laws on long-term prices

TRANSCRIPT

LAWS ON LONG-TERM PRICES*

byCHRISTIAN BIDARD

University of Paris XöNanterre

Long-term prices depend on distribution in a complex way, especiallywhen choice of technique is allowed. It is shown, however, that themovement of prices in terms of wage obeys certain laws. Moreprecisely the movement is characterized in terms of linear program-ming problems. Necessary or su¤cient conditions connected with theconvexity of the wage^pro¢t curves are also obtained. But, with regardto the relative prices of commodities, they vary arbitrarily, so thatthe Wicksell price e¡ects are not under control.

" Introduction

How do long-term prices vary with distribution? The technical aspects ofthe analytical treatment should not hide the importance of the question foreconomic theory.

Sra¡a's formalization of long-term prices is adopted (Sra¡a, 1960).Every commodity i is reproduced by means of commodities and homo-geneous labour; its price pi is equal to the total value of its inputsincreased by a rate of pro¢t (or interest) r. The assumption that the rateof pro¢t is uniform among all industries stems from the classicaltradition and is also adopted in modern analyses of long-term states.When the operated technique �A; l � and the pro¢t rate r are given, theprice and wage vector �p;w�, which is determined up to a factor, isobtained by solving a homogeneous system of equations. The prices arecalled `prices of production' according to the classical tradition becausethey depend on the technical characteristics of production, not ondemand. But they also depend upon distribution as re£ected by the levelof the pro¢t rate.

We are interested in the deformation of the price and wage vectorwhen distribution varies, e.g. the pro¢t rate increases. Two laws havelong been admitted. One is the famed Ricardian trade-o¡. It states thatall prices in terms of wage (i.e. prices pi=w obtained when labour ischosen as numeraire) increase with the pro¢t rate. Or, equivalently, thereal wage w=pi in terms of any commodity i is a decreasing function ofthe pro¢t rate (this relationship is represented by a decreasing r^w curve;the curve itself depends on the commodity or basket chosen asnumeraire). The Ricardian law can be established rigorously (Sra¡a,

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.Published by Blackwell Publishers Ltd, 108 Cowley Road, Oxford OX4 1JF, UK, and 350 Main Street, Malden, MA 02148, USA.

453

The Manchester School Vol 66 No. 4 September 19980025^2034 453^465

*Manuscript received 30.1.96; ¢nal version received 8.7.97.

1960, Section 49). A second `law' concerning the change of relative priceshas been less fortunate: the classicals thought that, when industry i ismore capital-intensive than industry j, the relative price pi=pj increaseswith the pro¢t rate. This statement does not hold true in general becausethe so-called `capital-intensive' industry might use `labour-intensive'inputs. More radically, the very distinction between capital-intensive andlabour-intensive industries is not founded. Sra¡a's only conclusion(Sra¡a, 1960, Section 20) is that `the pattern of the price-variationsarising from a change in distribution [is] complex'. This assertion is a bittoo pessimistic. The price movement can partly be disentangled (the ¢rststudy is by Schefold, 1976): for instance it has been shown that it ismonotonic when some adequately de¢ned viewpoint is adopted (Bidard,1991, Ch. 5; Bidard and Salvadori, 1995; Bidard and Krause, 1996;Bidard and Steedman, 1996; see Bidard and Ehrbar, 1996, for a com-prehensive study).

The question addressed here is more involved, because choice oftechnique is now allowed. When the pro¢t rate is at level rm, the operatedtechnique is represented by a couple �Am; lm� and the price and wage vector�pm;wm� is calculated on the basis of that technique for that rate of pro¢t.The operated methods are themselves chosen on the basis of a cost-minimization criterion, thus satisfying the condition that no alternativemethod yields extra pro¢ts. With choice of technique the Ricardian trade-o¡ still holds, though not the other laws of motion mentioned above. Thequestion arises whether additional properties of the price and wage vectorsin the presence of choice of technique exist. To our knowledge, this hasnever been discussed.

The existence of additional laws (Section 2) is suggested by the`corn model'. Assume there is only one good, say corn, in the economy,but several methods of production. If the technique (corn input a andlabour input l per unit of corn produced) is given and corn is chosenas numeraire, the r^w curve will be a decreasing straight line (itsequation is �1� r�a� wl � 1). As the operated method of productionmay change with distribution, the one �am; lm� adopted at the pro¢trate rm according to the cost-minimization criterion satis¢es a wage-maximization property. Therefore the r^w curve for the whole economyis the upper envelope of the straight lines rm^wm associated with theavailable techniques. The Ricardian trade-o¡ is tantamount to the factthat the envelope is decreasing. The envelope, however, has one moreproperty: it is also convex by construction. To sum up, in a one-sectormodel, the price of corn must vary in such a way that the r^w curveis decreasing (trade-o¡ ) and convex (additional property). In a multi-sectoral economy the shape of the r^w curve depends on the numeraire,but Theorem 1(iii) claims that some weak form of convexity ismaintained.

454 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

Let us be ambitious. We would not only like to ¢nd some propertiesof the price vectors in terms of wage, but derive all of them. This will beachieved when, considering M arbitrary rates of pro¢t and M arbitrarypositive vectors, we are able to recognize whether these vectors can beidenti¢ed with price vectors for some economy. Section 3 proposes such analgebraic characterization, stated in terms of linear programming(Theorem 2). The result allows us to understand better the nature of theproblem and obtain more results (Theorem 3 for any number of pricevectors, Corollaries for the two- and three-sets of prices).

The two main applications of this characterization are found inSection 4. A partial converse of the convexity law seen in Theorem 1(iii)is ¢rst obtained as Theorem 4. Given any positive vectors which arecandidates for being price vectors at given rates of pro¢t, let us build theassociated points �r;wi � w=pi� when commodity i is chosen as numeraire.If they lie on a convex curve for any i, then the vectors considered areprice vectors for some economy. The second conclusion concerns relativeprices. Let us now forget the wage component of the price and wagevectors and only consider the exchange ratios between commodities. Therelative prices do vary with the pro¢t rate except when the organiccomposition of the economy is uniform. In the context of the theory ofcapital, these changes are often called the `Wicksell price e¡ects' and havebeen identi¢ed as the source of many di¤culties: if relative prices didnot change, the various input items might be aggregated by using theinvariant prices as relative weights and all would happen as if, instead ofbeing made of heterogeneous capital goods, the capital was a `jelly'.Brie£y, most of the properties of the one-good model represented by theproduction function Q � f �K; L � would still hold true for multisectoralmodels. The attempt to build such a `surrogate production function'(Samuelson, 1962) fails precisely because of the variation of relativeprices (Garegnani, 1970).

Finding laws on relative prices would put the Wicksell e¡ectsunder control. If these e¡ects are not too important, the constructionof an `approximate aggregated function' is expected, associated withsome upper bound for the deviations between the one-commodity andthe multisectoral models. (The one-commodity model is intensivelyused for instance in macroeconomics as a proxy for a disaggregatedmodel.)

Theorem 5 does ¢nd all laws on relative prices: there are none! Inother words, given ten rates of pro¢t and ten arbitrary positive vectors,there exists a multisectoral economy in which these vectors representthe relative price vectors pm at these rates of pro¢t rm. The anarchy ofthe relative prices is an important negative result for the theory ofcapital and condemns it to remain basically a blank page of economictheory.

Laws on Long-term Prices 455

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

á Some Properties of Long-term Prices

Let there be G goods indexed by i; j or k varying from 1 to G. Everycommodity i can be reproduced by means of one or several processes,the mth method �m � 1; . . . ;M� being described by its vector of technicalcoe¤cients and its labour coe¤cient per unit of product i: �am

i ; lmi � 2

RG� � R�. Let method m be operated at the rate of pro¢t rm. With wages

paid post factum, the associated price and wage vector �pm;wm� 2 RG� � R�

satis¢es

�1� rm�pmami � wmlm

i � pmi �1:i:m�

(pm is written as a row vector whose jth component is pmj ; am

i is a columnvector). Prices in terms of wage are obtained by setting wm � 1:

�1� rm�pmami � lm

i � pmi �2:i:m�

The inequality

�1� rm�pmani � l n

i � pmi �3:i:m:n�

means that no alternative process n in industry i is more pro¢table thanthe operated one m at the given prices pm. Given rm, a speci¢c process�am

i ; lmi � is thus selected in every industry i (the same method may be

operated at di¡erent pro¢t rates). Equations (2.1.m)^�2:G:m� de¢ne theprice vector pm associated with the dominant technique �Am; lm� � �am

i �; �lmi �

at the pro¢t rate rm. Vector pm is strictly positive if the factor of pro¢tRm � 1� rm is smaller than the inverse of the Perron^Frobenius root ofmatrix Am and if labour is directly or indirectly necessary to production,which will be assumed.

A well-known property is that all prices in terms of wage increasewith the pro¢t rate (Sra¡a, 1960, Section 94). This is statement (i) inTheorem 1. Is that the only property of prices? No, since they also satisfystatements (ii) and (iii). Note the simplicity of the direct proofs: the onlydi¤culty is to guess the properties to be established. These properties arenew in the economic literature and have initially been obtained by meansof the dual method explained in the next section. Symbols x� 0, x > 0,x � 0 denote respectively the positivity, semi-positivity and non-negativityof vector x.

Theorem 1Let r1 < r2 < r3 be three factors of pro¢t and p1; p2; p3 the correspondingprice vectors in terms of wage �w � 1�. Then we have the following.(i) Prices in terms of wage increase with the pro¢t rate:

0� p1 � p2 � p3 �4�

456 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

(ii) For any i such that p2i 6� p1

i

p3i ÿ p2

i

p2i ÿ p1

i

� supj

�1� r3�p3j ÿ �1� r2�p2

j

�1� r2�p2j ÿ �1� r1�p1

j

�5:i�

(iii) Let k be a commodity for which the expression on the right-handside of �5:i� is maximum. When wages are measured in terms of k,the three points �w1; r1�; �w2; r2�; �w3; r3� belong to a non-increasingconvex curve.

Proof(i) Let i be a commodity such that p2

i =p1i � inf j�p2

j =p1j �, denoted a. We

have

p2 � ap1 �6�and

p2i � ap1

i �7�Relationships �2:i:2�, (6), 1� r2 � R2 > R1 � 1� r1, �3:i:1:2� and (7) aresuccessively used to obtain

p2i � R2p2a2

i � l 2i

� aR2p1a2i � l 2i � aR1p1a2

i � l 2i � a�p1i ÿ l 2i � � l 2i

� p2i � �1ÿ a�l 2i

A comparison of the extreme terms shows that a � 1 if l 2i > 0, and (4)follows from (6). If l 2i � 0, method 2 can be approximated by a methodwith a positive labour coe¤cient and inequality (4) still holds. (Sinceproduction by labour alone is not excluded, in which case pm

i � lmi , the

monotonicity property holds sensu lato.)

(ii) For any i, relationships �2:i:2� and �3:i:1:2�, then �2:i:2� and �3:i:3:2�,are successively used to obtain

�R2p2 ÿ R1p1�a2i � �R2p2a2

i � l 2i � ÿ �R1p1a2i � l 2i � � p2

i ÿ p1i

�R3p3 ÿ R2p2�a2i � �R3p3a2

i � l 2i � ÿ �R2p2a2i � l 2i � � p3

i ÿ p2i

If a2i � 0, these inequalities imply �5:i�. If a2

i � 0, method 2 can beapproximated by a method with positive input coe¤cients and inequality�5:i� still holds.

(iii) For good k de¢ned in the theorem, with the degeneracy p2k � p1

k beingstudied separately, inequality �5:k� can also be written, using determinantsand the notation wa � 1=pa

k for a � 1; 2; 3 (wa is the real wage in terms ofcommodity k at the pro¢t rate ra ),

Laws on Long-term Prices 457

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

0 �0 0 1

p3k ÿ p2

k p1k ÿ p2

k p2k

R3p3k ÿ R2p2

k R1p1k ÿ R2p2

k R2p2k

��������������

�1 1 1p1

k p2k p3

k

R1p1k R2p2

k R3p3k

��������������

� p1kp

2kp

3k

w1 w2 w3

1 1 1R1 R2 R3

��������������

0 �w1 w2 ÿ w1 w3 ÿ w2

1 0 0R1 r2 ÿ r1 r3 ÿ r2

������������ � �r3 ÿ r2��r2 ÿ r1� w3 ÿ w2

r3 ÿ r2ÿ w2 ÿ w1

r2 ÿ r1

� �

Hence the convexity property. &

â Characterization of Price Vectors

The question is whether all properties of price vectors are now found.Given two arbitrary positive vectors such that p1 � p2, does there exist aneconomy for which they are price vectors in terms of wage at given ratesof pro¢t r1 < r2? (The answer is positive.) Or, given three positive vectorsp1; p2; p3 which satisfy the conditions set in Theorem 1, are they pricevectors for some economy? (Not necessarily.) And so on.

De¢nition 1. Let there be M given positive rates of pro¢t rm

�m � 1; . . . ;M�. The positive vectors pm 2 RG� �m � 1; . . . ;M� are a set of

price vectors in terms of wage if there exist semi-positive vectors �ami ; l

mi �

such that conditions (2) and (3) hold for any triple i;m; n of indices�1 � i � G; 1 � m; n �M�.

The tool for the study is a transformation of relationships (2) and(3) by duality. More precisely the theorem of the alternative states that,for given vectors pm, there exist technical and labour coe¤cients (whichare now the unknowns) satisfying equalities (2) and inequalities (3) if andonly if some other system has no solution. The result is expressed in termsof linear programming.

De¢nition 2. For given indices i in f1; . . . ;Gg and m in f1; . . . ;Mg and agiven set of positive vectors fpm;m � 1; . . . ;Mg, let �Pm

i � be the linearprogramming problem in the Mÿ 1 non-negative scalar variablesfym; m � 1; . . . ;M;m 6� mg de¢ned by

458 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

�Pmi � V

mi � max

Xm 6�m

pmi ym subject toX

m 6�mym � 1 �8:1�

8j � 1; . . . ;GXm 6�m�1� rm�pm

j ym � �1� rm�pmj �8:2:j �

ym � 0 �m � 1; . . . ;M; m 6� m�The set fpm; m � 1; . . . ;Mg is said to satisfy property (P) if, for any indexi in f1; . . . ;Gg and any index m in f1; . . . ;Mg, the value V

mi of programme

�Pmi � is at most equal to p

mi .

Theorem 2fpm; m � 1; . . . ;Mg is a set of price vectors if and only if property (P)holds.

ProofFor any given i and n � m, conditions �2:i:m� and �3:i:m:m� for m � 1; . . . ;Mare a set of inequalities (the one equality �2:i:m� for m � m is replaced by twoinequalities with opposite signs � and �) which, being a¤ne in coe¤cientsami j and l

mi , is written as

�Q� ami

lmi

� �� �b�

By the theorem of the alternative, the existence of a semi-positive vector

ami

lmi

� �satisfying such a relationship is equivalent to the non-existence of a semi-positive row vector z � �z1; . . . ; zm; �zm; . . . ; zM� with M� 1 componentssuch that zQ � 0 and zb > 0. Matrix Q and vector b are equal to

Q �

R1p1 1

..

. ...

Rmpm 1ÿRmpm ÿ1

..

. ...

RMpM 1

266666666664

377777777775b �

p1i

..

.

pmi

ÿpmi

..

.

pMi

0BBBBBBBBBB@

1CCCCCCCCCCALet y � �y1; . . . ; ym; . . . ; yM� be the row vector with M components de¢nedby ym � zm � 0 for m 6� m and ym � zm ÿ �zm. Conditions zQ � 0 and zb > 0are written

Laws on Long-term Prices 459

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

XMm�1

ym � 0 �9:1�

XMm�1

Rmpmj ym � 0 � j � 1; . . . ;G� �9:2:j �

XMm�1

pmi ym > 0 �9:3�

Condition (9.1) shows that component ym is negative and, after homothetyon y, equality y m � ÿ1 is set without loss of generality. The non-existenceof a solution to system (9) amounts to saying that, when the non-negativevariables fym; m 6� mg are subject to the 1� G constraints (9.1) and (9.2),the value of

Pm 6�m pm

i ym ÿ pmi is at most equal to zero. Theorem 2 is another

expression of the same property. &

The dual characterization is useful to obtain non-obvious results.

Theorem 3Let M � G� 2. fpm; m � 1; . . . ;Mg is a set of M price vectors if and onlyif any subset of G� 2 vectors is a set of price vectors.

ProofThe condition is necessary. Conversely, assume that fpm; m � 1; . . . ;Mgis not a set of price vectors, i.e. the maximum value V

mi of programme

�P mi � is greater than p

mi for some �i; m�. The constraints (8.1) and (8.2)

de¢ne 1� G a¤ne inequalities on the Mÿ 1 non-negative variables ym,m 6� m, and the maximum value is reached at some vertex of thecorresponding polyhedron in RMÿ1

� , when Mÿ 1 inequalities are binding.If inequality 1� G < Mÿ 1 holds, any vertex has a null component ym1 .According to Theorem 2 the subset fpm; m 6� m1g is not a set of pricevectors. By induction some subset of G� 2 vectors is not a set of pricevectors. &

Another application of Theorem 2 is the algebraic characterizationof two- and three-sets of price vectors.

Corollary 1. Given r1 < r2, two positive vectors p1 and p2 are pricevectors in terms of wage at these pro¢t rates if and only if p1 � p2.

Proof. For M � 2, let us calculate the values of programmes �P mi � for

any i and m � 1; 2. If p1i > p2

i then val�P2i � > p2

i . Conversely, if p1i � p2

i , thenval�P1

i � � R1p1i =R

2 < p1i and val�P2

i � � p1i � p2

i . The conclusion follows fromTheorem 2. &

460 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

For M > 2 a set of price vectors is also non-decreasing. Conversely,let us consider a non-decreasing sequence of positive vectors. Forr1 � . . . � rM, m � 1 and y satisfying constraint �8:2:j �, we have

�1� r1�Xm 6�1

pmj ym �

Xm>1

�1� rm�pmj ym � �1� r1�p1

j

Similarly, for m �M and y satisfying constraint (8.1), we haveXm 6�M

pmj ym � pM

j

Xm<M

ym � pMj

The last two inequalities show that the conditions val�Pmi � � p

mi are

automatically satis¢ed for the extreme values m � 1 and m �M. If M � 3we thus obtain the following corollary.

Corollary 2. A three-set 0� p1 � p2 � p3 of vectors is a set of pricevectors if and only if, for any i � 1; . . . ;G, the value of the programme

maxy1�0;y3�0

p1i y

1 � p3i y

3 subject to

y1 � y3 � 1 �10:1�8j � 1; . . . ;G �1� r1�p1

j y1 � �1� r3�p3

j y3 � �1� r2�p2

j �10:2:j �

is at most equal to p2i .

Proof. Conditions (10) mean that val�P mi � � p

mi for m � 2. Since the

analogous inequalities are satis¢ed for m � 1 and m �M � 3, Theorem 2applies. &

Problem (10) can be analysed by means of a geometrical represent-ation in the �y1; y3� plane. The feasible set F is a non-empty polygonOMMkMkl . . .N (Fig. 1). The equation of the straight line �Dj� is given byrelationship �10:2:j � written as an equality, and k is the index for whichthe ¢rst coordinate of Mk is maximal, which corresponds to the samechoice k as in Theorem 1. Conditions (10) are satis¢ed if and only if thevalue of p1

i y1 � p3

i y3 is not greater than p2

i at all vertices of F (which is thecase at points O and M). A fully algebraic characterization is thusobtained, but its explicit expression depends on the shape of F accordingto various parameters. However, a necessary condition is that the valueof the objective function at point Mk is at most equal to p2

i . It is left tothe reader to check that this is condition �5:i� in Theorem 1. And, sincethe feasible set is included in OMMkNk (Fig. 1), a su¤cient condition isthat the same inequality also holds at point Nk. Therefore we haveCorollary 3.

Laws on Long-term Prices 461

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

Corollary 3. Let there be a three-set of vectors satisfying conditions (i)and (ii) in Theorem 1. If, for any i, inequality

p3i

p2i

� �1� r3�p3k

�1� r2�p2k

holds, it is a three-set of price vectors.

ã Families of Price Vectors

The main synthetic results are now stated. The su¤cient condition inTheorem 4 is reminiscent of the necessary condition in Theorem 1(iii).

Theorem 4For a set of positive vectors to be a set of price vectors in terms of wage,it is su¤cient that, for any commodity, all points �rm;wm� belong to a non-increasing convex curve.

ProofLet 0� p1 � . . . � pm � . . . � pM, and assume that these vectors are notprice vectors in terms of wage. According to Theorem 2, the value of �Pb

i �exceeds p

bi for some i and some b. This is a fortiori the case when all

constraints �8:2:j � for j 6� i are omitted, i.e. for the linear programmingproblem �Qb

i �:

Fig. 1 Study of Three-sets of Vectors

O M 1

462 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

maxXm 6�b

pmi ym subject toX

m 6�bym � 1 �11:1�X

m 6�bRmpm

i ym � Rbpbi �11:2�

ym � 0 �m � 1; . . . ;M; m 6� b�Inequality

Pm 6�b pm

i ym > pbi therefore holds at some vertex of the non-empty

polyhedron in the y-space in RMÿ1� de¢ned by the two constraints (11.1)

and (11.2). Any vertex has two positive components at most. The case ofone positive component is easily eliminated. Therefore the maximum valueof �Qb

i � is reached when constraints (11.1) and (11.2) are binding, withvector y admitting two positive components ya and yg only. To sum up, ifthe initial set of vectors is not a set of price vectors, there exist a and g,with ra < rg, such that the solution to

ya � yg � 1 �12:1�Rapa

i ya � Rgp

gi y

g � Rbpbi �12:2�

satis¢es inequalities ya > 0; yg > 0 and pai y

a � pgi y

g > pbi . There follows

Ra < Rb < Rg and, after calculation of ya and yg from (12.1) and (12.2),inequality �pg

i ÿ pbi �=�pg

i ÿ pai � > �Rgp

gi ÿ Rbp

bi �=�Rgp

gi ÿ Rapa

i � is obtained.When this relationship is transformed by choosing good i as numeraire, itappears that the r^w curve is not convex. In other words, the convexityassumption stated in Theorem 4 implies that the set of vectors which iscontemplated is a set of price vectors. &

De¢nition 3. Let there be G commodities and M given rates of pro¢t. Agiven set of M positive vectors fpm;m � 1; . . . ;Mg in RG

� is a set of relativeprice vectors if, for some economy, vectors pm are representative of theexchange ratios between the commodities at these rates of pro¢t. In otherwords, there exist positive scalars wm such that fpm=wmg is a set of pricevectors in terms of wage.

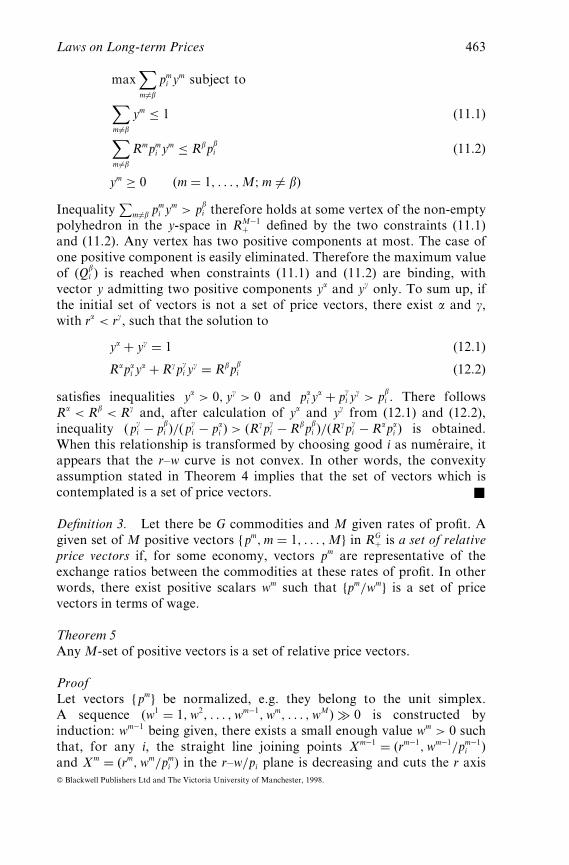

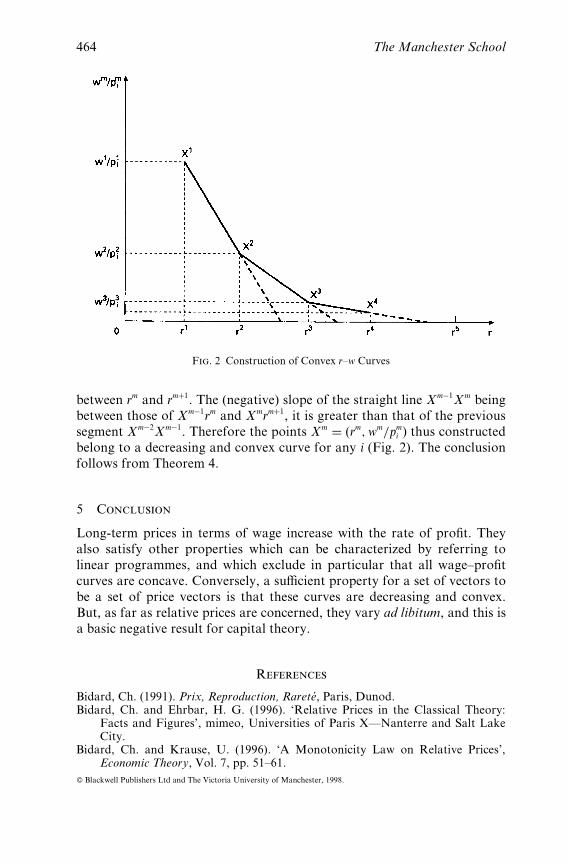

Theorem 5Any M-set of positive vectors is a set of relative price vectors.

ProofLet vectors fpmg be normalized, e.g. they belong to the unit simplex.A sequence �w1 � 1;w2; . . . ;wmÿ1;wm; . . . ;wM� � 0 is constructed byinduction: wmÿ1 being given, there exists a small enough value wm > 0 suchthat, for any i, the straight line joining points Xmÿ1 � �rmÿ1;wmÿ1=pmÿ1

i �and Xm � �rm;wm=pm

i � in the r^w=pi plane is decreasing and cuts the r axis

Laws on Long-term Prices 463

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

between rm and rm�1. The (negative) slope of the straight line Xmÿ1Xm beingbetween those of Xmÿ1rm and Xmrm�1, it is greater than that of the previoussegment Xmÿ2Xmÿ1. Therefore the points Xm � �rm;wm=pm

i � thus constructedbelong to a decreasing and convex curve for any i (Fig. 2). The conclusionfollows from Theorem 4.

ä Conclusion

Long-term prices in terms of wage increase with the rate of pro¢t. Theyalso satisfy other properties which can be characterized by referring tolinear programmes, and which exclude in particular that all wage^pro¢tcurves are concave. Conversely, a su¤cient property for a set of vectors tobe a set of price vectors is that these curves are decreasing and convex.But, as far as relative prices are concerned, they vary ad libitum, and this isa basic negative result for capital theory.

References

Bidard, Ch. (1991). Prix, Reproduction, Rarete, Paris, Dunod.Bidard, Ch. and Ehrbar, H. G. (1996). `Relative Prices in the Classical Theory:

Facts and Figures', mimeo, Universities of Paris XöNanterre and Salt LakeCity.

Bidard, Ch. and Krause, U. (1996). `A Monotonicity Law on Relative Prices',Economic Theory, Vol. 7, pp. 51^61.

Fig. 2 Construction of Convex r^w Curves

464 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.

Bidard, Ch. and Salvadori, N. (1995). `Duality between Prices and Techniques',European Journal of Political Economy, Vol. 11, pp. 379^389.

Bidard, Ch. and Steedman, I. (1996). `Monotonic Movement of Price Vectors',Economic Issues, Vol. 1, Part 2, pp. 41^44.

Garegnani, P. (1970). `Heterogeneous Capital, the Production Function and theTheory of Distribution', Review of Economic Studies, Vol. 37, pp. 407^436.

Samuelson, P.A. (1962). `Parable and Realism in Capital Theory: the SurrogateProduction Function', Review of Economic Studies, Vol. 29, pp. 193^206.

Schefold, B. (1976). `Relative Prices as a Function of the Rate of Pro¢t: aMathematical Note', Zeitschrift fÏr NationalÎkonomie, Vol. 36, pp. 21^48.

Sra¡a, P. (1960). Production of Commodities by Means of Commodities, Cambridge,Cambridge University Press.

Laws on Long-term Prices 465

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 1998.