l.o to construct a balance sheet with information given

TRANSCRIPT

L.OTo construct a balance sheet with information given

BALANCE SHEET

The balance sheet is a financial statement which shows the assets, liabilities and capital of a business on a particular date.

Items that are owned by the business or owed to the business

Is the money invested by the owners

Is the amount owed by the business

Assets, Liabilities & Capital

Assets & Liabilities

The Manager’s name

Liabilities & Capital

How much profit

Assets & Capital

The employee’s details

The flow of cash

The balance sheet shows the financial health of the business, as well as.....

Out of date

Thrown in the bin

Given to every employee

Done again

Laminated

Put on weighing scales

Sent to the government

Sold to the public

As soon as the balance sheet is produced it is....

Local Community

The environment

Your mum

Mr Fletcher

Competitors

The government

Suppliers

Shareholders

All stakeholders will be interested in the balance sheet, especially....

Assets

Current Liabilities

Liabilities

Fixed Assets

Capital

Buildings

Current Assets

Money

Items owned by the business, or owed to the business

Capital

Profit

Assets

A wise investment

Liability

Converted in to stock

A stupid idea

Put in the bank account

Money invested by the owners is.....

Liabilities

Assets

Debt

Debtors

Capital

Don’t know

Creditors

Fixed Assets

Items owed by the business are....

Why produce a balance sheet?

• It shows the owner what their investment has been used for and gives an idea of what the business is worth.

• Shows the financial health of a business.

• It shows where the money has come from and what it has been spent on.

Assets – Items owned by the business or owed to the business.

Fixed Assets – Items kept longer than 1

year. Buildings / Vehicles / equipment

Current Assets – Items kept less than 1 year

Stock / Debtors / Cash in hand

Liabilities – Amounts owed by the business

Long-term liabilitiesLiabilities due to be repaid over more than one year

Current liabilitiesLiabilities due to be repaid

in less than one year

Capital – Money invested by the owner of a business

How does a balance sheet balance?

£10£10 £10

How does a balance sheet balance?

Assets

Liabilities

Assets

Liabilities

How does a balance sheet balance?

BALANCE SHEET (TOP)

BALANCE SHEET (TOP)

BALANCE SHEET (BOTTOM)

Now your turnCreate a balance sheet using the information below for

‘MADE UP COMPANY LTD’

Premises - £100,000

Creditors - £50,000

Equipment - £ 20,000

Cash in bank - £20,000

Profit & Loss (Net profit) - £30,000

Debtors - £10,000

Stock - £5,000

Share capital - £65,000

Reserves - £10,000

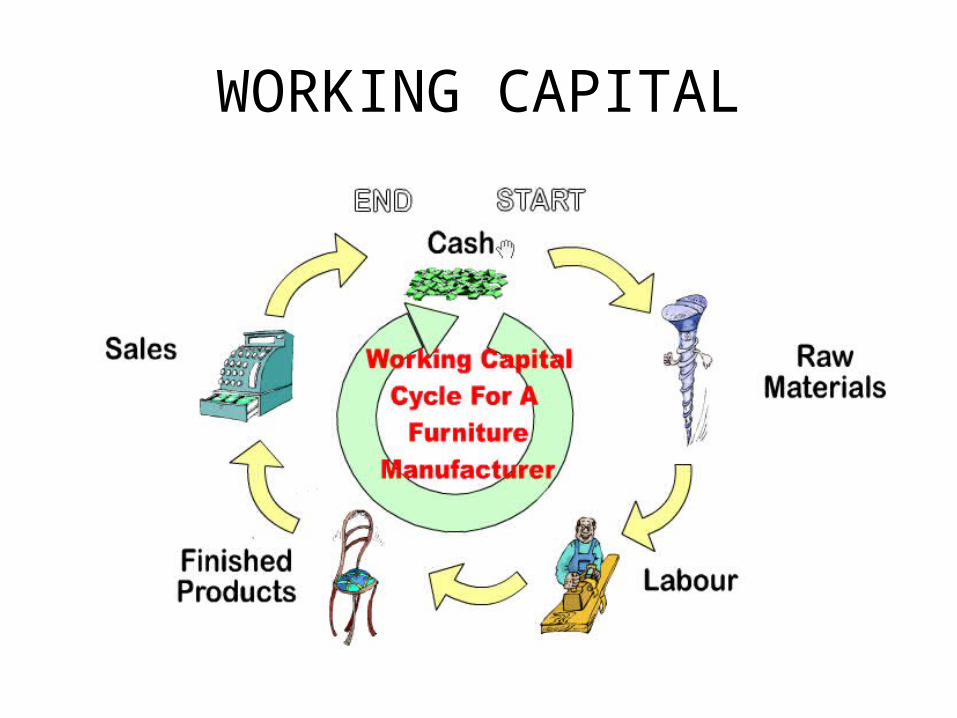

WORKING CAPITAL

Working Capital can be calculated as follows –

Working Capital = Current Assets – Current Liabilities

Anything the business owns and intends not to have for more than 1 year (raw materials / stock / debtors / cash)

Anything the business owes which must be paid in less than a year (creditors / overdraft / dividends)

WORKING CAPITAL

Working out working capitalWorking capital represents operating liquidity available to a business.

It is calculated as current assets minus current liabilities.

Working Capital = Current Assets − Current Liabilities

A company can have loads of assets and profitability but short of liquidity if its assets cannot readily be converted into cash.

Positive working capital is required to ensure that a firm is able to continue its operations and that it has sufficient funds to satisfy both maturing short-term debt and upcoming operational expenses.

Capital EmployedCapital employed is the value of the assets that contribute to a company’s ability to generate revenue

Fixed assets + current assets – current liabilities

Balance Sheet 1• Fixed assets £• Buildings 60,000• Equipment 20,000• Total fixed assets 80,000

• Current assets• Stock 20,000• Debtors 10,000• Cash in bank 10,000• Total current assets 40,000• (Total assets = £120,000)

Balance Sheet 2

LIABILITIES£

liabilitiesCreditors -10,000

Total assets less liabilities 110,000(This is the total assets - £120,000 - minus the liabilities)

Balance Sheet 3

•Capital and reserves £

•Share capital 70,000•Reserves 30,000•Profit and loss account 10,000

•Shareholders’ funds 110,000•(This is the total amount in capital and reserves. It must equal the same amount as the total assets minus liabilities)

Balance Sheet •ASSETS•Fixed assets (assets listed)•Total fixed assets £80,000 A•Current assets (assets listed)•Total current assets £40,000B

•LIABILITIES•Current liabilities –£10,000C•Total assets less current liabilities (Net assets) £110,000A + B – C______________________________________________________•Capital and reserves (all listed)•Shareholders’ funds £110,000D

Advantages of using ICT•Spreadsheets can be used to compile profit and loss accounts, formulae can be used to perform any calculations

•The spreadsheet template can be used again and again

•Advantages include speed, accuracy, instant access to information

•The spreadsheet can be used to create graphs

Disadvantages of using ICT

• Setting up the original template can be time-consuming

• If the formula are incorrect then the final accounts will be wrong

• Spreadsheet files can be easily deleted, and open to abuse.