long horizon investing in infrastructure - the journey ... · longhorizoninvestingininfrastructure...

TRANSCRIPT

Long horizon investing in infrastructure 1/29

Long horizon investing in infrastructureThe journey from investment beliefs to investment delegation and benchmarking

Frédéric Blanc-Brude, PhDResearch Director

EDHEC-Risk Institute

A presentation prepared for the June 2015 ICPM Discussion Forum

10 June 2015

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 2/29

Seminar structure

1. Investment beliefs

2. Agency

3. Benchmarking

4. Conclusions

5. Table assignment

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 3/29

Section outline

1. Investment beliefs1.1 2 Questions1.2 The infrastructure narrative1.3 Known evidence1.4 Nature of infrastructure assets

2. Agency

3. Benchmarking

4. Conclusions

5. Table assignment

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 4/29

Investment beliefs

Two questions:

Q1: Are the investment characteristics of infrastructure assets (debt or equity) drivenmainly by the industrial function (water supply, transport, etc.) performed by therelevant tangible infrastructure?

Q2: Should infrastructure assets be expensive (i.e. low yielding)?

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 5/29

Investment beliefs:the infrastructure investment narrative

The ”infrastructure investment narrative” (Blanc-Brude, 2013): the set of beliefscommonly held by investors about the investment characteristics of infrastructureassets. The role of infrastructure in modern societies and the nature and scale of therequired capital investments inform the following intuition:

investors in infrastructure are less exposed to business cycle because of the lowprice-elasticity of demand of the services they provide

and because the value of their investment is mostly determined by incomeprospects that extend far into the future and is little impacted by currentevents.

Sunk infrastructure investments thus create long-term value: they aremean-reverting assets par excellence.

In other words, this ideal-type implies

⋆ Improved diversification

⋆ Better liability-hedging

⋆ Less volatility than capital market valuations

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 6/29

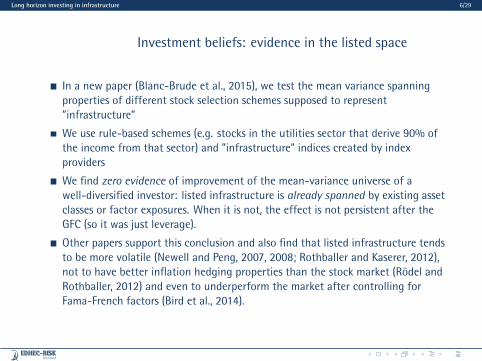

Investment beliefs: evidence in the listed space

In a new paper (Blanc-Brude et al., 2015), we test the mean variance spanningproperties of different stock selection schemes supposed to represent”infrastructure”

We use rule-based schemes (e.g. stocks in the utilities sector that derive 90% ofthe income from that sector) and ”infrastructure” indices created by indexproviders

We find zero evidence of improvement of the mean-variance universe of awell-diversified investor: listed infrastructure is already spanned by existing assetclasses or factor exposures. When it is not, the effect is not persistent after theGFC (so it was just leverage).

Other papers support this conclusion and also find that listed infrastructure tendsto be more volatile (Newell and Peng, 2007, 2008; Rothballer and Kaserer, 2012),not to have better inflation hedging properties than the stock market (Rödel andRothballer, 2012) and even to underperform the market after controlling forFama-French factors (Bird et al., 2014).

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 7/29

Are ”infrastructure” stocks already spanned?see Blanc-Brude et al. (2015)

●

●

●

●

●

●

●

Fixed Interest

Real Estate

Commodities

Hedge Funds

Developed Equities

Emerging Equities

90% Utilities

−0.05

0.00

0.05

0.10

0.15

0.20

0.00 0.05 0.10 0.15 0.20 0.25 0.30Standard Deviation

Ret

urns

Reference Assets Reference and Infrastructure Assets

Efficient Frontier January 2000 to December 2013

●●

● ●

●

●

●

Europe Stocks US Stocks

Size Value Term

Default

90% Utilities

−0.05

0.00

0.05

0.10

0.15

0.20

0.00 0.05 0.10 0.15 0.20 0.25 0.30Standard Deviation

Ret

urns

Reference Assets Reference and Infrastructure Assets

Efficient Frontier January 2000 to December 2013

●●

●

●

●

●

●

●

●

Government Bonds

Corporate Bonds

High Yield

Hedge Funds

Commodities

Real Estate

US Equities

World Ex−US Equities

FTSE Macquarie US Infra

−0.05

0.00

0.05

0.10

0.15

0.20

0.00 0.05 0.10 0.15 0.20 0.25 0.30Standard Deviation

Ret

urns

Reference Assets Reference and Infrastructure Assets

Efficient Frontier January 2000 to December 2013

●

●

●

●

●

●

Market

Size

Value

Term

Default

FTSE Macquarie US Infra

−0.05

0.00

0.05

0.10

0.15

0.20

0.00 0.05 0.10 0.15 0.20 0.25 0.30Standard Deviation

Ret

urns

Reference Assets Reference and Infrastructure Assets

Efficient Frontier February 2007 to December 2013

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 8/29

Investment beliefs: evidence in the unlisted space

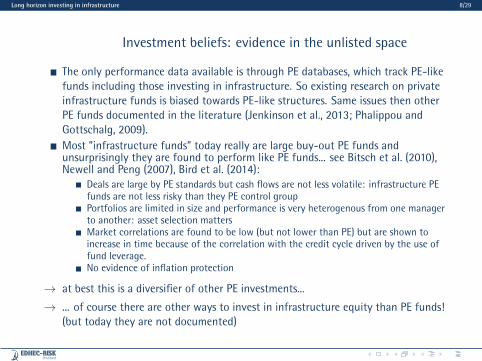

The only performance data available is through PE databases, which track PE-likefunds including those investing in infrastructure. So existing research on privateinfrastructure funds is biased towards PE-like structures. Same issues then otherPE funds documented in the literature (Jenkinson et al., 2013; Phalippou andGottschalg, 2009).Most ”infrastructure funds” today really are large buy-out PE funds andunsurprisingly they are found to perform like PE funds... see Bitsch et al. (2010),Newell and Peng (2007), Bird et al. (2014):

Deals are large by PE standards but cash flows are not less volatile: infrastructure PEfunds are not less risky than they PE control groupPortfolios are limited in size and performance is very heterogenous from one managerto another: asset selection mattersMarket correlations are found to be low (but not lower than PE) but are shown toincrease in time because of the correlation with the credit cycle driven by the use offund leverage.No evidence of inflation protection

→ at best this is a diversifier of other PE investments...

→ ... of course there are other ways to invest in infrastructure equity than PE funds!(but today they are not documented)

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 9/29

Investment beliefs: nature of infrastructure assets

The performance drivers of infrastructure investment is not about tangible assets,in fact infrastructure investment has nothing to do with real assets!→ Return to question 1: ”Are the investment characteristics of infrastructure assets

(debt or equity) driven mainly by the industrial function (water supply, transport, etc.)performed by the relevant tangible infrastructure?”

Contracts (and regulation) are everything because they determine the expectedvalue and the volatility of cash flows

The different types of risk transfer found in the contractual set up ofinfrastructure projects are found to explain the cost of capital (cost of debt)

These different factors of risk are priced and they are the main source ofpotential diversification between infrastructure projects

see Blanc-Brude and Strange (2007); Blanc-Brude and Ismail (2013); Blanc-Brude(2013)

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 10/29

Investment beliefs: the PFI portfolio

⋆ 5 listed firms mostly occupied with buying and holding the equity andsubordinated debt of PFI (private finance initiative) project companies in the UK...

Table: Total returns of the PFI portfolio, an infra index and the market, 2006-2014

pfi portoflio ftse all shares macquarie infra europe

ann. return 0.101 0.065 0.046ann. risk 0.082 0.172 0.184

ann. Sharpe ratio 1.171 0.345 0.224all price data in GBP, Datastream

Table: Maximum drawdown* of annualised returns, 2006-2014

pfi portoflio ftse all shares macquarie infra europe

Worst Drawdown 0.150 0.410 0.370*Measured as a percentage of maximum cumulative return i.e. from ”peak equity”

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 11/29

Investment beliefs: the PFI portfolio

Mar 06 Mar 07 Mar 08 Mar 09 Mar 10 Mar 11 Mar 12 Mar 13 Mar 14 Feb 15

1.0

1.5

2.0

● pfi portoflioftse all sharesmacquarie infra europe

Valu

e

total returns: growth of $1

●

●

●

●

●

●

●

UK Gilts

Real Estate

Hedge Funds

Commodities

UK Equities

World Ex−UK Equities

PFI Portfolio

−0.05

0.00

0.05

0.10

0.15

0.20

0.00 0.05 0.10 0.15 0.20 0.25 0.30Standard Deviation

Ret

urns

Reference Assets Reference and Infrastructure Assets

Efficient Frontier January 2000 to December 2013

Blanc-Brude et al. (2015)

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 12/29

What investment beliefsfor long-term investors in infrastructure?

Asset class or factors?”Infrastructure” as a heuristic→ Question 2: ”Should infrastructure assets be expensive (i.e. low yielding)?”

Contracts not concrete

Patience is not enough: long-term investment requires a (machine) learningprocess

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 13/29

Section outline

1. Investment beliefs

2. Agency2.1 2 Questions2.2 The infrastructure PE fund model2.3 Market failure2.4 Inter-temporal monitoring demand

3. Benchmarking

4. Conclusions

5. Table assignment

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 14/29

Agency

Two questions:

Q3: Amongst external infrastructure managers, have you come across attractivealternatives to the 2:20 PE infrastructure fund model?

Q4: Is the information reported today by infrastructure managers (internal orexternal) sufficient for asset owners’ purposes?

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 15/29

Agency:delegation and the infrastructure fund model

Infrastructure fund have proliferated since the 1990s

They tend to offer one possible way to gain exposure to infrastructure projects:relatively short-term and exit focused, possibly quite aggressive (extra leverage)and expensive (2:20)

This type of product has become notoriously unfashionable with large long-terminvestors...

Still, in a world with heterogenous skill endowments, there is value isspecialisation, hence, there should be value in delegation as well...

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 16/29

Agency:a pooling equilibrium (and how to get out of it)

Despite the decision to internalise infrastructure investment by very largeaccounts, the market for delegated service is not changing much...→ Question 3: Amongst external infrastructure managers, have you come across

attractive alternatives to the 2:20 PE infrastructure fund model?

There are never been so many infrastructure PE funds, with so much dry powderto invest than today

With so much competition between infrastructure managers, why aren’t newmodels emerging that offer what long-term investors actually want?

... this situation can be understood as a form of market failure (a poolingequilibrium) in which all service providers offer the same, low quality, high costproducts, because of information asymmetries between clients and managers arelarge and it is difficult (and costly) for those managers that could offer betterproducts to differentiate themselves from the crowd.

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 17/29

Agency:inventing new ways to delegate

Abandoning delegation is one way to respond to market failure...

... the other is to create ”revelation mechanism” (auctions) by which only themanagers that can actually deliver what clients want can be selected (self-select)

First investors need to define what they are after: from narrative to objectives,including the recognition that ”infrastructure” is just a heuristic

Then mandates can be auctioned so that they can reveal the service providersthat can deliver a service at the best cost

However, agency theory dictates that there is a cost to make the right agentsreveal their ’type’ - it should be compared with the full cost of not delegating(including the cost of less diversification)

Some managers may also try to ’signal’ their difference (e.g. recent formation ofindustry associations)

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 18/29

Agency:the inter-temporal monitoring demand

Long-term investing (buy and hold) increases the demand for monitoring of assetowners→ Question 4: Is the information reported today by infrastructure managers (internal or

external) sufficient for asset owners’ purposes?

Standardised data and performance reporting frameworks are needed.

Monitoring can be improved through information revelation mechanisms:well-designed delegation or cooperation (data pooling)

Monitoring is required whether there is delegation to an external manager ornot, including for performance attribution purposes

This is especially true if infrastructure investment is lumpy and takes time tobuild up: asset selection matters but claims of outperformance require a point ofreference: a benchmark!

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 19/29

Section outline

1. Investment beliefs

2. Agency

3. Benchmarking3.1 4 Questions3.2 A roadmap

4. Conclusions

5. Table assignment

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 20/29

Benchmarking:4 Questions...

1. Asset allocation: risk adjusted performance measures

2. Prudential regulation: extreme risk measures

3. ALM/LDI: duration and inflation hedging

4. ESG: investment impact measures

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 21/29

Benchmarking:...which we cannot answer today

Market proxies are ineffective

Existing research using private data is too limited

Reported metrics are inadequate

Impact metrics are not standardised and aggregated

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 22/29

Benchmarking:A roadmap (Blanc-Brude, 2014)

1. Define your terms

2. Design adequate pricing and risk models

3. Determine what data needs to be collected

4. Standardise data collection and populate a global database

5. Design useful reference portfolios

6. Track the performance of these portfolios in time

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 23/29

Benchmarking:Recent progress

1. Definitions: discussions with EIOPA

2. Asset pricing and cash flow models (Blanc-Brude et al., 2014; Blanc-Brude andHasan, 2015)

3. Data collection template (Blanc-Brude et al., 2015)

4. Data collection by EDHEC: currently 300 deals going back 20 years, 1,700+ by2017...

5. Design useful reference portfolios... (table assignment)

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 24/29

Benchmarking: Recent empirical results

Construction risk is idiosyncratic in project finance

0

10

20

30

40

50

60

70

-80 -60 -40 -20 0 20 40 60 80 100 120 140 160 180 200 220 240 260 280

Public construction risk - decision to build (Flyvbjerg dataset, n=110, 1950-2000)

Project !nance construction risk - !nancial close (NATIXIS dataset, n=75, 1993-2010)

Cash flow are lognormal in PPPs

0.0 0.5 1.0 1.5

01

23

45

density.default(x = ln_dscr)

N = 10000 Bandwidth = 0.01097

Den

sity

0 1 2 3 4 5

01

23

45

DSCR lognormal density, contracted infrastructure

N = 10000 Bandwidth = 0.0139

Den

sity

predictedactual

Greenfields diversify Brownfields...

Greeneld debt-only portfolio

Whole lifecyle debt portfolio

Portfolio Risk (percentage)

Portfolio Return(percentage)

Browneld debt-only portfolio

Lower credit risk comes at the cost of duration risk

−20 −10 0 10 20−15−10−505101520

Risk Trade−off (Rising DSCR family)

∆Duration(%)

∆Loss(%)

−20 −10 0 10 20−15−10−505101520

Risk Trade−off (Flat DSCR family)

∆Duration(%)

∆Loss(%)

see Blanc-Brude and Makovsek (2014), Blanc-Brude (2014), Blanc-Brude and Ismail (2013), Blanc-Brude et al. (2014)

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 25/29

Section outline

1. Investment beliefs

2. Agency

3. Benchmarking

4. Conclusions

5. Table assignment

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 26/29

Conclusions

Long-term investors in infrastructure are faced with a large and complexinformation problem

We can create the right tools and framework that can answer the most relevantquestions

This monitoring and benchmarking framework can be ”smart” and learnsequentially as and when new information becomes available

But it requires poling information that is otherwise scattered amongst investors

This is what EDHEC is currently implementing, but your investor input isextremely valuable.

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 27/29

Section outline

1. Investment beliefs

2. Agency

3. Benchmarking

4. Conclusions

5. Table assignment

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 28/29

Benchmarking

Table assignment:

1. What role do privately-held infrastructure assets play in the portfolio of a largewell-diversified, long-term investor? Discuss both equity and debt.

2. Given the lack of immediate investability of reference portfolios of privateinfrastructure equity or debt, what should we try to benchmark? Should wefocus on capturing the performance of an infrastructure ’asset class’ or try todocument something else? (and if yes, what could that be?)

3. Benchmarking privately-held infrastructure investments requires collectinginformation scattered amongst long-term investors on an ongoing basis. Whatwill make it worth investors’ while to participate to such an exercise?

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..

Long horizon investing in infrastructure 29/29

ReferencesBird, R., H. Liem, and S. Thorp (2014, May). Infrastructure: Real Assets and Real Returns. European Financial Management 20(4),

802–824.Bitsch, F., A. Buchner, and C. Kaserer (2010). Risk, Return and Cash Flow Characteristics of Infrastructure Fund Investments. EIB

Papers 15(1), 106–136.Blanc-Brude, F. (2013). Towards efficient benchmarks for infrastructure equity investments. EDHEC-Risk Institute Publications, 88.Blanc-Brude, F. (2014, June). Benchmarking Long-Term Investment in Infrastructure. EDHEC-Risk Institute Position Paper .Blanc-Brude, F., R. Delacroce, M. Hasan, C. Mandri-Perrot, J. Schwartz, and T. Whittaker (2015). Data collection for infrastructure

investment benchmarking: objectives, reality check and reporting framework. EDHEC-Risk Institute Position Paper .Blanc-Brude, F. and M. Hasan (2015). The valuation of privately-held infrastructure equity investments. EDHEC-Risk Institute

Publications January.Blanc-Brude, F., M. Hasan, and O. R. H. Ismail (2014). The valuation and performance of unlisted infrastructure debt. EDHEC-Risk

Institute Publications July.Blanc-Brude, F. and O. R. H. Ismail (2013). Who is afraid of Construction Risk? Portfolio Construction with Infrastructure Debt.

EDHEC-Risk Institute Publications, 128.Blanc-Brude, F. and D. Makovsek (2014). How much construction risk do sponsors take in project finance? EDHEC-Risk Institute

Publications.Blanc-Brude, F. and R. Strange (2007). How Banks Price Loans to Public-Private Partnerships: Evidence from the European

Markets. Journal of Applied Corporate Finance 19(4), 94–106.Blanc-Brude, F., S. Wilde, and T. Witthaker (2015). The performance of listed infrastructure equity: a mean-variance spanning

approach. EDHEC Business School Working Paper .Jenkinson, T., M. Sousa, and R. Stucke (2013). How Fair are the Valuations of Private Equity Funds? SSRN Electronic Journal.Newell, G. and H. W. Peng (2007). The significance and performance of retail property in Australia. Journal of Property Investment

& Finance 25(2), 147–165.Newell, G. and H. W. Peng (2008). The role of US infrastructure in investment portfolios. Journal of Real Estate Portfolio

Management 14(1), 21–34.Phalippou, L. and O. Gottschalg (2009). The performance of private equity funds. Review of Financial Studies 22(4), 1747–1776.Rödel, M. and C. Rothballer (2012). Infrastructure as Hedge against Inflation—Factor Fantasy? The Journal of Alternative

Investments 15(1), 110–123.Rothballer, C. and C. Kaserer (2012). Is Infrastructure Really Low Risk? An Empirical Analysis of Listed Infrastructure Firms.

Institute ...

.

...

.

...

.

...

.

...

.

...

.

..