lease financing - stephanie...

TRANSCRIPT

1

Lease Financing

Finance II

6 November 2014

Stephanie Kessinger, Seungho Kang, Jess Forman Army-Baylor University Graduate Program in Health and Business Administration

Agenda

Introduction

Leasing Concepts

Lease Evaluation

Group Exercise

2

Leasing Basic Terminology

4

A lease is a contractual agreement between

a lessor and a lessee, that gives the lessee*

the right to use specific property, owned by

the lessor**, for a specified period of time.

* The user of the leased asset.

* The owner of the property, usually the manufacturer or a leasing company.

Leasing Basics

5

Largest group of leased equipment

involves:

Information technology

Transportation (trucks, aircraft, rail)

Construction

Agriculture

• Banks: the largest lessors in the leasing industry.

Independents: leasing companies whose primary business is to perform general finance for other companies.

Captive leasing companies: subsidiaries whose primary business is to perform leasing operations for the parent company (i.e., structure lease contracts for the parent companies and their customers).

Leasing Basics Lessors

6

Leasing Basics Who are the players?

7

Leasing Basics

Operating Leases

Service Leases

Financial Leases

Capital Lease

8

Types of Leases

“Service leases”

Lessor retains the risk and benefit of ownership.

Typically the lessor maintains and services the equipment

Not fully amortized (not sufficient for the lessor to recover the full cost of the equipment)

The period of a lease contract is shorter than the expected useful life of the leased asset.

The lessor recover all costs, either by lease renewal payments or by sale of the equipment

Operating Lease

9

Contains a cancellation clause

Return prior to the expiration of the lease if obsolete or no longer needed

Lease (rental) payments

Conventional terms (fixed payments)

Per procedure terms (volume)

The leased equipment is reported on the LESSOR’s balance sheet in Property, Plant and Equipment subsection entitled “Equipment Leased to Others" and record depreciation.

Operating Lease

10

Capital Lease

Lessee has to maintain and service equipment

No cancellation

A period of the useful life of the assets (Fully amortized)

A series of equal payments covering the full purchase price and a stated return on the lessor’s investment)

The ownership transfer from the lessor to the lessee.

Financial Leases

11

A special type of financial lease.

Often used with real estate.

The user who owns the asset sells it to another party and simultaneously executes an agreement to lease the property for a stated period under specific terms.

The lessee receives an immediate cash payment in exchange for a future series of lease payments that must be made to rent the use of the asset sold.

Financial Leases (sale and leaseback)

12

What is the difference between an operating lease and a financial lease?

What is a sale and leaseback?

How do per-procedure payment terms differ from conventional terms?

Review Questions

13

Tax

Financial Statements

Lease Effects

14

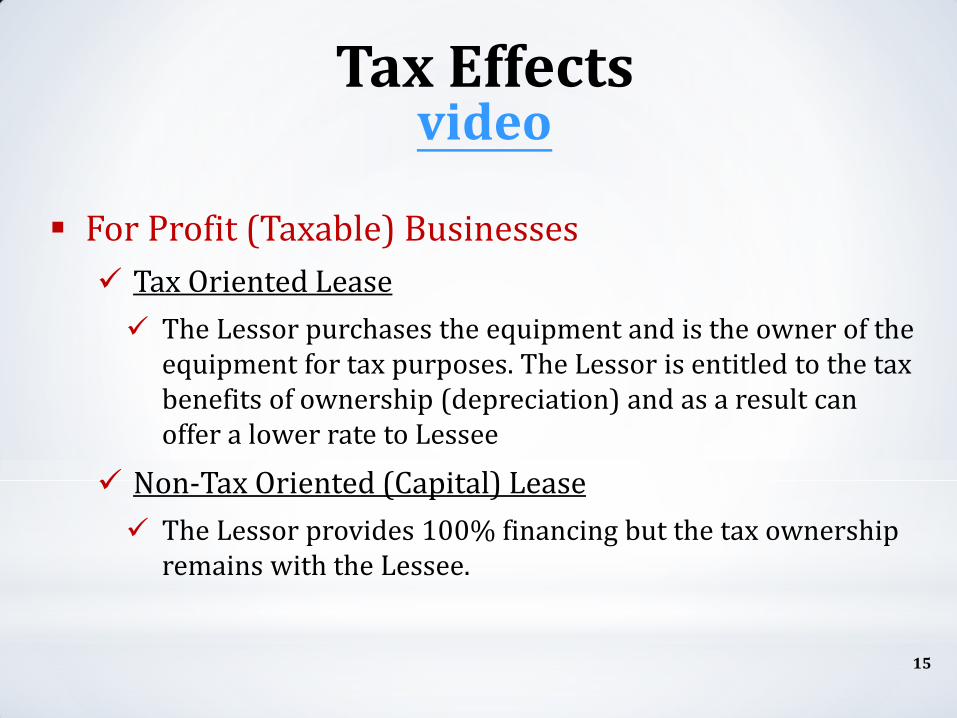

For Profit (Taxable) Businesses

Tax Oriented Lease

The Lessor purchases the equipment and is the owner of the equipment for tax purposes. The Lessor is entitled to the tax benefits of ownership (depreciation) and as a result can offer a lower rate to Lessee

Non-Tax Oriented (Capital) Lease

The Lessor provides 100% financing but the tax ownership remains with the Lessee.

15

Tax Effects video

Tax-oriented lease

the lessee’s lease payments are fully tax deductible.

Non-tax oriented lease

only the implied interest portion of each lease payment is deductible.

• The lessee obtains the tax depreciation benefits (the owner of the leased equipment)

16

Tax Effects: Lessee

Not-for-Profit (Tax-Exempt) Businesses

Not-for-profit firms do not obtain tax benefits from depreciation, the ownership of assets has no tax value.

When assets are owned by not-for-profit firms the depreciation tax benefit is lost, while when assets are leased the tax benefit is realized by the lessor rather than the lessee.

This realized benefit, in turn, can be shared with the lessee in the form of lower rental payments.

A special type of financial transaction has been created for not-for-profit businesses called a tax-exempt lease.

The implied interest portion of the lease payment is not classified as taxable income to the lessor (the return portion of the lessor’s payment is exempt from federal income taxes).

17

Tax Effects

Review Questions

1. What is the difference between a tax-oriented (guideline) lease and a non-tax-oriented lease?

2. Why should the IRS care about lease provisions?

3. What is a tax exempt lease?

18

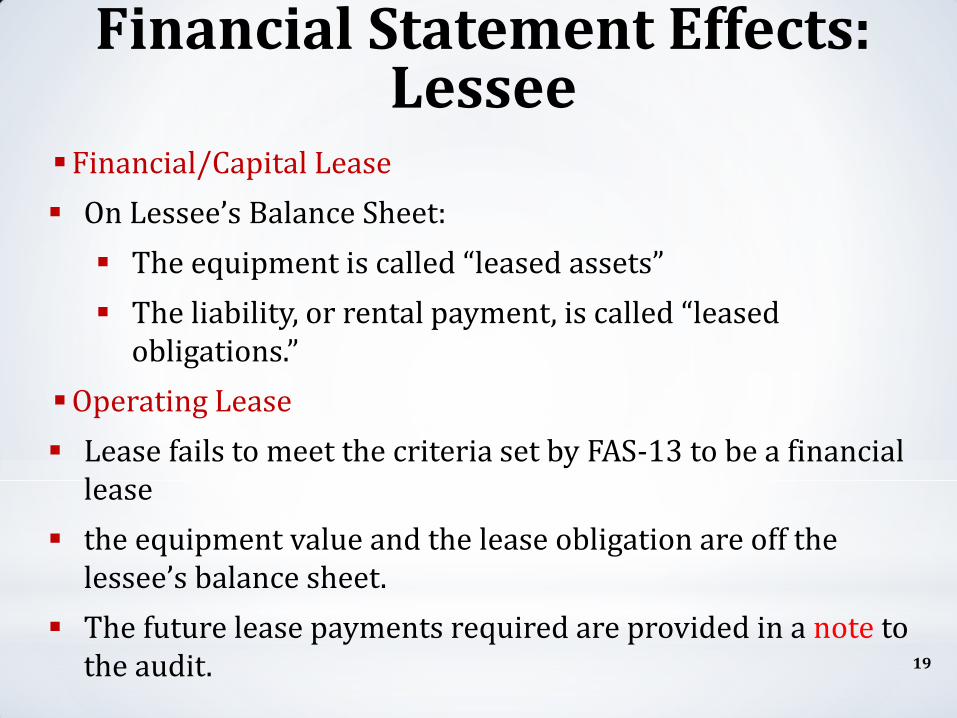

Financial/Capital Lease

On Lessee’s Balance Sheet:

The equipment is called “leased assets”

The liability, or rental payment, is called “leased obligations.”

Operating Lease

Lease fails to meet the criteria set by FAS-13 to be a financial lease

the equipment value and the lease obligation are off the lessee’s balance sheet.

The future lease payments required are provided in a note to the audit.

19

Financial Statement Effects: Lessee

Financial Lease Balance Sheet Example

20

1. Income Statement

• Expensed Item- Lease Expense Payment

• Part of annual depreciation expense (Financial/capital lease only)

2. Balance Sheet

• Only Financial/Capital lease, NOT operating lease

• Lease information found in the note section

3. Cash Flow Statement

• Part of Operating Expenses (cash outflow for Accounts payable)

• Not Specified or detailed

21

Financial Statement Effects: Lessee’s perspective

22

Financial Statement Effects: Lessee

B: Buying Company L: Leasing Company

Leasing Rules

23

Lease Accounting Rules

24

Businesses are required to disclose the existence of all leases longer than one year in the footnotes of their financial statements.

Generally leases are treated as debt for capital

structure purposes, and they have roughly the same effects as debt on the financial condition of the firm.

Strong footnote disclosure rules for non-

capitalized (operating) leases, are sufficient to ensure that no one will be fooled by lease financing.

Capital vs Operating Leases

25

Criteria Capital Lease (at least

one of the 4 criteria must be met)

Operating Lease (all 4 criteria must be met)

Automatic transfer of ownership at end of term

Yes No

Bargain purchase option

Yes No

Term ≥ 75% of useful life < 75% of useful life

Present value of rentals using the Incremental Borrowing Rate or the Implicit Lease Rate

≥ 90% of equipment cost

< 90% of equipment cost

It’s all about the Cash Flow. What’s best for your business at

the stage you’re in

Discussion

Under the Accounting rules (1977)

Capital (long term) leases: leased property is an asset

The PV of lease payments is a liability

Operating (short term) leases: The leased property is not on the balance sheet at all.

They are reported in the notes section of the financial statement

The most important proposed change is that leases would no longer be classified by accountants as operating or capital.

All leases would be accounted for in the same way on the balance sheet, with no differences between short-term and long-term leases

All leased property would be listed on the asset side as “right to use assets” and on the liability side as “lease liabilities”

The proposed rule change would eliminate operating leases as a source of off-balance-sheet financing

26

Discussion Questions

1. What do you think about the proposed change?

2. Why do you think it should be a different standard for capital and operating leases?

3. You’re a CEO, what impact will this change have on you?

4. Do you think investors are deceived? What impact would this change have on investors?

5. Would it make it easier for audits of financial statements?

6. Do you think the new rules would reduce/increase the amount of leasing that currently takes place?

7. When all factors are considered, should the change take place?

27

Think Big!

Compare Debt vs Lease

When LEASE is more

28

A loan is a financing agreement that allows a business to acquire, use, and own equipment.

A loan may require a down payment or a pledge of other assets for collateral. Under a loan financing, the borrower remains the owner of the equipment for tax and accounting purposes.

A lease allows a company to acquire and use equipment while conserving its cash flow and lines of credit.

Leasing also provides a new source of credit with the added benefit of being able to expense your lease payments in most instances. Leasing also can protect against equipment obsolescence when upgrades are included in a lease contract or the equipment is returned to the lessor at the end of the lease term. Termination clauses might be an option.

Secured Lending vs. Lease Financing

29

Conservation of cash Start-ups and Early Stage

Companies

100 Percent Financing

Preservation of Capital

Hedge Against Inflation

Improved Expense Planning and Business-Cycle Flexibility

Regular Technology Updates

Why would we lease equipment What’s our motivation?

30

Tax Considerations

Relationships with Equipment Experts

Obsolescence Management

Reliable Asset Management

Product and Service Bundling

Equipment Disposal

Think Big!

Benefits of Lease Finance

31

EQUIPMENT • Prefers to use equipment vs. ownership risks • Trade up to avoid obsolescence • Reduce cash requirements during life

BALANCE SHEET

CASH FLOW • Conserve cash for acquisitions • Match payments to seasonality • Sale/lease back to generate cash • Lowest monthly payment with minimal outlay

INCOME TAX •Deduct 100% of Lease Payments

There is no one-size-fits-all answer and there are advantages and disadvantages to both options. There are a few questions you should ask yourself that will help steer you in the right direction whether to lease or buy.

How often does the equipment need to be replaced?

How often does the technology change?

What costs are associated with the equipment?

Does the equipment need regular maintenance?

Will your staff need training?

Are additional parts or software required?

What is the financial state of your company? Do you have additional capital? Are you able to apply for credit?

Are you a new company? Are you well established?

Questions a manager should ask…

32

Think Big!

What are the strategic

implications of your decision?

Advantages

Continuous advancement of technology in the health care industry. Equipment becomes obsolete very fast.

Health care facilities are able to keep their budgets in line by leasing

Much cheaper to obtain this equipment regardless of whether you need new, used, refurbished, or re-manufactured ones.

Maintenance is covered

Flexible terms

Builds credit

You do not need collateral to get approved

Perhaps you can upgrade equipment at no extra cost at the end of the lease.

Ownership/responsibility belongs with the lessor.

Lease-to-own agreement (usually 10% of market value)

Can cancel the lease

Can decide if you want a short or long term lease.

Takes a short time to get approved.

Disadvantages

You do not own the equipment.

Dealing with lease contracts and negotiations.

It might not make financial sense

Healthcare Specific Leasing Advantages/Disadvantages

33

Think Big!

What is the current state of your company?

What are your goals?

Short & Long Term

What are the strategic implications of your decision?

Advantages

Perhaps lower long term cost

Tax deductions (depreciation)

Simplicity (not dealing with contracts)

Affordable items might make more sense to buy

Disadvantages

Unforeseen problems. You have responsibility

Equipment depreciation, become obsolete

Pricier up front $$$

More technology headaches/maintenance

Healthcare Buying Advantages/Disadvantages

34

Think Big!

Maybe buying makes more sense

https://www.pnc.com/en/corporate-and-institutional/topics/specialty-segments/healthcare/healthcare-videos.html

Healthcare Specific Look

PNC Equipment Finance Mark Tambussi

Senior VP PNC Equipment Finance

35

Lease Evaluation

Lease analysis is performed by both the lessee and lessor.

The lessee must determine whether to lease or buy the asset (a financing decision).

The lessor must determine whether or not to enter the lease (an investment decision).

We will focus on the lessee.

Dollar cost analysis

Percentage cost analysis

38

Lease vs Buy Analysis In 3 easy steps

1. Estimate the cash flows associated with borrowing and buying the asset

2. Estimate the cash flows associated with leasing the asset

3. Compare the two to determine which has the lower PV

Dollar Cost Analysis

Compare the dollar cost of owning to the cost of leasing

Lower cost of alternative is preferred

40

If the system is purchased:

System cost = $200,000

Bank loan rate before tax cost = 10%

A 4-year maintenance contract would cost $2,500 at the beginning of each year

Residual value (the value at the expiration of the lease) = $20,000

Other information:

Marginal tax rate = 40%

The system falls in to the MACRS five year class life

Dollar Cost Analysis

41

Assume that Nashville Radiology Group (a for-profit business) plans to acquire a new computer system for automating the Group’s clinical records as well as its accounting, billing, and collection process.

If the system is leased:

The group can obtain a 4-year lease that includes maintenance.

The rental payment would be $57,000 at the beginning of each year.

Lease Evaluation

42

MACRS Depreciation Rate

Dollar Cost Analysis (Cont.)

43

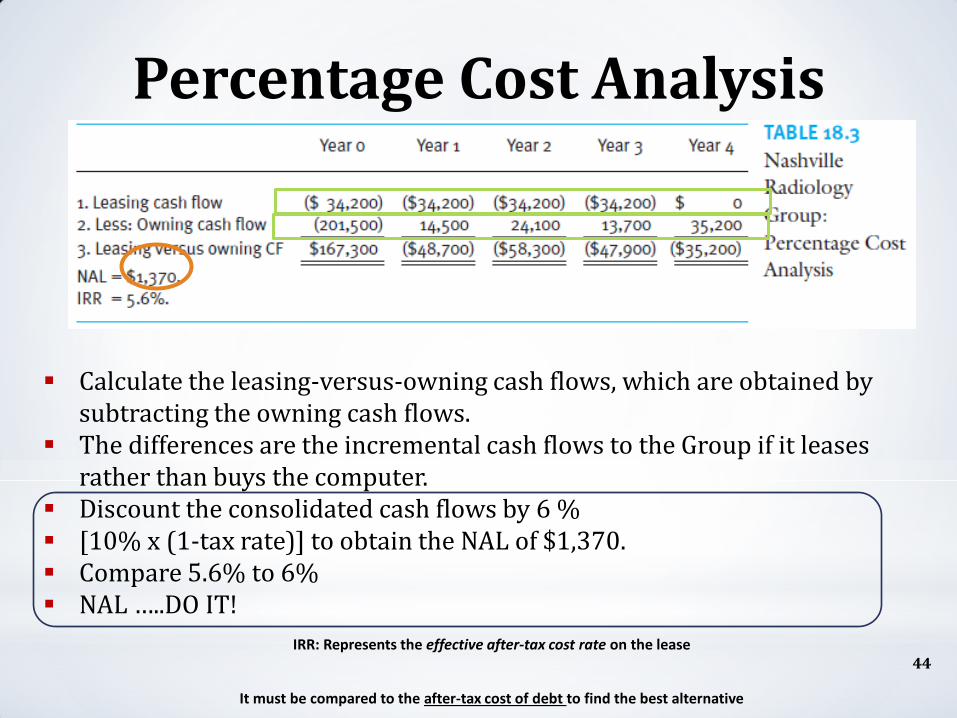

Percentage Cost Analysis

44

Calculate the leasing-versus-owning cash flows, which are obtained by subtracting the owning cash flows.

The differences are the incremental cash flows to the Group if it leases rather than buys the computer.

Discount the consolidated cash flows by 6 % [10% x (1-tax rate)] to obtain the NAL of $1,370. Compare 5.6% to 6% NAL …..DO IT!

IRR: Represents the effective after-tax cost rate on the lease

It must be compared to the after-tax cost of debt to find the best alternative

Medical equipment has historically been the number-one equipment type leased, according to the Equipment Leasing and Finance Association (ELFA).

About 62% of all medical equipment acquisitions are financed, many via leases, according to the Equipment Leasing & Finance Foundation. The rest are cash purchases.

However, after being first for 8 consecutive years, medical equipment fell to number 8 on ELFA’s (Equipment Lease & Financing Association) annual What’s Hot list, due to unknowns associated with the Affordable Care Act.

What do you think?!

Interesting Facts

45

Questions & an update

46

Be sure to watch: Shark Tank tomorrow night Stellavalle is talking Veteran Entrepreneurship at the White House. http://www.stellavalle.com/

Exercise (Lease Evaluation)

47

Scenario Based Exercise (Determine Lease vs. Purchase)

48 Katie’s son: Raylan (8 months)

Exercise 1 (Lease Evaluation)

49

Katie’s family went to the Universal Studio in Florida for family vacation. They watched the transformer show.

Exercise 1 (Lease Evaluation)

50

Katie decides to buy a Bumble Bee Transformer for her son after the trip to Universal Studio in Florida.

Exercise 1 (Lease Evaluation)

51

Katie plans to use her company called Bumble kids (day care company) to have a Bumble Bee.

Bumble Bee Lease Evaluation

52

Factors: The purchase price of a Bumble Bee is $2 million 15% Bank loan. A Bumble Bee falls into the three -year class for tax

depreciation, so the MACRS allowances are 33.33, 44.45, 14.81, and 7.41in Years 1 through 4, respectively.

The company's marginal tax rate is 40 percent. Annual maintenance cost is $100,000, payable

beginning of each year, when purchased. Tentative lease terms call for payments of $700,000

at the end of each year. The best estimate for the value of the Bumble Bee

after three years of wear and tear is $500,000.

Exercise 1 (Bumble Bee Lease Evaluation)

53

What is the NAL and IRR?

Lease or Purchase?

Team Tasks:

Come up with a creative name for your group.

Present the answer of assigned problem to class.

Group Project

54

Group Exercise Objectives:

55

What is the NAL and IRR?

Lease or Purchase?

Team 1 (Alarm System)

56

• Stephanie wants to install a new $1 million burglar alarm system in her business property “Britney Spear’s Fan Club” in Beverly Hill, CA.

• She plans to use the alarm system for only five years, at which time a brand new alarm system will be acquired that will accommodate total office care system including temperature control.

• She can obtain a 15% bank loan to buy the alarm system or she can lease the system for five years. Assume that the following facts apply to the decision:

57

Factors: The alarm system falls into the five-year class for tax

depreciation, so the MACRS allowances are 20.0, 32.0, 19.20, 11.52, 11.52, and 5.76 in Years 1 through 5, respectively.

Annual maintenance cost is $50,000, payable beginning of each year, whether lease or purchased.

The company's marginal tax rate is 40%. Tentative lease terms call for payments of $300,000

at the end of each year. The best estimate for the value of the alarm system

after five years of wear and tear is $200,000.

Team 1 (Alarm System)

Team 1 (Alarm System)

58

What if salvage value increases to

500,000? Lease or Purchase?

Team 2

59

Jess wants a Ski Nautique for her ski lesson company “On a Boat” on Lake Austin, Texas • She plans to use the boat for 5 years before she will need an

upgrade. • She can obtain a 15% bank loan to buy the boat or she can

lease the boat. • $150,000 purchase price

Team 2

60

Factors: • The boat purchase falls into the five-year class for

tax depreciation, so the MACRS allowances are 20.0, 32.0, 19.20, 11.52, 11.52, and 5.76 in Years 1 through 5, respectively.

• The company's marginal tax rate is 40 percent. • Tentative lease terms call for payments of $25,000

at the end of each year. • The best estimate for the value of the boat after four

years of wear and tear is $70,000 • Maintenance Cost: $3,000/year, payable beginning

of each year whether lease or purchased.

Team #2

What if salvage value decreases to 40,000?

Lease or Purchase? 61

Team 3

62

• K-C wants to expand his “Step’n’up Pizza Parlor” business to Vail, Colorado. He wants a new brick-oven to bake his own award winning pizza

• K-C wants to install a new $50,000 oven in his business

• He plans to use the oven for only five years, at which time he will need a brand new oven because he doesn’t plan on staying in the company. He plans on retiring in Mexico to venture into taco creation.

• He can obtain a 15% bank loan to buy the oven or he can lease the oven for five years.

Assume that the following facts apply to the decision:

• The oven purchase falls into the five-year class for tax depreciation, so the MACRS allowances are 20.0, 32.0, 19.20, 11.52, 11.52, and 5.76 in Years 1 through 5, respectively.

• The company's marginal tax rate is 30 percent.

• Tentative lease terms call for payments of $8,000 at the end of each year.

• The best estimate for the value of the oven after five years of wear and tear is $20,000

• Maintenance Cost: $1,000/year, payable beginning of each year when purchased.

Team #3

63

Team #3

What if salvage value increases to $25,000?

Lease or Purchase?

64

Questions ?

66