lessons from china’s pension reform experiences -...

TRANSCRIPT

1

Lessons from China’s Pension Reform Experiences

Mark C. Dorfman

World Bank Pensions Core CourseNovember 13, 2009

Organization1. Background - History

2. Overall Structure, Challenges

3. Urban Enterprise Scheme

• History

• Structure

• Demographics, Coverage and Financial flows

• Challenges

4. Public Sector Units and Civil Servants

• History, Benefits, Challenges

5. Rural Pension Systems

• Structure

• Challenges

• Reforms taken and being implemented

6. Treatment of Migrants

7. Voluntary Savings Arrangements

8. Conclusions 2

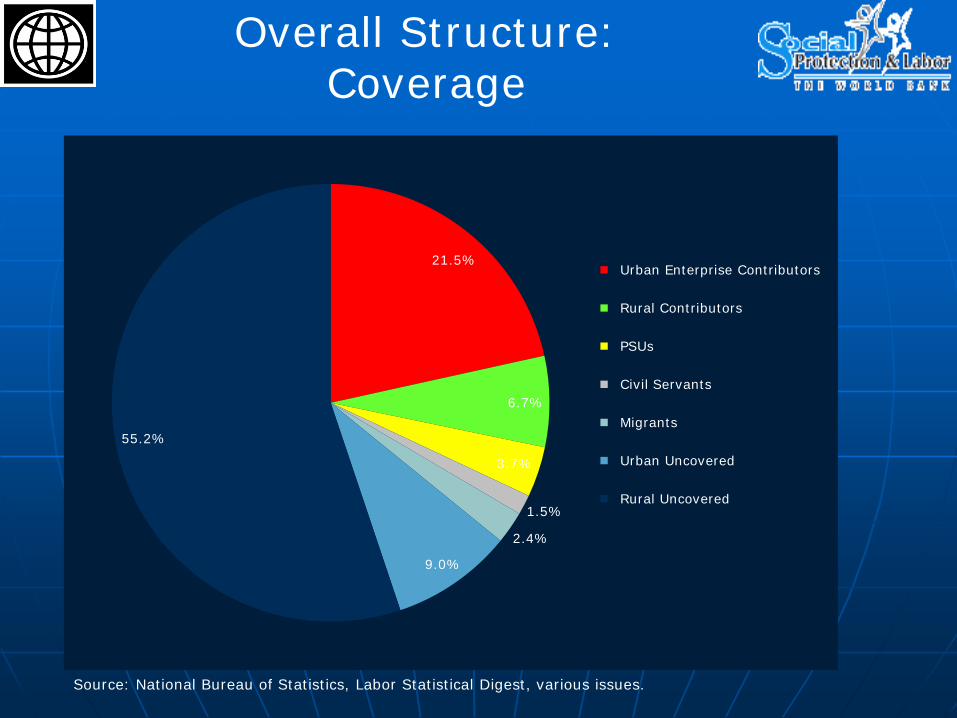

Overall Structure: Coverage

21.5%

6.7%

3.7%

1.5%

2.4%

9.0%

55.2%

Urban Enterprise Contributors

Rural Contributors

PSUs

Civil Servants

Migrants

Urban Uncovered

Rural Uncovered

Source: National Bureau of Statistics, Labor Statistical Digest, various issues.

Overall Structure: Urban Provisions

Overall Challenges

• Aging

• Economic Adjustment

• Coverage

• Fragmentation

• Lack of portability

• Legacy burden and financing strategy

• Decentralized fiscal and administrative structure

Aging Population (1)

China: Female and Male Age Groups, 1995

80000 60000 40000 20000 0 20000 40000 60000 80000

5-y

ear

ag

e g

rou

ps:

0-7

5+

Females and Males, in '000s

China: Female and Male Age Groups, 2030

80000 60000 40000 20000 0 20000 40000 60000 80000

5-y

ear

ag

e g

rou

ps:

0-7

5+

Females and Males, in '000s

Source, Sin, 2005.

• One Chile Policy and the 1-2-4 Family structure• Increases in life expectancy• Changes in the family structure

Aging Population (2)

China’s Population Will Age Rapidly After 2010

0

200

400

600

800

1000

1200

1990 1995 2000 2010 2020 2030 2050

Year

Million

0

5

10

15

20

25

30

35

%

1. Population in age group: 15-64(in millions)

2. Population in age group 65 and above (in millions)

3. Dependency ratio(%) (2)/(1)

Source: Sin, 2005

11/19/2009 8

Urban Enterprise Pensions History (1)

1951 Est. enterprise-based pay-as-you-go defined-benefit mandatory public pensions.

Iron Rice Bowl - pensions, health, employment, housing, maternity, work injury, basic living support

1960’sDevolution of pension management to enterprise (SOE) level

1986 Beg. pilot programs in municipal pooling

1992 Beg. pilot programs in individual accounts

1995 National mandate for choice of individual accounts and defined benefits

11/19/2009 9

Background – Urban History (2)

1997 National mandate and parameters for three-tiered benefit structure - basic benefit, individual account, supplementary pension and transition arrangements

1999 Coverage extension to non-SOE enterprises; central sector funds decentralized

2001 Liaoning Pilot Program,2001 Est. National Social Security (Reserve) Fund2004 Initiation of “Enterprise Annuity” Occupational

Pension Scheme2005 Parametric adjustments to Urban Enterprise

Scheme2009 Issuance of Draft Social Insurance Law for

Comment

11/19/2009 10

Urban Enterprise SchemeCurrent Structure (1)

Benefits (Phased in from 1996 to 2035 with different benefit formula for “old men”, “middle men” and “young men”):

Pillar 1a – 20% of ½ individual and ½ regional average wage (changed to 1% accrual rate for most provinces -2005)

Pillar 1b – Monthly Lifetime Annuity = Individual Account Accumulation / Annuity Factor

Transition Benefit - Defined Benefit accrual rate 1-1.4%/year for service prior to 1996

11/19/2009 11

Urban Enterprise Scheme Current Structure (2)

Qualifying Conditions

Retirement Age: • 50 for women workers

• 55 for women managers

• 60 for men

• 5 years early retirement for enterprises in transition + hazardous professions

• life expectancy at est. women retirement age of 50: 77; men est. retirement age of 56 for men: Age 76

Vesting: 15 years

11/19/2009 12

Urban Enterprise Scheme Current Structure (3)

Contribution Rates: Vary by Province and city - Employer contributions

20-23% of covered wages Employee contributions generally 8% Total pension contribution rates: 28-31% Wages subject to contributions: 60%-300% of

regional average covered wage.

Account Administration:

At the county and city level (having migrated from the enterprise level in most venues)

In select cities, with horizontal links to health, unemployment insurance, maternity and work injury

11/19/2009 13

Recent Demographics of the Urban Enterprise Scheme

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Millions

Contributors Pensioners System Dependency Ratio

Sources: National Bureau of Statistics, Labor Statistical Digest

11/19/2009 14

Urban Enterprise Scheme –Coverage

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Covered Employees Urban Labor Force Retirees

Sources: National Bureau of Statistics, Labor Statistical Digest

Coverage low but increasing (with growth and changes in economic composition.)

Pension System CoverageRelationship between Coverage and Income per

Capita

15

Kyrgyz Rep.

Moldova

Vietnam

India

Georgia

China

ArmeniaUkraine

Albania

Bosnia

Macedonia

Brazil

Serbia

Kazakhstan

Romania

Mexico

Russia

Poland

Croatia

Latvia

Lithuania

Hungary

Slovak Rep.

Estonia

Czech Rep.

JapanGermany

y = 0.2466ln(x) - 1.7331R² = 0.7764

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

- 10,000 20,000 30,000 40,000 50,000 60,000

Co

vera

ge (

acti

ve m

em

be

rs /

lab

or

forc

e

)

Income per Capita (PPP)

Source: World Economic Indicators.

11/19/2009 16

Urban Enterprise SchemeRecent Financial Flows (% GDP)

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Percen

t o

f G

DP

Revenues Disbursements Reserves

Sources: National Bureau of Statistics, Labor Statistical Digest

Although system revenues have been greater than disbursements, there are substantial regional differences and many individual accounts have been “empty”.

11/19/2009 17

Urban Enterprise SchemeRecent Growth in Subsidies

0

200

400

600

800

1000

1200

1400

2003 2004 2005 2006 2007

Million Yuan/Year Provincial/Local Government

Central Government

Source: Sin, 2008.

11/19/2009 18

Urban Enterprise Scheme – Individual Account Rate of Interest vs. Wages

Income replacement from individual accounts has dwindled as returns have been dwarfed in comparison to wage growth.

Marginal replacement rate decreased from target of 58%.

0

200

400

600

800

1000

1200

1400

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

In

dex (

19

90

= 1

00

)

Inflation Wage Growth Growth of 1-Year Term Deposits

Source: Sin, 2008.

11/19/2009 19

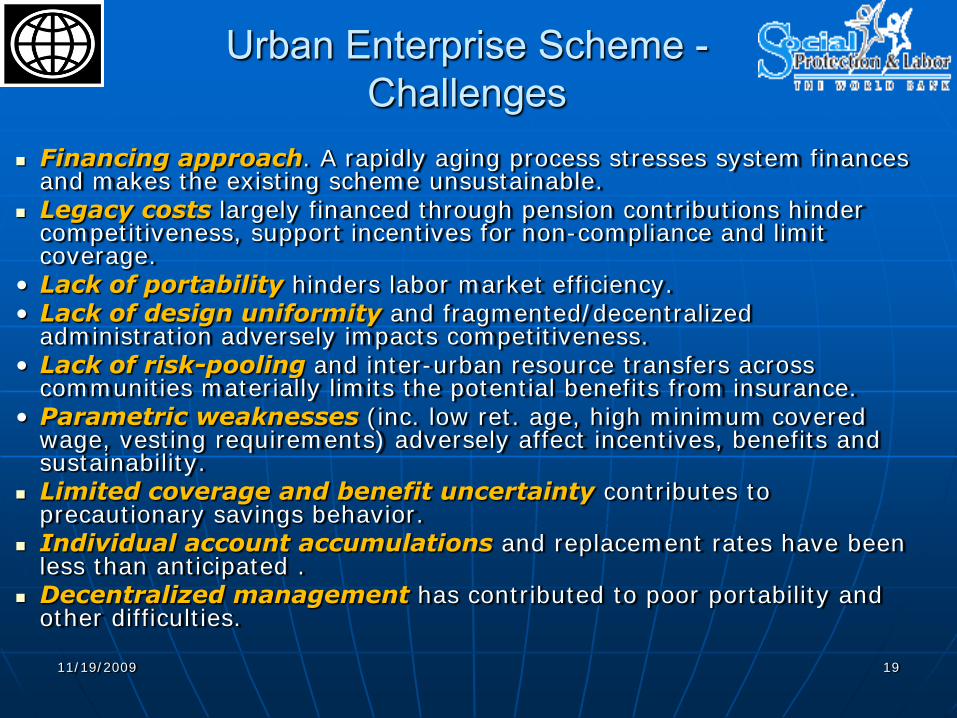

Urban Enterprise Scheme -Challenges

Financing approach. A rapidly aging process stresses system finances and makes the existing scheme unsustainable.

Legacy costs largely financed through pension contributions hinder competitiveness, support incentives for non-compliance and limit coverage.

• Lack of portability hinders labor market efficiency.• Lack of design uniformity and fragmented/decentralized

administration adversely impacts competitiveness. • Lack of risk-pooling and inter-urban resource transfers across

communities materially limits the potential benefits from insurance. • Parametric weaknesses (inc. low ret. age, high minimum covered

wage, vesting requirements) adversely affect incentives, benefits and sustainability.

Limited coverage and benefit uncertainty contributes to precautionary savings behavior.

Individual account accumulations and replacement rates have been less than anticipated .

Decentralized management has contributed to poor portability and other difficulties.

11/19/2009 20

Urban Enterprise SchemeLessons for Other Countries

The authorities enacted pro-active design reforms in the early 1990s aimed at remedying many of the weaknesses of the earlier defined-benefit, enterprise-centered approach.

Wage growth has dwarfed returns on individual accounts due to special circumstances of labor and financial markets.

The authorities were attentive to performance weaknesses, enacting parametric refinements in 2001 and 2005.

The pension system has been able to support the economic restructuring of the 1990s but financing legacy costs have been a burden to enterprises and workers alike, contributing to informality.

The central Government adopted a prudent financing strategy increasing Government subsidies in accordance with fiscal capacity.

The authorities have adopted a long-term perspective through the establishment of the National Social Security Fund to pre-fund future pension liabilities.

Civil Servants and Public Sector Units Pensions - History

21

1992 Local governments encouraged to experiment different schemes. Pilots in 6 provinces

1997 Experiments by 1,700 county governments in 28 provinces + 19 provincial governments. Some employees in fully self-funded PSUs required to join the urban enterprise system. Employee would contribute 2% to 4% of wages to individual accounts. Pension payments remained the responsibility of each PSU.

2008 New PSU trials introduced - objective to bring the PSU pension system more in line with the current urban enterprise pension system.

2009 February 2009 five provinces selected by the government to implement the pilot.

Civil Servants and Public Sector Units Pensions – Replacement Rates

Defined-benefit schemes based on the final salary and length of service.

Accrual rate is front-loaded

Retirement age. 60 for men and 55 for women.

22

Replacement Rates

Civil service PSU

Years %

≤ 10 40 50

> 10 and ≤ 20 60 70

> 20 and ≤ 30 75 80

>30 and ≤ 35 82 85

>35 and ≤ 40 88 90

Civil Servants and Public Sector Unit Pensions

23

40

50

60

70

80

90

100

1101

99

0

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

government replacement enterprise replacement

Average pension relative to average earnings: government and non-government employees

Source: Hu, Yu Wei, 2009.

Civil Servants and Public Sector Unit Pensions

24

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0

5

10

15

20

25

30

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

relative to wage bill

relative to GDP

Cost of civil service and PSU pensions

Source: Hu, Yu Wei, 2009.

Civil Servants and Public Sector Unit Pensions - Challenges

25

Portability and labor mobility. Lack of portability of rights to the urban enterprise scheme forces individuals into sub-optimal labor market decisions and impacts productivity.

Generosity and modality for promised income

replacement. Replacement rates much higher than for the urban scheme suggesting that integration with the urban enterprise scheme requires establishment of a top-up benefit as through an supplemental occupational annuity plan.

Financing. Efforts to integrate PSUs with the urban enterprise scheme are limited by very limited historic contributions.

11/19/2009 26

Rural Pensions (1)History

1986 Ministry of Civil Affairs (MOCA) Pilots in Beijing and Shanxi

1991 MOCA est. as lead for rural pensions1992 MOCA Basic Scheme for Rural Pensions at

County Level (+1995 Policy Document)1998 Rural Pensions in 31 Provinces – 80 million

participants1999 State Council Change in Policy leading in

sharp decline in coverage (60 million –2001, 55 million in 1900 counties by 2007)

2003 Renewal Phase initiated – social pooling +IA; flat benefit + IA; IA only; various incentives

2009 Est. of Rural Pension Pilot Program

11/19/2009 27

Rural Pensions (2)Coverage

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Percent of Rural

Labor Force

Rural pension converage (%)

Sources: National Bureau of Statistics, Labor Statistical Digest

11/19/2009 28

Rural Pensions (3)

State Council Document 32 – June 2009

Contributions: Contribution at 5 levels (100-500 Yuan/month) Minimum match of 35 Yuan/month (locally financed)Accumulations Based on 1 year time deposit rate Fund management Benefit: Annuitized benefit from account accumulation at age 60 (+

application of annuity factor) Flat benefit centrally financed of 55/month Yuan in 2009 termsQualifying conditions and transition provisions Age 60 (men and women) 15 years of service Those with less than 15 years subject to Family Binding

requirementTarget Coverage: 10% of counties in 1st stage; 100% by 2020.

11/19/2009 29

Rural Pensions (4)

Challenges

Aging Coverage Precautionary savings (reducing current

consumption) Elderly poverty prevalence Mobility and lack of portability Fragmentation – lack of integration of existing

schemes (including lack of support to migrants)

11/19/2009 30

Rural Pensions (5)

Lessons

Design experience and results. Chinese have experimented with rural pensions savings vehicles and flat defined-benefit provisions since 1992. Although credibility may have been affected by promotion followed by removal and reintroduction, the experience informed the latest policy design.

Financing. The authorities have experimented with different subsidy mechanisms, ex-ante and ex-post and have collective experience on the effects of different approaches adopted. Experience with financing from different levels (national, provincial, municipal) also instructive.

Impressive coverage of rural areas. Overall coverage levels achieved in the 1990s were substantial when compared to rural coverage benchmarks in other developing countries. The modalities designed to motivating rural residents to contribute towards retirement are also noteworthy.

11/19/2009 31

Migrants’ Pensions (1)

Modalities and Coverage “Hukou” system had deterred migration. Growing number of migrants in mid-2000s, est.

130 – 150 million workers (of an Econ Active Population of 786 million)

Varying migration duration and patterns (rural-rural, rural-urban)

Urban Ent. Scheme costly for migrants (28-31% cont. rate, min. wage subject to contributions: 60% of the regional average wage)

Urban Ent. Benefit accruals not portable. Est. 24 million migrant workers participating in

urban enterprise schemes (2008).

11/19/2009 32

Migrants (2)

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

2006 2007 2008

Contributors Est. Total

Sources: National Bureau of Statistics, Labor Statistical Digest

11/19/2009 33

Migrants (3)

Pilot Reform Program - Policy Blueprint -2009

Objective to achieve large coverage, transferability, portability and low contributions.

Uses existing urban enterprise architecture (social pooling + ind. Accounts)

Yet lower contribution rates (enterprises 12%, individuals 4-8%).

15 year vesting (as urban scheme)

Target for local management but national information system

11/19/2009 34

Voluntary Savings Arrangements (1)

History

Individual long-term savings products –limited use and low returns.

1997 Urban enterprise reform anticipated voluntary savings - but high urban contribution rates (28-31%) and returns lower than wage growth discouraged voluntary pension savings

2004 introduction of the Enterprise Annuity – a framework for employer sponsored voluntary pension savings arrangements.

11/19/2009 35

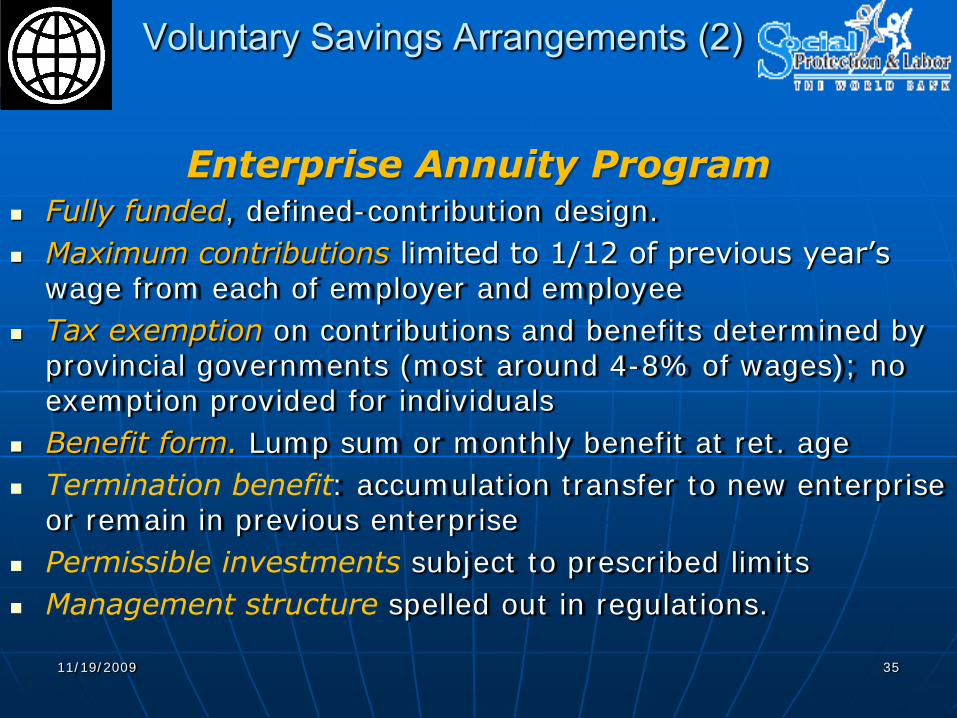

Voluntary Savings Arrangements (2)

Enterprise Annuity Program Fully funded, defined-contribution design.

Maximum contributions limited to 1/12 of previous year’s wage from each of employer and employee

Tax exemption on contributions and benefits determined by provincial governments (most around 4-8% of wages); no exemption provided for individuals

Benefit form. Lump sum or monthly benefit at ret. age

Termination benefit: accumulation transfer to new enterprise or remain in previous enterprise

Permissible investments subject to prescribed limits

Management structure spelled out in regulations.

11/19/2009 36

Voluntary Savings Arrangements (3)

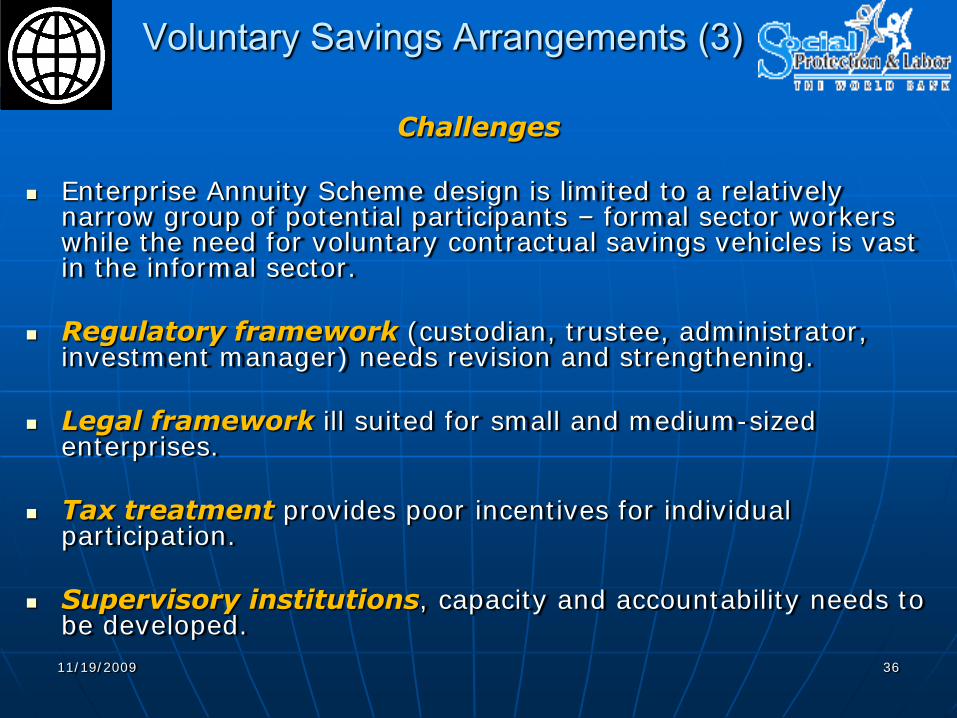

Challenges

Enterprise Annuity Scheme design is limited to a relatively narrow group of potential participants – formal sector workers while the need for voluntary contractual savings vehicles is vast in the informal sector.

Regulatory framework (custodian, trustee, administrator, investment manager) needs revision and strengthening.

Legal framework ill suited for small and medium-sized enterprises.

Tax treatment provides poor incentives for individual participation.

Supervisory institutions, capacity and accountability needs to be developed.

11/19/2009 37

Conclusions In the face of strong headwinds of aging, and economic adjustment,

the Authorities have been proactive in enacting constructive pension reforms since the 1990s. They have also been receptive to parametric modification as conditions and needs change and experience suggests.

Experience with rural pensions savings and subsidy schemes provide useful insights into current designs being considered.

The principles guiding reform articulated by the authorities (broad coverage, protect at a basic level, multilayered (diversified), sustainable and flexible (for rural pensions) are highly consistent with the Bank’s thinking of the guiding principles for pension reform in China.

For the future, the imperative of an integrated pension framework across professions, regions and linking work in urban and rural areas is essential to long-term growth, competitiveness and old age income protection. Such a system should satisfy the principles indicated by providing multiple instruments supporting the core objective.