liquidity analysis and reportingeoplugin.commpartners.com/fms/liquidity analysis and...

TRANSCRIPT

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning

Insert speaker logo here

www.fmsinc.org | 800-ASK-4FMS

Liquidity Analysis and Reporting

Jerry Boebel, CFAProfitStars

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Objectives• Define liquidity

• Current trends

• Evaluate traditional liquidity analysis

• Consider a new approach

– Better liquidity and NIM management

– Meet changing examiner expectations

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Liquidity

• Essential to compensate for expected and unexpected balance sheet fluctuations and provide funds for growth

• Liquidity risk occurs when you are not able to obtain funds at the optimal price within a reasonable time period to meet obligations as they become due

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Current Trends

• In Q2 2008, the securitization market froze

• Finance units that used to sell commercial paper to fund their lending started going after your deposits

• GMAC (now Ally Bank)

• ING

• Brokered deposits became more expensive (relative to asset yields)

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

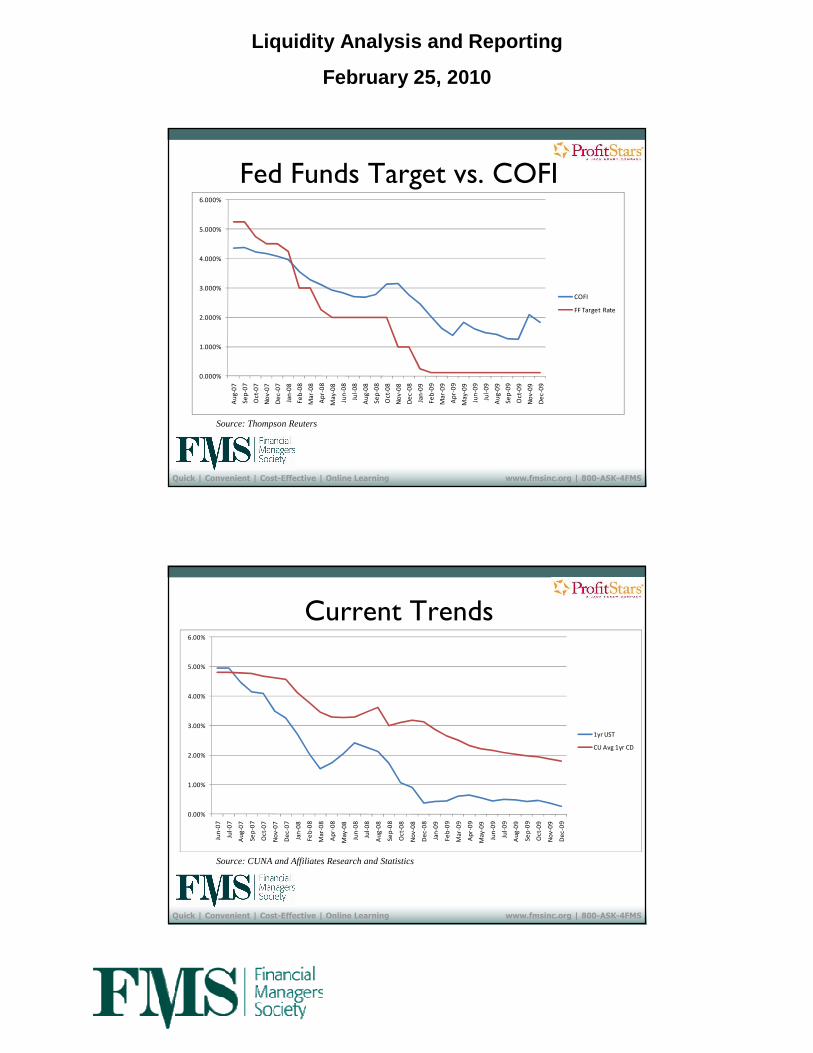

Fed Funds Target vs. COFI

Source: Thompson Reuters

0.000%

1.000%

2.000%

3.000%

4.000%

5.000%

6.000%

Au

g-0

7

Se

p-0

7

Oct-

07

No

v-0

7

De

c-0

7

Jan

-08

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

Ma

y-0

8

Jun

-08

Jul-

08

Au

g-0

8

Se

p-0

8

Oct-

08

No

v-0

8

De

c-0

8

Jan

-09

Fe

b-0

9

Ma

r-0

9

Ap

r-0

9

Ma

y-0

9

Jun

-09

Jul-

09

Au

g-0

9

Se

p-0

9

Oct-

09

No

v-0

9

De

c-0

9

COFI

FF Target Rate

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Current Trends

Source: CUNA and Affiliates Research and Statistics

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Jun

-07

Jul-

07

Au

g-0

7

Se

p-0

7

Oc

t-0

7

No

v-0

7

De

c-0

7

Jan

-08

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

Ma

y-0

8

Jun

-08

Jul-

08

Au

g-0

8

Se

p-0

8

Oc

t-0

8

No

v-0

8

De

c-0

8

Jan

-09

Fe

b-0

9

Ma

r-0

9

Ap

r-0

9

Ma

y-0

9

Jun

-09

Jul-

09

Au

g-0

9

Se

p-0

9

Oc

t-0

9

No

v-0

9

De

c-0

9

1yr UST

CU Avg 1yr CD

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

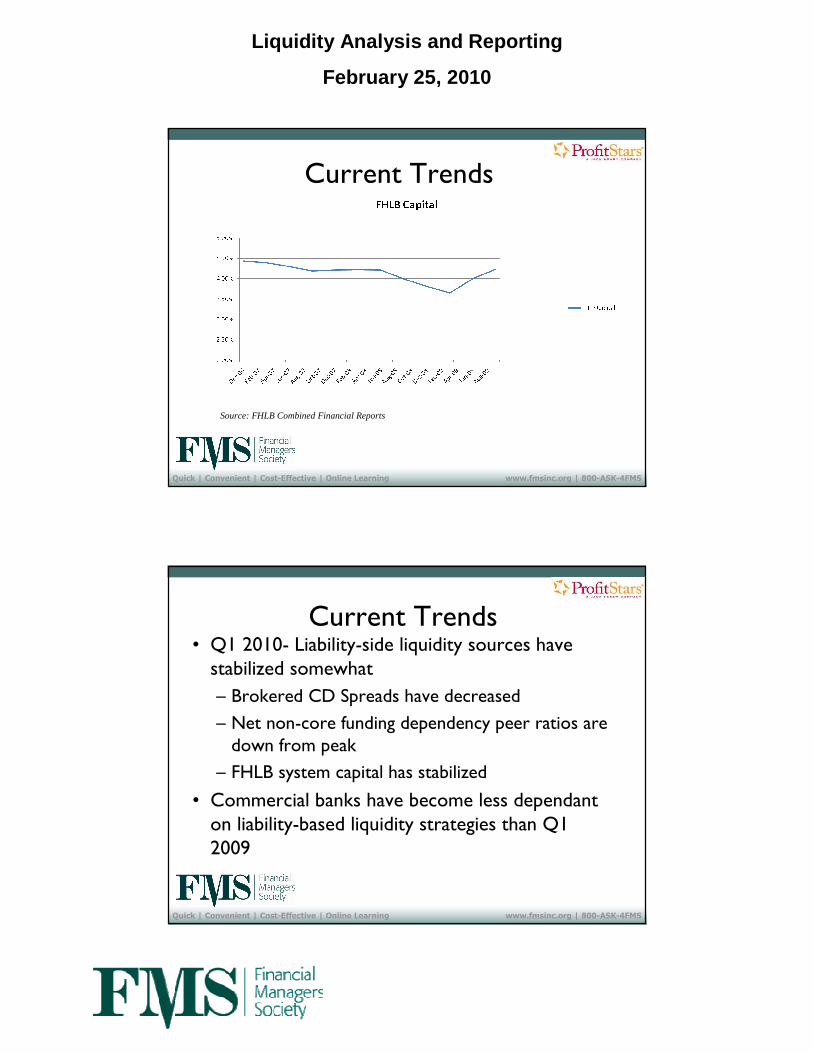

Current Trends

Source: FHLB Combined Financial Reports

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Current Trends• Q1 2010- Liability-side liquidity sources have stabilized somewhat

– Brokered CD Spreads have decreased

– Net non-core funding dependency peer ratios are down from peak

– FHLB system capital has stabilized

• Commercial banks have become less dependant on liability-based liquidity strategies than Q1 2009

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

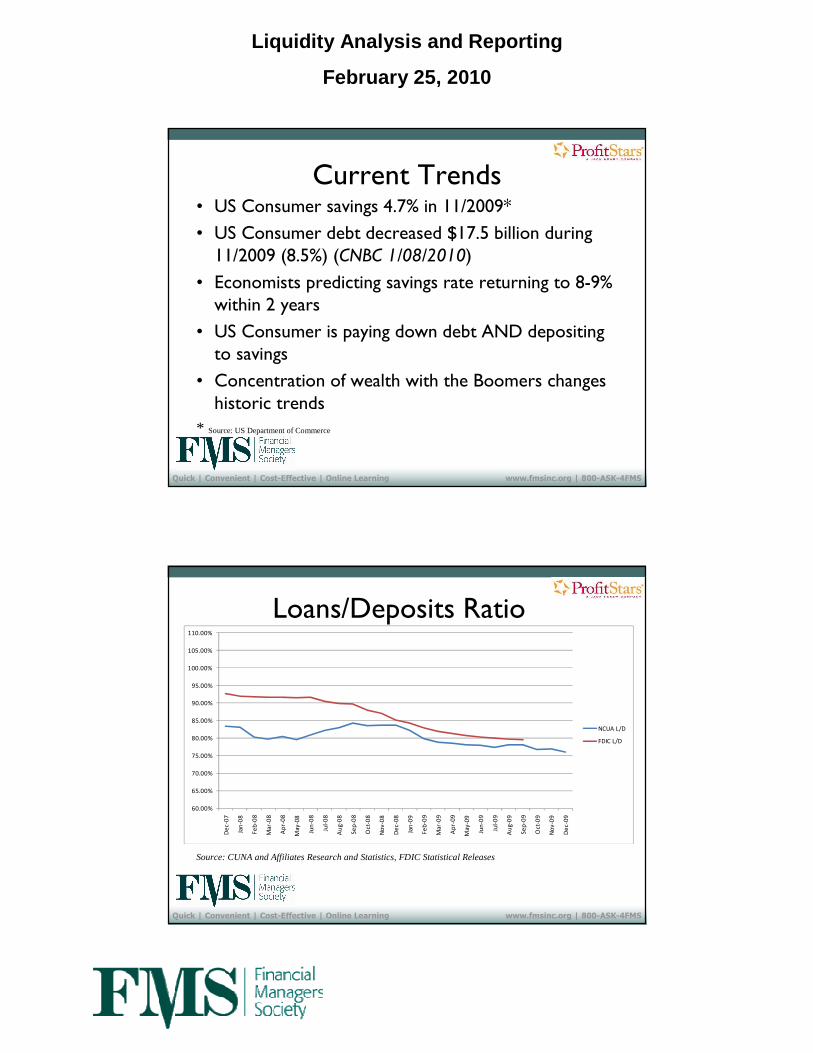

Current Trends• US Consumer savings 4.7% in 11/2009*

• US Consumer debt decreased $17.5 billion during 11/2009 (8.5%) (CNBC 1/08/2010)

• Economists predicting savings rate returning to 8-9% within 2 years

• US Consumer is paying down debt AND depositing to savings

• Concentration of wealth with the Boomers changes historic trends

* Source: US Department of Commerce

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Loans/Deposits Ratio

Source: CUNA and Affiliates Research and Statistics, FDIC Statistical Releases

60.00%

65.00%

70.00%

75.00%

80.00%

85.00%

90.00%

95.00%

100.00%

105.00%

110.00%

De

c-0

7

Jan

-08

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

May

-08

Jun

-08

Jul-

08

Au

g-0

8

Se

p-0

8

Oct-

08

No

v-0

8

De

c-0

8

Jan

-09

Fe

b-0

9

Ma

r-0

9

Ap

r-0

9

May

-09

Jun

-09

Jul-

09

Au

g-0

9

Se

p-0

9

Oct-

09

No

v-0

9

De

c-0

9

NCUA L/D

FDIC L/D

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Current Trends

• Will the funding always be there?– Retail deposit growth is very competitive

– Wholesale funds have regulatory stigma

• Regulation is pointing towards bringing back the traditional depository structure

• Failure to consider long-term liquidity will compress NIM

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Traditional Liquidity Analysis

• Asset Liquidity

– Investment sales

– Loan securitizations

– Collateral for borrowings

• Liability Liquidity

– Borrowing capabilities

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

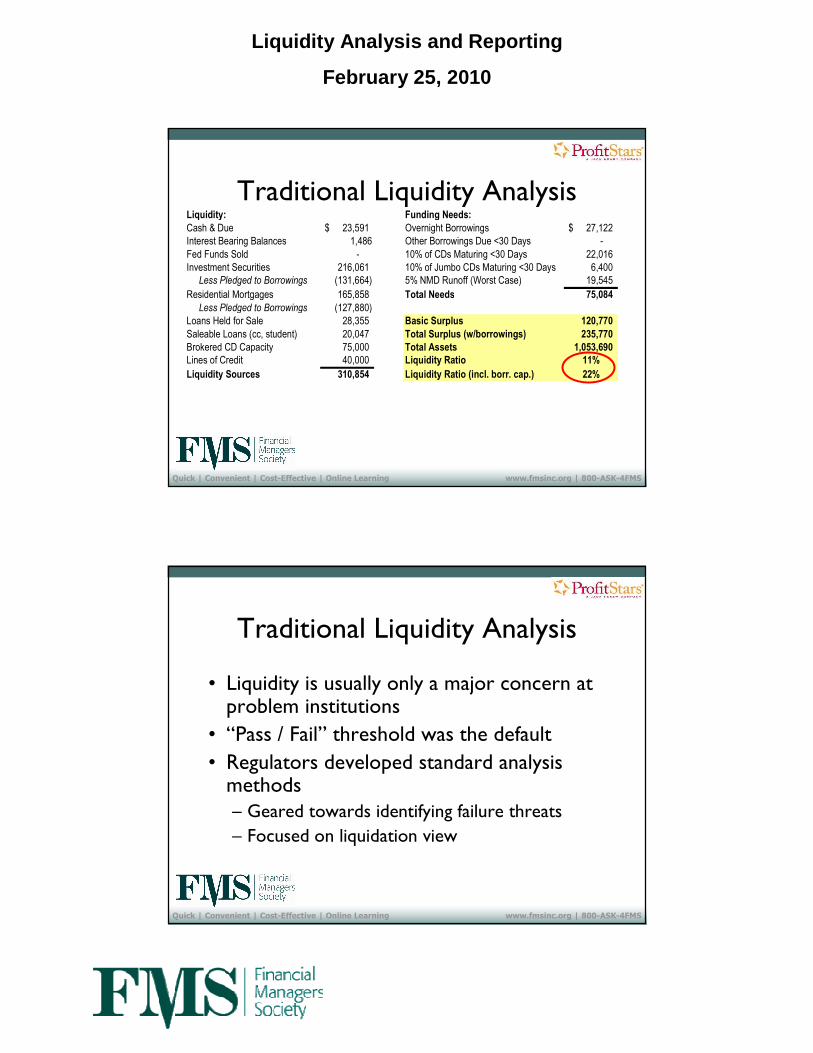

Liquidity: Funding Needs:

Cash & Due 23,591$ Overnight Borrowings 27,122$ Interest Bearing Balances 1,486 Other Borrowings Due <30 Days -

Fed Funds Sold - 10% of CDs Maturing <30 Days 22,016 Investment Securities 216,061 10% of Jumbo CDs Maturing <30 Days 6,400 Less Pledged to Borrowings (131,664) 5% NMD Runoff (Worst Case) 19,545

Residential Mortgages 165,858 Total Needs 75,084

Less Pledged to Borrowings (127,880) Loans Held for Sale 28,355 Basic Surplus 120,770

Saleable Loans (cc, student) 20,047 Total Surplus (w/borrowings) 235,770

Brokered CD Capacity 75,000 Total Assets 1,053,690

Lines of Credit 40,000 Liquidity Ratio 11%

Liquidity Sources 310,854 Liquidity Ratio (incl. borr. cap.) 22%

Traditional Liquidity Analysis

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Traditional Liquidity Analysis

• Liquidity is usually only a major concern at problem institutions

• “Pass / Fail” threshold was the default

• Regulators developed standard analysis methods– Geared towards identifying failure threats

– Focused on liquidation view

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Traditional Liquidity Analysis

• Focus had historically been on static measures– Short-Term Assets to Short-Term Liabilities

– Pledged Securities to Total Securities

– Brokered Deposits to Deposits

– Core Deposits to Total Liabilities

– Net Loans and Leases to Deposits

– Net Loans and Leases to Total Assets

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Current Liquidity Analysis

• Focus has evolved to evaluate broader measures and trends– Net Short-Term Non Core Funding Dependence

– Net Non-Core Funding Dependence Ratio

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

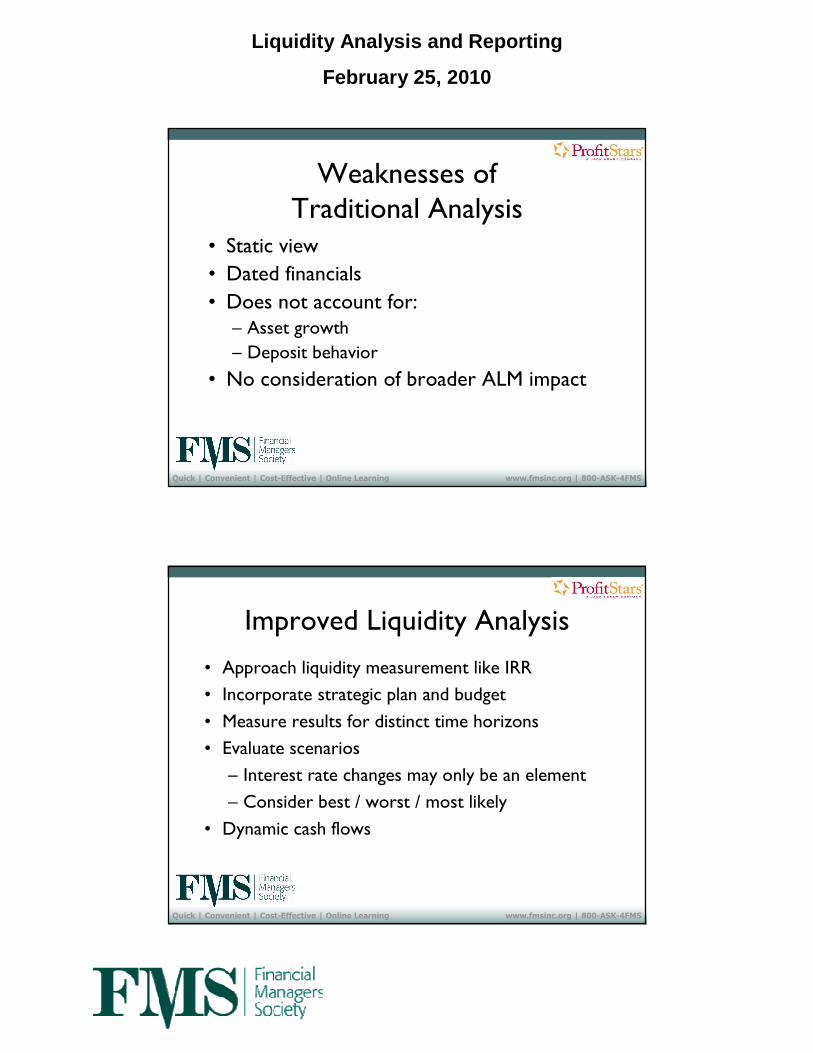

Weaknesses of Traditional Analysis

• Static view

• Dated financials

• Does not account for:– Asset growth

– Deposit behavior

• No consideration of broader ALM impact

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Improved Liquidity Analysis

• Approach liquidity measurement like IRR

• Incorporate strategic plan and budget

• Measure results for distinct time horizons

• Evaluate scenarios

– Interest rate changes may only be an element

– Consider best / worst / most likely

• Dynamic cash flows

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Step 1: Compile Realistic Numbers

• Separate internal liquidity sources from external sources– Makes it easier to do scenario testing– Examiners wish to focus on your internal capabilities

• Use your budget projections that are built into your ALM model

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Step 1: Compile Realistic Numbers• Cash & Due is not completely liquid• Determine true asset sale/pledge values– Show at current market values– Haircuts often apply for pledging– Many loan types require time to liquidate

• Accurately reflect borrowing capacity– FHLB or Corporate CU lines should be questioned– FHLB-required stock purchases should be netted– Brokered deposits take several days to settle

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

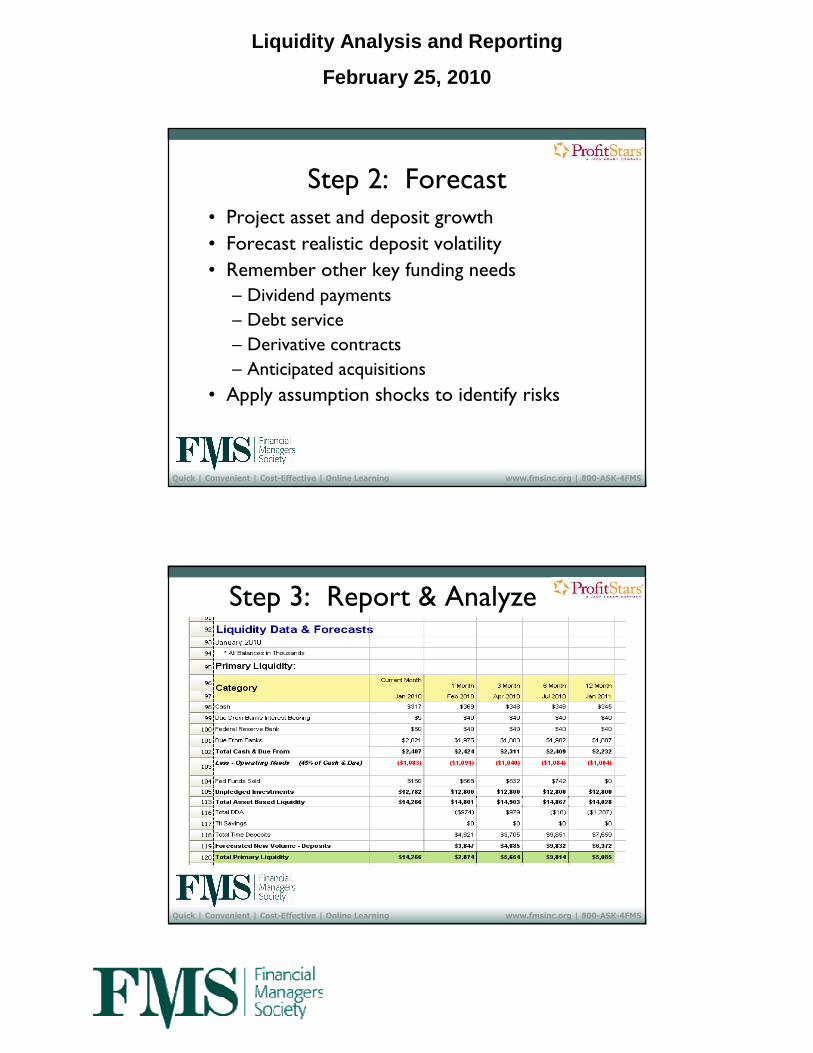

Step 2: Forecast• Project asset and deposit growth

• Forecast realistic deposit volatility

• Remember other key funding needs

– Dividend payments

– Debt service

– Derivative contracts

– Anticipated acquisitions

• Apply assumption shocks to identify risks

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Step 3: Report & Analyze

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Step 3: Report & Analyze

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

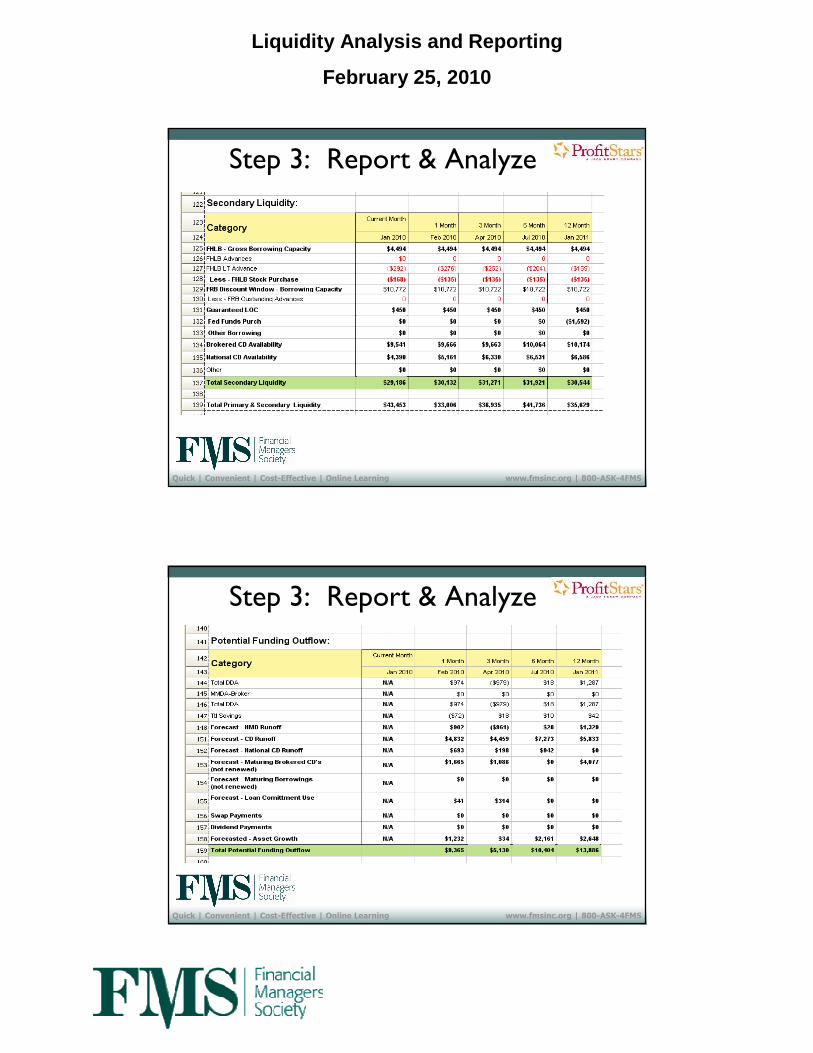

Step 3: Report & Analyze

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Step 3: Report & Analyze

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

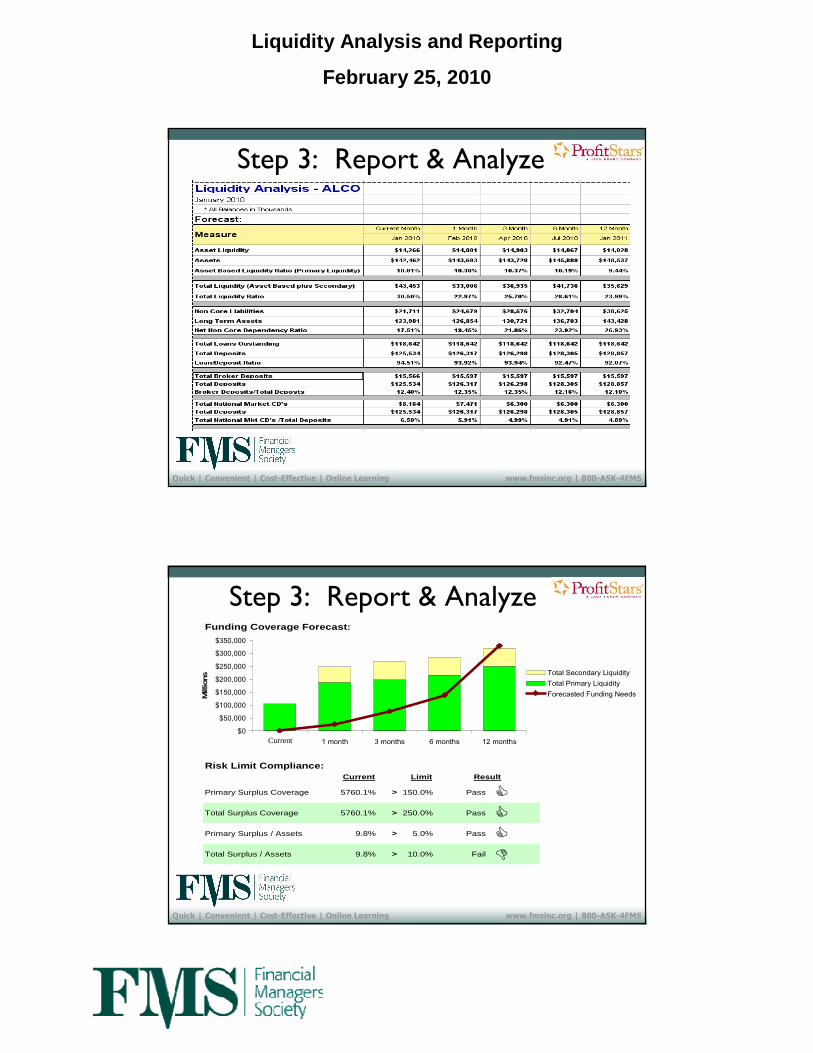

Step 3: Report & AnalyzeFunding Coverage Forecast:

Risk Limit Compliance:Current Limit Result

Primary Surplus Coverage 5760.1% > 150.0% Pass �

Total Surplus Coverage 5760.1% > 250.0% Pass �

Primary Surplus / Assets 9.8% > 5.0% Pass �

Total Surplus / Assets 9.8% > 10.0% Fail �

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

09/30/04 1 month 3 months 6 months 12 months

Mill

ions Total Secondary Liquidity

Total Primary Liquidity

Forecasted Funding Needs

Current

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Examiner Expectations

• What if:

– Lines of credit are reduced or closed

– Brokered market is unavailable

– Retail deposits runoff

• What if all of the above occur?

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Benefits• Integrates liquidity management into ALM program

• Forward-looking and dynamic

• Enables evaluation of impact on NIM from funding options

• Helps ALCO members see choices more clearly

• Demonstrates more sophisticated approach to liquidity management

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Resources Needed

• Reasonable budget process

– Includes input from functional areas

– Includes identification of key cash flow issues

• Effective forecasting model

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

Jerry Boebel, CFA

Profitstars (a Jack Henry Company)

800-356-9099

Liquidity Analysis and Reporting

February 25, 2010

Quick | Convenient | Cost-Effective | Online Learning www.fmsinc.org | 800-ASK-4FMS

The Financial Managers Society, Inc. is the only individual membership society exclusively devoted to serving the needs of finance & accounting professionals from financial institutions. Our more than 1,500 members are CFOs, controllers, CEOs, COOs, treasurers, investment officers and internal auditors from banks, thrifts and credit unions.

FMS offers career-enhancing education, targeted news and research, national leadership opportunities, a voice in shaping regulations and accounting principles and connections with other industry professionals.

MissionThe mission of the Financial Managers Society is to enhance the professional development of financial personnel within financial institutions.

The Society accomplishes this mission by: •Offering premier education and information to members and others within the financial services industry regarding accounting, financial management, regulatory, operational, auditing and other industry issues.

•Providing various forums for the exchange of information and practical applications.

•Articulating industry and member concerns to regulatory and accounting policy-setting bodies.

•Providing members with opportunities for technical, personal, and leadership growth and development.

About FMS