lecture 10: personal income tax discounted cash flow, section 3.1 © 2004, lutz kruschwitz and...

TRANSCRIPT

Lecture 10: Personal Income Tax

Discounted Cash Flow, Section 3.1

© 2004, Lutz Kruschwitz and

Andreas Löffler

3.1.1 The pros and cons

Why should we incorporate income tax?

German CPAs take personal tax into account since 1997.

CPAs in other countries are more hesitant.

3.1.1 Unlevered and levered

In Chapter 2 (Corporate Income Tax) we used the termsunlevered = not indebted

levered = indebted

This was appropriate because– high tax burden comes with low debt,– low tax burden comes with high debt

3.1.1 Continue former designation?

Now we are looking at personal income tax. Does the tax burden depend on indebtness?

No, if riskless interest and dividends are taxed with the same rate (which we will assume for the moment): the personal tax of the shareholder - given the distribution - is independent of debt.

3.1.1 New interpretation

Our focus lies on the tax burden of shareholders. And here we notice that

– high tax burden comes with full distribution,– low tax burden comes with partial distribution.

Corporate Income Tax

(Chapter 2)

Personal Income Tax

(Chapter 3)

unlevered

levered

not indebted

Indebted

full distribution

partial distribution

Debt and leverage

The levered and the unlevered firm in this chapter are completely self–financed (no debt):

That is to say that the unlevered firms of Chapters 2 and 3 are the same, but not the levered companies.

for levered and unlevered company we assume

Corporate income tax

Personal income tax

no retention (full distribution)

no debt (self–financed)

3.1.1 New interpretation of variables

Market value with full distribution

Market value with partial distribution

Free cash flow with full distribution

Free cash flow with partial distribution

Personal income tax with full distribution

Personal income tax with partial distribution

ut

lt

ut

lt

ut

lt

V

V

FCF

FCF

Tax

Tax

Positive dividends

With corporate income tax negative cash flows meant nothing more than that the financiers infused the company with further equity. If this was no longer possible we spoke of default.

But negative payments do not make any sense in the case of dividends. Thus we will presuppose that the levered and the unlevered firm’s cash flows are large enough so that the dividends cannot turn negative.

3.1.2 Unlevered and levered firms

To value a levered firm we need to value an unlevered firm.

This remains true in the case of firm income tax as well as in

the case of personal income tax.

Definition of cost of capital of unlevered firm as in Chapter 2, i.e.

1 1, 1.

u ut t tE u

t ut

E FCF Vk

V

F

3.1.2 Valuation equation, weak autoregressive cash flows

Then, with deterministic cost of capital (without proof)

Again we assume

, ,1 1

.(1 )...(1 )

uT

s tut E u E u

s t t s

E FCFV

k k

F

1 1u u

t t t tE FCF g FCFF

3.1.3 Personal income tax

The characteristics of personal income tax are:– The tax subject is a shareholder and creditor,– The tax base are for

shareholder: dividends, business income,… (capital repayment exempt from taxes)

Debt holder: interest.

– The tax rate is identical for dividends ( ) and interest ( ).D I

3.1.3 From gross cash flow to tax base

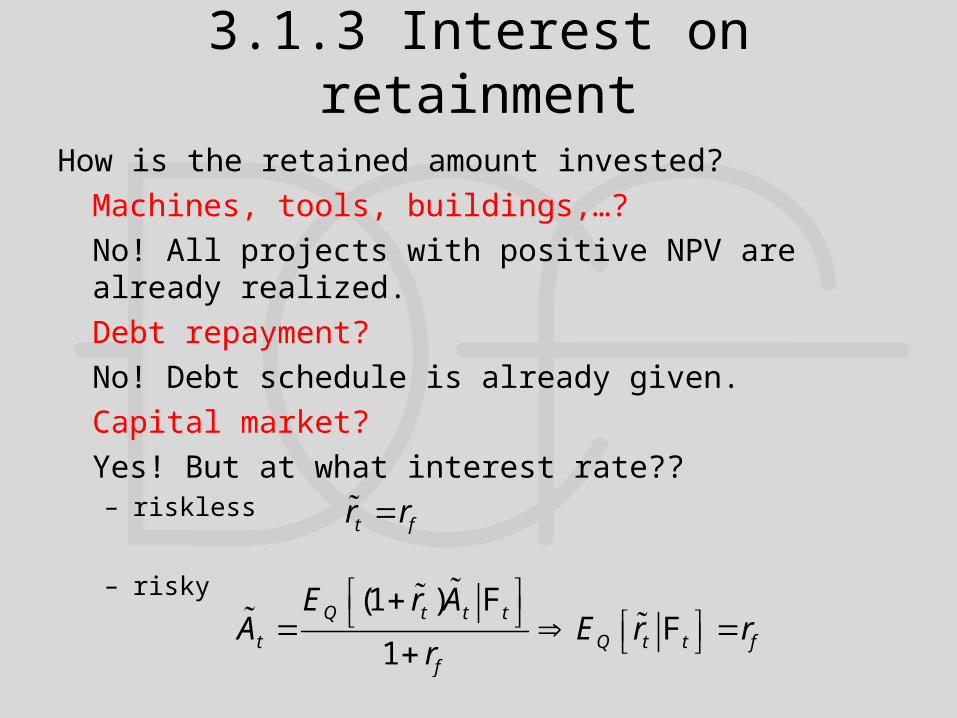

3.1.3 Interest on retainment

How is the retained amount invested?

Machines, tools, buildings,…?

No! All projects with positive NPV are already realized.

Debt repayment?

No! Debt schedule is already given.

Capital market?

Yes! But at what interest rate??– riskless

– riskyt fr r

FF

(1 )

1

Q t t t

t Q t t ff

E r AA E r r

r

3.1.3 Tax equations

The tax equations are

for the unlevered company

for the levered company

The tax payments of levered company can be written as

( )u Dt t tTax GCF Inv

1 1(1 ) .l D

t t t t t tTax GCF Inv A r A

1 1(1 ) .l u D

t t t t tTax Tax A r A

3.1.3 Tax difference of levered firm

We realize that the tax payments of the levered firm differ.

Although unlevered and levered firms have identical- gross cash flows,- stock depreciation and appreciation,- debt schedule and- investments

they differ in- dividends and- tax payments.

3.1.3 Tax advantage of levered firm

If dividends are not fully distributed, the levered firm pays less personal income taxes than the unlevered firm. There is a (personal income) tax shield for the levered firm – justifying our designation. The tax differences are

and after taking expectations

1 1

1 1

(1 )

1 (1 )

l u l ut t t t t t t

Dt t t

FCF FCF A r A Tax Tax

A r A

1 1 11 .l u

Q t t t f t Q t tE FCF FCF r A E AF F

1 1 1(1 ) 1 (1 )l u D D

Q t t t f t Q t tE FCF FCF r A E AF F

3.1.4 Remember: fundamental theorem

What is the fundamental theorem without any tax?

If capital markets are free of arbitrage, risk-neutral

probabilities Q exist such that

What changed with firm income tax?

Only payments were affected

1

.1

Q t t

tf

E XV

r

F

1tX

3.1.4 Fundamental theorem with firm income taxes

What changes will there be with personal income tax? Both payments and interest will be affected.

But how?! We do not prove here that

holds.

1tX

fr

1 1

11

Q t t t

It

f

E FCF VV

r

F

3.1.4 Gordon-Shapiro again

Gordon-Shapiro with personal income tax,

Cost of equity of unlevered firm is suitable as discount rates,

Remark: Cost of equity after income tax!

.u

u tt u

t

FCFV

d

, ,1

.(1 )...(1 )1 1

u uQ s t s t

s t E u E uI

t sf

E FCF E FCF

k kr

F F

,E uk

3.1.5 Differences in levered and unlevered firms

We know that the levered firm pays less taxes than the unlevered. But what is the value of this tax shield? And what does this value depend upon?

To this end we will assume that the last

retainment at 1, . . 0.TT i e A

3.1.5 Market values

The market value of the unlevered firm is

The market value of the levered firm is

1.

1 1 1 1

u uQ t t Q T tu

t T tI If f

E FCF E FCFV

r r

F F

1.

1 1 1 1

l lQ t t Q T tl

t T tI If f

E FCF E FCFV

r r

F F

3.1.5 Difference of market values

From both equations

1 1 2

2

2 1

2

1

1

(1 ) (1 ) (1 ) 1

1 1 1 1

(1 ) 1

1 1

(1 ) 1.

1 1

D DQ f t t t Q f t t tl u

t t I If f

DQ f T T t

T tI

f

DQ f T t

T tI

f

E r A A E r A AV V

r r

E r A A

r

E r A

r

F F

F

F0

TA

Which gives

3.1.5 Difference of market values (continued)

1 1

2

(1 )(1 )

1 1

(1 ) (1 ).

1 1 1 1

I Df Q t tl u D

t t t If

I D I Df Q t t f Q T t

T tI I

f f

r E AV V A

r

r E A r E A

r r

F

F F

3.1.5 Value of tax shieldCompare this to the firm income tax:

Although a different economic story, a similar formal structure! Only replaces

1.

1 1

f Q t t f Q T tl ut t T t

f f

r E D r E DV V

r r

F F

(1 )I Df tr A

f tr D

3.1.5 General procedure

We proceed as in Chapter 2:

1.We formulate different distribution policies.

2.We modify the main valuation equation with this distribution.

3.1.5 Different retainment policies

With firm income tax the debt schedule was important,

with personal income tax the retainment schedule is

important. We will look at

1. retainment based on cash flows,

2. retainment based on dividends,

3. retainment based on market values.

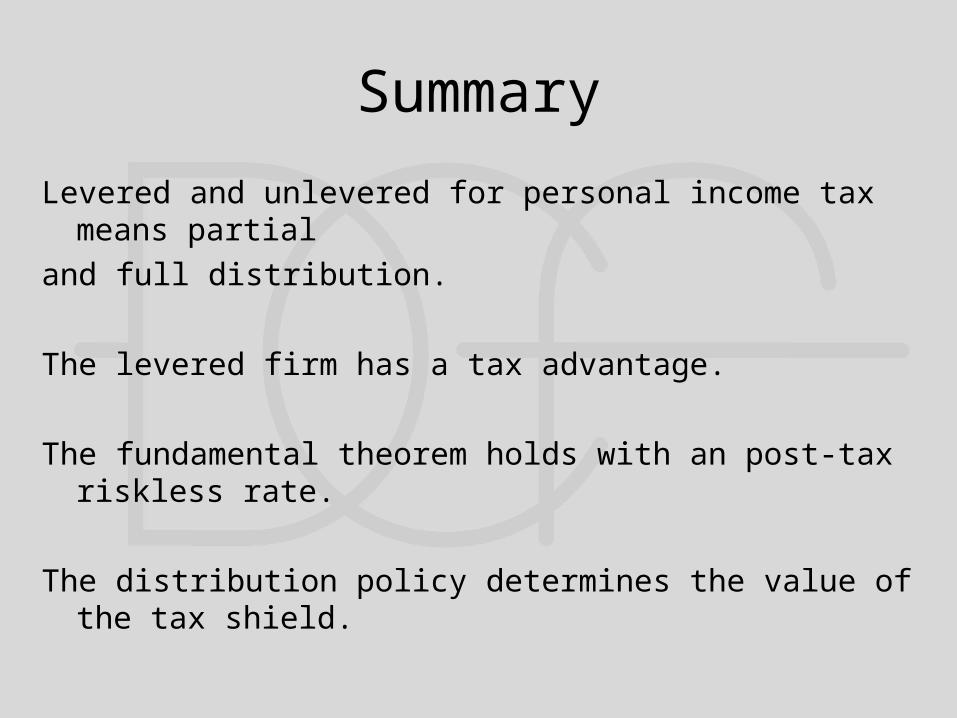

Summary

Levered and unlevered for personal income tax means partial

and full distribution.

The levered firm has a tax advantage.

The fundamental theorem holds with an post-tax riskless rate.

The distribution policy determines the value of the tax shield.