laws5144 – introduction to taxation la · laws5144 – introduction to taxation law final exam...

TRANSCRIPT

LAWS5144 – Introduction to Taxation Law

Final Exam Notes

Semester 1, 2009

Alexander Psaltis

40987910

Dated: 12 June 2009

LAWS5144 | Combined notes 2

Table of contents Taxation law overview ................................................................................................................. 13

1 General introduction .......................................................................................................... 13

Aspects of tax ...................................................................................................................... 13

Introduction...................................................................................................................... 13

Tax policy ......................................................................................................................... 14

The nature of taxation .......................................................................................................... 14

Defining tax ...................................................................................................................... 14

Complications ................................................................................................................... 14

Types of taxation within Australia .......................................................................................... 14

Direct taxes ...................................................................................................................... 14

Indirect taxes ................................................................................................................... 15

Tax as a social process ......................................................................................................... 16

2 How a tax system works? .................................................................................................. 16

Incidence of Taxation ........................................................................................................... 16

Types of tax systems......................................................................................................... 16

How this works in Australia ................................................................................................ 16

Functions and objects of taxation .......................................................................................... 17

Criteria for evaluating a tax system ....................................................................................... 17

3 Australia’s tax system ........................................................................................................ 18

Federal power to make taxation laws ..................................................................................... 18

The power to tax .............................................................................................................. 18

Limitations on the Commonwealth power ........................................................................... 18

Sources of Australian Taxation law ........................................................................................ 19

Statute law ....................................................................................................................... 19

Common law .................................................................................................................... 19

The Australian Tax Office .................................................................................................. 19

History of Australian taxation law .......................................................................................... 19

4 General overview of tax ..................................................................................................... 20

Income tax basics ................................................................................................................ 20

The tax formula ................................................................................................................ 20

The core provisions ........................................................................................................... 21

The core provisions explained ............................................................................................... 21

Ordinary income ............................................................................................................... 21

Statutory and non-assessable income ................................................................................. 21

Income tax accounting ...................................................................................................... 21

Capital gains tax ............................................................................................................... 22

General deductions ........................................................................................................... 22

Specific deductions ........................................................................................................... 22

LAWS5144 | Combined notes 3

Capital allowances and car expenses .................................................................................. 22

Tax offsets ....................................................................................................................... 22

Tax payable ...................................................................................................................... 22

Residence and source.................................................................................................................. 24

1 Introductory principles for calculating ‘taxable income’ ........................................................ 24

Introduction...................................................................................................................... 24

Section 4-10(3) ................................................................................................................. 24

Section 4-15(1) ................................................................................................................. 24

The nature of income ........................................................................................................ 24

Defining assessable income ............................................................................................... 25

2 Types of income ............................................................................................................... 25

Ordinary income – s 6-5 ....................................................................................................... 25

The provision .................................................................................................................... 25

Commentary ..................................................................................................................... 26

Statutory income – s 6-10 ITAA97 ......................................................................................... 26

The provision .................................................................................................................... 26

What is not assessable income – s 6-15 ITAA97 ..................................................................... 26

The provision .................................................................................................................... 26

Commentary ..................................................................................................................... 27

Exempt income – s 6-20 ....................................................................................................... 27

The provision .................................................................................................................... 27

Commentary ..................................................................................................................... 27

Non-assessable non-exempt income – s 6-23 ......................................................................... 27

The provision .................................................................................................................... 27

Commentary ..................................................................................................................... 27

Relationships amongst various rules about ordinary income – s 6-25 ....................................... 28

The provision .................................................................................................................... 28

Commentary ..................................................................................................................... 28

Tying this into residence and source .................................................................................. 29

3 Residence ......................................................................................................................... 29

Residence requirements generally ......................................................................................... 29

Introduction...................................................................................................................... 29

Foreign residents .............................................................................................................. 29

Temporary Resident (from 01 July 2006) ............................................................................ 30

Introductory matters to residence ...................................................................................... 30

Residence of individuals ........................................................................................................ 30

Residence defined – s 6(1) ITAA36 .................................................................................... 30

The ordinary concepts test ................................................................................................ 31

The domicile test – s 6(1) ITAA36 ...................................................................................... 33

The 183 day test ............................................................................................................... 36

The superannuation test .................................................................................................... 36

LAWS5144 | Combined notes 4

Residence of companies ....................................................................................................... 37

Introduction...................................................................................................................... 37

Incorporated in Australia ................................................................................................... 37

Carries on business in Australia with central management and control in Australia ................ 37

Carries on business in Australia with voting power controlled by Australian residents ............ 38

4 Source ............................................................................................................................. 39

Introduction ......................................................................................................................... 39

General principles ............................................................................................................. 39

Where these rules come from ............................................................................................ 39

Specific sources .................................................................................................................... 39

Sale of goods .................................................................................................................... 39

Source of services ............................................................................................................. 40

Source of interest ............................................................................................................. 40

Source of dividends ........................................................................................................... 41

Source of royalties ............................................................................................................ 42

Income....................................................................................................................................... 43

5 Income according to ordinary concepts .............................................................................. 43

Introduction...................................................................................................................... 43

General principles ............................................................................................................. 43

Characteristics of income ................................................................................................... 43

Specific instances of income according to ordinary concepts ................................................... 44

Income as a Flow .............................................................................................................. 44

Income must be a product of labour and/or property .......................................................... 44

Reward for services rendered ............................................................................................ 45

Gains (in the Eisen sense) must be realised ........................................................................ 45

Income must “come in” to the taxpayer ............................................................................. 46

There must be a gain ........................................................................................................ 47

Cash or convertible to cash – NB this has been modified by s 21A (see below) ..................... 47

Periodical gains have the character of income ..................................................................... 48

Disposal of capital asset versus an income stream .............................................................. 48

Gratuitous payments ......................................................................................................... 48

Receipts from Illegal Activities ........................................................................................... 49

Income from personal services .............................................................................................. 49

Introduction...................................................................................................................... 49

Receipts related directly to employment or services (Deane) ............................................... 50

Receipts unrelated to employment or services .................................................................... 50

Reward schemes ............................................................................................................... 51

Reward for services or capital? .......................................................................................... 51

Prizes ............................................................................................................................... 51

Categories of income from labour ...................................................................................... 52

6 Business income ............................................................................................................... 52

LAWS5144 | Combined notes 5

Introduction ......................................................................................................................... 52

Common law .................................................................................................................... 52

Statutory expansion – 3 fold .............................................................................................. 52

Identifying a business ........................................................................................................... 53

How is a business identified? ............................................................................................. 53

Has the business commenced? .......................................................................................... 53

Indicators of a business ........................................................................................................ 54

Introduction...................................................................................................................... 54

System and organisation ................................................................................................... 55

Scale of activities .............................................................................................................. 55

Sustained, regular and frequent transactions ...................................................................... 56

Profit motive – see TR 97/11 ............................................................................................. 56

Commercial character of transactions ................................................................................. 57

Characteristics or quantities of property dealt in ................................................................. 58

Other factors .................................................................................................................... 58

Example – Farming business/passive investment ................................................................ 58

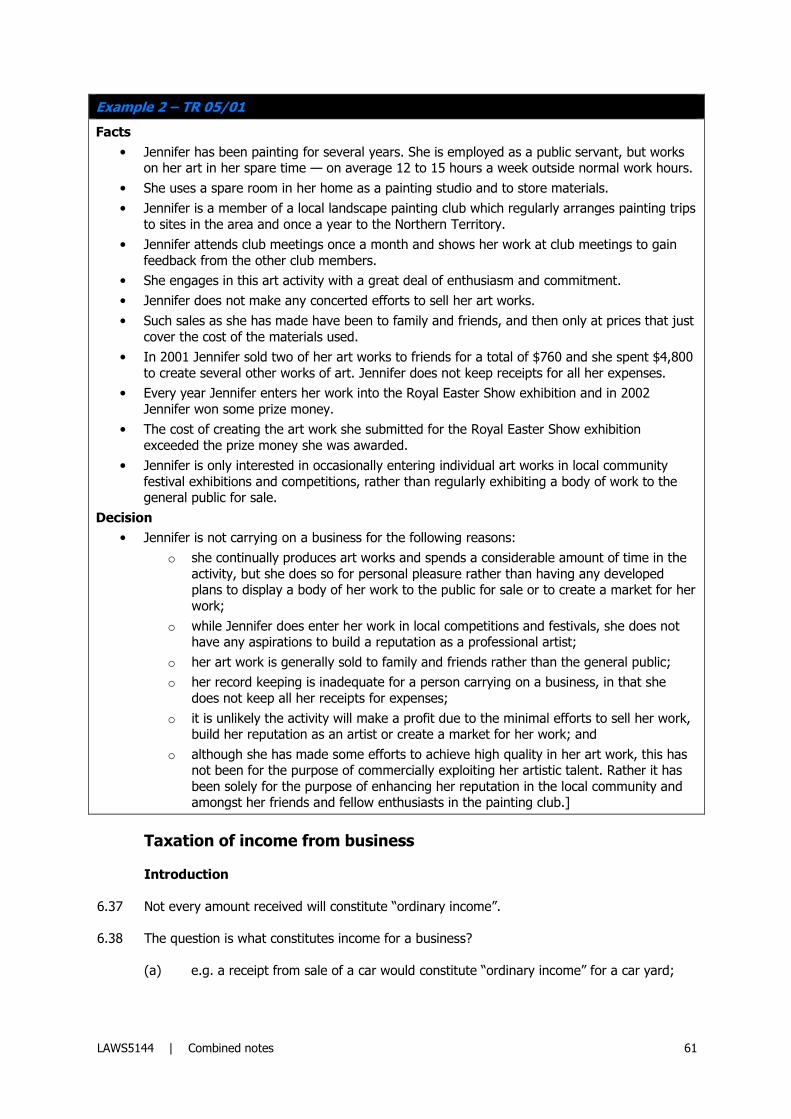

Turning talent to account for profit .................................................................................... 59

Taxation of income from business ......................................................................................... 61

Introduction...................................................................................................................... 61

Receipts received in the ordinary course of business ........................................................... 62

Business income from certain transactions ............................................................................. 63

Business income from ‘isolated’ transactions ....................................................................... 63

Business income from ‘extraordinary’ transactions ............................................................... 64

Lease incentives – application of the Myer principle............................................................. 65

7 Statutory income .............................................................................................................. 66

Allowances in relation to employment and services – s 15-2 ITAA97 ........................................ 66

Introduction...................................................................................................................... 66

s 15-2 – conditions ............................................................................................................ 66

There must be a benefit etc ............................................................................................... 67

Provided to the Taxpayer .................................................................................................. 68

Nexus with employment or services rendered ..................................................................... 68

s 15-2 examples ............................................................................................................... 68

Non-cash business benefits – s 21A ITAA36 ........................................................................... 69

Introduction...................................................................................................................... 69

Application ....................................................................................................................... 70

8 Other types of income ....................................................................................................... 71

Compensation payments ....................................................................................................... 71

General principles ............................................................................................................. 71

Distinguishing income from capital ..................................................................................... 71

Compensation categories ................................................................................................... 72

Statutory provisions .......................................................................................................... 74

LAWS5144 | Combined notes 6

Application of CGT on compensation payments generally .................................................... 74

Interest as Income ............................................................................................................... 74

Discounted securities and Div 16E securities .......................................................................... 75

Introduction...................................................................................................................... 75

Reason for the introduction of Div 16E ............................................................................... 76

Income from real property .................................................................................................... 76

Introduction...................................................................................................................... 76

Negative gearing ............................................................................................................... 76

Dividend imputation ............................................................................................................. 77

The classical system .......................................................................................................... 77

Statutory dividend imputation system – s 207-20 ITAA97 .................................................... 77

Franking credits in practice ................................................................................................ 79

Franking Credit Formula .................................................................................................... 79

Shareholder level (shareholder in 45% bracket) .................................................................. 79

Shareholder level (shareholder in 30% bracket) .................................................................. 79

Shareholder level (shareholder in 15% bracket) .................................................................. 80

Dividend advices ............................................................................................................... 80

Non-assessable income ......................................................................................................... 80

Non-assessable income generally – s 6-15 ITAA97 .............................................................. 80

Exempt income ................................................................................................................. 80

Category One – Exempt entities – Div 50 ITAA97 ................................................................ 81

Category Two – Exempt income – Div 51 ITAA97 ............................................................... 81

Category three – see the legislation ................................................................................... 82

Interest on judgment debt .................................................................................................... 82

Introduction...................................................................................................................... 82

Structured settlement payments ........................................................................................ 82

Consequences of an amount being exempt income ................................................................ 82

Non assessable non exempt income ...................................................................................... 83

General principle ............................................................................................................... 83

Examples .......................................................................................................................... 83

Capital gains tax (CGT) ............................................................................................................... 84

1 CGT as a process .............................................................................................................. 84

The 3 steps of CGT ............................................................................................................... 84

2 Step 1 – have you made a capital gain or loss? ................................................................... 84

Introduction ......................................................................................................................... 84

Step 1 can be broken up into 4 questions ........................................................................... 84

Question 1 – What attracts CGT? .......................................................................................... 84

Introduction...................................................................................................................... 84

12 categories of CGT events .............................................................................................. 84

Event A1 – Disposal of a CGT asset .................................................................................... 85

Event B1 – Use and enjoyment before title passes .............................................................. 86

LAWS5144 | Combined notes 7

Event C1 – the end (loss or destruction) of a CGT asset ...................................................... 87

Event C2 – the end (cancellation, surrender or similar) of an intangible asset ....................... 87

Event C3 – the end of an option to acquire shares .............................................................. 88

Event D1 – the bringing into existence of a contractual (or other) right in another entity ....... 89

Event D2 – the granting of an option ................................................................................. 90

Events D3 and D4 – specific events .................................................................................... 90

Events E1 – E9 – events relating to trusts ........................................................................... 90

Events F1 – F5 – events dealing with leases ....................................................................... 91

Event F4 – lessee receives payment for changing a lease .................................................... 91

Event F5 – lessor receives payment for changing lease ....................................................... 92

Events G1 – G3 – events dealing with shares ...................................................................... 92

Event G3 – liquidator declares shares worthless .................................................................. 92

Events H1 – H2 – special capital receipts ............................................................................ 93

Events I1 – I2 – ending of Australian residency .................................................................. 93

Events J1 – J4 – reversal of rollovers .................................................................................. 93

Events K1 – K2 – other CGT events .................................................................................... 94

Events L1 – L8 – consolidated groups ................................................................................. 94

Question 2 – What is a CGT asset?..................................................................................... 95

Introduction...................................................................................................................... 95

General principles ............................................................................................................. 95

Collectables ...................................................................................................................... 96

Personal use assets ........................................................................................................... 97

Separate CGT assets ......................................................................................................... 97

Timing of acquisition of the assets ..................................................................................... 99

Question 3 – does an exception (Div 104) or exemption apply (Div 118)? ................................ 99

General principles ............................................................................................................. 99

Exempt assets ................................................................................................................ 100

Exempt or loss denying transactions ................................................................................ 100

Anti-overlap provisions .................................................................................................... 101

Small business relief ........................................................................................................ 101

Main residence exemption ............................................................................................... 104

Question 4 – Can there be a roll-over? ............................................................................. 108

3 Step 2 – work out the amount of the capital gain or loss ................................................... 109

Introduction ....................................................................................................................... 109

Step 2 can be broken down into 3 questions ..................................................................... 109

Question 1 – what is a capital gain or loss? .......................................................................... 109

Question 2 – what factors come into calculating a capital gain or loss? .................................. 109

Question 3 – how to calculate the gain or loss for most CGT events? ..................................... 109

Introduction.................................................................................................................... 109

Calculation 1 – capital proceeds ....................................................................................... 110

Calculation 2 – cost base ................................................................................................. 112

LAWS5144 | Combined notes 8

Calculation 5 – reduced cost base .................................................................................... 115

4 Step 3 – work out your net capital gain or loss for the year ............................................... 115

Introduction ....................................................................................................................... 115

Step 3 can be broken down into 2 questions ..................................................................... 115

Question 1 – How do you work out your net capital gain or loss? .......................................... 116

Introduction.................................................................................................................... 116

Calculation 1 – gains and losses for the income year ......................................................... 116

Calculation 2 – use previous years capital losses ............................................................... 116

Calculation 3 – discount percentage ................................................................................. 117

Calculation 4 – small business concessions ....................................................................... 118

Calculation 5 – determining the capital gains .................................................................... 118

3 step process for net capital losses – see s 102-10 .......................................................... 118

Question 2 – How do you comply with CGT? ........................................................................ 118

Deductions ............................................................................................................................... 119

1 Introduction.................................................................................................................... 119

General principles ........................................................................................................... 119

Key points ...................................................................................................................... 119

The nature of deductions ................................................................................................. 120

Substantiation: Div 900 ................................................................................................... 120

2 General deductions ......................................................................................................... 120

Introduction ....................................................................................................................... 120

Limbs ............................................................................................................................. 120

Positive limbs ..................................................................................................................... 121

Introduction.................................................................................................................... 121

Common elements .......................................................................................................... 121

Gaining or producing your assessable income ................................................................... 122

Nexus test ...................................................................................................................... 122

Necessarily incurred in carrying on a business .................................................................. 123

Involuntary Expenses ...................................................................................................... 123

Connection with income earning activities......................................................................... 123

Temporal connection ....................................................................................................... 124

Characterising losses and outgoings ................................................................................. 125

Grossly excessive expenditure (TR 2006/3)....................................................................... 126

Negative limbs ................................................................................................................... 127

Introduction.................................................................................................................... 127

Loss or outgoing of capital, or capital in nature ................................................................. 127

Private or domestic in nature ........................................................................................... 129

Incurred in relation to gaining or producing exempt income .............................................. 130

Where another provision in the ITAA prevents the TP from a deduction ............................. 130

Apportionment: ‘To the extent that…’ .................................................................................. 132

Common general deduction types ....................................................................................... 132

LAWS5144 | Combined notes 9

Introduction.................................................................................................................... 132

Expenses incurred in gaining employment ........................................................................ 133

Relocation Expenses ........................................................................................................ 133

Child care expenses ........................................................................................................ 133

Travel Expenses .............................................................................................................. 133

Self-education expenses .................................................................................................. 134

Home office expenses ..................................................................................................... 135

Clothing Expenses ........................................................................................................... 137

Interest expense ............................................................................................................. 137

Legal Expenses .................................................................................................................. 138

General principles ........................................................................................................... 138

3 Specific Deductions ......................................................................................................... 139

Introduction ....................................................................................................................... 139

Tax related expenses .......................................................................................................... 140

Repairs .............................................................................................................................. 140

Introduction.................................................................................................................... 140

What is a repair? ............................................................................................................. 140

Essential attributes .......................................................................................................... 141

Notional repairs .............................................................................................................. 142

Non-deductible repairs .................................................................................................... 143

Additions ........................................................................................................................ 143

Improvements ................................................................................................................ 143

Example ......................................................................................................................... 144

Example ......................................................................................................................... 144

Example ......................................................................................................................... 144

Initial Repairs ................................................................................................................. 145

Example ......................................................................................................................... 145

Combination of repairs and non-deductible renovations ..................................................... 145

Payment for lease obligation to repair .............................................................................. 146

Repairs to assets used only partly for income-producing purposes ..................................... 146

Bad debts .......................................................................................................................... 147

Requirements ................................................................................................................. 148

Payments to Associations .................................................................................................... 149

Travel between work places ................................................................................................ 149

Borrowing expenses ........................................................................................................... 150

Losses by theft ................................................................................................................... 150

Car expenses ..................................................................................................................... 151

Introduction.................................................................................................................... 151

Available methods ........................................................................................................... 151

Cents per kilometre - Div 28-C ......................................................................................... 152

12% of original value - Div 28-D ...................................................................................... 152

LAWS5144 | Combined notes 10

1/3 of actual expenses - Div 28-E .................................................................................... 152

Log book method - Div 28-G ............................................................................................ 152

Substantiation rules for car expenses ............................................................................... 152

Extent of substantiation required ..................................................................................... 153

Gifts .................................................................................................................................. 154

Prior year losses ................................................................................................................. 154

Principles ........................................................................................................................ 155

Example ......................................................................................................................... 155

4 Capital Allowances .......................................................................................................... 155

Key Points .......................................................................................................................... 155

Introduction.................................................................................................................... 155

Expenditure on depreciating assets ..................................................................................... 156

Deductions for depreciating assets ................................................................................... 156

Deducting amounts for depreciating assets ....................................................................... 156

‘taxable purpose’ ............................................................................................................. 156

Circumstances in which Div 40 has no application ............................................................. 156

What is a depreciating asset? .......................................................................................... 156

Holding a depreciating asset ............................................................................................ 158

Deduction for decline in value .......................................................................................... 158

Diminishing value method – where asset is first held on or after 10 May 2006 .................... 159

Diminishing value method – where asset is first held pre-10 May 2006 ............................... 159

Prime cost ...................................................................................................................... 159

Base value ...................................................................................................................... 159

Asset’s cost .................................................................................................................... 159

Effective Life ................................................................................................................... 160

Exceptions ......................................................................................................................... 161

Immediate deduction for low-cost assets .......................................................................... 161

Low value pools .............................................................................................................. 161

Decline in value of a low-value pool ................................................................................. 162

Car Depreciation Limit ..................................................................................................... 162

Balancing Adjustments ....................................................................................................... 162

General principles ........................................................................................................... 162

Amount of Balancing Adjustment ..................................................................................... 163

Black hole expenditure........................................................................................................ 164

Capital works ..................................................................................................................... 165

Tax accounting and trading stock ............................................................................................... 166

5 Introduction.................................................................................................................... 166

6 Period and timing issues .................................................................................................. 166

The tax period ................................................................................................................... 166

Timing of income ............................................................................................................... 167

Introduction.................................................................................................................... 167

LAWS5144 | Combined notes 11

Salary and wages, interest, and rent ................................................................................ 168

Income from professional practices .................................................................................. 168

Income from business ..................................................................................................... 170

Pre-paid income .............................................................................................................. 171

Deemed derivation .......................................................................................................... 171

Examples ........................................................................................................................ 172

Timing of deductions .......................................................................................................... 172

Introduction.................................................................................................................... 172

TR 97/7 - Summary......................................................................................................... 173

Prepaid Expenses ............................................................................................................ 174

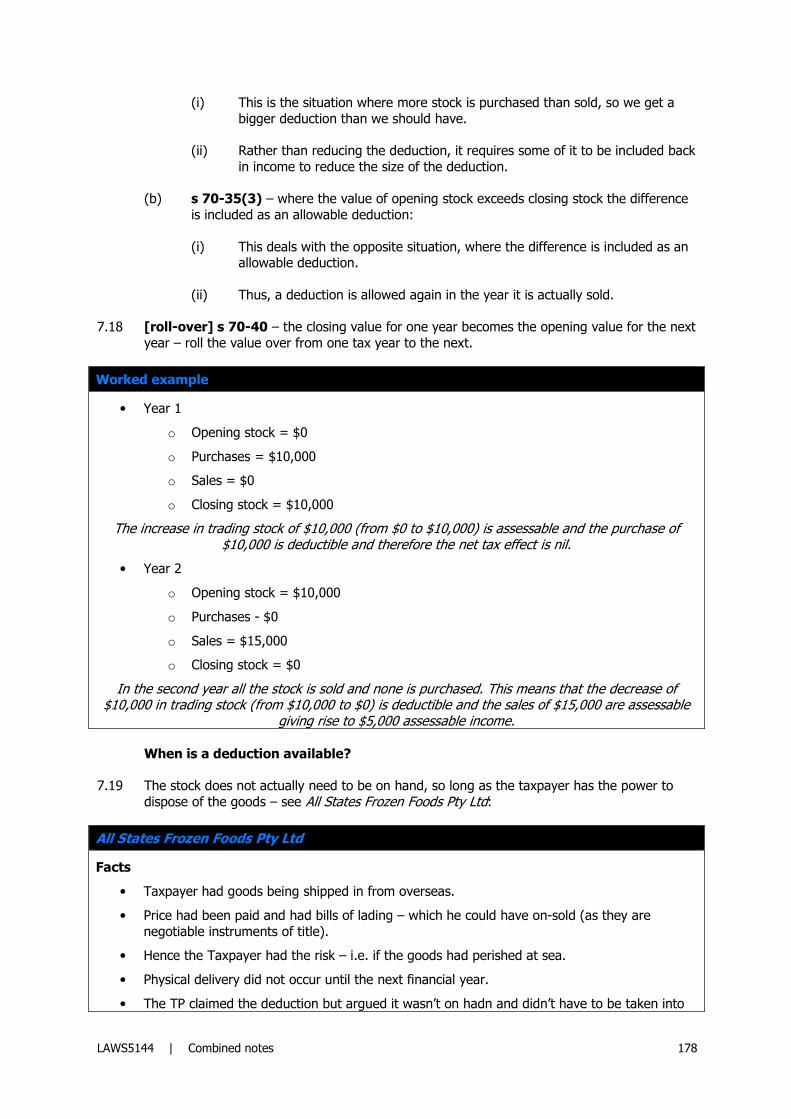

7 Trading stock – Division 70 .............................................................................................. 175

General principles ............................................................................................................... 175

What this division is about? ............................................................................................. 175

3 key features of tax accounting for trading stock ............................................................. 175

What is “trading stock”? .................................................................................................. 176

The taxpayer’s purpose ................................................................................................... 176

Division 70 & tax accounting ............................................................................................ 177

When is a deduction available? ........................................................................................ 178

Valuation of trading stock ................................................................................................ 179

Transactions outside the ordinary course of business ........................................................... 180

Extraordinary disposals .................................................................................................... 180

Starting to hold as trading stock an item already owned .................................................... 180

Ceasing to hold an item as trading stock .......................................................................... 181

Private use example ........................................................................................................ 181

Gift example ................................................................................................................... 181

Tax offsets, tax payable and tax administration .......................................................................... 183

1 Tax payable .................................................................................................................... 183

General principles ............................................................................................................... 183

The formula .................................................................................................................... 183

Tax payable .................................................................................................................... 183

Tax rates ........................................................................................................................ 183

PAYG – pay as you go ..................................................................................................... 184

Help debt ....................................................................................................................... 184

Medicare levy ..................................................................................................................... 184

General principles ........................................................................................................... 184

Example of the base case ................................................................................................ 185

Relief for Low Income Earners ......................................................................................... 185

High income earners – Medicare levy surcharge ................................................................ 185

2 Tax offsets ..................................................................................................................... 185

General principles ............................................................................................................... 185

What is a tax offset? ....................................................................................................... 185

LAWS5144 | Combined notes 12

3 Types of Offsets ........................................................................................................... 186

General principles for offsets ........................................................................................... 186

Common offsets ................................................................................................................. 187

Introduction.................................................................................................................... 187

Dependant rebates.......................................................................................................... 187

Entrepreneurs’ tax offset ................................................................................................. 189

Low income earners rebate.............................................................................................. 190

Medical expenses rebate ................................................................................................. 190

Private health insurance tax offset ................................................................................... 190

Zone Rebate ................................................................................................................... 191

Overseas Defence Force Rebate ....................................................................................... 191

Dividend imputation ........................................................................................................... 192

The classical system ........................................................................................................ 192

Statutory dividend imputation system – s 207-20 ITAA97 .................................................. 192

Franking credits in practice .............................................................................................. 193

Franking Credit Formula .................................................................................................. 194

Shareholder level (shareholder in 45% bracket) ................................................................ 194

Shareholder level (shareholder in 30% bracket) ................................................................ 194

Shareholder level (shareholder in 15% bracket) ................................................................ 194

Dividend advices ............................................................................................................. 195

3 Self-assessment .............................................................................................................. 195

LAWS5144 | Combined notes 13

Topic 1 Taxation law overview

1 General introduction

Aspects of tax

Introduction

1.1 This course is not about tax in terms of employees, it is generally about business taxation (e.g. small business taxation) – once these concepts are understood, the taxation of partnerships, companies and trusts are readily understandable.

1.2 Tax is not all about number crunching, the way we think about tax can be divided into 3 categories – which involve economists, lawyers (of all sorts), financiers, accountants etc who all deal with tax:

(a) Tax Policy – what is the policy behind a particular tax rule?

(i) Kerrie uses the example of the ATO fact sheet for “People in the Adult Industry”:

(A) e.g. whether or not to tax

(B) under the ATO ruling they are treated as sole traders,

(ii) This is up to Treasury not the ATO – i.e. the tax law is made by treasury (full of lawyers and economists, writing tax policy);

(iii) ATO is an administering body, they do not make the tax laws;

(iv) This is how you make tax make sense, by going to the fundamental rule/policy behind the provisions.

(b) Tax Technical – taxed on income earned and then allowed a deduction on work related expenses

(i) e.g. with the adult industry, could get deduction for pole dancing lessons but not gym membership

(c) Tax Compliance – the need to have an ABN, file tax returns etc.

(i) e.g. in the adult industry, you are required to have an ABN and if earn over a certain amount must register and charge for GST and must keep records and file tax returns etc

(ii) this part of tax is not a comment on how many will apply, rather what should happen.

1.3 Cases have application to tax when you least expect it – e.g. Whittaker – final award of damages (with interest), ATO wanted their share (of her damages), she argued her interest was not assessable.

LAWS5144 | Combined notes 14

Tax policy

1.4 How much tax should be collected?

1.5 Who pays tax?

1.6 TB: table as to who pays (i.e. super funds, companies, individuals, trustees, partnership, mutual insurance association, etc). See 9-1 ITAA 97

The nature of taxation

Defining tax

1.7 Definitions – suggest it is about revenue raising (and that is exactly what it should be):

(a) “Tax” is a “contribution levied on persons, property or business in the support of government”;

(b) “a compulsory exaction of money by a public authority for public purposes enforceable by law”; and

(c) The process of “raising money for the purposes of government by means of contributions from individual persons.

These definitions suggest that tax is about revenue raising – which is what it should be.

Complications

1.8 However, the system (in Australia) is a lot more complicated than just revenue raising, divide into 2 parts:

(a) Revenue raising – i.e. amount earned and tax on that etc; and

(b) Policy reasons – social policy and economic policy:

(i) e.g. currently complying super funds get a concessionary tax rate (15%) c.f. normal rate (30%) – this has nothing to with revenue raising, it is rather, a social and economic policy to encourage saving in super for retirement;

(ii) e.g. similarly, co’s who invest in R&D and venture capital get larger concessions and deductions.

1.9 Therefore, think about why a provision is there and examine what its function is – e.g. deductions on donations to charities to encourage us to do that v higher taxes on cigarettes etc.

Types of taxation within Australia

Direct taxes

LAWS5144 | Combined notes 15

Examples of direct taxes

• Income Taxes: personal income tax (sliding scale above), company tax (30%), poll taxes

(Aus doesn’t have), CGT (but somewhat of a misnomer as capital gains are included under assessable income and is therefore not really a separate tax), gift duty (Aus doesn’t have), inheritance taxes (Aus doesn’t have)

• Property Taxes: death duty (Aus doesn’t have), wealth tax (Aus doesn’t have) • FBT is in separate legislation

1.10 CGT – is not actually a separate tax (and is actually included in the ITAA) – our net capital gain gets included in our income:

(a) it should not be put in with GST or FBT (paid by the employer not the employee);

(b) i.e. these are separate taxes, contained in separate pieces of legislation.

Indirect taxes

Examples of indirect taxes

• Sales Taxes: sales tax (Aus removed when GST introduced in 2000), GST (aka VAT) (10%),

turnover tax (Aus doesn’t have), purchase tax (GST), expenditure tax (GST), stamp duties (some have been abolished e.g. shares, and all were meant to be as part of GST), customs & excise, profits from Government industries

• Factor Taxes: pay-roll tax, land tax (a change from unimproved value to improved value for basis of investment recently as a result of a Court decision – will probably discourage investment in Qld land), real estate tax

1.11 Stamp duties were supposed to be abolished with the introduction of GST, but these are still there.

LAWS5144 | Combined notes 16

Tax as a social process

1.12 What affects the tax system?

(a) political changes – clear when a change of govt there will be tax changes – e.g. Henry Review – root and branch review (probably will change company tax (30% rate – and imputation credits);

(b) economic changes – a recession will obviously create changes – Kerrie thinks it will be interesting to see what will happen in the May Budget – there may be changes there (e.g. more stimulus packages);

(c) social factors – this includes views such as encouraging certain behaviours over others – e.g. super encouragement, alcopops tax (did it honestly have anything to do with revenue raising?) – there are over 300 socially motivated taxes.

2 How a tax system works?

Incidence of Taxation

Types of tax systems

2.1 This is – how does it work in terms of collecting money from us? – i.e. what makes the system works?

2.2 Tax may be either:

(a) Regressive – i.e. takes a decreasing proportion of income as income arises (e.g. takes $1 from everyone – therefore it takes less of income as you earn more ($1/$10 is 10%, $1/$100 is 1% etc);

(b) Proportional – i.e. takes the same portion no matter what we earn (i.e. 10% applied across the board, etc but a higher earner will have a higher amount in their pocket); and

(c) Progressive – i.e. an increasing proportion of tax is paid as your income increases – this is our system with tax brackets etc (e.g. $180,000 = 45% tax (on amounts over $180,000 etc).

How this works in Australia

2.3 In Australia we have a progressive system; therefore, we have Marginal rates of tax and average rates of tax:

(a) Marginal rate of tax – is the bracket in which you fit into (e.g. over $180,000 you pay 45c in every dollar you earn;

(b) Average rate of tax – tax liability as a % of your taxable income – this will always be lower than your marginal tax – i.e. it changes after $180,000 for the top bracket – always get the benefit of the lower marginal rate on the first part of you income:

(i) you will only be paying 45% for amounts over $180,000;

(ii) you will pay nothing on your first $6,000; and

(iii) you will then pay increasing percentages above that until you hit $180,000.

LAWS5144 | Combined notes 17

2.4 Medicare levy = 1.5% but exemption for low-income earners (+ Medicare Levy Surcharge). See Div 785 ITAA 97

2.5 Financial impact of a tax ! i.e. who actually bears the burden of paying the tax:

(a) Formal (nominal) incidence: X is nominated as the taxpayer;

(b) Effective (actual) incidence: X shifts the impact of the tax forwards or backwards to Y, the effective incidence falls with Y;

(c) E.g. manufacturer may be the nominal taxpayer but may be able to shift the effective incidence of the tax forward on to consumers OR employees shifting an income tax backward on to employers by demanding higher wages

Functions and objects of taxation

2.6 Tax was originally to generate revenue for State based projects (i.e. to allow the government to govern; now this is broader):

(a) Enables the government to provide:

(i) social goods – i.e. joint/non rival consumption, e.g. street lighting – something we can all enjoy; and

(ii) merit goods – i.e. deemed beneficial to the user and must meet criteria, e.g. schools (7 year olds entitled to free education but 4 year olds not) and health-system (you have to be sick to actually use it),

(b) Supports those for whom a free market would not otherwise provide – social security, unemployment benefits, pensions, low-cost housing, the $900 handout from KRudd etc (these are examples of our taxpayer money going to this); and

(c) Corrects other free market imperfections – subsidies, e.g. farming subsidies, flood effected subsidies etc.

Criteria for evaluating a tax system

2.7 There are various criteria for evaluating a tax system – and these date back to Adam Smith who came up with the first criteria, and they alter over time. The Ralph Committee talked about: Equity, Simplicity and Certainty.

2.8 Fairness or equity:

(a) Horizontal – taxpayers earning the same amount, pay the same amount of tax (in an ideal system, but does not happen due to concessions etc); and

(b) Vertical – in our system, the more you earn, the more you should pay, but it is a question of how much more and what is appropriate (c.f. a regressive system or a proportional system – see above).

2.9 Simplicity – we all want it to be simple – i.e. in order to reduce compliance costs etc, we have tried to make it simpler:

(a) e.g. E-Tax which automatically uploads information;

(b) also want simplicity in the legislation itself – this has not been achieved in Australia (ITAA 1936 and ITAA 1997 – 1936 was meant to be re-written and replaced with

LAWS5144 | Combined notes 18

1997, but then, this stoped and we now have 2 acts – in looking for a section 1997 has ‘–’ in between sections e.g. 7-5.

2.10 Certainty – we want certainty of:

(a) incidents (who has to actually pay);

(b) liability (easy to work out and how much to pay);

(c) avoidance (how much is being avoided, and govt trying to overcome this; and

(d) fiscal marksmanship or budgeting (how much is the govt getting so they can budget accordingly).

2.11 Efficiency or neutrality – any decisions (business, consumption etc) should be tax neutral:

(a) Therefore, should make decisions without having to consider how much tax will be paid as a result of the decision;

(b) but this is not the case (there will always be examples where this doesn’t occur).

2.12 Flexibility – i.e. ability to adapt to current circumstances (e.g. hardship provisions – victims of the Victorian Bushfires – where there is a link built into the ATO website to discuss exemptions etc).

3 Australia’s tax system

Federal power to make taxation laws

The power to tax

3.1 s 51(ii) of the Constitution - “The Commonwealth Parliament shall have power to make laws with respect to taxation, but not so as to discriminate between States or parts of States”:

(a) this is a concurrent power, but States cannot charge an income tax – as this power has been ceded to the Commonwealth;

(b) the GST was going to be a problem for States, as such, they now get certain percentages (but that caused problems w/ NSW complaining)

Limitations on the Commonwealth power

3.2 s 55 of the Constitution: taxation laws shall deal only with the imposition of taxation: i.e. cannot tie tax laws to other laws;

3.3 s 99 of the Constitution: the Commonwealth may not give preference to any one state – i.e. can’t discriminate between States and parts of States;

3.4 s 114 of the Constitution: the Commonwealth cannot impose tax on property belonging to a state; and

3.5 s 53 of the Constitution: proposed laws imposing taxation shall not originate in the Senate (must originate in House of Representatives) and the Senate cannot amend tax laws, only suggest amendments which the House of Representatives must actually amend.

LAWS5144 | Combined notes 19

Sources of Australian Taxation law

Statute law

3.6 There are the two key acts, but this also includes attached regulations:

(a) Income Tax Assessment Act 1936;

(b) Income Tax Assessment Act 1997;

(i) Both contain definition provisions – e.g. 995-1; and

(ii) See section 1-3 ITAA97: where different words are used

Common law

3.7 The common law has been quite prolific in terms of tax law.

(a) Creation of law to fill a legislative vacuum – i.e. where policy is lacking; and

(b) Statutory interpretation – this is where tax decisions usually fall (e.g. s 6-5 ITAA97 says you are assessed on ‘income according to ordinary concepts’ – courts have interpreted this, because it is not defined in the ITAA97).

The Australian Tax Office

3.8 The practice of the ATO can make tax determinations etc.

3.9 It is not entirely accurate to say the ATO makes law, as the ATO does not make the law, but they put out various quasi-legal documents:

(a) Rulings (TR) – these are the ATO’s views on how the law applies:

(i) usually based on cases – e.g. gives the ATO explanation of cases;

(ii) are binding on the ATO to the extent that if a tax-payers situation fits within the ruling and the tax-payer relies on the ruling the ATO must follow the ruling;

(iii) but are not binding on the tax-payer – obviously though, ATO may take you to court over it – these may sometimes be wrong (e.g. their interpretation of a case);

(iv) They are a pretty good source of information and give useful examples,

(b) There are also determinations, etc.

History of Australian taxation law

3.10 Pre-World War II

(a) Customs and Excise duties

(b) 1915 Commonwealth Income Tax

3.11 The 1960’s

LAWS5144 | Combined notes 20

(a) Need for reform; and

(b) System was in dire-straits.

3.12 1970’s-1980’s

(a) The era of tax avoidance – greed is good;

(b) Everyone did everything they could do avoid tax – the Bottom of the Harbour Schemes.

3.13 Labor Government reforms (Hawke and Keating)

(a) CGT (1985) – remember this is really not a separate ‘tax’; and

(b) FBT (1986).

3.14 Liberal Government reforms (Howard and Costello)

(a) GST (2000); and

(b) the Ralph Business reforms (partially dealt with selling the GST)

3.15 Rudd Labor Government – 2008 Henry Review, it will be interesting to see where this will lead.

4 General overview of tax

Income tax basics

The tax formula

4.1 The tax formula – s 4-1 ITAA97 (starting point) – remember this formula:

Income tax Payable =

Taxable Income x Tax rate – Tax offsets

Where Taxable Income = Assessable income – deductions

4.2 Attempts to get to an income tax payable:

(a) Accessible income – 5-6 weeks of the course – CGT comes in here;

(b) When you get lost in the course, come back to the formula and work out which part we’re looking at;

(c) This formula will help make the course make sense;

(d) s 4-1 ITAA97 is the starting point for the calculation of tax; and

(e) See also the pyramid which Kerrie does not think is particularly useful – s 2-5 ITAA97 contains the pyramid (and this was put in to show how the act should work).

LAWS5144 | Combined notes

The core provisions

4.3 See below for an illustration of how the core provisions operate.

The Tax Pyramid

NB – the international aspects of income taxation concerned with the core provisions.

The core provisions explained

Ordinary income

4.4 This is always the starting point in our analysis of income tax.

4.5 We will identify the amount of income (c.f. capital) which are assessable

4.6 Div 6 of the ITAA97 deals with income and is divided into various categoriesand non-assessable income as well)

4.7 The first step in the taxation process is to examine a flow of money inwards and determine whether that flow of money represents inc

4.8 Since most income we will consider in this subject is assessable, it is important to identify it (as distinct from capital) and determine the amount of it (for the purposes of calculating income tax payable).

Statutory and non-assessable income

4.9 The next step is to look at specific types of income and see how they are treated for taxation purposes. This includes examining exempt income and statutory income as well as income from property.

Income tax accounting

See below for an illustration of how the core provisions operate.

international aspects of income taxation – will not be dealt with in this course, we are

provisions explained

tarting point in our analysis of income tax.

We will identify the amount of income (c.f. capital) which are assessable – s 6-5.

of the ITAA97 deals with income and is divided into various categories (e.g. statutory assessable income as well).

The first step in the taxation process is to examine a flow of money inwards and determine whether that flow of money represents income.

Since most income we will consider in this subject is assessable, it is important to identify it (as distinct from capital) and determine the amount of it (for the purposes of calculating

assessable income

next step is to look at specific types of income and see how they are treated for taxation purposes. This includes examining exempt income and statutory income as well as income

21

will not be dealt with in this course, we are

.

(e.g. statutory

The first step in the taxation process is to examine a flow of money inwards and determine

Since most income we will consider in this subject is assessable, it is important to identify it (as distinct from capital) and determine the amount of it (for the purposes of calculating

next step is to look at specific types of income and see how they are treated for taxation purposes. This includes examining exempt income and statutory income as well as income

LAWS5144 | Combined notes 22

4.10 Third, in the income component is the accounting treatment. This is because the law varies from accounting principles.

4.11 For example, trading stock is treated differently in determining the taxation burden from the accounting for stock that we have covered in our introductory studies.

Capital gains tax

4.12 Capital as distinct from income flows is then considered, particularly the taxation of capital gains realised on the sale of capital items (as distinct from trading stock).

4.13 Even though we imply that it is a separate tax, there is no such thing – it is just included in our assessable income.

General deductions

4.14 See s 8-1 ITAA97 – when all of the possible sources of income have been considered and their eligibility for taxation purposes considered, those items which constitute assessable income will be added together, from which amount will be deducted items the taxation regime allows.

4.15 NB – deductions are not offsets and are not as valuable as offsets – which come off the final figure (see formula).

Specific deductions

4.16 Also s 8-5 ITAA97 – examples will be considered (Div 25 ITAA97 has a lot of specific deduction provisions).

4.17 NB – deductions are not offsets and are not as valuable as offsets – which come off the final figure (see formula).

Capital allowances and car expenses

4.18 We are allowed deductions for expenditure where the item purchased lasts for more than one year

Tax offsets

4.19 A generic term in the ITAA97 to refer to credits and rebates – have nothing to do with revenue raising (usually social policy) – e.g. childcare rebate.

4.20 Once the income and deductions from income have been determined, a net amount of assessable income is then calculated, from which a preliminary amount of tax payable may be calculated. This amount of taxation payable is called basic tax payable. Basic tax payable may then be adjusted for amounts we will generally refer to as offsets.

4.21 These can throw out the idea of horizontal equity – but are different to deductions – they are not taken off assessable income, rather they are offset at the end and are much more valuable.

Tax payable

4.22 From the previous process, we are able to account for other amounts to arrive at a sum of money which amounts to the individual taxpayer’s share of the taxation burden or a refund of money owed to the taxpayer.

LAWS5144 | Combined notes 23

4.23 Kerrie wants us to look at the tax rates, from 15% up to 45% - they are in the learning unit and see if you can have a fiddle and work out how to calculate them!

LAWS5144 | Combined notes 24

Topic 2 Residence and source

1 Introductory principles for calculating ‘taxable income’

Introduction

1.1 The following provisions are general provisions relating to calculating income for tax purposes – i.e. your assessable income.

1.2 This does not necessarily follow ordinary meanings of income and there are process which must be applied to work out what is assessable income.

1.3 These provisions are found in Div 4 – a core division of the ITAA97 – and it explains the whole process of working out income tax payable.

1.4 The provisions below apply equally to assessing what is assessable income as to whether someone is an Australian resident or not for tax purposes.

Section 4-10(3)

1.5 This is the tax formula and it is used to work out your income tax for the financial year:

Income Tax =

(taxable income x rate) – offsets