littlefield corporationlittlefield.com/wp-content/uploads/2017/01/littlefield-corporation... ·...

TRANSCRIPT

LITTLEFIELD CORPORATION

CONSOLIDATED FINANCIAL STATEMENTS UNAUDITED

FOR THE YEAR ENDED DECEMBER 31, 2015

WITH INDEPENDENT ACCOUNTANTS' REVIEW REPORT

LITTLEFIELD CORPORATION

DECEMBER 31, 2015

TABLE OF CONTENTS

Page Number

Independent Accountants' Review Report . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . .. . . . . . . . . . . . . . . . . . . . . . . 1

FINANCIAL STATEMENTS

Consolidated Balance Sheet.......... ................................................... ...... .... .... .................. 2

Consolidated Statement of Income.................................................................................. 3

Consolidated Statement of Stockholders' Equity..... .. ..................................................... 4

Consolidated Statement of Cash Flows ......... .... ......... ...... .......... ..... ..... .... .... ............... ... . 5

Notes to the Consolidated Financial Statements.............................................................. 6- 18

PATTI L L 0, B Il 0 W N & HI L L, L. L. P . CUHIFIED PUIHIC ACCOUNTANTS • BUSINESS CONSUlTANtS

INDEPENDENT ACCOUNTANTS' REVIEW REPORT

To the Board of Directors Littlefield Corporation

We have reviewed the accompanying financial statements of Littlefield Corporation (the "Company"), which comprises the consolidated balance sheet as of December 31, 2015, and the related consolidated statement of income, consolidated statement of stockholders' equity, and consolidated statement of cash flows for the year then ended, and the related notes to the consolidated financial statements. A review includes primarily applying analytical procedures to management's financial data and making inquiries of company management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole. Accordingly, we do not express such an opinion.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Accountants' Responsibility

Our responsibility is to conduct the review engagement in accordance with the Statements on Standards for Accounting and Review Services promulgated by the Accounting and Review Services Committee of the AICP A. Those standards require us to perform procedures to obtain limited assurance as a basis for reporting whether we are aware of any material modifications that should be made to the consolidated financial statements for them to be in accordance with accounting principles generally accepted in the United States of America. We believe that the results of our procedures provide a reasonable basis for our conclusion.

Accountants' Conclusion

Based on our review, we are not aware of any material modifications that should be made to the accompanying consolidated financial statements in order for them to be in accordance with accounting principles generally accepted in the United States of America.

:f~ ) ~1 t/tJ1 1LtfJ Pattillo, Brown & I-fi ll, LLP Waco, Texas December 1, 2016

1 401 WEST HIGHWAY 6 • P. 0. BOX 20725 • WACO, TX 76702-0725 • (254) 772-4901 • FAX: (254) 772-4920 • www.pbhcpa.com

AFFILIATE OFFICES: HILLSBORO, TX (254) 582-2583 • HOUSTON, TX (281) 671-26259 RIO GRANDE VALLEY, TX (956) 544-7778 • TEMPLE, TX (254) 791-3460 • ALBUQUERQUE, NM (505) 266-5904

LITTLEFIELD CORPORATION

CONSOLIDATED BALANCE SHEET

UNAUDITED

DECEMBER 31, 2015

ASSETS

Current Assets: Cash and cash equivalents Accounts receivable, net of allowance for doubtful accounts

of$115,407 Other current assets Deferred tax asset - current portion Note receivable - current portion

Total Current Assets

Property, plant and equipment, net

Other assets: Goodwill Intangible assets, net Note receivable - net of current portion Deferred tax asset Other non-current assets

Total Other Assets

Total Assets

Current Liabilities: Accounts payable Accrued expenses Deferred revenue

LIABILITIES AND STOCKHOLDERS' EQUITY

Current portion of long term debt Total Current Liabilities

Long-term Liabilities: Long term debt, net of current portion

Total Long-term Liabilities

Total Liabilities

Stockholders' Equity: Common stock, par value $0.001; ( 40,000,000 shares authorized, 18,817,406

shares issued, 17,285,73 7 shares outstanding, respectively) Additional paid-in capital Treasury Stock, 1,531,669 shares, at cost

Accumulated deficit Total Stockholders' Equity

Total Liabilities and Stockholders' Equity

$

$

$

2,280,190

395,480 24,293 18,750

349,272 3,067,985

4,274,216

3,195,433 862,049 619,683 312,181 131,953

5,121,299

12,463,500

59,511 132,787

4,147 1,874,912 2,071,357

681,144 681,144

2,752,501

18,818 31,364,466

1,397,216) 20,275,069)

9,710,999

$=~1~2~,4,;;,;63~,5;,;;0,;,0

See accompanying notes and independent accountants' review report 2

LITTLEFIELD CORPORATION

CONSOLIDATED STATEMENT OF INCOME

UNAUDITED

FOR THE YEAR ENDED DECEMBER 31, 2015

REVENUE

COST OF REVENUE Salaries and other compensation Rent and utilities Other direct operating expenses Depreciation and amortization License expense

Total Cost of Revenue

GROSS PROFIT

GENERAL AND ADMINISTRATIVE EXPENSES Salaries and other compensation Legal and accounting fees Depreciation and amortization

Other general and administrative

Total General and Administrative Expenses

INCOME (LOSS) FROM OPERATIONS

OTHER INCOME (EXPENSE) Interest income

Interest expense

Other, net

Total Other Income (Expense)

INCOME (LOSS) BEFORE PROVISION FOR INCOME TAXES

PROVISION FORT AXES Federal income taxes State taxes

Total Provision For Income Taxes

NET INCOME (LOSS)

EARNINGS (LOSS) PER SHARE:

Basic earnings (loss) per share

Weighted average shares outstanding - basic

$ 4,674,825

50,198 1,830,852 1,080,138

518,550 51 ,167

3,530,905

1,143,920

630,500 106,675 39,031

310,266

1,086,472

57,448

33,886

104,128)

150,539

80,297

137,745

18,353 65,138

83,491

$.===,;;.54.;J;,2;;;;5;.;4

$===,;,;0·,;,00;;,;;3,;.1

17,285,737

See accompanying notes and independent accountants' review report 3

BALANCE, DECEMBER 31, 2014, AS PREVIOUSLY REPORTED

Prior period adjustments

BALANCE, DECEMBER 31, 2014, RESTATED

Net income (loss)

BALANCE, DECEMBER 31, 2015

LITTLEFIELD CORPORATION

CONSOLIDATED STATEMENT OF STOCKHOLDERS' EQUITY

UNAUDITED

FOR THE YEAR ENDED DECEMBER 31, 2015

Common Stock Additional Number of Paid-in Treasury

Shares Amount Capital Stock

17,285,737 $ 18,818 $ 31,364,466 $( 1,397,216)

- - - -

17,285,737 18,818 31,364,466 ( 1,397,216)

- - -

17,285,737 $ ~.818 $ 31,364,466 $ (1,397,216)

See accompanying notes and independent accountants' review report 4

Total Accumulated Stockholders'

Deficit Equity

$( 20,833,371) $ 9,152,697

504,048 504,048

( 20,329,323) 9,656,745

54,254 54,254

$( 20,275,069) $ 9,710,999

LITTLEFIELD CORPORATION CONSOLIDATED STATEMENT OF CASH FLOWS

UNAUDITED

FOR THE YEAR ENDED DECEMBER 31, 2015

CASH FLOWS FROM OPERATING ACTIVITIES Net income (loss) Adjustments to reconcile net income (loss) to

net cash provided (used) by operating activities: Depreciation and amortization

Increase (decrease) in cash flows as a result in changes in operating assets and liabilities:

Accounts receivable Deferred tax asset Other assets Accounts payable Deferred revenue Accrued expenses and other liabilities

Net Cash Provided (Used) by Operating Activities

CASH FLOWS FROM INVESTING ACTIVITIES Purchase of property and equipment Proceeds from repayment of notes receivable

Net Cash Provided (Used) by Investing Activities

CASH FLOWS FROM FINANCING ACTIVITIES Payments on notes payable

Net Cash Provided (Used) by Financing Activities

NET INCREASE (DECREASE) IN CASH

CASH, BEGINNING OF YEAR

CASH, END OF YEAR

SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION

Cash paid during the year for interest

Cash paid during the year for income taxes

$

(

(

(

( (

54,254

557,581

71,464) 18,353 10,985 74,404)

691 51,010

547,006

57,261) 406,947 349,686

145,515) 145,515)

751 177

1,529,013

$=~2~,2;.;:_80;:.b, 1;;.;_9..;_0

$==~1;,;,04~·,;;;;12;;.8

$"=====

See accompanying notes and independent accountants' review report 5

LITTLEFIELD CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2015

1. NATURE OF OPERATIONS

Littlefield Corporation actively participates in the U.S. charitable bingo market. The Company's corporate headquarters is located in Waco, Texas, and the Company operates primarily through wholly owned subsidiaries in Texas, Alabama and Florida. The Company generates its revenues from bingo centers in these three states.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Accounting Method

The financial statements of the Company have been prepared on the accrual basis of accounting and, accordingly, reflect all significant receivables, payables and other liabilities in accordance with generally accepted accounting principles.

Codification

The Financial Accounting Standards Board's (FASB) Accounting Standards Codification (ASC) is the single official source of authoritative, nongovernmental U. S. generally accepted accounting principles (GAAP).

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of Littlefield Corporation and its seventy-one subsidiaries (herein collectively referred to as the "Company"). All significant intercompany accounts and transactions have been eliminated in the consolidation

Use of Accounting Estimates

Management uses estimates and assumptions in preparing these financial statements in accordance with generally accepted accounting principles. Those estimates and assumptions affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities, and the reported revenues and expenses. Actual results could vary from the estimates that were used. Key significant estimates of the Company include allowance for uncollectible accounts receivable, depreciable lives of fixed assets, deferred tax valuation allowance, and amortization period of intangible assets.

See independent accountants' review report 6

Cash and Cash Equivalents

The indirect method is used to prepare the statement of cash flows. For the purposes of this statement, the Company considers cash in bank and all highly liquid investments with original maturity of three months or less at the date of acquisition to be "cash equivalents."

Accounts Receivable

Accounts receivable consist of amounts due from charitable organizations that conduct bingo events at the company's various bingo centers and are generally payable within one month of the event. Receivables also include rent due from operators of concessions located within certain bingo centers. Accounts receivable are not secured and are stated net of an allowance for doubtful accounts. Management provides an allowance for doubtful accounts, which reflects its estimate of the uncollectible receivables. Management determines if accounts are uncollectible based on the age of the account and past experience. For the year ended December 31, 2015, the allowance for doubtful accounts was $115,407.

Notes Receivable

Notes receivable are stated at the outstanding principal amount net of allowance for uncollectible notes. Management determines the allowance for uncollectible notes based on the review of outstanding amounts, historical collection information and existing economic conditions. Outstanding notes accrue interest based on the terms of the respective note agreements. Overdue notes are placed on nonaccrual status when management determines there is substantial doubt as to the total collectability of the note. Notes are written off when all collection efforts have been exhausted. Based on management's assessment, it has concluded that realization losses on balances outstanding at year end will be immaterial. Therefore, there was no allowance for uncollectible notes at December 31, 2015.

Property and Equipment

Property and equipment is recorded at cost, less accumulated depreciation. Depreciation for financial reporting is provided using the straight-line method over the following estimated useful lives:

Equipment, furniture and fixtures Buildings Building improvements

2-7 years 40 years

7-40 years

Leasehold improvements are amortized over the lesser of the remaining term of the lease or the estimated useful lives. For federal income tax purposes, depreciation is computed using the straight-line and accelerated depreciation methods.

Expenditures for major betterments that extend the useful lives of property and equipment are capitalized. Repair and maintenance costs that do not extend asset lives are expensed as incurred. When property and equipment are retired or otherwise disposed, the cost and accumulated depreciation are removed from the accounts and any resulting gain or loss is included in income for the respective year.

See independent accountants' review report 7

Goodwill and Intangible Assets

Intangible assets, which primarily consist of goodwill, bingo licenses and non-compete covenants resulting from the acquisition of bingo entities, are periodically reviewed by management to evaluate the future economic benefits or potential impairments, which may affect their recorded values. Goodwill represents the excess of the cost of assets acquired over the fair market value of those tangible assets on the date of their acquisition. Under the Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") 350, Intangibles, Goodwill and Other, goodwill acquired in a business combination for which the acquisition date is after June 30, 2001, shall not be amortized, but shall be reviewed for impairment in value annually. The Company has defined a single operating segment in that the Company's operations share similar economic characteristics and similar customers, among other characteristics.

Since 2002, goodwill and intangible assets with indefinite lives are no longer amortized. These indefinite-lived assets only pertain to halls in the state of Texas. The Company has one class of assets that is classified as indefinite and not subject to periodic amortization. This class of asset is known as a "Grandfathered license." In discussing these Grandfathered licenses, a distinction should be made as to the types of bingo licenses the Company owns. There are two classes of commercial lessor licenses in Texas, Grandfathered and a Tier. The Grandfathered license refers to any license that was in existence prior to 1989 in which a non-renewal has not occurred.

A Grandfathered license allows the operator to have up to seven (7) charities in a hall and charge up to $600 per session in rent. These licenses are regulated by the Texas Lottery Commission and must be renewed at least annually. There is an annual fee associated with the renewal of these licenses, which is expensed throughout the year. There are a limited number of these licenses available and they are traded between individuals and organizations. They are a traded commodity, in that they have a cash value which is determined by the market place. These licenses can only be revoked or canceled by failing to renew them by the renewal date or for illegal activity.

A Tier license is deemed by the Company to have no value as an asset and is not recorded as an asset. A Tier commercial lessor license is any license issued after 1989 or any license issued prior to 1989 in which a non-renewal occurred. A Tier license allows the operator to have one (1) charity in a hall and charge up to $600 per session in rent. These licenses are issued, renewed, and applied for through the Texas Lottery Commission. The only cost associated with obtaining and keeping this type of license is an annual renewal fee, which is expensed throughout the year. These licenses are not sold on a negotiated basis, at this time.

In Alabama, there is a business license which is based upon the gross amount of rents, these are renewed annually and expensed during the year. These licenses are not recorded as assets and, therefore, have no related amortization.

Non-compete covenants are amortized over the periods of the stated benefits, ranging from one to five years, and are monitored for contractual compliance. If the projected and undiscounted future cash flows related to the intangible assets are less than the recorded value, the intangible asset is written down to fair value.

See independent accountants' review report 8

Compensated Absences

The Company does not provide compensated vacation or sick pay for employees. Therefore, no amount has been accrued in the financial statements for the year ended December 31, 2015.

Advertising Expenses

The Company has the policy of expensing advertising costs as incurred. Advertising costs charged to expenses were $92,360 in 2015.

Revenue Recognition

The Company generates revenues from rental income and other revenue sources such as concessions, vending machines, bingo supplies and other sources. Rental revenues are accrued and accounted for in the month that they are due and realizable. Other revenues are recognized in the month they are earned when collectability is probable.

Income Taxes

Deferred income tax assets and liabilities are recognized for the expected future tax consequences of temporary differences between the tax basis and financial reporting carrying amounts of assets and liabilities. The Company periodically evaluates its deferred tax assets and adjusts any related valuation allowance based on the estimate of the amount of such deferred tax assets which the Company does not believe will meet the "more-likely-than-not" recognition criteria. At December 31, 2015, the Company did not recognize a liability for uncertain tax positions. The Company does not expect its unrecognized tax benefits to change significantly over the next twelve months. The Company's income tax returns for 2013-2015 are open to examination by the IRS and 2012-2015 for the States of Texas, Alabama, Florida and Delaware.

Per Share Data

Basic earnings (loss) per share of common stock is calculated by dividing net income (loss) available to common stockholders by the weighted average number of common shares actually outstanding during each period. Diluted earnings (loss) per share of common stock is calculated by dividing net income (loss) by the fully diluted weighted average number of common shared outstanding during each period, which includes dilutive stock options and convertible shares.

Fair Value of Financial Instruments

The Company's financial instruments consist primarily of cash, accounts receivable, notes receivable and accounts payable. The carrying amounts of these instruments reported in the balance sheet as current are considered to approximate their respective fair values due to the short-term nature of such financial instruments.

See independent accountants' review report 9

3. CONCENTRATION OF CREDIT RISK

The Company mainly maintains its cash and certificates of deposit in banks which are insured by the Federal Deposit Insurance Corporation ("FDIC") up to $250,000. At December 31, 2015, approximately $1,454,681, of cash in banks exceeded FDIC coverage limits.

The Company generates its revenues exclusively from the bingo market in the states of Texas, Alabama and Florida. The concentration of credit risk may be affected by changes in the local and federal economy or other conditions of the bingo market.

4. NOTES RECEIVABLE

Notes receivable at December 31, 2015 consists of the following:

Note receivable from borrower, due in quarterly installments of$79,019, including a fixed interest rate of3%, maturing June 30, 2018, secured by stock or membership in limited liability companies

Note receivable from borrower, due in monthly installments of $1,333, including a fixed interest rate of 4%, maturing July 1, 2029, secured by a guaranty agreement

Note receivable from borrower, due in monthly installments of $8,765, including a fixed interest rate of 6%, maturing May 10, 2016, unsecured

Less current maturities

Notes receivable, net of current portion

2015

$ 758,551

167,228

43,176

968,955 ( 349,272)

$ 619,683

Payments received on long-term receivables for each of the next five fiscal years and thereafter are as follows:

Years ending December 31, 2016 2017 2018 2019 2020

Thereafter

$ 349,272 315,481 166,527

10,664 11,099

115,912

$==...;_9...;_68~,9~5=5

See independent accountants' review report 10

5. PROPERTY AND EQUIPMENT

Property and equipment at December 31,2015 consists ofthe following:

2015

Land $ 740,468

Buildings 3,459,541

Leasehold improvements 5,455,239

Equipment, furniture and fixtures 2,902,131

Automobiles 136,162

12,693,541

Less accumulated depreciation ( 8,419,325)

$ 4,274,216

Depreciation expense of property and equipment charged to operations for the year ended December 31, 2015 was $4 79,248.

6. GOODWILL AND OTHER INTANGIBLE ASSETS

Goodwill at December 31, 2015 is as follows:

Gross Carrying Accumulated

Amount Amortization

Goodwill at December 31, 2014 $ 3,848,667 $( 653,234)

Goodwill acquired during period Goodwill impairment losses

Goodwill at December 31, 2015 $ 3,848,667 $( 653,234)

See independent accountants' review report 11

Total

$ 3,195,433

$ 3,195,433

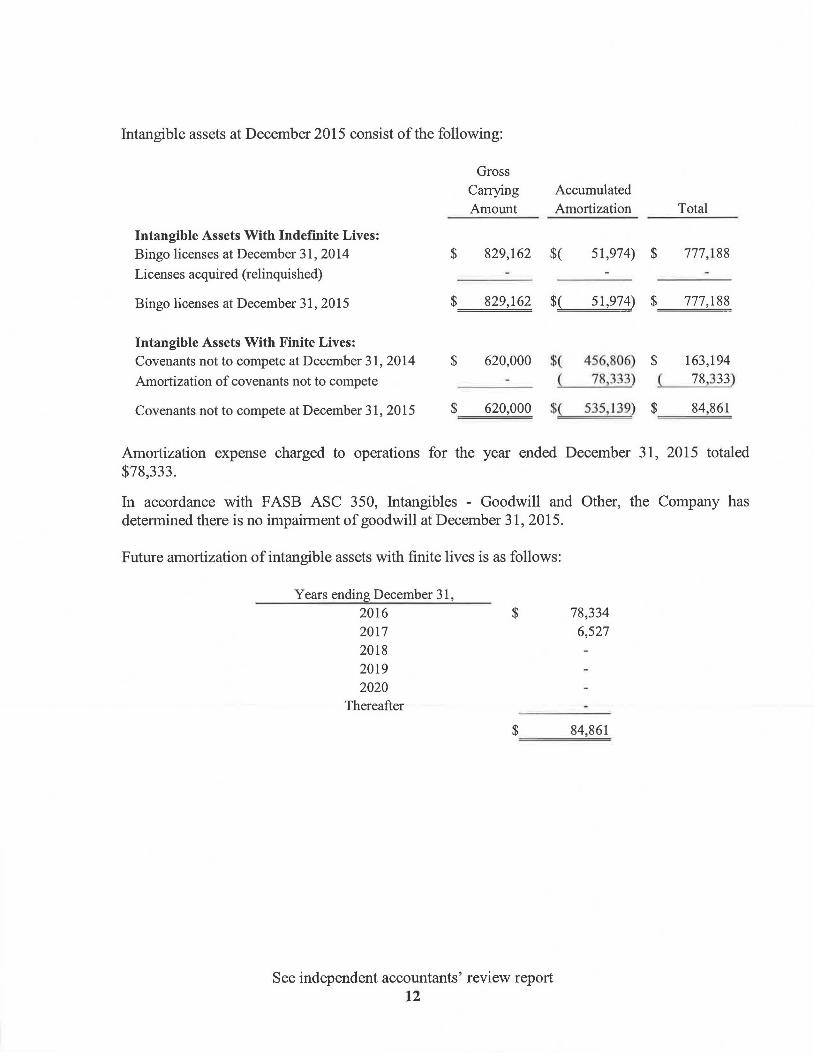

Intangible assets at December 2015 consist of the following:

Gross Carrying Accumulated

Amount Amortization Total

Intangible Assets With Indefinite Lives: Bingo licenses at December 31,2014 $ 829,162 $( 51,974) $ 777,188

Licenses acquired (relinquished)

Bingo licenses at December 31, 2015 $ 829,162 $( 51,974) $ 777,188

Intangible Assets With Finite Lives: Covenants not to compete at December 31, 2014 $ 620,000 $( 456,806) $ 163,194

Amortization of covenants not to compete { 78,333) ( 78 333)

Covenants not to compete at December 31, 20 15 $ 620,000 $~ 535, 139) $ 84,861

Amortization expense charged to operations for the year ended December 31, 2015 totaled $78,333.

In accordance with FASB ASC 350, Intangibles - Goodwill and Other, the Company has determined there is no impairment of goodwill at December 31, 2015.

Future amortization of intangible assets with finite lives is as follows:

Years ending December 31, 2016 $ 2017 2018 2019 2020

Thereafter

$

See independent accountants' review report 12

78,334 6,527

84,861

7. LONG-TERM DEBT

Long-term debt at December 31, 2015 consists of the following:

Note payable to the bank, due in monthly installments of $16,398, including interest at approximately 4.65% (bank interestbearing liabilities index plux 4.00%), maturing December 2016, secured by real estate and stockholder guarantee. *

Mortgage note payable to a bank, due in monthly installments of $4,454, including interest at 4.50%, maturing July 2019, secured by a deed of trust on the real estate.

Installment note payable to a third party, due in annual installments of $36,667, unsecured, maturing January 2017.

Less current maturities

Long-term debt, net of current portion

2015

$ 1,838,245

$

644,478

73,333

2,556,056 ( 1,874,912)

681,144

* The Company renewed the note for an additional year and intended to renew the note again before its maturity date. Subsequent to year end, the Company sold the real estate held as collateral and paid the outstanding balance in full as noted in Note 12.

Interest expense for the year ended December 31, 2015 was $104,128.

Payments oflong-term debt for each of the next five fiscal years and thereafter are as follows:

Years ending December 31, 2016 $ 1,874,912

2017 61,178

2018 25,655 2019 594,311 2020

Thereafter

$ 2,556,056

See independent accountants' review report 13

8. STOCKHOLDERS' EQUITY

The total authorized number of shares that the Company may issue is 40,000,000 shares of $0.001 par value stock, 18,817,406 shares are issued, and 17,285,737 shares are outstanding as of December 31, 2015. The Company holds 1,531,669 shares as treasury stock as of December 31, 2015.

On February 6, 2013, the company voluntarily terminated its registration under Section 12 of the Securities Exchange Act of 1934 (the "Exchange Act") and ceased filing periodic and current reports with the Securities and Exchange Commission (the "SEC"). The Company determined that it had only 105 stockholders ofrecord as of February 5, 2013. Accordingly, the Company filed a Form 15 with the SEC pursuant to Rule 12h-3(b)(1)(i), to notify the SEC of the suspension of its duty to file reports under the Exchange Act. The company was current in all of its filing obligations under the Exchange Act at that time.

In 2015, the company did not issue shares of treasury stock under the Employee Stock Purchase Plan and 401 (k) Plan. Furthermore, the Company had no stock-based compensation and did not issue stock options for the year ended December 31,2015.

9. INCOME TAXES

Significant components of the Company's deferred tax assets and liabilities at December 31, 2015 were as follows:

Deferred tax assets Deferred tax liability Valuation allowance for deferred tax asset

$

2015

4,101,775

( 478,263) ( 3,292,581)

330,931

These amounts have been presented in the financial statements as follows :

Current deferred tax asset $ 18,750

Non-current deferred tax asset 312,181

See independent accountants' review report 14

$ 330,931

The components of for deferred tax assets (liabilities) at December 31, 2015 are as follows:

Deferred tax asset (liability)

Net operating loss carryforward

Depreciation

Allowance for doubtful accounts

Section 1231 loss carryforward Valuation allowance

2015

$ 3,809,784

( 478,263)

28,852 263,139

( 3,292,581)

$ 330,931

The company does not expect to incur material federal income tax charges until the depletion of its accumulated federal income tax loss carry-forwards. At December 31, 2015, the company has net operating loss carry forwards for federal income tax purposes of approximately $15,239,000 million that begin expiring in the year 201 7.

10. COMMITMENTS AND CONTINGENCIES

Operating Leases

See independent accountants' review report 15

See independent accountants' review report 16

The Company is obligated under various operating leases. Generally, the leases provide for minimum annual rentals as well as a proportionate share of the real estate taxes, insurance, and certain common area charges. Minimum annual rentals under these leases are as follows:

Minimum Year Ended December 31 Rentals

2016 $ 1,271,096

2017 1,175,784

2018 897,902

2019 689,825

2020 625,687 Thereafter 1,644,842

$ 6,305,136

Rent expense for the years ended December 31,2015 amounted to approximately $1,631,653. Included in the rent expense, the Company paid $262,933 in 2015 for common area maintenance.

The Company is party to certain subleases requiring monthly rent. The minimum annual future receipts under these subleases are as follows:

Year Ended December 31 , 2016 2017 2018

2019 2020

Thereafter

Minimum Rentals

$ 18,000

$ 18,000

The Company is subject to various claims, legal proceedings, and investigations covering a wide range of matters that arise in the ordinary course of business. In the opinion of management, all such matters are adequately covered by insurance or by accruals and, if not so covered, are without merit or are of such kind or involve such amounts that would not have a significant effect on the financial position or results of operations of the Company if disposed of unfavorably. As of December 31, 2015, the Company is involved in ongoing mediation that is expected to be adequately covered by insurance.

See independent accountants' review report 17

11. PRIOR PERIOD ADJUSTMENT

Certain errors resulting in an understatement of previously reported notes receivable and net deferred tax asset and an overstatement of previously reported accounts payable were discovered during the current year. Accordingly, an adjustment of$129,764, $349,284 and $25,000 was made during 2015 to restate notes receivable, net deferred tax assets and accounts payable, respectively, as of the beginning of the year. A corresponding entry was made to increase previously reported retained earnings by $504,048.

12. SUBSEQUENT EVENTS

Subsequent to year end, the Company sold the real estate held as collateral on a long-term note payable. As of December 1, 2016 the funds are being held by a 1031 intermediary in contemplation of reinvesting in a replacement property.

Management has evaluated subsequent events through December 1, 2016, the date on which the financial statements were available to be issued.

See independent accountants' review report 18