legacy of the downturn - alfi.lu · filf cap ita l f parameters and investor board iable investing...

TRANSCRIPT

LEGACY OF THE DO

ALFI European Alternative InvesALFI European Alternative InvesReal Estate WorkshopLuxemburg22 November 2011

Lonneke LöwikLonneke LöwikINREV, Director Research and M

OWNTURN

stment Funds Conferencestment Funds Conference

Market Information

AGENDA

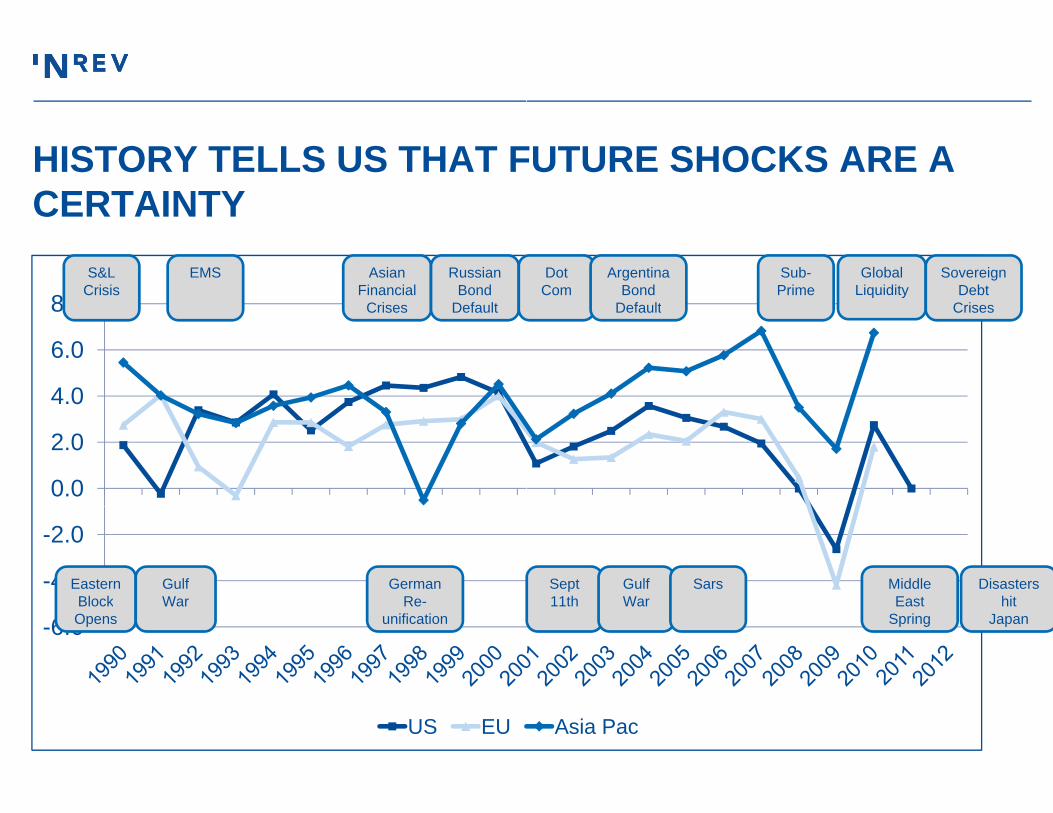

– The only certainty is change

HISTORY TELLS US THAT FCERTAINTY

8 0

CERTAINTYS&L

CrisisEMS Asian

Financial Crises

Russian Bond

Default

4.0

6.0

8.0 Crises Default

0.0

2.0

-4.0

-2.0

Eastern Block

Gulf War

German Re-

-6.0BlockOpens

War Reunification

US EU

FUTURE SHOCKS ARE A

DotCom

Argentina Bond

Default

Sub-Prime

Global Liquidity

Sovereign Debt

CrisesDefault Crises

Sept 11th

Gulf War

Sars Middle East

Disastershit11th War East

Springhit

Japan

Asia Pac

AGENDA

– The only certainty is change

– Trends in the principal drivers of no

‘knowable’ future:

– Economy

– Equity

– Debt

– Regulation

Wh t d it f th t t– What does it mean for the structure

on listed real estate point towards the

f li t d l t t ?e of non-listed real estate?

ECONOMY

SUMMARY OF ECONOMIC T

– Governance risk of Southern European Go e a ce s o Sout e u opeacountries dampens economic recovery

– European economy is set to under-perform growth in US and Asia into medium term

– Exogenous, cost-push inflation risks have escalated

– A fight for capital and higher real bond ratesrates

– Given rescue packages, many would argue current interest rate levels are artificially low

TRENDS AND RISKS

Real vs. nominal long term

12 014.016.0

ginterest rates 1975 to 2010

4 06.08.0

10.012.0

0.02.04.0

80 83 86 89 92 95 98 01 04 07 10

198

198

198

198

199

199

199

200

200

200

201

Real Bond Yield UK Nominal Bond Yield UK

Real Bond Yield US Nominal Bond Yield USSource: IMF, 2011; OECD, 2011

IMPLICATIONS FOR EUROP

– Re-channelling of inter-regional real estate capital away from Europe based on riskcapital away from Europe based on risk adjusted returns

– Over medium term, inter-regional capital flows from Asia to Europe may increase

– Fight for talent pool intensifies– A sharp rise in real bond rates may

decrease appetite for real estate as need for enhanced returns diminishesenhanced returns diminishes

– Ageing populations suggest shift in availability of fixed income capital

PEAN REAL ESTATE

Investment vs. Gross Savings 1980 - 2015f

23.025.027.0

17.019.021.0

15.017.0

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

f2

World InvestmentWorld Gross nat. savingsAdvanced Economies InvestmentAd d i G t iAdvanced economies Gross nat. savings

Source: IMF, Oct 2010

EQUITY CAPITAL

NON-LISTED REAL ESTATEON EVERY FRONT

70%Product range and investment alloca

ON EVERY FRONT

50%

60%

70%

30%

40%

50%

10%

20%

30%

0%

10%

Infrastructure Listed Real Estate

Real Estate Debt Funds

MezzanDebt

Investment Basket

E COMPETING FOR CAPITAL

ated

ine Real estate derivatives

Real estate hedge funds

Other None of the above

Investment madeSOURCE:INREV

INVESTORS ARE TAKING M

Preference for single country funds 2008 11

80%

100%funds 2008-11

60%

80%

20%

40%

0%

20%

2008 2009 2010 2011Investors Fund Managers

SOURCE: INREV Investment Intentions Survey 2008 - 2011

MORE CONTROL

100%JVs vs. non-listed by investor size

70%80%90%

100%

40%50%60%70%

10%20%30%40%

0%10%

Increase Cap alloc. to JVs

Increase Cap alloc.to non listed

Small Medium LargeSource: INREV Investment Intentions Survey 2011

LOWER EQUITY BASE FOR REAL ESTATE FUNDSREAL ESTATE FUNDS

Declining allocation to alternativesDeclining allocation to alternatives

Increasing regional competition f it lfor capital

Large investors shift d f i t tmode of investment

• DExtension of asset andasset and

product range

• CumulativCapital d lidecline

EUROPEAN NON-LISTED

• Structural and regulatory pressuress pressuress

• Relatively Europe lagging

• Preference for control

ilution of allocation to non-listed real estate

ve impact of increasing competition

DEBT CAPITAL

LOW AVAILABILITY AND EL

– Limited re-awakening of debt marke

– Marginal cost of debt remains eleva

– Big players in corporate real estate – RBS HBOS AIB Bank of Ireland– RBS, HBOS, AIB, Bank of Ireland,– German Lenders refocusing dome

– Reversal of financial globalisation mReversal of financial globalisation mand demand of capital

– New approach and expansionBNP P ib D bt f d– BNP Paribas, Debt funds

– Lack of diversity in funding sources

LEVATED COST

ets

ated with variance across markets

lending withdrawn or withdrawingWestimmo, Westimmo

estically (DG Hypo, HSH Nordbank)

may lead to mismatch between supplymay lead to mismatch between supply

s in Europe hinders progress

REGULATORY CHANGE

They’ve been downloading since

yesterdayyesterday

SUMMARY OF MAJOR REGU

• Basel III• Solvency IISolvency II• EMIR• AIFMD

Mark to Market

Accounting

Capital Adequacy

• Basel III• Solvency II• EMIR

q y

EMIR• AIFMD

ULATORY IMPACT

• Basel III• Solvency IISo e cy• EMIR

Higher gCost of Capital

Increase Reporting / Mgt Costs

• Basel III• Solvency II• AIFMD

Mgt Costs

AIFMD

IMPLICATIONS FOR NON-LI

– Lower availability and higher cost of debt capitalcapital

– Lower availability and / or higher return hurdles for equity capital

– Higher cost base for Fund ManagersHigher cost base for Fund Managers– Reporting– Capital Adequacy– Financial management

– EU pass-porting provides a remedy that points to industry consolidation and restructuringP l i ti f b t l t t f d– Polarisation of core, beta real estate funds and private equity, alpha funds

STED REAL ESTATE

Impact on Insurance All tiAllocations

Fewer

2626

Investments No Longer invest Low/no

1622

Low/no leverage fundsOpportunistic FundsN ff t

5522 No effect

Not Specified

Source: Prequin, 2011

WHAT DOES THIS MEAN FOESTATE INDUSTRY?ESTATE INDUSTRY?

Interesting so when dInteresting … so when dthreatened and endang

OR THE NON-LISTED REAL

did you first start feelingdid you first start feeling gered? …2007 or 2011?

STRUCTURE OF INDUSTRY DUE TO MARKET POLARISADUE TO MARKET POLARISA

UK DE ES ITFR Benelux Nordic

EXPECTED TO CHANGE ATIONATION

CONCLUSIONS

– Polarisation of investment objective

– Core, beta tracking real estate fun– Opportunity, alpha generating priv

– Polarisation of investment managem

– Large platforms with low margin pS i li b i i h hi h– Specialist boutiques with high mar

– Investor preferences for single couinconsistent with manager’s need

– Changing role of large investors

– Recognise their value as a sourceRecognise their value as a source– Leverage their own knowledge and

es

dsvate equity funds

ment

roduct (high volume by low value)i d (hi h l b l l )rgin product (high value by low volume)

untry funds with limited no. of investors to create economies of scale

e of capitale of capitald expertise

CONCLUSIONS (CONTD)

– Changing role of medium investorsR i h i l– Recognise their value as a source o

– Require greater control - narrowing o

Ch i l f ll i t– Changing role of smaller investors– Recognise non-listed presents only v– But don’t have to invest in real estate

– Changing base of fund managers– Industry consolidation creates winne

A ll b f l l tf– A smaller number of larger platformsbut aggregate for Europe is lower

– A larger number of smaller more locA larger number of smaller, more loc

f i lf capitalof parameters and investor board

viable investing option in real estate e

ers and losersf it l b b l tf ls for core – capital base by platform larger

cal and specialist platforms for opportunitycal and specialist platforms for opportunity

“We always overestimate the change & underestimate the change that will

Don't let yourself be lulled into inacti

Bill Gates

that will occur in the next two years occur in the next ten.

ion. “