lecture 7: term structure models - bu personal websitespeople.bu.edu/sgilchri/teaching/ec 745 fall...

TRANSCRIPT

Lecture 7: Term Structure Models

Simon GilchristBoston Univerity and NBER

EC 745Fall, 2013

Bond basics

A zero-coupon n period bond is a claim to a sure payoff of 1 attime t+ n. The price is denoted P (n)

t and it satisfies therecursion:

P(n)t = Et

(Mt+1P

(n−1)t+1

),

P(0)t = 1.

We define the yield of a bond with maturity n at time t throughthe equation

P(n)t =

1(1 + Y

(n)t

)n ,i.e. it is the per period (e.g. per year) return that you get if youbuy a bond today and hold it until it matures.The holding period return is the return if you buy a bond ofmaturity n at time t and sell it back at time t+ 1 :

R(n)t+1 =

P(n−1)t+1

P(n)t

.

With p = log(P ), y = log(1 + Y ), and hpr = logR, we have

p(n)t = −ny(n)t ,

hpr(n)t+1 = p

(n−1)t+1 − p(n)t .

The forward rate is the rate at which you commit today toborrow/lend for one period, N periods from now:

1 + F(N→N+1)t =

P(N)t

P(N+1)t

.

orfn→n+1t = pnt − pn+1

t

Yield curve with iid stochastic discount factor

Suppose that {Mt+1} is iid. Then the yield curve is constant andflat, i.e. y(n)t = yt = y for all t, n.

Proof: Let p = E(M). Start with n = 2 and showP

(n)t = Et

(Mt+1P

(n−1)t+1

)= Et

(Mt+1p

n−1)

= p.pn−1 = pn.

If P (n)t = pn, then y(n)t = y with 1 + y = 1

P .

Implication: if the short-rate is constant, all yields are constant,and hence bonds of all maturities have risk-free returns (Whereasin general, only the one-period bond has a return that isrisk-free.)

Nominal discount factors

Arbitrage:Ptqt

= Et

(Mt+1

Dnomt

qt+1

),

where qt =price index (CPI). Hence, inflation is πt+1 = qt+1/qt.

Define a nominal SDF

Mnomt+1 =

Mt+1

πt+1,

The bond pricing recursion holds for nominal bonds using thisnominal SDF:

P(n)t = Et

(Mnomt+1 P

(n−1)t+1

).

Comovement

All yields (long and short) are highly correlated - they tend tomove up and down together a lot; more precisely, one can doprincipal components to find the factors which move yields.

The first, by far most important factor is the “level”: all yieldsmove up and down together; second, there is a “slope” effect i.e.long term yields and short term yields move in oppositedirection; last, there is a “curvature” effect i.e. the concavity ofthe yield curve changes somewhat.

Monthly Nominal Treasury Yields (1985:2013)

05

1015

1985m1 1990m1 1995m1 2000m1 2005m1 2010m1 2015m1date

treas03m treas02ytreas05y treas10y

Daily Nominal Treasury Yields (1996:2013)

02

46

8

01jan199601jan199801jan200001jan200201jan200401jan200601jan200801jan201001jan201201jan2014date

treas03m treas02ytreas05y treas10ytreas15y treas30y

Daily Forward Rates (1996:2013)

02

46

8

01jan199601jan199801jan200001jan200201jan200401jan200601jan200801jan201001jan201201jan2014date

ftreas02y1 ftreas04y1ftreas09y1

Term Spread

On average the yield curve is somewhat upward sloping; i.e. theyield on long-term bonds is larger than on short-term bonds.

The slope of the yield curve, i.e. the term spread measured as thedifference between a long rate (≥ 5 years) and a short rate (≤ 1year) is correlated with the business cycle: an inverted yieldcurve predicts a recession, and at the trough of the recession, theyield curve is steeply upward sloping.

Monthly Term Spreads (1985:2013)

-10

12

34

1985m1 1990m1 1995m1 2000m1 2005m1 2010m1 2015m1date

TS_10y_2y TS_10y_3m

Volatility

Long-term bond prices are fairly volatile; the std dev of the 10yreturn is about 8% per year, i.e. almost half that of stocks. Interms of yields, the std dev of yields as a function of maturity ishump-shaped.

n (years) E(hpr) s.e. σ(hpr)1 5.83 .42 2.832 6.15 .54 3.653 6.40 .69 4.664 6.40 .85 5.715 6.36 .98 6.58

Table1

Expectation hypothesis (EH)

The EH states that the expected log (holding period) returns onall bonds is the same:

Ethpr(n)t+1 = Ethpr

(1)t+1 = y

(1)t , alln ≥ 0.

The N-period (log) yield is the average of expected futureone-period (log) yields:

y(N)t =

1

NEt

(y(1)t + y

(1)t+1 + ...+ y

(1)t+N−1

).

The forward rate equals the expected future spot rate (in logs):

fN→N+1t = Et

(y(1)t+N

).

Weaker version of EH

A weaker form of the EH is that these relations hold “up to aconstant”, i.e.

Ethpr(n)t+1 = y

(1)t+1 + constant,

y(N)t =

1

NEt

(y(1)t + y

(1)t+1 + ...+ y

(1)t+N−1

)+ constant,

fN→N+1t = Et

(y(1)t+N

)+ constant,

where the constant may depend on maturity n but not on time t.

Key point: the EH is almost assuming risk-neutrality - expectedreturns should be the same on all assets. (It is not quite that,because it is in logs instead of levels.)

Implication and test of EH:

Under the EH, if the long-term yield is high today relative to theshort yield, it must be that the short yield will rise in the future,so that if you invest in short rate only every period you will endup getting the same return at the end.

In the data, the expectation hypothesis does not work very well:the expected return on bonds is forecastable,

Ethpr(n)t+1 − y

(1)t+1 = α+ βXt

i.e. there are times when investing in long-term bonds bringsexcess returns.

Intuition

One way to summarize the results is to go back to the exampleexplaining the EH – in the data, on average, when short < long,the short yield does not increase enough in the future, so there isa positive excess return to borrowing short term and buyinglong-term bonds.

More precisely, the variable Xt that researchers use to predictreturns on long-term bonds is usually based on current yields orforward rates. Fama and Bliss use the difference between theforward rate at time t+ n and the current short rate, to forecastthe maturity n bond excess return. Cochrane and Piazzesi findthat a particular combination of forward rates forecast allmaturities of excess bonds returns. (Refs: Fama and Bliss (1988),Campbell and Shiller (1991), Cochrane and Piazzesi (2005)).

Testing the EH

The expectation hypothesis is often tested through to thefollowing equation:

yn−1t+1 − ynt = α+ βn

(ynt − y1tn− 1

)+ εt+1.

The expectation hypothesis implies that βn = 1. In the data,βn < 1, often negative, and decreasing with the horizon n.

Table: Expectation Hypothesis Tests

n = 2 n = 3 n = 4 n = 5Slope Coefficients - 1961-1979

−1.03 −1.52 −1.55 −1.43[0.65] [0.71] [0.83] [0.96]

Slope Coefficients - 1988-20060.61 −0.13 −0.19 −0.21[0.89] [0.90] [0.97] [1.02]

Summing up

Just like for stocks, we need a model which explains:1 the mean return on long-term bonds, relative to short-term bonds,2 the volatility of long-term bond returns3 the variation over time in the expected returns.

A simple affine model:

Assume conditional log-normality of Mt+1 and Pnt then forn > 1

pnt = Et (mt+1 + pn−1,t+1) +1

2vart (mt+1 + pn−1,t+1)

andp1t = Etmt+1 +

1

2vart (mt+1)

Supposemt+1 = −xt + et+1

wherext+1 = (1− φ)µ+ φxt + vt+1

Also assumeet+1 = βvt+1 + ηt+1

where vt+1 and ηt+1 are iid uncorrelated.

Simplified version:

For simplicity set ηt+1 = 0 so that

mt+1 = −xt + βvt+1

(it only affects the level of the term structure). In this case mt+1

is an ARMA(1,1) (sum of AR1 and white noise).

Note if β = 1/φ we have

mt+1 = −xt+1

φ+

(1− φ)

φµ

which may be interpreted as renormalized consumption growth,hence a form of CARRA.

One period yield:

For the one period yield

y1t = −p1t

so

y1t = xt − β2σ2

2

Since short-rate inherits AR1 dynamics we can think of xt as theprocess for the short-rate process itself.

N period yield

Guess a solution of the form

−pnt = An +Bnxt

Since the yield on an n-period bond is

ynt = −pntn

we are guessing that the yield on any maturity is an affinefunction of xt.

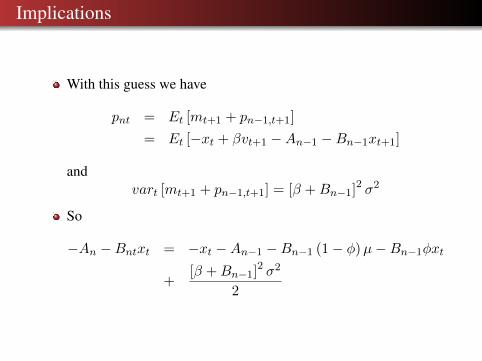

Implications

With this guess we have

pnt = Et [mt+1 + pn−1,t+1]

= Et [−xt + βvt+1 −An−1 −Bn−1xt+1]

andvart [mt+1 + pn−1,t+1] = [β +Bn−1]

2 σ2

So

−An −Bntxt = −xt −An−1 −Bn−1 (1− φ)µ−Bn−1φxt

+[β +Bn−1]

2 σ2

2

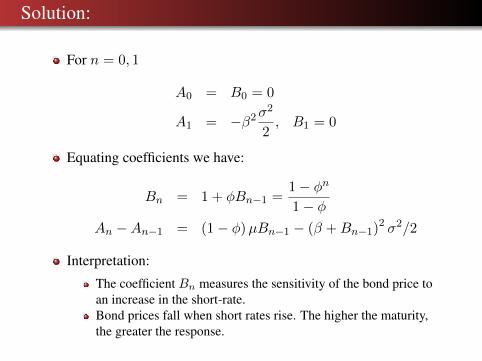

Solution:

For n = 0, 1

A0 = B0 = 0

A1 = −β2σ2

2, B1 = 0

Equating coefficients we have:

Bn = 1 + φBn−1 =1− φn

1− φAn −An−1 = (1− φ)µBn−1 − (β +Bn−1)

2 σ2/2

Interpretation:

The coefficient Bn measures the sensitivity of the bond price toan increase in the short-rate.Bond prices fall when short rates rise. The higher the maturity,the greater the response.

Expected excess holding period return:

The expected holding period return is

Etrn,t+1 = Etpn−1,t+1 − pn,t=

[− (1− φ)µBn−1 + (β +Bn−1)

2 σ2/2]

+ xt

so all expected holding period returns increase one for one withthe short-rate.The excess holding period return is defined as

Etrn,t+1 − y1t +vart (rn,t+1)

2= −covt (rn,t+1,mt+1)

Etrn,t+1 − y1t +vart (xt+1)

2= Bn−1covt (xt+1,mt+1)

This implies

Etrn,t+1 − y1t +B2n−1σ

2

2= −Bnβσ2

We can interpret Bnσ as the amount of risk for an n periodholding period return and βσ as the price of risk.

Interpretation:

Assume thatmt+1 = log δ − γ∆ct+1

thenγ (∆ct+1 − Et∆ct+1) = βvt+1

If β > 0 a shock to vt+1 represents positive news about futureconsumption growth which then follows a persistent AR1process. (i.e. β governs the covariance between consumptioninnovations and expected future consumption growth).

So if β > 0 a positive shock signals that future consumptiongrowth and hence interest rates will be high. A rise in expectedfuture interest rates implies a reduction in current bond prices.So bond returns covary negatively with current consumptiongrowth – they are therefore a good hedge and carry a negativerisk premium.

Forward rates:

The forward rate satisfies

fnt = pnt − pn+1,t

= −p1t + (Etpn,t+1 − pn+1,t + p1t)− (Etpn,t+1 − pnt)= y1t + Etrn+t,t+1 − y1t − (Etpn,t+1 − pnt)

wherepn,t+1 − pnt = −BnEt∆xt+1

This implies

fnt = µ−[β +

1− φn

1− φ

]2 σ22

+ φn (xt − u)

With this specification we can get rising, humped-shaped orinverted yield curves depending on xt.If xt = µ the yield curve is initially rising relatively steeplyowing to the squared term.

Conditional Heteroskedasticity

Cox-Ingersoll-Ross in discrete time:

−mt+1 = xt +√xtβvt+1

xt+1 = (1− φ)µ+ φxt +√xtvt+1

We now have

p1t = Etmt+1 = −xt(

1− β2σ2

2

)so A1 = 0, B1 =

(1− β2 σ2

2

)and the recursion

Bn = 1 + φBn−1 − (β +Bn−1)2 σ

2

2An −An−1 = (1− φ)µBn−1

In the limit Bn solves a quadratic but is roughly equal to 11−φ as

before so it is positive and increasing in n.

Expected excess log bond return:

We now have

Etrn,t+1 − y1t +B2n−1

vart (xt+1)

2= Bn−1covt (xt+1,mt+1)

Etrn,t+1 − y1t +B2n−1xt

σ2

2= −Bn−1xtβσ2

We can again interpret Bn−1√xtσ as the amount of risk and

β√xtσ as the price of risk.

Thus, in this model, the price of risk rises with the (square root)of the level of interest rates.

Ten-year term premium vs ten minus 2 year term spread

-10

12

34

01jan199601jan199801jan200001jan200201jan200401jan200601jan200801jan201001jan201201jan2014date

term_premium term_spread

Ten-year term premium vs ten-year treasury yield

02

46

8treas10y

-10

12

term_premium

01jan199601jan199801jan200001jan200201jan200401jan200601jan200801jan201001jan201201jan2014date

term_premium treas10y