libor - sizing the potential damage - bluematrix

TRANSCRIPT

European Banks 16 July 2012

LIBOR - Sizing the potential damage

The potential financial and reputational damage caused by Barclays' falseLIBOR submissions has rightly raised company and sector concerns.Unequivocally, the LIBOR probes are a negative development and could havewide-ranging consequences. The direct financial penalties (£290m for Barclays)are unhelpful, but likely to be very manageable. The far larger issue is thepotential for (1) substantial civil damages, and/or (2) implications for seniormanagement if found to be complicit. While we claim no legal expertise andacknowledge that estimates are necessarily speculative, we attempt to sizepotential industry damages. We arrive at U$35bn. Most impacted would beBarclays/RBS/Deutsche, where our estimated damages amount to£3.1bn/£3.0bn/€3.4bn, accounting for 46%/18%/34% of 2012-14E Basel 3 capitalbuild, respectively. We take some comfort from (1) prior securities settlements,and (2) a likely elongated legal process, and our base case is that this situationdoes not bring with it external capital risk.

Civil actions could be material... Direct damages (ie, fines) are likely to be verymanageable, and we see greater financial risk from potential civil actions. We size thepotential issue for the industry, but with inherent difficulty in estimation, we caveatthat the list of assumptions in our methodology is long, the numbers large and thesensitivities high.

...we estimate U$35bn of industry settlements. We estimate U$35bn for theindustry, 0.1-1.2% of 2012E B2 RWAs across the European panel banks. We use thenotional size of the (large) interest rate derivatives market as our base, adjusted foraffected currencies and intra-dealer exposures. We then estimate the period affected,level of LIBOR suppression and the size of any settlement as a % of overall possibledamages. We provide a sensitivity.

Burden of proof will be high. We find little correlation between the average CDS ofthe panel banks and LIBOR-OIS, simplistically leaving some element of suppressionfrom the panel banks as possible. However, correlations alone are not incontrovertibleand we believe the burden of proof will be high.

Recommendations intact. Large, class action lawsuits take a lot of time to complete,with 5-8 years between filing and settlement not uncommon, in turn allowing even themost impacted banks to increase capital ratios ahead of any potential settlement. Weremain buyers of Barclays (tgt, 280p), RBS (tgt 330p), Credit Suisse (tgt CHF 27.2),UBS (CHF 16.8) and HSBC (tgt 640p).

Industry Update

Mark Phin, CFAAnalyst+44 20 7663 [email protected]

Andrew StimpsonAnalyst+44 20 7663 [email protected]

Vasco MorenoAnalyst+44 20 7663 [email protected]

Luke BirtwistleAssociate+44 207 663 [email protected]

Please refer to important disclosures and analyst certification information on pages 22 - 25.

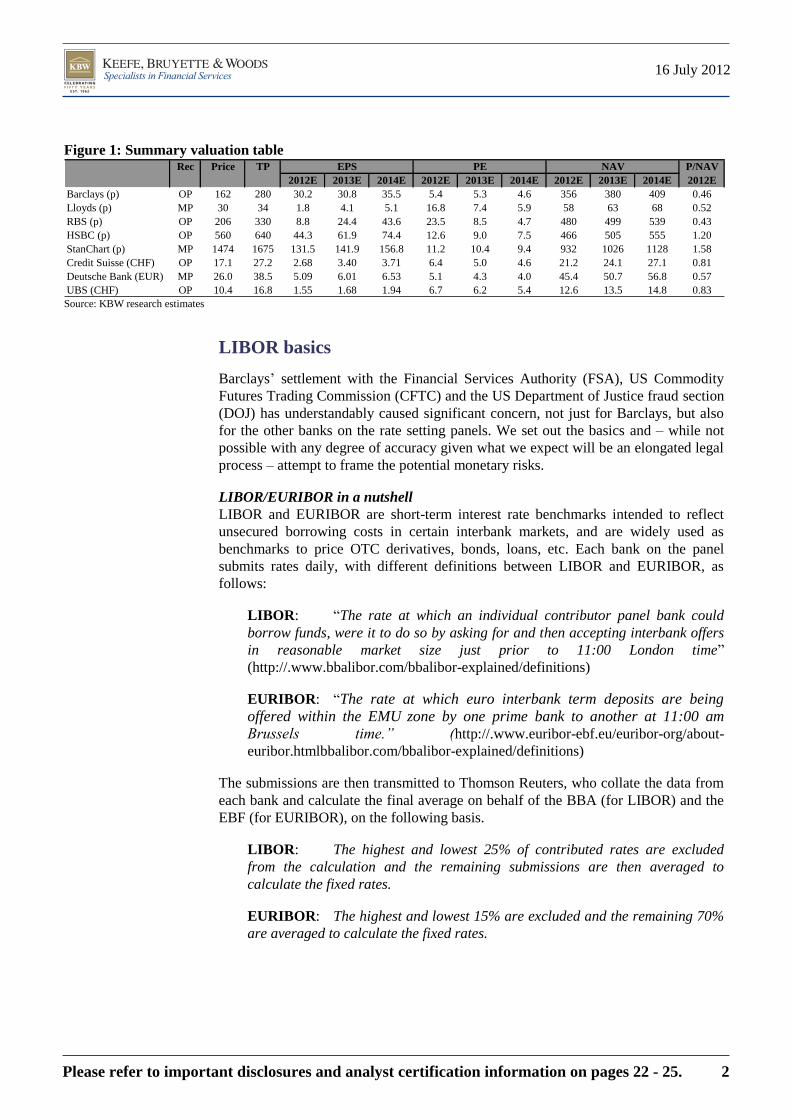

Figure 1: Summary valuation table Rec Price TP P/NAV

2012E 2013E 2014E 2012E 2013E 2014E 2012E 2013E 2014E 2012E

Barclays (p) OP 162 280 30.2 30.8 35.5 5.4 5.3 4.6 356 380 409 0.46

Lloyds (p) MP 30 34 1.8 4.1 5.1 16.8 7.4 5.9 58 63 68 0.52

RBS (p) OP 206 330 8.8 24.4 43.6 23.5 8.5 4.7 480 499 539 0.43

HSBC (p) OP 560 640 44.3 61.9 74.4 12.6 9.0 7.5 466 505 555 1.20

StanChart (p) MP 1474 1675 131.5 141.9 156.8 11.2 10.4 9.4 932 1026 1128 1.58

Credit Suisse (CHF) OP 17.1 27.2 2.68 3.40 3.71 6.4 5.0 4.6 21.2 24.1 27.1 0.81

Deutsche Bank (EUR) MP 26.0 38.5 5.09 6.01 6.53 5.1 4.3 4.0 45.4 50.7 56.8 0.57

UBS (CHF) OP 10.4 16.8 1.55 1.68 1.94 6.7 6.2 5.4 12.6 13.5 14.8 0.83

EPS PE NAV

Source: KBW research estimates

LIBOR basics

Barclays‘ settlement with the Financial Services Authority (FSA), US Commodity

Futures Trading Commission (CFTC) and the US Department of Justice fraud section

(DOJ) has understandably caused significant concern, not just for Barclays, but also

for the other banks on the rate setting panels. We set out the basics and – while not

possible with any degree of accuracy given what we expect will be an elongated legal

process – attempt to frame the potential monetary risks.

LIBOR/EURIBOR in a nutshell

LIBOR and EURIBOR are short-term interest rate benchmarks intended to reflect

unsecured borrowing costs in certain interbank markets, and are widely used as

benchmarks to price OTC derivatives, bonds, loans, etc. Each bank on the panel

submits rates daily, with different definitions between LIBOR and EURIBOR, as

follows:

LIBOR: ―The rate at which an individual contributor panel bank could

borrow funds, were it to do so by asking for and then accepting interbank offers

in reasonable market size just prior to 11:00 London time‖

(http://.www.bbalibor.com/bbalibor-explained/definitions)

EURIBOR: ―The rate at which euro interbank term deposits are being offered within the EMU zone by one prime bank to another at 11:00 am Brussels time.” (http://.www.euribor-ebf.eu/euribor-org/about-

euribor.htmlbbalibor.com/bbalibor-explained/definitions)

The submissions are then transmitted to Thomson Reuters, who collate the data from

each bank and calculate the final average on behalf of the BBA (for LIBOR) and the

EBF (for EURIBOR), on the following basis.

LIBOR: The highest and lowest 25% of contributed rates are excluded

from the calculation and the remaining submissions are then averaged to

calculate the fixed rates.

EURIBOR: The highest and lowest 15% are excluded and the remaining 70%

are averaged to calculate the fixed rates.

Please refer to important disclosures and analyst certification information on pages 22 - 25. 2

16 July 2012

Figure 2: BBA LIBOR panel banks, 2007

USD GBP EUR

Bank of America Abbey National plc Bank of America

Bank of Tokyo – Mitsubishi UFJ Bank of America Barclays Bank plc

Barclays Bank plc Bank of Tokyo – Mitsubishi UFJ Bank of Tokyo – Mitsubishi UFJ

Citibank NA BNP Paribas Citibank NA

Credit Suisse Barclays Bank plc Credit Suisse

Deutsche Bank AG Citibank NA Deutsche Bank AG

HBOS Deutsche Bank AG HBOS

HSBC HBOS HSBC

JP Morgan Chase HSBC JP Morgan Chase

Lloyds TSB Bank plc JP Morgan Chase Lloyds TSB Bank plc

Rabobank Lloyds TSB Bank plc Rabobank

Royal Bank of Canada Rabobank Royal Bank of Canada

The Norinchukin Bank Royal Bank of Canada Société Générale

The Royal Bank of Scotland Group The Royal Bank of Scotland Group The Royal Bank of Scotland Group

UBS AG UBS AG UBS AG

West LB AG West LB AG West LB AG

JPY CHF

Bank of America Barclays Bank plc

Bank of Tokyo – Mitsubishi UFJ Bank of Tokyo – Mitsubishi UFJ

Barclays Bank plc Citibank NA

Citibank NA Credit Suisse

Deutsche Bank AG Deutsche Bank AG

HSBC HSBC

JP Morgan Chase JP Morgan Chase

Lloyds TSB Bank plc Lloyds TSB Bank plc

Mizuho Corporate Bank Société Générale

Rabobank The Royal Bank of Scotland Group

Société Générale UBS AG

Sumitomo Mitsui Banking Corporation Europe Ltd (SMBCE)West LB AG

The Norinchukin Bank

The Royal Bank of Scotland Group

UBS AG

West LB AG Source: BBA, KBW Research. NB. KBW European coverage emboldened by KBW Research

Barclays LIBOR-related settlement

Simply put, at various times, Barclays input false LIBOR/EURIBOR submissions.

There are, however, two very separate reasons leading to separate implications:

1. Trading positions of its derivative traders: Employees responsible for

LIBOR/EURIBOR submissions accommodated trader requests (in at least

London, New York and Tokyo) on the level of those submissions. On

occasion, that affected the overall LIBOR average. There was also co-

ordination with traders at other financial institutions, including other panel

members. There was a clear profit motive. Additionally, the FSA identifies

systems and control failings at Barclays, as well as compliance failings (as

LIBOR-related issues were escalated to the IB compliance function on three

occasions in 2007/8). It is very clear from the documentation that Barclays

was not alone here, and we would fully expect other banks and individuals

to be implicated. At this stage, though, we do not know exactly which ones.

Barclays traders not

alone in

manipulating LIBOR

Please refer to important disclosures and analyst certification information on pages 22 - 25. 3

16 July 2012

2. Concerns about negative media attention: In 2008, Barclays‘ relatively

high USD LIBOR submissions were cited by the press as, perhaps, reflective

of liquidity issues. As a result, Barclays‘ senior management (now known to

be Jerry del Missier, COO) directed that those submissions should be

lowered, resulting in input rates that did not reflect the cost of obtaining

interbank funding. There is no evidence that the intention of Barclays‘

management was to affect official published LIBOR rates. We think this is

potentially a far bigger issue for the industry given the magnitude of the

possible suppression and subsequent damages.

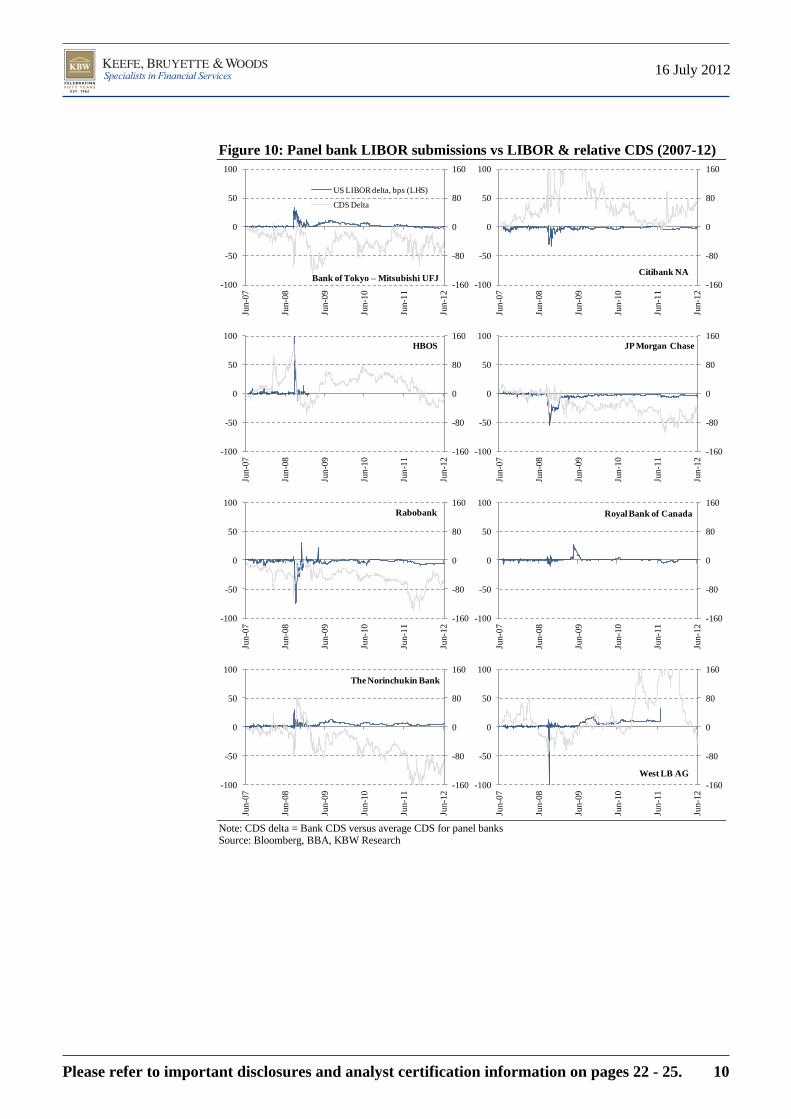

Being outside the banks means that judging this will always be a tricky exercise.

However, we believe it is sensible to assume that there should be a correlation

between the LIBOR-OIS spread and the average CDS spread of the LIBOR panel

banks. While some periods do show an element of correlation (2H11, 2Q10, 1Q09),

the majority does not tally: we note that LIBOR-OIS came down materially in 2H08

even as CDS continued rising until March 2009.

Figure 3: Panel-bank CDS correlates poorly with LIBOR-OIS

0.0

1.0

2.0

3.0

4.0

5.0

6.0

06

/07

08

/07

10

/07

12

/07

02

/08

04

/08

06

/08

08

/08

10

/08

12

/08

02

/09

04

/09

06

/09

08

/09

10

/09

12

/09

02

/10

04

/10

06

/10

08

/10

10

/10

12

/10

02

/11

04

/11

06

/11

08

/11

10

/11

12

/11

02

/12

04

/12

06

/12

%

U$ 3 Mth LIBOR LIBOR/OIS spread Average CDS of U$ LIBOR panel

Source: Bloomberg, BBA, KBW Research

Three potential impacts

Direct financial penalties: The combined financial penalties imposed on

Barclays were £290m, following settlement with the DoJ (U$160m), US

CFTC (U$200m) and FSA £59.5m (after a 30% discount for early

settlement). While unhelpful, with a c£100m provision taken in 1Q12, the

charge represents a modest c5bps of 1Q12 RWAs. In addition, Barclays was

granted conditional leniency from the DoJ in connection with antitrust

violations with respect to financial instruments that reference EURIBOR.

Management implications: The fallout from the LIBOR case has already

resulted in (1) the resignation of Marcus Agius (Chairman) on 2nd

July, (2)

the resignation of Bob Diamond (CEO) on 3rd

July (with Marcus Agius

named as interim full-time Chairman to lead the search for a new CEO), and

(3) Jerry del Missier (COO) on 3rd

July (following disclosure that he passed

direction to the LIBOR submitters to lower inputs). To date, none of the

Bigger issue: were all

banks suppressing the

LIBOR average?

Please refer to important disclosures and analyst certification information on pages 22 - 25. 4

16 July 2012

divisional managers have been affected, nor implicated, but it is impossible to

dismiss further fallout. The position of other banks and respective

management teams will only become clear in time, although we note press

reports of several trader suspensions at multiple banks (e.g. Reuters 9 Feb

2012).

Civil actions: As the results of the investigations are placed into the public

domain, we would expect claims to grow (class action litigation has been

forming for some time, with one US judge having already consolidated

cases). We explore the costs of potential civil action cases in the next section,

which we believe could be meaningful.

Civil damages could reach ~U$35bn

We make an initial industry estimate of potential damages from the LIBOR case of

cU$35bn, with Barclays, RBS and Deutsche most affected in absolute terms within

our European coverage universe. We set out our methodology below, which we apply

equally across all affected banks on the US$ LIBOR panel. We expect the details on

which banks are likely to be more affected by such litigation to become clear over the

next few months and years, rather than weeks. Given the difficulties in calculating

litigation losses, we acknowledge that our estimates are speculative and include a

sensitivity table.

Figure 4: KBWe LIBOR litigation loss estimation U$tr Industry Barclays RBS HSBC Lloyds DBK CS UBS*

Notional rate derivatives (2010), all currencies 465.3 64.9 61.8 18.1 3.5 58.8 41.2 35.2

% U$ and € combined 70% 70% 70% 70% 70% 70% 70% 70%

Notional rate derivatives (2010), U$ and € (estimate) 327.7 45.7 43.5 12.8 2.5 41.4 29.0 24.8

% customer business 71% 71% 71% 71% 71% 71% 71% 71%

Notional customer derivatives (estimate) 232.7 32.5 30.9 9.1 1.8 29.4 20.6 17.6

Number of years 4

% of time LIBOR suppressed 25%

LIBOR supression 0.20%

Settlement % of 'damages' 10%

Potential settlement (U$bn) taxed (@25%) 34.9 4.9 4.6 1.4 0.3 4.4 3.1 2.6

Potential settlement (Local currency) taxed 3.1 3.0 1.4 0.2 3.4 2.9 2.5

% of 2012 B2 RWA (%) 0.8% 0.7% 0.1% 0.1% 1.2% 1.3% 1.3%

% of 2012 B3 RWA (%) 0.7% 0.5% 0.1% 0.0% 0.7% 1.0% 0.8%

Current 2012-14E B3 capital build 1.5% 3.0% 1.8% 3.0% 2.1% 3.9% 4.8%

Settlement estimate % capital build 46% 18% 6% 2% 34% 26% 16% Note: *Damages may be reduced by 2/3 for UBS to allow for DOJ leniency agreement benefit. We use a standard 25% tax rate across all banks. Source: Bank of International Settlements, Company reports, KBW Research estimates

Our estimates by bank are dictated by outstanding notional interest rate derivatives at

end-2010, and we make no attempt to differentiate or apportion ‗blame‘. We see

Barclays (£3.1bn net), RBS (£3.0bn net) and Deutsche (€3.4bn net) as potentially

most impacted in absolute terms, with Lloyds (£0.2bn) and HSBC (U$1.4bn) least.

Damages of this magnitude would clearly be unhelpful as banks look to increase

capital levels in advance of Basel 3 implementation, but crucially, our estimates of

potential damages are equivalent to 2-46% of our 2012-14E Basel 3 capital build

estimates, rather than moving capital ratios down from those at end-2012. As noted

below, we also think that any settlement could well occur beyond our forecast period,

in turn allowing a further period to build capital.

Please refer to important disclosures and analyst certification information on pages 22 - 25. 5

16 July 2012

Figure 5: Sensitivity of industry losses to changes in: Increase of: ∆ losses (U$bn)

Affected assets +/-$100bn 15.0

% time LIBOR suppressed +/-5% 7.0

LIBOR suppression size +/-0.10% 17.5

Settlement % damages +/-1% 3.5 Source: Bloomberg, BBA, KBW Research

Estimating the damages and settlements

Given the difficulties in estimating potential legal costs, we acknowledge that our

estimates are subjective, and almost all our assumptions used here could be open to

debate. However, we explain our thinking and methodology in estimating damages

and likely settlement amounts below:

Size of affected securities

In judging the size of the potential affected securities, we establish our start point as

the notional amount of interest rate derivatives: we believe this forms a reasonable

proxy for the size of the potential Libor-related market. This market has grown from

U$42bn in 1998 to U$504bn at end-2011, according to BIS data, with ~70% in US$

and EUR.

Figure 6: Interest rate derivatives outstanding (notional), 1H98-2H11

0

100

200

300

400

500

600

1H

98

2H

98

1H

99

2H

99

1H

00

2H

00

1H

01

2H

01

1H

02

2H

02

1H

03

2H

03

1H

04

2H

04

1H

05

2H

05

1H

06

2H

06

1H

07

2H

07

1H

08

2H

08

1H

09

2H

09

1H

10

2H

10

1H

11

2H

11

U$

tril

lio

n

Canadian $ Euro Jap yen Sterling Swed krona Swiss franc US $ Other

Source: Bank of International Settlements, KBW Research

BIS data also helps us to eliminate the amount of notional derivatives that exist

between the ―reporting dealers‖, which by BIS definitions is essentially investment

banks and securities houses which we assume will not sue each other (i.e. zero sum

between dealers). On the 2010 BIS data, this is ~29% of the total volume. The

notional value of customer interest rate derivatives at risk of applying for damages is

therefore reduced to $233tr.

Please refer to important disclosures and analyst certification information on pages 22 - 25. 6

16 July 2012

Figure 7: Interest rate derivatives counterparty split U$bn Dec-09 Jun-10 Dec-10 Jun-11 Dec-11

Total contracts 449,875 451,831 465,260 553,240 504,098

o/w Reporting dealers 138,580 132,128 134,483 159,222 157,330

o/w Other financial institutions 275,688 282,031 293,490 354,281 309,362

o/w Non-financial customers 35,607 37,673 37,286 39,737 37,406

"Reporting dealers" 31% 29% 29% 29% 31%

Non "reporting dealers" 69% 71% 71% 71% 69% Source: Bank of International Settlements, KBW Research

Estimating the size of the damages sought

The Schwab case highlights a period of 4 years where LIBOR was potentially

suppressed from 2007-2011. However, we would also assume that LIBOR was not

suppressed at all times through that period. Also, even during the prolonged crisis

there were times when the market was working and things calmed slightly (e.g. in

mid-2009, European banks‘ equity rallied to 1.6x 12m forward NAV). We therefore

assume that LIBOR was suppressed for ~25% of those 4 years.

The size of the suppression itself is difficult to measure. Clearly the plaintiffs in the

Schwab case will argue it is high (they cite various sources showing estimates of 30-

40bp), while, should a case get to this stage, the banks will argue the suppression is

smaller. In our scenario we assume a 20bps average suppression, in turn bringing

potential ‗damages‘ down to U$349bn.

Estimating the size of potential settlements

While it is difficult to predict any settlement amount with any degree of accuracy, we

find a study of securities class action settlements by Cornerstone Research

informative. Based on a research sample of common stock fraud cases (ie, excluding

cases with alleged classes comprising only bondholders, preferred stockholders, etc),

they make a number of interesting observations, but most importantly that settlements

as a % of ‗estimated damages‘ ranges from 10% in small cases to 1% for large cases

and an average of 3%.

Figure 8: Securities settlement (2002-2011) and Median Settlement as % of ‘estimated damages’* by damage range (1996-2011)

0

2

4

6

8

10

12

14

16

18

20

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Sett

lem

en

t (U

$b

n)

Settlement (ex large cases) WorldCom Enron Tyco

0%

2%

4%

6%

8%

10%

12%

Med

ian

Sett

lem

nt

% o

f 'e

stim

ate

d

da

ma

ges'

1996-2010 2011

Source: Cornerstone Research 2011 Review and Analysis. Charts reproduced by KBW Research from http://www.cornerstone.com/files/Publications/a0e54ba8-2830-4c00-9481-108208ec4ed8/Presentation/PublicationAttachment/f03e4174-ec8a-4eb3-ba22-19bd5162f09e/Cornerstone_Research_Settlements_2011_Analysis.pdf *Cornerstone Research uses as a simplified approach to calculate ‗estimated damages‘ and do not intend for any damages estimate to be indicative of actual economic damages borne by shareholders.

Settlement % typically

a fraction of potential

damages

Please refer to important disclosures and analyst certification information on pages 22 - 25. 7

16 July 2012

Clearly, each case has to be taken in isolation, and the numbers related to LIBOR are

potentially larger than anything that we know of, but we observe the following with

regard to prior securities class actions:

The typical duration between filing date and settlement hearing date is around

3.5 years, but can be substantially longer.

Credit-crisis related cases have settled at a slower rate than traditional cases,

and while those have settled for higher U$ amounts (than non credit-crisis

related cases), they have settled at a lower % of ‗estimated damages‘ (c3% on

average 2009-11).

Settlements generally increase as estimated damages increase, but also

settlements as a percentage of ‗estimated damages‘ typically decrease as

damages increase.

The burden of proof

We expect the burden of proof on the part of plaintiffs to be high, something which is

very apparent even in the Schwab case. We expect some of the challenges to be:

Establishing whether LIBOR was incorrectly stated in the first place.

With some firms acting as whistleblower and co-operating fully with

investigations, along with the Barclays fines and evidence, we think the trader

element should be straightforward to prove for at least some of the defendant

banks where trader emails and instructions/requests exist. However, this is a

small part of the case, and we think LIBOR will only have been marginally

impacted and not in the same direction.

The more difficult part of the case will be to prove that LIBOR rates were

suppressed for an extended period, which we expect to be the substantive part

of the potential damages claim.

If LIBOR is proven to have been incorrectly stated, the plaintiffs will need to

prove that a loss has actually taken place. Nearly all counterparties will have

some element of borrowing costs themselves, so saying that they lose out on

purchasing a LIBOR-based instrument ignores the economic profit from

being able to refinance oneself with cheaper funds as well.

Please refer to important disclosures and analyst certification information on pages 22 - 25. 8

16 July 2012

Appendix 1

Figure 9: Panel bank LIBOR submissions vs LIBOR & relative CDS (2007-12)

-160

-80

0

80

160

-100

-50

0

50

100

Jun-0

7

Jun

-08

Jun-0

9

Jun-1

0

Jun

-11

Jun-1

2

HSBC

US LIBOR delta, bps (LHS)

CDS Delta

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun-1

2

Barclays

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

Lloyds

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

RBS

-160

-80

0

80

160

-100

-50

0

50

100

Jun-0

7

Jun

-08

Jun-0

9

Jun-1

0

Jun

-11

Jun-1

2

UBS

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun-1

2

Credit Suisse

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

Deutsche Bank

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

Bank of America

Note: CDS delta = Bank CDS versus average CDS for panel banks Source: Bloomberg, BBA, KBW Research

Please refer to important disclosures and analyst certification information on pages 22 - 25. 9

16 July 2012

Figure 10: Panel bank LIBOR submissions vs LIBOR & relative CDS (2007-12)

-160

-80

0

80

160

-100

-50

0

50

100

Jun-0

7

Jun-0

8

Jun-0

9

Jun

-10

Jun

-11

Jun

-12

Bank of Tokyo – Mitsubishi UFJ

US LIBOR delta, bps (LHS)

CDS Delta

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun-0

9

Jun-1

0

Jun

-11

Jun

-12

Citibank NA

-160

-80

0

80

160

-100

-50

0

50

100

Jun-0

7

Jun-0

8

Jun-0

9

Jun

-10

Jun

-11

Jun

-12

HBOS

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun-0

9

Jun-1

0

Jun

-11

Jun

-12

JP Morgan Chase

-160

-80

0

80

160

-100

-50

0

50

100

Jun-0

7

Jun-0

8

Jun-0

9

Jun

-10

Jun

-11

Jun

-12

Rabobank

-160

-80

0

80

160

-100

-50

0

50

100Ju

n-0

7

Jun

-08

Jun-0

9

Jun-1

0

Jun

-11

Jun

-12

Royal Bank of Canada

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

The Norinchukin Bank

-160

-80

0

80

160

-100

-50

0

50

100

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

West LB AG

Note: CDS delta = Bank CDS versus average CDS for panel banks Source: Bloomberg, BBA, KBW Research

Please refer to important disclosures and analyst certification information on pages 22 - 25. 10

16 July 2012

Appendix 2: Report & Accounts extracts (2011)

Barclays

The FSA, the US Commodity Futures Trading Commission, the SEC, the US

Department of Justice Fraud Section of the Criminal Division and Antitrust Division

and the European Commission are amongst various authorities conducting

investigations into submissions made by Barclays and other panel members to the

bodies that set various interbank offered rates. Barclays is co-operating in the relevant

investigations and is keeping regulators informed. In addition, Barclays has been

named as a defendant in a number of class action lawsuits filed in US federal courts

involving claims by purported classes of purchasers and sellers of LIBOR-based

derivative products or Eurodollar futures or options contracts between 2006 and 2009.

The complaints are substantially similar and allege, amongst other things, that

Barclays and other banks individually and collectively violated US antitrust and

commodities laws and state common law by suppressing LIBOR rates during the

relevant period. Barclays has been informed by certain of the authorities investigating

these matters that proceedings against Barclays may be recommended with respect to

some aspects of the matters under investigation, and Barclays is engaged in

discussions with those authorities about potential resolution of those aspects. It is not

currently possible to predict the ultimate resolution of the issues covered by the

various investigations and lawsuits, including the timing and the scale of the potential

impact on the Group of any resolution.

Lloyds

Several government agencies in the UK, US and overseas, including the US

Commodity Futures Trading Commission, the US SEC, the US Department of Justice

and the FSA as well as the European Commission, are conducting investigations into

submissions made by panel members to the bodies that set various interbank offered

rates. The Group, and/or its subsidiaries, were (at the relevant time) and remain

members of various panels that submit data to these bodies. The Group has received

requests from some government agencies for information and is co-operating with

their investigations. In addition, recently the Group has been named in private

lawsuits, including purported class action suits in the US with regard to the setting of

London interbank offered rates (LIBOR). It is currently not possible to predict the

scope and ultimate outcome of the various regulatory investigations or private

lawsuits, including the timing and scale of the potential impact of any investigations

and private lawsuits on the Group.

RBS

Certain members of the Group have been named as defendants in a number of class

actions and individual claims filed in the US with respect to the setting of LIBOR.

The complaints are substantially similar and allege that certain members of the Group

and other panel banks individually and collectively violated US commodities and

antitrust laws and state common law by manipulating LIBOR and prices of LIBOR

based derivatives in various markets through various means. The Group considers

that it has substantial and credible legal and factual defences to these and prospective

claims.

The Group continues to receive requests from various regulators investigating the

setting of LIBOR and other interest rates, including the US Commodity Futures

Please refer to important disclosures and analyst certification information on pages 22 - 25. 11

16 July 2012

Trading Commission, the US Department of Justice, the European Commission, the

FSA and the Japanese Financial Services Agency. The authorities are seeking

documents and communications related to the process and procedures for setting

LIBOR and other interest rates, together with related trading information. In addition

to co-operating with the investigations as described above, the Group is also keeping

relevant regulators informed. It is not possible to estimate with any certainty what

effect these investigations and any related developments may have on the Group.

HSBC

Various regulators and competition and enforcement authorities around the world

including in the UK, the US and the EU, are conducting investigations related to

certain past submissions made by panel banks in connection with the setting of

London interbank offered rates (‗LIBOR‘) and European interbank offered rates. As

certain HSBC entities are members of such panels, HSBC and/or its subsidiaries have

been the subject of regulatory demands for information and are cooperating with their

investigations. In addition, HSBC and other panel banks have been named in putative

class action lawsuits filed by private parties in the US with respect to the setting of

US dollar LIBOR. Based on the facts currently known, it is not practicable at this

time for HSBC to predict the resolution of these regulatory investigations or putative

class action lawsuits, including the timing and potential impact, if any, on HSBC.

Deutsche

Deutsche Bank AG has received various subpoenas and requests for information from

certain regulators and governmental entities in the United States and abroad,

including the U.S. Department of Justice, the U.S. Commodity Futures Trading

Commission, the U.S. Securities and Exchange Commission, and the European

Commission, in connection with setting interbank offered rates for various currencies.

These inquiries relate to various periods between 2005 and 2011. Deutsche Bank is

cooperating with these investigations. In addition, a number of civil actions, including

putative class actions, have been filed in federal courts in the United States against

Deutsche Bank AG, an affiliate and numerous other banks on behalf of certain parties

who allege that they transacted LIBOR-based financial instruments and that the

defendants manipulated, through various means, the U.S. dollar LIBOR rate and

prices of U.S. dollar LIBOR-based derivatives in various markets. Claims for

damages are asserted under various legal theories, including violations of the

Commodity Exchange Act and the antitrust laws. The civil actions have been

consolidated for pre-trial purposes in the United States District Court for the Southern

District of New York. The litigations are in their early stages.

UBS

Several government agencies, including the SEC, the US Commodity Futures Trading

Commission, the DOJ and the FSA, are conducting investigations regarding

submissions with respect to British Bankers‘ Association LIBOR rates. We

understand that the investigations focus on whether there were improper attempts by

UBS (among others), either acting on our own or together with others, to manipulate

LIBOR rates at certain times. In addition, the Swiss Competition Commission

(WEKO) has commenced an investigation of numerous banks and financial

intermediaries concerning possible collusion relating to LIBOR and TIBOR reference

rates and certain derivatives transactions.

Please refer to important disclosures and analyst certification information on pages 22 - 25. 12

16 July 2012

UBS has been granted conditional leniency or conditional immunity from authorities

in certain jurisdictions, including the Antitrust Division of the DOJ and WEKO, in

connection with potential antitrust or competition law violations related to

submissions for Yen LIBOR and Euroyen TIBOR. WEKO has also granted UBS

conditional immunity in connection with potential competition law violations related

to submissions for Swiss franc LIBOR and certain transactions related to Swiss franc

LIBOR. The Canadian Competition Bureau has granted UBS conditional immunity in

connection with potential competition law violations related to submissions for Yen

LIBOR. As a result of these conditional grants, we will not be subject to prosecutions,

fines or other sanctions for antitrust or competition law violations in the jurisdictions

where we have conditional immunity or leniency in connection with the matters we

reported to those authorities, subject to our continuing cooperation. However, the

conditional leniency and conditional immunity grants we have received do not bar

government agencies from asserting other claims against us. In addition, as a result of

the conditional leniency agreement with the DOJ, we are eligible for a limit on

liability to actual rather than treble damages were damages to be awarded in any civil

antitrust action under US law based on conduct covered by the agreement and for

relief from potential joint-and-several liability in connection with such civil antitrust

action, subject to our satisfying the DOJ and the court presiding over the civil

litigation of our cooperation. The conditional leniency and conditional immunity

grants do not otherwise affect the ability of private parties to assert civil claims

against us.

On 16 December 2011, the Japan Financial Services Agency (JFSA) commenced an

administrative action against UBS Securities Japan Ltd (UBS Securities Japan) based

on findings by the Japan Securities and Exchange Surveillance Commission (SESC)

that (i) a trader of UBS Securities Japan engaged in inappropriate conduct relating to

Euroyen TIBOR (Tokyo Interbank Offered Rate) and Yen LIBOR, including

approaching UBS AG, Tokyo Branch, and other banks to ask them to submit TIBOR

rates taking into account requests from the trader for the purpose of benefiting trading

positions; and (ii) serious problems in the internal controls of UBS Securities Japan

resulted in its failure to detect this conduct. Based on the findings, the JFSA issued a

Business Suspension Order requiring UBS Securities Japan to suspend trading in

derivatives transactions related to Yen LIBOR and Euroyen TIBOR from 10 January

to 16 January 2012 (excluding transactions required to perform existing contracts).

The JFSA also issued a Business Improvement Order that requires UBS Securities

Japan to (i) develop a plan to ensure compliance with its legal and regulatory

obligations and to establish a control framework that is designed to prevent

recurrences of the conduct identified in the JFSA‘s administrative action, and (ii)

provide periodic written reports to the JFSA regarding the company‘s implementation

of the measures required by the order. On the same day the JFSA also commenced an

administrative action against UBS AG, Tokyo Branch, based on a finding that an

employee of the Tokyo branch ―continuously received approaches‖ from an employee

of UBS Securities Japan regarding Euroyen TIBOR rate submissions, which was

determined to be an inappropriate practice that was not reported to the branch‘s

management. Pursuant to this administrative action, the JFSA issued an order under

the Japan Banking Act which imposes requirements similar to those imposed under

the Business Improvement Order directed to UBS Securities Japan.

A number of putative class actions and other actions have been filed in federal courts

in the US against UBS and numerous other banks on behalf of certain parties who

transacted in LIBOR based derivatives. The complaints allege manipulation, through

Please refer to important disclosures and analyst certification information on pages 22 - 25. 13

16 July 2012

various means, of the US dollar LIBOR rate and prices of US dollar LIBOR based

derivatives in various markets. Claims for damages are asserted under various legal

theories, including violations of the US Commodity Exchange Act and antitrust laws.

Credit Suisse

On February 3, 2012, following related investigations in the US and in the UK by the

respective authorities, the Swiss Competition Commission commenced an

investigation involving twelve banks and certain other financial intermediaries,

including the Group, concerning alleged collusive behaviour among traders to affect

the bid ask spread for derivatives tied to the LIBOR and TIBOR reference rates fixed

with respect to certain currencies. The investigation also relates to alleged collusive

agreements to influence these reference rates. Credit Suisse is not a panel bank for

Yen LIBOR, Yen TIBOR or Euroyen TIBOR. Credit Suisse is cooperating fully with

these investigations.

Please refer to important disclosures and analyst certification information on pages 22 - 25. 14

16 July 2012

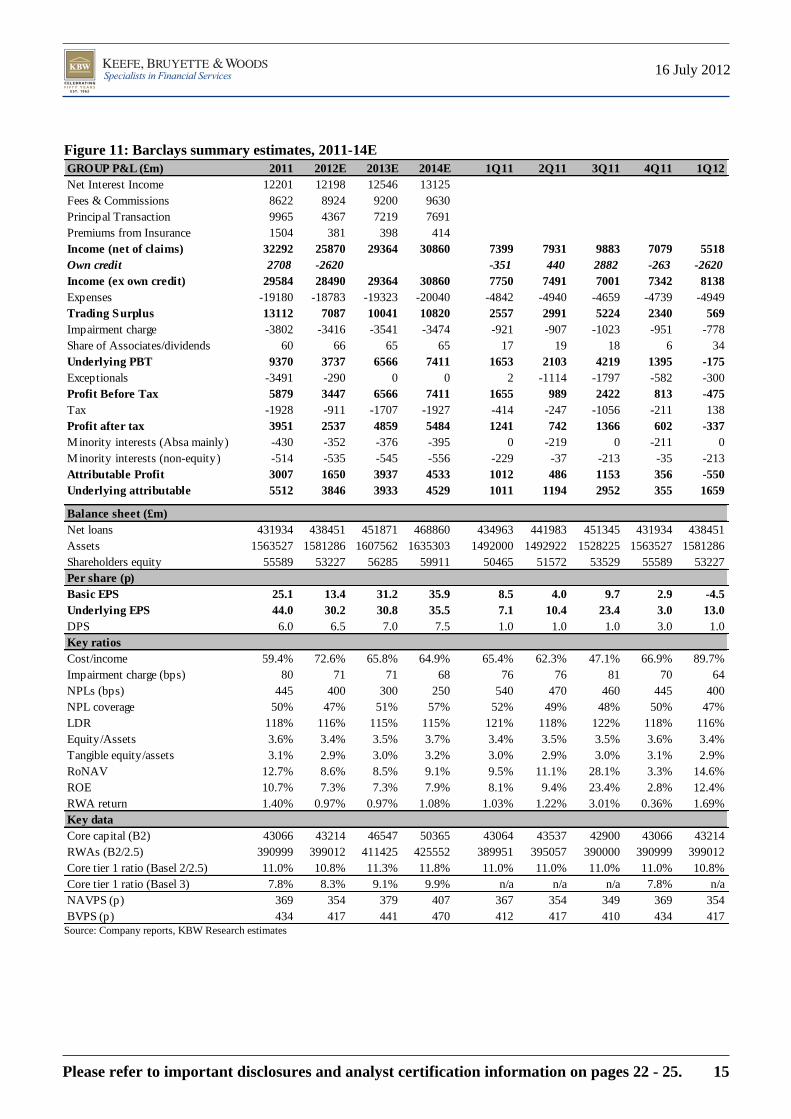

Figure 11: Barclays summary estimates, 2011-14E

GROUP P&L (£m) 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12

Net Interest Income 12201 12198 12546 13125

Fees & Commissions 8622 8924 9200 9630

Principal Transaction 9965 4367 7219 7691

Premiums from Insurance 1504 381 398 414

Income (net of claims) 32292 25870 29364 30860 7399 7931 9883 7079 5518

Own credit 2708 -2620 -351 440 2882 -263 -2620

Income (ex own credit) 29584 28490 29364 30860 7750 7491 7001 7342 8138

Expenses -19180 -18783 -19323 -20040 -4842 -4940 -4659 -4739 -4949

Trading Surplus 13112 7087 10041 10820 2557 2991 5224 2340 569

Impairment charge -3802 -3416 -3541 -3474 -921 -907 -1023 -951 -778

Share of Associates/dividends 60 66 65 65 17 19 18 6 34

Underlying PBT 9370 3737 6566 7411 1653 2103 4219 1395 -175

Exceptionals -3491 -290 0 0 2 -1114 -1797 -582 -300

Profit Before Tax 5879 3447 6566 7411 1655 989 2422 813 -475

Tax -1928 -911 -1707 -1927 -414 -247 -1056 -211 138

Profit after tax 3951 2537 4859 5484 1241 742 1366 602 -337

Minority interests (Absa mainly) -430 -352 -376 -395 0 -219 0 -211 0

Minority interests (non-equity) -514 -535 -545 -556 -229 -37 -213 -35 -213

Attributable Profit 3007 1650 3937 4533 1012 486 1153 356 -550

Underlying attributable 5512 3846 3933 4529 1011 1194 2952 355 1659

Balance sheet (£m)

Net loans 431934 438451 451871 468860 434963 441983 451345 431934 438451

Assets 1563527 1581286 1607562 1635303 1492000 1492922 1528225 1563527 1581286

Shareholders equity 55589 53227 56285 59911 50465 51572 53529 55589 53227

Per share (p)

Basic EPS 25.1 13.4 31.2 35.9 8.5 4.0 9.7 2.9 -4.5

Underlying EPS 44.0 30.2 30.8 35.5 7.1 10.4 23.4 3.0 13.0

DPS 6.0 6.5 7.0 7.5 1.0 1.0 1.0 3.0 1.0

Key ratios

Cost/income 59.4% 72.6% 65.8% 64.9% 65.4% 62.3% 47.1% 66.9% 89.7%

Impairment charge (bps) 80 71 71 68 76 76 81 70 64

NPLs (bps) 445 400 300 250 540 470 460 445 400

NPL coverage 50% 47% 51% 57% 52% 49% 48% 50% 47%

LDR 118% 116% 115% 115% 121% 118% 122% 118% 116%

Equity/Assets 3.6% 3.4% 3.5% 3.7% 3.4% 3.5% 3.5% 3.6% 3.4%

Tangible equity/assets 3.1% 2.9% 3.0% 3.2% 3.0% 2.9% 3.0% 3.1% 2.9%

RoNAV 12.7% 8.6% 8.5% 9.1% 9.5% 11.1% 28.1% 3.3% 14.6%

ROE 10.7% 7.3% 7.3% 7.9% 8.1% 9.4% 23.4% 2.8% 12.4%

RWA return 1.40% 0.97% 0.97% 1.08% 1.03% 1.22% 3.01% 0.36% 1.69%

Key data

Core capital (B2) 43066 43214 46547 50365 43064 43537 42900 43066 43214

RWAs (B2/2.5) 390999 399012 411425 425552 389951 395057 390000 390999 399012

Core tier 1 ratio (Basel 2/2.5) 11.0% 10.8% 11.3% 11.8% 11.0% 11.0% 11.0% 11.0% 10.8%

Core tier 1 ratio (Basel 3) 7.8% 8.3% 9.1% 9.9% n/a n/a n/a 7.8% n/a

NAVPS (p) 369 354 379 407 367 354 349 369 354

BVPS (p) 434 417 441 470 412 417 410 434 417 Source: Company reports, KBW Research estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 15

16 July 2012

Figure 12: HSBC summary estimates, 2011-14E

PROFIT & LOSS (U$m) 2010 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12

Net interest income 39441 40662 37600 37671 39981 9911 10324 10370 10057 10087

Fee income 17355 17160 17947 18949 20064 4371 4436 4257 4096 4310

Trading income 7210 6506 8317 8739 9329 2556 2256 106 1588 2882

Other income 4241 7952 910 3452 3645 202 1638 5214 898 -1078

Non-interest income 28806 31618 27174 31141 33038 7129 8330 9577 6582 6114

Total income 68247 72280 64774 68812 73019 17040 18654 19947 16639 16201

o/w own debt fair value -63 3933 -2644 0 0 -589 446 4114 -38 -2644

Total income (ex FVOD) 68310 68347 67418 68812 73019 17629 18208 15833 16677 18845

Expenses -37688 -41545 -38802 -37843 -38628 -10369 -10141 -9869 -11166 -10353

Pre-impairment profit 30559 30735 25972 30969 34392 6671 8513 10078 5473 5848

Pre-impairment profit (ex FVOD) 30622 26802 28616 30969 34392 7260 8067 5964 5511 8492

Impairment -14039 -12127 -10571 -9823 -8816 -2384 -2882 -3890 -2971 -2366

Profit after impairment 16520 18608 15401 21146 25575 4287 5631 6188 2502 3482

Associates/JV's 2517 3264 3779 4272 4831 619 937 967 741 840

Underlying PBT 19037 21872 19181 25417 30406 4906 6568 7155 3243 4322

Exceptionals 0 0 2900 0 0 0 0 0 0 0

PBT 19037 21872 22081 25417 30406 4906 6568 7155 3243 4322

o/w own debt fair value -63 3933 -2644 0 0 -589 446 4114 -38 -2644

PBT before fair value 19100 17939 24725 25417 30406 5495 6122 3041 3281 6966

Attributable 12746 16224 15930 18474 22414 4010 4919 5079 2216 2438

Balance Sheet

Gross loans 978449 957940 1008251 1046119 1096162 1016417 1056620 982148 957940 978860

Assets 2454689 2555579 2614855 2685336 2793354 2627728 2690987 2747732 2555579 2637218

Deposits 1227725 1253925 1316621 1382452 1451575 1274820 1318987 1271044 1253925 1284428

Per share (U$)

Basic EPS 0.72 0.91 0.87 1.00 1.20 0.22 0.28 0.28 0.12 0.13

Underlying EPS 0.72 0.91 0.71 1.00 1.20 0.23 0.27 0.28 0.12 0.13

DPS 0.36 0.41 0.45 0.50 0.54 0.09 0.09 0.09 0.14 0.09

BVPS 7.9 8.3 9.1 9.7 10.5 8.2 8.5 8.2 0.0 8.6

ROE 9.7% 11.3% 8.3% 10.7% 12.0% 11.3% 13.2% 13.6% 6.0% 6.4%

NAV 6.2 6.7 7.5 8.1 8.9 6.5 6.7 6.4 0.0 7.0

RoNAV 12.5% 14.2% 10.2% 12.9% 14.2% 14.3% 16.7% 17.3% 7.6% 8.0%

Key ratios

Margin (bps) 268 251 228 218 221

Cost/income (ex FVO) 55% 61% 58% 55% 53% 59% 56% 62% 67% 55%

Impairment charge (bps) 143 119 108 96 82

NPLs (bps) 479 434 430 400 350 492 434

NPL coverage 43% 42% 38% 41% 45% 73% 42%

Equity/assets 6.0% 6.2% 6.7% 7.0% 7.3% 5.8% 6.0% 5.8% 6.2% 6.2%

Tangible equity/assets 4.8% 5.1% 5.5% 5.9% 6.2% 4.7% 4.8% 4.6% 5.1% 5.1%

Core tier 1 ratio (Basel 2/2.5) 10.5% 10.1% 11.6% 12.3% 13.0% 10.7% 10.8% 10.6% 10.1% 10.5%

Core tier 1 ratio (B3) 7.5% 8.0% 9.5% 10.6% 11.4% n/a n/a n/a 8.0% n/a

GEOGRAPHIC SUMMARY

Europe 4302 4671 739 4532 5486 652 1495 2955 -431 -997

Hong Kong 5692 5823 6388 6654 7385 1562 1519 1288 1454 1897

Rest of Asia Pacific 5902 7471 8187 9150 10262 1634 2108 2008 1721 2024

Middle East 892 1492 1485 1698 1893 335 412 405 340 332

North America 454 100 309 635 2301 181 425 -265 -241 462

Latin America 1795 2315 2072 2748 3080 542 609 764 400 604

Total 19037 21872 19181 25417 30406 4906 6568 7155 3243 4322 Source: Company reports, KBW Research estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 16

16 July 2012

Figure 13: Lloyds summary estimates, 2011-14E

GROUP P&L 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12

Net interest income 12233 10570 10292 9620 3303 3063 3051 2816 2645

Other income 9111 8736 8716 8915 2391 2540 1952 2228 2194

Effects of liability mge, volatility & asset sales122 -240 0 0 -775 -146 159 884 -240

Operating income 21466 19066 19008 18534 4919 5457 5162 5928 4599

Insurance claims -343 -347 -344 -340 -114 -84 -87 -58 -108

Non-interest income 8768 8389 8373 8574 2277 2456 1865 2170 2086

Income (net of claims) 21123 18719 18665 18194 4805 5373 5075 5870 4491

Underlying income (net of claims) 21001 18959 18665 18194 5580 5519 4916 4986 4731

Expenses -10621 -10224 -9994 -9614 -2751 -2581 -2577 -2712 -2564

Operating profit 10502 8495 8671 8580 2054 2792 2498 3158 1927

Impairment charge -9787 -6697 -4343 -3102 -2608 -2814 -1956 -2409 -1657

Associates/joint ventures 27 21 16 11 9 3 5 10 3

PBT (before FV unwind) 742 1818 4344 5489 -545 -19 547 759 273

FV unwind 1943 750 -50 -300 829 839 97 178 355

PBT (pro-forma) 2685 2568 4294 5189 284 820 644 937 628

Exceptionals -6227 -1550 -418 -500 -3754 -601 -1251 -621 -340

PBT -3542 1018 3875 4689 -3470 219 -607 316 288

Attributable -2787 436 2746 2110 -2439 134 -519 37 0

Underlying attributable 1984 1211 2859 3519 189 558 514 165 12

Balance sheet

Gross loans (£bn) 584 534 470 466 n/d 607 596 584 557

Assets (£bn) 971 941 886 897 n/d 979 984 971 967

Shareholders equity (£bn) 45.9 46.6 49.3 52.1 n/d 44.9 45.7 45.9 46.1

AIEA (£bn) 585.4 547.0 509.9 453.6

Per share (p)

Basic EPS -4.1 0.6 4.0 4.5 -3.6 0.2 -0.8 0.1 0.0

o/w Core 7.4 5.5 5.6 6.1 0.0 0.0 1.8 2.4 2.0

o/w Non-Core -11.5 -4.9 -1.7 -1.6 0.0 0.0 -2.6 -2.4 -2.0

Basic diluted EPS -4.1 0.6 4.0 4.5 -3.6 0.2 -0.8 0.1 0.0

Diluted underlying EPS 2.9 1.8 4.1 5.1 0.3 0.8 0.8 0.2 0.0

DPS 0.0 0.0 0.0 1.5 0.0 0.0 0.0 0.0 0.0

Key ratios

Cost/income 50.3% 54.6% 53.5% 52.8% 57.3% 48.0% 50.8% 46.2% 57.1%

Margin (bps) 207 193 199 209 216 209 205 197 195

Impairment charge (bps) 164 120 87 66 130 163 116

NPLs (bps) 1031 850 756 356 1048 1031

NPL coverage 46% 56% 61% 89% 45% 45% 46% 46% 47%

LDR 139% 122% 111% 106% 150% 149% 146% 139% 131%

Tangible equity/assets 4.0% 4.3% 4.9% 5.2% 3.7% 3.9% 4.0% 4.0% 4.1%

Key data

Core tier 1 ratio (Basel 2.5) 10.8% 11.7% 13.4% 14.7% 10.0% 10.1% 10.3% 10.8% 10.9%

Tier 1 ratio (Basel 2.5) 12.5% 13.5% 15.4% 16.8% 11.4% 11.6% 11.9% 12.5% 12.6%

Core tier 1 ratio (Basel 3) 7.0% 7.5% 9.0% 10.5% n/a n/a n/a 7.0% n/a

NAVPS (p) 57 58 63 68 54 56 57 57 57

DIVISIONAL SUMMARY

Retail 2,797 2,250 2,215 2,210

Wholesale -1,346 -240 532 1,116

Commercial 446 457 500 549

Wealth & International -4,130 -2,301 -672 -247

Insurance 1,465 1,484 1,544 1,617

Group & Central 1,510 169 226 243 Source: Company reports, KBW Research estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 17

16 July 2012

Figure 14: RBS summary estimates, 2011-14E

GROUP P&L (£m) 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12

Net interest income 12689 11738 11292 11642 3302 3233 3078 3076 3007

Non-interest income (ex premiums) 10764 9948 9822 11274 3662 3459 1979 1664 3186

Insurance premiums (net of claims) 1288 1166 1158 0 237 297 302 452 289

Non-interest income 12052 11114 10980 11274 3899 3756 2281 2116 3475

Total income (net of claims) 24741 22852 22273 22917 7201 6989 5359 5192 6482

Operating Expenses -15478 -14862 -13766 -12988 -4121 -3892 -3821 -3644 -3984

Pre-impairment profit 9263 7990 8506 9929 3080 3097 1538 1548 2498

Impairment charges -7439 -4989 -3817 -2617 -1947 -2264 -1536 -1692 -1314

Operating Profit 1824 3000 4689 7312 1133 833 2 -144 1184

Exceptionals -2590 -3472 -692 -492 -1249 -1511 2002 -1832 -2588

PBT -766 -472 3997 6820 -116 -678 2004 -1976 -1404

Attributable profit -1997 -1730 2124 4403 -528 -897 1226 -1798 -1524

Balance sheet

Loans 454112 424267 389810 381298 494148 489572 485573 454112 440406

Assets 1506867 1333514 1235504 1172971 1413253 1445969 1607728 1506867 1403021

Funded balance sheet 977249 909820 875363 866851 1052205 1051097 1035384 977249 949667

S/hers equity (incl B Shares) 70075 68866 70990 75392 69332 70000 72699 70075 68672

Per share (B share diluted)

Basic EPS (p) -18.1 -15.8 19.1 39.7 -4.9 -8.3 10.4 -16.2 -14.1

Adjusted EPS (p) 2.1 8.8 24.4 43.6 3.9 2.9 -1.9 -2.5 4.2

Core adjusted EPS (p) 38.9 36.5 42.7 47.5 15.2 11.4 6.7 5.7 11.7

Key ratios

Cost/income 62.6% 65.0% 61.8% 56.7% 57.2% 55.7% 71.3% 70.2% 61.5%

Margin (bps) 192 183 186 199 200 196 184 184 189

Impairment charge (bps) 151 113 94 68 152 181 119 141 116

NPLs (bps) 862 800 700 400 799 830 844 862 864

NPLs (£m) 40845 33941 27287 15252 41041 42350 42726 40845 39800

NPL coverage 49% 58% 54% 74% 47% 49% 49% 49% 51%

RoNAV 0.4% 1.8% 5.0% 8.4% 3.1% 2.3% -1.7% -2.1% 3.5%

RoE 0.3% 1.4% 3.9% 6.7% 2.5% 1.8% -1.3% -1.6% 2.8%

Key data

Basel II

Core tier 1 ratio (Basel 2) 10.6% 11.4% 11.9% 13.5% 11.2% 11.1% 11.3% 10.6% 10.8%

Core tier 1 ratio (Basel 3) 6.8% 8.0% 9.5% 11.0% n/a n/a n/a 6.8% 7.2%

Tier 1 ratio (Basel 2) 13.0% 13.9% 14.2% 15.9% 13.5% 13.5% 13.8% 13.0% 13.2%

NAVPS (p) 477 480 499 539 493 493 499 477 480

BVPS (p) 612 613 632 672 625 625 633 612 614

Tangible equity/assets 3.5% 4.0% 4.5% 5.2% 3.9% 3.5% 3.5% 3.5% 3.8%

Tangible equity/assets (ex derivs) 5.5% 5.9% 6.4% 7.0% 5.2% 5.4% 5.4% 5.5% 5.7%

DIVISIONAL SUMMARY

Markets 899 1683 2043 2156 1029 327 -348 -109 824

International Banking 755 485 548 619 226 149 228 152 97

UK Retail 2021 1890 1834 1950 518 535 510 458 477

UK Corporate 1924 1840 1761 1879 617 472 429 406 492

Wealth 248 312 364 410 70 60 45 73 45

Ulster Bank -984 -1001 -306 -35 -365 -178 -208 -233 -310

US Retail & Commercial 537 601 706 819 94 143 123 177 102

RBS Insurance 454 388 452 n/a 67 139 123 125 84

Central items 191 -144 0 0 -32 56 78 89 -144

Total Core 6045 6054 7403 7798 2224 1703 980 1138 1667

Non-Core -4221 -3053 -2714 -486 -1091 -870 -978 -1282 -483

Underlying PBT 1824 3000 4689 7312 1133 833 2 -144 1184 Source: Company reports, KBW Research estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 18

16 July 2012

Figure 15: Credit Suisse summary estimates, 2009-14E Group 2009 2010 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12E 2Q12 / 2Q12 /

CHF mn 1Q12 2Q11

Net interest income 6,891 6,541 6,433 7,592 8,068 9,094 1,753 1,377 1,646 1,657 1,884 1,807 -4% 31%

Fee and commission income 13,750 14,078 12,952 13,489 15,209 16,666 3,671 3,463 3,061 2,757 3,172 3,427 8% -1%

Net trading income 12,151 9,338 5,020 2,379 4,256 3,853 2,011 1,116 1,920 -27 189 880 366% -21%

Other income 502 1,429 1,820 1,252 1,000 1,000 721 936 62 101 802 150 -81% -84%

Revenues 33,294 31,386 26,225 24,712 28,532 30,613 8,156 6,892 6,689 4,488 6,047 6,264 4% -9%

Loan loss charge -506 79 -187 -218 -316 -320 7 -13 -84 -97 -34 -57 66% —

Personnel expense -15,013 -14,599 -13,213 -12,309 -11,955 -12,810 -4,029 -3,096 -3,067 -3,021 -3,711 -2,800 -25% -10%

Other expense -9,698 -9,379 -9,364 -8,186 -8,505 -9,137 -2,168 -2,143 -2,694 -2,359 -2,104 -2,076 -1% -3%

Operating profit 8,077 7,487 3,461 3,999 7,756 8,347 1,966 1,640 844 -989 198 1,332 572% -19%

Intangible effects 0 0 0 0 0 0 0 0 0 0 0 0 — —

Extraordinary items, net 0 0 0 0 0 0 0 0 0 0 0 0 — —

Accounting changes, net 0 0 0 0 0 0 0 0 0 0 0 0 — —

Discontinued operations, net 169 -19 0 0 0 0 0 0 0 0 0 0 — —

Pre-tax profit 8,246 7,468 3,461 3,999 7,756 8,347 1,966 1,640 844 -989 198 1,332 572% -19%

Tax -1,835 -1,548 -671 -879 -1,788 -1,941 -465 -271 -332 397 16 -315 -2069% 16%

Minorities 313 -822 -837 -560 -959 -948 -362 -601 171 -45 -170 -130 -24% -78%

Net profit [before pref dividend] 6,724 5,098 1,953 2,560 5,009 5,457 1,139 768 683 -637 44 887 1915% 15%

Preferred dividend -131 -162 -216 -200 -200 -200 0 -102 0 -114 0 -100 — —

Net profit [after pref dividend] 6,593 4,936 1,737 2,360 4,809 5,257 1,139 666 683 -751 44 787 1688% 18%

Deduct: unvested share awards -388 -309 -195 -142 -280 -306 -65 -91 -39 0 -3 -47 — —

Net profit [for basic EPS] 6,205 4,627 1,542 2,218 4,529 4,951 1,074 575 644 -751 41 739 1703% 29%

Net profit [for basic EPS] – reported 6,205 4,627 1,542 2,218 4,529 4,951 1,074 575 644 -751 41 739 1703% 29%

Deduct: disposal gains, net -188 0 0 -146 — — — — — 0 -146 —

Add: intangible effects 0 0 0 0 — — — — — 0 0 —

Add: restructuring charges, net 0 0 1,284 272 — — — 94 209 981 47 75

Add: litigation charges etc 602 183 453 0 — — — — 428 25 0 —

Deduct: own-debt gains [FVOD, stand-alone & DVA] 1,088 -162 -1,194 1,110 0 0 467 -69 -1,245 -348 1,110 0

Deduct: other -601 -522 0 0 0 — 0 0 0 0 0 0

Net profit – adjusted 7,105 4,126 2,085 3,454 4,529 4,951 1,541 600 36 -93 1,052 814 — 36%

LLC / net loans 0.21% -0.04% 0.08% 0.10% 0.14% 0.14% -0.01% 0.02% 0.15% 0.17% 0.06% 0.10%

Cost / income 74% 76% 86% 83% 72% 72% 76% 76% 86% 120% 96% 78%

Tax rate [effective] 22% 21% 19% 22% 23% 23% 24% 17% 39% 40% -8% 24%

Op. RoNAV 31.9% 17.2% 9.1% 14.4% 15.5% 15.1% 26.0% 10.3% 0.6% -1.7% 18.4% 13.8%

Shares outstanding [basic] 1,169 1,174 1,220 1,268 1,311 1,311 1,201 1,199 1,203 1,220 1,225 1,268

Ø shares outstanding [FD] 1,210 1,201 1,207 1,290 1,333 1,333 1,188 1,208 1,224 1,207 1,257 1,301

EPS [diluted] 5.13 3.85 1.28 1.72 3.40 3.71 0.90 0.48 0.53 -0.62 0.03 0.57

Operating EPS [diluted] 5.87 3.44 1.73 2.68 3.40 3.71 1.30 0.50 0.03 -0.08 0.84 0.63

Book per share [basic] 32.1 28.4 27.6 27.9 30.7 33.7 28.4 26.0 27.9 27.6 27.4 26.7

NAV per share [basic] 23.9 20.8 20.32 21.17 24.13 27.13 21.1 19.2 20.7 20.3 20.4 20.0 -2% 4%

ANAV per share [basic] 20.8 19.6 18.15 20.01 23.00 27.13 20.3 18.4 18.7 18.2 19.2 18.8 -2% 2%

Buy-back per share [basic] 0.0 0.0 0.0 0.0 0.0 0.0

Dividend per share [basic] 2.00 1.30 0.75 0.75 1.00 1.50

Group AUM 1,229,000 1,253,000 1,229,500 1,290,669 1,355,202 1,422,962 1,282,400 1,233,300 1,196,800 1,229,500 1,249,600 1,244,434

AUM growth 4.7% 2.0% -1.9% 5.0% 5.0% 5.0% 2.3% -3.8% -3.0% 2.7% 1.6% -0.4%

Group inflows 44,200 69,000 40,900 21,820 38,649 54,234 19,100 14,300 7,100 400 -7,100 7,804

'Headline' tier 1 capital 36,207 37,725 36,844 38,728 38,108 43,099 38,514 37,076 37,124 36,844 36,668 37,674

Deduct: 'hybrid capital' [CS basis] -12,198 -11,098 -10,888 -9,046 -9,046 -9,046 -10,948 -10,364 -10,564 -10,888 -9,046 -9,046

Deduct: perpetual notes -1,742 -3,350 -3,365 -3,417 -3,417 -3,417 -3,492 -3,526 -3,435 -3,365 -3,417 -3,417

'Equity' tier 1 capital 22,267 23,277 22,591 26,265 25,645 30,636 24,074 23,186 23,125 22,591 24,205 25,211

Risk-weighted assets 221,609 218,702 241,753 216,211 279,020 282,221 212,196 203,741 210,138 241,753 234,390 227,594

Ø RWA 239,309 227,478 214,076 228,162 247,616 280,620 215,449 207,969 206,940 225,946 238,072 230,992

'Headline' tier 1 ratio 16.3% 17.2% 15.2% 17.9% 13.7% 15.3% 18.2% 18.2% 17.7% 15.2% 15.6% 16.6%

'Equity' tier 1 ratio 10.0% 10.6% 9.3% 12.1% 9.2% 10.9% 11.3% 11.4% 11.0% 9.3% 10.3% 11.1%

Basel 3 common tier 1 capital (KBWe) 11,674 18,206 13,546 19,561 25,645 30,636 16,964 16,959 16,197 13,546 15,240 17,132

Basel 3 RWA [no phasing] (KBWe) 371,857 393,185 335,690 282,651 279,020 282,221 387,966 372,093 369,731 335,690 293,768 296,095

Basel 3 common tier 1 ratio (KBWe) 3.1% 4.6% 4.0% 6.9% 9.2% 10.9% 4.4% 4.6% 4.4% 4.0% 5.2% 5.8%

Tier 1 leverage ratio [FINMA style] 4.2% 4.4% 4.6% 4.9% 4.8% 5.4% 4.7% 4.7% 4.9% 4.6% 4.7% 4.8% Source: KBW estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 19

16 July 2012

Figure 16: Deutsche Bank summary estimates, 2009-14E Group 2009 2010 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12E 2Q12 / 2Q12 /

€ mn 1Q12 2Q11

Net interest income 12,460 15,582 17,444 14,953 15,849 16,355 4,167 4,492 4,274 4,511 4,193 3,908 -7% -13%

Commissions 8,915 10,670 11,544 11,305 11,997 12,597 3,081 3,047 2,806 2,610 2,849 2,854 0% -6%

Trading revenues, net 2,581 3,353 3,059 6,229 6,553 6,867 2,653 710 -422 118 2,399 1,319 -45% 86%

Other -527 -1,039 1,181 61 416 400 573 291 657 -340 -248 102 -141% -65%

Revenues 23,429 28,566 33,228 32,263 34,815 36,219 10,474 8,540 7,315 6,899 9,193 7,858 -15% -8%

Loan loss charge -2,630 -1,273 -1,840 -1,569 -1,394 -1,294 -373 -464 -463 -540 -314 -419 34% -10%

Compensation and benefits -11,310 -12,672 -13,135 -13,175 -13,820 -14,058 -4,278 -3,365 -2,694 -2,798 -3,656 -3,135 -14% -7%

Other expenses -8,949 -10,616 -12,863 -11,123 -11,308 -11,502 -2,802 -2,933 -3,216 -3,912 -3,334 -2,565 -23% -13%

Operating profit 540 4,005 5,390 6,396 8,293 9,365 3,021 1,778 942 -351 1,889 1,739 -8% -2%

Intangible effects 134 -29 0 -10 0 0 0 0 0 0 -10 0 — —

Accounting changes, net 0 0 0 0 0 0 0 0 0 0 0 0 — —

Pre-tax profit 674 3,976 5,390 6,386 8,293 9,365 3,021 1,778 942 -351 1,879 1,739 -7% -2%

Tax -243 -1,646 -1,064 -1,907 -2,654 -2,997 -891 -545 -165 537 -478 -557 16% —

Minority Interest 14 -20 -194 -110 -120 -120 -68 -35 -52 -39 -20 -30 — —

Net profit 445 2,310 4,132 4,368 5,520 6,248 2,062 1,198 725 147 1,381 1,153 — -4%

Net profit – reported 445 2,310 4,132 4,368 5,520 6,248 2,062 1,198 725 147 1,381 1,153 — —

Add: restructuring charges, net 296 0 293 304 225 0 59 30 31 173 68 83 — —

Deduct: disposal gains, net -807 0 407 193 0 0 — — — 407 193 0 — —

Provisions/releases, net -74 0 285 0 0 0 — — — 285 0 0 — —

Other, net 0 2,338 259 0 0 0 259 — — — 0 0 — —

Add: intangible effects -134 -179 0 0 0 0 — — — — 0 0 — —

Tax releases etc -1,159 0 0 0 0 0 — — — — 0 0 — —

Net profit – adjusted -1,433 4,469 5,375 4,865 5,745 6,248 2,380 1,228 756 1,012 1,642 1,235 -25% 1%

Cost / income 86% 82% 78% 75% 72% 71% 68% 74% 81% 97% 76% 73%

LLC / net loans 1.02% 0.31% 0.45% 0.40% 0.37% 0.33% 0.38% 0.47% 0.45% 0.52% 0.31% 0.42%

Pre-tax return on Ø 'active equity' 2.0% 9.7% 10.7% 11.5% 13.9% 14.5% 24.8% 14.4% 7.5% -2.7% 14.0% 12.6%

Tax rate [effective] 36.1% 41.4% 19.7% 29.9% 32.0% 32.0% 29.5% 30.7% 17.5% 153.0% 25.4% 32.0%

ROE 1.3% 5.6% 8.2% 7.9% 9.3% 9.6% 16.7% 9.6% 5.7% 1.1% 10.2% 8.4%

Op. RONAV -6.0% 15.8% 15.2% 12.2% 13.0% 12.7% 27.9% 14.0% 8.4% 10.9% 17.1% 12.5%

# shares outstanding [basic] 697 932 919 914 914 914 940 928 914 919 916 923

Ø # shares [diluted] 714 773 959 955 957 957 969 968 951 949 960 958

EPS [diluted] 0.62 2.99 4.31 4.57 5.77 6.53 2.13 1.24 0.76 0.15 1.44 1.20

Operating EPS [diluted] -2.01 5.79 5.60 5.09 6.01 6.53 2.46 1.27 0.79 1.07 1.71 1.29

Book per share [basic] 52.6 52.4 58.1 62.6 67.9 74.0 53.2 53.9 56.8 58.1 60.0 60.0

NAV per share [basic] 38.0 35.6 40.9 45.4 50.7 56.8 37.1 37.9 39.8 40.9 42.8 43.0

Dividend per share [basic] 0.68 0.75 0.75 0.75 0.75 1.00

Group AUM 880,000 1,179,000 1,116,000 n/a n/a n/a 1,112,000 1,109,000 1,083,000 1,116,000 1,128,000 n/a

Group AUM growth 7.8% 34.0% -5.3% n/a n/a n/a n/a -0.3% -2.3% 3.0% 1.1% n/a

Group inflows 13,000 -1,000 -2,000 n/a n/a n/a 5,000 0 -10,000 3,000 -2,000 n/a

Group inflows / AUM 1.6% -0.1% -0.2% n/a n/a n/a 0.4% 0.0% -0.9% 0.3% -0.2% n/a

B2.5 B2.5 B3 B3 B2 B2 B2.5 B2

'Headline' tier 1 capital 34,406 42,565 49,047 51,852 52,249 59,101 43,802 44,658 46,638 49,047 49,419 50,400

Deduct: hybrid capital -10,616 -12,593 -12,734 -12,416 -12,416 -12,416 -12,222 -12,141 -12,548 -12,734 -12,416 -12,416

Add: unrealised gain on industrial holdings n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a

'Equity' tier 1 capital 23,790 29,972 36,313 39,436 39,833 46,685 31,580 32,517 34,090 36,313 37,003 37,984

B2.5 B2.5 B3 B3

Credit RWA 217,003 285,218 258,398 224,779 364,385 369,356 266,361 261,803 278,498 258,398 251,775 232,038

Market RWA 24,880 23,660 68,123 82,000 82,000 82,000 24,553 21,490 22,423 68,123 64,929 82,000

Operational RWA 31,593 37,326 50,697 50,700 50,700 50,700 36,960 36,376 36,697 50,697 51,718 50,700

Risk-weighted assets (RWA) 273,476 346,204 381,200 357,479 497,085 502,056 327,874 319,669 337,618 381,200 368,422 364,738

RWA growth -11% 27% 10% -6% 39% 1% -5% -3% 6% 13% -3% -1%

'Headline' tier 1 ratio 12.6% 12.3% 12.9% 14.5% 10.5% 11.8% 13.4% 14.0% 13.8% 12.9% 13.4% 13.8%

'Equity' tier 1 ratio [no transition] 8.7% 8.7% 9.5% 11.0% 8.0% 9.3% 9.6% 10.2% 10.1% 9.5% 10.0% 10.4%

Basel 3 common tier 1 capital (KBWe) 31,419 34,849 39,833 46,685 31,393 30,815 31,399 31,419 32,444 33,294

Basel 3 RWA [no phasing] (KBWe) 525,380 482,466 497,085 502,056 616,436 592,085 591,459 525,380 507,609 499,217

Basel 3 common tier 1 ratio (KBWe) 6.0% 7.2% 8.0% 9.3% 5.1% 5.2% 5.3% 6.0% 6.4% 6.7%

Level 3 assets 58,220 46,656 47,573 n/a n/a 0 44,089 45,521 49,533 47,573 42,409 n/a

Level 3 liabilities 18,169 13,003 13,421 n/a n/a 0 11,673 11,866 15,140 13,421 11,883 n/a

Level 3 assets & liabilities 76,389 59,659 60,994 n/a n/a 0 55,762 57,387 64,673 60,994 54,292 n/a

Level 3 assets & liabilities / tier 1 2.2x 1.4x 1.2x n/a n/a 0.0x 1.3x 1.3x 1.4x 1.2x 1.1x n/a

Total assets [IFRS] 1,500,664 1,906,000 2,164,000 1,912,428 1,768,670 1,678,541 1,842,000 1,850,000 2,282,000 2,164,000 2,103,000 2,029,823

Deduct: derivative netting / other -609,664 -695,000 -897,000 -656,428 -512,670 -422,541 -640,000 -641,000 -986,000 -897,000 -847,000 -773,823

Total assets [US GAAP style] 891,000 1,211,000 1,267,000 1,256,000 1,256,000 1,256,000 1,202,000 1,209,000 1,296,000 1,267,000 1,256,000 1,256,000

Adjusted sh' equity [DBK style] 39,269 52,368 59,160 61,163 65,997 71,560 53,290 53,278 57,608 59,160 58,905 59,368

Leverage multiple [DBK style] 22.7x 23.1x 21.4x 20.5x 19.0x 17.6x 22.6x 22.7x 22.5x 21.4x 21.3x 21.2x Source: KBW estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 20

16 July 2012

Figure 17: UBS summary estimates, 2009-14E Group [incl. indu hldgs] 2009 2010 2011 2012E 2013E 2014E 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12E 2Q12E / 2Q12E /

CHF mn 1Q12 2Q11Net interest income 6,445 6,215 6,827 6,149 6,260 6,592 1,781 1,440 1,861 1,745 1,591 1,600 1% 11%

Net fee and commission income 17,711 17,160 15,236 15,341 16,685 17,918 4,240 3,879 3,557 3,560 3,843 3,700 -4% -5%

Net trading income -324 7,471 4,342 5,842 7,714 8,019 2,203 1,724 -28 443 961 1,569 63% -9%

Other income 599 1,214 1,468 193 0 0 117 112 1,111 128 93 100 8% -11%

Total revenues 24,431 32,060 27,873 27,526 30,659 32,530 8,341 7,155 6,501 5,876 6,488 6,969 7% -3%

Loan loss charge -1,832 -66 -84 -119 -208 -269 3 16 -89 -14 37 -52 -241% -425%

Personnel expense -16,542 -16,920 -15,591 -14,806 -16,191 -16,708 -4,407 -3,925 -3,758 -3,501 -3,643 -3,685 1% -6%

Other expense -7,296 -7,503 -6,721 -6,159 -6,208 -6,284 -1,679 -1,569 -1,623 -1,850 -1,556 -1,564 1% 0%

Operating profit -1,239 7,571 5,477 6,442 8,051 9,268 2,258 1,677 1,031 511 1,326 1,668 26% -1%

Amort. of intangibles -1,324 -117 -126 -92 -92 -133 -24 -22 -51 -29 -23 -23 0% 5%

Discontinued operations, net -7 2 0 0 0 0 0 0 0 0 0 0 — —

Pre-tax profit -2,570 7,456 5,351 6,350 7,959 9,135 2,234 1,655 980 482 1,303 1,645 26% -1%

Tax 443 380 -923 -1,111 -1,393 -1,599 -426 -377 40 -160 -476 -329 -31% -13%

Minorities -611 -304 -268 -271 -260 -260 -2 -262 -2 -2 -1 -270 26900% 3%

Net profit -2,738 7,532 4,160 4,968 6,306 7,277 1,806 1,016 1,018 320 826 1,046 27% 3%

Net profit, reported -2,738 7,532 4,160 4,968 6,306 7,277 1,806 1,016 1,018 320 826 1,046 27% 3%

Deduct: disposal gains, net 311 -392 -578 0 0 0 0 0 -578 0 0 0

Add: intangible effects 1,324 117 126 92 92 133 24 22 51 29 23 23

Add: restructuring charges, net 575 105 317 101 0 0 0 0 310 7 101 0

Add: litigation charges etc 0 173 0 0 0 0 0 0 0 0 0 0

Deduct: own-debt & MCN gains 1,725 558 -1,536 1,164 0 0 133 25 -1,765 71 1,164 0

Deduct: other -1,240 0 0 -388 0 0 0 0 0 0 -388 0

Operating profit, net -43 8,093 2,489 5,937 6,398 7,410 1,963 1,063 -964 427 1,726 1,069 -38% 1%

Cost / income 98% 76% 80% 76% 73% 71% 73% 77% 83% 91% 80% 75%

LLC / net loans 0.60% 0.02% 0.03% 0.04% 0.07% 0.09% 0.00% -0.02% 0.11% 0.02% -0.05% 0.07%

Tax rate [effective] 17.2% -5.1% 17.2% 17.5% 17.5% 17.5% 19.1% 22.8% -4.1% 33.2% 36.5% 20.0%

ROE -7.8% 16.7% 8.5% 9.1% 10.8% 11.6% 15.4% 8.7% 8.2% 2.4% 6.2% 7.8%

Op. RoNAV -0.2% 23.6% 6.3% 13.2% 13.0% 13.8% 21.2% 11.3% -9.5% 4.0% 15.7% 9.7%

Shares outstanding [basic] 3,794 3,793 3,747 3,776 3,776 3,776 3,804 3,768 3,741 3,747 3,776 3,776

Ø shares outstanding [diluted] 3,669 3,837 3,834 3,819 3,819 3,819 3,849 3,869 3,815 3,800 3,819 3,819

EPS [diluted] -0.75 1.96 1.09 1.30 1.65 1.91 0.47 0.26 0.27 0.08 0.22 0.27

Operating EPS [diluted] -0.01 2.11 0.65 1.55 1.68 1.94 0.51 0.27 -0.25 0.11 0.45 0.28

Book per share [basic] 10.81 12.35 14.29 15.09 15.96 17.24 12.28 12.54 13.85 14.29 14.10 14.27

NAV per share [basic] 7.91 9.76 11.70 12.64 13.53 14.84 9.74 10.19 11.34 11.70 11.62 11.80 2% 16%

Buy-back per share 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Dividend per share 0.00 0.00 0.10 0.40 0.65 0.80

Group AUM 2,233,000 2,152,000 2,167,000 2,138,092 2,270,183 2,426,976 2,198,000 2,069,000 2,025,000 2,167,000 2,088,000 2,076,515

Group AUM growth 2.7% -3.6% 0.7% -1.3% 6.2% 6.9% 2.1% -5.9% -2.1% 7.0% -3.6% -0.6%Group inflows -147,300 -14,400 41,400 29,709 44,531 66,005 22,300 8,700 5,200 5,200 2,700 7,278

Group inflows / AUM -6.8% -0.6% 1.9% 1.4% 2.1% 2.9% 1.0% 0.4% 0.3% 0.3% 0.1% 0.3%

'Headline' tier 1 capital 31,798 35,272 38,370 42,579 46,431 49,437 36,379 37,387 38,121 38,370 39,570 40,238

Deduct: hybrid capital -7,224 -4,903 -4,356 -4,286 -4,286 -3,036 -4,561 -4,252 -4,327 -4,356 -4,286 -4,286

'Equity' tier 1 capital 24,574 30,369 34,014 38,293 42,145 46,401 31,818 33,135 33,794 34,014 35,284 35,952

Credit RWA 140,494 119,919 126,804 111,988 183,716 187,511 121,854 115,986 123,543 126,804 116,654 115,907

Non-counterparty 7,026 6,195 6,050 6,051 6,051 6,051 6,153 5,862 5,924 6,050 6,051 6,051

Market RWA 12,861 20,813 49,241 40,087 40,087 38,453 25,389 34,832 28,462 49,241 34,387 40,087

Operational RWA 46,144 51,948 58,867 53,999 53,999 49,000 49,964 49,544 49,328 58,867 53,999 53,999

Risk-weighted assets 206,525 198,875 240,962 212,125 283,853 281,014 203,361 206,224 207,257 240,962 211,092 216,044

Ø RWA 247,701 206,244 209,190 216,946 291,477 282,434 201,118 204,793 206,741 224,110 226,027 213,568

RWA growth -32% -4% 21% -12% 34% -1% 2% 1% 1% 16% -12% 2%

'Headline' tier 1 ratio 15.4% 17.7% 15.9% 20.1% 16.4% 17.6% 17.9% 18.1% 18.4% 15.9% 18.7% 18.6%

'Equity' tier 1 ratio 11.9% 15.3% 14.1% 18.1% 14.8% 16.5% 15.6% 16.1% 16.3% 14.1% 16.7% 16.6%

Basel 3 RWA (KBWe) 350,594 389,608 380,000 317,171 283,853 281,014 407,044 402,231 400,000 380,000 350,000 333,438

Basel 3 common tier 1 capital (KBWe) 14,400 19,190 25,400 29,302 34,798 39,554 21,108 24,101 24,600 25,400 26,100 26,644

B3 CET1 ratio 4.1% 4.9% 6.7% 9.2% 12.3% 14.1% 5.2% 6.0% 6.2% 6.7% 7.5% 8.0%

Level 3 assets, net 37,600 24,500 25,200 n/a n/a n/a 23,500 20,800 24,500 25,200 21,200 n/a

Level 3 liabilities, net 27,700 24,700 23,500 n/a n/a n/a 22,200 20,100 20,800 23,500 20,400 n/a

Level 3 assets & liabilities 65,300 49,200 48,700 n/a n/a n/a 45,700 40,900 45,300 48,700 41,600 n/a

Level 3 assets & liabilities / tier 1 2.1x 1.4x 1.3x n/a n/a n/a 1.3x 1.1x 1.2x 1.3x 1.1x n/a

Tier 1 leverage ratio [FINMA style] 3.9% 4.4% 5.4% 6.2% 6.9% 7.5% 4.8% 4.9% 5.5% 5.4% 5.6% 5.8% Source: KBW estimates

Please refer to important disclosures and analyst certification information on pages 22 - 25. 21

16 July 2012

IMPORTANT DISCLOSURES

RESEARCH ANALYST CERTIFICATION: We, Mark Phin, CFA, Andrew Stimpson, Vasco Moreno and Luke Birtwistle, herebycertify that the views expressed in this research report accurately reflect our personal views about the subject companies and theirsecurities. We also certify that We have not been, and will not be receiving direct or indirect compensation in exchange for expressing thespecific recommendation in this report.

Analysts’ Compensation: The equity research analysts responsible for the preparation of this report receive compensation based uponvarious factors, including the quality and accuracy of research, client feedback, competitive factors, and overall firm revenues, whichinclude revenues from, among other business units, Institutional Equities and Investment Banking.

For disclosures pertaining to recommendations or estimates made on a security mentioned in this report, please see the most recentlypublished company report or visit our global disclosures page on our website at http://www.kbw.com/research/disclosures or see thesection below titled "Disclosure Information" for further information on how to obtain these disclosures.

AFFILIATE DISCLOSURES: This report has been prepared by Keefe, Bruyette & Woods Inc. (“KBWI”) and/or its affiliates Keefe,Bruyette & Woods Limited and Keefe, Bruyette & Woods Asia Limited all of which are subsidiaries of KBW, Inc. (collectively“KBW”). Keefe, Bruyette & Woods Inc. is regulated by FINRA, NYSE, and the United States Securities and Exchange Commission, andits headquarters is located at 787 7th Avenue, New York, NY 10019. Keefe, Bruyette & Woods Limited is registered in England andWales, no. 04605071 and its registered office is 7th Floor, One Broadgate, London EC2M 2QS. KBWL is authorised and regulated by theUK Financial Services Authority ("FSA"), entered on the FSA's register, no. 221627 and is a member of the London Stock Exchange.Keefe, Bruyette & Woods Asia Limited is a licensed corporation regulated by the Securities and Futures Commission of Hong Kong("SFC") (CE No.: AUI281). Its headquarters is located at 3101, 31/F Central Plaza, 18 Harbour Road, Wanchai, Hong Kong. Disclosuresin the Important Disclosures section referencing KBW include one or all affiliated entities unless otherwise specified.

Registration of non-US Analysts: Any non-US Research Analyst employed by a non-US affiliate of KBWI contributing to this report isnot registered/qualified as research analyst with FINRA and/or the NYSE and may not be an associated person of KBWI and thereforemay not be subject to NASD Rule 2711 or NYSE Rule 472 restrictions on communications with a subject company, public appearances,and trading securities held by a research analyst account.

Disclosure Information. For current company specific disclosures please write to one of the KBW entities: Keefe, Bruyette &Woods Research Department at the following address: 787 7th Avenue, 4th Floor, New York, NY 10019. The Compliance Officer,Keefe, Bruyette and Woods Limited, 7th Floor, One Broadgate, London EC2m 2QS. The Compliance Officer, Keefe, Bruyette andWoods Asia Limited, 3101, 31/F Central Plaza, 18 Harbour Road, Wanchai, Hong Kong. Or visit our website athttp://www.kbw.com/research/disclosures. KBW has arrangements in place to manage conflicts of interest including information barriersbetween the Research Department and certain other business groups. As a result, KBW does not disclose certain client relationships with,or compensation received from, such companies in its research reports.

Distribution of Ratings/IB ServicesKBW

*IB Serv./Past 12 Mos.

Rating Count Percent Count Percent

Outperform [BUY] 197 29.58 55 27.92Market Perform [HOLD] 324 48.65 78 24.07Underperform [SELL] 61 9.16 9 14.75Restricted [RES] 0 0.00 0 0.00Suspended [SP] 84 12.61 17 20.24Covered -Not Rated [CNR] 2 0.30 1 50.00

* KBW maintains separate research departments; however, the above chart, "Distribution of Ratings/IBServices," reflects combined information related to the distribution of research ratings and the receipt ofinvestment banking fees globally.

Explanation of Ratings: KBW Research Department provides three core ratings: Outperform, Market Perform and Underperform, andthree ancillary ratings: Suspended, Restricted, and Covered - Not Rated. For purposes of New York Stock Exchange Rule 472 andFINRA Rule 2711, Outperform is classified as a Buy, Market Perform is classified as a Hold, and Underperform is classified as a Sell.Suspended indicates that KBW’s investment rating and/or target price have been temporarily suspended due to applicable regulationsand/or KBW policies. Restricted indicates that KBW is precluded from providing an investment rating or price target due to the firm'srole in connection with a merger or other strategic financial transaction. Covered - Not Rated indicates that KBW is not providing aninvestment rating and/or price target due to the lack of publicly available information and/or its inability to adequately quantify thepublicly available information to sufficiently produce such metrics.

North American Stocks are rated based on an absolute rate of return (percentage price change plus dividend yield).Outperform

Please refer to important disclosures and analyst certification information on pages 22 - 25. 22

16 July 2012

represents a total rate of return of 15% or greater. Market Perform represents a total rate of return in a range between -5% and+15%.Underperform represents a total rate of return at or below -5%.

European and Asian Stocks are rated based on the share price upside to target price relative to the relevant sector index performance ona 12-month horizon. Outperform rated stocks have a greater than 10 percentage point (“pp”) relative performance versus the sector,Market Perform rated stocks between +10pp to -10pp relative performance versus the sector, and Underperform rated stocks a lower than10pp relative performance versus the sector. The 12-month price target may be determined by the stock’s fundamentally driven fair valueand/or other factors (e.g., takeover premium or illiquidity discount).

KBW Model Portfolio: "Model Portfolio Buy" - Companies placed on this list are expected to generate a total rate of return (percentageprice change plus dividend yield) of 10% or more over the next 3 to 6 months.