lusltano mortgages no.2 public limited company and ... · lusitano mortgages no. 2 public limited...

TRANSCRIPT

Lusltano Mortgages No.2 Public Limited Company and Subsidiary

Dlrectors report and audited financial statements

For the year ended 31 December2014

Rqhtned number 374631

Lusitano Mortgages No.2 Public Limited Company and Subsidiary

ContentsPage(s)

Directors and other informationI

Directors report2-5

Statement of directors’ responsibilities 6

Independent audito?s report7-8

Group Statement of comprehensive income 9

Group Statement of financial position 10

Company Statement of financial position II

Group and Company Slatement of changes in equity 12

Group Statement of cash flows 13

Company Statement of cash flows 11

Notes to the financial statements 15-38

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary

Page IDirectors and other information

Directors Fimir McGrathDavid McGuinness

Registered Office (Asfronz 20 October 20I4 (Until 19 October 2011)6th Floor 5 Harbourmaster PlacePinnaclc 2 International Financial Services CentreEastpoint Business Park Dublin IDublin 3 IrelandIreland

Administrator & Deutsche tntemational Corporate Services tireland) LimitedCompany Secretary (Asfrom 20 October 2014 ((hi/il /9 October 2013,)

6th Floor 5 Harbourmaster PlacePinnacle 2 International Financial Services CentreEastpoint Business Park Dublin IDublin 3 IrelandIreland

Trustee Deutsche Trustee Company LimitedWinchester I-louseI Great Winchester StreetLondon EC2N 2DBUnited Kingdom

Independent Auditor KPMGChartered Accountants, Statutory Audit FirmI Harbourmaster PlaceInternational Financial Services CentreDublin IIreland

Bankers Deutsche Bank AG London Bank of IrelandWinchester House 2 Burlington PlanI Great Winchester Street Burlington RoadLondon LC2N 2DB Dublin 4United Kingdom Ireland

Solicitor Matheson70 Sir John Rogerson’s QuayDublin 2Ireland

Custodian and Novo Banco, S.A. (formerly Banco Espirito Santo, SA.)Servicer Avenida da Liberdade. 195. 1250-142

LisbonPortugal

Swap Counterparty Credit Agricole Indosuez9. quai Paul Downer92920 Paris La DefenseFrance

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 2

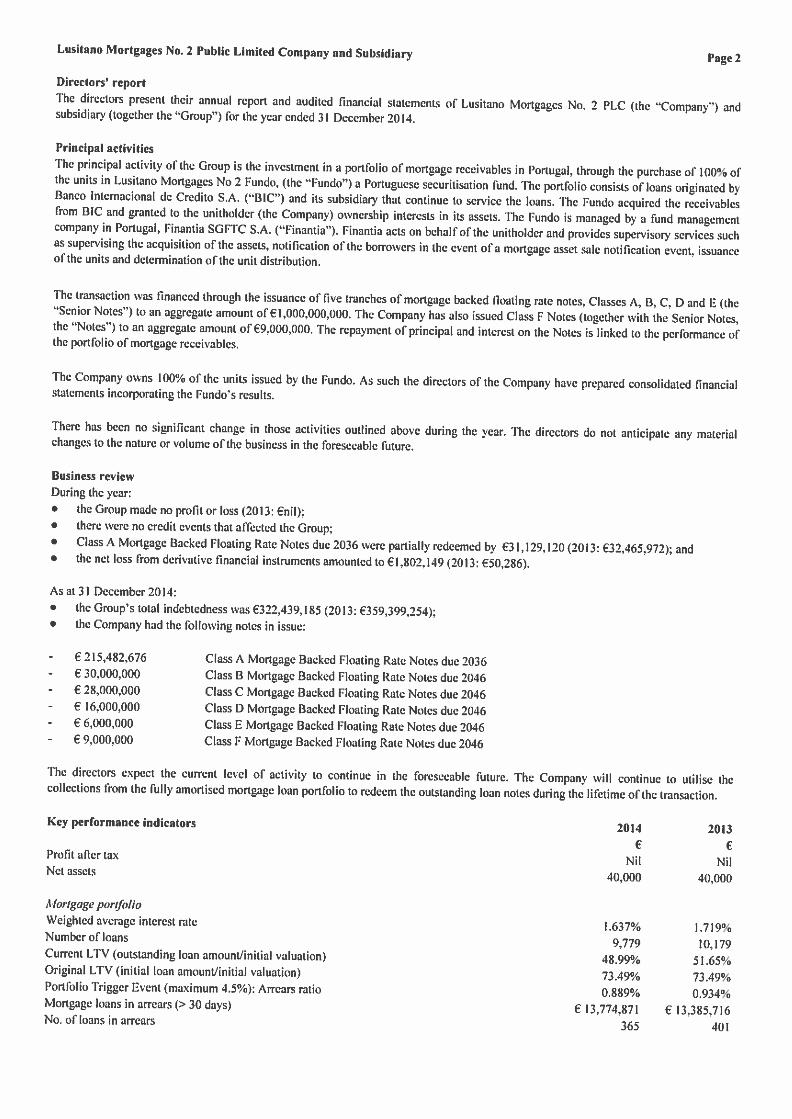

Directors’ reportThe directors present their annual report and audited financial statements of Lusitano Mortgages No. 2 PLC (the “Company”) andsubsidiary (together the “Group”) for the year ended 31 December2014.

Principal activitiesThe principal activity’ of the Group is the investment in a portfolio of mortgage receivables in Portugal. through the purchase of 100% oFthe units in Lusitano Mortgages No 2 Fundo. (the “Fundo”) a Portuguese securitisation fund. The portfolio consists of loans originated byBanco Internacional de Credito S.A. (131C”) and its subsidiary that continue to service the loans. The Fundo acquired the receivablesfrom HIC and granted to the unitholder (the Company) ownership interests in its assets. The Fundo is managed by a fund managementcompany in Portugal, Finantia SGFTC S.A. (“Finantia”). Finantia acts on behalf of the unitholder and provides supervisory services suchas supervising the acquisition of the assets, notification of the borrowers in the event of a mortgage asset sale notification event, issuanceof the units and determination of the unit distribution,

The transaction was financed through the issuance of five tranches of mortgage backed floating rate notes, Classes A, H. C. 13 and E (the“Senior Notes”) to an agaregate amount olE 1,000,000,000. The Company has also issued Class F Notes (together with the Senior Notes.the “Notes”) to an aggregate amount of €9,000,000. The repayment of principal and interest on the Notes is linked to the performance ofthe portfolio of mortgage receivables.

The Company owns 100% of the units issued by the Fundo. As such the directors of the Company have prepared consolidated financialstalements incorporating the Fundo’s results.

There has been no significant change in those activities outlined above during the year. The directors do not anticipate any materialchanges to the nature or volume of the business in the foreseeable future.

Business reviewDuring the year:• the Group made no profit or loss (2013: €nil);• there were no credit events that affected the Group:• Class A Mortgage Hacked Floating Rate Notes due 2036 were partially redeemed by €31,129,120 (2013: €32,465,972): and• the net loss from derivative financial instruments amounted to €1,802,149 (2013: €50.286).

As at 31 December 2014:• the Group’s total indebtedness was €322,439,185 (2013: €359.399.254):• the Company had the following notes in issue:

- €215,482,676 Class A Mortgage Hacked Floating Rate Notes due 2036- € 30.000,000 Class H Mortgage Backed Floating Rate Notes due 2046- € 26,000,000 Class C Mortgage Backed Floating Rate Notes due 2046- € 16.000,000 Class 13 Mortgage Backed Floating Rate Notes due 2046- f 6,000,000 Class £ Mortgage Backed Floating Rate Notes due 2046- € 9,000,000 Class F Mortgage Backed Floating Rate Notes due 2046

The directors expect the current level of activity to continue in the foreseeable future. The Company will continue to utilise thecollections from the fUlly amortised mortgage loan portfolio to redeem the outstanding loan notes during the lifetime of the transaction.

Key performance indicators 2014 2013€ €

Profit after tax Nil NilNet assets 40.000 40,000

Mortgage porfoIioWeighted average interest rate 1.637% 1.719%Number of loans 9.779 10.179Current LTV (outstanding loan amount/initial valuation) 48.99% 51.65%Original LTV (initial loan amount/initial valuation) 73.49% 73.49%Portfolio Trigger Event (maximum 4.5%): Arrears ratio 0.889% 0.934%Mortgage loans in arrears (>30 days) € 13,774.871 € 13.385.716No. of loans in arrears 365 40!

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 3

Directors’ report (continued)

Key performance indicators (continued)The directors of the Company manage their credit risk exposure of loans and receivables by monitoring the loan to value ratios, mortgagearrears balances and related ratios. The loan to value ratio is a mathematical calculation which expresses the current principal balance ofa mortgage as a percentage of the total initial value of the property. The arrears ratio is the ratio of the principal outstanding balance ofmortgage loans in arrears between 90 to 365 days divided by the principal outstanding balance of initial mortgage backed credit portfolioas at the determination date.

Future developmentsThe board will continue to seek new opportunities for the Company and will continue to ensure proper management of the currentportlblio of notes of the Company.

Results and dividends for the yearThe results lbr the year are set out on page 9. The directors do not recommend the payment of a dividend for the year under review (2013:nil).

Changes in directors, secretary and registered officeOn 6 November 2014. the registered office of the Company changed from 5 I larbourmaster Place, IFSC. Dublin I. Ireland to 6th Floor.Pinnacle 2, Eastpoint Business Park, Dublin 3, Ireland.

There were no other changes in directors, secretary or registered office during the year and/or since the year end

Directors and secretary and their interestsThe directors and secretary. who held office on 31 December 2014, did not hold any shares in the Company at that date, or during theyear. There were no contracts of any significance in relation to the business of the Company in which the directors had any interest, asdefined in the Companies Act 1990, at any time during the year.

Principal risks and uncertaintiesThe Group and Company are subject to various risks. The key risks facing the Group and Company and the manner in which these riskshave been dealt with are disclosed in note 25 of the financial statements.

Going concernThe group’s financial statements for the year ended 31 December 2014 have been prepared on a going concern basis. The directorsanticipate that the loans and receivables will continue to generate enough cash flow on an ongoing basis to meet the Company liabilitiesas they fall due. Majority of the Notes in issue as at 31 December 2014 will mature in 2046. For these reasons, the directors believe thatthe going concern basis is appropriate.

Operational riskOperational risk is the risk of director indirect loss arising from a wide variety of causes associated with an entity’s processes. personneland infrastructure, and from external factors other than credit, market and liquidity risks such as those arising from legal and regulatoryrequirements and generally accepted standards of corporate behaviour.

Operational risks arise from all of the Group’s operations. The Company was incorporated with the purpose of engaging in those activitiesoutlined in Note 1. The aroup limits its exposure to operational risks by outsoureing all management and administration flinctions toDeutsche International Corporate Services (Ireland) Limited (“DICSIL”) Ibr the Company.

The Fundo is managed by a fund management company in Portugal, Finantia SGFTC S.A.

Credit riskCredit risk is the risk of the financial loss to the Group and Company if counterparty to a financial asset Ibils to meet its contractualobligations, and arises principally from the Group and Company’s credit linked assets.

During the li(b of the transaction, the originator (Banco lntemacional de Credito SM is able to modify the terms and conditions of someof the loans on a limited basis or substitute some loans.

These changes may have an impact on the risk profile of the pool. The originator’s ability to make changes to the terms and conditions ofthe loans securitised is limited by permitted variations and substitutions language included in the securitisation documentation.

Any reduction in the value of the mortgage receivables will be matched by a reduction in the repayment obligations of the Notes. Becauseof the ring-fenced nature of the debt issued by the Company any such losses would ultimately be borne by either the swap counterparty orthe noteholders.

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 4

Directors’ report (continued)

Corporate Governance Statement

IntroductionThe Company is subject to and complies with Irish Statute comprising the Companies Acts 1963102013 and the Listing rules of the IrishStock Exchange. The Company does not apply additional requirements in addition to those required by the above. Each of the seiwiceproviders engaged by the Company is subject to their own corporate governance requirements.

Financial Reporting ProcessThe Board of Directors (“the Board”) is responsible fbr establishing and maintaining adequate internal control and risk managementsystems of the Company in relation to the financial reporting process. Such systems arc designed to manage rather than eliminate the riskof failure to achieve the Companys linancial reporting objectives and can only provide reasonable and not absolute assurance againstmaterial misstatement or loss.

The Board has established processes regarding internal control and risk management systems to ensure its effective oversight of thefinancial reporting process. These include appointing the Administrator. DIUSIL. to maintain the accounting records of the Companyindependently of the Arranger and the Custodian. The Administrator is contractually obliged to maintain proper books and records asrequired by the Corporate Administration agreement. To that end the Administrator performs reconciliations of its records to those of theArranger and the Custodian. The Administrator is also contractually obliged to prepare for review and approval by the Board the annualreport including financial statements intended to give a true and fair view.

The Board evaluates and discusses significant accounting and reporting issues as the need arises. From time to time the Board alsoexamines and evaluates the Administrator’s financial accounting and reporting routines and monitors and evaluates the external auditors’perlbrmance. qualifications and independence. The Administrator has operating responsibility for internal control in relation to thefinancial reporting process and the Administrator’s report to the Board.

Risk AssessmentThe Board is responsible for assessing the risk of irregularities whether caused by fraud or error in financial reporting and ensuring theprocesses are in place for the timely identification of internal and external matters with a potential elThct on financial reporting. TheBoard has also put in place processes to identif’ changes in accounting rules and recommendations and to ensure that these changes areaccurately reflected in the Companys financial statements.

More specifically:- The Administrator has a review procedure in place to ensure errors and omissions in the financial statements are identified and

corrected.- Regular training on accounting rules and recommendations are provided to the accountants employed by the administrator.- Accounting bulletins, issued by Deutsch Bank AG. London Branch. an entity related to DICSIL. are distributed monthly to all

accountants employed by the Administrator.

Control ActivitiesThe Administrator is contractually obliged to design and maintain control structures to managc the risks which the Board judges to besignificant fbr internal control over financial reporting. These control structures include appropriate division of responsibilities andspecific control activities aimed at detecting or preventing the risk of significant deficiencies in financial reporting for every significantaccount in the financial statements and the related notes in the Company’s annual report.

tThnitoringThe Board has an annual process to ensure that appropriate measures are taken to consider and address the shortcomings identified andmeasures recommended by the independent auditors.

Given the contractual obligations on the Administrator, the Board has concluded that there is currently no need lbr the Company to have aseparate internal audit function in order for the board to perform elThctive monitoring and oversight of the internal control and riskmanagement systems olthe Company in relation to the financial reporting process.

Capital StructureNo person has a significant direct or indirect holding of securities in the Company. No person has any special rights of control over theCompany’s share capital.

There are no restrictions on voting rights.

Directors’ report (continued)

Lusitano Mortgages ND. 2 Public Limited Company and Subsidiary PageS

Corporate Governance Statement (continued)

Appointmen! and replacement of directors and amendment in the articles ofassociationWith regard to the appointment and replacement of Directors, the Company is governed by its Articles of Association, Irish Statutecomprising the Companics Acts. 1963 to 2013 and the Listing Rules of the Irish Stock Exchange. The Articles of Association themselvesmay be amended by special resolution of the shareholders.

Poii’ers of DirectorsThe Board is responsible for managing the business affairs of the Company in accordance with the Articles of Association. The Directorsmay delegate certain functions to the Administrator and other parties. subject to the supenision and direction by the Directors. TheDirectors have delegated the day to day administration of the Company to the Administrator.

The Articles of Association provide that the Directors may exercise all the powers of the Company to borrow money, to mortgage orcharge its undertaking property of any part thereof and may delegate these powers to the Arranger.

The instrument of transfer of any share shall be executed by or on behalf of the transftror and, in eases where the share is not fully paid.by or on behalf of the transferee. The transferor shall be deemed to remain the holder of the share until the name of the transferee enteredon the register in respect thereof. The Directors, in their absolute discretion and without assigning any reason therefore, may decline toregister any transfer of share. If the Directors refuse to register a transfer, they shall, within two months after the date on which thetransfer was lodged with the Company. send to the transferee notice of the refusal.

Audit committeeStatutory audits in Ireland are regulated by the European Communities Regulations, 2011 (S.f. 220 of 2011). According to the regulations.if the sole business of the Irish SPV relates to the issuing of asset backed securities, the SPV is exempt from the requirement to establishan audit committee (under Regulation 9 1(9) (d) of the Regulations). In this respect, the Company is not required to establish an auditcommittee.

Subsequent eventsThere has been no subsequent significant event that requires disclosures in these financial statements up to the date of signing this report.

Accounting recordsThe directors believe that they’ have complied with the requirements of Section 202 of the Companies Act, 1990 with regard to the booksof account by employing accounting personnel with the appropriate expertise and by providing adequate resources to the financialfunction. The books of account of the Company are maintained at 5 Ifarbourmaster Place. IFSC, Dublin I, Ireland.

Independent auditorIn accordance with Section 160(2) of the Companies Act, 1963, KPMG. Chartered Accountants. Statutory Audit Firm has expressed theirwillingness to continue in office.

ci( Eamir Mcçiath

Director

On behalf of the Board

Director

Date: 29 April, 2015

Statement of directors’ responsibilities

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 6

The Directors are responsible for preparing the Directors’ Report and the Group and Company financial statements in accordance withapplicable law and regulations.

Company law requires the directors to prepare Group financial statements for each financial year. Under that law the directors haveelected to prepare the Company financial statements in accordance with International Financial Reporting Standards (IFRSs) as adoptedby the EU.

The Company’s financial statements are required by law and IFRSs as adopted by the EU to present fairly the financial position andpcrlbrmance of the Group and the Company. The Companies Acts, 1963 to 2013 provide in relation to such financial statements thatreferences in the relevant parts of those Acts to financial statements giving a true and fair view are references to their achieving a fairpresentation.

In preparing each of the group and company financial statements, the directors are required to;

• select suitable accounting policies and then apply them consistently;

• makejudgments and estimates that are reasonable and prudent;

• state that the financial statements comply with IFRSs as adopted by the EU; and

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue inbusiness.

The Directors are responsible for keeping proper books of account that disclose with reasonable accuracy at any time the financialposition of the Company and enable them to ensure that its financial statements comply with the Companies Acts 1963 to 2013. They’ arealso responsible for taking such steps as are reasonably open to them to salëguard the assets of the Group and to prevent and detect fraudand other irregularities.

The Directors are also required by the Transparency (Directive 2004/109/EC) Regulation 2007 and the Transparency Rules of the IrishFinancial Services Regulatory Authority to include a Directors’ report containing a fair review of the business and a description of theprincipal risks and uncertainties facing the Group.

The Directors (who are listed on page I), confirm that. to the best of their knowledge and belieI

• they have complied with the above requirements in preparing the Group and Company financial statements;

• the Group financial statements, prepared in accordance with IFRSs as adopted by the EU. give a true and fair view of the state of theassets, liabilities, financial position and of the profit of the Group for the year then ended; and

• the Directors’ report includes a fair review of the development and performance of the business of the Group, together with adescription of the principal risks and uncertainties that it faces.

On behalf of the Board

Director Director

Date: 29 April, 20:

KPMGAudit1 Hatc.srnasle PaceIFSCDbir 1Ire and

INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OF LUSITANO MORTGAGESNO.2 PUBLIC LIMITED COMPANY AND SUBSIDIARY

We have audited the financial statements (“financial statements”) of Lusitano Mortgages No. 2 PublicLimited Company and Subsidiary for the year ended 3! December 2014 which comprise the GroupStatement of Comprehensive Income, the Group Statement of Financial Position, the CompanyStatement of Financial Position, the Group and Company Statement of Changes in Equity, the GroupStatement of Cash Flows, the Company Statement of Cash Flows and the related notes. The financialreporting framework that has been applied in their preparation is Irish law and International FinancialReporting Standards (WRS5) as adopted by the European Union and, as regards the Company financialstatements, as applied in accordance with the provisions of the Companies Acts 1963 to 2013.

This report is made solely to the Company’s members, as a body, in accordance with section 193 of theCompanies Act 1990. Our audit work has been undertaken so that we might state to the Company’smembers those matters we are required to state to them in an auditor’s report and for no other purpose.To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other thanthe Company and the Company’s members as a body, for our audit work, for this report, or for theopinions we have formed.

Respective responsibilities of directors and auditor

As explained more fully in the Statement of Directors’ Responsibilities set out on page 6, the Directorsare responsible for the preparation of the financial statements giving a true and fair view. Ourresponsibility is to audit and express an opinion on the financial statements in accordance with Irish lawand International Standards on Auditing (UK and Ireland). Those standards require us to comply withthe Financial Reporting Council’s Ethical Standards for Auditors.

Scope of the audit of the financial statements

An audit involves obtaining evidence about the amounts and disclosures in the financial statementssufficient to give reasonable assurance that the financial statements are free from material misstatement,whether caused by fraud or error. This includes an assessment of: whether the accounting policies areappropriate to the Group and the Company’s circumstances and have been consistently applied andadequately disclosed; the reasonableness of significant accounting estimates made by the Directors; andthe overall presentation of the financial statements. In addition, we read all the financial and nonfinancial information in the Director’s report to identify material inconsistencies with the auditedfinancial statements and to identify any information that is apparently materially incorrect based on, ormaterially inconsistent with, the knowledge acquired by us in the course of performing the audit. If webecome aware of any apparent material misstatements or inconsistencies, we consider the implicationsfor our report.

an rrt partnQsh!D and a cnembe rn, a4 1h9 KPMGre,.wa,ha r.Crcnncrt e.bEr I ml aft - an1 .tl K0’.3 e,r.acaI

I KP,C nIB’ naro’,aI a Sa,as or, v

LW

INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OF LUSITANO MORTGAGESNO.2 PULIC LIMITED COWANY AND SUBSIDIARY (Continued)

Opinion on financial statements

In our opinion:• The Group financial statements give a true and fair view, in accordance with WRSs as adopted by

the European Union, of the state of the Group’s affairs as at 31 December2014 and of its result forthe year then ended;

• the Company Statement of Financial Position gives a true and fair view, in accordance with WRSsas adopted by the European Union and in accordance with the provisions of the Companies Acts1963 to 201 3, of the state of the Company’s affairs as at 3 I December 2014; and

• the financial statements have been properly prepared in accordance with the requirements of theCompanies Acts 1963 to 2013 and, as regards the Group financial statements, Article 4 of the lASRegulation.

Matters on which we are required to report by the Companies Acts 1963 to 2013

We have obtained all the information and explanations which we consider necessary for the purposesof our audit.

The Company’s Statement of Financial Position is in agreement with the books of account and, in ouropinion, proper books of account have been kept by the Company.

In our opinion, the information given in the Directors’ report is consistent with the financial statementsand the description in the Corporate Governance Statement of the main features of the internal controland risk management systems in relation to the process for preparing the Group financial statements isconsistent with the Group financial statements.

The net assets of the Company, as stated in the Company Statement of Financial Position, are more thanhalf of the amount of its called-up share capital and, in our opinion, on that basis, there did not exist at31 December 2014 a financial situation which under Section 40(l) of the Companies (Amendment)Act, 1983 would require the convening of an extraordinary general meeting of the Company.

Matters on which we are required to report by exception

We have nothing to report in respect of the provisions in the Companies Acts 1963 to 2013 whichrequire us to report to you ii, in our opinion, the disclosures of Directors’ remuneration and transactionsspecified by law are not made.

c o%—CoIm ClifforffFor and on behalf ofKPMGChartered Accountants, Statutory Audit FirmI Harbounnaster Place!FSC, DublinIreland

Date: 29 APRL

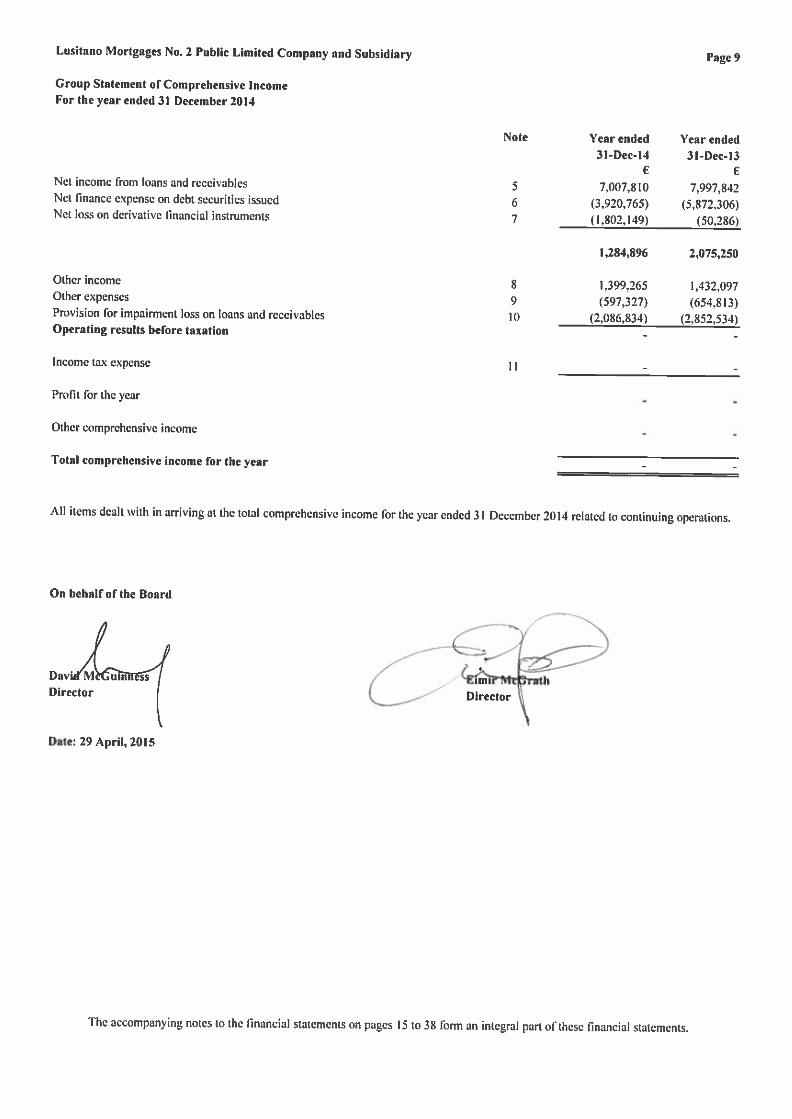

Lusitano Mortgages No.2 Public Limited Company and Subsidiary Page 9

Group Statement of Comprehensive IncomeFor the year ended 31 December 2014

Other incomeOther expensesProvision for impairment loss on loans and receivablesOperating results before taxation

Income tax expense

Profit lbr the year

Other comprehensive income

Total comprehensive income for the year

II

All items dealt with in arriving at the total comprehensive income for the year ended 31 December 2014 related to continuing operations.

On behalf of the Board

Dav NI urn ssDirector

Date; 29 Aprit, 2015

-% iE_mifltcfraIhDirector

N

Note Year ended Year ended31-Dec-14 31-Dec-13

€ €Net income from loans and receivables 5 7,007.810 7,997,842Net finance expense on debt securities issued 6 (3,920.765) (5,872.306)Net loss on derivative financial instruments 7 (1.802,149) 50.286)

89ID

1.284,896 2,075,250

1.399.265 1,432,097(597.327) (654.813)

(2.086.834) (2.852.534)

The accompanying notes to the financial statements on pages 15 to 38 form an integral pan of these financial statements.

Lusitano Mortgages No.2 Public Limited Company and Subsidiary Page 10

Group Statement of Financial PositionAs at 31 December 2014

ASSETS

Cash and cash equivalentsOther receivablesDerivative financial assetsLoans and receivables

Total Assets

Total Liabilities

EquityShare capitalRetained eaminus

Total equity

Total liabilities and equity

16IS1718

32.318.105 35.111.441449.322 500.384

- 3.788.480289.711.758 320.038.949

David McGuinnessDirector

Date: 29 r

C*athDirector

31-Dec-14 31-Dec-13€ €

Note

1213IS14

LIABILITIES AND EQUITY

LiabilitiesOther payablcsDerivative financial liabilitiesLiquidity facilityDebt securities issued

322,479,185 359,439,254

442,360 1,706,3161,710,364 186,342

17.728,961 19,596.708302,557.500 337.909.888

322,439,185 359,399,254

40.000 40,000

40,000 40,000

322,479,185 359,439,254

20

On behalf of the Board

The accompanying notes to the financial statements on pages 15 to 38 fbrm an integral part of these financial statements.

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page II

Company Statement of Financial PositionAs at 31 December 2014

ASSETS

Cash and cash equivalentsOther receivablesDerivative financial assetsLoans and receivables

Total Assets

Total Liabilities

EquityShare capitalRelained earnings

Total equity

Total liabilities and equity

12131514

16IS1718

I it—‘-Eimiritf!rath

Directo\

Note 31-Dec-14 31-Dec-13€

26.757.087 28,630,6961,277,034 1.620,365

- 3,788.480294.352.083 325,299.504

LIABILITIES AND EQUITY

LiabilitiesOther payablesDerivative financial liabilitiesLiquidity facilityDebt securities issued

322,386,204 359,339,045

339,379 1.606.1071.710.364 186.342

17.728.961 19.596.708302.557.500 337,909.886

322,346,204 359,299,045

40,000 40.000

40,000 40,000

322,386,204 359,339,045

20

rOn bebalf of the Board

CDate: 29 April, 2015

/

The accompanying notes to the financial statements on pages 15 to 38 lbrm an integral part of these financial statements.

Lusitano Mortgages No.2 Public Limited Company and Subsidiary Page 12

Group and Company Statement of Changes in EquityFor the year ended 31 December 2014

Balance as at 1 January 2013

Profit for the year 2013

Other comprehensive income

Total comprehensive income

Balance as at 31 December 2013

Balance as at 1 January 2014

Profit for the year 2014

Other comprehensive income

Total comprehensive income

Balance ns at 31 December 2014

40,000 - 40,000

40,000 - 40,000

40,000 - 40,000

Share capital Retained Total€ € €

40,000 - 40,000

The accompanying notes to the financial statements on pages 15 to 38 form an integral part of these financial statements.

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 13

Group statement of cash flowsFor the year ended 31 December 2014

Net cash flows from operating activitiesResult from ordinary activities after taxation

66

65l07

(74.907)7.388

3,988.284(7,007.810)

2.086.8345.312.5034,312,292

(5,016)(7.274)

4,300,002

(74.907)7,388

5.939.825(7,997,842)

2,852.534(1.160.879)

(433,881)

Note Year ended31-Dec-14

\‘ear ended31 -Dcc- 13

€ €

.1djustmentsfor:Amorlisation of premiumAmortisation of issue costsInterest expense during the yearInterest income during the yearNet increase in provision for impairment loss on loans and receivablesUnrealised loss’(gain) on derivatie financial instrumentsOperating cash flow before movements in working capitalDecrease in other receivables(Decrcase)/increase in other payablesNet cash used in operating activities

Cash flows from investing activitiesCollections on portfolio of loan receivablesInterest received during the yearNet cash generated from investing activities

Cash flows from financing activitiesRepayment of liquidity facilityPayment for redemption of notesInterest paid during the yearNet cash used in financing activities

Net decrease in cash and cash equivalents

Cash and cash equivalents at beginning of the year

Cash and cash equivalents at end of the year

14

‘7

12

12

6.435(427,446)

28,240.357 30,031.1707.063.888 8.14L.313

35,304,245 38,172,483

(1.867.747) (1,947,958)(35,284,869) (32,465.972)

(5,244.967) (5,221.141)(42,397,583) (39,635,071)

(2,793,336) (1,890,034)

35.111.441 37.001.475

32,318,105 35,111,441

The accompanying notes to the financial statements on pages 15 to 38 lbrm an integral pan of these financial statements.

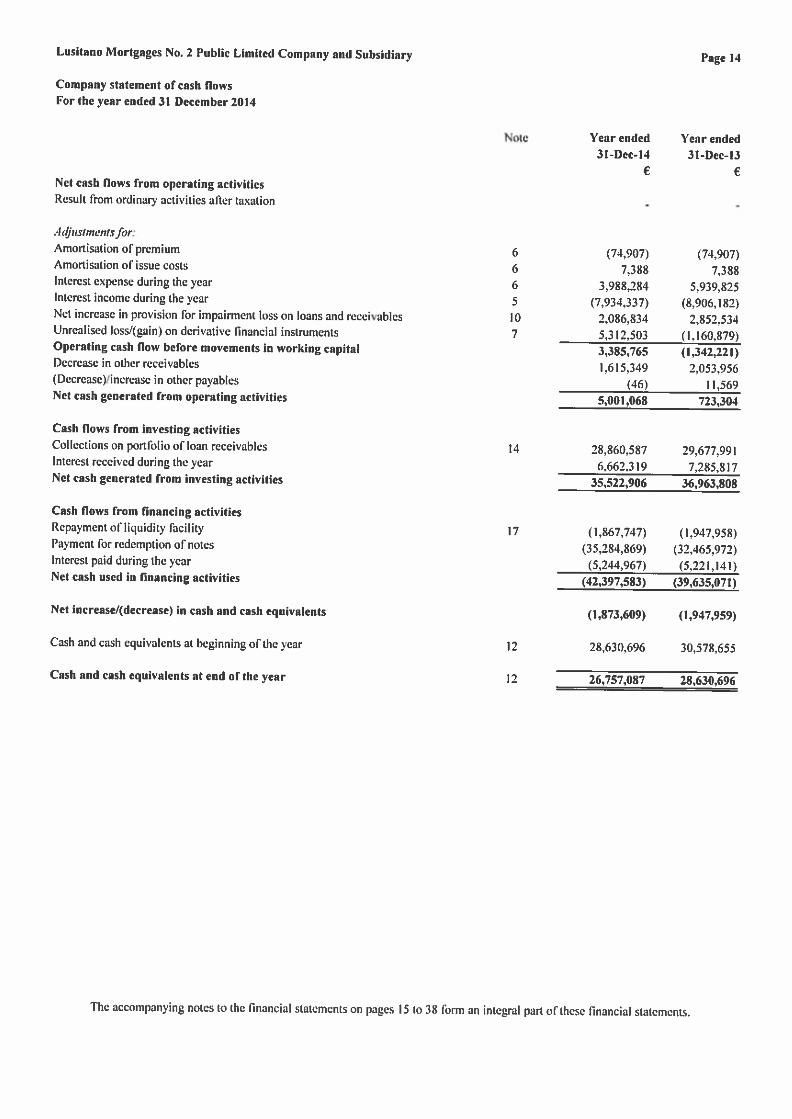

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 14

Company statement of cash flowsFor the year ended 31 December 2014

Net cash flows from operating activitiesResult from ordinary activities after taxation

ID7

(74.907)7.388

3,988,284(7,934.337)

2.086.8345.312.5033,385,7651,615,349

(46)5,001,068

(74.907)7.388

5,939.825(8.906,182)

2.852.534(1.160.879)(1,342,221)

2,053.95611,569

723,304

Year ended31-Dec-14

€

Year ended31-Dec-13

Note

66

65

:ldjztsiiiietztsfor:Amonisation of premiumAmortisation of issue costsInterest expense during the yearInterest income during the yearNet increase in provision for impairment loss on loans and receivablesUnrealised loss/Lain) on derivative financial instrumentsOperating cash flow before movements in working capitalDecrease in othcr receivables(Decrease)/increase in other payablesNet cash generated from operating activities

Cash flows from investing activitiesCollections on portfolio of loan receivablesInterest received during the yearNet cash generated from investing activities

Cash flows from financing activitiesRepayment of liquidity facilityPayment for redemption of notesInterest paid during the yearNet cash used in financing activities

Net increase/(decrease) in cash and cash equivalents

Cash and cash equivalents at beginning olthe year

Cash and cash equivalents at end of the year

14

17

12

12

28.860.587 29,677,9916.662,319 7,285.6 17

35,522,906 36,963,808

(1.867.747) (1.947.958)(35.284.869) (32,465.972)

(5.244.967) (5.221.141)(42,397,583) (39,635,071)

(1.873,609) (1,947,959)

28.630.696 30,578.655

26,757,087 28,630,696

The accompanying notes to the financial statements on pages 15 to 36 tbrm an integral part of these financial statements.

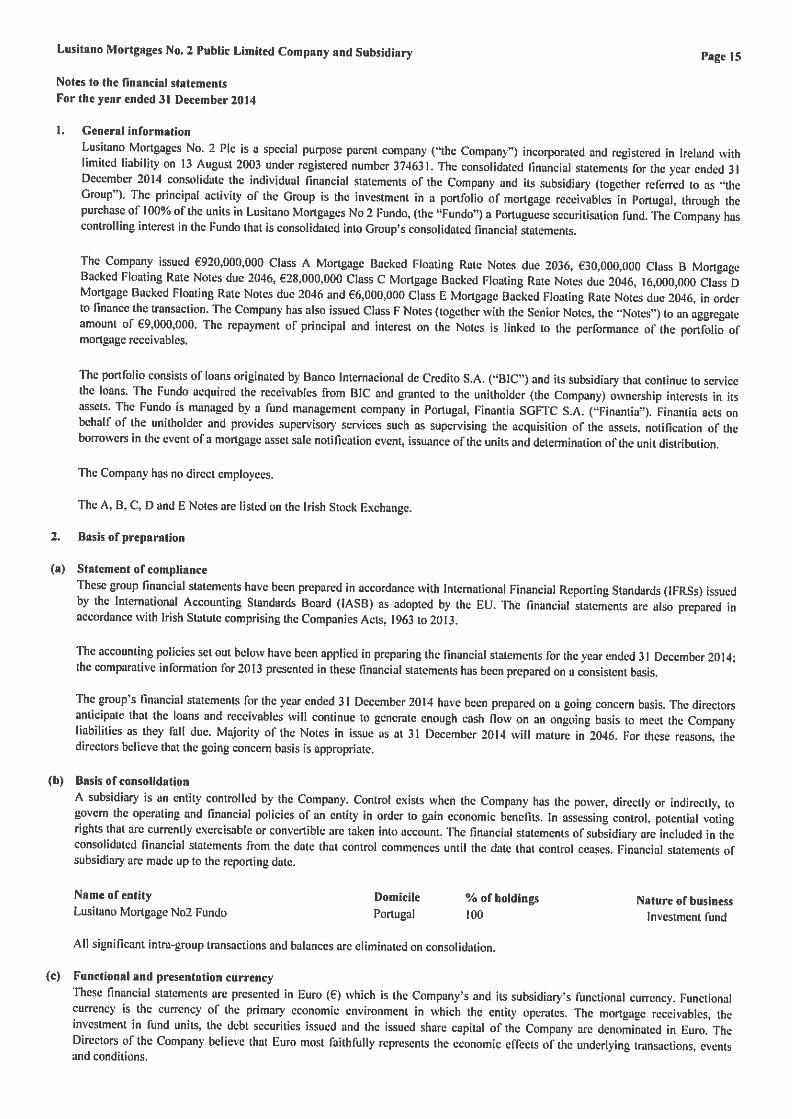

Lusitano Mortgages No.2 Public Limited Company and Subsidiary Page 15

Notes to the financial statementsFor the year ended 31 December 2014

General informationLusimno Mortgages No. 2 Plc is a special purpose parent company (he Company”) incorporated and registered in Ireland withlimited liability on 13 August 2003 under registered number 374631. The consolidated financial statements for the year ended 31December 2014 consolidate the individual financial statements of the Company and its subsidiary (together referred to as “theGroup”). The principal activity of the Group is the investment in a portfolio of mortgage receivables in Portugal. through thepurchase of 100% of the units in Lusitano Mortgages No 2 (‘undo. (the Fundo”) a Portuuuese securitisation fund. The Company hascontrolling interest in the (‘undo that is consolidated into Group’s consolidated financial statements.

The Company issued €920,000,000 Class A Mortgage Backed Floating Rate Notes due 2036. €30,000,000 Class B MortgageBacked Floating Rate Notes due 2046, €28,000,000 Class C Mortgage Backed Floating Rate Notes due 2046, 16,000,000 Class BMortgage Backed Floating Rate Notes due 2046 and €6,000,000 Class F Mortgage Backed Floating Rate Notes due 2046, in orderto finance the transaction. The Company has also issued Class F Notes (together with the Senior Notes. the “Notes”) to an aggregateamount of €9,000.000. The repayment of principal and interest on the Notes is linked to the perfbrmance of the portfolio ofmortgage receivables.

The portfblio consists of loans originated by Banco Internacional de Credito S.A. (“BIC”) and its subsidiary that continue to servicethe loans. The Fundo acquired the receivables from BIC and granted to the unitholder (the Company) ownership interests in itsassets. The Fundo is managed by a Fund management company in Portugal, Finantia SGFTC S.A. (“Finantia”). Finantia acts onbehalf of the unitholder and provides supervisory services such as supervising the acquisition of the assets, notification of theborroners in the event of a mortgage asset sale notification event, issuance of the units and determination of the unit distribution.

The Company has no direct employees.

The A, B. C, U and C Notes are fisted on the Irish Stock Exchange.

2. Basis of preparation

(a) Statement of complianceThese group financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs) issuedby the International Accounting Standards Board (IASB) as adopted by the EU. The financial statements are also prepared inaccordance with Irish Statute comprising the Companies Acts. 1963 to 2013.

The accounting policies set out below have been applied in preparing the financial statements for the year ended 3! December 2014;the comparative information fbr 2013 presented in these financial statements has been prepared on a consistent basis.

The group’s financial statements for the year ended 31 December 2014 have been prepared on a going concern basis. The directorsanticipate that the loans and receivables will continue to generate enough cash flow on an ongoing basis to meet the Companyliabilities as they fall due. Majority of the Notes in issue as at 31 December 2014 will mature in 2046. For these reasons, thedirectors believe that the going concern basis is appropriate.

(b) Basis of consolidationA subsidiary is an entity controlled by the Company. Control exists when the Company has the power, directly or indirectly, togovern the operating and financial policies of an entity in order to gain economic benefits. In assessing control. potential votingrights that are currently exercisable or convertible are taken into account. The financial statements of subsidian are included in theconsolidated financial statements from the date that control commences until the date that control ceases, Financial statements ofsubsidiary are made up to the reporting date.

Name of entity Domicile % of holdings Nature of businessLusitano Mortgage No2 Fundo Portugal 100 ln’estment fund

All significant intra-group transactions and balances are eliminated on consolidation.

(c) Functional and presentation currencyThese financial statements are presented in Euro (€) which is the Company’s and its subsidiary’s functional currency. Functionalcurrency is the currency of the primary economic environment in which the entity operates. The mortgage receivables, theinvestment in fund units, the debt securities issued and the issued share capital of the Company are denominated in Euro. TheDirectors of the Company believe that Euro most faithfully represents the economic effcts of the underlying transactions, eventsand conditions.

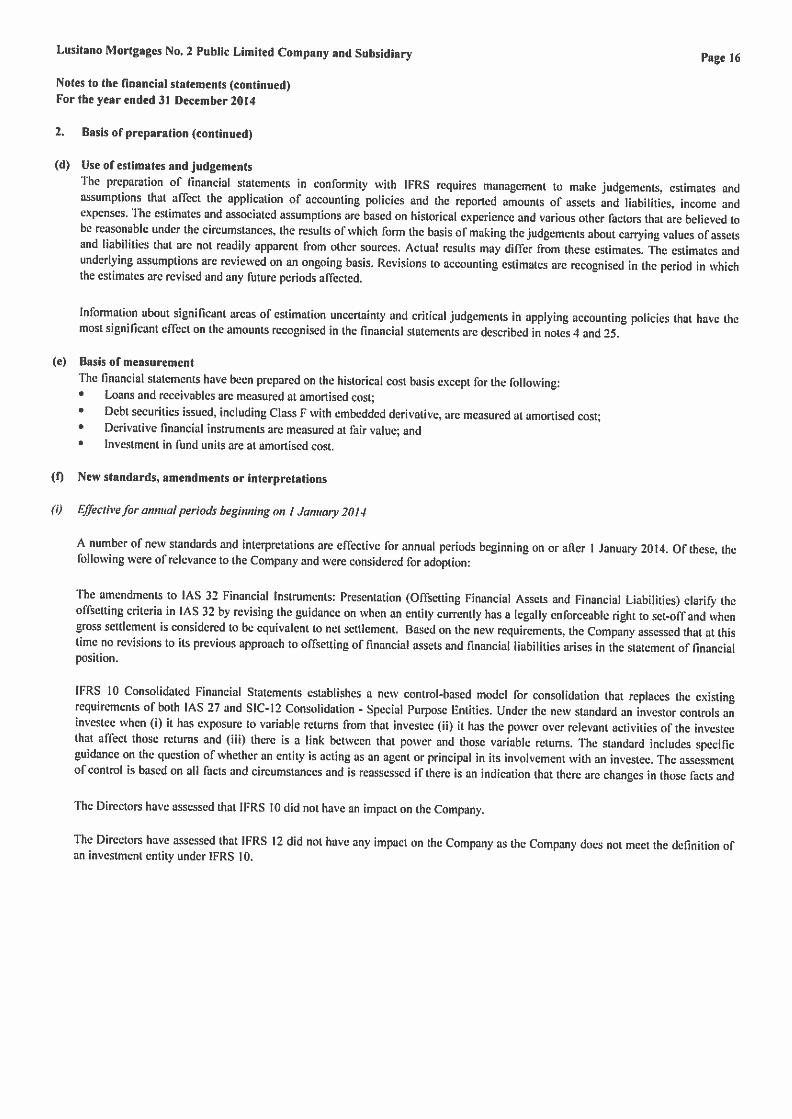

Lusitano Nlongages No.2 Public Limited Company and Subsidiary Page 16

Notes to the financial statements (continued)For the year ended 31 December 2014

2. Basis of preparation (continued)

(d) Use of estimates and judgementsThe preparation of financial statements in conformity with IERS requires management to make judgements. estimates andassumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, income andexpenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed tobe reasonable under the circumstances, the results of which form the basis of making the judgements about carrying alues of assetsand liabilities that are not readily apparent from other sources. Actual results may diflèr from these estimates. The estimates andunderlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in whichthe estimates are revised and any tUture periods affected.

Information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have themost significant effect on the amounts recognised in the financial statements are described in notes 4 and 25.

(e) Basis of measurementThe financial statements have been prepared on the historical cost basis except for the following:• Loans and receivables are measured at amortised cost;• Debt securities issued, including Class F with embedded derivative, are mcasured at amonised cost;• Derivative financial instruments are measured at fair value; and• Investment in lUnd units are at amortised cost.

(t New standards, amendments or interpretations

(D Effectivefor annual periods beginning on 1 Janua’y 2014

A number of new standards and interpretations are effective for annual periods beginning on or after I January 2014. Of these. thefollowing were of relevance to the Company and were considered for adoption:

The amendments to lAS 32 Financial Instruments: Presentation (Offsetting Financial Assets and Financial Liabilities) clarify theoffsetting criteria in lAS 32 by revising the guidance on when an entity currently has a legally enlbrceable right to set-off and whengross settlement is considered to be equivalent to net settlement. based on the new requirements. the Company assessed that at thistime no revisions to its previous approach to offsetting of financial assets and financial liabilities arises in the statement of financialposition.

IFRS 10 Consolidated Financial Statements establishes a new control-based model for consolidation that replaces the existingrequirements of both lAS 27 and SIC-12 Consolidation - Special Purpose Entities. Under the new standard an investor controls aninvestee when (i) t has exposure to variable returns from that investee (ii) it has the power over relevant activities of the investeethat affect those returns and (iii) there is a link between that power and those variable returns. The standard includes specificguidance on thc question of whether an entity is acting as an agent or principal in its involvement with an investee. The assessmentof control is based on all fUeLs and circumstances and is reassessed if there is an indication that there are changes in those facts and

The Directors have assessed that IFRS 10 did not have an impact on the Company.

The Directors have assessed that IFRS 12 did not have any impact on the Company as the Company does not meet the definition ofan investment entity under IFRS ID.

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 17

Notes to the financial statements (continued)For the year ended 31 December 2014

2. Basis of preparation (continued)

(fl New standards, amendments or interpretations (continued)

(ii) Effeethe for annual periods beginning after I Jaiu.aiy 2014

Description Effective date (periodDefined Benefit Plans: Employee Contributions (Amendments to lAS 19) I February 2015Annual Improvements to IFRSs 2010-2012 Cycle and Annual Improvements to IFRSs 2011-2013 Cycle I February 2015”Amendments to IFRS II: Accounting for acquisitions of interests in Joint Operations 1 January 2016IFRS 14: Regulatory Deferral Accounts I January 2016Amendments to lAS 16 and lAS 38: Clarification of acceptable methods of depreciation andamonisation I January 2016Amendments to lAS 16 Property, Plant and Equipment and lAS 41 Bearer Plants I January 2016Amendments to lAS 27 Equity method in Separate Financial Statements I January 2016Amendments to IFRS 10 and lAS 28: Sale or contribution of assets between an investor and itsassociate or joint venture I Januan 2016Amendments to IERS 10, IFRS 12 and lAS 28: Investment Entities: Applying the ConsolidationException I January 2016Amendments to lAS 1: Disclosure Initiative 1 January 2016Annual Improvements to IFRSs 2012-2014 C’cle I January 2016IFRS 15: Revenue from contracts with customers I Januaiw 2017IFRS 9 Financial Instruments (2009. and subsequent amendments in 2010 and 2013) I January 2018

*Where new requirements are endorsed the EU effective date is disclosed. For un-endorsed standards and interpretations, thelASH’s effective date is noted. Where any of the upcoming requirements are applicable to the Company. it will apply them fromtheir EU efTective date.

— EU endorsed

The Directors have considered the new standards, amendments and interpretations as detailed in the above table and does not plan toadopt these standards early. The application of all of these standards, amendments or interpretations will be considered in detail inadvance of a confirmed effective date by the Company. The Directors have concluded that the following may be relevant and arestill reviewing the impact of the upcoming standards to determine their impact.

lAS 24 Related Party Disclosure: This improvement relates to the identification of an entity providing key management personnel(KPM) services to the reporting entity being a related party of the reporting entity.

Amendments to lAS I: Disclosure Initiative: These amendments to lAS I Presentation of Financial statements address some of theconcerns expressed about existing presentation and disclosure requirements and ensure that the entities are able to use judgementwhere applying lAS I. The amendments relate to the following; materiality, order of the notes, subtotals, accounting policies anddisaggregation.

IFRS 9 Financial Instruments (2014): IFRS 9 Financial Instruments issued on 24 July 2014 is the IASB’s replacement of lAS 39’sFinancial Instruments: Recognition and Measurement. The Standard includes requirements tbr recognition and measurement.impairment. derecognition and general hedge accounting.

The impact of these amendments are currently under consideration by the Company.

(Ii) Segment reportingThe Group is engaged as one segment which involves investment in a portfolio of mortgage receivables in Portugal financed throughissue of debt securities. The standard on segmental reporting puts emphasis on the management approach to reporting on operatingsegments. An operating segment is a component of the Company that engages in business activities from which it may earn revenueand incur expenses. The Directors perform regular reviews of the operating results of the group and make decisions using financialinformation at the group level considering it as one entity. Accordingly the directors believe that the Company has only onereportable operating segment. The Directors are responsible for ensuring that the Company carries out business activities in line withtransaction documents. They may delegate some of the day to day management of the business to other parties both internal andexternal to the Company. The decisions of such panics are reviewed on regular basis to ensure compliance with the policies andlegal responsibilities of the Directors.

Lusitano Mortgages No.2 Public Limited Company and Subsidiary Page 18

Notes to the financial statements (continued)For the year ended 31 December 2014

3. Significant accounting policies

The accounting policies set out below have been applied consistently to all periods in these linancial statements.

(a) Income from loans and receivablesIncome from loans and receivables includes interest earned on loans and receivables which is recognised using elThctive interesi ratemethod.

The effective interest method is a method of calculating the amortised cost of a financial asset or a financial liability and ofallocating the interest income or interest expenses over the relevant period. The efThctive interest rate is the rate that exactlydiscounts estimated future cash payments and receipts through the expected lilb of the financial instrument or, when appropriate, ashorter period to the net carrying amount of the financial asset or financial liability. When calculating the effective interest rate, thecompany estimates cash flows considering all contractual terms of the financial instrument (for example. prepayment options) butdoes not consider fUture credit losses. The calculation includes all lbes and points paid or received between parties to the contractthat are an integral part of the effective interest rate, transaction costs and all other premiums or discounts.

(b) Net finance expense on debt securities issuedFinance expenses on debt securities issued held at amortised cost are charged through profit or loss using the efThctive interest ratemethod.

(c) Net gai&(loss) on derivative financial instrumentsNet gainf(loss) in derivative financial instruments relates to the interest rate swaps held by the Company for risk managementpurposes and includes realised and unrealised fair value changes. settlements and foreign exchange difThrences. It also includes fairvalue changes on derivatives which is embedded in Class F Notes.

(d) Foreign currency transactionTransactions in foreign currencies are translated to the fUnctional currency of the Company and its subsidiary’s at exchange rates atthe dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslatedto the functional currency at the exchange rate at that date. The foreign currency gain or loss on monetary items is the ditThrencebetween amortised costs in the functional currency at the beginning of the period, adjusted for effective interest and pa)ments duringthe period, and amortised cost in foreign currency translated at the exchange rate at the end of the period. Non monetary assets andliabilities denominated in foreign currencies that are measured at fair value are retranslated to the functional currency at theexchange rate at the date that the fair value was determined. Foreign currency differences arising on retranslation are recognisedthrough profit or loss in the statement of comprehensive income,

(e) Other income and expensesAll other income and expenses are accounted for on an accrual basis.

(fl Income taxIncome tax expense comprises current and deferred tax. Income tax expense is recognised in the statement of comprehensive incomeexcept to the extent that it relates to items recognised directly in equity, in which case it is recognised in equity.

Current tax is the expected tax payable on the taxable income for the year. using tax rates applicable to the Group’s and Company’sactivities enacted or substantively enacted at the balance sheet date, and adjustment to tax payable in respect of previous years.

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be available against which theasset can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longerprobable that related tax benefit will be realised.

(g) Cash and cash equivalentsCash and cash equivalents include cash in hand, deposits held at call with banks, other short-term highly liquid investments withoriginal maturities of less than three months, which are subject to insignificant risk of changes in their fair value, and are used by theCompany for the purpose of inserting in short term commitments rather than for investment or other purposes. Cash and cashequivalents are carried at amortised cost in the statement of financial position.

(h) Other receivablesOther receivables do not carry any interest and are short-term in nature and are accordingly stated at their nominal value as reducedby appropriate allowances for estimated irrecoverable amounts. Other receivables are carried at amortised cost.

Lusitano Mortgages No.2 Public Limited Company and Subsidian’ Page 19

Notes to the financial statements (continued)For the year ended 31 December 2014

3. Significant accounting policies (continued)

(i) Other payablesOther payables are not interest-bearing and are stated at amortised cost.

(j) Financini instrumentsThe financial instruments held by the Group and the Company include the following:• Loans and receivables (mortgage receivables);• Derivative financial instruments;• Debt securities issued:• Investment in fund units;• Other receivables; and• Other payables.

CategorisationThe Group and Company measures all derivative financial instruments at fair value through profit or loss at initial recognition. TheGroup and Company has classified loans and receivables. investment in fund units (loan investment) and debt securities issued as atamortised cost. Loans and receivables and loan investment arc non derivative financial assets with fixed or determinable paymentsnot quoted in active market. Other receivables and other payables are measurcd at amonised cost.

initial recognitionThe Group initially recognises all financial assets and liabilities as at fur value on the trade date at which the Group becomes a partyto the contractual provisions of the instruments. Purchases and sales of’ financial assets and financial liabilities are recognised usingtrade date accounting. From trade date, any gains and losses arising from changes in fair value of the financial assets or financialliabilities at fair value through profit or loss are recorded through profit or loss in statement of comprehensive income. Financialassets and liabilities not at fair value through profit or loss are subsequently measured at amonised cost.

DerecognitionThe Group derccognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rightsto receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards ofownership of the financial asset are transferred and does not retain control of the financial assets, Any interest in transferredfinancial assets that is created or retained by the Group is recognised as a separate asset or liability.

The Group derecognises a financial liability when its contractual obligations are discharged, cancelled or expired.

OffsettingFinancial assets and liabilities are offset and the net amount presented in the statement of financial position when, and only when,the Group has a legal right to offset the amounts and intends either to settle on a net basis or to realise the asset and settle theliability simultaneously. Income and expenses are presented on a net basis only when permitted by the accounting standards,

(k) Loans and receivablesThe loans and receivables are initially measured at fair value adjusted for initial direct costs and subsequently measured at amortisedcost, The Group’s investments in a portfolio of mortgage receivables in Portugal are classified as loans and receivables and arecarried at amonised cost using effbctivc interest method and adjusted for provision for impairment. Impairment provisions are madeto reduce the value of the loans and are written ofiwhere there is no longer any likelihood of fUture recovery of the balance.

(I) ImpairmentFinancial assets that are stated at amonised cost are reviewed at each year end date to determine whether there is objective evidenceof impairment. If an’ such indications exist. an impairment loss is recognised through profit or loss in the Statement ofComprehensive Income as the difference between the asset’s carrying amount and the present value of’ estimated fUture cash flowsdiscounted at the financial asset’s original effective rate.

If in a subsequent period the amount of an impairment loss recognised on a financial asset carried at amortised cost decreases andthe decrease can be linked objectively to an event occurring after the write-down, the write don is reversed through profit or loss inthe statement of comprehensive income.

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 20

Notes to the financial statements (continued)For the year ended 31 December 2014

3. Significant accounting policies (continued)

(m) Investment in fund units (“loan investment”)The loan investment represents an investment in a subsidiary undertaking (the Fund) which is principally backed by a pool ofmortgage receivables.

The assets of the fund comprise cash at bank, interest receivable and the mortgage loans less provision for impairment. To the extentmortgages are prepaid and repaid, these repayments are used to repay the Company’s loan investment.

(n) Derivative financial instrumentsAll changes in its fair value are recognised immediately through profit or loss in the statement or comprehensive income as acomponent of net gain or loss on derivative financial instruments carried at fair value.

Fair values are obtained from quoted market prices in active markets, including recent market transactions and valuation techniques,and discounted cash flow models and options pricing models as appropriate. Derivatives are included in assets when their fair valueis positive and liabilities when their fair value is negative, unless there is the legal ability and intention to settle net.

Profits or losses are only recognised on initial recognition of derivatives when there are observable current market transactions orvaluation techniques that are based on observable market inputs. The best evidence of the lhir value of a derivative at initialrecognition is the transaction price (i.e. the fair value of the consideration given or received) unless the tir value of that instrumentis evidenced by comparison with other observable current market transactions in the same instrument (i.e. without modification orrepackaging) or based on a valuation technique whose variables include only data from observable markets.

(0) Debt securities issuedThe debt securities issued are initially measured at fair value adjusted lbr initial direct costs and are subsequently measured at theiramortised cost using the effective interest rate method.

The amortised cost of the financial asset or liability is the amount at which the financial asset or liability is measured at initialrecognition, minus principal repayments, plus or minus the cumulative amortisation using the effective interest rate method of anydifference between the initial amount recognised and the maturity amount, minus any reduction for impairment.

Subsequent to initial recognition, these interest-bearing borrowings are stated at amortised cost with any difierence between cost andredemption value being recognised in the statement of comprehensive income over the period of the borrowings on an effectiveinterest rate basis.

(p) Embedded derivatives in Class F NotesDerivatives may be embedded in another contractual arrangement (a “host contract”). The Company accounts for an embeddedderivative separately from the host contract when the host contract is not itself carried at fair value through profit or loss, the termsof the embedded derivative would meet the definition of a derivative if it was contained in a separate contract, and the economiccharacteristics and risks of the embedded derivative are not closely related to the economic characteristics and risks of the hostcontract. However, an embedded derivative with risks and characteristics closely related to those of host contract are not separatedand accordingly is measured as part of the overall amortised cost of the related instrument.

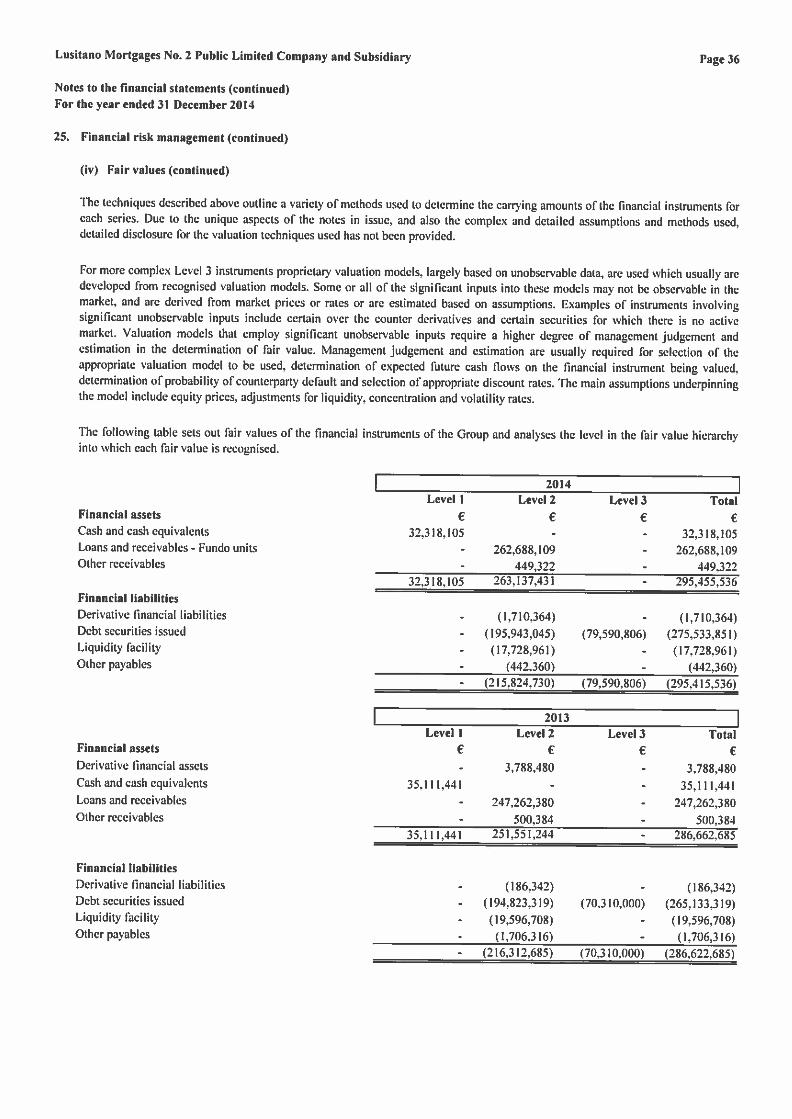

4. Determination or fair values

The determination of fair value for financial assets and liabilities for which there is no observable market price requires the use ofvaluation techniques as described in Note 25 (iv) to the financial statements. For financial instruments that trade infrequently andhave little price transparency, Ihir value is less objective, and requires varying degrees of judgement depending on liquidity,concentration, uncertainty of market factors, pricing assumptions and other risks affecting the specific instrument.

For more complex instruments, the Company uses proprietary models, which usually are developed from recognised valuationmodels. Some or all of the inputs into these models may not be market observable, and are derived from market prices or rates or areestimated based on assumptions.

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 21

Notes to the financial statements (continued)For the year ended 31 December 2014

4. Determination of fair values (continued)

Critical accounting judgements in applying the Company’s accounting policiesCritical accounting judgements made in applying thc Group’s accounting policies in relation to valuation of financial instruments isfurther described in Note 25.

Fair value measurement principlesThe determination of fair values of financial assets and financial liabilities is based on quoted market prices or dealer pricequotations for financial instruments traded in active markets, where these arc available. ha quoted market price is not available on arecognised stock exchange, the fair value of the financial instruments may be estimated by the directors based on values obtainedfrom brokers and specialist pricing vendors who may use a variety of valuation techniques such as discounted cash flow techniques,option pricing models or any other valuation techniques that provides an estimate of prices obtained should the investment be traded.If other independent prices were available Ibr the financial instruments, the valuation may be different to those presented and thosedifThrenccs could be material.

Where discounted cash flow techniques are used, estimated future cash flows are based on the directors best estimates and applyingappropriate discount rates. The discount rate used is a market rate at the statement of financial position date applicable fbr aninstrument with similar terms and conditions. Where other pricing models are used. inputs are based on market data available at thereporting date. Subsequent changes in the fair value of financial instruments at fair value through profit or loss are recognised in thestatement of comprehensive income.

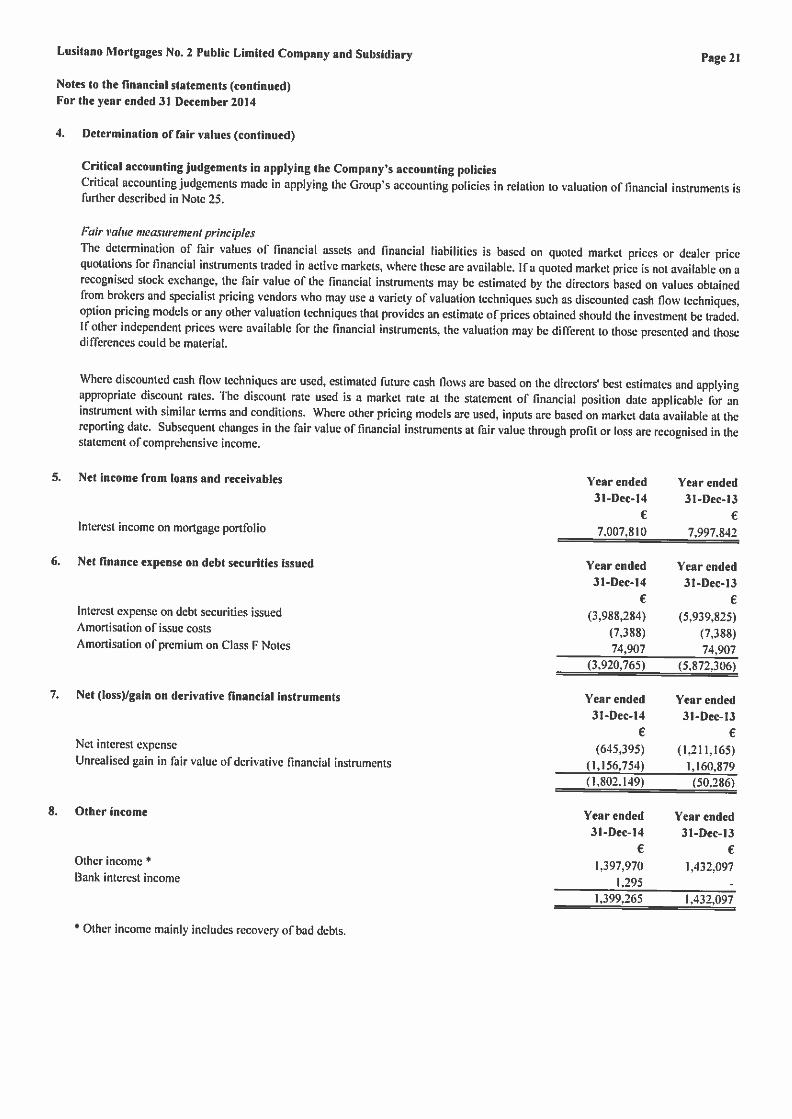

Interest income on mortgage portfolio

6. Net finance expense on debt securities issued

Interest expense on debt securities issuedAmortisation of issue costsAmortisation of premium on Class F Notes

Net interest expenseLinrealised gain in fbir value of derivative financial instruments

Other income *

Bank interest income

5. Net income from loans and receivables Year ended31-Dec-14

€

Year ended31-Dec-13

€

7. Net (loss)/gain on derivative financial instruments

8. Other income

7.007,810 7.997.842

Year ended Year ended31-Dec-14 31-Dec-13

€ €(3.988.284) (5.939.825)

(7.388) (7.388)74.907 74,907

(3,920.765) (5,872.306)

Year ended Year ended31-Dec-14 31-Dec-13

€ €(645.395) (1.211.165)

(1.156.754) 1.160,879(1,802,149) (50,286)

Year ended Year ended31-Dec-14 31-Dec-13

€ €1,397,970 1,432.097

1.2951.399.265 1.432.097

* Other income mainly includes recovery of bad debts.

Lusi(ano Mortgages Na. 2 Public Limited Company and Subsidiary Page 22

Notes to the financial statements (continued)For the year ended 31 December 2014

9. Other expenses Year ended31-Dec-14

CommissionsFund taxesTrustee feesAdministration expensesProfessional feesAudit feesAgent feesVAT expensesBank charges

(451.813)(19.821)(25.827)(26.230)(35.763)(15.990)(10.027)(11.841)

The Company is administered by Deutsche tntemationat Corporate Services (Iretand) Limited and has no employees.

Auditor’s remuneration (exclusive of VAT)

Statutory auditOther assurance servicesTax advisory servicesOther non-audit services

Balance at beginning of the yearProvision for impairment for the yearImpairment provision utitised during the ‘earBalance at end of the year

Profit before income tax

Current tax at standard rate of 25%Current tax charge

f(496.300)(27,458)(28.0221(26.230)(36.835)(15.990)(10,000)(13.978)

The Company is charged to corporation tax at a rate of 25% (2013: 25%). Theaccordance with Section 110 of the Taxes Consolidation Act, 1997.

Company will continue to be actively taxed at 25% in

Deferred tat

Any temporary difference arising on the assets will be offset by a corresponding difference in the liabilities.

All of the Companys cash balances arc held with Deutsche bank AG. London branch (99.92%) and Bank of Ireland (0.08%). AResent Fund is contained in the Reserve account to cover any revenue shortfalls in respect of an interest period.

Year ended31-Dec-13

(IS) -

(597.327) (654.813)

Year ended31-Dec-14

(13.000)

(5.500)

10. Provision for impairment loss on loans and receivables

Year ended31-Dec-13

f(13,000)

(5,500)

11. Income lax expense

(18,500) (18.500)

Year ended Year ended31-Dec-14 31-Dec-13

E €(809,710) (931,064)

(2,086.834) (2,852.534)2.162.094 2.973.888(734.450) (809710)

Year ended Year ended31-Dec-14 31-Dec-13

€ €

12. Cash and cash equivalents

Issuer operating accountResent accountFund operating accountbank of Ireland

Group31-Dec-14

€17.729.1799.000.0015.561,018

27,907

Company31-Dec-14

€

17.729.1799.000.001

€

Company31 -Dee- 13

€

19.597.2409.000.001

Group31-Dec-13

19.597.2409.000,0016.480,745

33,45535,111.441

27,907 33,45532.318,105 26,757.087 28,630.696

Refer to Note 25(i) and (ii) for credit risk and interest rate disclosures relating to cash and cash equivalents.

Lusitano Mortgages No.2 Public Limited Company and Subsidian’ Page 23

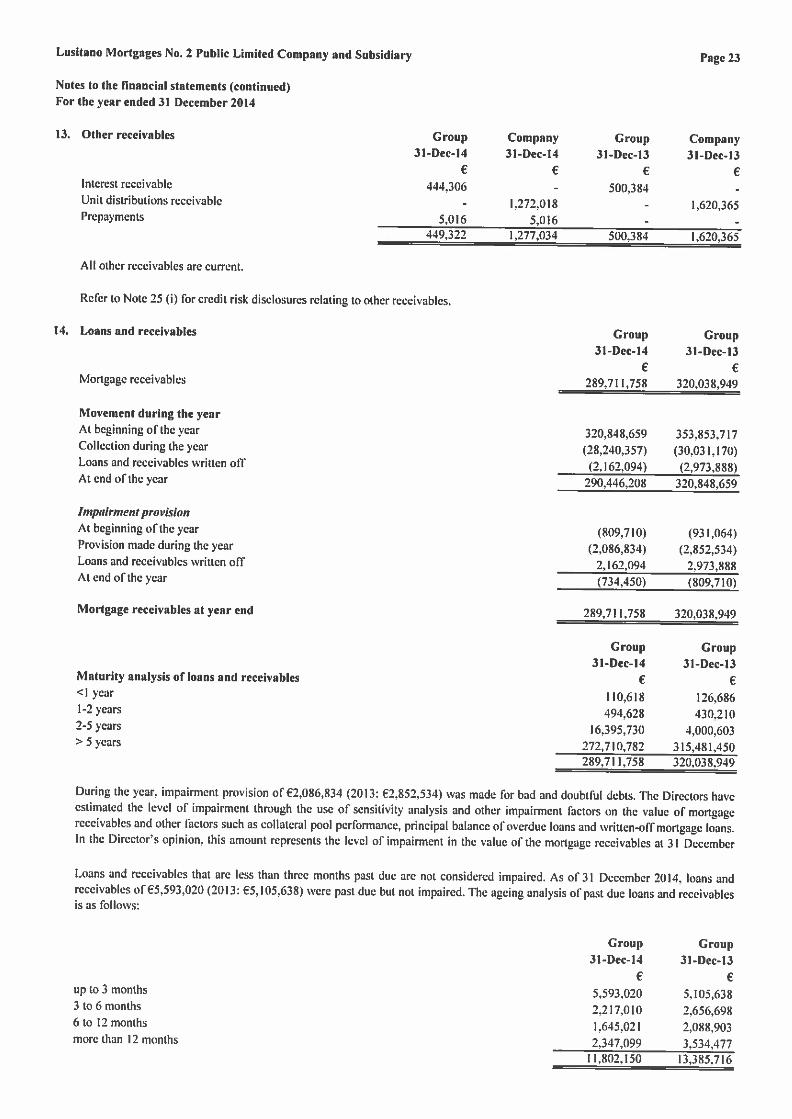

Interest receivableUnit distributions receivablePrepayments

14. Loans and receivables

Mortgage receivables

Movement during the yearAt beginning of the yearCollection during the yearLoans and receivables written offAt end of the year

Impairment provisionAt beginning of the yearProvision made during the yearLoans and receivables ‘written offAt end of the year

Mortgage receivables at year end

Maturity analysis of loans and receivables<1 year1-2 ‘ears2-5 years> 5 years

€

444.306

5,016449,322

1.272,018

€ €500.384

5.016 -

l.277.034 500.384

up to 3 months3 to 6 months6 to 12 monthsmore than 12 months

Group31-Dec-14

€

5.593,0202.217.0101.645.0212.347,099

11.802.150

Group31-Dec-13

€

5.105.6382.656.6982.088.9033.534.477

13.385.716

Notes to the financial statements (continued)For the year ended 31 December 2014

13. Other receivables Group31-Dec-14

Company31-Dec-14

Group31-Dec-13

Company31-Dec-13

€

1.620.365

All other receivables are current.

Refer to Note 25(i) for credit risk disclosures relating to other receivables.

1.620.365

Group31-Dec-14

Group31-Dec-13

€ €289.71L758 320.038,949

320.848,659 353,853.717(28,240.357) (30,03 1.170)

(2.162,094) (2.973.888)290.446.208 320,848.659

(809,710) (931.064)(2,086,834) (2,852,534)

2.162.094 2.973,888(734,450) (809.710)

289.711,758 320,038,949

Group Group31-Dec-14 31-Dec-13

U €110.618 126.686494.628 430.210

16.395.730 4,000.603272,710,782 315,481,450289.711,758 320,038.949

During the year. impairment provision of €2,086,834 (2013: €2.852.534) was made for bad and doubtful debts. ‘The Directors haveestimated the level of impairment through the use of sensitivity analysis and other impairment thctors on the value of mortgagereceivables and other factors such as collateral poc1 performance, principal balance of overdue loans and written-off mortgage loans.In the Director’s opinion, this amount represents the level of impairment in the value of the mortgage receivables at 31 December

Loans and receivables that are less than three months past due are not considered impaired. As of 31 December 2014, loans andreceivables of €5.593.020 (2013: €5.105.638) were past due but not impaired. The ageing analysis of past due loans and receivablesis as follows:

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 24

Notes to the financial statements (continued)For the year ended 31 December 2014

14. Loans and receivables (continued)

Impairment provisionAt beginning of the yearMovement during the year

__________________________________

At end of the year

Fundo Units at 31 December

Group undertakingsThe subsidiary undertaking of the Group is Lusitano Mortgages No 2 Fundo (‘the Fundo’), a Portuguese Securitisation fundincorporated under the laws of the Portuguese Republic. The Company has invested in 100% of the units of the Fundo, being IOUunits with a nominal value of LIOm each. The principal activity of the Fundo is the investment in a portfolio of mortgage

Refer to Note 25 (i) for credit risk disclosure relating to loans and receivables.

IS. Derivative financial instruments

As of3l December2014. the Company and Group’s holdings in derivative financial instruments were as specified in the table below

As of3l December 2013, the Company and Group’s holdings in derivative financial instruments were as specified in the table below

Type of contract

Interest rate swapInterest rate swap

Notional GroupFair value

of assets31-Dec-13

€ € €Euro 16 Aug 2029 319,702,969 3,788,480 3,788.480

Fair value Fair valueof liabilities of liabilities

31-Dec-13 31-Dec-13€ € €

7.127.082 (186.342) (186.342)

31-Dec-14 31-Dec-13

€ €3.602.138 2.441,259

(5.3 12,502) 1.160,879(1.710.364) 3.602.138

Under the interest rate swap agreement with CAYLON (the “swap counterpartf) on each interest payment date, until the earlier ofthe date of maturity of the debt securities issued or the date of the early repayment of the debt securities issued, the parties to theagreement will pay as follows:

Investment in Fund Units (loan investment) Company Company31-Dec-14 31-Dec-13

(‘ost € €At beginning of the year 345,116.515 374.794.506Unit principal distributions (28,860.587) (29,677,991)At end of the year 316.255,928 345.116,515

(19.817.011) (16.964.477)(2.086.834) (2.852.534)

(21.903.845) (19.817.011)

294.352,083 325.299.504

Type of contract Currency Expiration Notional Group CompanyFair value Fair value

of liabilities of liabilities31-Dec-14 31-Dec-14

€ € €Interest rate swap Euro (6 Aug 2029 319,702.969 (1.167.339) (1.167,339)Interest rate swap Euro 16 Aug 2029 7,127,082 (543.025) (543,025)

(1,710,364) (1,710,364)

Currency Expiration CompanyFair value

of assets31-Dec-13

Interest rate swap Euro 16 Aug 2029

A !oi’ement in derivative financial instruments (Group and Company)

At beginning of the yearNet changes in fair value of derivativesAt end of year

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 25

NDtes to the financial statements (continued)For the year ended 31 December 2014

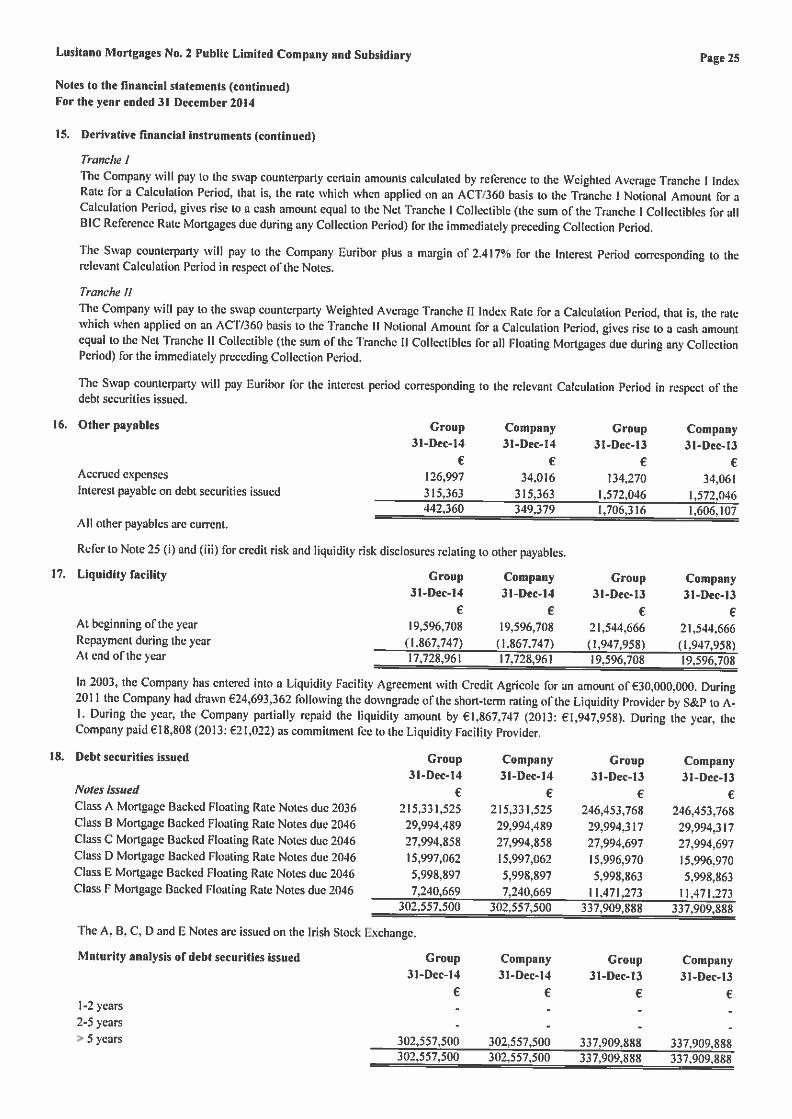

15. Derivative financial instruments (continued)

Tranciw IThe Company will pay to the swap counterpany certain amounts calculated by reference to the Weighted Average Tranche I IndexRate for a Calculation Period, that is, the rate which when applied on an ACT/360 basis to the Tranche I Notional Amount for aCalculation Period, gives rise to a cash amount equal to the Net Tranche I Collectible (the sum of the Tranche I Collectibles tbr allBIC Reference Rate Mortgages due during any Collection Period) for the immediately preceding Collection Period.

The Swap countemanv will pay to the Company Euribor plus a margin of 2.4 17% for the Interest Period corresponding to therelevant Calculation Period in respect of the Notes.

Tranche HThe Company will pay to the swap counterparty Weighted Average Tranche II Index Rate for a Calculation Period, that is, the ratewhich when applied on an ACT/360 basis to the Tranche II Notional Amount for a Calculation Period, gives rise to a cash amountequal to the Net Tranche II Collectible (the sum of the Tranche II Collectibles for all Floating Mortgages due during any CollectionPeriod) for the immediately preceding Collection Period.

The Swap counterpart will pay Euribor for the interest period corresponding to the rele’ ant Calculation Period in respect of thedebt securities issued.

16. Other payables Group Company Group Company31-Dec-14 31-Dec-14 31-Dec-13 31-Dec-13

€ € € €Accrued expenses 126,997 34,016 134,270 34.061Interest payable on debt securities issued 315.363 315,363 1.572,046 1,572.046

442,360 349.379 1,706,316 1,606.107All other payables are current.

Refer to Note 25 (i) and (iii) for credit risk and liquidity risk disclosures relating to other payables.

17. Liquidity facility Group Company Group Company31-Dec-I 4 31-Dec-I 4 31-Dec-13 31-Dec-13

€ € € €At beginning of the year 19,596.708 19,596,708 21,544,666 21,544.666Repayment during the year (1.867,747) (1.867,747) (1,947,958) (1.947.958)At end ofthe year 17,728,961 17.728,961 19.596,708 19,596,708

In 2003, the Company has entered into a Liquidity Facility Agreement with Credit Agricole for an amount of €30,000,000. During2011 the Company had drawn €24,693,362 following the downgrade of the short-term rating of the Liquidity Provider by S&P to AI. During the year. the Company partially repaid the liquidity amount by €1,867,747 (2013: €I.947.958). During the year. theCompany paid €18,808 (2013: €21,022) as commitment fee to the Liquidity Facility Provider.

IN. Debt securities issued Group Company Group Company31-Dec-14 31-Dec-14 31-Dec-13 31-Dec-13

Notes issued € € € €ClassA Mortgage Backed FloatingRateNotcsdue2o36 215.331,525 215.331.525 246.453.768 246.453.768Class B Mortgage Backed Floating Rate Notes due 2046 29.994.489 29,994,489 29,994.317 29.994.317Class C Mortgage Backed Floating Rate Notes due 2046 27,994.858 27,994,858 27.994,697 27,991,697Class D Mortgage Backed Floating Rate Notes due 2046 15,997,062 15,997,062 15.996,970 15,996,970Class E Mortgage Backed Floating Rate Notes due 2046 5,998.897 5,998,897 5.998,863 5,998.863Class F Mortgage Backed Floating Rate Notes due 2046 7.230,669 7,240.669 11,471.273 11.471.273

302,557.500 302,557,500 337,909,888 337,909,888

The A. B, C. D and E Notes arc issued on the Irish Stock Exchange.

Maturity analysis of debt securities issued Group Company Group Company31-Dec-I 4 31-Dec-I 4 31-Dec-13 31-Dec-13

€ € €1-2 ‘ears2-5 years> 5 years 302,557,500 302,557,500 337,909,888 337.909.888

302,557,500 302,557,500 337,909,888 337,909,888

Lusitano Mortgages No. 2 Public Limited Company and Subsidiary Page 26

Notes to the financial statements (continued)For the year ended 31 December 2014

IS. Debt securities issued (continued)

The Notes comprised, at issue, of €920,000.000 Class A Notes. €30.000.000 Class B Notes. €28.000.000 Class C Notes.€16,000,000 Class D Notes and €6,000,000 Class E Notes and €9,000,000 Class F Notes. Interest on the above mentioned Notes ispayable quarterly in arrears equal to the sum of EURIBOR and the Applicable Margin (as defined below) on the basis of a 360 dayyear over the actual number days elapsed. The ‘Applicable Margin’ will be as follows:

• Class A Notes: 0.21% per annum on and prior to the Step-up date (16 November 2012) and at 0.48% per annum thereafter;• Class B Notes, 0.18% per annum on and prior to the Step-up date (16 November 2012) and at 0.96% per annum thereafter:• Class C Notes, 0,64% per annum on and prior to the Step-up date (16 November 2012) and at 1.28% per annum thereafter;• Class D Notes, 1.20% per annum on and prior to the Step-up date (16November20 12) and at 2.40% per annum thereafter:• Class F Notes, 3.75% per annum on and prior to the Step-up date (16 November 2012) and at 4.75% per annum thereafter;• Class F Notes receive interest based on the remaining income of the Company after expenses.

The directors consider that the timing of the repayment of the Notes is uncertain given that the timing of such payments is dependenton the receipt of interest and principal amounts yielded by the assets. The Notes are subject to mandatory redemption in part at eachinterest payment date in an amount equal to the principal received or recovered in respect of the mortgage receivables.

If not otherwise redeemed, purchased or cancelled, the Notes will be redeemed at their principal amount outstanding on the lastinterest payment date falling in December 2036 for Class A Notes and December 2046 for Class B. C, D, F and F Notes.Accordingly. all Notes outstanding at 31 December 2014 have been classified as falling due after more than five years.

Reconciliation of debt securities issued Nominal Premium Issue costs Net proceedsInitial issuance € € F €Class A Mortgage Backed Floating Rate Notes due 2036 920,000,000 (227.948) 919,772,052Class B Mortgage Backed Floating Rate Notes due 2046 30,000.000 - (7.433) 29,992.567Class C Mortgage Backed Floating Rate Notes due 2046 28,000.000 - (6,938) 27,993.062Class U Mortgage Backed Floating Rate Notes due 2046 16,000.000 - (3,964) 15,996,036Class E Mortgage Backed Floating Rate Notes due 2046 6,000,000 - (1,487) 5.998.513Class F Mortgage Backed Floating Rate Notes due 2046 9.000,000 3,234,600 (2,230) 12.232.370

1,009,000,000 3,234,600 (250,000) 1,011,983.600

31-Dec-14Credit Cumulative Cumulative Embedded

Notes ratings Cumulative issue costs premium derivative Balance at 31issued (Moody’s) Net proceeds redemptions amortisation amortisation adjustment December 2014

€ C € € € €Class A Al 919,772,052 (704,517,324) 76,797 - - 215.331,525Class B A3 29,992,567 - 1,922 - - 29,994,489Class C Baa3 27,993.062 - 1.796 - - 27,994.858Class U BI 15.996,036 - 1.026 - - 15,997.062Class F Caa2 5,998.513 - 384 - - 5,998.897Class F Not rated 12.232.370 - 579 (836,531) (4,155,749) 7.240,669

1.011,984,600 (704.517,324) 82,504 (836,531) (4.155,749) 302,557.500

31-Dec-13

Credit Cumulative Cumulativeratings Cumulative issue costs premium Balance at 31

Notes issued (Moody’s) Net proceeds redemptions amortisation nmortisation December 2013€ € € £ F

Class A Baa3 919,772,052 (673.388.204) 69,920 - 246,453,768Class B Ba2 29,992,567 - 1.750 - 29,994.317Class C B2 27,993.062 - 1,635 - 27.994,697Class U Caal 15.996,036 - 934 - 15,996.970Class F Caa3 5,998,513 - 350 - 5,998.863Class F Not rated 12.232.370 - 527 (761,624) 11.471,273

1,011.984,600 (673,388,204) 75,116 (761,624) 337,909.888

Lusitano Mortgages No.2 Public Limited Company and Subsidiary Page 27

Notes to the financial statements (continued)For the year ended 31 December 2014

18. Debt securities issued (continued)

Reconciliation of issue costs and set up fees 31-Dec-14 31-Dec-13