lecture notes mth5124: actuarial mathematics i

TRANSCRIPT

Lecture Notes

MTH5124: Actuarial Mathematics I

Dr Adrian BauleSchool of Mathematical SciencesQueen Mary University of London

November 3, 2021

2

Contents

0 Prologue 70.1 What is an actuary? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70.2 About this course . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70.3 About these notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80.4 Life Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80.5 Books and tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90.6 Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1 Compound interest 131.1 Two types of interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.1.1 Simple interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141.1.2 Compound interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

1.2 Nominal and effective interest rates . . . . . . . . . . . . . . . . . . . . . . . . . . . 161.2.1 Accumulation factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161.2.2 Nominal interest rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171.2.3 Effective interest rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

1.3 Force of interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 201.3.1 Time-dependent interest rates . . . . . . . . . . . . . . . . . . . . . . . . . 201.3.2 Force of interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 211.3.3 Special case of constant force of interest . . . . . . . . . . . . . . . . . . . . 23

1.4 Rates of discount . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 251.4.1 Relation between nominal rates of discount and interest . . . . . . . . . . . . 26

1.5 Discounting Cash Flows or Present Values . . . . . . . . . . . . . . . . . . . . . . . 281.5.1 Discrete cash flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

1.6 Annuities-certain: introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311.6.1 Immediate annuity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311.6.2 Annuity-due . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311.6.3 Perpetuities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 321.6.4 Deferred annuities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 321.6.5 Increasing annuities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

1.7 Annuities-certain: more variations . . . . . . . . . . . . . . . . . . . . . . . . . . . 331.7.1 Annuities payable p-thly . . . . . . . . . . . . . . . . . . . . . . . . . . . . 331.7.2 Annuities payable continuously . . . . . . . . . . . . . . . . . . . . . . . . . 341.7.3 Accumulated values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

1.8 Continuous cash flows (not examinable) . . . . . . . . . . . . . . . . . . . . . . . . 371.8.1 Continuous cash flow with variable force of interest . . . . . . . . . . . . . . 38

1.9 Repayment of Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 401.9.1 Schedule of payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 401.9.2 Consolidating loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

3

1.10 Investment project appraisal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

1.10.1 Payback periods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

1.10.2 Yield . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

1.11 Immunisation of cash flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2 Fixed Interest Securities and Other Investments 51

2.1 Fixed Interest Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

2.1.1 Bond Terminology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

2.1.2 Example of a Government Security . . . . . . . . . . . . . . . . . . . . . . . 52

2.1.3 Types of Corporate Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

2.1.4 Valuation of a Bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

2.2 Cash including Treasury Bills . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

2.3 Inflation Linked Bonds and Real Returns . . . . . . . . . . . . . . . . . . . . . . . . 55

2.3.1 Calculating the Real Rate of Return . . . . . . . . . . . . . . . . . . . . . . 56

2.3.2 Valuation of Index-Linked Bonds . . . . . . . . . . . . . . . . . . . . . . . . 57

2.4 Equities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

2.4.1 Valuation of Shares by Discounting Future Dividends . . . . . . . . . . . . . 60

2.4.2 Characteristics of Preference Shares . . . . . . . . . . . . . . . . . . . . . . 61

2.5 Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

2.6 Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

2.6.1 Income Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

2.6.2 Tax on Capital Gains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

2.7 The term structure of interest rates . . . . . . . . . . . . . . . . . . . . . . . . . . 66

2.7.1 Spot rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

2.7.2 Forward rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

3 Life tables and life-table functions 69

3.1 Lifetime as a random variable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

3.1.1 Future lifetime . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

3.2 Basic life-table functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

3.2.1 Definitions of life-table function . . . . . . . . . . . . . . . . . . . . . . . . 71

3.2.2 Relation between lx and s(x) . . . . . . . . . . . . . . . . . . . . . . . . . 73

3.2.3 Basic life-table functions in terms of lx . . . . . . . . . . . . . . . . . . . . 74

3.3 Force of mortality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

3.3.1 Relation between µ(x) and other functions . . . . . . . . . . . . . . . . . . 77

3.3.2 The curve of deaths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

3.4 Analytical laws of mortality (not examinable) . . . . . . . . . . . . . . . . . . . . . 78

3.5 The expectation of life . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

3.5.1 The complete expectation of life . . . . . . . . . . . . . . . . . . . . . . . . 79

3.5.2 The curtate expectation of life . . . . . . . . . . . . . . . . . . . . . . . . . 80

3.6 Interpolation for fractional ages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

3.6.1 Linear interpolation on s(x) and lx . . . . . . . . . . . . . . . . . . . . . . 83

3.6.2 Derivation of relation between complete and curtate expectations of life . . . 85

3.6.3 Other interpolation schemes on s(x) and lx . . . . . . . . . . . . . . . . . . 86

3.6.4 Assumptions to obtain µ(x) . . . . . . . . . . . . . . . . . . . . . . . . . . 86

3.7 Select mortality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

4

4 Life insurance and related functions 954.1 Introduction to life assurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

4.1.1 Commutation functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 964.2 Whole-life assurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

4.2.1 Death benefit payable at instant of death . . . . . . . . . . . . . . . . . . . 974.2.2 Death benefit payable at end of year of death . . . . . . . . . . . . . . . . . 99

4.3 Whole-life annuities payable annually . . . . . . . . . . . . . . . . . . . . . . . . . . 1024.3.1 Whole-life annuity-due . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1024.3.2 Whole-life immediate annuity . . . . . . . . . . . . . . . . . . . . . . . . . . 1044.3.3 Life assurance premiums . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

4.4 Policies of duration n . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1064.4.1 n-year life assurance for life aged x . . . . . . . . . . . . . . . . . . . . . . 1064.4.2 n-year pure endowment for life aged x . . . . . . . . . . . . . . . . . . . . . 1074.4.3 n-year endowment policy for life aged x . . . . . . . . . . . . . . . . . . . . 1094.4.4 n-year life annuities for life aged x . . . . . . . . . . . . . . . . . . . . . . . 109

4.5 p-thly payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1114.5.1 Whole-life assurance paid p-thly . . . . . . . . . . . . . . . . . . . . . . . . 1114.5.2 Whole-life p-thly annuities . . . . . . . . . . . . . . . . . . . . . . . . . . . 1134.5.3 Alternative approximation for A(p)

x . . . . . . . . . . . . . . . . . . . . . . . 115

5

6

Chapter 0

Prologue

0.1 What is an actuary?

“An actuary is someone who expects everyone to be dead on time.” is one definition you canfind on the internet.1 In fact, actuaries do much more than deal with the probabilities of peo-ple dying! In short, they use financial and statistical theories to quantify and manage risk inall areas of business. Traditionally actuaries specialize in consultancy, investment, life and gen-eral insurance or pensions. However, their analytical skills are also increasingly valuable in otherareas—after all, “risk management” is of wide importance in financially turbulent times. Actuar-ies are highly-regarded and (well-paid!) professionals. For more details of career paths, etc., seehttp://www.actuaries.org.uk/becoming-actuary/.

0.2 About this course

The idea of this course is to introduce you to some of the basic mathematical ideas used in actuarialwork. MTH5124 is designed for second or third year undergraduates and assumes a backgroundin basic Calculus and Probability.2 All practicalities about the course itself (timetable, coursework,assessment details), etc., can be found on the course QM+ websitehttp://qmplus.qmul.ac.uk/course/view.php?id=18186.

Important announcements and corrections will also be posted there.The course uses familiar mathematical concepts (e.g., geometric series, probability distributions)

but in an unfamiliar context. I hope you will be interested to see how maths you already know canbe used effectively in the “real world”. However, one of the problems in applying maths to a differentfield is that you often have to learn new terminology, notation, etc. in order to communicate withspecialists in that area. This is certainly the case here; indeed you will soon be introduced to awhole zoo of complicated actuarial symbols and new vocabulary. It is crucial for success that youlearn this “new language” so that the familiar mathematical objects do not become lost in the fogof unfamiliar actuarial terminology.

The course has four main “chapters”:

1. Compound interest: Here we will cover various (interrelated) ways to quantify how compoundinterest is added to a loan/investment. You will learn how to calculate accumulations given theforce of interest (or related parameters) and how to deal with series of payments, in particularannuities-certain and perpetuities.

1A quick search with Google yields a variety of other humorous, and not-so-humorous, definitions as well as moreuseful career descriptions.

2Formal prerequisites are Calculus II and Introduction to Probability.

7

2. Fixed interest securities and other investments: You will learn about the most commonforms of investments and how to value investments using compound interest.

3. Life tables and life-table functions: Life tables are the actuary’s basic tool. You will learnhow to interpret them in order to find various probabilities related to life and death.

4. Life insurance and related functions: Here we will combine material from the first twochapters to deal with situations involving payments (with compound interest) whose valueand/or timing may depend on a person’s survival or death! Life insurance is the classicexample here.

0.3 About these notes

These notes will cover the material in roughly the same order as the lectures but their style willprobably be slightly different. In particular, the printed notes may contain some longer explanationsand extra examples which time prevents me covering in class. The lectures, however will be importantfor emphasizing the main points and giving exam tips—I strongly recommend that you attend or atleast follow the recordings on QM+!

To help you with revision, all important actuarial terms are printed in bold. You must be sureto understand what these mean, both in everyday language (could you explain them to your grand-mother or your next-door neighbour?) and in terms of the associated mathematical formulation.The notes will also contain a number of “examples” and “exercises”. For the former you will findfull details of the working; for the latter (usually) only the answers. A good way to check your ownunderstanding would be to read the text and try the associated exercises (contact me if you haveany difficulty getting the stated answers). I intend the unstarred exercises to correspond roughly tothe Key Objectives for the course (i.e., everyone should be able to do them); starred exercises willbe somewhat harder and should be attempted by those aiming for a high grade.

0.4 Life Tables

The examples in this document are based on the following life tables:

• English Life Table No 17,

• AMC00 mortality table for assured lives.

These are available on the QM+ page for MTH5124. Copies will be provided in the examination.

Full details of mortality tables published by the CMI can be found athttps://www.actuaries.org.uk/learn-and-develop/continuous-mortality-investigation/cmi-mortality-and-morbidity-tables.

The CMI is a subsidiary of the Institute and Faculty of Actuaries, and was previously knownas The Continuous Mortality Investigation. CMI tables relate to the mortality experience of lifeinsurance policyholders and the members of pension schemes.

The English Life Tables represent the mortality experience of the population of England andWales. Tables are published by the Office of National Statistics (ONS); further information onELT17 can be found athttps://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/lifeexpectancies-/bulletins/englishlifetablesno17/2015-09-01.

8

0.5 Books and tables

The course is designed to be fairly self-contained and does not follow any one textbook. However,you may find the following useful for background reading:

• S. J. Garrett An Introduction to the Mathematics of Finance (Butterworth-Heinemann);

– cited in these notes as [Gar13].

• J. J. McCutcheon & W. F. Scott An Introduction to the Mathematics of Finance (Butterworth-Heinemann);

– cited in these notes as [MS86].

• D. C. M. Dickson, Mary R. Hardy & Howard R. Waters Actuarial Mathematics for Life Con-tingent Risks (Cambridge University Press);

– cited in these notes as [DHW13].

• A. Neill Life Contingencies (Heinemann);

– cited in these notes as [Nei77].

• N. L. Bowers, H. U. Gerber, J. C. Hickman, D. A. Jones and C. J. Nesbitt Actuarial Mathe-matics (Society of Actuaries);

– cited in these notes as [BGH+97].

0.6 Acknowledgements

These notes have been produced by Jim Webber from notes for the predecessor module MTH6100Actuarial Mathematics, a module which covered a very similar syllabus. Great credit and thanks toDr Rosemary Harris for her excellent work in producing the original draft of the MTH6100 notes.Also thanks to Dr D. Stark and Dr W. Just for their additions and amendments to the notes sincethe original draft. In her original introduction, Dr Harris gave credit to the previous notes of Prof.B. Khoruzhenko and also the work of another previous lecturer, Dr L. Rass.

The changes I have made have been limited, but I take full responsibility for this edition of thenotes and the mistakes and contradictions that students will inevitably find. Please alert me to anymistake that you find by sending an email to: [email protected].

9

10

Bibliography

[Ber89] J. Bernoulli. Tractatus de seriebus infinitis. manuscript, 1689.

[BGH+97] N. L. Bowers, H. U. Gerber, J. C. Hickman, D. A. Jones, and C. J. Nesbitt. ActuarialMathematics. Society of Actuaries, Schaumburg, 1997.

[DHW13] D. C. M. Dickson, M. R. Hardy, and H. R. Waters. Actuarial Mathematics for LifeContingent Risks. Cambridge University Press, Cambridge, 2013.

[Gar13] S. J. Garrett. An Introduction to the Mathematics of Finance. Butterworth-Heinemann,Oxford, 2013.

[Hal93] E. Halley. An estimate of the degrees of mortality of mankind, drawn from the curioustables of the births and funerals at the city of Breslaw, with an attempt to ascertain theprice of annuities upon lives. Philosophical Transactions, 17:596–610, 1693.

[MS86] J. J. McCutcheon and W. F. Scott. An Introduction to the Mathematics of Finance.Butterworth-Heinemann, Oxford, 1986.

[Nei77] A. Neill. Life Contingencies. Heinemann, London, 1977.

[Pac94] L. Pacioli. Summa de Arithmetica. Venice, 1494.

11

12

Chapter 1

Compound interest

The material in this Chapter is covered very well in ([Gar13]). It is also covered in Chapters 1–4 of([MS86].)

1.1 Two types of interest

Often in the course of daily life and business, people need (or choose) to borrow money. For example,you might have a student loan or, later in life, need a mortgage or business loan. On the otherhand, if you happen to have “spare” money you can lend it to a bank, for example, by investing ina savings account or fixed term bond. In general, in all these situations the money lender receives akind of “reward” for lending the money; you can also think of this as the charging of “rent” for theuse of the money.

To be more specific the original loan/investment is called the capital (or principal) and the“reward” to the lender/investor is the interest. The time-dependent value of the investment, i.e.,the original loan plus the interest, is known as the accumulated amount (or accumulation).

Interest is expressed as a rate in two senses: per unit capital and per unit time. In practice,the interest rate is often quoted in percent and usually, but not always the basic time unit is oneyear. Note that “p.a.” is often used as an abbreviation for per annum (i.e., each year). To avoidconfusion you should always state the basic time period when giving an interest rate.

The interest rate on a transaction is affected by various factors including:

• the market rate for similar loans;

• the risk involved in the use to which the borrower puts the money (cf. mortgage loan ratesand unsecured personal loan rates);

• the anticipated rate of appreciation or depreciation in the value of the currency in which thetransaction is carried out (e.g., in times of high inflation the interest is higher).

For the present we assume that interest rates are constant in time and that there is no dependenceon the sum invested. We will later relax the first of these assumptions but the second will remainthroughout the course.

Now let’s consider a concrete example—a savings account with an interest rate of 5% p.a.. Inother words, one gets a return of £5 in one year for each £100 invested. Suppose you were to invest£200 then you could close the account after one year and withdraw £210 made up of the principal(£200) and the interest (£10). But what if the account were kept open for a period of time whichwas longer (or shorter) than one year? In that case we would need to distinguish between simpleinterest and compound interest.

13

1.1.1 Simple interest

For the bank account considered above then, in the case of simple interest, £10 would be addedeach year to your original deposit of £200. In general, the accumulated amount is after one timeunit (n = 1)

Accumulation = P + iP = P (1 + i) (1.1)

After n time units you obtain interest of niP and thus

Accumulation = P + niP = P (1 + ni) (1.2)

where P = principal invested;i = rate of interest;n = duration of investment/loan.

Expression (1.2) applies for all non-negative values of n. The normal commercial practice inrelation to fractional periods of a year is to pay interest on a pro rata basis (i.e., proportional to thetime the account is open). For an account of duration of less than one year it is usual to allow forthe actual number of days the account is held.

What happens when n is greater than 1 year? Imagine investing the £200 of our example fortwo years (again at 5% p.a. simple interest) then after these two years the accumulation will be

£200(1 + 2× 0.05) = £220.

Is there a way to make more money?Yes, you can close this account (Let’s call it account A.) after one year, at which time you will

withdraw £210 [see (1.2)]. Then place this sum on deposit in a new account, say B. When youclose account B after one further year, the sum withdrawn will be £210(1+1× 0.05)=£220.50. Inother words, you will have gained the princely sum of 50p!

The difference here is that, effectively, account B pays interest on the interest already earned.In general, banks do not want people to be frequently opening and closing accounts. (Whilst youmight not bother to do that to gain 50p you probably would for £50,000!) This is one reason why,for periods greater than one year, most bank accounts do not pay simple interest but instead theinterest is compounded...

1.1.2 Compound interest

In this case interest is paid on the previous interest accrued1. After one time unit (n = 1) we havethe same result as for simple interest

Accumulation = P (1 + i). (1.3)

After two time units (n = 2) we also accumulate the interest on the interest accrued in the previoustime period

Accumulation = P (1 + i) + P (1 + i)i = P (1 + i)(1 + i) = P (1 + i)2. (1.4)

The general formula for the accumulated amount thus becomes

Accumulation = P (1 + i)n. (1.5)

Another way to see this is that if An is the accumulation after n time units then An = An−1(1+i) =An−2(1 + i)2 = . . . = A0(1 + i)n, where A0 is the capital invested initially, i.e. P . This argumentobviously holds for integer n; the validity of (1.5) for non-integer n will be established in Section 1.3.

1Here “interest accrued” simply means interest already earned / applied to the account.

14

Exercise 1.1.1: Effect of compound interestConvince yourself that applying compound interest according to (1.5) has the same effect as closing an accountwith simple interest after each time period and reinvesting the money in an account paying the same interest.

Exercise 1.1.2: Compound interest formulaWrite a formal proof of (1.5) for integer n using induction.

From now on, “interest” always means compound interest unless explicitly stated otherwise.However, simple interest calculations (which you should be able to do in your head!) can sometimesbe a useful tool for checking that compound interest results are in the right ballpark. Simpleinterest is a good approximation for compound interest when n and i are small since in that case(1 + i)n ≈ 1 + ni.

Example 1.1.1: Low interest ratesSuppose you invest £1,000 for three years in a bank account which pays interest annually at 1.5% p.a.. Whatis the difference in accumulation if the bank pays compound interest compared to simple interest?

SolutionFor simple interest then, using (1.2),

Accumulation = £1000× (1 + 3× 0.015) = £1045.00. (1.6)

On the other hand, if interest is compounded, then we use (1.5):

Accumulation = £1000× (1 + 0.015)3 = £1045.68. (1.7)

[Unless stated otherwise, you should always give monetary answers rounded to the nearest penny.] So theaccumulation is only 68p greater if compound interest is paid.

In real-life there are many different kinds of transactions such as:

• payment of a series of premiums throughout a given time period in return for a lump sum atthe end of the period;

• mortgage loans, i.e., loans which are made for the specific purpose of house purchase (Theproperty to be purchased usually acts as security for the loan);

• fixed interest securities, such as regular income payments throughout a given time period andan additional lump sum at the end of the period in return for a one-off payment.

Knowledge of compound interest can be useful in comparing the merits of such transactions.

Example 1.1.2: Investment adviceYou have £10,000 to invest now and are being offered £22,500 after ten years as the return from theinvestment. The market rate is 10% p.a. (compound interest). Ignoring complications such as the effect oftaxation, the reliability of the company offering the contract, etc., do you accept the investment?

SolutionInvesting £10,000 for ten years with 10% compound interest will yield

Accumulation = £10000(1 + 0.1)10 = £25937. (1.8)

Since this is more than £22,500 you should reject the offered investment and just put the money in the bank.

Summary of 1.1

Accumulation of P units of money, simple interest: A = P (1 + ni)Accumulation of P units of money, compound interest: A = P (1 + i)n

15

321

i

t

0A13

(a)

321

0

A1A2

(b)

Figure 1.1: Schematic of investment and accumulation in two different scenarios. The PoC (1.10)says that the accumulated amount at t3 is the same in both cases.

1.2 Nominal and effective interest rates

Now we generalize the set-up of the previous section and consider how to define interest rates whenthe interest is compounded more frequently than annually. For example, many bank accounts payinterest monthly or quarterly.

1.2.1 Accumulation factor

Let A(t1, t2) be the accumulated value at time t2 of 1 unit of money invested at time t1. A(t1, t2)is called the accumulation factor and has the following useful properties:

1. A(t, t) = 1 (by definition)

2. Assuming that interest rates don’t depend on the size of the investment, then the accumulationat t2 of an investment of P at t1 is P ×A(t1, t2).

3. In a “consistent” market we expect that the accumulation doesn’t depend on when, or howoften, money is withdrawn and re-invested. This assumption is called the principle of con-sistency (PoC) and implies.

A(t1, t3) = A(t1, t2)A(t2, t3) ∀ t1 ≤ t2 ≤ t3. (1.9)

You may find this easier to understand with the aid of the diagram in Fig. 1.1.

4. From (1.9), it follows that

A(t1, t2) =A(t0, t2)

A(t0, t1)∀ t0 ≤ t1 ≤ t2. (1.10)

Exercise 1.2.1:Check Eq. (1.10).

Suppose the basic unit of time is one year and interest is compounded yearly at constant rate i.Then we have A(0, 1) = (1 + i) or, more generally,

A(t, t+ n) = (1 + i)n (1.11)

where n is (for now) an integer. This statement is just another way of writing (1.5).Now consider what happens if interest is paid more frequently. In this case we can have accu-

mulations over fractional time periods. In general we say that interest is compounded p-thly (orconvertible p-thly) if it is paid p times in each unit time interval, i.e., paid after a “term” of length1/p. For example, in the usual case where the basic unit of time is one year, then p = 4 meansinterest paid quarterly, whereas p = 12 means interest paid monthly.

16

1.2.2 Nominal interest rates

A nominal interest rate is a rate, per unit time, of interest which applies over a different timeperiod. For example, “overnight money” means that a yearly rate of interest is applied daily (i.e.interest is converted into capital daily, but interest is quoted as a rate per annum).

A nominal interest rate of i(p) per basic time unit is defined to mean that interest is compoundedp-thly with an interest rate of i(p)/p in a time interval of length 1/p. Equivalently, we have

A

(t, t+

1

p

)= 1 +

i(p)

p. (1.12)

For example, a nominal interest rate of 12% p.a. compounded monthly (p=12) means an interestrate of 1% per month and therefore an accumulation factor A(t, t+ 1/12) = 1.01.

Note on notation:

• i(p) does not mean i raised to the power p. The brackets are there to remind you that the phere is just a label.

• In fact, a number in brackets to the top right of any actuarial symbol usually tells you aboutthe frequency of payments; we will see other examples later.

• In [MS86] you will find that i(p) is sometimes written as ih where h = 1/p; we will not usethis notation.

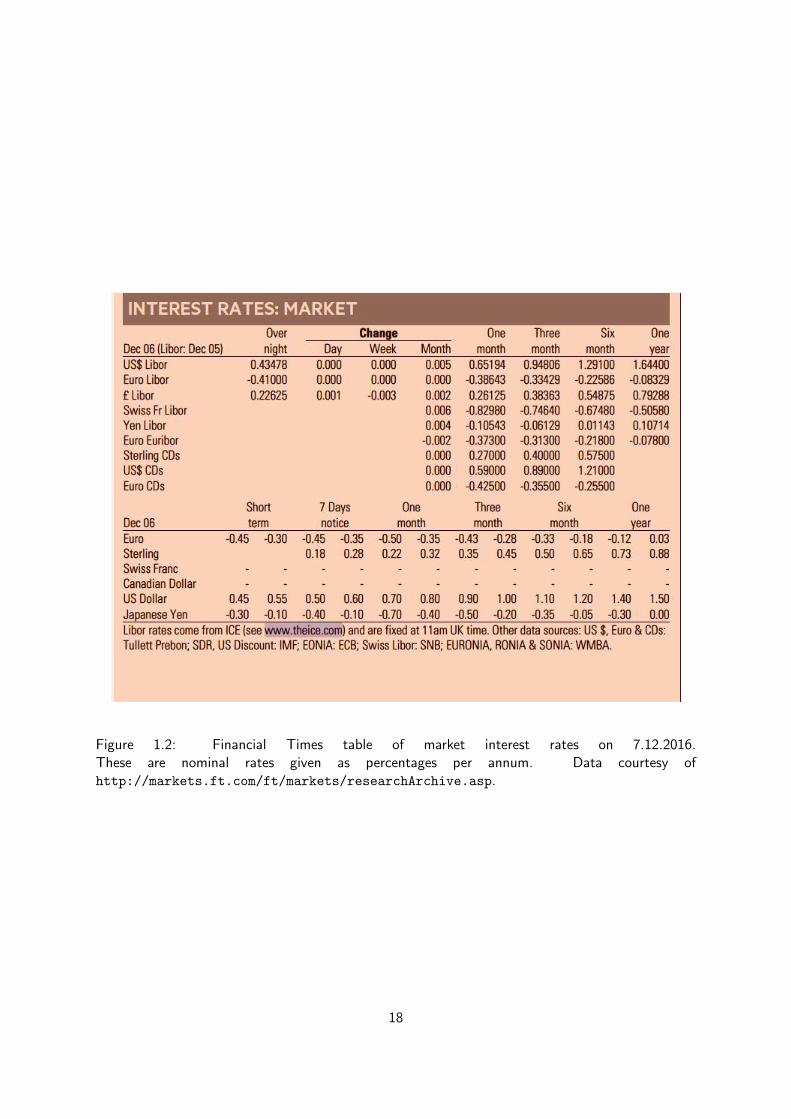

Nominal interest rates for different periods (i.e., terms of length 1/p for different p) are oftenquoted in the financial press, for example, see the excerpt from the Financial Times presented inFig. 1.2.

Example 1.2.1: Nominal interest ratesConsider the nominal market interest rates (% p.a.) given in Fig. 1.2. Look at the line labelled “£ Libor”.2

Assuming these interest rates, find the accumulation of an investment of £10,000 on 7.12.16 after (a) onequarter and (b) 1 day (overnight money).

SolutionHere the basic time unit is one year (interest rates are quoted p.a.) but we are considering interest paid afterfractions of this time.(a) p = 4; from the table we have a nominal interest rate of 0.38363% per year which means i(4) = 0.0038363.The accumulated amount is given by

Accumulation = P ×A(

0,1

4

)(1.13)

= £10000×(

1 +0.0038363

4

)[using (1.12)] (1.14)

= £10009.59 (to the nearest penny). (1.15)

(b) p = 365; i(365) = 0.0022625 and

Accumulation = £10000×(

1 +0.0022625

365

)(1.16)

= £10000.06 (to the nearest penny). (1.17)

[Note that to get these answers correct to the nearest penny you need to keep all available decimal places forthe interest rates. Never round up until the end of a calculation!]

2Libor stands for the “London Interbank Offered Rate” and is based on the interest demanded by banks in theLondon wholesale money market when borrowing from each other.

17

Figure 1.2: Financial Times table of market interest rates on 7.12.2016.These are nominal rates given as percentages per annum. Data courtesy ofhttp://markets.ft.com/ft/markets/researchArchive.asp.

18

1.2.3 Effective interest rates

The effective interest rate i is the total interest paid on one unit of money over one basic timeperiod. In other words, it is the interest rate converted from the nominal rate into the “equivalent”rate if compounding were carried out at the end of one basic time unit (rather than p-thly).

By equivalent, we mean the rate which gives the same accumulation after unit time. Now, theaccumulation factor for one time unit with interest at rate i per unit time is just [see Eq. (1.11)]

A(0, 1) = (1 + i). (1.18)

On the other hand, for compounding p-thly we have

A

(0,

1

p

)A

(1

p,

2

p

). . . A

(1− 1

p, 1

)=

(1 +

i(p)

p

)p. (1.19)

So, if the accumulations are the same, we require

1 + i =

(1 +

i(p)

p

)p. (1.20)

This is a very important relationship between the effective interest rate i and the nominal interest rateconverted p-thly i(p). You need to remember (1.20) or be able to reproduce quickly the argumentwhich gives it. Similarly, the rearranged formula

i(p) = p[(1 + i)1/p − 1], (1.21)

is often useful.Note:

• i = i(1).

• When the basic time period is 1 year, i is called the Effective Annual Rate (EAR) or theAnnual Equivalent Rate (AER).

• The AER is useful for comparing the annual cost of financial products with different periodsof compounding.

• Adverts for credit legally have to include the so-called Annual Percentage Rate (APR).3

This is defined as the effective annual rate of interest on a transaction obtained by taking intoaccount all the items entering the total charge for credit (i.e., including fees, etc.).

Example 1.2.2: AERYou wish to take out a loan and are offered two different deals. Bank A charges interest weekly at the nominalrate of 11% per annum. Bank B charges interest quarterly at the rate of 3% per quarter. Calculate the AERin each case and hence decide which bank offers the better deal.

SolutionBank A: Setting the basic time unit as 1 year, we have p = 52 since there are (approximately) 52 weeksin 1 year. We are given the nominal rate i(52) = 0.11 and therefore can use (1.20) to calculate the annualequivalent rate:

i =

(1 +

0.11

52

)52

− 1 (1.22)

= 0.1161 (to 4 d.p.). (1.23)

3Consumer Credit Act (1974)

19

Bank B: Here we are given that i(4)/4 = 0.03 (rate per quarter) and, using again (1.20),

i = (1 + 0.03)4 − 1 (1.24)

= 0.1255 (to 4 d.p.). (1.25)

Notice that in both cases the effective interest rate is slightly higher than the nominal interest rate (dueto the compounding of interest). Bank A offers a lower AER (approximately 11.61% p.a.) than Bank B(approximately 12.55% p.a.) so it is obviously the better choice for the loan.

An alternative strategy in problems which only involve one compounding time period (ratherthan a comparison) is to set the basic time unit equal to the compounding period. This is usuallyslightly quicker but, if you find it confusing, you may feel safer always setting unit time equal to oneyear (i.e., always measuring time in years).

Example 1.2.3: Quarterly interestIf interest is paid quarterly at the rate of 2% per quarter, what is the accumulation of an investment of £500after two years?

SolutionLet us set the basic time unit to be equal to one quarter. Then i(1) = i = 0.02 and (since there are 8 quartersin two years) we have

Accumulation = P × (1 + i)n (1.26)

= £500× (1 + 0.02)8 (1.27)

= £585.83 (to the nearest penny). (1.28)

Exercise 1.2.2: Quarterly interestConsider the same scenario as Example 1.2.3. Check that one gets the same answer by taking the basic timeunit to be equal to one year (so that i(4)/4 = 0.02); calculating i via (1.20) and then finding the accumulationfor n = 2.

Exercise 1.2.3: High APRFirst Premier Bank offers a credit card with an “APR of 79.9%” (p.a. is assumed here). If the interest iscompounded monthly and there are no other charges/fees (i.e., the APR is just the annual effective interestrate), determine how much a loan of $1000 increases to after just one month.[Answer: $1050.15 (to the nearest cent)]

Summary of 1.2

For general rates:

Accumulation factor for interest converted p-thly: A(t, t+ 1

p

)= 1 + i(p)(t)

p

Only for time-independent rates:

Relation between nom. and effect. interest rates: 1 + i =(

1 + i(p)

p

)p1.3 Force of interest

1.3.1 Time-dependent interest rates

So far we have assumed that interest rates are time-independent. In reality of course, interestrates usually vary due to changing economic circumstances. For time-dependent rates we define atime-dependent nominal rate i(p)(t), for transactions of term 1/p starting at time t, such that

A

(t, t+

1

p

)= 1 +

i(p)(t)

p(1.29)

20

or, on rearranging,

i(p)(t) =A(t, t+ 1

p)− 1

1/p. (1.30)

Equation (1.29) means that if we know the nominal rates at some time t0 we can calculate theaccumulation for terms (of length 1/p) starting at time t0 but not for terms starting at any othertime. For example, the data in the table of Fig. 1.2 allow us to calculate the accumulations for timeperiods starting on 7.12.16 just as was done in Example 1.2.1. However, since for time-dependentrates the accumulation factors on the left-hand side of (1.19) are all different we can no longerdefine an effective rate i via the simple relation (1.20).

What can we say in general about the function i(p)(t)? Inspection of data, such as that inFig. 1.2, suggest that i(p)(t) is usually a decreasing function of p. Generically, one also observesthat as p becomes very large i(p)(t) approaches a t-dependent limiting value (approximately 0.57for the £ Libor data in Fig. 1.2). Motivated by this observation, in the next section we will see apowerful general formalism for dealing with time-dependent rates.

Exercise 1.3.1: *Trend of i(p) as function of pIn the time-independent case, show from (1.21) that the nominal interest rate i(p) corresponding to constanteffective rate i decreases when the frequency of compounding p increases. [Hint: You may use, without proof,the inequality e−x > 1− x which holds for x > 0.]

Exercise 1.3.2: Limit of i(p)

In the time-independent case, prove from (1.21) that limp→∞ i(p) = ln(1 + i). [Hint: Use l’Hopital’s rule.]

1.3.2 Force of interest

Following on from the remarks in the previous section about the trend of nominal interest rates, weassume that, as p increases, i(p)(t) tends to a t-dependent limiting value and define

δ(t) = limp→∞

i(p)(t). (1.31)

The quantity δ(t) is called the force of interest per unit time at time t. It can also be describedas the “instantaneous rate of interest per unit time at time t” or the “nominal rate of interest perunit time at time t convertible momently”. (Here “convertible momently” means that interest iscompounded continuously.)

In many problems it is useful to treat δ(t) as the fundamental parameter and derive otherquantities from it. The following is a particularly important theorem.

Theorem 1.3.1:If δ(t) and A(t0, t) are continuous functions of t for t ≥ t0, and the Principle of Consistency (PoC)holds, then for t0 ≤ t1 ≤ t2,

A(t1, t2) = exp

[∫ t2

t1

δ(s) ds

]. (1.32)

ProofWe start by combining (1.31) and (1.30):

δ(t) = limp→∞

A(t, t+ 1p)− 1

1/p. (1.33)

21

Now let h = 1/p, then

δ(t) = limh→0+

A(t, t+ h)− 1

h(1.34)

= limh→0+

A(t0, t)A(t, t+ h)−A(t0, t)

hA(t0, t)(1.35)

=1

A(t0, t)limh→0+

A(t0, t+ h)−A(t0, t)

h[using PoC]. (1.36)

Next, for convenience, we let F (t) = A(t0, t) (i.e., the value at t of one unit of money invested att0) and observe that (1.36) can be written as

δ(t) =1

F (t)limh→0+

F (t+ h)− F (t)

h. (1.37)

Recognising here the derivative4 of F we have

δ(t) =1

F (t)

dF (t)

dt(1.38)

=d

dt[lnF (t)] [chain rule]. (1.39)

Straightforward integration then yields∫ t

t0

δ(s) ds = lnF (t)− lnF (t0) (1.40)

= ln

(F (t)

F (t0)

), (1.41)

and upon inverting both sides and using F (t0) = A(t0, t0) = 1, we obtain

F (t) = A(t0, t) = exp

[∫ t

t0

δ(s) ds

], (1.42)

which proves the theorem, since t0, t are arbitrary.

Notice the appearance of the exponential function in this proof. In fact, the mathematicalconstant e was first “discovered” by Jacob Bernoulli during his 1683 studies of interest compoundedcontinuously [Ber89].

By substituting (1.32) in (1.30), we obtain i(p)(t) in terms of δ(t)

i(p)(t) =exp

[∫ t+1/pt δ(s) ds

]− 1

1/p, (1.43)

and the p = 1 case gives

i(t) = exp

[∫ t+1

tδ(s) ds

]− 1. (1.44)

Example 1.3.1: Force of interest and accumulation factorAssume that the force of interest varies with time and is given by δ(t) = a + b

t . Find the formula for theaccumulation of one unit of money from time t1 to time t2.

4Strictly the right-sided derivative.

22

SolutionBy Eq. (1.32),

A(t1, t2) = exp

[∫ t2

t1

(a+

b

s

)ds

](1.45)

= exp [(at2 + b ln t2)− (at1 + b ln t1)] (1.46)

= exp

[a(t2 − t1) + b ln

t2t1

](1.47)

= exp [a(t2 − t1)]

(t2t1

)b. (1.48)

Example 1.3.2: Force of interest and value of investmentAssume that the force of interest varies with time and is given by δ(t) = 0.02(1 + 1

1+t2 ) where t is measuredin years. Find the accumulation at time t = 1 of £1,000 invested at time t = 0.

SolutionAgain using Eq. (1.32),

Accumulation = C ×A(0, 1)

= £1000 exp

{∫ 1

0

0.02

(1 +

1

1 + s2

)ds

}= £1000 exp

{0.02 [s+ arctan s]

10

}= £1000 exp

{0.02

(1 +

π

4− 0− 0

)}= £1036.35 (to nearest penny).

Exercise 1.3.3: Force of interest and nominal interest ratesAssume that the force of interest varies as in Example 1.3.2. Use the relation (1.43) to find the value att = 0.5 of the nominal rate of interest per annum on transactions of term three months.[Answer: 3.45% p.a. (to 2 d.p.)]

Exercise 1.3.4: *Stoodley’s formulaStoodley’s formula is sometimes used to model gradually increasing or decreasing interest rates. It has theform

δ(t) = p+s

1 + rest(1.49)

where p, r and s are suitable parameters. Show that, if this formula holds, the accumulation of one unit ofmoney from time 0 to time t is given by

A(0, t) = exp[(p+ s)t]1 + r

1 + rest. (1.50)

1.3.3 Special case of constant force of interest

In some situations (including many exam questions) a constant, i.e., time-independent force ofinterest is assumed. For this special case δ(t) = δ for all t. Hence

A(t1, t2) = eδ×(t2−t1) (1.51)

which, in (1.43), leads straightforwardly to

i(p) = p(eδ/p − 1). (1.52)

The p = 1 case gives an important relationship between the effective rate i and the force of interest

i = eδ − 1 (1.53)

23

or, equivalently,δ = ln(1 + i). (1.54)

Combining this last equation with (1.51) we obtain that, for any n,

A(t0, t0 + n) = eδn (1.55)

= (1 + i)n. (1.56)

In other words, if interest on fractional time periods is paid at the nominal rate corresponding to thesame effective rate i, then the compound interest formula (1.11) [or (1.5)] holds also for non-integern!

Example 1.3.3: Double your money!If interest is compounded at an effective rate of 5% p.a., how long does it take an investment of £200 todouble in value?

SolutionWe take the basic time unit to be 1 year and set i = 0.05. Hence the doubling time is n years where nsatisfies the equation

400 = 200(1 + 0.05)n. (1.57)

This simplifies to2 = 1.05n, (1.58)

which is solved by taking logarithms of both sides to give

n =ln 2

ln 1.05= 14.21 (to 2 d.p.). (1.59)

So the investment doubles in approximately 14.2 years or, to the nearest month, 14 years and 2 months.[Note that the size of the original investment is irrelevant.]

Exercise 1.3.5: “Rule of 72”A rough rule-of-thumb dating back to at least the 15th Century [Pac94] is that, if interest is compounded atan effective rate of K% p.a., an investment takes approximately 72/K years to double. Check this againstthe exact doubling time for interest rates of 4%, 8% and 12%. You should find that for these values therelative error implied by the “Rule of 72” is less than 2%.

Example 1.3.4: Quadruple your money!Find the force of interest if an investment of 2000 Icelandic Krona quadruples in value in 10 years.

SolutionFrom Eq. (1.51), the force of interest δ must satisfy

2000eδ×10 = 8000 ⇔ e10δ = 4. (1.60)

Taking logarithms then yields

δ =1

10ln 4 = 0.1386 p.a. (to 4 d.p.). (1.61)

Exercise 1.3.6: Limit of i(p)

Starting from Eq. (1.52), show that limp→∞ i(p) = δ, i.e., the special case of (1.31) for time-independentrates. [Hint: Compare Exercise 1.3.2.]

Exercise 1.3.7: *Approximate expressions for δ and i in terms of i(p) when p is largeStarting from Eqs. (1.54) and (1.20) use Taylor’s expansion of ln(1 + x), |x| < 1 (Calculus I) to obtain:

δ = i(p) − [i(p)]2

2p+ ε, where |ε| ≤ [i(p)]3

3p2(1.62)

= i(p) − [i(p)]2

2p+

[i(p)]3

3p2+ ε, where |ε| ≤ [i(p)]4

4p3. (1.63)

24

Formula (1.62) can be used to give another proof of the fact that the force of interest is the nominal rate ofinterest compounded instantly. Try to find this proof.

Summary of 1.3

Force of interest: δ(t) = limp→∞

i(p)(t) = limh→0+

A(t,t+h)−1h

Accumulation at t2 of a unit invest. at t1: A(t1, t2) = exp[ ∫ t2

t1δ(s) ds

]Constant force of interest δ: eδ = 1 + i =

[1 + i(p)

p

]p1.4 Rates of discount

Let us consider the case of a time-varying force of interest δ(t) (i.e., for now we do not assume aconstant force of interest).

Assume that interest is compounded p-thly and recall, from Section 1.2, that the interest foruse of one unit of money over one subperiod of time of length 1/p starting at time t is i(p)(t)/p.Note that it is assumed that this interest is paid in arrears at the end of the subperiod, i.e., at timet+ 1/p. So, restating our previous definition, we have:

i(p)(t) is the rate per unit time and per unit capital at which interest for use of money over timeperiod [t, t+ 1/p] is paid in arrears (i.e., at t+ 1/p).

However, in some circumstances one might pay for use of money in advance at the start ofthe subperiod. The amount of the equivalent payment, for use of one unit of money, is denoted byd(p)(t)/p where d(p)(t) is called the nominal rate of discount compounded p-thly (or convertiblep-thly) and defined such that:

d(p)(t) is the rate per unit time and per unit capital at which interest for use of money over timeperiod [t, t+ 1/p] is paid in advance (i.e., at t).

When p = 1 we drop the subscript, i.e., d(t) is the rate at which interest for use of money over unittime period is paid in advance.

We have defined A(t1, t2) as the accumulation at time t2 of one unit of money invested at timet1. Analogously, we now define D(t1, t2) as the value of an investment at time t1 which gives areturn of one unit of money at time t2. You should be able to convince yourself easily that

D(t1, t2) =1

A(t1, t2)(1.64)

= exp

[−∫ t2

t1

δ(s) ds

]. (1.65)

Now, when we borrow one unit of money for use over one subperiod and pay interest in advance,we actually receive 1− d(p)(t)/p at time t and repay 1 at time t+ 1/p. Hence it follows that

D

(t, t+

1

p

)= 1− d(p)(t)

p. (1.66)

Exercise 1.4.1: Rates of discount for differing subperiodsBy working backwards through one time unit (and assuming the Principle of Consistency) show that

1− d(0) =

[1−

d(4)( 34 )

4

][1−

d(2)( 14 )

2

] [1− d(4)(0)

4

]. (1.67)

25

1.4.1 Relation between nominal rates of discount and interest

The nominal rates of interest and discount are related since payment of d(p)(t)/p at time t isequivalent to payment of i(p)(t)/p at time t + 1/p. Or, in other words, an investment of d(p)(t)/pat time t gives a return of i(p)(t)/p at time t+ 1/p. Therefore

A

(t, t+

1

p

)d(p)(t)

p=i(p)(t)

p. (1.68)

The validity of this equation can be easily seen as follows. Imagine that we have instead

A

(t, t+

1

p

)d(p)(t)

p>i(p)(t)

p. (1.69)

Then it would be possible to obtain a risk-free profit: 1. Borrow 1 unit of money at time t with

interest paid in arrears. For this you need to pay i(p)(t)p at time t + 1/p. 2. Loan this money to

another person with interest paid in advance. You receive d(p)(t)p at time t. But now you can invest

this money in a bank account over the time period [t, t + 1/p], and if Eq. (1.69) holds you can

pay i(p)(t)p and still make a profit. A similar reasoning can be made for < in Eq. (1.69) switching

borrowing and loaning. In a financial market, such a risk-free profit is not possible, therefore theequality has to hold in Eq. (1.69).

Using Eq. (1.29), we obtain

d(p)(t)

p=

i(p)(t)p

1 + i(p)(t)p

(1.70)

Notice that this equation implies that the nominal rate of discount compounded p-thly is alwayssmaller than the nominal rate of interest compounded p-thly. Trivial rearrangement of (1.70) gives

1

d(p)(t)=

1

i(p)(t)+

1

p(1.71)

which may be easier to remember. From this form of the relation it follows obviously that

limp→∞

d(p)(t) = limp→∞

i(p)(t) = δ(t) (1.72)

which is consistent with the intuition that for compounding continuously it makes no differencewhether we pay interest in advance or in arrears.

Exercise 1.4.2: Relation between nominal rates of discount and interestGive an alternative derivation of (1.70) starting from (1.64).

Special case of constant force of interest

For the remainder of Section 1.4 we specialize again to the practically important case of constantforce of interest. By substituting i(p)(t) = i(p) = p(eδ/p − 1) [see (1.52)] in (1.70) we obtain thatd(p)(t) = d(p) where

d(p) = peδ/p − 1

1 + eδ/p − 1(1.73)

= p(1− e−δ/p). (1.74)

For p = 1 we have

d =i

1 + i= 1− e−δ, (1.75)

where d is called the effective rate of discount (or, if unit time is one year, the annual rate ofdiscount).

26

Exercise 1.4.3: Relation between d and iInterpret the first equality in (1.75) in words.

Relation between nominal and effective rates of discount

There are many ways to derive a relation between d and d(p). One possibility is to start from (1.74)which can be rearranged to give

e−δ/p = 1− d(p)

p(1.76)

which leads to

e−δ =

(1− d(p)

p

)p(1.77)

and, using (1.75),

1− d =

(1− d(p)

p

)p. (1.78)

Equation (1.78) should be compared with (1.20).

Example 1.4.1: Interest and discountSuppose interest is paid at an AER of 3% p.a.. You take out a loan of £1,000 for 6 months. How muchinterest should you pay if the interest is paid in arrears? And how much if the interest is paid in advance?

SolutionTake the basic time unit equal to 1 year, then i = 0.03 and

i(2)

2=

2[(1 + i)1/2 − 1]

2[using (1.21)] (1.79)

= 0.14889 (to 5 d.p.) (1.80)

Now

Interest paid in arrears = £1000× i(2)

2(1.81)

= £14.89 (to nearest penny), (1.82)

and

Interest paid in advance = £1000× d(2)

2(1.83)

= £1000×i(2)

2

1 + i(2)

2

[using (1.70)] (1.84)

= £14.67 (to nearest penny). (1.85)

Noticee that, as we expect, the interest paid in advance is slightly less than the interest paid in arrears; indeed£14.67 = £14.89/(1 + i)1/2.

Exercise 1.4.4: Key relationshipsLook back through Sections 1.2–1.4 and combine equations to show that, for constant force of interest,[

1 +i(p)

p

]p= 1 + i = eδ =

1

1− d=

1[1− d(p)

p

]p . (1.86)

If you remember this series of equalities then, given any one of i(p), i, δ, d(p) or d, you can find any of theothers by simple rearrangement.

27

Example 1.4.2: Conversion from d to i(12)

Given that d = 0.0625, find i(12).

SolutionFrom Eq. (1.86), we have [

1 +i(p)

p

]p=

1

1− d(1.87)

which can be rearranged to yield

i(p) = p

[1

(1− d)1/p− 1

]. (1.88)

Hence, for d = 0.0625,

i(12) = 12[(1− 0.0625)−1/12 − 1

](1.89)

= 0.0647 (to 4 d.p.). (1.90)

[Note that it should not be necessary to memorize (1.88), or to calculate intermediate quantities such as i orδ.]

Exercise 1.4.5: *Inequalities for ratesShow that

d = d(1) < d(2) < d(3) < . . . < d(p) < . . . < δ < . . . < i(p) < . . . < i(3) < i(2) < i(1) = i (1.91)

[Hint: Compare Exercise 1.3.1.]

Summary of 1.4

For general force of interest:

Discounted value at t1 of a unit invst. at time t2: D(t1, t2) = exp[−∫ t2t1δ(s)ds

]When interest is converted p-thly: D

(t, t+ 1

p

)= 1− d(p)(t)

p

Relation between nom. discount and interest rates: 1d(p)(t)

= 1i(p)(t)

+ 1p

Only for constant force of interest:

Relation between nom. and eff. discount rates: 1− d =[1− d(p)

p

]p1.5 Discounting Cash Flows or Present Values

From Section 1.3, we know that the value at time t2 of an investment of C at time t1 is C ×A(t1, t2) = C exp

[∫ t2t1δ(s)ds

]. On the other hand, from Section 1.4, the value at time t1 of an

investment of C at time t2 is C × D(t1, t2) = C exp[−∫ t2t1δ(s)ds

]. This enables us to find the

value at any time of an investment whose value we know at any other time. In this section, we willuse this approach to compare the values of cash flows restricting the analysis to the case of constantforce of interest (with the exception of Exercises 1.8.1 and 1.8.2).

For constant force of interest we have,

A(t1, t2) = (1 + i)(t2−t1) and D(t1, t2) = (1 + i)−(t2−t1). (1.92)

For brevity of writing we now define the discounting factor

v =1

1 + i= 1− d = e−δ (1.93)

28

and note that with this notation A(t, 0) = D(0, t) = vt.

The quantity Cvt is called the (discounted) present value of C due at time t. We will abbreviatethis to P.V..

In practice this means that you must remember the following simple rules. Suppose we investan amount of C at some time. Then...

• ...to find the value of the investment t years later you multiply C by (1 + i)t;

• ...to find the value of the investment t years earlier you multiply C by vt .

We will now use these rules to evaluate and compare the values of cash flows. Here a cash flowmeans a series of payments. When considering cash flows, it is important to recognise the timing ofeach cash flow; is the cashflow at the beginning of the month or the end of the month or, perhaps,in the middle of the month?

1.5.1 Discrete cash flows

This is the most common case. Consider payments of c1, c2, . . . cn due at times t1, t2, . . . , tn in thefuture. The present value 5 (i.e. at time t = 0) of such a cash flow is given by

P.V. of discrete cash flow = c1vt1 + c2v

t2 + . . .+ cnvtn =

n∑j=1

cjvtj . (1.94)

In many problems we are interested in comparing cash inflow and cash outflow. To compare twocash flows we must look at their values at the same time; it’s usually best to choose the present timeand to compare P.V.s. Two cash flows are equivalent if they have the same P.V.. If the presentvalue of cash inflows is equal to the present value of cash outflows at a particular rate of interest,it means that the outgoing cash flows when invested with interest will generate the incoming cashflows. Equality of inflows and outflows is expressed by the so-called equation of value

P.V. of outgoing cash flows = P.V. of incoming cash flows. (1.95)

The equation of value can be expressed at any point of time. It brings together three quantities:amount(s), time(s) and rate of interest. If the others are known, an unknown quantity from this listcan be determined by the equation of value.

Example 1.5.1: Equation of valueA borrower is under an obligation to repay a bank £6,280 in four years’ time, £8,460 in seven years’ time and£7,350 in thirteen years’ time. As part of a review of his future commitments the borrower now offers eitherof the following:

• to discharge his liability for these three debts by making an appropriate single payment five years fromnow (offer A);

• to repay the total amount owed (i.e., £22,090) in a single payment at an appropriate time (offer B).

On the basis of a constant rate of interest 8% per annum effectively, find the appropriate single paymentif offer A is accepted by the bank, and the appropriate time to repay the entire indebtedness if offer B isaccepted.

5Many authors use the terminology Net Present Value, abbreviated to NPV, to denote the present value of a cashflow.

29

SolutionWe take 1 year as the basic time unit so that i = 0.08 and

v =1

1 + i=

1

1.08. (1.96)

Offer A:We need to find £C such that the following two cash flows are equivalent.

Out: £C at t = 5,

In: £6280 at t = 4, £8460 at t = 7, and £7350 at t = 13.

The equation of value expressed at the present time, t = 0, is

Cv5 = 6280v4 + 8460v7 + 7350v13 (1.97)

but in fact the equation of value expressed at t = 4 has a simpler form

Cv = 6280 + 8460v3 + 7350v9. (1.98)

This is easily solved for C

C =6280 + 8460v3 + 7350v9

v(1.99)

= 18006.46 (to 2 d.p.). (1.100)

So the borrower should make a single payment of £18,006.46 (to the nearest penny).

Offer B:We need to find tp such that the following two cash flows are equivalent.

Out: £22090 at t = tp,

In: £6280 at t = 4, £8460 at t = 7, and £7350 at t = 13.

In this case, the equation of value expressed at the present time, t = 0, is

22090vtp = 6280v4 + 8460v7 + 7350v13, (1.101)

and solving for tp yields

tp =ln 6280v4+8460v7+7350v13

22090

ln v(1.102)

= 7.66 (to 2 d.p.). (1.103)

So the borrower should make the payment after approximately 7 years and 8 months.

Summary of 1.5

Discounting factor: v = 11+i = 1− d

Discounted present value of C due in time t: Cvt

Equation of value: P.V. of outflow = P.V. of inflow

30

1.6 Annuities-certain: introduction

An annuity is a series of payments made at regular time intervals. We restrict ourselves here mainlyto level annuities where the payments are all equal.

There are two sorts of annuities: annuities-certain and life annuities. For an annuity certainthe number of payments is certain and specified in the contract. In contrast, the payments maydepend on the survival of one or more human lives, then we say life annuity. In that case, the numberof payments is uncertain. For example, pensions are life annuities.

In this section we look at annuities-certain; life annuities will be considered later. We willderive the P.V.s, for annuities-certain where one unit of money is paid per unit time. Obviously forannuities where payment is C units of money per unit time, the P.V. is obtained by multiplying thecorresponding expression by C.

The main mathematical result we will need is the well-known formula for the sum of a geometricprogression:

N−1∑j=0

qj = 1 + q + q2 + . . .+ qN−1 =1− qN

1− q, for any q 6= 1. (1.104)

1.6.1 Immediate annuity

Consider n payments of one unit of money to be made at intervals of one unit of time with the firstpayment due one unit of time from now (i.e., the first payment is at time 1 and the last at time n).This situation is known as an immediate annuity, the symbol for its present value is an and

an = v + v2 + . . .+ vn = v1− vn

1− v. (1.105)

OR

an =1− vn

imultiplying numerator and denominator by (1 + i) and simplifying. (1.106)

Note that the payments are made in arrears, i.e., at the end of each time period and that here, asthroughout this section, we assume a constant (and strictly positive) force of interest. In actuarialnotation, a subscript enclosed in a right angle always indicates the (fixed) term of the given financialobject.

1.6.2 Annuity-due

Now consider the same series of payments as in the previous paragraph but with payments made inadvance, i.e., at the beginning of each time period (so that the first payment is at time 0 and thelast at n − 1). This situation is known as an annuity-due, the symbol for its present value is anand

an = 1 + v + . . .+ vn−1 =1− vn

1− v. (1.107)

Notice that an = van , and an = 1 + an−1 . An immediate annuity is also known as an annuitypaid in arrears.

Exercise 1.6.1: Relations between annuitiesInterpret the equalities in the last sentence in words.

Example 1.6.1: Annuity-dueA loan of £300,000 is to be repaid by ten equal annual instalments, the first is due now. Find the annualpayment if the interest on the loan is charged at the AER of 12.99% p.a..

31

SolutionLet £C be the annual payment. Take 1 year as the unit time. Then i = 0.1299 and the discounting factor isgiven by

v =1

1 + i=

1

1.1299. (1.108)

Now the loan is to be repaid by an annuity-due payable annually at rate £C per annum. The presentvalue of the repayments is thus Ca10 and equating P.V.s we obtain the equation of value:

300000 = Ca10 . (1.109)

Hence

C =300000

a10=

300000(1− v)

1− v10= 48911.2067 (to 4 d.p.). (1.110)

So the annual repayment is £48, 911.21 (to the nearest penny).Note, if there is likely to be any confusion about the value of i (and especially for questions involving

more than one interest rate), it is wise to state explicitly the interest rate implicit in a given function. Forexample, one could write (1.109) in the form

300000 = Ca10 at 12.99%. (1.111)

An alternative notation is to use a vertical bar and an @ symbol. For example

C =300000(1− v)

1− v10

∣∣∣∣@i=0.1299

. (1.112)

An annuity-due is also known as an annuity paid in advance.

1.6.3 Perpetuities

Notice that an and an are monotone increasing functions of n. Considering the limit of n → ∞corresponds to payments being made “in perpetuity”. One finds

a∞ = limn→∞

an =v

1− v=

1

i, (1.113)

and

a∞ = limn→∞

an =1

1− v=

1

d, (1.114)

which give the present values of an immediate perpetuity and a perpetuity-due respectively.The income from equity share or from a property investment will often be valued ”in perpetuity”

using the approach above.

1.6.4 Deferred annuities

Suppose a series of n unit payments starts at time m+ 1, the last one due at time m+n. This maybe considered as an immediate annuity deferred m time periods. The symbol for the presentvalue is m|an and

m|an = vm+1 + . . .+ vm+n = vman (1.115)

Similarly one can define an annuity-due deferred m time periods whose present value is m|an =vman .

Exercise 1.6.2: More relations between annuitiesShow that m|an = am+n − am and m|an = am+n − am .

Exercise 1.6.3: Deferred annuityJohn Doe wishes to purchase a deferred annuity of £10,000 per annum paid out for ten years. Payments aremade annually, the first payment being due in two years’ time. What is the present value of the annuity ifthe annual effective interest rate stays at 10% over this period?[Answer: £55,859.70 (to nearest penny)]

32

1.6.5 Increasing annuities

Annuities where the payments are not equal are called varying annuities. In particular, an annuitywhich pays k units of money at the end of the kth time period (i.e., 1 unit of money at the end ofthe first time period, 2 units of money at the end of the second time period, and so on, up to nunits of money at the end of the nth time period) is called an increasing immediate annuity. Itspresent value is denoted (Ia)n and it can be shown that

(Ia)n = v + 2v2 + 3v3 + . . .+ nvn =an − nvn

i. (1.116)

Similarly, an annuity paying k units of money at the beginning of the kth time period for n timeperiods is an increasing annuity-due and has present value

(Ia)n = 1 + 2v + 3v2 + 3v3 + . . .+ nvn−1 = (1 + i)(Ia)n . (1.117)

Summary of 1.6

P.V. of annuity-due: an = 1−vn1−v

P.V. of immediate-annuity: an = vanP.V.s of deferred annuities: m|an = vman , m|an = vman

1.7 Annuities-certain: more variations

1.7.1 Annuities payable p-thly

Consider an annuity of one unit of money per unit time payable over n units of time in instalmentsof 1/p at p-thly intervals. In the case where the payments are made in arrears (so that the first one isdue one p-thly interval from now at time 1/p), we have an immediate annuity payable p-thly. Its

present value is denoted by the symbol a(p)n . By summing the present values of the n× p individual

payments we obtain

a(p)n =

1

pv1/p +

1

pv2/p + . . .+

1

pvnp/p (1.118)

=1

pv1/p

(1 + v1/p + . . .+ v(np−1)/p

)(1.119)

=1

pv1/p

1− vn

1− v1/p[using (1.104) with q = v1/p]. (1.120)

Obviously the p = 1 case reduces to the present value of an “ordinary” immediate annuity paidannually, as given by (1.105).

Example 1.7.1: Mobile phone contractSuppose you sign a mobile phone contract agreeing to pay £15 at the end of each month for the next twoyears. Assuming a constant AER of 2% p.a., what is the present value of the whole series of payments? (Inother words, what lump sum of money would you need to put in the bank now to cover all the future monthlypayments?)

SolutionTake 1 year as the basic time unit, then i = 0.02 and

v =1

1 + i=

1

1.02. (1.121)

33

The payments form an immediate annuity payable monthly (p = 12) at the rate of £180 per year. Hence therequired P.V. is given by

P.V. = £180× a(12)2

(1.122)

= £180× 1

12v1/12

1− v2

1− v1/12(1.123)

= £352.67 (to the nearest penny). (1.124)

As expected, this is slightly less than £360 because of the interest paid over the two years.

Exercise 1.7.1: *Mobile phone contract (alternative solution)An alternative solution for Example 1.7.1 is to choose 1 month as the basic time unit. Then i (the effectiveinterest rate per time unit) is given by (1 + 0.02)1/12 − 1 = 0.00165158 (to 8 d.p.) and

v =1

1 + i≈ 1

1.00165158. (1.125)

With 1 month as the basic time unit and v as given by (1.125) the required P.V. is

P.V. = £15× a24 . (1.126)

Check that this gives the same answer as (1.124), and that you understand why. [To avoid numerical errors,be careful not to round up the value for v given in (1.125).]

Now consider the same situation (an annuity of one unit of money per unit time payable p-thlyover n time units) but with the first payment due at time 0, i.e., payment in advance. In this casewe have an annuity-due payable p-thly whose P.V. is given by

a(p)n =

1

p

(1 + v1/p + . . .+ v(np−1)/p

)=

1

p

1− vn

1− v1/p. (1.127)

Analogously to the discussion at the end of Section 1.6 one can also consider annuities payable

p-thly deferred by m time units. It should be obvious that their P.V.s are given by m|a(p)n = vma(p)n

and m|a(p)n = vma(p)n . In particular, note that 1/p|a

(p)n = a

(p)n . (Why?)

One can also derive alternative formulae for the P.V.s of annuities payable p-thly which illustratethe relation to nominal rates of interest/discount. For example, start from (1.120) and use thatv1/p = e−δ/p [follows from Eq. (1.93)] to obtain

a(p)n =

1

pe−δ/p

1− vn

1− e−δ/p(1.128)

=1− vn

p(eδ/p − 1)(1.129)

=1− vn

i(p)[using (1.52)]. (1.130)

Exercise 1.7.2: Alternative formula for a(p)n

Show that

a(p)n =

1− vn

d(p). (1.131)

1.7.2 Annuities payable continuously

If payments are frequent they can be approximated by the theoretical construction of a continuousannuity as we discuss below.

34

Suppose payments are made continuously over n units of time at the rate of one unit of moneyper unit time. The present value of this payment stream is denoted by an . To evaluate it, we firstimagining partitioning each time unit into small subintervals of length 1/p. Then

an =

np∑k=1

{P.V. of payment in between t =

k − 1

pand t =

k

p

}(1.132)

If p is large, so that each subinterval is small, then we can approximate the continuous paymentbetween t = (k − 1)/p and t = k/p as a discrete payment of 1/p at t = k/p. Hence, for large p,we have,

an ≈np∑k=1

1

pvk/p = a

(p)n . (1.133)

The approximate relation an ≈ a(p)n becomes exact in the limit p → ∞ which gives one way of

calculating an :

an = limp→∞

a(p)n (1.134)

= limp→∞

1− vn

i(p)[using (1.130)] (1.135)

=1− vn

δ. [using the time indep. form of (1.31)]. (1.136)

Exercise 1.7.3: p→∞ of annuity-due

Show that taking limp→∞ a(p)n gives the same result as (1.136), and explain why (in words).

Example 1.7.2: Deferred perpetuitiesThe AER is 8% p.a.. Find the present value of a deferred annuity of £13,000 per year paid in perpetuity inthe following cases:(i) Payments are made monthly with the first payment in 6 months’ time.(ii) Payments are made continuously in time starting in 6 months’ time.

SolutionWe take the basic time unit to be one year so that i = 0.08 and

v =1

1.08. (1.137)

(i) Here we have a perpetuity-due payable 12-thly and deferred by half a time unit (6 months). Rememberthat the symbol a (with associated labels) always refers to an annuity of one unit of money per unit time sothat here the required P.V. (in pounds) is expressed as:

P.V. = 13000× 1/2|a(12)∞ (1.138)

= 13000v1/2 limn→∞

a(12)n (1.139)

= 13000v1/2 limn→∞

1

12

1− vn

1− v1/12(1.140)

=13000

12

v1/2

1− v1/12(1.141)

= 163061.8827 (to 4 d.p.). (1.142)

So the present value of the specified perpetuity is £163,061.88 (to the nearest penny).6

6Note that if you’ve specified that you’re working in pounds (as we did here above (1.138)), then you don’t needto include the £ sign in the intermediate calculations but you should always give units in the final answer.

35

(ii) Here we have a perpetuity payable continuously, again deferred by half a time unit (6 months). Therequired P.V. (in pounds) is given by

P.V. = 13000× 1/2|a∞ (1.143)

= 13000v1/2 limn→∞

an (1.144)

= 13000v1/2 limn→∞

1− vn

δ(1.145)

= 13000v1/2

δ(1.146)

= 13000v1/2

ln(1 + i)(1.147)

= 162540.1066 (to 4 d.p.). (1.148)

So the present value of the specified perpetuity is £162,540.11 (to the nearest penny).

1.7.3 Accumulated values

Until now we have discussed how to calculate the present value of an annuity at time 0. Supposethat instead, we are interested in the accumulated value (accumulation) at the end of the series ofpayments, i.e., at time n if it’s an annuity of term n. In fact, this is very simple to obtain from thecorresponding present value but does involve the introduction of yet another symbol...

To be specific consider an immediate annuity (of one unit of money per unit time) payablep-thly over n time units. The accumulated value at time n, after the last payment has been made,

is usually denoted by s(p)n . From the discussion at the beginning of Section 1.5 it follows that

s(p)n = (1 + i)na

(p)n , or a

(p)n = vns

(p)n . (1.149)

Of course, there is a similar relation between the present and accumulated values of an annuity-due,

s(p)n = (1 + i)na

(p)n , or a

(p)n = vns

(p)n , (1.150)

and between the present and accumulated values of a continuous annuity,

sn = (1 + i)nan , or an = vnsn , (1.151)

Don’t worry too much about remembering the s symbol. It’s much more important that youunderstand that the accumulated value of an annuity-certain, of term n, is always given by theassociated present value multiplied by (1 + i)n.

Summary of 1.7

P.V. of annuity-due payable p-thly: a(p)n = 1

p

[1−vn1−v1/p

]P.V. of immediate-annuity payable p-thly: a

(p)n = v1/pa

(p)n

P.V. of continuous annuity: an = 1−vnδ

Accumulated values of annuities: s(p)n = (1 + i)na

(p)n , s

(p)n = (1 + i)na

(p)n

36

1.8 Continuous cash flows (not examinable)

Continuously payable cash flows are also known as payment streams. They are a theoretical conceptbut sometimes a useful approximation, e.g., payments made daily or weekly can be consideredpractically continuous if we are interested in times on a scale of years. The cash flow can consist ofboth incoming and outgoing transactions and so it’s possible that the net cash flow ρ(t) is negative.

We define ρ(t) as the rate (per unit time) at which payment is made at time t, i.e.,

ρ(t) = limh→0+

{1

h× (amount paid over [t, t+ h])}. (1.152)

The present value of such a continuous payment stream over time interval [t1, t2] in the future isthen given by

P.V. of continuous cash flow =

∫ t2

t1

vtρ(t) dt. (1.153)

The integration in the case where ρ(t) = ρ is particularly simple:

P.V. of constant continuous cash flow =

∫ t2

t1

vtρ dt (1.154)

=

∫ t2

t1

e−δtρ dt (1.155)

=[−ρδe−δt

]t2t1

(1.156)

=ρ

δ(e−δt1 − e−δt2). (1.157)

Example 1.8.1: Linear cash flowConsider a continuous cash flow having a linear payment density of the form

ρ(t) =

{at for t1 ≤ t ≤ t20 otherwise

(1.158)

with a a time-independent constant. Find the present value of this cash flow at time t = 0.

Solution

P.V. =

∫ t2

t1

vtat dt (1.159)

= a

∫ t2

t1

e−δtt dt (1.160)

= a

{[t

(−1

δe−δt

)]t2t1

−∫ t2

t1

(−1

δe−δt

)dt

}[integration by parts] (1.161)

= a

{[−δte−δt − e−δt

δ2

]t2t1

}(1.162)

=a{(1 + δt1)e−δt1 − (1 + δt2)e−δt2}

δ2. (1.163)

Exercise 1.8.1: *Another derivation of the P.V. of a continuous annuityConsider a continuous cash flow between t1 = 0 and t2 = n with rate ρ = 1 per unit time. The present valueof such a payment stream is given by the integral in (1.154). Show that this gives the same expression foran as in (1.136).

37

t=0 t= 1p t= 2

p ... t= p−1p t=1 Time, t

(1) d

(2) d(p)

pd(p)

pd(p)

p . . . d(p)

p

(3) i(p)

pi(p)

p . . . i(p)

pi(p)

p Payments

(4) i

(5) ←− Continuous payment at rate δ −→

Table 1.1: Five equivalent ways of paying interest on 1 unit of money over [0, 1].

1.8.1 Continuous cash flow with variable force of interest

In fact, it is not very hard to extend this approach to treat also the case of a time-dependent forceof interest δ(t). Consider a cash flow at rate ρ(t) units of money per unit time.

Let us revisit (1.65). Since

1

A(0, t)×A(0, t) = 1,

the value at time 0 of 1 unit of money received at time t is

D(0, t) =1

A(0, t)= exp

(−∫ t

0δ(s)ds

).

The present value of the cash flow ρ(t) is therefore∫ t2

t1

ρ(t)D(t1, t)dt =

∫ t2

t1

ρ(t) exp

(−∫ t

0δ(s)ds

)dt. (1.164)

Exercise 1.8.2: *P.V.s with piecewise constant force of interestSuppose that the force of interest at time t years is given by

δ(t) =

{0.05 for t < 6

0.07 for t ≥ 6.(1.165)

Use (1.164) to determine the present value of a continuous payment stream at a (constant) rate of £1000p.a. for 10 years beginning at time 0.

[Answer: £7768.20]

For example, we can use this approach to confirm that various ways of paying interest on a loan(see Table 1.1) are equivalent.

Example 1.8.2: Equivalent ways of paying interestShow that a single payment of d at time t = 0 (entry (1) in Table 1.1) is equivalent to a single payment ofi at time t = 1 (entry (4) in the table) or a continuous payment at constant rate ρ(t) = δ over [0, 1] (entry(5) in the table).

SolutionThe P.V. of (1) is obvious,

P.V. of (1) = d, (1.166)

38

and the other two are easily calculated

P.V. of (4) = iv (1.167)

= d [using (1.75)], (1.168)

P.V. of (5) =δ

δ(1− e−δ) [using (1.157)] (1.169)

= d [again using (1.75)]. (1.170)

The three cash flows have the same P.V., therefore they are all equivalent.

Exercise 1.8.3: Equivalent ways of paying interestShow that entries (2) and (3) in Table 1.1 are also equivalent to the three methods of paying interest consideredin Example 1.8.2. [Hint: You will need to sum a geometric progression.]

Example 1.8.3: Increasing annuity payable continuouslyConsider a continuous annuity which has a constant rate of payment k (per unit time) throughout the kthtime period. The present value of such an annuity is denoted by (Ia)n ; show that it is given by

(Ia)n =an − nvn

δ. (1.171)

SolutionObviously the total P.V. can be expressed as a sum over the P.V.s for each time period so we have

(Ia)n =

n∑k=1

(∫ k

k−1kvt dt

)(1.172)

=

n∑k=1

k

δ

(e−δ(k−1) − e−δk

)[using (1.157)] (1.173)

=

∑n−1j=0 (j + 1)e−δj −

∑nk=1 ke

−δk

δ[using j = k − 1] (1.174)

=

∑n−1k=0(k + 1)e−δk −

∑n−1k=0 ke

−δk − ne−δn

δ[relabelling j as k] (1.175)

=

∑n−1k=0 e

−δk − ne−δn

δ(1.176)

=

∑n−1k=0 v

k − nvn

δ(1.177)

=an − nvn

δ. (1.178)

Exercise 1.8.4: *Spot the difference!Another form of increasing continuous annuity has a rate of payment t at time t (i.e., a linear paymentdensity). The present value of this variation is denoted by (I a)n ; show that it is given by

(I a)n =an − nvn

δ. (1.179)

[Hint: Consider Example 1.8.1]

Accumulated value of a continuous cash flow

Suppose that for a continuous time cash flow payments begin at time t1 and end at time t2 andassume time-dependent force of interest δ(t). The accumulated value of a continuous time cashflow ρ(t) at the time t2 is∫ t2

t1

ρ(t)A(t, t2)dt =

∫ t2

t1

ρ(t) exp

(∫ t2

tδ(s)ds

)dt.

39

1.9 Repayment of Loans

1.9.1 Schedule of payments