local budgets study 2010 -...

TRANSCRIPT

Research Report

Local Budget Management Performance (KIPAD) 2010

1

INTERIM REPORT

LOCAL BUDGETS STUDY 2010

Local Budget Management Performance in 42 Kabupatens and Cities in Indonesia

The Asian Foundation Seknas FITRA UKaid Royal Netherlands Embassy

Translated into English by Denis Fisher

from the Depart-

ment of Internat- ional Development

Research Report

Local Budget Management Performance (KIPAD) 2010

2

Acknowledgements

This Report on Local Budget Management Performance is the result of cooperation between the National Secretariat

of the Indonesian Forum for Budget Transparency (Seknas FITRA) and The Asia Foundation. The Seknas FITRA

team was led its Secretary-General, Yuna Farhan, and included Fitra staff members Yenni Sucipto and Muhammad

Maulana. The Asia Foundation‘s contribution was coordinated by R. Alam Surya Putra and Hana Satriyo. Taufik,

Zulkarnain and Hari Kusdaryanto helped with data processing and logistics.

The Report is based on findings of fieldwork undertaken by the following local researchers from 30 civil society

organizations: Baihaqi, Yulianto and Mulyadi (GERAK Aceh), Rurita Ningrum (FITRA North Sumatra), Aryadie

Adnan and Wibawadi Murdwiono (PKSBE West Sumatra), Fahriza (FITRA Riau), Ferry Triatmodjo and Rini Budi Astuti (Maarif Institute), Muhammad Fahmi (FITRA South Sumatra), Edi Surahman (Pinus/Mapag, North

Gorontalo), Ben Satriatna (Sanggar Bandung), Khirzuddin, Syamsul, Drs. HA.Muhith Efendy and Syaiful

Mustai‘n (Lakpesdam NU), Andwi Joko Mulyanto, Eko Adi Purwanto, Arifin, Dina Nur Solati, Rosihan Widhi

Mugroho, Zaffaron, Asiswanto Darsono and Nur Hidayat (Pattiro), Nur Hadi (FITRA Tuban), Dwi Endah (PW

Aisyiyah East Java), Eka (Lensa), Denywan Putra (Legitimed), Husni Anshori (YPKM), Milita Priatna Utami

(LSBH), Zulkarnain (SOMASI) Andi Nilawati Ridha, Sudirman and Wildayanti (YLP2EM), St. Hasmah (LPP Bone),

Masitah (Yasmib), Risnawati (KPPA), Arusdin Bone (LP2G), Lim Kheng Sia (Fakta) dan Muttaqien (Labda

Jogjakarta). Members of the data verification team were: Hendriadi Jamaludin (Somasi), Rosniaty (Yasmib),

Ermy Sri Ardhiyanti (Pattiro), Devi (Maarif Institute), Nunik Handayani (FITRA South Sumatra) dan Dahkelan

(FITRA East Java) and Yenti Nur Hidayat (SANGGAR).

This research was undertaken with support from the UK Department for International Development (DFID) and The Royal Netherlands Embassy.

The opinions, findings and conclusions contained in this report are those of the civil society groups involved and should not be attributed to The Asia Foundation, DFID or the Royal Netherlands Embassy.

Research Report

Local Budget Management Performance (KIPAD) 2010

3

Table of Contents

ACKNOWLEDGEMENTS 2

LIST OF TABLES AND ILLUSTRATIONS 5

GLOSSARY OF ABBREVIATIONS AND TERMS 6

CHAPTER I: FOREWORD: A MORE DETAILED LOOK AT LOCAL BUDGET PROCESSES 8

A. Background 9

B. Research Methodologies 9

1. Research Instrument and Scoring System 10

2. Research Structure and Methods 10

3. Documents Studied 10

4. Reliability and Validity 10

5. Index Categorization 12

C. Areas Studied 12

CHAPTER II: PERFORMANCE IN TRANSPARENCY OF LOCAL BUDGET

MANAGEMENT 14

A. Testing the Availability of Budget Documents 14

B. Institutional Support for Freedom of Information Services 17

C. Index of Transparency of Local Budget Management 18

CHAPTER III: PERFORMANCE IN PARTICIPATION IN LOCAL BUDGET MANAGEMENT

20

A. Mechanisms for Participation and Categories of Participants 20

B. Regulatory Provisions on Public Participation 22

C. Index of Participation in Local Budget Management 23

CHAPTER IV: PERFORMANCE IN ACCOUNTABILITY OF LOCAL BUDGET

MANAGEMENT 25

A. Timeliness 26

B. Mechanisms for Supply of Goods and Services 27

C. Opinions of National Audit Board 28

D. Index of Accountability of Budget Management 28

Research Report

Local Budget Management Performance (KIPAD) 2010

4

CHAPTER V: PERFORMANCE IN PROMOTING EQUALITY IN LOCAL BUDGET

MANAGEMENT 30

A. Special Mechanisms for Womens Participation 30

B. Institutionalization of Gender Mainstreaming 30

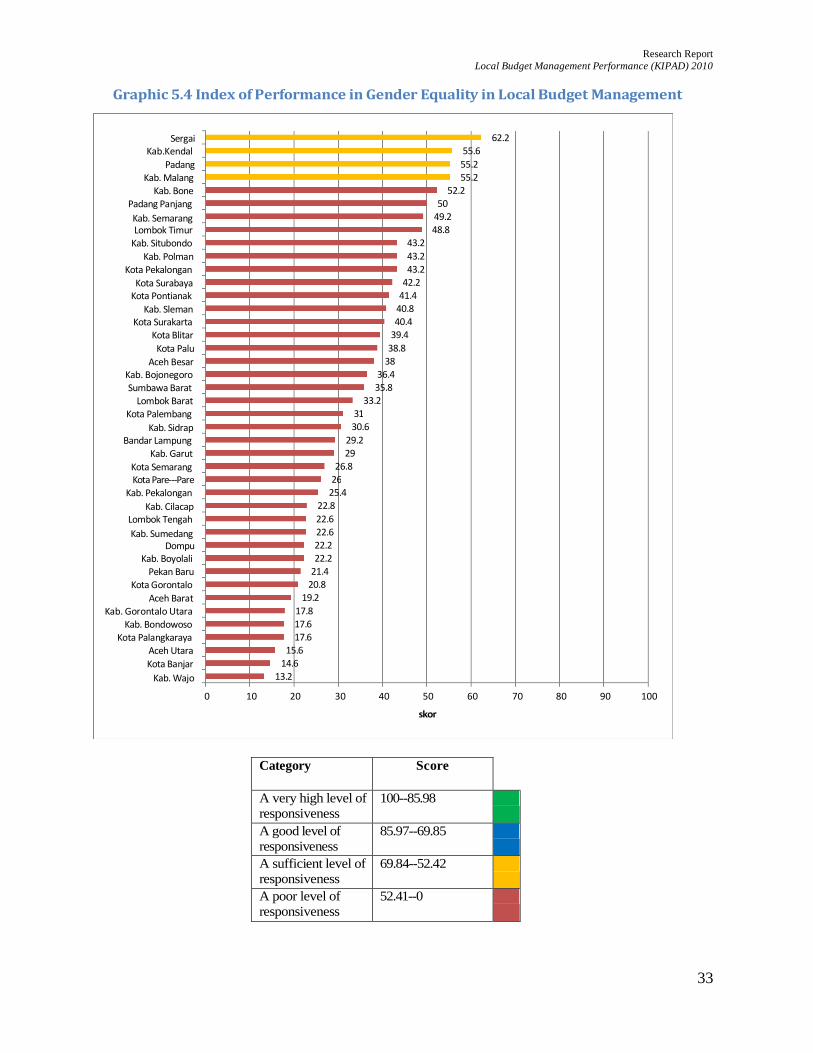

C. Index of Performance in Gender Mainstreaming 32

CHAPTER VI: PERFORMANCE IN LOCAL GOVERNMENT MANAGEMENT 34

CHAPTER VII: RECOMMENDATIONS 37

Research Report

Local Budget Management Performance (KIPAD) 2010

5

List of Tables and Graphics

TABLE 1.1 Documents Studied for KIPAD 2010 10

TABLE 1.2 Reliability of Dimensions and Cycles 11

TABLE 1.3 Correlations between Dimensions 11

TABLE 1.4 Correlations between Cycles 12

TABLE 1.5 Categorizations of Ratings of Areas Studied 12

TABLE 4.1 Regulatory Framework for Deadlines for Final Approval of Budget Documents 26

TABLE 4.2 Regulatory Framework for Timeframes for Discussion of Budget Documents 26

TABLE 4.3 Extent to Which Governments Studied Met Deadlines for Final Approval of Budget Documents 26

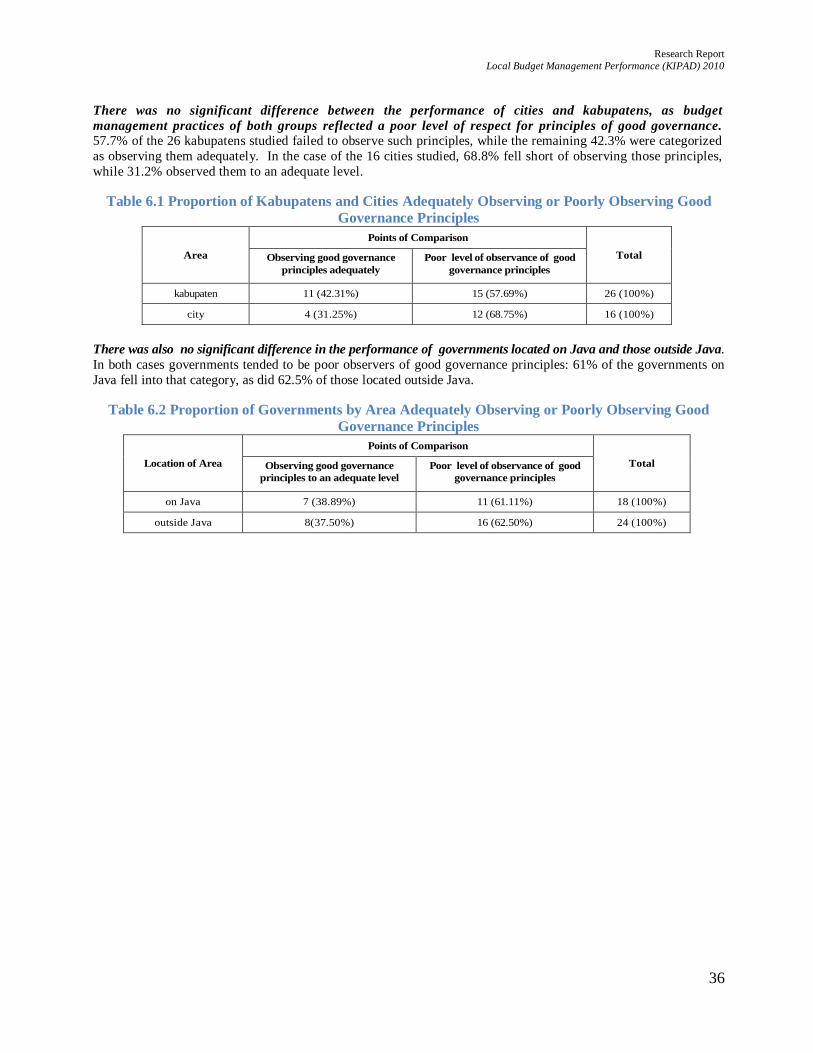

TABLE 6.1 Proportion of Local Govts Observing or Not Fully Observing Good Governance Principles 36

TABLE 6.2 Proportion of Govts by Area Observing or Not Fully Observing Good Governance Principles 36

GRAPHIC 1.1 Areas Studied in KIPAD 2010 ...................................................................................................................................... 13

GRAPHIC 2.1 Level of Public Access to Documents by Local Government Area.............................................................. 15

GRAPHIC 2.2 Degrees of Access to Budget Documents .............................................................................................................. 16

GRAPHIC 2.3 Time Taken to Provide Documents............................................................................................................................. 16

GRAPHIC 2.4 Level of Accessibility of Budget Documents by Budget Cycle Phase ..................................................... 16

GRAPHIC 2.5 Level of Access to Budget Documents by Title .................................................................................................... 17

GRAPHIC 2.6 Areas with or without SOPs for FOI Requests ..................................................................................................... 18

GRAPHIC 2.7 Index of Performance in Transparency of Local Budget Management ...................................................... 19

GRAPHIC 3.1 Mechanisms for Participation Provided by 42 Governments Studied ......................................................... 21

GRAPHIC 3.2 Community Involvement by Consultative Mechanism Provided ............................................................... 21

GRAPHIC 3.3 Differences between Participation Index of Areas with PIKs and those without PIKs ........................ 22

GRAPHIC 3.4 Proportion of Areas Providing Mechanisms for Participation by Budget Cycle Phase

............................................................................................................................................................ 22

GRAPHIC 3.5 Index of Performance in Participation in Local Budget Management........................................................ 24

GRAPHIC 4.1 Ways Used to Advertise Tenders in the 42 Kabupatens and Cities Studied ........................................... 27

GRAPHIC 4.2 Availability of Black Lists of Companies in the 42 Kabupatens and Cities Studied ......................... 27

GRAPHIC 4.3 Index of Performance in Accountability of Local Budget Management ................................................ 29

GRAPHIC 5.1 Establishment of Gender Mainstreaming Institutions ................................................................ 31

GRAPHIC 5.2 Use of Disaggregated Data for Certain Programs ............................................................................................. 31

GRAPHIC 5.3 Proportion of Local Government Departments Headed up by Females ..................................................... 31

GRAPHIC 5.4 Index of Performance in Gender Equality in Local Budget Management .................................................. 33

GRAPHIC 6.1 Performance in Local Budget Management Based on Good Governance Principles ....................... 34

GRAPHIC 6.2 Index of Performance in Local Budget Management ........................................................................................ 35

Research Report

Local Budget Management Performance (KIPAD) 2010

6

Glossary of Abbreviations and Terms

(Compiled and inserted by translator) APBD (or APBD murni) Anggaran Pendapatan dan Belanja Daerah—regional (local) government budget as approved

APBD-P Anggaran Pendapatan dan Belanja Daerah (Perubahan)—revised local government budget

BPK Badan Pemeriksa Keuangan Republik Indonesia—national Audit Board

CSIAP Civil Society Initiative against Poverty

DPA Dokumen Pelaksanaan Anggaran—budget implementation document

DPA SKPD Pen/Kes/PU Dokumen Pelaksanaan Anggaran Satuan Kerja Peringkat

Daerah/Pendidikan/Kesehatan/Pekerjaan Umum—budget implementation document of the

local government departments of education/health/public works

DPRD Dewan Perwakilan Rakyat Daerah—regional (local) legislative assembly: the legislative

wing of government at the provincial, kabupaten and city level

FGD Focus group discussion

FOI freedom of information

GBRI Gender Sensitive Budget Imitative

GM Gender mainstreaming

HoG head of (local) government

ILPPD Informasi Laporan Pelaksanaan Pemerintahan Daerah—information on regional

governance implementation report. See also LPPD.

Kabupaten The name of Indonesian local government area below the level of province and equal in status to a city.

KIPAD Kinerja Pengelolaan Anggaran Daerah—Local Budget Management Performance

KUA-PPAS Kebijakan Umum Anggaran–Prioritas dan Plafom Anggaran Sementara—General Budget

Policies – Provisional Budget Priorities and Funding Levels

Laporan Realisasi Smt I Laporan Realisasi Semester I—report on implementation of local budget (APBD) for the first semester.

LKPD Laporan Keuangan Pemerintah Daerah—Local Government Fiscal Report

LKPJ Laporan Keterangan Pertanggung Jawaban—Accountability Information Report

Local government any sub-national government (provincial, kabupaten and city) (pemerintah daerah)

LPPD Laporan Penyelenggaraan Pemerintahan Daerah—Regional Governance Implementation

Report

Musrenbang Musyawarah Perencanaan Pembangunan—community consultations on development

planning

Perda Peraturan Daerah—local government regulation

Perda PTJ Pelaksanaan APBD Peraturan Daerah Pertanggung jawaban Pelaksanaan APBD—local government regulation on

accountability of local budget implementation

Perkada Peraturan Kepala Daerah—head of local government regulation

Perkada Penjabaran APBD Peraturan Kepala Daerah Penjabaran APBD—head of local government regulation on

detailed implementation of local budget

Perkada Penjabaran APBD-P Peraturan Kepala Daerah Penjabaran APBD-Perubahan—head of local government

regulation on detailed implementation of the revised local budget

Permendagri Peraturan Menteri Dalam Negeri—Minister of Home Affairs regulation

PIK Pagu Indikatif tingkat kecamatan—indicative funding figures at sub-district level

PKK Pemberdayaan Kesejahteraan Keluarga—empowerment of family welfare

Pokja Kelompok Kerja—working group

Research Report

Local Budget Management Performance (KIPAD) 2010

7

Posyandu Pos Pelayanan Terpadu—integrated health post

PP Peraturan Pemerintah—central government regulation

PPID Pejabat Pengelolaan Informasi dan Dokumentasi—Office for the Management of Information

and Documentation (Freedom of Information (FOI) office)

Region any sub-national area (particular government areas: provinces, kabupatens and cities)

Regional government any sub-national (local) government at the level of province, kabupaten or city

Renja SKPD Pemda Rencana Strategis Satuan Kerja Peringkat Daerah Pemerintah Daerah—strategic plans of

local government departments

Renja SKPD Kes/PU/Pen Rencana Strategis Satuan Kerja Peringkat Daerah Pemerintah Daerah Kesehatan/Pekerjaan

Umum/Pendidikan—Strategic plans of local government departments of health/public

works/education

RAPBD Rancangan Anggaran Pendapatan dan Belanja Daerah—draft local government budget

RAPBD-P Rancangan Anggaran Pendapatan dan Belanja Daerah (Perubahan)—draft revised local

government budget

RKA Rencana Kerja dan Anggaran—Budget and Work Plans

RKPD Rencana Kerja Pemerintah Daerah—Local Government Work Plans

RPJMD Rencana Pembangunan Jangka Menengah Daerah—regional medium-term development plan

SKPD Satuan Kerja Pemerintah Daerah—local government department (work unit)

SOP Standard Operation Procedures

Sub-district Kecamatan: administrative level immediately below kabupaten and cit y

UU (KIP) Undang Undang No. 14/2008 (Keterbukaan Informasi Publik)—law on Freedom of Information

Research Report

Local Budget Management Performance (KIPAD) 2010

8

Chapter I

Foreword: A More Detailed Look at Local Budget Processes

A. Background

This report on Local Budget Management Performance (KIPAD) in 2010 is a continuation of

research undertaken last year on the same broad issues. The study examines four broad areas of sub-national (regional, local) government budgetary processes: planning when local governments undertake a

range of activities to plan what needs to be done and to prepare draft budgets; discussion when

governments discuss and make determinations about provisions of draft budgets; implementation during which governments carry out programs contained in endorsed budgets with funding appropriations

contained therein; and, finally, accountability at which point governments have to account for

implementation of budget programs and expenditure.

This KIPAD research project was the brainchild of a network of NGOs which also developed and

implemented it as a means of monitoring and evaluating local government budget performance.

With support from The Asia Foundation, the National Secretariat of the Indonesian Forum for Budget Transparency (Seknas FITRA) organized the various research stages in collaboration with 28 like-minded

groups in regional areas, including NGOs, other community groups and university research units.

The research’s overall aim was to assess the extent to which principles of good governance

(transparency, participation, accountability and gender equality) were being integrated into local

budgetary processes in areas studied. More specifically, it aimed to provide feedback to local governments to help them to lift their performance in budgetary cycles from start to finish. By looking at

this report, local governments will be able to tell to what extent their budgetary processes are in accord with

requirements outlined and to benchmark innovative practices put in place by other governments. The

central government will hopefully also use the study as a chance to have a fresh look at national policies for improved sub-national budget performance throughout Indonesia. NGOs too should be able to use it as a

resource for their advocacy work, particularly on budgetary issues—especially pro-poor advocacy on

budgets in areas studied.

This report is based on the premise that decentralization can be relied upon to give local governments space

to develop innovative policies in regions. Since decentralization was introduced in Indonesia, several

innovative policies have been developed in regions aimed at enhancing people‘s welfare. Such innovations do not just benefit areas which introduce them, but also encourage other regions to adopt similar or even

more progressive policy approaches. So, at the very least, this report seeks to engender a spirit of

competition among local governments to help them become more efficient and effective managers—especially of their budgets.

Research Report

Local Budget Management Performance (KIPAD) 2010

9

As budgets are an integral part of political process, they act as a vehicle for both executive and

legislative branches of local governments to

implement pro-people policies and programs. Any

region‘s development depends in no small part on political decisions on budgetary issues. Thus a key

factor determining people‘s well-being is the extent to

which executive and legislative branches of local

governments have the same perspectives on how local budgets should be framed. In other words, budgets

determine the welfare of local communities.

In making judgments on the various indicators

researched in this report, researchers looked more

deeply at issues involved than in last year’s study.

Thus to test transparency, researchers used legal

provisions in freedom of information (FOI) legislation (known as UU KIP) and regulations to gain access to

information. To test participation in budgetary processes,

they identified—more carefully than last year—who was involved in budgetary planning and formulation

processes. A closer study was also made of

accountability of public tendering for supply of goods and services. And, finally, on gender issues,

they more closely assessed how effective

institutional and other arrangements were in

promoting greater gender equality.

B. Research Methodology

The basic methodology used for KIPAD 2010 was

similar to that used in the 2009 study. Research

tools and indicators used this time were the same as for

the previous study.

But the research methodology used in 2009 was fine-tuned a little for KIPAD 2010. The changes

(outlined in the following paragraphs) were based on

inputs from various quarters, in particular local

governments and NGOs, after publication of the first report.

1. Research Instrument and Scoring System

KIPAD 2010’s survey instrument contained 97 questions. These were designed to cover four elements

or dimensions regarded as representative of good governance: transparency (42 questions), participation

(15 questions), accountability (15 questions) and gender equality (25 questions). Each dimension was examined at various stages of the budgetary process, including planning (28 questions), discussion (24

questions), implementation (28 questions) and accountability (17 questions).

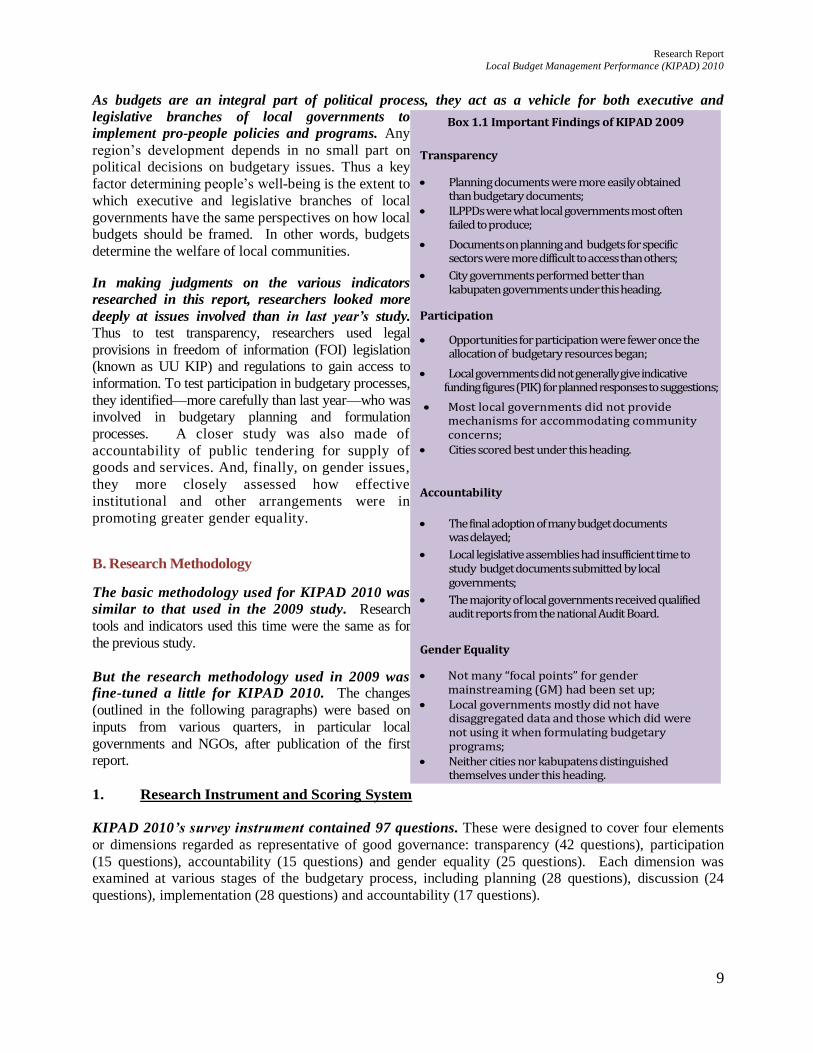

Box 1.1 Important Findings of KIPAD 2009

Transparency

Planning documents were more easily obtained than budgetary documents;

ILPPDs were what local governments most often failed to produce;

Documents on planning and budgets for specific sectors were more difficult to access than others;

City governments performed better than kabupaten governments under this heading.

Participation

Opportunities for participation were fewer once the allocation of budgetary resources began;

Local governments did not generally give indicative funding figures (PIK) for planned responses to suggestions;

Most local governments did not provide mechanisms for accommodating community concerns;

Cities scored best under this heading.

Accountability

The final adoption of many budget documents was delayed;

Local legislative assemblies had insufficient time to study budget documents submitted by local governments;

The majority of local governments received qualified audit reports from the national Audit Board.

Gender Equality

Not many “focal points” for gender mainstreaming (GM) had been set up;

Local governments mostly did not have disaggregated data and those which did were not using it when formulating budgetary programs;

Neither cities nor kabupatens distinguished themselves under this heading.

Research Report

Local Budget Management Performance (KIPAD) 2010

10

Available choices under each question were allocated a value (with the lowest score being 0 and the highest 100). Every question carried equal weight in index calculation, which ipso facto meant that each

index ranged between 0 and 100. That made them easy to read and compare. An area‘s overall budget

performance (KIPAD) index was calculated by taking the average of the answers to all 97 questions. The same applied to calculation of indices for each element of good governance (transparency,

participation, accountability and gender equality).

2. Research Structure and Methods

In line with the evidence-based approach used in this research, all answers had to be supported by solid evidence. Various tools were used to verify answers given: documentary evidence, interviews and focus group discussions (FGD). Every region studied had a specially trained assessor, who evaluated

research done on the area concerned. Following that evaluation, assessors sent their findings to verifiers

whose job it was not just to verify answers given but also to assess the extent to which supporting

evidence was compelling. Verifiers—positioned by geographical area—were each responsible for between 5 and 8 assessors. No verifier could double as an assessor and making ―expert judgments‖ was

the preserve of verifiers.

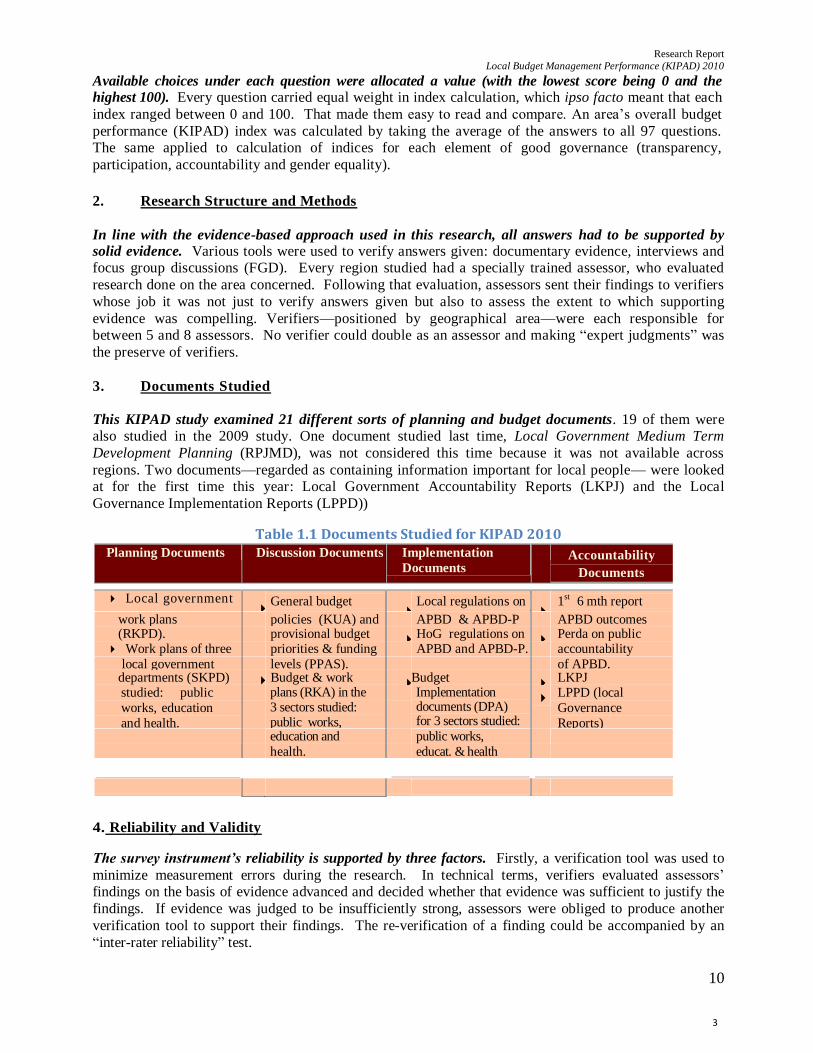

3. Documents Studied

This KIPAD study examined 21 different sorts of planning and budget documents. 19 of them were also studied in the 2009 study. One document studied last time, Local Government Medium Term

Development Planning (RPJMD), was not considered this time because it was not available across

regions. Two documents—regarded as containing information important for local people— were looked at for the first time this year: Local Government Accountability Reports (LKPJ) and the Local

Governance Implementation Reports (LPPD))

Table 1.1 Documents Studied for KIPAD 2010 Planning Documents Discussion Documents Implementation

Documents

Accountability

Documents

Pertanggungjawaba

n

Local government

wo General budget

Local regulations on

1st 6 mth report

work plans policies (KUA) and APBD & APBD-P APBD outcomes (RKPD). provisional budget HoG regulations on Perda on public Work plans of three priorities & funding APBD and APBD-P. accountability

local government levels (PPAS). of APBD.

departments (SKPD) Budget & work Budget

Implementation LKPJ

studied: public

works, education

and health.

plans (RKA) in the 3 sectors studied: public works,

Implementation documents (DPA) for 3 sectors studied: studied : public

LPPD (local

Governance

Reports) education and

health.

public works,

educat. & health

4. Reliability and Validity

The survey instrument’s reliability is supported by three factors. Firstly, a verification tool was used to

minimize measurement errors during the research. In technical terms, verifiers evaluated assessors‘ findings on the basis of evidence advanced and decided whether that evidence was sufficient to justify the

findings. If evidence was judged to be insufficiently strong, assessors were obliged to produce another

verification tool to support their findings. The re-verification of a finding could be accompanied by an

―inter-rater reliability‖ test.

3

Research Report

Local Budget Management Performance (KIPAD) 2010

11

A second source of support for our research instrument’s reliability is the “split-half test”. For a

research instrument containing 97 questions like that used in this study, it is more appropriate to use the split-half test than the so called Chronbach‘s Alpha test. The latter is sensitive to the number of

questions asked, whereas the split-half test produced a correlation of 0.731 between two sections of the

instrument. That can be regarded as a strong correlation.

A third source of support for the survey form’s reliability comes from calculation of Chronbach’s

Alpha coefficients in the imaginary situation where the survey’s 4 segments (each with its 4 cycles)

are regarded as distinct research instruments. Table 1.2 shows that, in that situation, all 4 instruments

have a satisfactory level of reliability and that even in the case of accountability which has the lowest Alpha values those values can be regarded as moderate.

Table 1.2 Reliability of Dimensions and Cycles

Instrument Total No. of Questions Chronbach’s Alpha

Transparency 42 0.911 Participation 15 0.793 Accountability 16 0.575

Equality 25 0.877 Planning Cycle 28 0.779 Discussion Cycle 24 0.862 Implementation Cycle 28 0.827 Accountability Cycle 18 0.824

The research instrument’s validity is supported by the solid foundations on which its composition

was based. Various legal requirements (enshrined in State law and regulations) were factored into their formulation in so far as they had a direct bearing on research content and validity. An attempt

was made to ensure that every question was formally correct, thereby guaranteeing that the research

instrument would elicit the information which it was intended to elicit and was therefore ―valid‖.

A second argument supporting the research instrument’s validity emerges when its four dimensions

(each with its four cycles) are regarded as separate research instruments. When that is done, it becomes

evident that the four dimensions and cycles studied are in fact interrelated in ways in which they should interrelate in theory. Such interrelationships are evidence of a high level of convergent validity. Tables

1.3 and 1.4 provide details of the correlations between the four dimensions and cycles.

Table 1. 3 Correlations between Dimensions

Transparency Participation Accountability Equality

Transparency

1 .334* .336

* .801

**

Participation 1 .516**

.458**

Accountability 1 .416**

Equality 1

Research Report

Local Budget Management Performance (KIPAD) 2010

12

Table 1.4 Correlations between Cycles

Planning Discussion Implementation Accountability

Planning 1 .652**

.719**

.537**

Discussion

1 .718**

.621**

Implementation 1 .641**

Accountability

1

5. Index Categorization

Unlike the 2009 KIPAD, this study attempts to break new ground by categorizing areas studied as

“very good”, “good”, “adequate” or “poor”. These categorizations were arrived at on the basis of

expert judgment. Specifically, researchers answered every question in the questionnaire and made judgments about what answers they might well have expected to receive. For example, on question

No.1 concerning public access to regional Government Work and Budget Plans (RKPDs), researchers

would take the view that, given its importance, a ―very good‖ government should have made this document available within 1-10 days, a ―good‖ government within 11-17 days and an ―adequate‖ one

sometime after 17 days. By contrast, in response to question No. 79 on when local governments

presented revised budgets (APBD-P) to local legislative assemblies (DPRDs), a ‗very good‖ performance would have been ―before October‖, while submission ―during October‖ would be

regarded as ―good‖ or ‖satisfactory‖.

This method of categorization was assessed as being superior to a method which arbitrarily attributed values to differing performance levels. Use of ―expert judgment‖ allowed researchers to

apply their knowledge to local situations and to make judgments about them based on existing

regulatory requirements. By contrast the ―arbitrary values approach‖ was regarded as not sufficient ly sensitive to differing local dynamics or to the extent to which local situations were in accord or not

with what researchers might have expected to find. Table 1.4 allocates values to various categories

within the KIPAD index.

Table 1.5 Categorization of Ratings of Areas Studied

Category Index rating Transparency

Index rating Participation

Index rating Accountability

Index rating Equality

KIPAD Index

Overall Rating V. good 84.17 –100 77 –100 94.33 –100 89.40 –100 85.98 –100 Good 67.98 – 84.16 66.33 – 76.99 76 – 94.32 71.40 – 89.39 69.85 – 85.97 Adequate 50.24 – 67.97 52.33 – 66.32 50.67-‐75.99 57.20 – 71.39 52.42 – 69.84 Poor 0–50.23 0–52.32 0–50.66 0–57.19 0–52.41

C. Areas Studied This research was conducted in 42 kabupatens and cities marked on the following map (see Graphic1.1)

The areas studied were target areas of the Civil Society Initiative against Poverty (CSIAP) and the Gender-Responsive Budget Initiative (GBRI) developed by The Asia Foundation with local partners. CSIAP and

GBRI had virtually the same objectives, namely to bolster the role of civil society groups (both NGOs and

other community organizations) in changing local budgetary policies to make them more pro-poor and gender-responsive. CSIAP was supported by the UK Department for International Development (DFID)

and GBRI by the Royal Netherlands Embassy.

Research Report

Local Budget Management Performance (KIPAD) 2010

13

Graphic1.1 Areas Studied in KIPAD 2010

AREAS STUDIED IN KIPAD 2010

Research Report

Local Budget Management Performance (KIPAD) 2010

14

Chapter II

Performance in Transparency of Local Budget Management

Law No. 14/2008 on Freedom of Access to Public Information (UU KIP) is based on article 23, paragraph (1) of

the Constitution which states that the State budget shall be implemented in an open and accountable manner in

order to best attain the prosperity of the people. UU KIP guarantees the right of every citizen to obtain

information from public institutions including sub-national governments, including information and documents on

budget management. The following formal legal provisions require that budget management processes be

transparent:

1. Article 23 of the 1945 Constitution: ―The State Budget, as the basis of the management of state funds, shall be determined annually by law and shall be implemented in an open and accountable manner in order to best

attain the prosperity of the people‖

2. Article 3 paragraph (1) of Law 17/2003 concerning State Finances: ―The nation‘s finances shall be

managed in an orderly way, in accordance with the provisions of law, efficiently, economically, effectively, transparently and accountably, keeping justice and propriety front and centre.‖

3. Article 5 of Law No. 10/2004 concerning Enactment of Legislation: ―The formulation of regulations issued

to enact legislation must be based on good principles of law enactment which include clarity of objectives, appropriate institutional arrangements, consistency of content, ability to be implemented, ease of use,

outcomes-focused, clarity of formulation and transparency‖.

4. Article 23 paragraph (2) of Law No. 32/2004 concerning Regional Government: ―The management of regional government finances referred to paragraph (1) shall be conducted efficiently, effectively,

transparently, accountably, correctly, justly, appropriately and in conformity with law.

5. Article 4 of Government Regulation No. 58/2005 concerning Management of Regional Government

Finances: ―Regional government finances shall be managed correctly, in accordance with law, efficiently,

effectively, transparently and accountably, keeping in mind principles of justice, propriety and being of

benefit to the people.

Two indicators were used in this study to measure transparency performance. Firstly, to test observance of

the law on FOI (UU KIP), the study sought to assess how readily budget management documents were made

publicly available. Second, the extent to which local governments had made institutional arrangements to service FOI requests from the public was assessed. Both these indicators aimed at assessing the level of local

governments‘ transparency in terms of both their granting of routine public access to information at each part

of the budget cycle and their being prepared to implement UU KIP‘s provisions.

A. Testing the Availability of Budget Documents

The study tested freedom of access to public information using the procedures for making FOI requests laid down in UU KIP. Responses were sorted into several categories: documents already in the public domain;

documents made available within 0-10 working days of receipt of requests; documents provided within 11-17

working days of lodgment of requests; documents supplied after more than 17 days; documents produced internally

but not provided publicly; and documents not produced at all.

Research Report

Local Budget Management Performance (KIPAD) 2010

15

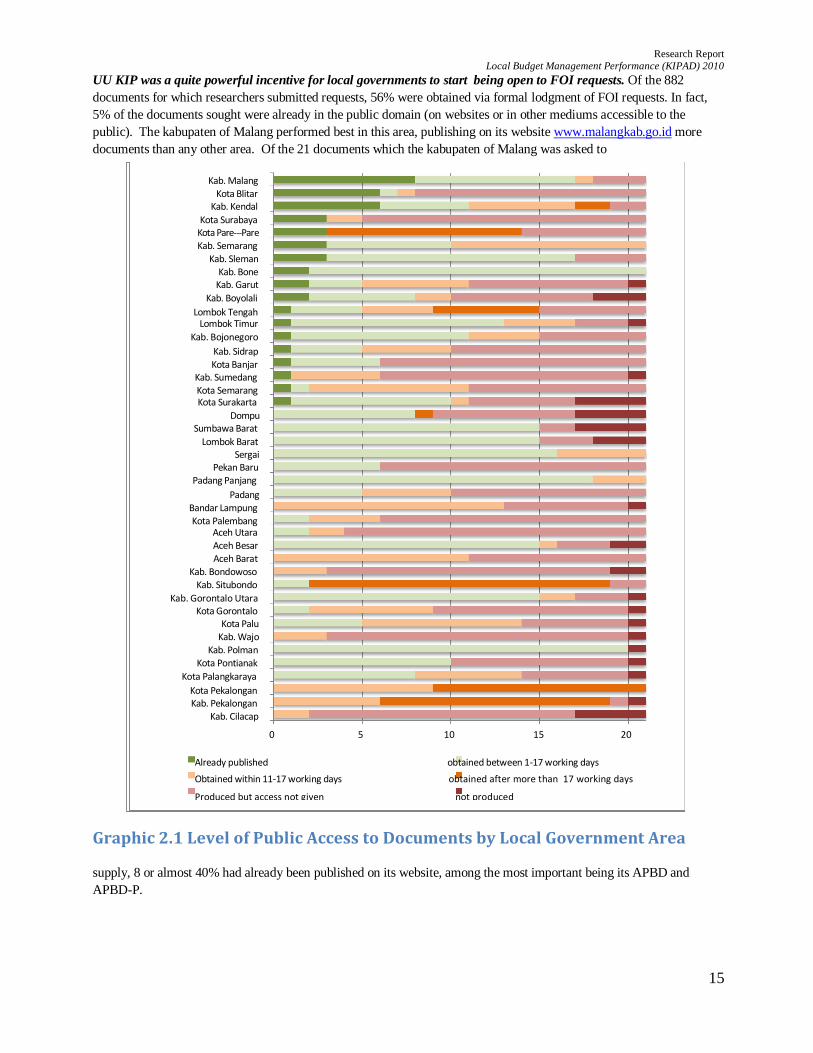

UU KIP was a quite powerful incentive for local governments to start being open to FOI requests. Of the 882

documents for which researchers submitted requests, 56% were obtained via formal lodgment of FOI requests. In fact,

5% of the documents sought were already in the public domain (on websites or in other mediums accessible to the

public). The kabupaten of Malang performed best in this area, publishing on its website www.malangkab.go.id more

documents than any other area. Of the 21 documents which the kabupaten of Malang was asked to

Graphic 2.1 Level of Public Access to Documents by Local Government Area

supply, 8 or almost 40% had already been published on its website, among the most important being its APBD and

APBD-P.

0 5 10 15 20

Already published obtained between 1-17 working days

Obtained within 11-17 working days obtained after more than 17 working days

Produced but access not given not produced

Kab. Malang

Kota Blitar

Kab. Kendal

Kota Surabaya

Kota Pare-‐‐Pare

Kab. Semarang

Kab. Sleman

Kab. Bone

Kab. Garut

Kab. Boyolali

Lombok Tengah

Lombok Timur

Kab. Bojonegoro

Kab. Sidrap

Kota Banjar

Kab. Sumedang

Kota Semarang

Kota Surakarta

Dompu

Sumbawa Barat

Lombok Barat

Sergai Pekan Baru

Padang Panjang

Padang

Bandar Lampung

Kota Palembang

Aceh Utara

Aceh Besar

Aceh Barat

Kab. Bondowoso

Kab. Situbondo

Kab. Gorontalo Utara

Kota Gorontalo

Kota Palu

Kab. Wajo

Kab. Polman

Kota Pontianak

Kota Palangkaraya

Kota Pekalongan

Kab. Pekalongan

Kab. Cilacap

Research Report

Local Budget Management Performance (KIPAD) 2010

16

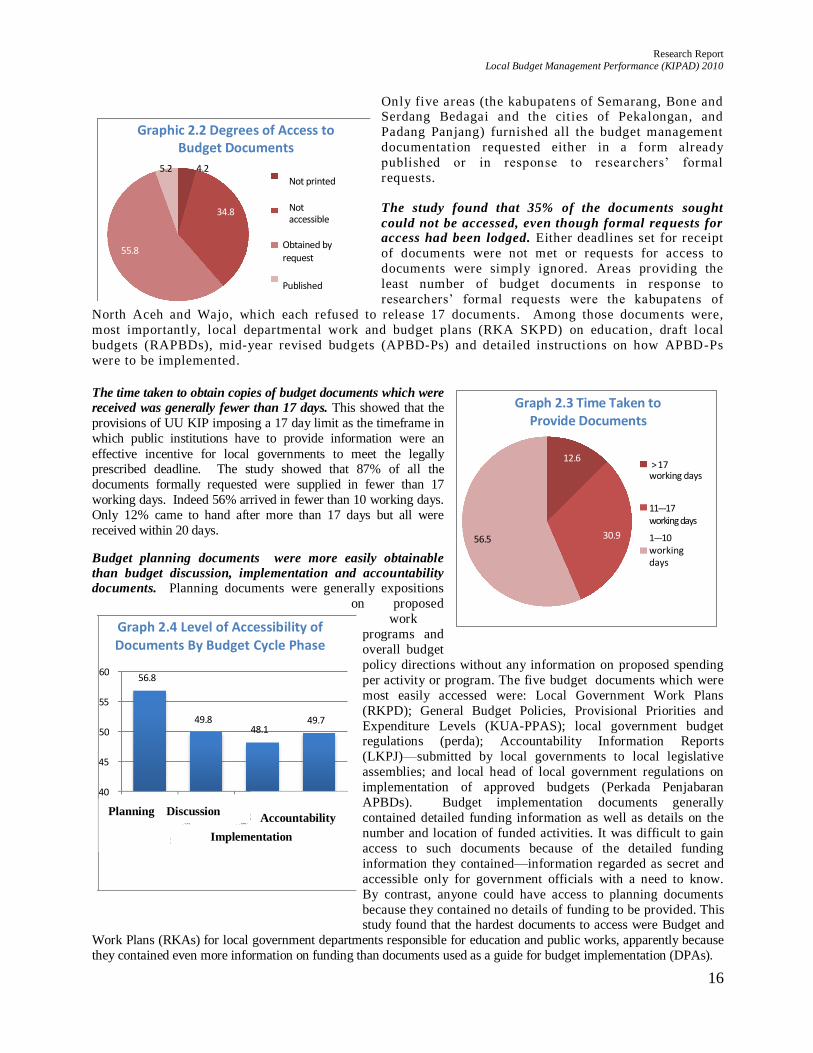

Only five areas (the kabupatens of Semarang, Bone and Serdang Bedagai and the cities of Pekalongan, and

Padang Panjang) furnished all the budget management

documentation requested either in a form already

published or in response to researchers‘ formal

requests.

The study found that 35% of the documents sought

could not be accessed, even though formal requests for access had been lodged. Either deadlines set for receipt

of documents were not met or requests for access to

documents were simply ignored. Areas providing the

least number of budget documents in response to

researchers‘ formal requests were the kabupatens of

North Aceh and Wajo, which each refused to release 17 documents. Among those documents were,

most importantly, local departmental work and budget plans (RKA SKPD) on education, draft local

budgets (RAPBDs), mid-year revised budgets (APBD-Ps) and detailed instructions on how APBD-Ps

were to be implemented.

The time taken to obtain copies of budget documents which were

received was generally fewer than 17 days. This showed that the

provisions of UU KIP imposing a 17 day limit as the timeframe in

which public institutions have to provide information were an

effective incentive for local governments to meet the legally prescribed deadline. The study showed that 87% of all the

documents formally requested were supplied in fewer than 17

working days. Indeed 56% arrived in fewer than 10 working days.

Only 12% came to hand after more than 17 days but all were

received within 20 days.

Budget planning documents were more easily obtainable

than budget discussion, implementation and accountability

documents. Planning documents were generally expositions

on proposed

work

programs and

overall budget

policy directions without any information on proposed spending

per activity or program. The five budget documents which were

most easily accessed were: Local Government Work Plans

(RKPD); General Budget Policies, Provisional Priorities and

Expenditure Levels (KUA-PPAS); local government budget regulations (perda); Accountability Information Reports

(LKPJ)—submitted by local governments to local legislative

assemblies; and local head of local government regulations on

implementation of approved budgets (Perkada Penjabaran

APBDs). Budget implementation documents generally

contained detailed funding information as well as details on the

number and location of funded activities. It was difficult to gain

access to such documents because of the detailed funding

information they contained—information regarded as secret and

accessible only for government officials with a need to know.

By contrast, anyone could have access to planning documents

because they contained no details of funding to be provided. This study found that the hardest documents to access were Budget and

Work Plans (RKAs) for local government departments responsible for education and public works, apparently because

they contained even more information on funding than documents used as a guide for budget implementation (DPAs).

55.8

Graphic 2.2 Degrees of Access to Budget Documents

5.2 4.2

34.8

Not printed

Not accessible

Obtained by request

Published

56.5

Graph 2.3 Time Taken to Provide Documents

12.6

30.9

> 17 working days

11-‐‐17 working days

1-‐‐10

working days

45

40

60

55

50

56.8

Graph 2.4 Level of Accessibility of Documents By Budget Cycle Phase

49.8

48.1

49.7

Planning Discussion

Implementation

Accountability

Research Report

Local Budget Management Performance (KIPAD) 2010

17

“More really serious political negotiation on budgets occurs during the process of approving Perda on APBD-Ps, than during approval processes for Perda on the original budget (APBD murni).

(Khairiansyah Salman, Expert Staff, national Audit Board)

Regional Governance Implementation Reports (LPPDs) were the most widely published of all local budget

documents. Twelve (29%) of local governments studied had published their LPPDs on their websites in accordance a requirement in PP No.3/2007 that LPPDs be published in both electronic and written form. This situation was especially

interesting given that KIPAD 2009 concluded that LPPDs were least likely to be produced at all by local governments.

Access to regional government regulations (perda) on APBDs (as originally approved) and on implementation of

APBDs was somewhat easier for this study. But perda on revised budgets (APBD-Ps) and head of government

regulations on implementation of APBD-Ps remained the most difficult to obtain of the 21 documents sought. In

55% of all 42 areas studied perda on APBD-Ps were unobtainable. By contrast, documents on APBDs and their implementation were available in 70% of areas studied. This situation served to reinforce suspicion of many that real

power play over budgets occurs not so much when APBDs are approved but rather when they are revised mid-year.

Another angle here is that central government sanctions imposed on regional governments for lack of timeliness in

budget approval are applicable only to the original APBDs and not to mid-year revised APBD-Ps.

B. Institutional Support for Freedom of Information Services

Most local governments had yet to establish offices for management of information and documentation (PPIDs) to provide freedom of information (FOI) services. Only nine areas studied— the cities of Surakarta,

Gorontalo, Bandar Lampung and Padang and the kabupatens of Sumedang, Bojonegoro, Aceh Besar, North Aceh and

Serdang Bedagai— had established some kind of PPID in accordance with FOI law (UU KIP) which requires all public

Already published Obtained by request within 1-10 working days

Obtained by request within 11-17 working days Obtained by request after more than 17 workdays

Produced but unobtainable Not produced

42

36

30

24

18

12

6

0

LKPJ

LPPD

RKPD

Perd

a PTJ

pel

aks

anaan A

PBD

Lap.

Rea

lisas

i Sm

t I

Perk

ada

Penj. A

PBD

P

Per

kada

Pen

j. A

PBD

Ren

ja S

KPD k

e.

Ren

ja S

KPD

Pen

d.

Ren

ja S

KPD P

U

DPA S

KPD

Pen

d.

Perd

a APBD

P

Perd

a APBD

RKA S

KPD

Pen

d.

ILPPD

DPA S

KPD

PU

DPA S

KPD K

es.

RAPBD

RKA S

KPD

PU

RKA S

KPD

Kes

.

KU

A-P

PAS

Planning Discussionn

Implement-ation Accountability

Graphic 2.5 Level of Accessibility of Budget Documents by Title (See Glossary (page 6) for explanation of abbreviations of titles of documents referred to in this graphic)

Research Report

Local Budget Management Performance (KIPAD) 2010

18

institutions to set up PPIDs. Other areas had not done so, perhaps understandably, because UU KIP‘s enabling

regulation (PP No. 61/2010) set August 2011as the deadline for the establishment of PPIDs.1

Box 2.1 Functions and Role of Office for the Management of Information and Documentation (PPID)

An Office for Management of Information and Documentation (PPID) will be an office with responsibility for the storage, documenting and provision of public information and/or the provision of freedom of information services to the public. The role and responsibility of the PPID will be to manage the process of providing freedom of information services, including processes relating to the storage, documentation, and provision of public information and freedom of information services. The PPID will have the task of gathering information from all areas of the public institution under the direction of the head of institution.

(Source: : Law No. 14/ 2008 and Central Information Commission Regulation No.1/2010)

Most local governments did not have standard operating procedures (SOP) for handling freedom of information (FOI) requests. For the purposes of this study, a SOP was taken to mean information issued by

a local government on procedures to be followed by the public to gain

access, in a structured and institutionalized way, to public information,

including on budgets. Only fifteen of the areas studied had SOPs for

handling FOI services—established by local government regulation or

otherwise. In four areas—the kabupatens of Garut and Sumedang

and the cities of Blitar and Palembang—a head of government

regulation (perkada) had been the vehicle.

C. Index of Transparency of Local Budget Management

Based on the above findings, the overall level of transparency of budget

management of local governments studied was categorized as adequate.

Although no single area could be put in the category of having a very good

level of transparency, ten were classified as having a good level of

transparency. Highest on the list was the kabupaten of Bone, followed by

the kabupaten of Serdang Bedagai and the city of Pandang Panjang. In Bone researchers were able to gain access to all documents sought within 1-10 working days of requests being lodged. The documents obtained included those which

were hard to access in other areas. They included revised budgets (APBD-Ps); implementing regulations for APBD-Ps;

and work and budget plans (RKAs) and budget implementation guidelines (DPAs) of local departments of education,

health and public works. Bone had also published its regional government work plans (RKPD) and information reports

on regional governance implementation (ILPPDs). The performances of Serdang Bedagai and Pandang Panjang

matched that of Bone, except that they took longer to provide some documentation (11-17 working days).

Seventeen governments were classified as having an adequate level of transparency and fifteen as having a poor level. Within the latter group the kabupaten of Wajo was ranked lowest. Not only had many of Wajo‘s budget

documents not been published, they had also not been made publicly available even in response to formal freedom

of information requests.

1 Article 21 paragraph (1) of Government Regulation No. 61/2010 (which entered into force on 23 August 2010) reads: ―PPIDs must be established

within one year, at the latest, of the entry into force of this regulation.‖

Graphic 2.6 Areas With or Without SOPs

for Processing FOI Requests

No

SOP for

FOI requests,

27

With SOP for FOI

requests,

15

Research Report

Local Budget Management Performance (KIPAD) 2010

19

Graphic 2.7 Index of Transparency of Local Budget Management

Category Score

Very good level of transparency 100-84.17

Good level of transparency 84.16-67.98

Adequate level of transparency 67.97-50.24

Poor level transparency 50.23-0

11

Kab. Gorontalo Utara

Kota Palangkaraya

Bandar Lampung

Kab. Bondowoso

Kota Pekalongan

Kab. Bojonegoro

Kab. Pekalongan

Kota Palembang

Padang Panjang

Sumbawa Barat

Lombok Tengah

Kab. Sumedang

Kota Gorontalo

Kab. Situbondo

Kota Pontianak

Kota Semarang

Kab. Semarang

Kota Pare-‐‐Pare

Kota Surakarta

Lombok Timur

Kota Surabaya

Lombok Barat

Kab. Boyolali

Kab. Polman

Kab. Malang

Kab. Sleman

Kab. Cilacap

Kab.Kendal

Kota Banjar

Pekan Baru

Aceh Utara

Aceh Besar

Kab. Sidrap

Aceh Barat

Kab. Garut

Kota Blitar

Kab. Wajo

Kab. Bone

Kota Palu

Padang

Dompu

Sergai

0 10 20 30 40 50 60 70 80 90

29.5

32.4

35.2

35.2

40.0

41.0

41.8

42.4

42.4

43.8

44.3

48.6

48.6

49.0

50.0

51.4

51.9

52.9

53.3

55.2

55.2

55.7

55.7

56.2

56.4

56.9

58.1

59.5

62.4

63.6

64.8

65.7

68.1

68.8

72.6

73.6

74.3

75.7

78.1

78.5

79.9

81.7

Research Report

Local Budget Management Performance (KIPAD) 2010

20

Chapter III

Performance in Participation in Local Budget Management

Public participation is an important indicator of good governance. A participatory approach demands that a

government treats people as active participants in development activities and budget management. That means that

people should be involved in every decision making process. Indonesia‘s legal regulatory framework guarantees the

right of people to be involved in the formulation and determination of public policy. Law No. 25/2004 concerning

Development Planning Systems and Law No. 32/2004 concerning Regional Governance both provide for public

participation in the development planning process. It is every citizen‘s right to share responsibility for the public domain, for bringing together issues of concern, for planning community agendas and for overseeing the

performance of elected representatives and governments to ensure that they faithfully discharge popular mandates.

This applies especially to political decisions on development and budgetary issues that impact directly on people‘s

welfare. Following are details of provisions in Indonesian law on public participation:

1. Article 53 of Law No. 10/2004 concerning Enactment of Legislation reads: ―The people shall have the right to provide oral and written inputs for preparation and discussion of draft local government laws and

regulations.‖

2. Article 139 of Law No. 32/2004 concerning Regional Governance reads: ―The people shall have the right

to provide oral or written inputs for preparation and discussion of draft local government regulations.‖

3. Article 2 paragraph (4) point d, Article 5 paragraph (3), Article 6 paragraph (2) and Article 7 paragraph (2) of Law No. 25/2004 concerning Development Planning Systems stipulate that

development planning shall make optimal use of the involvement of the people.

Two indicators were used to measure performance in facilitating public participation. Firstly, the study looked at the extent of existing mechanisms for public participation and who was invited to use them. Second, it examined the

content of local government regulatory provisions on public participation in budget management. Public participation

indicators were based on answers to 15 questions in the research instrument.

A. Mechanisms for Participation and Categories of Participants

Local governments still had only limited mechanisms for public participation in budgetary processes. The only mechanism consistently used by local governments was what is termed musrenbang (community

consultations on development planning). Beyond that, executive branches of local governments conducted very

little public consultation when preparing draft budgets (RAPBDs), revised budgets (APBD-Ps), basic documentation

on budget policies and funding (KUA-PPASs) and accountability documentation. That said, the study found that local

legislative assemblies (DPRDs) were starting to take the initiative in this area. They were consulting more widely than

the executive by holding public consultations on the documents referred to above. In fact, researchers found that 50% of DPRDs were holding such public consultations before taking decisions on these documents. Of the three local

government departments surveyed, public works was worst at providing mechanisms for participation.

Research Report

Local Budget Management Performance (KIPAD) 2010

21

The kabupatens of Serdang Bedaga and Malang and the city of Padang were more innovative than other areas

in providing mechanisms for public participation in budgetary processes. These three areas employed all the consultative mechanisms used in the study as measures of performance in participation. These results show that

overall people are being provided with increasing opportunities to have a say in the formulation of local budget

policies.

Graphic 3.1 Mechanisms for Participation Provided by 42 Governments Studied

Public participation—especially of women, NGOs and delegates to community development conferences

(musrenbang)—was at its height during the musrenbang process but fell away when discussion of budget documents (KUA PPASs and APBDs) commenced. Professional organizations and institutions of higher education

consistently played a greater role in any public consultation process than other community groups. A more complete

picture is provided in Graphic 3.2.

Graphic 3.2 Community Involvement by Consultative Mechanism Provided

JNo.

of M

echan

ism

s use

i

11

10

Comments on LKPD Pub Cons (in DPRD) on PTJ APBD Public Consult (in DPRD) on RAPBD

Pub Cons (in DPRD) on KUA-‐‐PPAS Pub Cons on PTJ APBD Public Cons on RAPBD

Pub Consultations on KUA-‐‐PPAS Musrenbang Pub For Pub Works

Public Forum on Health Public Forum on Education

4

9

8

7

6

5

3

2

0

1

Kab

. Situbondo

Kab. W

ajo

Kota

Palu

Kota

Goro

nta

lo

Kota

Pala

ngkara

ya

Kab

. Sidra

p

Kota

Pare

-Pare

Kab

. Goro

nta

lo U

tara

Ace

h B

ara

t Ace

h U

tara

Bandar Lam

pung

Lom

bok B

ara

t D

om

pu

Sum

baw

a B

ara

t Kab. Pekalo

ngan

Kab

. Sem

ara

ng

Kota

Pekalo

ngan

Kota

Sem

ara

ng

Kab

. G

aru

t Pekan B

aru

Kab

. Ken

dal

Kota

Sura

karta

Kab. Sum

edang

Kab. Bone

Lom

bok T

engah

Kab. Bondow

oso

Kab. Bojo

negoro

Kota

Sura

bay

a

Kab

. Slem

an

Kota

Pontianak

Kab

. Boyo

lali

Kab

. Cila

cap

Kota

Banja

r Kota

Pale

mbang

Kab

. Polm

an

Kota

Blitar

Ace

h B

esa

r Padang P

anja

ng

Lom

bok T

imur

Kab. M

ala

ng

Padang

Serg

ai

Public discussion of APBD

Pub. Part. in framing APBD

Public discussion of KUA-‐‐PPAS

Pub. Part. In framing KUA-‐‐PPAS

musrenbang

Public Works Cons

Public forums on education

pendidikan Public forums on education

0% 20% 40% 60% 80% 100%

Percentage of Participation by Community Group

The h’capped other groups Womens groups

NGOs private companies musrenbang.

Professional organizations local assembles drafting team

Research Report

Local Budget Management Performance (KIPAD) 2010

22

Suggestions put forward during the musrenbang process were not taken up and funded. In the main, musrenbang consultations were a formality used to hear what people wanted without any follow up in terms of funding. More than 60% of governments studied did not provide indicative funding figures at the sub-district (kecamatan) level

(known as PIK). As a result, musrenbang discussions were just so much hot air; and there was no one in a position to follow up on them to make sure that suggestions were funded in APBDs. On the basis of the correlations carried

out in this study, it emerged that governments with PIKs in place (38% of those studied) tended to have more public participation than those without them.

Graphic 3.3 Participation Indices of Areas with PIKs and Those without PIKs

B. Regulatory Provisions on Public Participation

Existing local government regulations provided a disappointing basis for development of public participation in ways which met people’s needs. Although more than 60% of areas studied had regulations in place ―guaranteeing‖ public participation in budgetary processes, public involvement was nonetheless largely confined to development planning

conferences (musrenbang). It was not so evident in subsequent processes, where real budget negotiations occurred. Indeed this study concluded just that: public consultation dropped away once budget cycles entered the discussion phase

(Graphic 3.4).

Graphic 3.4 Areas Providing Mechanisms for Participation by Budget Cycle Phase (%)

Par

ticip

atio

n In

dex

Score

40

70

60

50

30

20

10

0

Padang

Padang P

anja

ng

Kab. Bojo

negoro

Kab

. Boyo

lali

Kota

Banja

r Kota

Blit

ar

Serg

ai

Kab. Sum

edang

Kota

Pontianak

Ace

h B

esa

r Kab

. Cila

cap

Kota

Sem

ara

ng

Kab. Sem

ara

ng

Kab

. Sid

rap

Kab

. Goro

nta

lo U

tara

Ace

h B

ara

t Kab. Situbondo

Kota

Pal

angka

raya

D

om

pu

Kota

Goro

nta

lo

Kab

. W

ajo

Ace

h U

tara

Bandar

Lam

pung

Lom

bok

Bara

t Lo

mbok

Tengah

Peka

n B

aru

Kota

Pare

-Pare

Kota

Pal

u

Sum

baw

a B

ara

t Kab. G

aru

t Kab. Bondow

oso

Kab

. Kendal

Kota

Sura

baya

Kab. Bone

Kab

. Sle

man

Kab. Polm

an

Kab. Peka

longan

Kota

Peka

longan

Kab. M

ala

ng

Lom

bok

Tim

ur

Kota

Pale

mbang

Kota

Sura

kart

a

Had PIKs Did not have PIKs

Public

Foru

m o

n h

eal

th

Public

Foru

m o

n E

duca

tion

% o

f A

reas P

rovid

ing M

echan

ism

s

for P

ublic

Part

icip

ation ,„

8

6

100

. 4 0

0

0

0

0

100

76

45 45_______________

31 34 33

14

67______________

57 52

Planning Discussion and Adoption

Musr

enbang K

ab/

City

Pub W

ork

s Fo

rum

Public

Cons

on K

UA-

PPAS (in

DPRD

)

Public

cons

on

k KUA-

PPAS

Public

Cons

on p

erd

a on

APBD

(in

DPRD

)

Public

cons

on

dra

ft A

PBD

Public

Cons

on P

TJ

APBD

Pro

vidin

g F

eed

back

on L

KPD

Public

cons

on d

raft reg

on

Phi A

PBD

(in

DPRD

)

Accountability

Research Report

Local Budget Management Performance (KIPAD) 2010

23

The enactment of local regulations on public participation in budget planning did not of itself increase public

participation levels in areas studied. After comparing areas with such regulations and those without them, researchers concluded that neither group stood out as having more or less public participation in budgetary processes. One reason

for this situation might have been that local regulations were replications of central government regulations on

participation in musrenbang processes. They did not, therefore, provide a good legal basis for developing public

participation in budget management processes. Indeed there were indications that in some areas public participation

was trending downwards.

Local governments generally provided mechanisms for taking people’s complaints on board. Thirty nine (39)

governments had established one or more of the following mechanisms: conduct of a specific complaints-related activity; a

special complaints unit; or a database for community complaints. 16 areas had conducted special activities and 15 had

established special units. But only 8 governments had set up special databases for registration of people‘s complaints.

Generally speaking none of these mechanisms was enshrined in local regulations, so their continuation could not be

guaranteed. The kabupatens of Sleman, Bone and Sumedang and the city of Surakarta were each using all three of the

above mechanisms.

C. Index of Participation in Local Budget Management

On average, the performance of governments under study in terms of public participation in budgetary processes was disappointing. All but two areas surveyed—the cities of Padang Panjang and Padang—were categorized

as having a poor level of public participation. This situation was very worrying because it showed that both national and

regional legislative frameworks were too weak to foster greater public participation in budget management processes.

The cities of Padang and Padang Panjang were ranked most highly for their levels of public participation in budget management processes. This ranking for Padang was justified by the high level of commitment of the city‘s

executive and legislative branches of governments to using creative ways to involve people in budget

management processes. In addition to mechanisms for participation laid down in government regulation,

Padang held public consultations (or public hearings within the DPRD) to encourage people to provide inputs

for preparation of budgetary documents. But Padang had no mechanism in place to accommodate community

complaints about public services. Nonetheless, these two areas used almost all public consultation mechanisms

currently in use. Both also had a local regulatory framework supportive of public participation and mechanisms

for accommodating complaints from the community (sic). In addition they both had indicative funding figures

(PIK) by sector and geographical area, thereby guaranteeing that community suggestions could be accommodated

in budgetary processes.

There were more cities than kabupatens among the five areas rated most highly on the public participation index. But that did not mean that cities studied were best at including people in budget management processes. After all,

several city governments were ranked in the middle and towards the bottom of the index. The key factor determining an

area‘s level of public participation was the level of commitment of its government—be it city or kabupaten.

Research Report

Local Budget Management Performance (KIPAD) 2010

24

Graphic 3.5 Index of Performance in Public Participation in Local Budget Management

Category Score

Very good level of participation

100-77.0

Good level of participation 76.99-66.33

Sufficient level of participation

66.32-52.33

Poor level of participation 52.32-0

ka b

/cit

ies

Kab. Gorontalo Utara

Kota Palangkaraya

Bandar Lampung

Kab. Bondowoso

Kota Pekalongan

Kab. Bojonegoro

Kab. Pekalongan

Kota Palembang

Padang Panjang

Lombok Tengah

Sumbawa Barat

Kab. Sumedang

Kota Gorontalo

Kab. Situbondo

Kota Pontianak

Kota Semarang

Kab. Semarang

Kota Pare-‐‐Pare

Kota Surakarta

Lombok Timur

Kota Surabaya

Lombok Barat

Kab. Boyolali

Kab. Malang

Kab. Polman

Kab. Sleman

Kab. Cilacap

Kab. Kendal

Kota Banjar

Aceh Besar

Aceh Utara

Pekan Baru

Kab. Sidrap

Aceh Barat

Kab. Garut

Kota Blitar

Kab. Bone

Kab. Wajo

Kota Palu

Padang

Dompu

Sergai

0.00 1 0 . 0 0 2 0 . 0 0 3 0 . 0 0 4 0 . 0 0 5 0 . 0 0 6 0 . 0 0 7 0 . 0 0 8 0 . 0 0 9 0 . 0 0 1 0 0 . 0 0

7.0

7.3

10.3

11.0

11.7

12.7

12.7

13.0

13.0

13.7

14.3

15.3

16.3

16.3

18.0

18.0

7.0

19.3

21.3

22.7

23.0

23.

26.7

26.7

29.7

30.3

31.3

31.7

33.7

34.3

36.0

37.7

39.0

39.0

39.7

42.0

44.3

mark

45.3

47.7

49.3

62.0

62.7

Research Report

Local Budget Management Performance (KIPAD) 2010

25

Chapter IV

Performance in Accountability of Local Budget Management

The principle of public accountability requires that local governments should be held to public account for

every policy they implement (including budget management policies). After all, ordinary people are the rightful

beneficiaries of government policies. This principle requires that those responsible for implementing government

policies and programs should be transparently accountable to those affected by what they do. It is, after all, the latter

group that is entitled by right to know how government policies and programs have been carried out. Accountability

also demands that a government agency be prepared to receive a critique of both its successes and failures in fulfilling

its mission to achieve goals and targets set for it from time to time. Thus every government agency has the

responsibility to render an account of its management of resources at every stage of the process (from planning, through

implementation, to evaluation).2 Following are details of provisions in Indonesian law on public accountability:

1. Article 23 of the 1945 Constitution: ―The State budget, as the basis of the management of State funds, shall be determined annually by law and shall be implemented in an open and accountable manner in order to best

attain the prosperity of the people

2. Article 3 paragraph (1) of Law 17/2003 concerning State Finances: ―The State‘s finances shall be

managed in an orderly way, in accordance with the provisions of law, efficiently, economically,

effectively, transparently and accountably, keeping justice and propriety front and centre.‖

3. Article 23 paragraph (2) of Law No. 32/2004 concerning Regional Governance: ―The management of regional finances referred to paragraph (1) shall be conducted efficiently, effectively, transparently,

accountably, correctly, justly, appropriately and in conformity with law.

4. Article 4 of PP No. 58/2005 concerning Management of Regional Finances: ―Regional finances shall be managed correctly, in accordance with law, efficiently, effectively, transparently and accountably, keeping

in mind principles of justice, propriety and being of benefit to the people.

Three indicators were used to measure the performance of local governments in the area of accountability.

Firstly, the study assessed the timeliness of both production of local budget documents and of decisions on them.

Such timeliness was regarded as being a crucial part of budget management: Not only did it affect program

implementation and provision of public services; it also had a potentially significant impact locally and could result in

imposition of central government sanctions. Second, the study looked at local government mechanisms for the supply

of goods and services. This involved a close examination of local government public tendering processes and the

extent to which black-lists of companies banned from tendering existed. Third, researchers reviewed national Audit Board reports on the budgetary performance of governments surveyed.

2 See Max H Pohan‘s, Mewujudkan Tata Pemerintahan Lokal yang Baik (Good Governance) dalam Era Otonomi Daerah, a paper presented to the third round of “large-scale consultations” on development in the area of Musi Banyuasin, Sekayu, 29 September–1 October 2000.

Research Report

Local Budget Management Performance (KIPAD) 2010

26

A. Timeliness

In assessing the timeliness of both production of local budget documents and decisions on them, researchers were

guided by existing legal provisions. Table 4.1 outlines deadlines set by current central government regulations for

both preparation and adoption of various budgetary documents.

Table 4.1 Regulatory Framework for Deadlines for Final Approval of Budget Documents

Document

Deadline for Final Approval

Basis in Law

RKPD

End of May

PP No. 58 / 2005 Art. 33 para (2)

Hm Affairs Min Reg. 13/ 2006 Art. 82 Para 2

APBD

The beginning of December immediately

preceding the start of the fiscal year

PP No. 58 / 2005 Art. 45 para (1)

Home Affairs Min Reg. 13/ 2006 Art. 104 Para (2)

APBD-P

3 months before the end of the fiscal year

Home Affairs Min Reg. 13/ 2006 Art. 172 Para (5)

The timing of discussion of planning and budgetary documents is governed by the following regulations:

Table 4.2 Regulatory Framework for Timeframes for Discussion of Budget Documents

Document

Submission Date

Basis in Law

KUA-PPAS

Start of June

Hm Affairs Min Reg. 13/ 2006 RAPBD

First week of October

Home Affairs Min Reg. 13/ 2006

RAPBD-P

Second week of September

Home Affairs Min Reg. 13/2006 Art. 172 para (2)

The study showed that many budget documents were in fact finalized and submitted to local legislative

assemblies (DPRDs) in accordance with these prescribed timeframes. This situation differed from the findings of

KIPAD 2009, which found that many areas were slow to finalize their planning and budgetary documents and that late

presentation of documents meant that DPRDs did not have enough time to discuss them properly. Thus KIPAD 2010 indicates that regional government efforts to implement accountable fiscal management procedures have paid dividends.

Table 4.3 Proportion of Governments Meeting Deadlines for Final Approval of Budget Documents

Document

Final approval date prescribed in law

Performance of governments studied

RKPD

End of May

50% of governments did not met this deadline:

approval and adoption occurred after May

APBD

The beginning of December before start

of current fiscal year

70% of governments met this deadline

APBDP

3 months before end of current fiscal yearr

(beginning of October)

Almost 80% of governments met this

deadline

LKPJ

To be submitted to DPRDs by the month of

June immediately after end of fiscal year

More than 50% of governments did not meet this

deadline

The document outlining regional government work plans (RKPD) was the only budget document which was, in

most cases, not approved and adopted on time by local governments. This situation not only violated existing

government regulations but also affected subsequent budget policy formulation processes by holding up discussion and

approval of other budget documents. In particular, given that RKPDs are essential inputs in KUA-PPASs (basic policy

documents on budget policies and spending levels), their late appearance meant that KUA-PPASs were submitted late

to DPRDs. And that impacted on preparation and approval of subsequent budget documentation, including draft APBDs themselves. Despite all that, only 17 of the governments surveyed observed legal deadlines for final adoption

of RKPDs and submission of the KUA-PPASs to DPRDs.

Even though in most cases draft APBDs were submitted late to local DPRDs, they were generally submitted

Research Report

Local Budget Management Performance (KIPAD) 2010

27

during October and thus were adopted and ratified as approved budgets (APBD murni) by the December

deadline. This same applied to revised budgets (APBD-Ps).

B. Mechanisms for Supply of Goods and Services

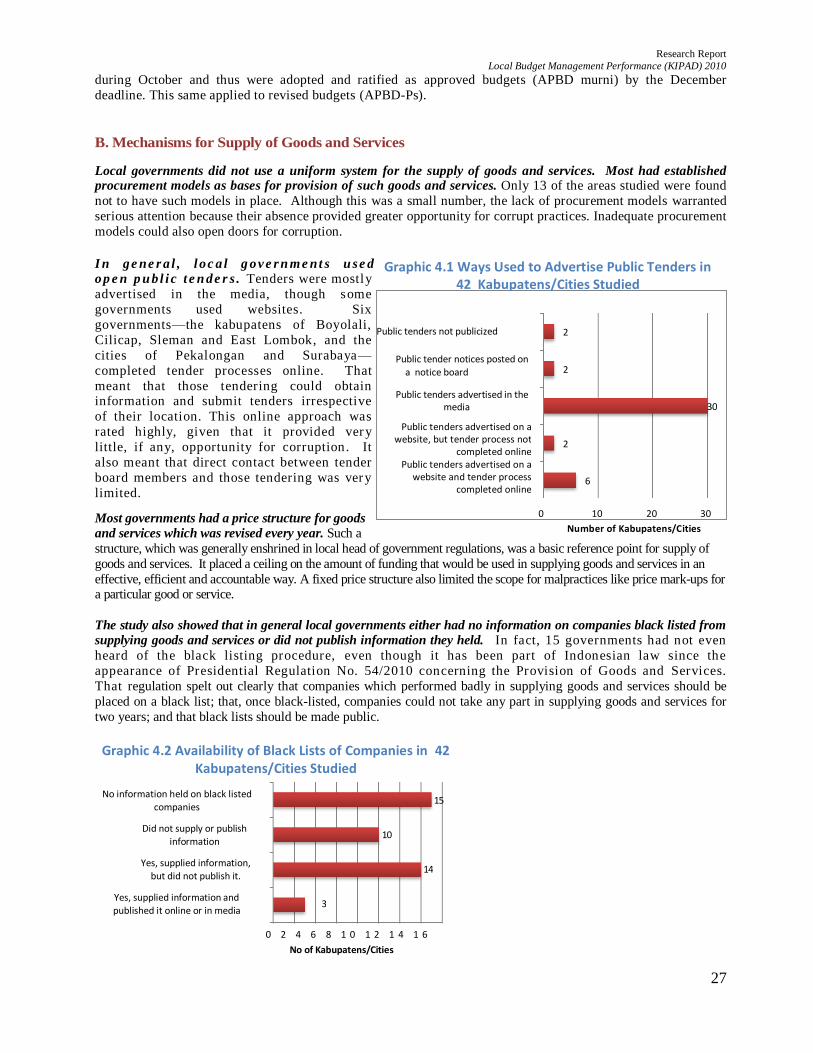

Local governments did not use a uniform system for the supply of goods and services. Most had established procurement models as bases for provision of such goods and services. Only 13 of the areas studied were found

not to have such models in place. Although this was a small number, the lack of procurement models warranted

serious attention because their absence provided greater opportunity for corrupt practices. Inadequate procurement

models could also open doors for corruption.

I n ge ne r a l , l oc a l g ov e r n m e nt s u se d

op e n p u b l i c t e n de r s . Tenders were mostly

advertised in the media, though some

governments used websites. Six

governments—the kabupatens of Boyolali,

Cilicap, Sleman and East Lombok, and the

cities of Pekalongan and Surabaya—

completed tender processes online. That

meant that those tendering could obtain information and submit tenders irrespective

of their location. This online approach was

rated highly, given that it provided very

little, if any, opportunity for corruption. It

also meant that direct contact between tender

board members and those tendering was very

limited.

Most governments had a price structure for goods

and services which was revised every year. Such a

structure, which was generally enshrined in local head of government regulations, was a basic reference point for supply of

goods and services. It placed a ceiling on the amount of funding that would be used in supplying goods and services in an

effective, efficient and accountable way. A fixed price structure also limited the scope for malpractices like price mark-ups for a particular good or service.

The study also showed that in general local governments either had no information on companies black listed from

supplying goods and services or did not publish information they held. In fact, 15 governments had not even

heard of the black listing procedure, even though it has been part of Indonesian law since the

appearance of Presidential Regulation No. 54/2010 concerning the Provision of Goods and Services.

That regulation spelt out clearly that companies which performed badly in supplying goods and services should be

placed on a black list; that, once black-listed, companies could not take any part in supplying goods and services for

two years; and that black lists should be made public.

Public tenders not publicized

Public tender notices posted on a notice board

Public tenders advertised in the media

Public tenders advertised on a website, but tender process not

completed online

Public tenders advertised on a website and tender process

completed online

2

2

30

2

6

0 10 20 30

Number of Kabupatens/Cities

Graphic 4.2 Availability of Black Lists of Companies in 42 Kabupatens/Cities Studied

0 2 4 6 8 1 0 1 2 1 4 1 6

No information held on black listed companies

perusahaan

Did not supply or publish information

Yes, supplied information, but did not publish it.

Yes, supplied information and published it online or in media

10

3

15

14

No of Kabupatens/Cities

Graphic 4.1 Ways Used to Advertise Public Tenders in 42 Kabupatens/Cities Studied

Research Report

Local Budget Management Performance (KIPAD) 2010

28

C. Opinion of National Audit Board

An examination of national Audit Board (BPK) opinions on the financial management of local governments

studied revealed quite a change since KIPAD 2009. That report recorded that five governments in East Java had

received ―disclaimer opinions‖ (no opinion offered). In 2010 most governments studied received ―qualified

opinions‖; four received ―disclaimer opinions‖; and one an ―adverse opinion‖. All areas in East Java included in

KIPAD 2010 received ―qualified opinions‖.

Although most governments studied received quite favorable BKP opinions, an important body of work remains to

be done by DPRDs in overseeing follow up on BPK findings. Researchers suspected that many local governments

took no follow up action at all on BPK findings, which were non-binding. Thus, in their role as institutions charged

with oversight of local government, DPRDs should exercise control over governments‘ follow-up on audit reports.

One way of doing that would be to encourage local governments to accept that such follow-up should be obligatory. What Semarang has done in this area is a good case study for all concerned (see Box 4.1).

Box 4.1 Semarang follows up on Findings in National Audit Board (BPK) Opinions

On the initiative of the City of Semarang‘s DPRD, the local government regulation (perda) on Accounting for the Implementation of the 2009 APBD, as finally adopted, contained a provision on the need for the government to take follow up

action on the BPK‘s audit report on the 2009 budget. This measure represented a formal move by the legislature to get the executive to genuinely follow up on BPK reports, bearing in mind that previous BPK findings had vanished into thin air without any follow-up at all. By incorporating a requirement for such follow-up into a perda, the DPRD will be able to verify whether or not government has taken the BPK‘s findings on board. Some of those findings were referred to specifically in the perda concerned:

Provision of land for a water retention pond potentially costing Rp 2.7 billion more than the price determined in the appraisal process.

Inclusion, without supporting evidence, of an amount of Rp 17 billion as tax owing for advertising.

Source : Ari Purbono, Presentation on Monitoring the Audits of Local Budgets, 2011