life insurance m&a - member | soa life industry has traded-off materially as a result of...

TRANSCRIPT

Session 159 PD, Life Insurance M&A

Moderator:

David J. Weinsier, FSA, MAAA

Presenters: Germante Boncaldo

Su Meng Lee, FSA, CERA, MAAA Philip Salem

SOA Antitrust Disclaimer SOA Presentation Disclaimer

© Oliver Wyman

Life Insurance M&A2016 Society of Actuaries Annual MeetingSession #159

October 26, 2016

1© Oliver Wyman 1

AgendaIn this session, a panel of experts will provide an overview of the North American life and annuity mergers and acquisitions (M&A) landscape

I. Introduction (David Weinsier, Oliver Wyman)a. Summary of recent transactionsb. Themes driving current and future M&A activity

II. Investment banker’s view (Philip Salem, Goldman Sachs) a. Challenges facing U.S. life insurers and how companies are respondingb. Life insurance segment analyticsc. Trends and drivers of M&A activity

III. Global reinsurer’s view (Germante Boncaldo, Swiss Re)a. Value proposition of reinsurance in M&Ab. Reinsurance as a capital management toolc. Reinsurance as a financing partner

IV. Actuarial consultant’s view (Su Meng Lee, Milliman) a. Buy-side support Phase 1: review opportunityb. Buy-side support Phase 2: evaluate targetc. Buy-side support Phase 3: closing

V. Q&A

2© Oliver Wyman 2

Recent DealsSeveral very large transactions closed in 2014 & 2015, however 2016 has been relatively quiet to date

3© Oliver Wyman 3

Regulatory change

International influence

• European/Canadian solvency requirements

• SIFI influence

Risk and capital• Diversification and scale

• Tax benefits

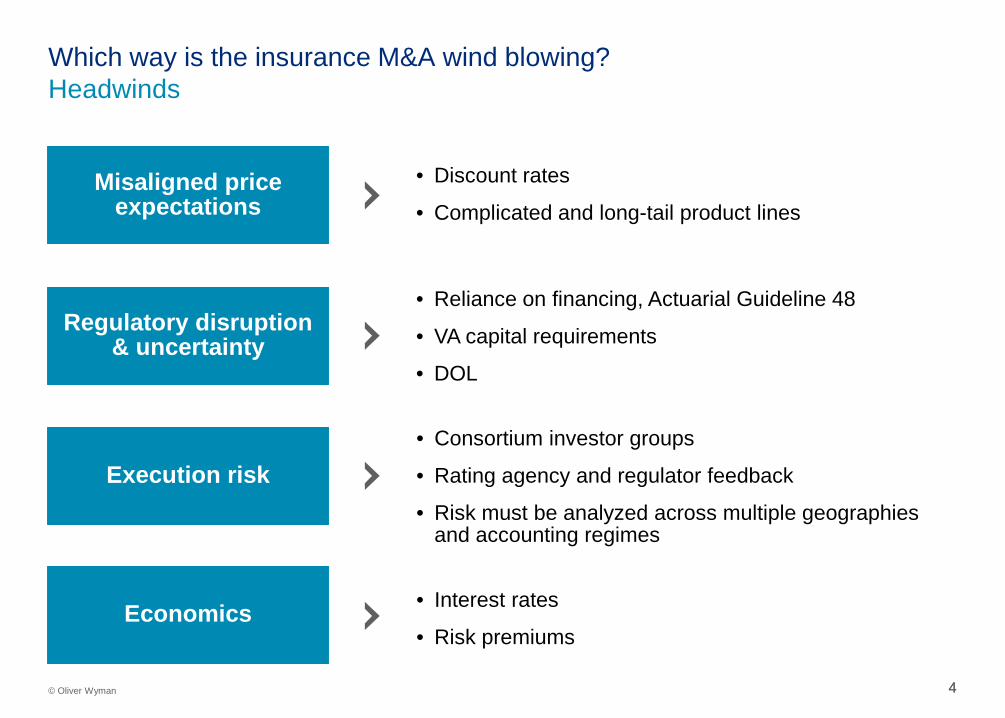

Which way is the insurance M&A wind blowing?Tailwinds

• Seeking non-domestic growth

• Currency discrepancies

• Offsets to low investment returns

Economics• Low cost of debt

• Excess capital

• Motivations to shed low ROE business

4© Oliver Wyman 4

Misaligned price expectations

Execution risk

• Discount rates

• Complicated and long-tail product lines

Regulatory disruption & uncertainty

• Reliance on financing, Actuarial Guideline 48

• VA capital requirements

• DOL

Which way is the insurance M&A wind blowing?Headwinds

• Consortium investor groups

• Rating agency and regulator feedback

• Risk must be analyzed across multiple geographies and accounting regimes

Economics • Interest rates

• Risk premiums

5© Oliver Wyman 5

Q&A

Life Insurance Trends

2016 Society of Actuaries Annual Meeting

October 26, 2016

1

U.S. Life Sector Facing Numerous Challenges

Challenging Macro-Economic Factors

Difficulty in Driving Revenue Growth

Mixed Demographic Trends

Emergence of New Entrants Driving Competition

Technology Emerging as a Disrupter

Growing Regulatory Pressures

Increased Shareholder Activism

A

B

C

D

E

F

G

2

Life Industry Has Traded-off Materially as a Result of Industry Pressures and Negative Sentiment

Source: Bloomberg, CapIQ, Company filings and SNL FinancialNote: Market data as of 20-Sep-2016.¹Protection Peers: Aflac, Unum, Torchmark, Primerica, CNO, Genworth and FBL Financial.²Accumulation Peers: MetLife, Prudential, Ameriprise, Principal Financial Group, Lincoln National, VOYA and American Equity.

CNO

UNM

AFL

PRI

GNW

TMK

FFG

MET

PRU

AMP

PFG

VOYA

LNC

AEL

50 %

60 %

70 %

80 %

90 %

100 %

0.00 x 0.50 x 1.00 x 1.50 x 2.00 x 2.50 x 3.00 x

% o

f 52

Wee

k H

igh

P/BV (ex. AOCI)Protection Peers¹ Accumulation Peers²

# of Companies: 7

# of Companies: 7

3

Industry ROEs Have Been Slowly RecoveringFY2 ROE Median Analyst Estimates │ 2004 to Current

Source: IBES as of 20-Sep-2016¹ Protection Peers include Primerica, Aflac, FBL Financial, Torchmark, CNO, Unum and Genworth (GNW excluded after 12/31/2007). ² Capital Intensive Accumulations Peers include Prudential, Lincoln, Metlife, VOYA and American Equity.³ Non-Capital Intensive Accumulation Peers include Principal and Ameriprise.4 Pre-Crisis goes from 01-01-2004 to 12-31-2007.5 Post-Crisis goes from 01-01-2010 to 20-09-2016.

Protection peer ROE’s have been more stable and are in-

line with pre-crisis levels

Capital intensive

peer ROE’s have not

recovered to pre-crisis

levels whereas

non-capital intensive

peers have exceeded pre-crisis

levels

7.0 %

9.0 %

11.0 %

13.0 %

15.0 %

17.0 %

19.0 %

21.0 %

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

FY2

RO

E

Protection Peers¹ Capital Intensive Accumulation Peers² Non-Capital Intensive Accumulation Peers³

Average Pre-Crisis4 Post-Crisis5 3YProtection Peers¹ 10.4 % 11.9 % 12.3 %Capital Intensive Accumulation Peers² 13.1 11.3 11.6Non-Capital Intensive Accumulation Peers³ 13.1 15.4 18.4

19.6 %

12.6 %

10.7 %

4

But Cost of Capital Still Elevated

Historical Beta Historical Cost of Equity

Source: Bloomberg, SNL Financial, CapIQ, Company filings. Note: Market data as of 20-Sep-2016. Peer composites based on average cost of equity across peers. ¹ Protection Peers include Primerica, Aflac, FBL Financial, Torchmark, CNO, Unum and Genworth (GNW excluded after 12/31/2007).² Capital Intensive Accumulations Peers Include Prudential, Lincoln, Metlife, VOYA and American Equity.³ Non-Capital Intensive Accumulation Peers include Principal and Ameriprise.4 Pre-Crisis goes from 01-01-2004 to 12-31-2007.5 Post-Crisis goes from 01-01-2010 to 20-09-2016.

7.0 %

9.0 %

11.0 %

13.0 %

15.0 %

17.0 %

19.0 %

21.0 %

23.0 %

25.0 %

2004 2006 2008 2010 2012 2014 2016

Impl

ied

Cos

t of E

quity

Protection Peers¹Capital Intensive Accumulation Peers²Non-Capital Intensive Accumulation Peers³

12.3 %

11.6 %

9.9 %

Average 04-Present Pre-Crisis4 Post-Crisis5

Protection Peers¹ 12.06 10.61 11.78Capital Intensive Accumulation Peers² 14.52 11.99 14.87Non-Capital Intensive Accumulation Peers³ 14.81 11.90 14.01

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2004 2006 2008 2010 2012 2014 2016

His

toric

al A

xiom

a B

eta

Protection Peers¹Capital Intensive Accumulation Peers²Non-Capital Intensive Accumulation Peers³

Average 04-Present Pre-Crisis4 Post-Crisis5

Protection Peers¹ 1.24 0.80 1.42Capital Intensive Accumulation Peers² 1.52 0.99 1.76Non-Capital Intensive Accumulation Peers³ 1.47 0.98 1.63

1.48 1.40 1.27

5

How are Life Insurers Responding to Industry Challenges?

De-risking of Products and Reduction in Product Guarantees

Utilizing M&A to Optimize Business Portfolio, Add Scale and Enhance Capabilities

Re-Structuring and/or Breaking-Up of Complex and Multi-Line Companies

Searching for Enhanced Investment Yield

Investments in Technology and VC

Utilizing Capital Return to Enhance Returns to Shareholders

Sale of Certain Companies to Buyers With Lower Return Threshold

Increasing Cost Reduction Efforts

A

B

C

D

E

F

G

H

6

38 44 5886 79 863

3

4 39

38 4761

90 8295

2010 2011 2012 2013 2014 2015All Other Industries Financial Institutions

2012 2015

Activist AUM ($bn)2 $114 $181

Alumni Funds’ AUM ($bn)3 $4 $13

Total Public Campaigns>$500mm

50 78

Mega CapCampaigns >$20bn 3 14

Days Before Settlement forBoard Seats4

101 60

Key Trends in Activism Size and Scope of Activism

Shareholder Activism Continues to Become More “Mainstream”

Source: FactSet, Thomson, Public sources as of 31-Dec-2015Note: Campaigns data are annualized and consist of U.S. public campaigns by funds belonging to the FactSet “SharkWatch50” universe.1 Includes SharkWatch 50 campaigns announced from 2012 – 2015; equity market capitalization >$500mm; including private and public settlements for board seats.2 Aggregate equity portfolio of activists included in FactSet “SharkWatch50” as of 31-Dec-2015 13F filings.3 Represents equity portfolio of alumni funds including Corvex, Marcato, Engaged, Sachem Head and Sarissa, as of 31-Dec-2015 13F filings.4 Includes activist campaigns at companies with equity market capitalization >$500mm; involving activists on FactSet’s “SharkWatch50” list. Represents average time elapsed between initial public agitation and

the date at which board seats were granted ; excluding activism directed at funds.5 Data includes public activism situations initiated by a SharkWatch50 activist at companies >$500 million market capitalization.

Increased Pressure: Market volatility and rise of index funds have put pressure on active managers to support activists

Active Engagement: Institutional investors becoming more active with portfolio companies

Growing Communication: Increased dialogue among investors is changing investor relations

Increased Target Size: Large cap focus necessitated by surge in assets under management

Pressure on Boards: Heightened scrutiny of board composition and tenure

Faster Settlements: Companies are settling quicker and more often to avoid proxy fights; approximately 48% of activist campaigns from 2012 – 2015 sought board seats, 80% of which gained at least 1 seat1

1

2

3

4

5

6

New Activism Campaigns5 Shareholder Activism in the Insurance Industry is Becoming More Frequent

7

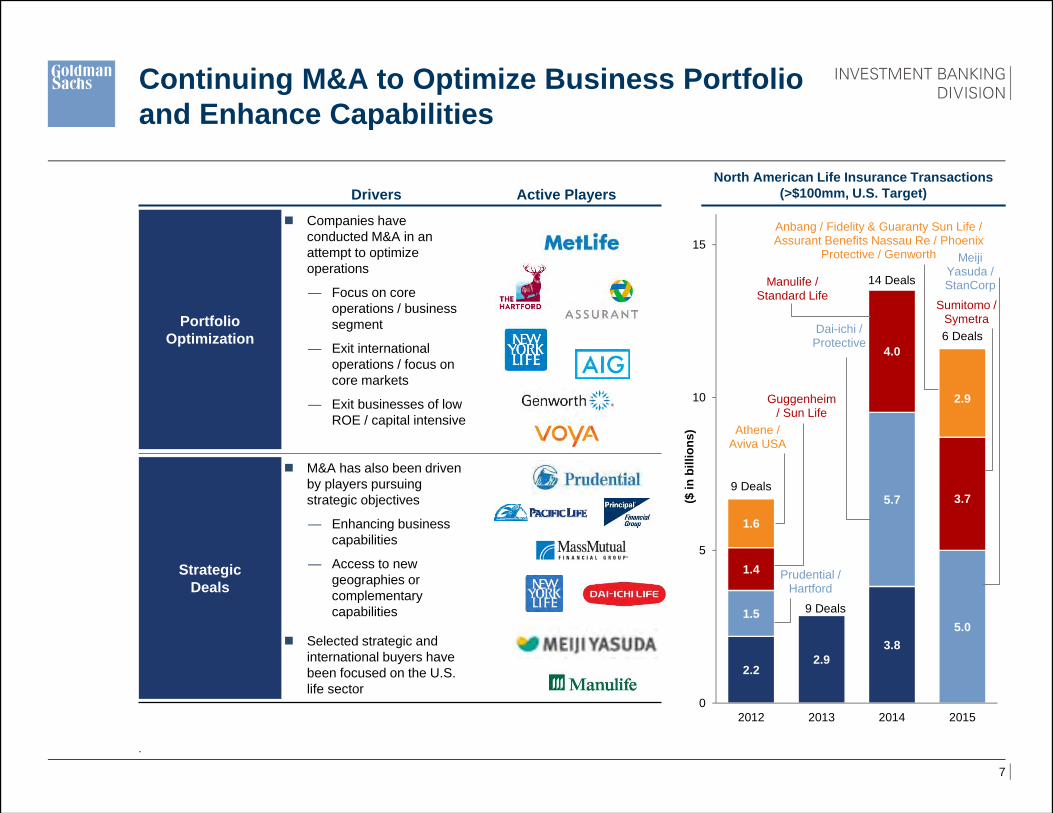

Continuing M&A to Optimize Business Portfolio and Enhance Capabilities

Drivers Active Players

PortfolioOptimization

Companies have conducted M&A in an attempt to optimize operations

— Focus on core operations / business segment

— Exit international operations / focus on core markets

— Exit businesses of low ROE / capital intensive

StrategicDeals

M&A has also been driven by players pursuing strategic objectives

— Enhancing business capabilities

— Access to new geographies or complementary capabilities

Selected strategic and international buyers have been focused on the U.S. life sector

North American Life Insurance Transactions (>$100mm, U.S. Target)

.

2.22.9

3.8

1.5

5.7

5.0

1.4

4.0

3.7

1.6

2.9

9 Deals

9 Deals

14 Deals

6 Deals

0

5

10

15

2012 2013 2014 2015

($ in

bill

ions

)

AXA

/AXA

Fin

Prudential / Hartford

Athene / Aviva USA

Guggenheim / Sun Life

Dai-ichi / Protective

Manulife / Standard Life

Anbang / Fidelity & Guaranty Sun Life / Assurant Benefits Nassau Re / Phoenix

Protective / Genworth

Sumitomo / Symetra

Meiji Yasuda / StanCorp

8

Emergence of New Entrants Driving Competition

Active Investors Financial / Run-off Investors

General Public Release

Reinsurance in M&A

General Public Release

Society of Actuaries Annual Meeting 26 October 2016

General Public Release

Socie ty of Actuaries Annual Meeting | 2 6 October 2 0 1 6

• The possible role of Reinsurance in an M&A transaction

• Reinsurance capital management example

• Reinsurance financing s tructure – what works & not

Reinsurance in M&A

2

General Public Release

Socie ty of Actuaries Annual Meeting | 2 6 October 2 0 1 6 3

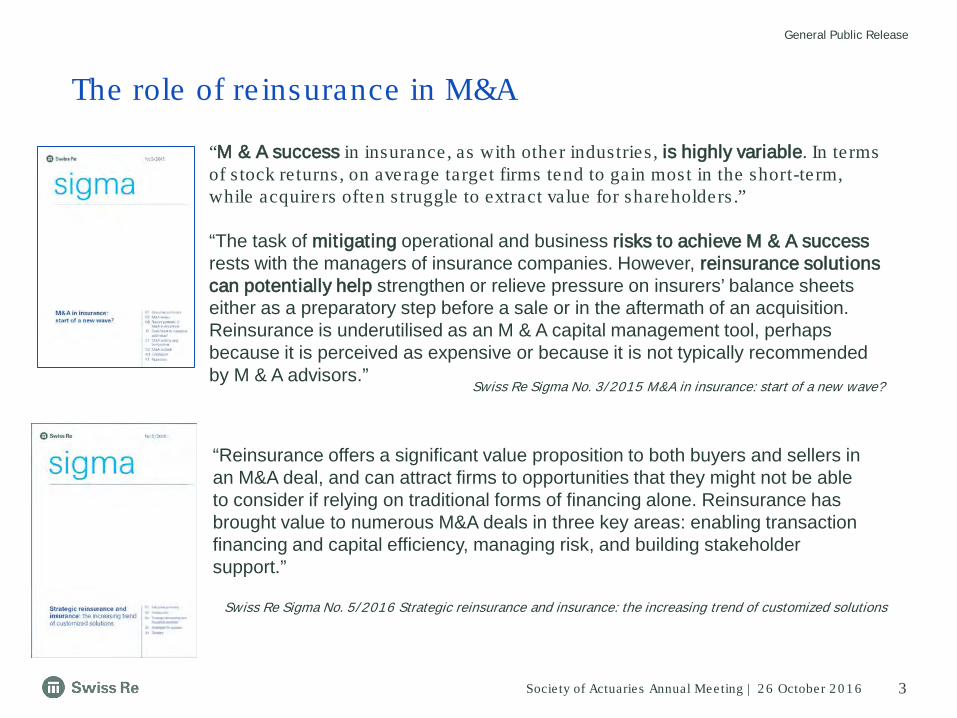

The role of re insurance in M&A

“M & A success in insurance, as with other industries , is highly variable. In terms of s tock returns, on average target firms tend to gain most in the short-term, while acquirers often s truggle to extract value for shareholders .”

“The task of mitigating operational and business risks to achieve M & A success rests with the managers of insurance companies. However, reinsurance solutions can potentially help strengthen or relieve pressure on insurers’ balance sheets either as a preparatory step before a sale or in the aftermath of an acquisition. Reinsurance is underutilised as an M & A capital management tool, perhaps because it is perceived as expensive or because it is not typically recommended by M & A advisors.”

“Reinsurance offers a significant value proposition to both buyers and sellers in an M&A deal, and can attract firms to opportunities that they might not be able to consider if relying on traditional forms of financing alone. Reinsurance has brought value to numerous M&A deals in three key areas: enabling transaction financing and capital efficiency, managing risk, and building stakeholder support.”

Swiss Re Sigma No. 3/ 2015 M&A in insurance: start of a new wave?

Swiss Re Sigma No. 5/ 2016 Strategic reinsurance and insurance: the increasing trend of customized solutions

General Public Release

Socie ty of Actuaries Annual Meeting | 2 6 October 2 0 1 6 4

Reinsurance can be applied to achieve the key goals of both parties in a transaction

Reinsurance Value PropositionReinsurance solves hurdles to deal execution

Build Stakeholder

Support

SecureTransaction Financing

Optimize Post-Deal Risk

Deliver Post-Deal Performance Targets

Unlock Trapped Capital Before Execution

Avoid Post-Transaction

al Issues

Improve Transaction

Certainty

Realize Full Deal Value

Buyers

Sellers

1. Capital: Enabling transaction financing and capital efficiency

2. Risk: Managing acquired and ongoing risk/ volatility

3. Stakeholder support: Building s takeholder support by addressing different needs

General Public Release

Socie ty of Actuaries Annual Meeting | 2 6 October 2 0 1 6 5

Reinsurance as Capital ManagementLeverage Effect

Companies maintain a Solvency ratio >100% to have a buffer against adverse developments and capital market volatility

A reduction in SCR increases the Solvency ratio in a more effective and sustainable way than an increase in own funds– Capital relief of USD 33m has the same impact as increasing own funds by USD 50m– In adverse claims developments, reinsurance protects own funds and provides capital relief

Increase in own funds

Current Solvencyratio: 100 %

OwnFunds

SCR

USD +50m

Target Solvency ratio: 150 %

USD -33m

Target Solvency ratio: 150 %

OwnFunds

SCR

100150

OwnFunds

SCR

Re-insurance

100100 100 67

General Public Release

Socie ty of Actuaries Annual Meeting | 2 6 October 2 0 1 6 6

Successful and Un-successful M&A transactionsVIF Financing success & what doesn’t work

M&A Buy-side EvaluationSu Meng Lee, FSA, MAAA, CERAOctober 26, 2016

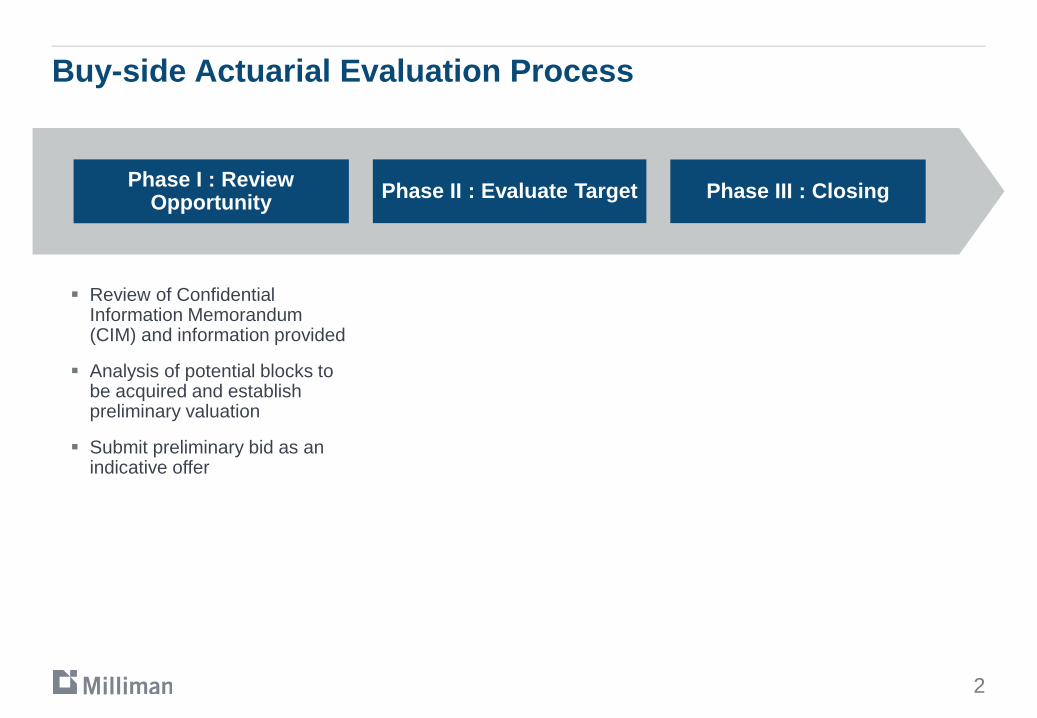

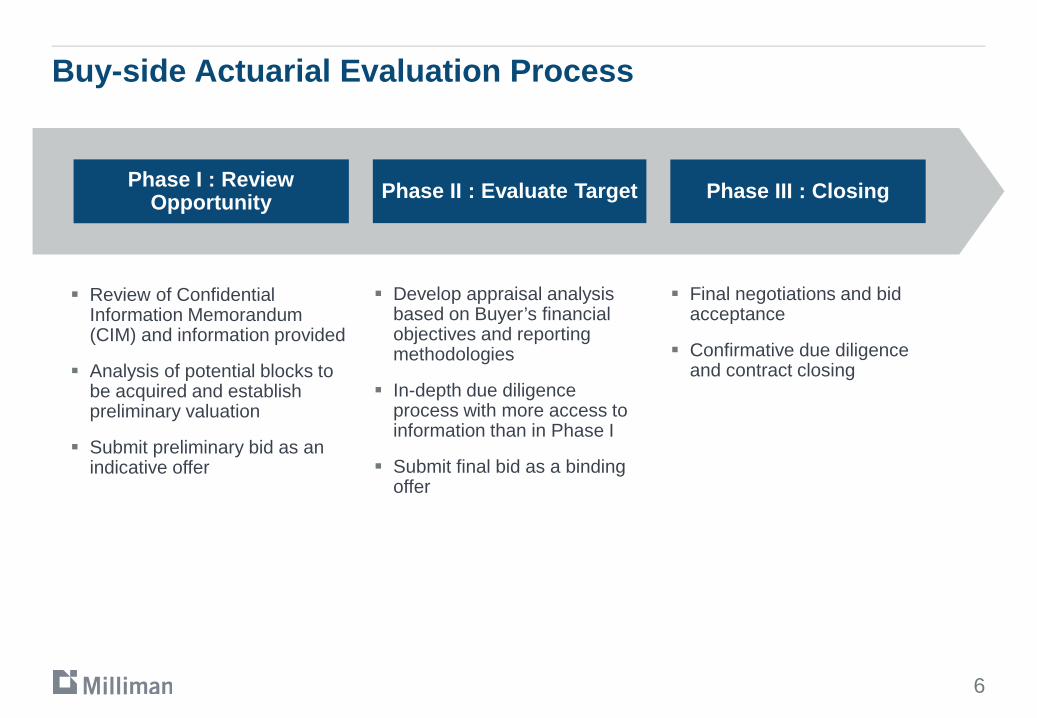

Buy-side Actuarial Evaluation Process

Phase I : Review Opportunity

Review of Confidential Information Memorandum (CIM) and information provided

Analysis of potential blocks to be acquired and establish preliminary valuation

Submit preliminary bid as an indicative offer

Phase II : Evaluate Target Phase III : Closing

2

Phase I : Analysis of Life & Annuity Products

3

Products Buyer Interest Mortality Exposure

GA Investment Risk Comments

Life

Traditional • Relatively less issues compared to the

other products

Term • XXX Regulations - financing difficulties

UL/EIUL

• Products with secondary guarantee carry tail risk

• AXXX Regulations - financing difficulties

LTC

• Lack credible experience – tail exposure

• Insurers increasing rates• Other risks : Morbidity & lapses

Annu

ities

DA/FIA • ALM risk

Structured Settlements

• ALM risk• Mortality – substandard risk

VA

• Regulation changes – uncertainties• Volatile reserves and capital balance• Other risks : Lapses & policy holder

behavior

HighestHighMediumLow

Buy-side Actuarial Evaluation Process

Phase I : Review Opportunity

Review of Confidential Information Memorandum (CIM) and information provided

Analysis of potential blocks to be acquired and establish preliminary valuation

Submit preliminary bid as an indicative offer

Phase II : Evaluate Target

Develop appraisal analysis based on Buyer’s financial objectives and reporting methodologies

In-depth due diligence process with more access to information than in Phase I

Submit final bid as a binding offer

Phase III : Closing

4

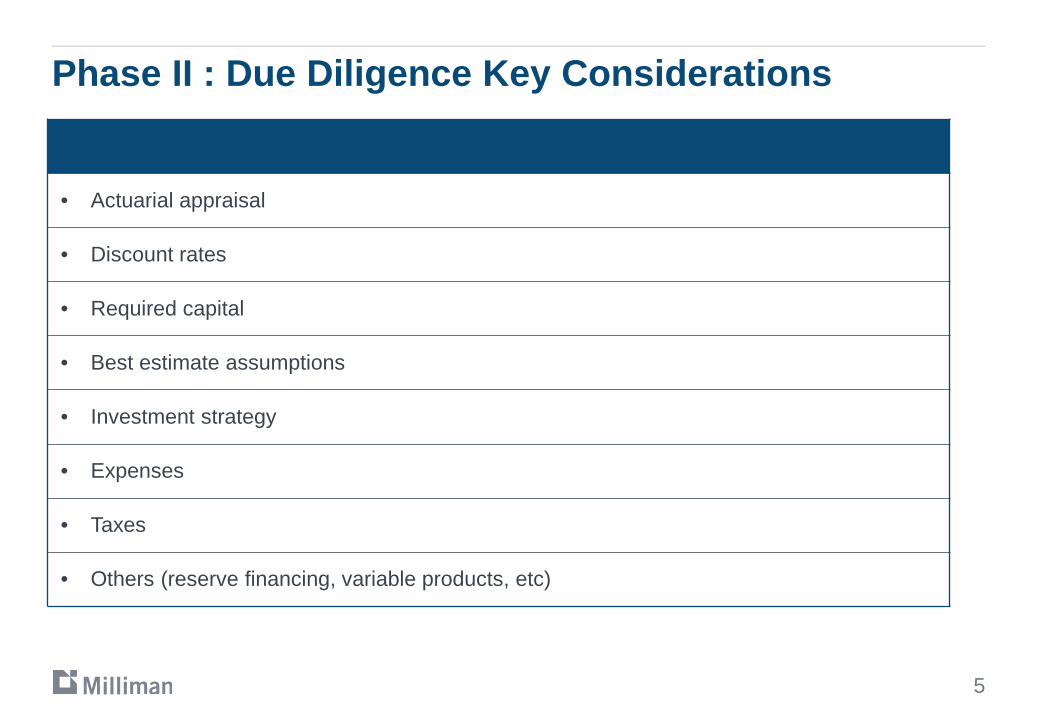

Phase II : Due Diligence Key Considerations

• Actuarial appraisal

• Discount rates

• Required capital

• Best estimate assumptions

• Investment strategy

• Expenses

• Taxes

• Others (reserve financing, variable products, etc)

5

Buy-side Actuarial Evaluation Process

Phase I : Review Opportunity

Review of Confidential Information Memorandum (CIM) and information provided

Analysis of potential blocks to be acquired and establish preliminary valuation

Submit preliminary bid as an indicative offer

Phase II : Evaluate Target

Develop appraisal analysis based on Buyer’s financial objectives and reporting methodologies

In-depth due diligence process with more access to information than in Phase I

Submit final bid as a binding offer

Phase III : Closing

Final negotiations and bid acceptance

Confirmative due diligence and contract closing

6

Phase III : Common Reasons Deals Do Not Close

7

Regulatory uncertainties

Deal Fall Through

External market forces

Incompatible structure

Unable to mutually agree on valuation