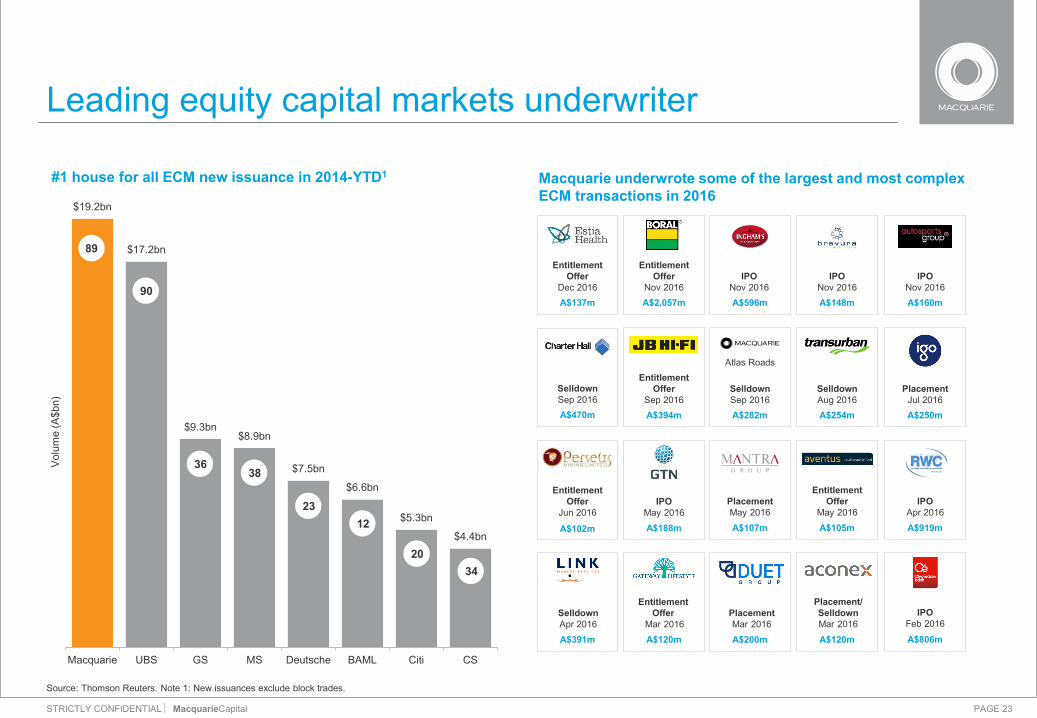

Source: Thomson Reuters. Note 1: New issuances exclude block trades.

#1 house for all ECM new issuance in 2014-YTD1 Macquarie underwrote some of the largest and most complex ECM transactions in 2016

Leading equity capital markets underwriter

89

90

3638

2312

2034

A$391m

SelldownApr 2016

A$919m

IPOApr 2016

A$107m

PlacementMay 2016

A$188m

IPOMay 2016

A$102m

Entitlement Offer

Jun 2016

A$250m

PlacementJul 2016

A$254m

SelldownAug 2016

A$282m

SelldownSep 2016

Atlas Roads

A$394m

Entitlement Offer

Sep 2016A$470m

SelldownSep 2016

A$596m

IPONov 2016

A$148m

IPONov 2016

A$160m

IPONov 2016

A$2,057m

Entitlement Offer

Nov 2016A$137m

Entitlement Offer

Dec 2016

A$806m

IPOFeb 2016

A$200m

PlacementMar 2016

A$120m

Placement/ SelldownMar 2016

A$120m

Entitlement Offer

Mar 2016

A$105m

Entitlement Offer

May 2016

PAGE 24STRICTLY CONFIDENTIAL MacquarieCapital

$13.6bn

$10.9bn

$8.6bn

$6.9bn

$5.2bn

$3.1bn $3.0bn$2.5bn

Macquarie UBS GS CS Deutsche MS Citi JPM

Vol

ume

(A$b

n)

Macquarie has led more ANZ IPOs over the last decade than any other bank1

Australia’s leading IPO underwriter

Source: Thomson Reuters. Note 1: IPOs since 2006.

74

15

27

12

58

34

21

22

Macquarie has lead managed 74 IPOs in the last decade

A$439m

IPOJune 2015

A$207m

IPOJune 2015

A$947m

IPOOct 2015

A$919m

IPOApr 2016

A$188m

IPOMay 2016

A$806m

A$148m

IPONov 2016

A$160m

IPONov 2016

A$145m

IPODec 2013

A$350m

IPOApr 2014

A$113m

IPOJuly 2014

A$439m

IPOOct 2013

A$334m

IPOJuly 2013

IPOFeb 2016

A$596m

IPONov 2016

A$583m

IPOMay 2014

A$2,255m

IPOJuly 2014

A$656m

IPOJune 2014

A$316m

IPOJune 2014

A$239m

IPOJune 2014

A$380m

IPOMay 2015

A$141m

IPODec 2014

A$5,921m

IPONov 2014

A$486m

IPOOct 2014

A$303m

IPOOct 2015

A$332m

IPODec 2015

PAGE 25STRICTLY CONFIDENTIAL MacquarieCapital

Market leading debt advisory and underwriting platform that delivers customised solutions for our clients

Leading experience in leveraged finance transactions…

A leading arranger of debt for clients

Originate, arrange, underwrite and syndicate bank loans and mezzanine financing for acquisition and leveraged finance, corporate bridge facilities and project finance

Advise, structure and arrange debt finance for clients across all industries

Adv

isor

y

Originate, structure, underwrite and execute bondmarket solutionsB

onds

Loan

s

DEB

T C

APIT

AL M

ARKE

TS

…advising on complex facilities…

…with infrastructure expertise

Note 1: Year ending 31 March 2016. Based on 100% of the deal value (and not the amount of the transaction attributed to Macquarie) where Macquarie acted as adviser, arranger, underwriter or participant to the transaction.

Financial adviser, Debt underwriter

Mezzanine facilities for the acquisition of

Cancer Partners UKc.$A170mJune 2015

Joint Bookrunner, Joint Lead Arranger

Senior Debt Facility for Platinum’s 70% acquisition

$US365February 2014

Joint Bookrunner, Joint Lead Arranger

Senior Secured refinancing credit facilities

$A1.4bnAugust 2013

Financial Adviser

Financial advisor to Healthscope on is

inaugural US Private Placement issuance

$US300mMarch 2016

Exclusive Financial Adviser

Refinancing of existing senior debt facilities

$A285mAugust 2015

Exclusive Financial Adviser

Refinancing of senior debt facilities of Worsley Multi-fuel Cogeneration Plant

$A870mDecember 2014

Exclusive Financial Adviser and Debt Arranger

Debt financing for acquisition of

majority stake in Ausgrid$A13,000m

October 2016

Financial adviser, debt co-underwriter

Debt financing for the acquisition of ANU’s

student accommodation ConfidentialAugust 2016

Sponsor, commercial and financial adviser, debt co-underwriter

Senior secured debt facilities for ACT Law

Courts PPP$A180m

December 2015

PAGE 26STRICTLY CONFIDENTIAL MacquarieCapital

Your Macquarie contacts

Hugh FalconCo-Head of ECM Australia and [email protected]: +61 3 9635 9478

Jacqui VanzellaExecutive [email protected]: +61 2 8232 4109

Peter AppleyardDivision [email protected]: +61 2 8232 8539

Stuart OwenAssociate [email protected]: +61 8 9224 0636

Angus FirthCo-Head of ECM and [email protected]: +61 2 8232 4039

Mark WarburtonHead of ECM [email protected]: +61 2 8237 4954

Aaron BlackDivision [email protected]: +61 2 8237 1157

Georgina LalorDivision [email protected]: +61 2 8232 6742

Michael DaleyAssociate [email protected]: +61 2 8237 7799

Equity Capital Markets Debt Capital Markets

Neil WatsonChairman of ECM [email protected]: +61 2 8232 3847

Andrew ScadeDivision [email protected]: + 61 2 8232 7593

Belinda LeeDivision [email protected]: +61 3 9635 8082

Tom FraczekAssociate [email protected]: +61 3 9635 8201

Equity Syndication

Greg Levy Head of DCM Australia and [email protected]: +61 2 8232 7941

Navodit NarainHead of [email protected]: +61 2 8232 3656

Iain MelhuishDivision [email protected]: +61 2 8232 6745

Paul StainesCo-Head of [email protected]: +61 2 8232 7781

Tiffany WardAssociate [email protected]: +61 2 8232 5151