lecture 1 the great depression - post-crash … · creation. bubbles, panics and crashes 22 . temin...

TRANSCRIPT

Bubbles, Panics and Crashes: An Introduction to Alternative Theories of Economic Crisis

Dr. Sakir Devrim Yilmaz

Economics

University of Manchester

Lecture 1

The Great Depression

Bubbles, Panics and Crashes 1

• Great Depression: The most severe crisis the industrial world has experienced thus far

• Different schools of economic thought have very different explanations about the fundamental reasons of the depression

• These can broadly be classified as • New-Keynesian/Monetarist Approach (Bernanke-Romer-Temin)

• Keynesian-Demand Side Approach (Keynes!)

• Credit Bubble - Post-Keynesian Approach (Kindleberger, Minsky, Eichengreen to some extent) Bubbles, Panics and Crashes 2

• Austrian Business Cycle Theory (Mises, Robbins, Rothbard)

• Major Technological Bubble (Perez)

What happened? • 29 October 1929 (Black Tuesday) – The famous Wall

Street crash • Subsequent fall in income and prices that lasts over

four years in the U.S • Unemployment surging to 25% in the U.S, similar

figures in Europe and Britain. • Food riots break out in 1931, as well as deportation of

foreign workers from the U.S • By 1933, over 35% of the 30000+ banks in the U.S had

closed.

Bubbles, Panics and Crashes 3

Bubbles, Panics and Crashes http://www.nydailynews.com 4

Bubbles, Panics and Crashes 5

Bubbles, Panics and Crashes 6

Bubbles, Panics and Crashes 7

Bubbles, Panics and Crashes 8

Bubbles, Panics and Crashes 9

Bubbles, Panics and Crashes 10

Bubbles, Panics and Crashes 11

Bubbles, Panics and Crashes 12

Vernon (1993)

Bubbles, Panics and Crashes 13

Bubbles, Panics and Crashes 14

Why did it happen? • There is not only a single explanation, rather a

combination of several forces at work • Let us start with some data for the period before

the Depression and major events leading to the depression.

• In any analysis of a credit boom a good indicator as a starting point is the ratio of private credit to GDP.

• Japan, U.K and U.S have experienced significant increases in this. (Sounds familiar?)

Bubbles, Panics and Crashes 15

Eichengreen (2004)

Bubbles, Panics and Crashes 16

Bubbles, Panics and Crashes 17

• A rapid expansion of new technologies such as radio and employment of mass production techniques (Fordism-Taylorism) creating opportunities of high profits for companies.

• Particularly in the U.S, a real estate boom, beginning from 1925 and peaking in 1929, had developed.

• This was accompanied by a stock market bubble in the same period, and a surge in durable goods demand/production financed by credit.

• One reason suggested for the emergence of the credit boom in the U.S is the large gold reserves accumulated by the U.S during the First World War (gold standard era) Bubbles, Panics and Crashes 18

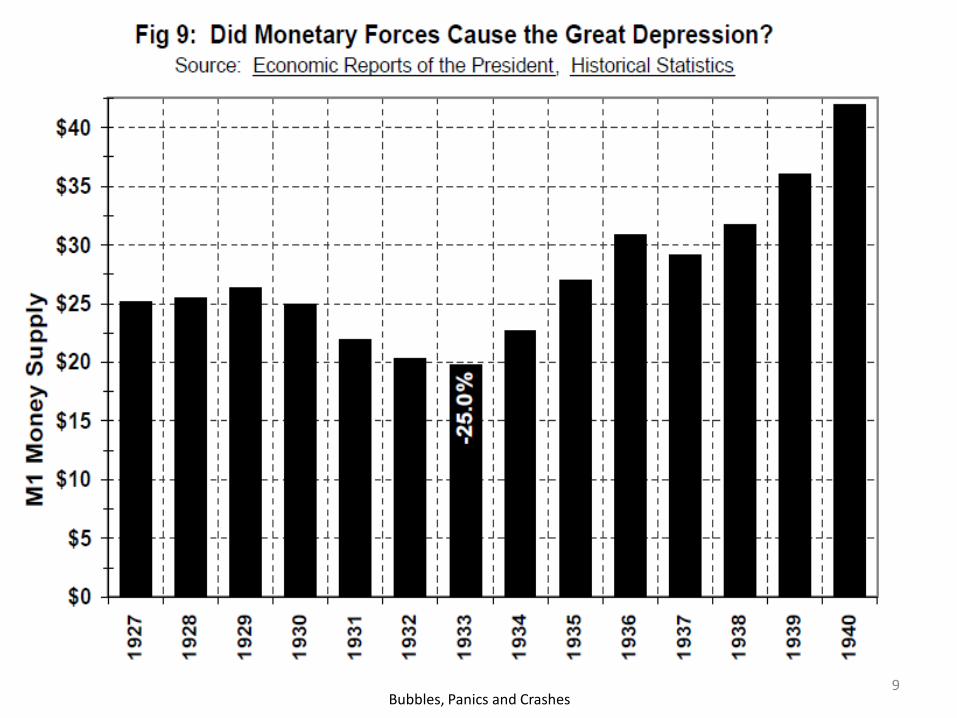

• Rothbard (1963) provides the data for U.S money supply and deposits/loans for 1921-1929

• There is a significant increase in the money supply due to the increase in lending in the U.S in this period.

• Another important indicator is the difference between total dollar claims and the federal reserve banks. The mass difference shows the amount of credit created by the banks (henceforth money) but not backed by gold. (Remember this, a similar story is going to come up in the Credit Crunch)

• This refutes the argument that the surge in money supply was mainly due to massive inflows of gold to U.S

Bubbles, Panics and Crashes 19

Rothbard (1963)

Bubbles, Panics and Crashes 20

Bubbles, Panics and Crashes 21

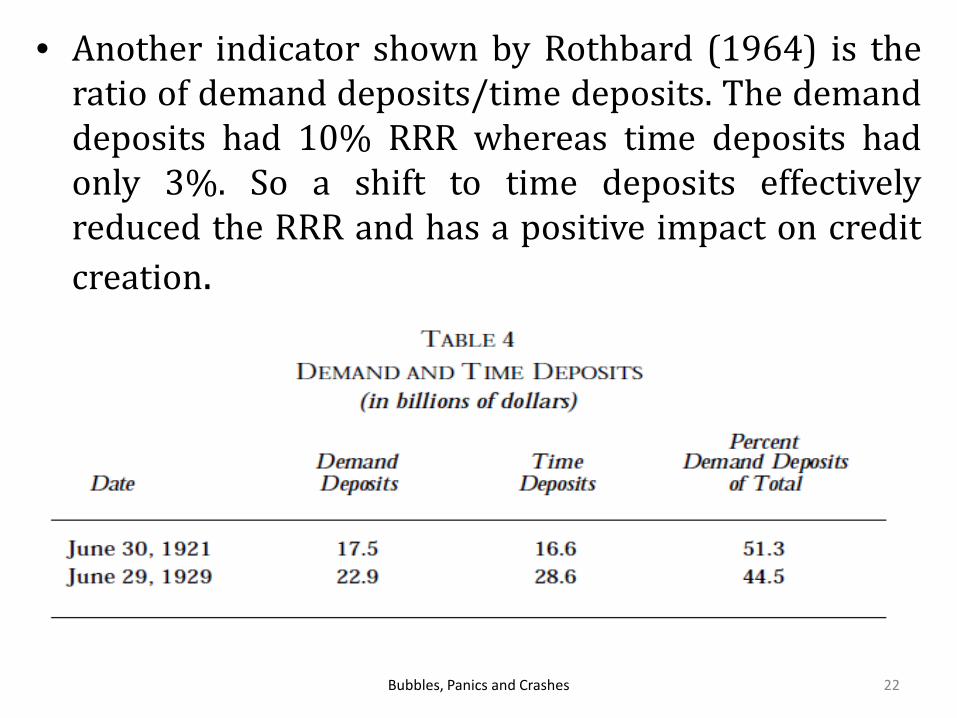

• Another indicator shown by Rothbard (1964) is the ratio of demand deposits/time deposits. The demand deposits had 10% RRR whereas time deposits had only 3%. So a shift to time deposits effectively reduced the RRR and has a positive impact on credit creation.

Bubbles, Panics and Crashes 22

Temin (1993)

Bubbles, Panics and Crashes 23

• Eichengreen (2004) also develops a composite indicator that shows signs of credit boom.

• As usual, excessive credit creation and financial innovation fuelled a stock market boom in the U.S, as well as several other categories of assets experiencing large price increases (See Galbraith 1972 for a detailed presentation this view)

• Private investors were drawn to the market and engaged in speculation though leveraging.

• Large capital gains especially in 1927 and 1928 create the impression that stock prices can “only” go up! (Familiar?)

Bubbles, Panics and Crashes 24

•Leverage: Total Assets/Equity Consider a household first Suppose the household has put an upfront payment (equity) of 10K for a house, and has got a mortgage worth of 90K, where the house is worth 100K. The leverage of this household would be 100/10 = 10. The balance sheet would look like:

Bubbles, Panics and Crashes 25

What does this imply? • Assume a 1% change in the value of asset held and

the price of the house increases to 101 • Net Return on Investment: 11/10 = 10% • So a 1% increase in asset prices leads to a 10%

return on initial investment • This is precisely because leverage is equal to 10. • Remember that it is the downturn (or fall in asset

prices) when leverage is lethal. • Any idea about how leveraged commercial and

investment banks were before the Credit Crunch? Bubbles, Panics and Crashes 26

Bubbles, Panics and Crashes 27

Bubbles, Panics and Crashes 28

• Leverage now falls to 101/11 = 9.18. If the investor wants to keep leverage constant at the initial value of 10, Assets/Equity = 10 must hold. (101+D)/11 = 10 must hold, which gives D = 9. So the investor borrows 9$ to buy more securities. Final balance sheet looks like:

Bubbles, Panics and Crashes 29

• Therefore, in an environment of rising asset prices and leverage, an investor will borrow increasing amounts of debt if he/she targets a constant leverage.

• However, this also implies that enormous adjustments to the existing debt stock need to be made when asset prices are falling (Consider the opposite case: a 1$ fall in the price of the security will require a liquidation of 9$ of debt to keep leverage constant)

• Do you think investors keep a constant leverage ratio during a fall in asset prices? What would happen if they were reducing leverage during downturns?

Bubbles, Panics and Crashes 30

• Households could leverage up to 10:1 to buy stocks before the crash of October 1929.

• The highly leveraged households speculate on further increases in stock prices with borrowed funds.

• As speculation accelerated, P/E ratios did not matter any more, as individual investors sought capital gains through equity price increases.

• Eventually, the stock market crashes, leading to defaulting loans, bank runs and massive deflation and unemployment. (Keep in mind this does not mean that stock market crash is the reason for the depression)

Bubbles, Panics and Crashes 31

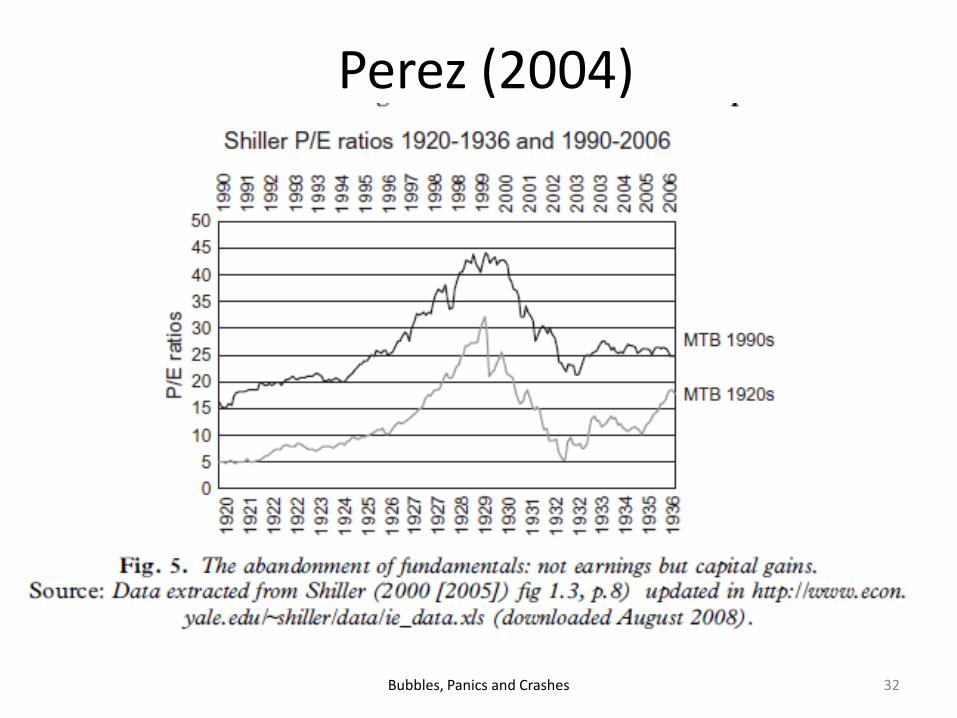

Perez (2004)

Bubbles, Panics and Crashes 32

• Another important factor in the Great Depression is the Gold Standard, especially according to the mainstream and (post) Keynesian view .

• Abolished during WW1 years, the gold standard was re-established in 1917.

• Under the gold standard, the exchange rates were fixed, and participating countries currencies were fully convertible to gold at these fixed rates.

• The money created by Central Banks had to be backed by gold. This meant that currencies would be exchanged with gold by the Central Bank upon request.

Bubbles, Panics and Crashes 33

• In theory, just like any other fixed exchange rate regime, this eliminates the FX risk for private investors, as the exchange rate is fixed.

• However, the interwar-era gold standard has the problems of fixed exchange rate regimes.

• Consider a country with a fixed exchange rate regime that experiences massive capital inflows. What happens to real exchange rates, trade balance, current account balance?

Bubbles, Panics and Crashes 34

• Capital Inflows CB Sterilization of FX Increase in Domestic Money Supply Increase in Domestic Demand Inflation Real Exchange Rate Appreciation Trade Deficit Current Account Deficit

• How do these episodes end? • Literature on sudden stops discusses fixed

exchange rate mechanisms and the recessions that follow such episodes.

• When investors feel that CB cannot defend the fixed exchange rate, there’s an attack on domestic currency

Bubbles, Panics and Crashes 35

• Foreign investors liquidate their domestic currency assets and ask for FX to leave the country. Coupled with domestic flight to FX, the Central Bank cannot defend the peg if it does not have sufficient FX reserves devaluation.

• The gold standard works precisely the same way. Gold is the FX, as the value of the currency is fixed in terms of gold.

• So private investors can ask for gold at any time and ship it abroad. Therefore, if the CB printed too much money, private investors could convert these banknotes to gold and leave. Thus, there’s a downward pressure on inflationary policies.

Bubbles, Panics and Crashes 36

• However, unlike fixed exchange rates with fiat money, this also had an equilibrating role.

• If a country run trade deficits, the exporters to this country would exchange the dollars they get with gold, and take them abroad. This would reduce the gold reserves, and reduce the money supply domestically. So a continuous trade deficit meant an eventual depletion of gold reserves.

• The reduction in the domestic money supply, however, reduces domestic demand, prices fall, and the country regains competitiveness.

• Deflation as an in-built equilibrating mechanism rather than devaluation

Bubbles, Panics and Crashes 37

• Further, fixed exchange rates under a Gold standard implies that an individual central bank has to follow similar policies to foreign central banks (particularly when foreign banks raise interest rates) since otherwise they would observe a depletion of their gold reserves.

• This created a transmission mechanism which helped spread the depression among the industrial countries

Bubbles, Panics and Crashes 38

Fisher (1933) • Debt-Deflation theory of Depressions • Fisher argues only when misallocations in prices,

or overproduction/underconsumption coincides with a large overhang of debt, we experience depressions

• Mild Gloom and Confidence Shock Debt Liquidation Distress Selling More Gloom Fall in security prices More Liquidation

• Fall in Commodity Prices Rise in Real Interest Rates and Real Value of Debt More Pessimism and Distress Selling More Liquidation

Bubbles, Panics and Crashes 39

Rothbard (1963)

Bubbles, Panics and Crashes 40

• Ben Bernanke on deflation http://www.bis.org/review/r021126d.pdf • Deflation is a general decline in price level (be careful

here, not a decline in prices in a single market) • The basic reason for a deflationary spiral is a collapse in

aggregate demand due to massive debt overhang. (Fisher’s debt deflation theory)

• In a deflationary period, one of the basic problems is that interest rates may be reduced to zero, and hit a lower bound

• However, even in such a case, the real interest rate will be positive (depending on the degree of deflation)

Bubbles, Panics and Crashes 41

• When interest rates hit zero, the CB runs out of conventional ammunition to affect aggregate demand

• In general, this is referred as a “liquidity trap”, as the positive impact of lowering the interest rates on investment and consumption disappears. In such a case, there is a danger that increasing money supply will directly lead to inflation.

• Deflation harms the debtors as the real value of debt goes up, and favours the creditors.

• The Central Bank should do all it can to prevent falling into a deflationary spiral

Bubbles, Panics and Crashes 42

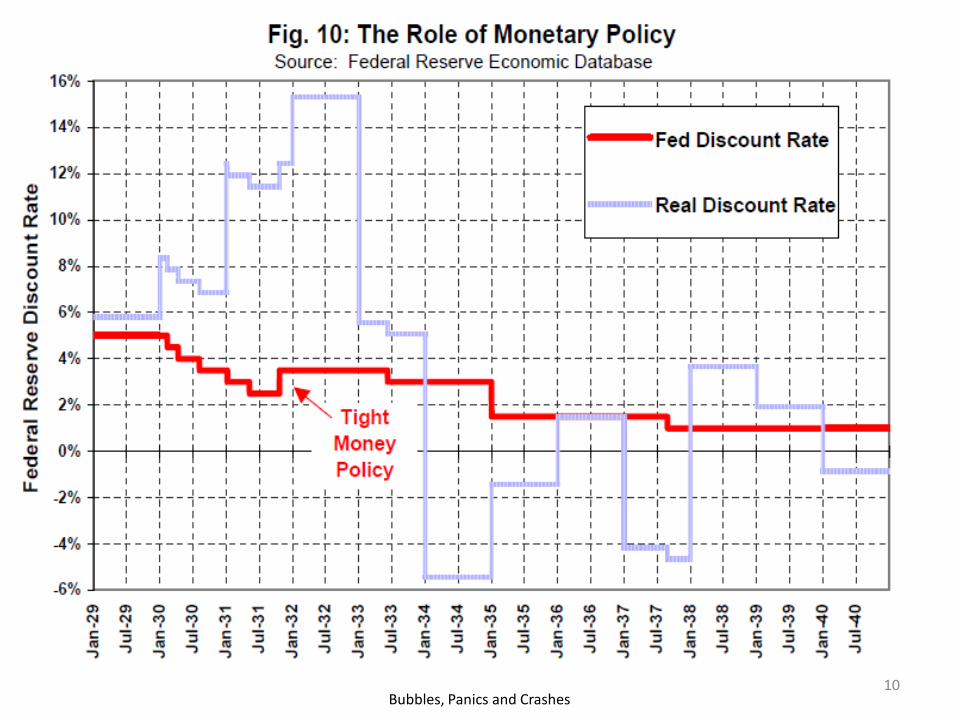

• Bernanke’s views stem from his interpretation of the Great Depression. According to this monetarist view (first expressed by Friedman and Schwartz), the major reason of the Great Depression is the mistake in monetary policy

• In particular, their diagnosis is that monetary policy was not expansionary enough.

• Friedman and Schwartz identify four major mistakes during the Great Depression, with which Bernanke fully agrees.

Bubbles, Panics and Crashes 43

• The first one was to raise the interest rates in 1928 in order to curb speculation.

• The second one was to defend the speculative attack on the dollar in 1931 by raising interest rates in order to make dollar more attractive to investors. This made on ongoing depression even worse, and lengthened the recovery period.

• The third mistake was to refuse to ease monetary policy in 1932, arguing that the interest rates were already low, and monetary policy was eased enough.

• Fourth, the FED neglected the problems in U.S banking sector, and did not act to stop bank runs.

Bubbles, Panics and Crashes 44

• Therefore, in short, the monetarist perspective claims that inadequate contractionary monetary policy was what led to the Great Depression.

• On the other hand, Bernanke and Gertler (2002) argue that the best response of the CB to asset price bubbles is not to respond, as long as the bubble does not affect expected inflation.

• In line with this perspective, it is no surprise that the FED did not try to prick the asset bubble in early 2000s. However, contrary to these arguments, FED raised the interest rates to try to contain the bubble after 2004 (We will talk more on this when we are covering credit crunch).

Bubbles, Panics and Crashes 45

Recovery Policies • Keynesian ideas played an important role in

the recovery from the Great Depression • Although Keynes’s General Theory was

published in 1936, the idea of implementing an expansionary fiscal policy as a solution to the depression had been proposed by Keynes (and others) in the early years of the depression.

• Roosevelt’s Significance and the New Deal • 3-day Bank Holiday in 1933 in order to solve

bankruptcy problems

Bubbles, Panics and Crashes 46

Bubbles, Panics and Crashes 47

• Introduction of Federal Deposit Insurance Corporation (FDIC) in 1933 in order to insure bank deposits.

• Keynesian policies: A massive increase in employment of unemployed by the public sector.

• Public Works Administration founded in 1933 to employ up to 4million unemployed.

• Works Progress Administration founded in 1935 and liquidated in 1943 to employ workers in public projects

• From 1934 to 1938, employment in federal public works programs equalled 13–15 % of the total number of workers unemployed, with work relief construction employment amounting to an additional 18–21 % of that number.

• National Industrial Recovery Act (1933): NIRA introduced industry codes that would ban child labour, end unfair business competition, limit the length of the workweek, make it easier for unions to organize workplaces, and regulate wages and prices.

• National Labour Relations Act (1935): Making labour organization in workplace easier.

• See Papadimitrou & Hansen (2009) “Lessons from the New Deal: Did the New Deal Prolong or Worsen the Great Depression?” for a very detailed discussion of these policies

Bubbles, Panics and Crashes 48

• Further expansionary policies before and during the Second World War in particularly Germany, U.S and Europe.

• See Temin (1990) “Socialism and Wages in the Recovery from the Great Depression in the U.S and Germany” for a comparison of German and U.S recovery from a neo-classical perspective

Bubbles, Panics and Crashes 49

Middleton (2010)

Bubbles, Panics and Crashes 50

Bubbles, Panics and Crashes 51