lev finance cov lite article july 2014

TRANSCRIPT

Leveraged Finance:

Covenant-Lite Issuance Casts A CloudOver Future Default Levels

Primary Credit Analysts:

John W Sweeney, New York (1) 212-438-7154; [email protected]

Kenneth J Fleming, New York (1) 212-438-1490; [email protected]

David P Wood, New York (1) 212-438-7409; [email protected]

David C Tesher, New York (1) 212-438-2618; [email protected]

Table Of Contents

Covenant-Lite Issuance Is Swelling, Especially 'B' Rated Loans

Default And Recovery Data On Covenant-Lite Loans

Covenant-Lite Borrowing Is More Prevalent In Certain Industry Sectors

Than Others

How Standard & Poor's Assesses Covenant-Lite Risk

Positive Market Momentum May Be Veiling Credit Risk--The Surge In 'B'

Rated Loans Is The Major Concern

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 1

1357219 | 300614293

Leveraged Finance:

Covenant-Lite Issuance Casts A Cloud OverFuture Default Levels

With the current hyper-liquidity in the capital markets, largely due to central bank "cheap-money" policies, and

investors' unquenchable thirst for yield, the issuance of covenant-lite first-lien loans, which lack financial maintenance

covenants, has boomed in 2013 and thus far in 2014. Standard & Poor's Ratings Services is concerned that the sizable

amount of first-lien covenant-lite loans now outstanding, particularly those rated in the 'B' category, along with rapid

growth in traditional 'B' first-lien loan issuance, could result in elevated refinancing risk and/or a spike in defaults in

the event of a future liquidity crisis. (Watch the related CreditMatters TV segment titled, "Booming ‘B’-Rated

Covenant-Lite Issuance Heightens Restructuring And Default Risk," dated July 15, 2014.)

Overview

• There has been a proliferation of covenant-lite corporate loan borrowing in the U.S. over the past 18 months, a

majority of which Standard & Poor's rates in the 'B' category.

• General market stability and positive economic conditions are masking the credit risk associated with 'B' rated

covenant-lite and traditional loans.

• In the event of a significant financial market liquidity crunch, default rates for covenant-lite borrowers could

spike well above the levels seen during the 2008-2009 financial crisis.

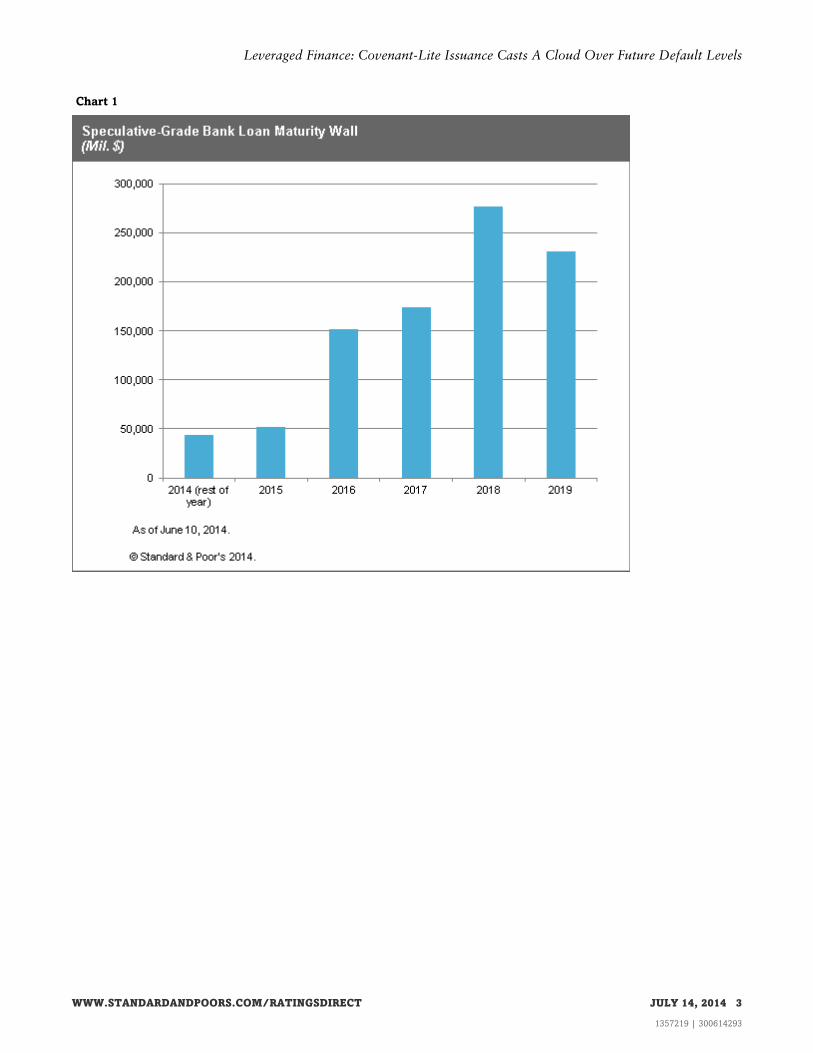

Loan refinancing risk currently peaks in the 2017-2019 period (see chart 1). If a liquidity crunch were to occur in any of

these years, banks and investors would become more risk averse as issuer performance and liquidity deteriorates.

Refinancing risk could then amplify for borrowers of maturing loans without financial maintenance covenants, as these

borrowers could become less attractive to a more limited and discerning lender base. Rapid credit erosion could then

occur for companies unable to satisfy their new funding requirements. In our opinion, lenders should not interpret

historical covenant-lite default levels from the last downturn--or currently subdued default rates--as a sign of what the

future holds, and should expect default rates for 'B' rated loans--particularly 'B' rated covenant-lite loans--to increase

during the next downturn.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 2

1357219 | 300614293

Chart 1

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 3

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

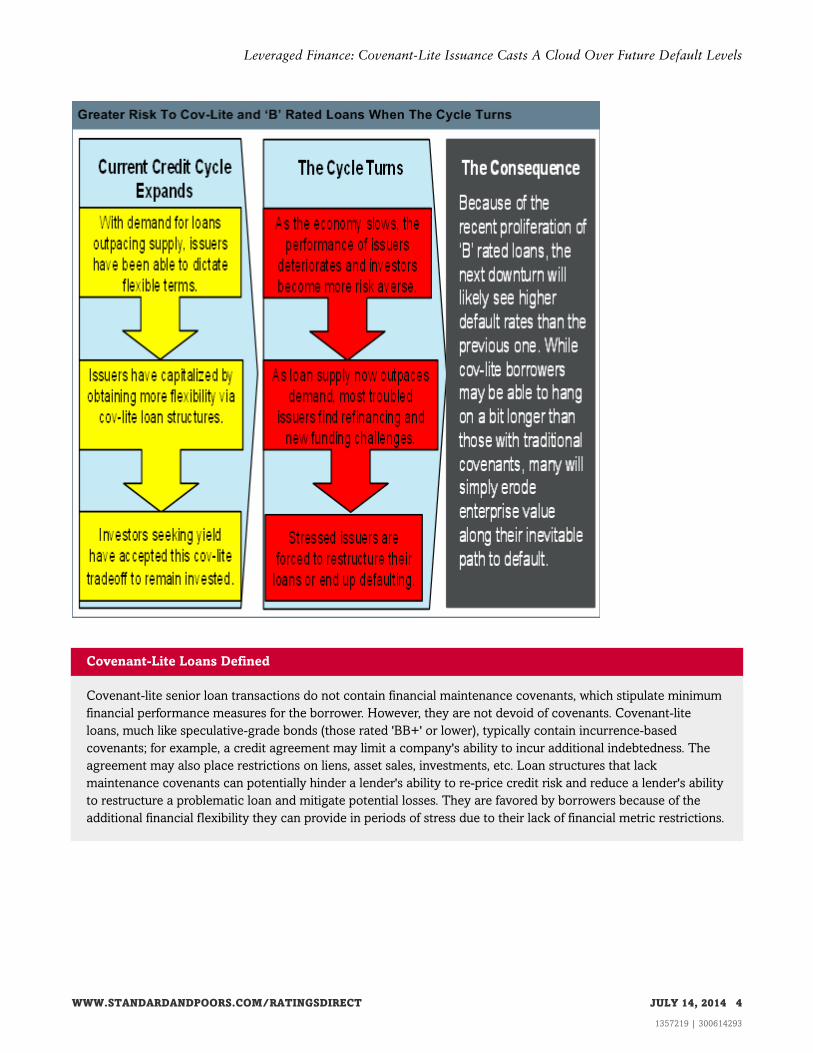

Covenant-Lite Loans Defined

Covenant-lite senior loan transactions do not contain financial maintenance covenants, which stipulate minimum

financial performance measures for the borrower. However, they are not devoid of covenants. Covenant-lite

loans, much like speculative-grade bonds (those rated 'BB+' or lower), typically contain incurrence-based

covenants; for example, a credit agreement may limit a company's ability to incur additional indebtedness. The

agreement may also place restrictions on liens, asset sales, investments, etc. Loan structures that lack

maintenance covenants can potentially hinder a lender's ability to re-price credit risk and reduce a lender's ability

to restructure a problematic loan and mitigate potential losses. They are favored by borrowers because of the

additional financial flexibility they can provide in periods of stress due to their lack of financial metric restrictions.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 4

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

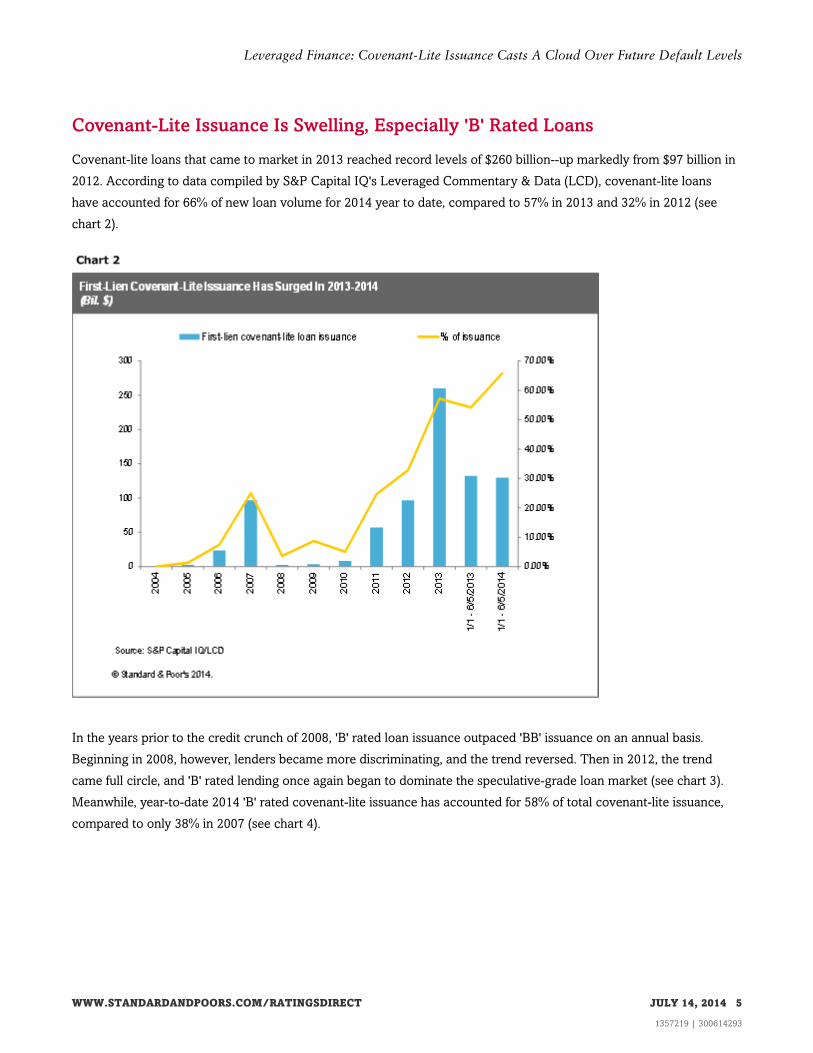

Covenant-Lite Issuance Is Swelling, Especially 'B' Rated Loans

Covenant-lite loans that came to market in 2013 reached record levels of $260 billion--up markedly from $97 billion in

2012. According to data compiled by S&P Capital IQ's Leveraged Commentary & Data (LCD), covenant-lite loans

have accounted for 66% of new loan volume for 2014 year to date, compared to 57% in 2013 and 32% in 2012 (see

chart 2).

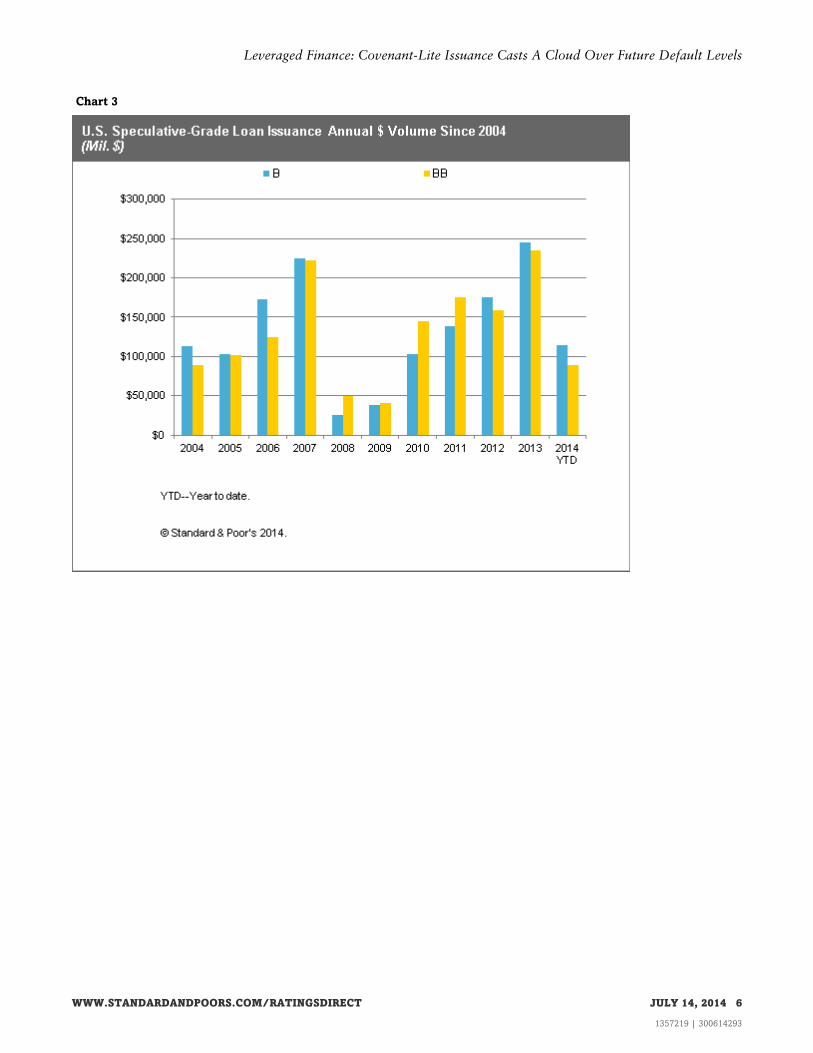

In the years prior to the credit crunch of 2008, 'B' rated loan issuance outpaced 'BB' issuance on an annual basis.

Beginning in 2008, however, lenders became more discriminating, and the trend reversed. Then in 2012, the trend

came full circle, and 'B' rated lending once again began to dominate the speculative-grade loan market (see chart 3).

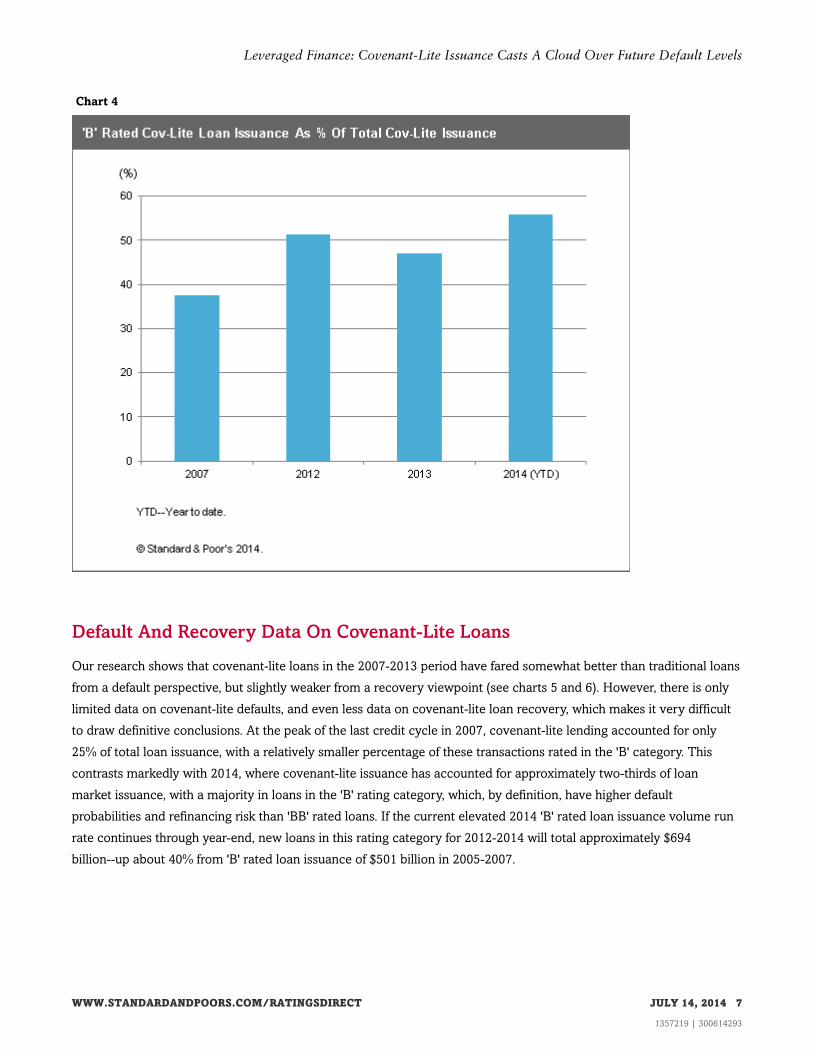

Meanwhile, year-to-date 2014 'B' rated covenant-lite issuance has accounted for 58% of total covenant-lite issuance,

compared to only 38% in 2007 (see chart 4).

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 5

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

Chart 3

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 6

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

Chart 4

Default And Recovery Data On Covenant-Lite Loans

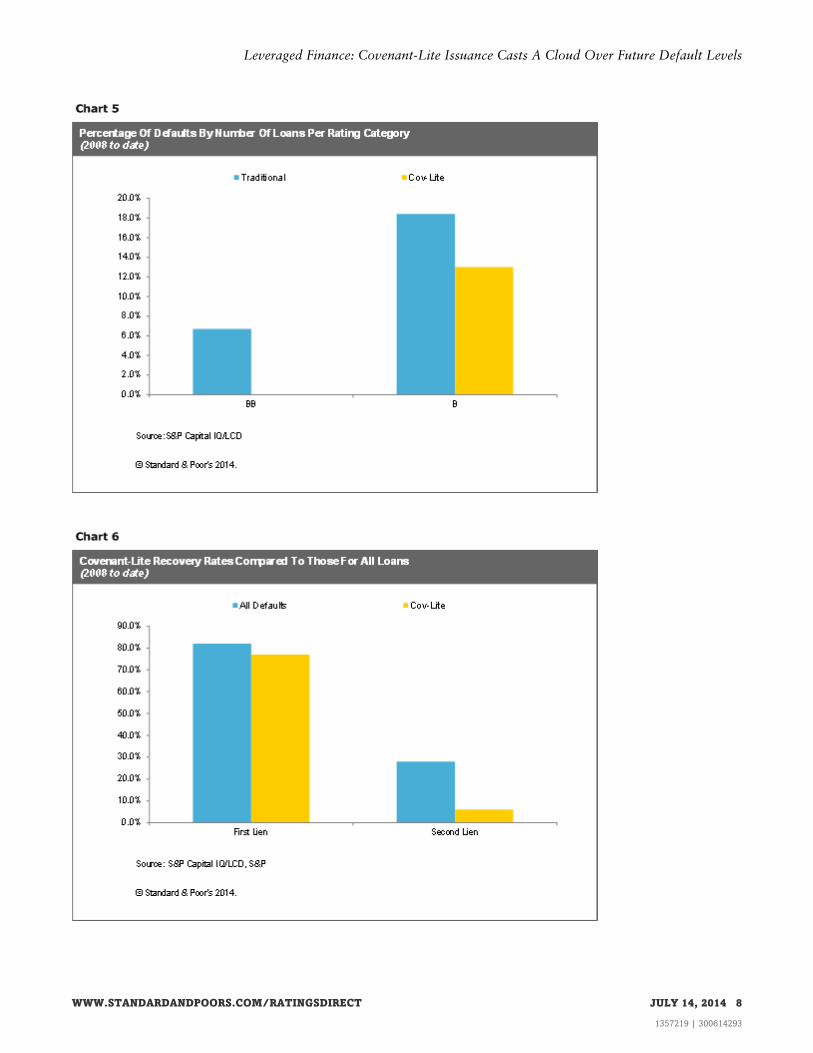

Our research shows that covenant-lite loans in the 2007-2013 period have fared somewhat better than traditional loans

from a default perspective, but slightly weaker from a recovery viewpoint (see charts 5 and 6). However, there is only

limited data on covenant-lite defaults, and even less data on covenant-lite loan recovery, which makes it very difficult

to draw definitive conclusions. At the peak of the last credit cycle in 2007, covenant-lite lending accounted for only

25% of total loan issuance, with a relatively smaller percentage of these transactions rated in the 'B' category. This

contrasts markedly with 2014, where covenant-lite issuance has accounted for approximately two-thirds of loan

market issuance, with a majority in loans in the 'B' rating category, which, by definition, have higher default

probabilities and refinancing risk than 'BB' rated loans. If the current elevated 2014 'B' rated loan issuance volume run

rate continues through year-end, new loans in this rating category for 2012-2014 will total approximately $694

billion--up about 40% from 'B' rated loan issuance of $501 billion in 2005-2007.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 7

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 8

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

Covenant-Lite Borrowing Is More Prevalent In Certain Industry Sectors ThanOthers

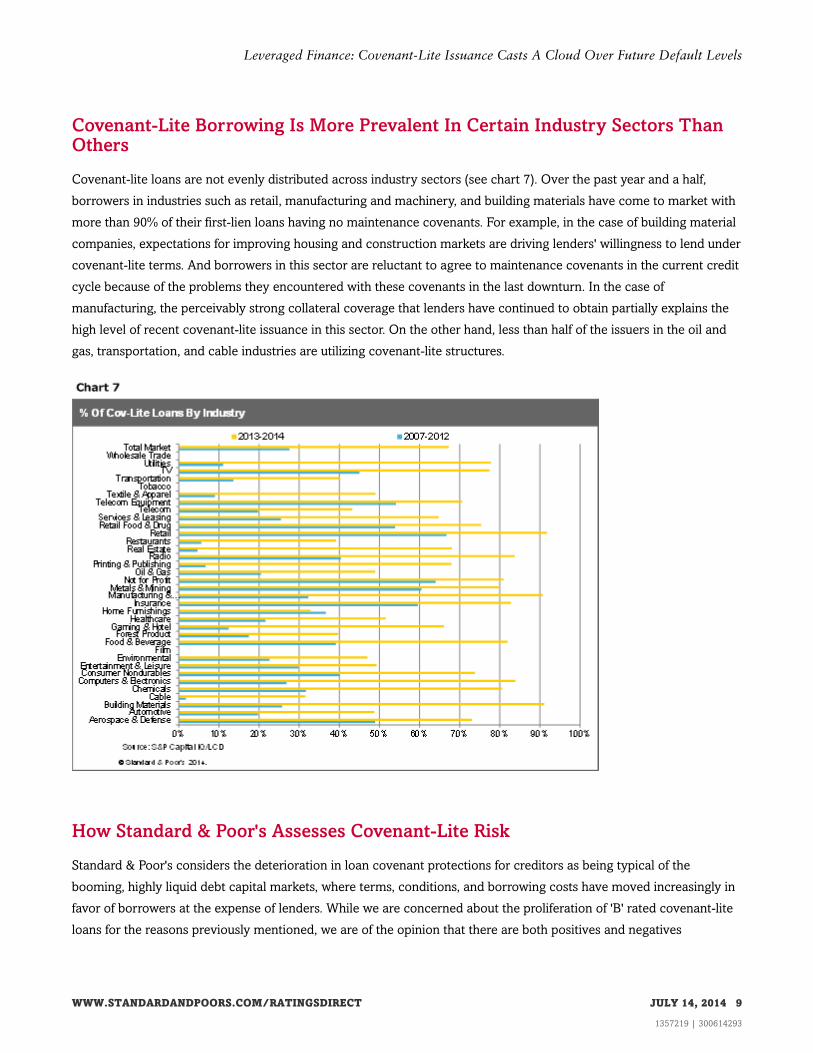

Covenant-lite loans are not evenly distributed across industry sectors (see chart 7). Over the past year and a half,

borrowers in industries such as retail, manufacturing and machinery, and building materials have come to market with

more than 90% of their first-lien loans having no maintenance covenants. For example, in the case of building material

companies, expectations for improving housing and construction markets are driving lenders' willingness to lend under

covenant-lite terms. And borrowers in this sector are reluctant to agree to maintenance covenants in the current credit

cycle because of the problems they encountered with these covenants in the last downturn. In the case of

manufacturing, the perceivably strong collateral coverage that lenders have continued to obtain partially explains the

high level of recent covenant-lite issuance in this sector. On the other hand, less than half of the issuers in the oil and

gas, transportation, and cable industries are utilizing covenant-lite structures.

How Standard & Poor's Assesses Covenant-Lite Risk

Standard & Poor's considers the deterioration in loan covenant protections for creditors as being typical of the

booming, highly liquid debt capital markets, where terms, conditions, and borrowing costs have moved increasingly in

favor of borrowers at the expense of lenders. While we are concerned about the proliferation of 'B' rated covenant-lite

loans for the reasons previously mentioned, we are of the opinion that there are both positives and negatives

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 9

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

associated with this type of transaction from a credit risk perspective at the individual loan and issuer level. Hence, we

do not view the structure as inherently good or bad.

In our view, the absence of maintenance financial covenants can provide a company with additional financial flexibility

(i.e., liquidity) in times of stress, precluding lenders from having the ability to accelerate a loan via a technical

event-of-default provision. This added liquidity can provide a lifeline for an issuer in a period of stress, ultimately

enabling a company to recover without defaulting or needing to renegotiate terms, conditions, and pricing. That said,

the lack of maintenance covenants can also give aggressive financial management teams and sponsors more latitude

to pursue shareholder-friendly and other actions that may ultimately hurt their credit profiles. Instead of saving a

company, a covenant-lite loan structure, under certain circumstances, could simply delay an inevitable default--and

severely undermine a company's enterprise value along the way, impairing lenders' recovery prospects.

From an analytical perspective, Standard & Poor's considers maintenance covenants in two specific areas of our

corporate and recovery ratings. First, when financial triggers are embedded in a debt structure (i.e., in a "traditional"

non-covenant-lite transaction), our forward looking projection analysis captures these triggers via our liquidity

analysis. Second, the potential for aggressive management from a financial sponsor, which is further increased with

covenant-lite transactions, is an explicit factor we incorporate into our forward-looking speculative-grade corporate

credit ratings.

As part of our recovery analysis, we simulate a hypothetical path to default for the borrower. We assume that

borrowers with maintenance covenants in their loan agreements will trigger these covenants as their financial position

weakens and they approach insolvency. Such a scenario typically results in an amendment/waiver process where the

bank syndicate subsequently demands higher interest margin compensation to offset the greater default risk to which

they are now perceivably exposed. The increase in interest expense implies that a company will default at a slightly

higher level of profitability than it would have otherwise attained (because it will likely default sooner than it would

have minus the maintenance covenants), resulting in less business value deterioration and, thus, relatively greater

recovery prospects for lenders.

In our recovery study published in January 2013 and updated in February of this year (see "Standard & Poor's U.S.

Recovery Rating Performance--A Five Year Study," published Jan. 29, 2013, and "U.S. Recovery Rating Performance

Study: 2007-2013," Feb. 25, 2014), we compared the default and recovery performance of covenant-lite facilities to

those of our entire universe of rated speculative-grade corporate debt. From 2007 through 2013, we found that

covenant-lite loans have slightly lower default rates, but that recovery levels were not quite as robust. When defaults

for covenant-lite loans did ultimately occur, however, enterprise values experienced slightly greater erosion than

secured loans with traditional maintenance covenants, thereby reducing lender recoveries.

Positive Market Momentum May Be Veiling Credit Risk--The Surge In 'B' RatedLoans Is The Major Concern

Although the absence of maintenance financial covenants can help a company by providing it with additional financial

flexibility, covenant-lite loan structures increase the likelihood that financial managers/sponsors will take aggressive

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 10

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

actions that could hurt the borrower's credit profile. Standard & Poor's incorporates this risk into its forward-looking

financial policy assessment of sponsor-owned and highly leveraged corporate entities. Further, when defaults do occur,

we'd expect the financials of companies without maintenance covenants to deteriorate somewhat more than those

with traditional financial covenants, which would likely modestly reduce overall debt recovery rates.

Currently favorable economic and market conditions are masking the risks associated with the spate of covenant-lite

and traditional loans--particularly the 'B' rated ones--recently coming to market. It is our view that if a marked liquidity

crisis were to occur, preventing covenant-lite and traditional loan structure borrowers from acquiring new funding, the

default rate for bank loans, as well as the dollar value of defaults, would rise--possibly significantly--from the levels

experienced in 2008-2009.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 11

1357219 | 300614293

Leveraged Finance: Covenant-Lite Issuance Casts A Cloud Over Future Default Levels

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2015 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JULY 14, 2014 12

1357219 | 300614293