leading the rates debate vlga essential mayors’ weekend john comrie 17 jan 2013

TRANSCRIPT

LEADING THE RATES DEBATE

VLGA Essential Mayors’ Weekend John Comrie 17 Jan 2013

2

Perennial challenge for all governments

Citizens invariably ask their governments to deliver more services than they wish to pay taxes to fund A key responsibility of governments is to

manage communities expectations re what’s possible

Over medium to longer term cost of services provided needs to be offset by revenue

3

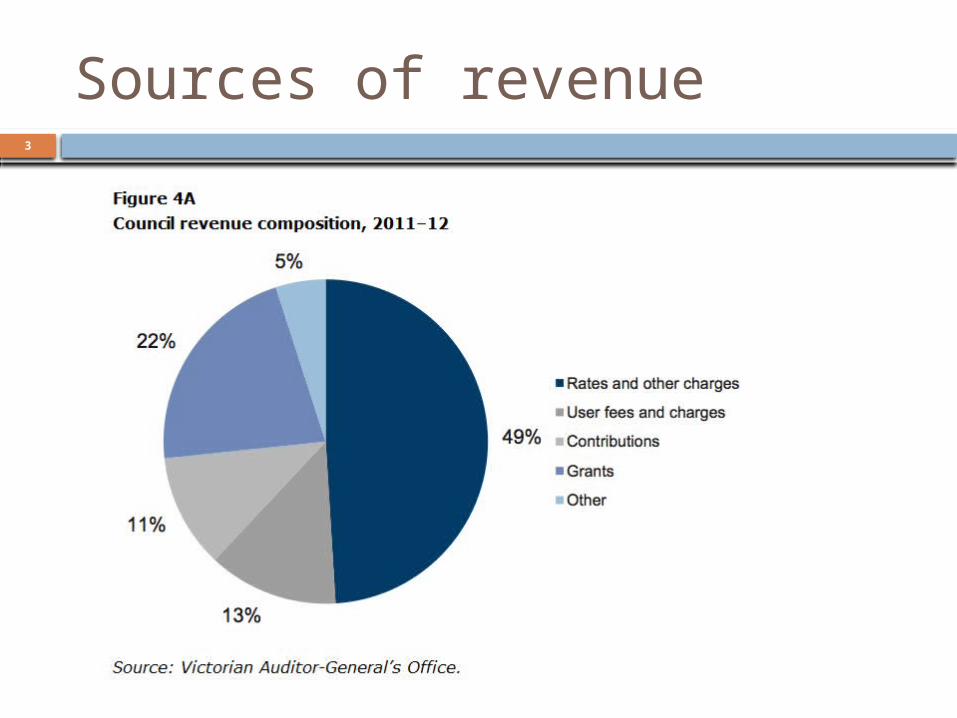

Sources of revenue

4

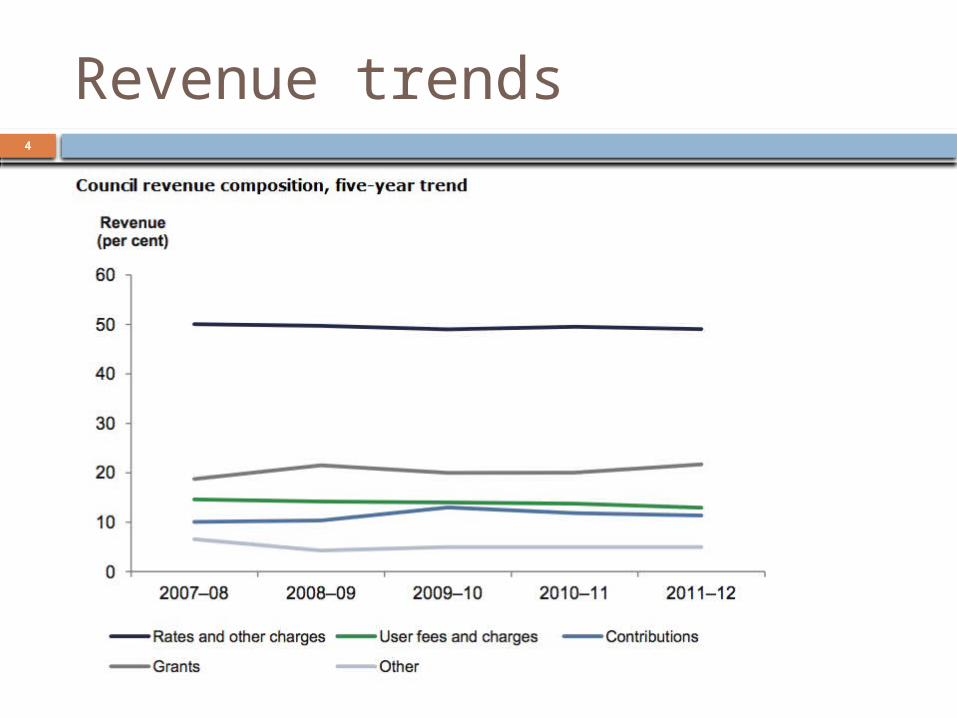

Revenue trends

5

LG revenue prediction

Untied grants not likely to materially increase in next few years councils that need to raise more revenue need

to consider making greater use of own source revenue raising powers LG Act provides considerable flexibility Before making greater use need to consider

whether existing means of raising revenue are fair and appropriate

Most councils have reasonable capacity to manage own financial destiny

6

Responsible financial decision-making (1)

Not just about rates Need to focus primarily on long run

operating result ie difference between operating revenue

and operating expenses (inclusive of depreciation) result

Is the difference between cost of services & revenue received – an ongoing negative operating result implies service levels may not be sustainable

7

Responsible financial decision-making (2)

Need: to be mindful of community preferences and

affordability of range and level of services provided Efficient and effective service delivery Need good Council Plan & Strategic Resource Plan Responsible use of debt (LG is asset intensive)

Use of reliable up-to-date asset management plan and long-term financial plan essential for good financial decision-making

8

Responsible financial decision-making (3)

All mayors should know and be able to explain to others: Whether current and preferred future

service levels are sustainable What needs to be done to achieve/maintain

financial sustainability Whether their debt levels are reasonable

See eg VAGO assessments

9

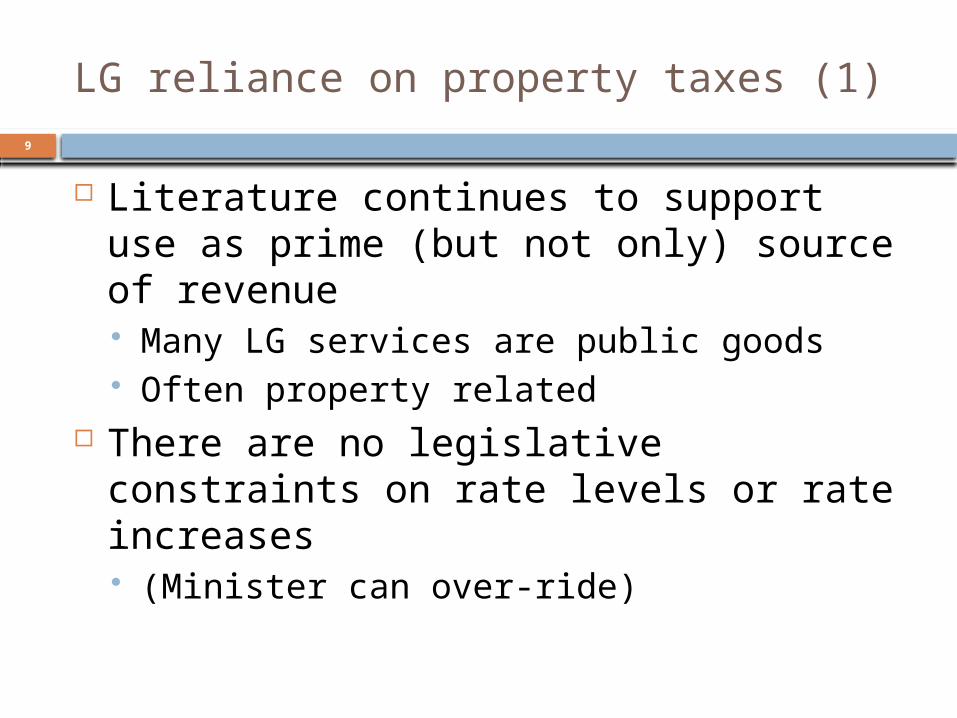

LG reliance on property taxes (1)

Literature continues to support use as prime (but not only) source of revenue Many LG services are public goods Often property related

There are no legislative constraints on rate levels or rate increases (Minister can over-ride)

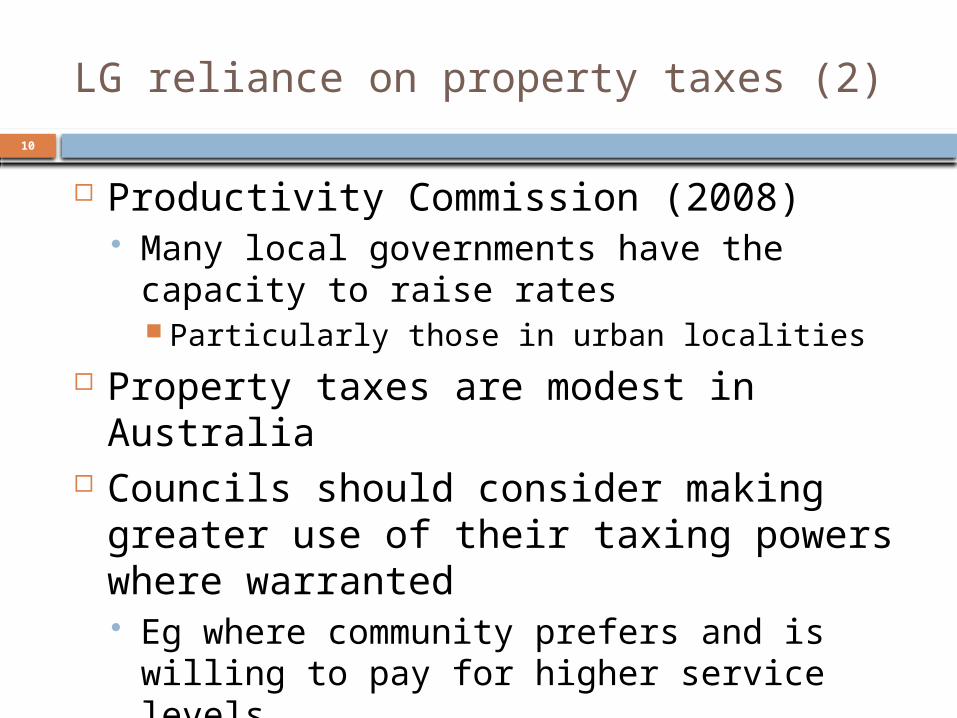

10

LG reliance on property taxes (2)

Productivity Commission (2008) Many local governments have the capacity

to raise rates Particularly those in urban localities

Property taxes are modest in Australia Councils should consider making greater

use of their taxing powers where warranted Eg where community prefers and is willing

to pay for higher service levels

11

LG reliance on property taxes (3)

Property taxes often unpopular and perceived as unfair. Why? Relative amounts payable not necessarily

correlated with relative services? Can adversely impact on asset rich/income poor? Concerns re reliability of valuation data?

But do councils do enough to: Consider various rating tool options? ‘Sell’ rationale for their basis of rating?

Often possible to both address valid concerns and raise more revenue

12

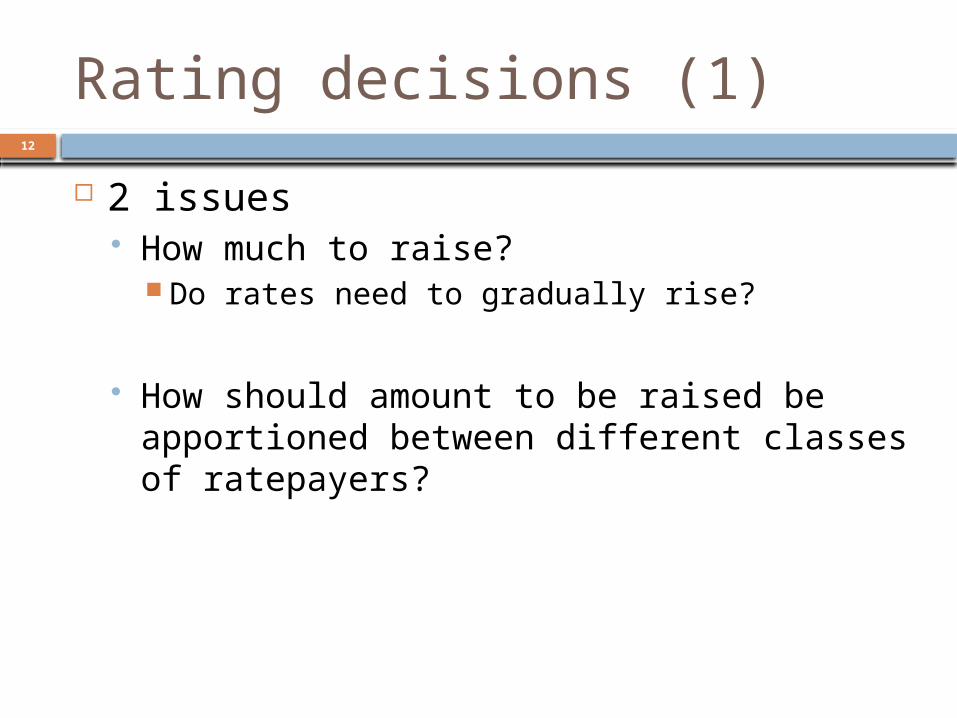

Rating decisions (1)

2 issues How much to raise?

Do rates need to gradually rise?

How should amount to be raised be apportioned between different classes of ratepayers?

13

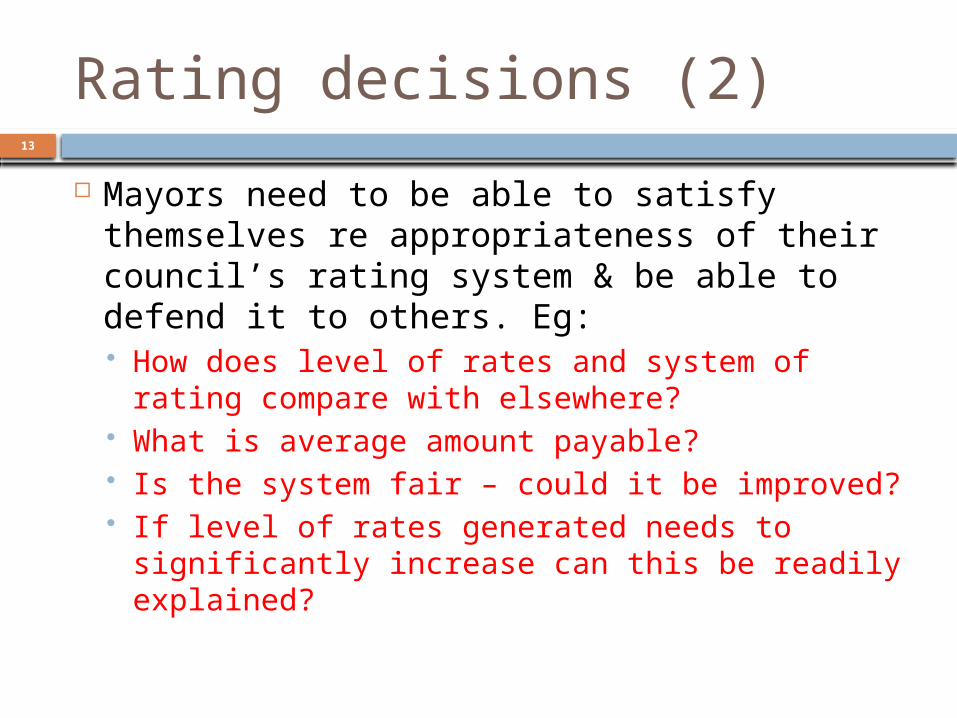

Rating decisions (2)

Mayors need to be able to satisfy themselves re appropriateness of their council’s rating system & be able to defend it to others. Eg: How does level of rates and system of rating

compare with elsewhere? What is average amount payable? Is the system fair – could it be improved? If level of rates generated needs to

significantly increase can this be readily explained?

Local Government Act

14

15

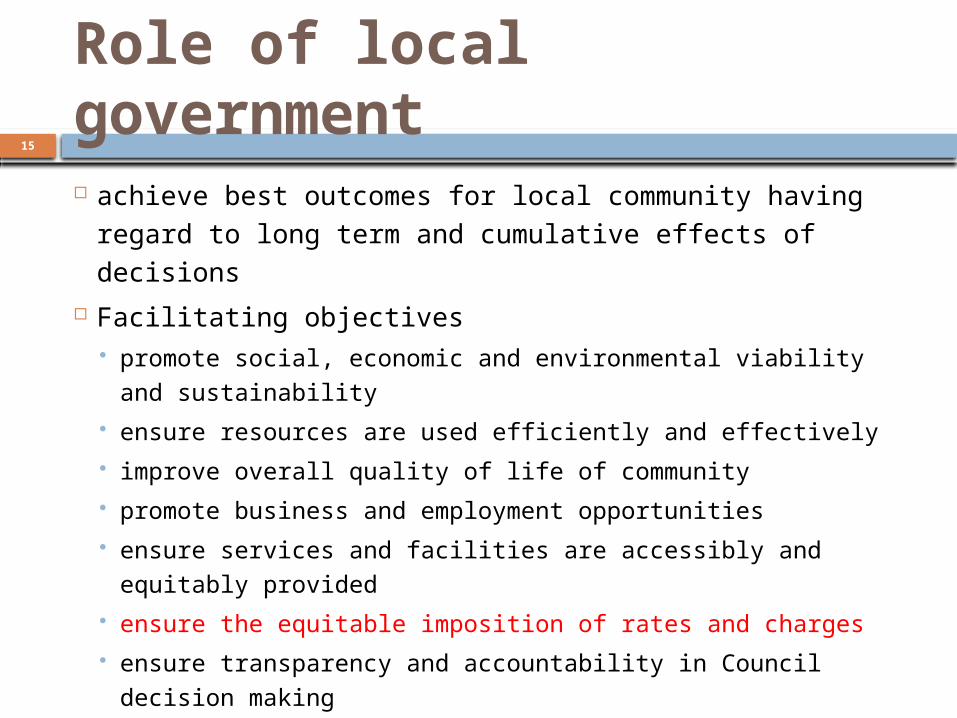

Role of local government

achieve best outcomes for local community having regard to long term and cumulative effects of decisions

Facilitating objectives promote social, economic and environmental viability and

sustainability ensure resources are used efficiently and effectively improve overall quality of life of community promote business and employment opportunities ensure services and facilities are accessibly and equitably

provided ensure the equitable imposition of rates and charges ensure transparency and accountability in Council decision

making

16

Revenue raising tools (1)

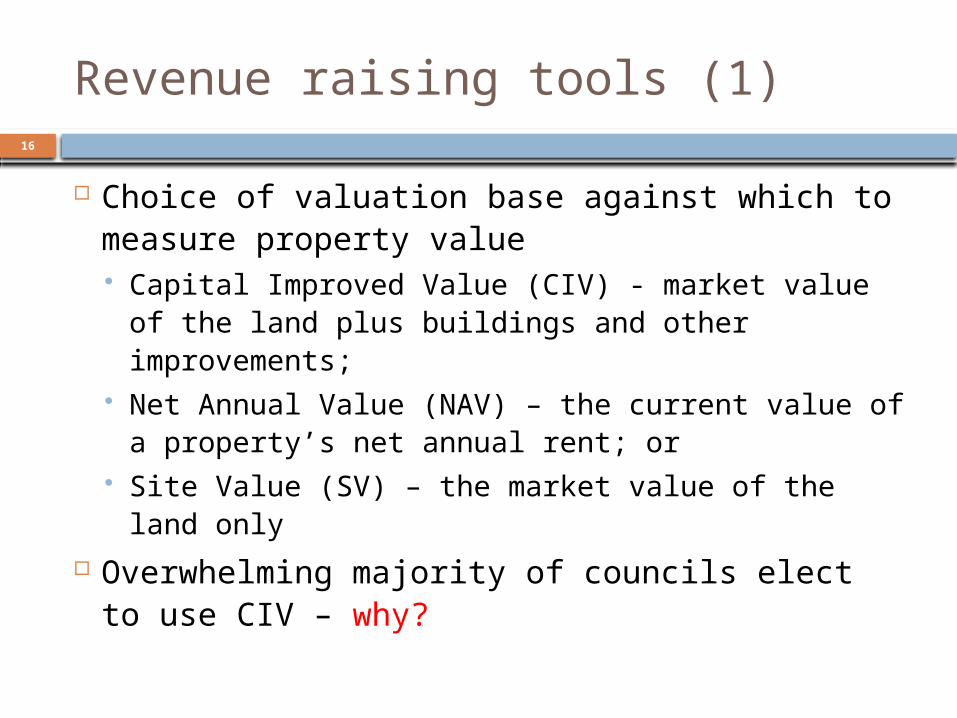

Choice of valuation base against which to measure property value Capital Improved Value (CIV) - market value of

the land plus buildings and other improvements; Net Annual Value (NAV) – the current value of a

property’s net annual rent; or Site Value (SV) – the market value of the land

only Overwhelming majority of councils elect to

use CIV – why?

17

Revenue raising tools (2)

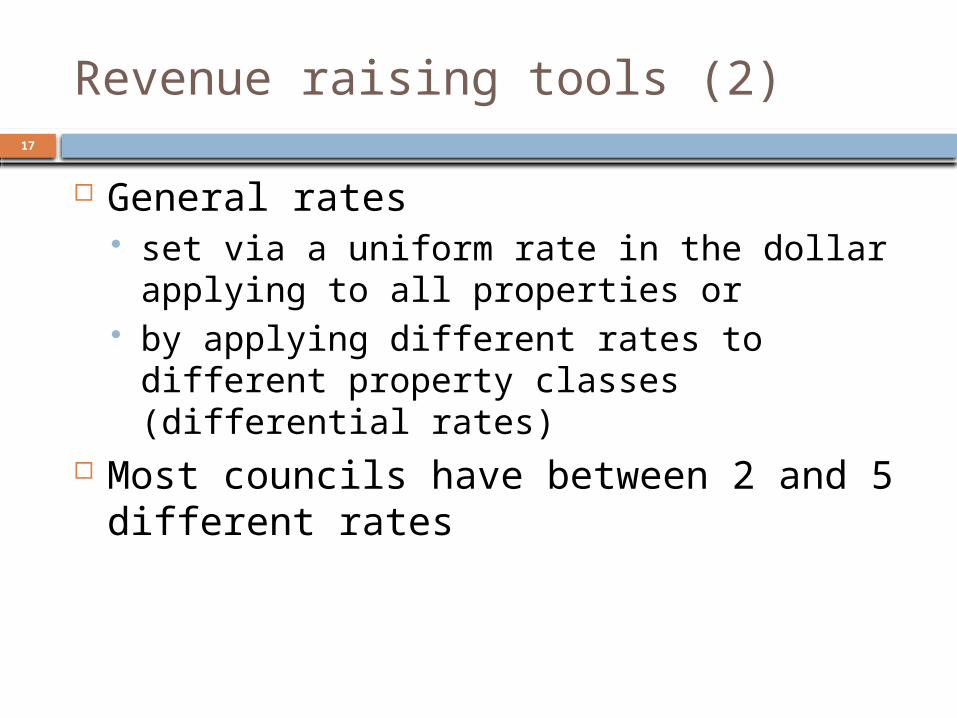

General rates set via a uniform rate in the dollar applying

to all properties or by applying different rates to different

property classes (differential rates) Most councils have between 2 and 5

different rates

18

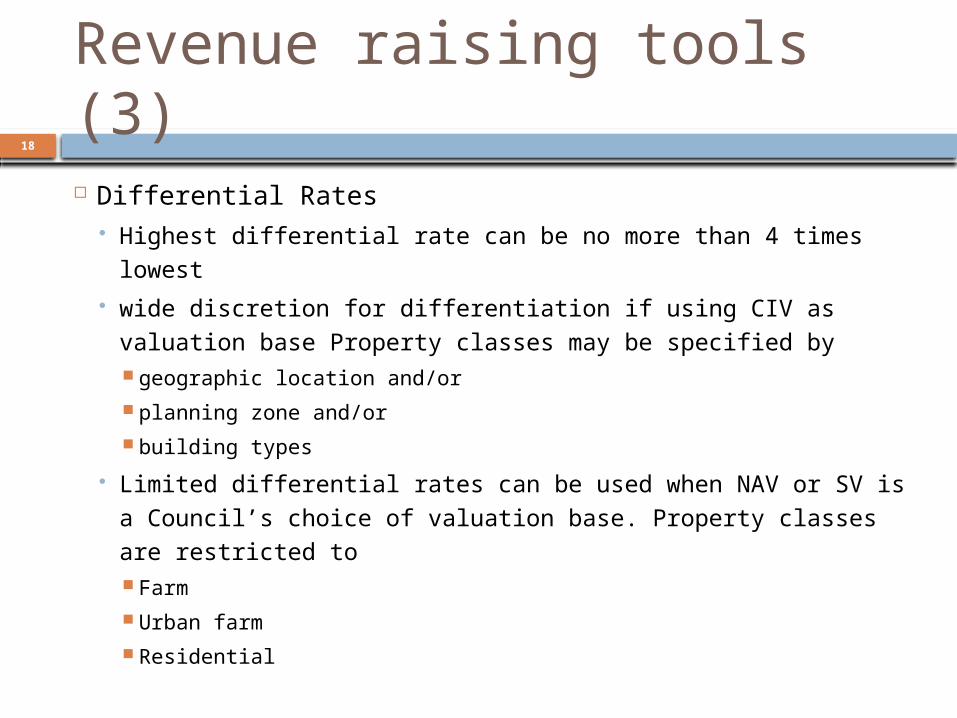

Revenue raising tools (3)

Differential Rates Highest differential rate can be no more than 4 times lowest wide discretion for differentiation if using CIV as valuation

base Property classes may be specified by geographic location and/or planning zone and/or building types

Limited differential rates can be used when NAV or SV is a Council’s choice of valuation base. Property classes are restricted to Farm Urban farm Residential

19

Revenue raising tools (4)

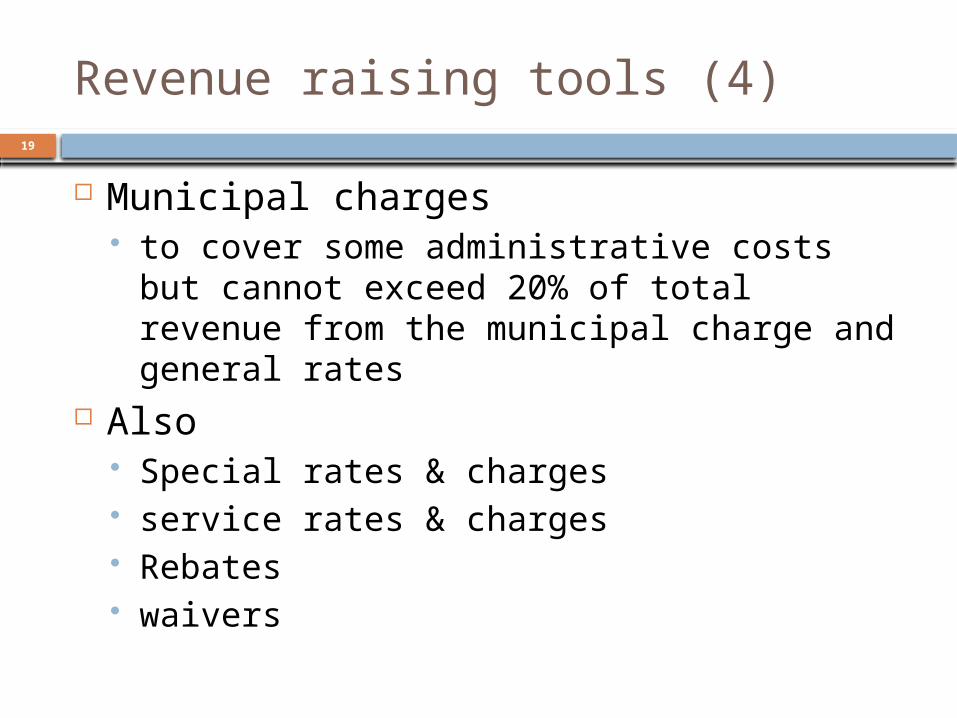

Municipal charges to cover some administrative costs but

cannot exceed 20% of total revenue from the municipal charge and general rates

Also Special rates & charges service rates & charges Rebates waivers

Rating Theory & Practice

20

21

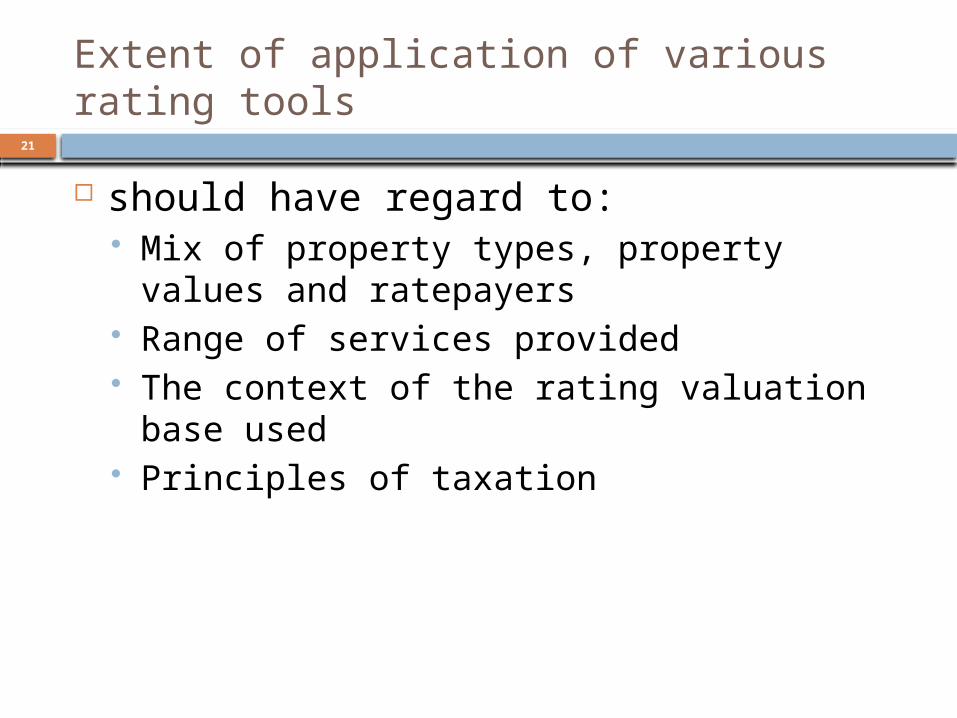

Extent of application of various rating tools

should have regard to: Mix of property types, property values and

ratepayers Range of services provided The context of the rating valuation base

used Principles of taxation

22

Principles of taxation (1)

Equity: Capacity to pay (i.e. those with greater

economic capacity contribute more). Benefits (i.e. those who benefit more

contribute more) Simplicity – in terms of administration

and compliance Efficiency – minimal distortion to

property ownership and development decisions

23

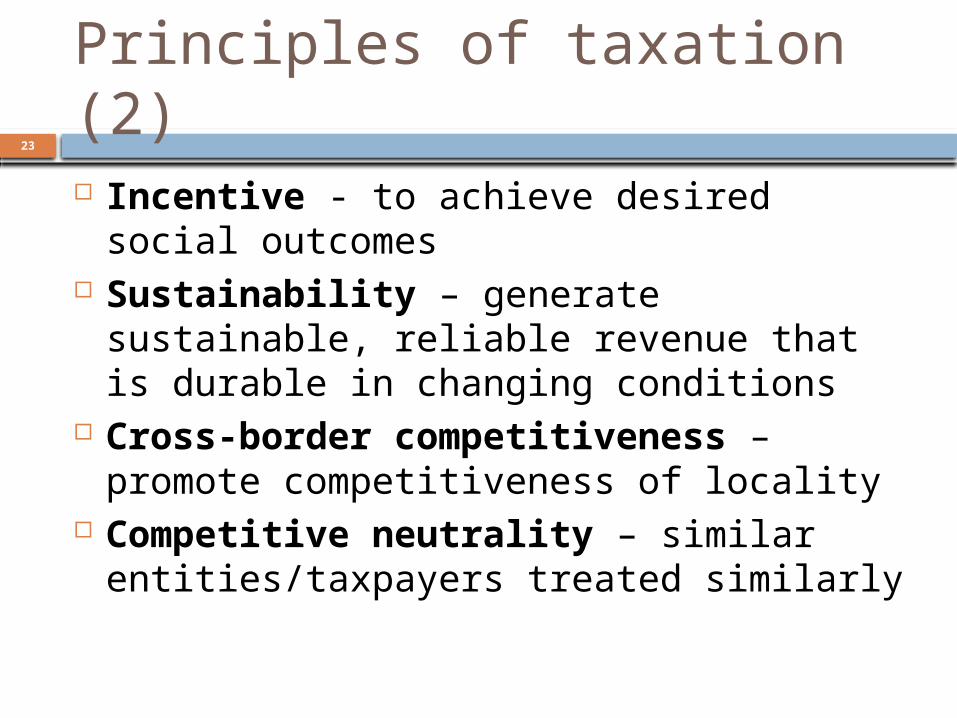

Principles of taxation (2)

Incentive - to achieve desired social outcomes

Sustainability – generate sustainable, reliable revenue that is durable in changing conditions

Cross-border competitiveness – promote competitiveness of locality

Competitive neutrality – similar entities/taxpayers treated similarly

24

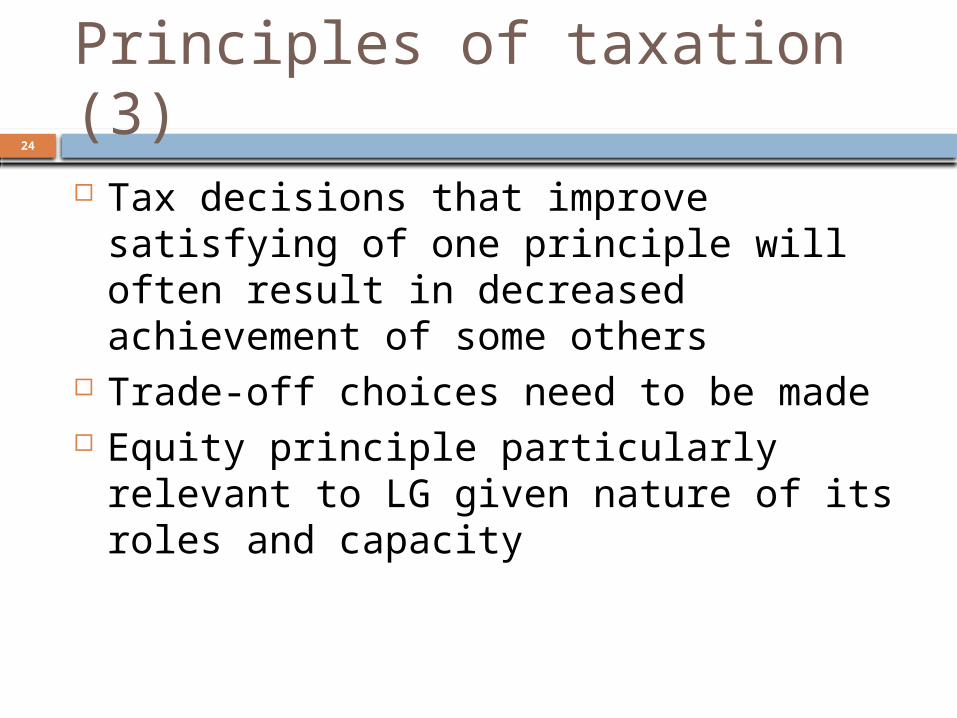

Principles of taxation (3)

Tax decisions that improve satisfying of one principle will often result in decreased achievement of some others

Trade-off choices need to be made Equity principle particularly relevant to

LG given nature of its roles and capacity

25

Principles of taxation

Equity Other things being equal those with greater capacity

to pay should pay more

Other things being equal those who receive greater benefits should pay more

Benefits received and capacity to pay often not correlated and taxation decisions need to have regard to relevance of both factors trade-offs likely to need to be made (i.e. balanced

approach)

26

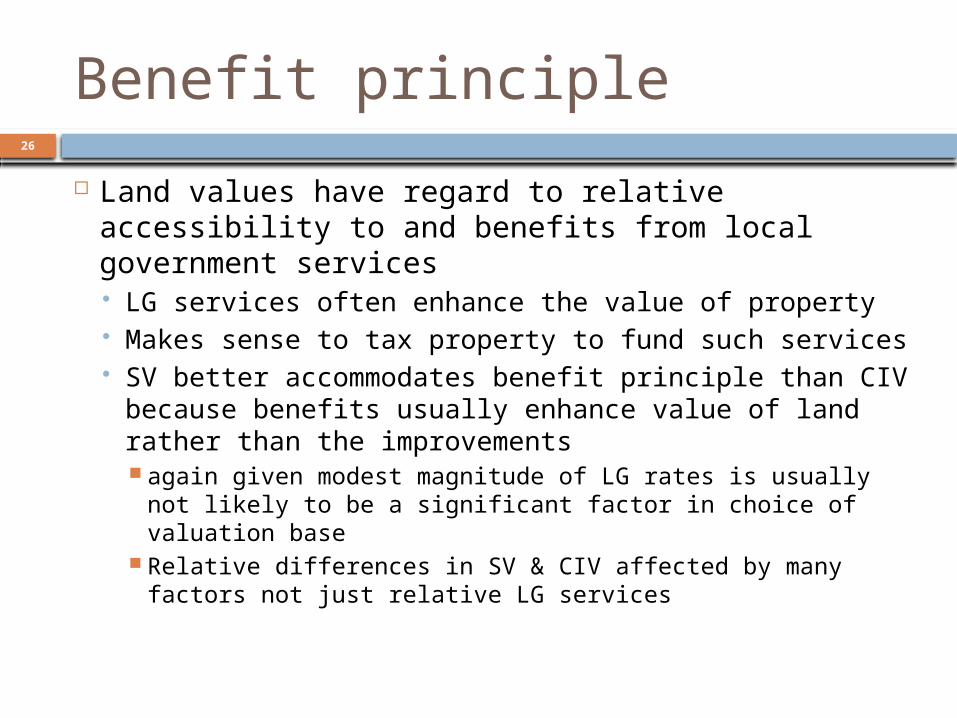

Benefit principle

Land values have regard to relative accessibility to and benefits from local government services LG services often enhance the value of property Makes sense to tax property to fund such services SV better accommodates benefit principle than CIV

because benefits usually enhance value of land rather than the improvements again given modest magnitude of LG rates is usually not

likely to be a significant factor in choice of valuation base Relative differences in SV & CIV affected by many factors

not just relative LG services

27

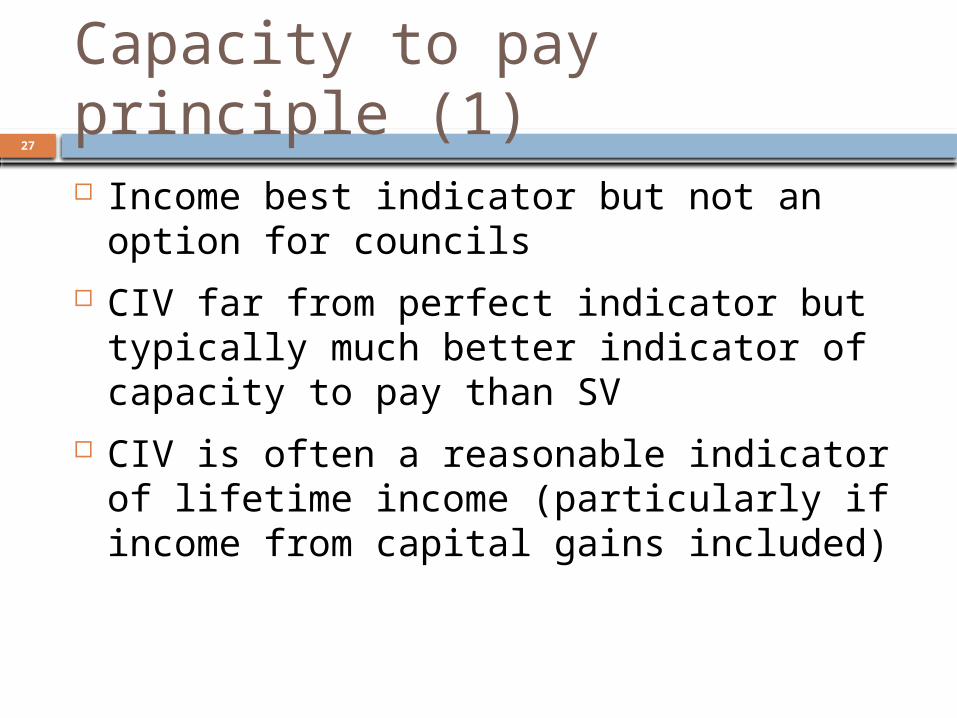

Capacity to pay principle (1)

Income best indicator but not an option for councils

CIV far from perfect indicator but typically much better indicator of capacity to pay than SV

CIV is often a reasonable indicator of lifetime income (particularly if income from capital gains included)

28

Capacity to pay principle (2)

it is reasonable to assume legislators, decision-makers and community see capacity to pay as key criteria in determining rating system structure given that most councils apply CIV and

that CIV is probably inferior to SV on most other grounds

But shouldn’t be only criteria, eg Should a property with double CV of another pay double

amount of rates?

29

Municipal charge

Use of municipal charge can enhance equity, eg If some services benefit all properties equally or

equally benefit people then could recover cost via municipal charge (benefit principle)

Extent of reliance on municipal charge can be tailored to vary extent to which property value influences amount payable (capacity to pay)

Is limited (to 20% of total of general rate and municipal charge revenue) Most councils either do not apply or have very

modest fixed charge – why?

30

Economic efficiency principle A tax is economically efficient if it doesn’t distort

behaviour

Site Value is more economically efficient than Capital Improved Value

Given modest magnitude of local government rates this is usually not a significant factor in choice between SV and CIV Eg does CIV act as a material disincentive to

invest in higher valued properties?

Maintain/improve properties?

Need to look at other considerations to determine best valuation base

31

Incentive principle

Directly counter to efficiency – aims to alter behaviour Effective application usually limited in practice due to

Modest level of rate burden relative to entity’s income limited range of differentials

If aiming to promote particular behaviour - likely to subsidise those already undertaking desirable behaviour, without changing behaviour of others

If aiming to discourage particular behaviour – unlikely to change behaviour in practice

Trade-offs with other principles such as simplicity and consistency

32

Other principles of taxation

Shouldn’t ignore Simplicity Sustainability Cross-border competitiveness Competitive neutrality

Ultimately weighting of all principles is a judgement call but does warrant objective consideration

Use of Differential Rates

33

34

Reliance on differential rates Differential rates can improve outcomes

in some circumstances, but over-reliance can lead to undesirable/inconsistent outcomes & complexity

Can be a fairly ‘blunt tool’ Ratepayers can apply for review by VCAT Should consider using other policy tools

instead of or as well as eg service & special rates & charges and

rebates and waivers

35

Differential rates guidelines

Government committed to issuing Consultation draft about to be released Rating decisions can be over-ruled if not

consistent with guidelines

36

Differential rates

Probably reasonable to assume that material benefits arising from local government services and relative differences in services (or access to services) are reflected in property values

Justification for use of differential rates would seem to rely therefore more on capacity to pay relativities less than or in excess of

property value relativities - but often hard to make objective assessment of this

Higher or lower servicing costs not reflected in property values

37

Differential rates

For example; Rural areas may have lower differential

rates if perceived capacity to pay (eg income) is modest relative to property values

Commercial and industrial properties often subject to higher differential rates than residential rates – presumably because council rates perceived to typically be modest relative to income and other business expenses

38

Differential rates

Having lots of different property classes can undermine the simplicity principle

In the absence of clear and accepted principles to guide use of differential rates, councils are exposed to rent seeking behaviour and pressure for preferential treatment

39

Differential rates

Care should be taken when considering use of or adjusting differentials to take account of relative movements in valuations between different classes of property If change in assessed value is long-term this

suggests a change in relative capacity to pay If change is short-term (due to volatility),

applying a limit to rate increases for affected properties through use of a ‘cap’ (waiver) may be better

Other Issues in Developing a Soundly Based Rating System & Concluding Remarks

40

41

Service and special rates and charges

Generally appropriate for full cost recovery for private goods and other material services that benefit some classes of ratepayer and not others, eg: Kerbside waste and recycling service

Helps service recipients appreciate costs involved and provide feedback on value to service providers

42

Postponements

If rating system well designed then problem of ‘asset rich income poor’ best accommodated by deferral rather than rebate

Deferral effectively has no cost to council (or other ratepayers)

With increasing proportion of population being retired, ‘asset rich (or at least asset richer than many younger families) and income poor’ is going to become increasingly significant public policy issue

43

Economic incidence

Should be mindful of who actually bears the cost of a tax eg landlords may pass higher rates on to

tenants, businesses may pass it on to their customers

44

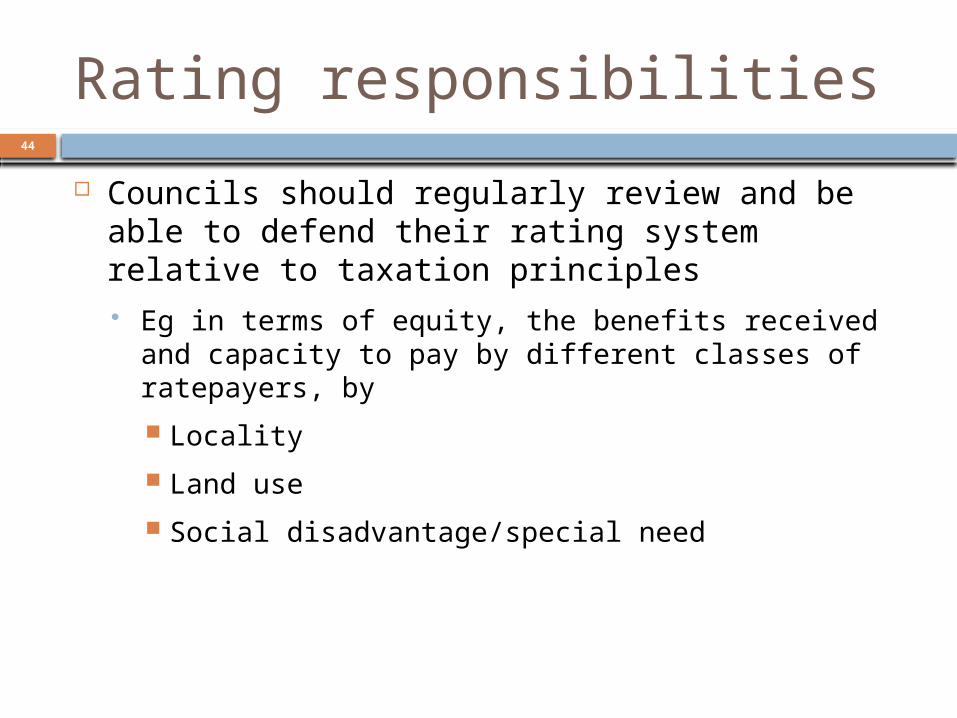

Rating responsibilities

Councils should regularly review and be able to defend their rating system relative to taxation principles Eg in terms of equity, the benefits received and

capacity to pay by different classes of ratepayers, by

Locality

Land use

Social disadvantage/special need

45

Review of rating system

Any significant change in rating system will generate complaints and possible political/media agitation regardless of policy merit

Proceed carefully - staff can model impact on various classes of ratepayer of alternative options to help inform decision-making

46

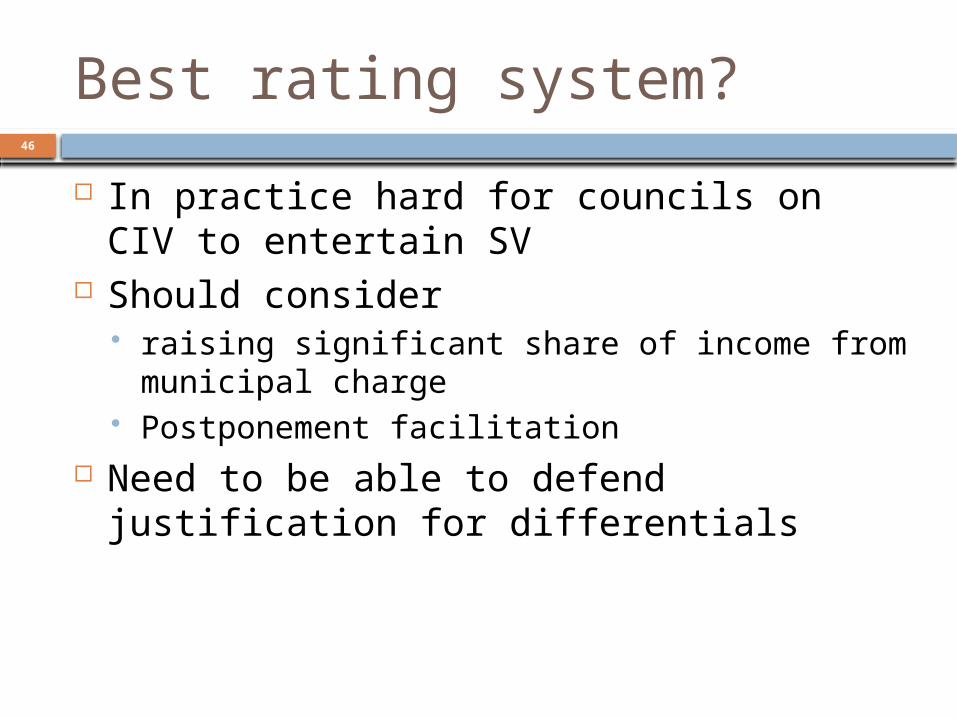

Best rating system?

In practice hard for councils on CIV to entertain SV

Should consider raising significant share of income from

municipal charge Postponement facilitation

Need to be able to defend justification for differentials

47

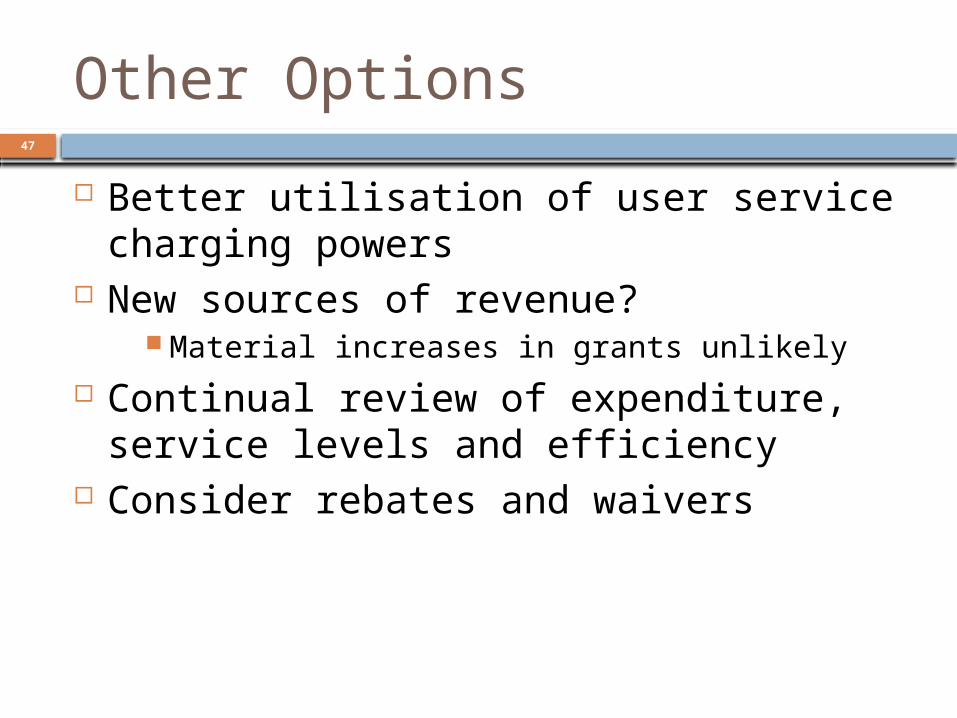

Other Options

Better utilisation of user service charging powers

New sources of revenue? Material increases in grants unlikely

Continual review of expenditure, service levels and efficiency

Consider rebates and waivers

48

The Politics?

Rating is a zero-sum game A change that reduces amount payable for

some ratepayers must result in an increase for others

Invariably those who are adversely impacted have more motivation to make their voice heard than others

A soundly based, up to date, well communicated rating policy is best defence against ‘squeaky wheels’

49

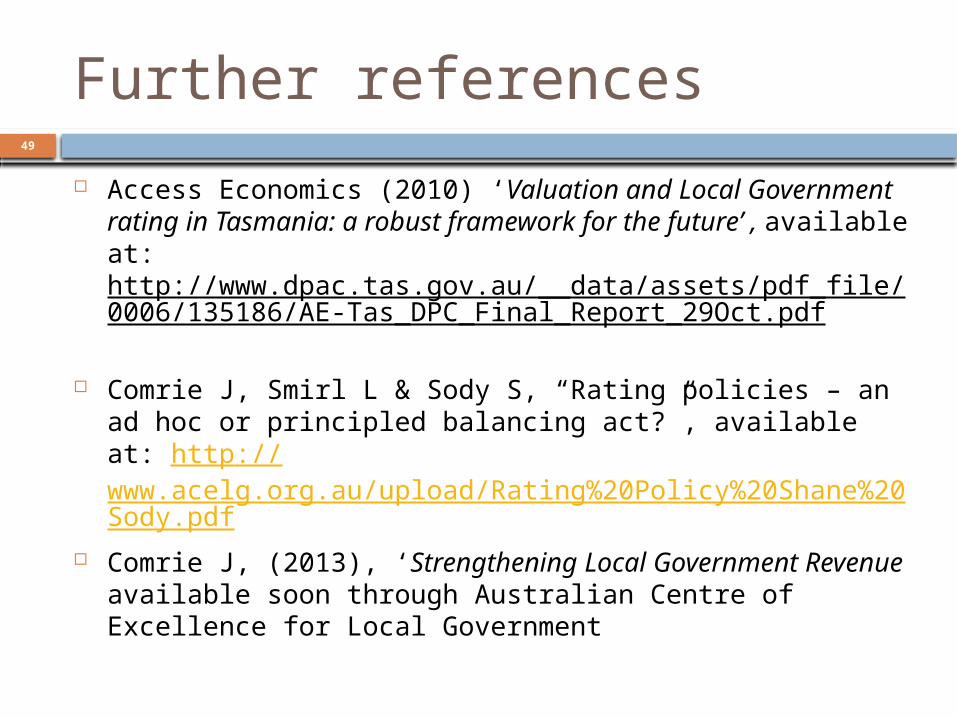

Further references

Access Economics (2010) ‘Valuation and Local Government rating in Tasmania: a robust framework for the future’ , available at: http://www.dpac.tas.gov.au/__data/assets/pdf_file/0006/135186/AE-Tas_DPC_Final_Report_29Oct.pdf

Comrie J, Smirl L & Sody S, “Rating policies – an ad hoc or principled balancing act?”, available at: http://www.acelg.org.au/upload/Rating%20Policy%20Shane%20Sody.pdf

Comrie J, (2013), ‘Strengthening Local Government Revenue available soon through Australian Centre of Excellence for Local Government