law of large number and central limit theorem under - math tube

TRANSCRIPT

Law of Large Number and Central Limit Theoremunder Uncertainty, the Related New Ito’s Calculus

and Applications to Risk Measures

Shige Peng

Shandong University, Jinan, China

Presented at

1st PRIMA Congress, July 06-10, 2009

UNSW, Sydney, Australia

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 1

/ 53

A Chinese Understanding of Beijing Opera

A popular point of view of Beijing opera by Chinese artists

,

Translation (with certain degree of uncertainty)

The universe is a big opera stage,

An opera stage is a small universe

Real world ⇐⇒ Modeling world

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 2

/ 53

A Chinese Understanding of Beijing Opera

A popular point of view of Beijing opera by Chinese artists

,

Translation (with certain degree of uncertainty)

The universe is a big opera stage,

An opera stage is a small universe

Real world ⇐⇒ Modeling world

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 2

/ 53

A Chinese Understanding of Beijing Opera

A popular point of view of Beijing opera by Chinese artists

,

Translation (with certain degree of uncertainty)

The universe is a big opera stage,

An opera stage is a small universe

Real world ⇐⇒ Modeling world

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 2

/ 53

Scientists point of view of the real world after Newton:

People strongly believe that our universe is deterministic: it can be

precisely calculated by (ordinary) differential equations.

After longtime explore

our scientists begin to realize that our universe is full of uncertainty

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 3

/ 53

Scientists point of view of the real world after Newton:

People strongly believe that our universe is deterministic: it can be

precisely calculated by (ordinary) differential equations.

After longtime explore

our scientists begin to realize that our universe is full of uncertainty

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 3

/ 53

A fundamental tool to understand and to treatuncertainty: Probability Theory

Pascal & Fermat, Huygens, de Moivre, Laplace, · · ·

Ω: a set of events: only one event ω ∈ Ω happens but we don’t know

which ω (at least before it happens).

The probability of A ⊂ Ω:

P(A) number times A happens

total number of trials

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 4

/ 53

A fundamental tool to understand and to treatuncertainty: Probability Theory

Pascal & Fermat, Huygens, de Moivre, Laplace, · · ·

Ω: a set of events: only one event ω ∈ Ω happens but we don’t know

which ω (at least before it happens).

The probability of A ⊂ Ω:

P(A) number times A happens

total number of trials

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 4

/ 53

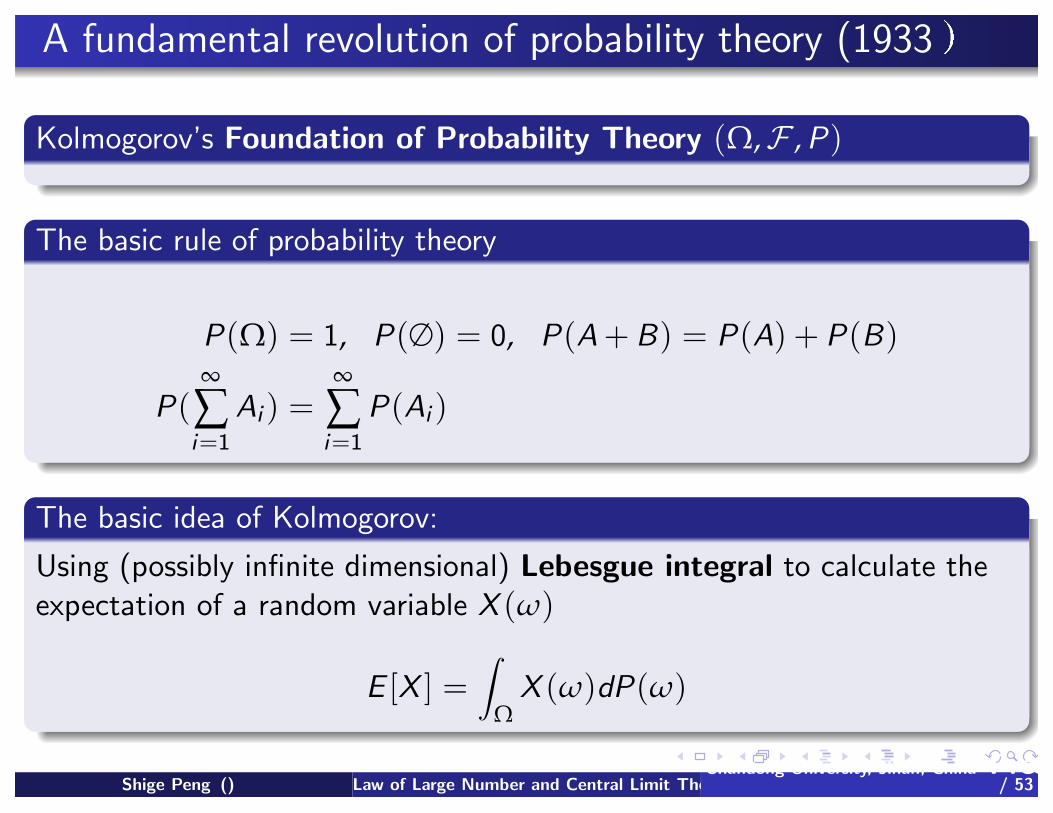

A fundamental revolution of probability theory (1933

Kolmogorov’s Foundation of Probability Theory (Ω,F , P)

The basic rule of probability theory

P(Ω) = 1, P(∅) = 0, P(A + B) = P(A) + P(B)

P(∞

∑i=1

Ai ) =∞

∑i=1

P(Ai )

The basic idea of Kolmogorov:

Using (possibly infinite dimensional) Lebesgue integral to calculate the

expectation of a random variable X (ω)

E [X ] =

ΩX (ω)dP(ω)

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 5

/ 53

A fundamental revolution of probability theory (1933

Kolmogorov’s Foundation of Probability Theory (Ω,F , P)

The basic rule of probability theory

P(Ω) = 1, P(∅) = 0, P(A + B) = P(A) + P(B)

P(∞

∑i=1

Ai ) =∞

∑i=1

P(Ai )

The basic idea of Kolmogorov:

Using (possibly infinite dimensional) Lebesgue integral to calculate the

expectation of a random variable X (ω)

E [X ] =

ΩX (ω)dP(ω)

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 5

/ 53

A fundamental revolution of probability theory (1933

Kolmogorov’s Foundation of Probability Theory (Ω,F , P)

The basic rule of probability theory

P(Ω) = 1, P(∅) = 0, P(A + B) = P(A) + P(B)

P(∞

∑i=1

Ai ) =∞

∑i=1

P(Ai )

The basic idea of Kolmogorov:

Using (possibly infinite dimensional) Lebesgue integral to calculate the

expectation of a random variable X (ω)

E [X ] =

ΩX (ω)dP(ω)

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 5

/ 53

vNM Expected Utility Theory: The foundation of moderneconomic theory

E [u(X )] ≥ E [u(Y )] ⇐⇒ The utility of X is bigger than that of Y

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 6

/ 53

Probability Theory

Markov Processes

Ito’s calculus: and pathwise stochastic analysis

Statistics: life science and medical industry; insurance, politics;

Stochastic controls;

Statistic Physics;

Economics, Finance;

Civil engineering;

Communications, internet;

Forecasting: Whether, pollution, · · ·

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 7

/ 53

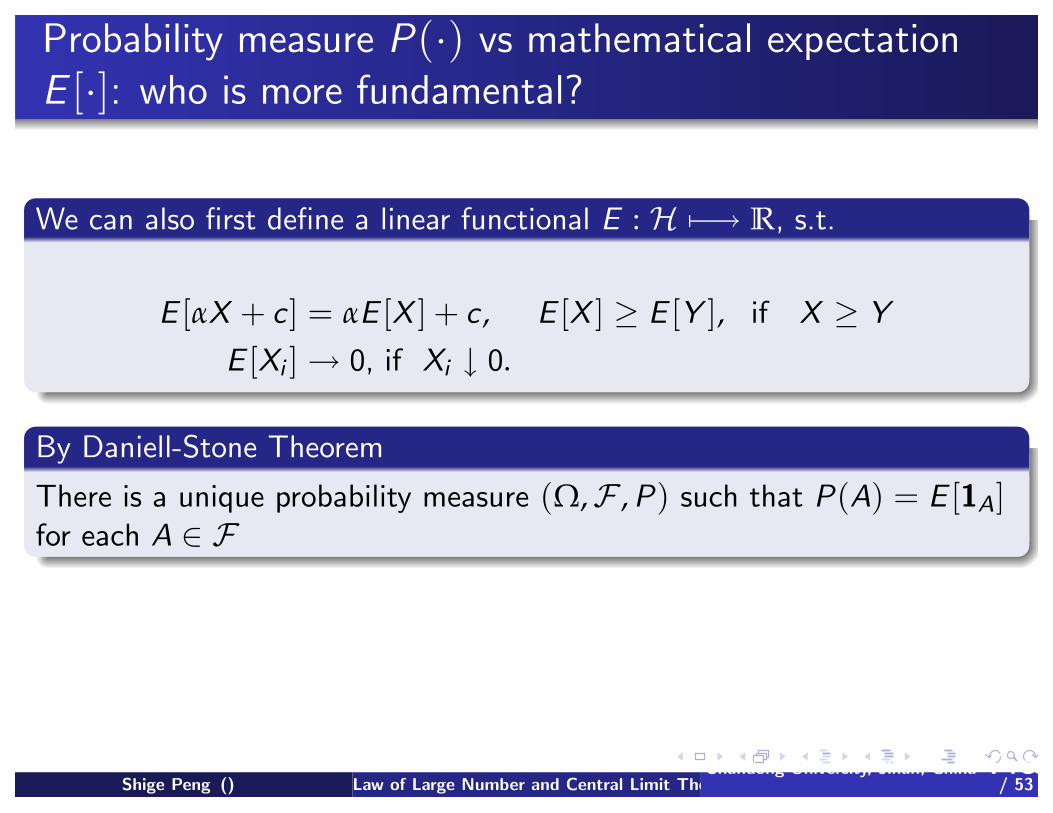

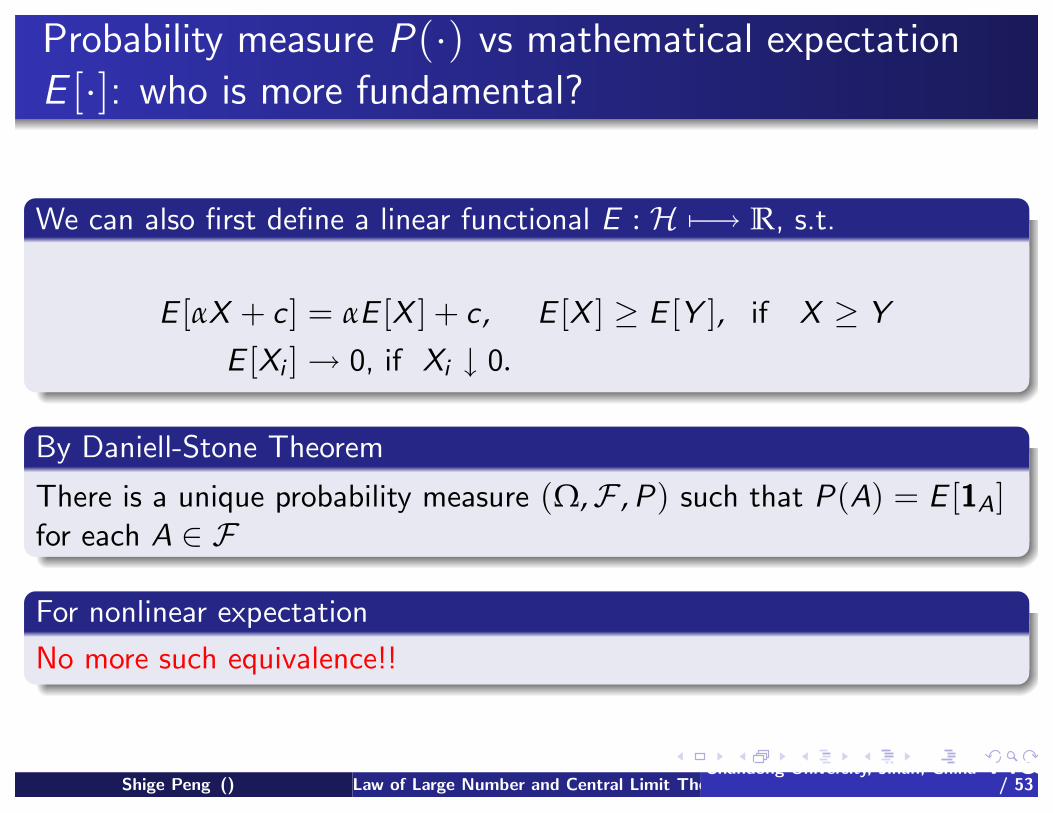

Probability measure P(·) vs mathematical expectationE [·]: who is more fundamental?

We can also first define a linear functional E : H −→ R, s.t.

E [αX + c ] = αE [X ] + c , E [X ] ≥ E [Y ], if X ≥ Y

E [Xi ] → 0, if Xi ↓ 0.

By Daniell-Stone Theorem

There is a unique probability measure (Ω,F , P) such that P(A) = E [1A]for each A ∈ F

For nonlinear expectation

No more such equivalence!!

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 8

/ 53

Probability measure P(·) vs mathematical expectationE [·]: who is more fundamental?

We can also first define a linear functional E : H −→ R, s.t.

E [αX + c ] = αE [X ] + c , E [X ] ≥ E [Y ], if X ≥ Y

E [Xi ] → 0, if Xi ↓ 0.

By Daniell-Stone Theorem

There is a unique probability measure (Ω,F , P) such that P(A) = E [1A]for each A ∈ F

For nonlinear expectation

No more such equivalence!!

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 8

/ 53

Probability measure P(·) vs mathematical expectationE [·]: who is more fundamental?

We can also first define a linear functional E : H −→ R, s.t.

E [αX + c ] = αE [X ] + c , E [X ] ≥ E [Y ], if X ≥ Y

E [Xi ] → 0, if Xi ↓ 0.

By Daniell-Stone Theorem

There is a unique probability measure (Ω,F , P) such that P(A) = E [1A]for each A ∈ F

For nonlinear expectation

No more such equivalence!!

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 8

/ 53

Why nonlinear expectation?

M. Allais Paradox Ellesberg Paradox in economic theory The linearity

of expectation E cannot be a linear operator

[1997 1999Artzner-Delbean-Eden-Heath] Coherent risk measure

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 9

/ 53

A well-known puzzle: why normal distributions are sowidely used?

If someone faces a random variable X with uncertain distribution, he will

first try to use normal distribution N (µ, σ2).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 10

/ 53

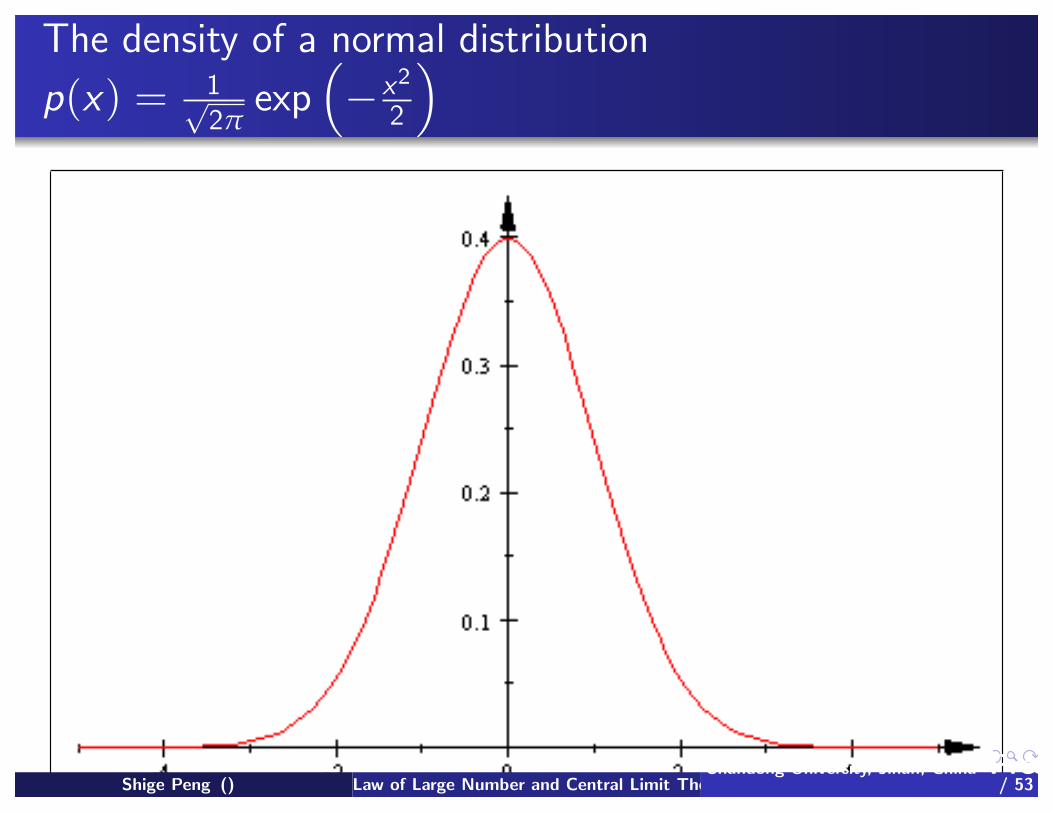

The density of a normal distribution

p(x) = 1√2π

exp−

x2

2

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 11

/ 53

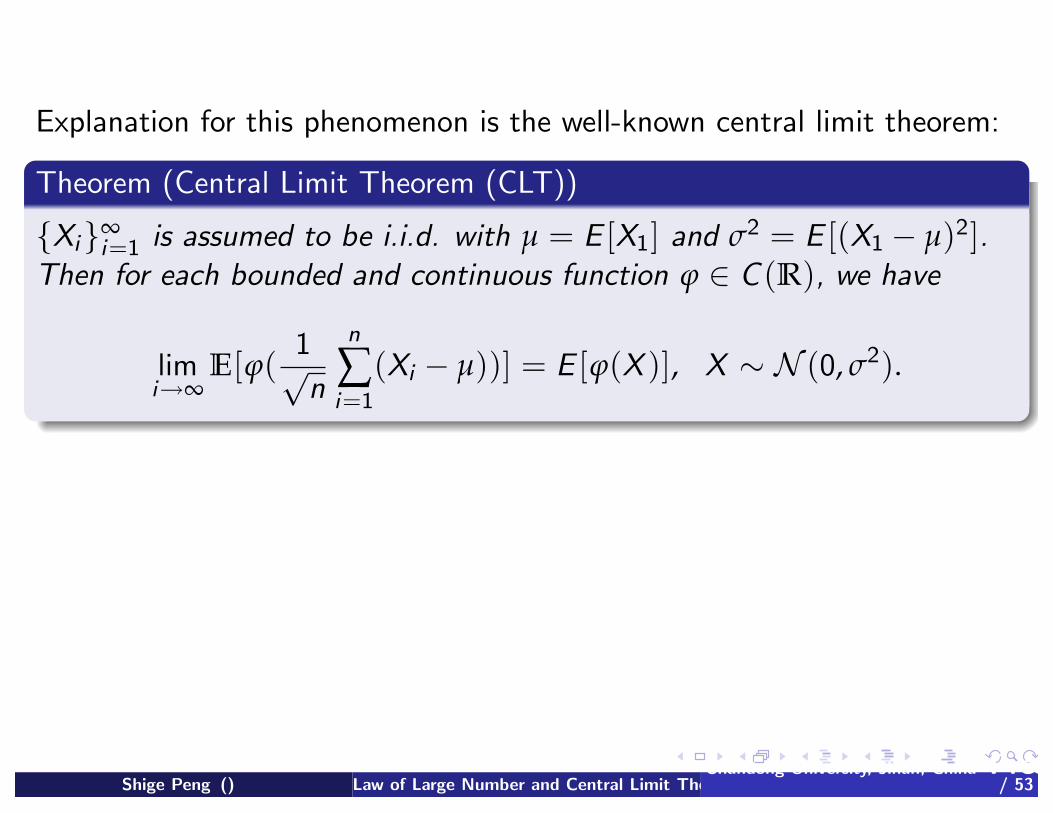

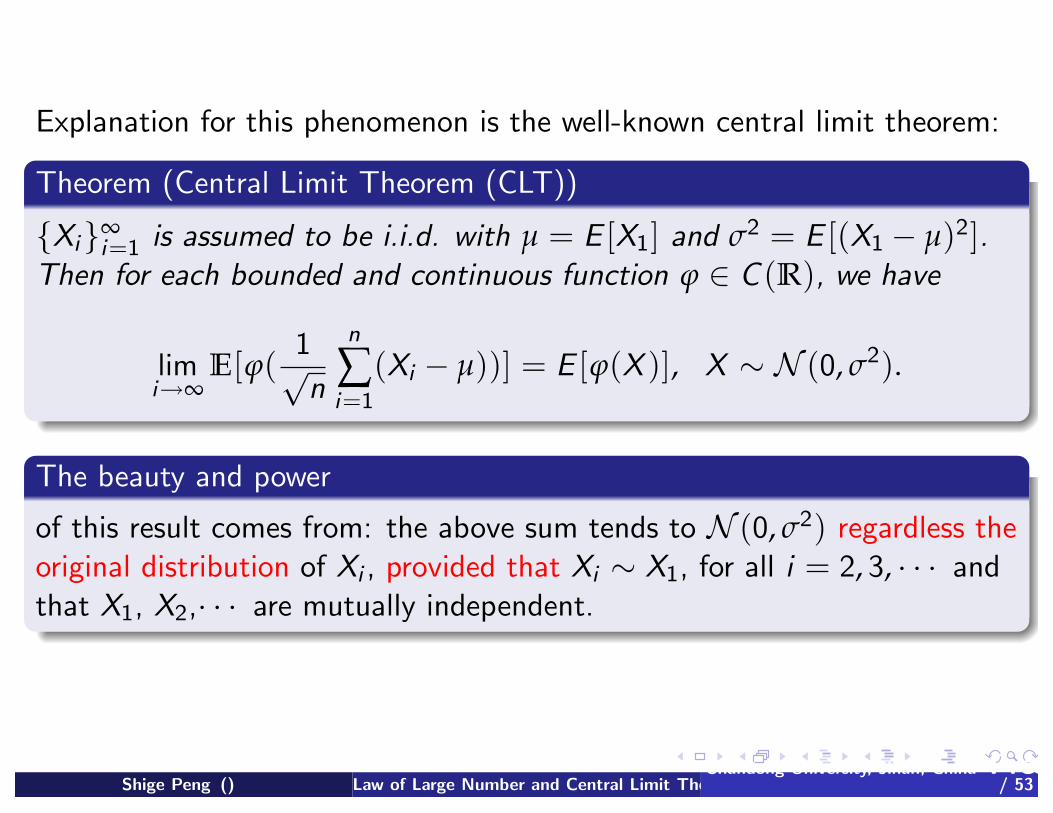

Explanation for this phenomenon is the well-known central limit theorem:

Theorem (Central Limit Theorem (CLT))

Xi∞i=1 is assumed to be i.i.d. with µ = E [X1] and σ2 = E [(X1 − µ)2].

Then for each bounded and continuous function ϕ ∈ C (R), we have

limi→∞

E[ϕ(1√

n

n

∑i=1

(Xi − µ))] = E [ϕ(X )], X ∼ N (0, σ2).

The beauty and power

of this result comes from: the above sum tends to N (0, σ2) regardless the

original distribution of Xi , provided that Xi ∼ X1, for all i = 2, 3, · · · and

that X1, X2,· · · are mutually independent.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 12

/ 53

Explanation for this phenomenon is the well-known central limit theorem:

Theorem (Central Limit Theorem (CLT))

Xi∞i=1 is assumed to be i.i.d. with µ = E [X1] and σ2 = E [(X1 − µ)2].

Then for each bounded and continuous function ϕ ∈ C (R), we have

limi→∞

E[ϕ(1√

n

n

∑i=1

(Xi − µ))] = E [ϕ(X )], X ∼ N (0, σ2).

The beauty and power

of this result comes from: the above sum tends to N (0, σ2) regardless the

original distribution of Xi , provided that Xi ∼ X1, for all i = 2, 3, · · · and

that X1, X2,· · · are mutually independent.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 12

/ 53

Explanation for this phenomenon is the well-known central limit theorem:

Theorem (Central Limit Theorem (CLT))

Xi∞i=1 is assumed to be i.i.d. with µ = E [X1] and σ2 = E [(X1 − µ)2].

Then for each bounded and continuous function ϕ ∈ C (R), we have

limi→∞

E[ϕ(1√

n

n

∑i=1

(Xi − µ))] = E [ϕ(X )], X ∼ N (0, σ2).

The beauty and power

of this result comes from: the above sum tends to N (0, σ2) regardless the

original distribution of Xi , provided that Xi ∼ X1, for all i = 2, 3, · · · and

that X1, X2,· · · are mutually independent.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 12

/ 53

History of CLT

Abraham de Moivre 1733,

Pierre-Simon Laplace, 1812: Theorie Analytique des Probabilite

Aleksandr Lyapunov, 1901

Cauchy’s, Bessel’s and Poisson’s contributions, von Mises, Polya,

Lindeberg, Levy, Cramer

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 13

/ 53

‘dirty work’ through “contaminated data”?

But in, real world in finance, as well as in many other human science

situations, it is not true that the above Xi∞i=1 is really i.i.d.

Many academic people think that people in finance just widely and deeply

abuse this beautiful mathematical result to do ‘dirty work’ through

“contaminated data”

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 14

/ 53

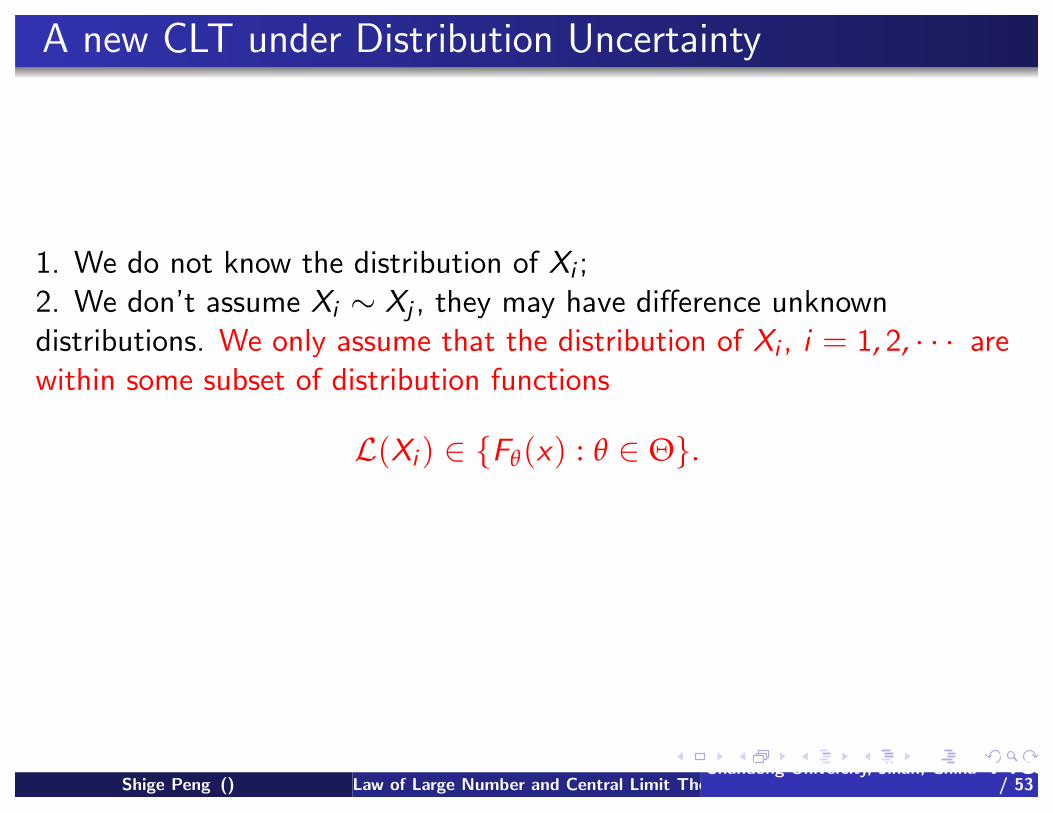

A new CLT under Distribution Uncertainty

1. We do not know the distribution of Xi ;

2. We don’t assume Xi ∼ Xj , they may have difference unknown

distributions. We only assume that the distribution of Xi , i = 1, 2, · · · are

within some subset of distribution functions

L(Xi ) ∈ Fθ(x) : θ ∈ Θ.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 15

/ 53

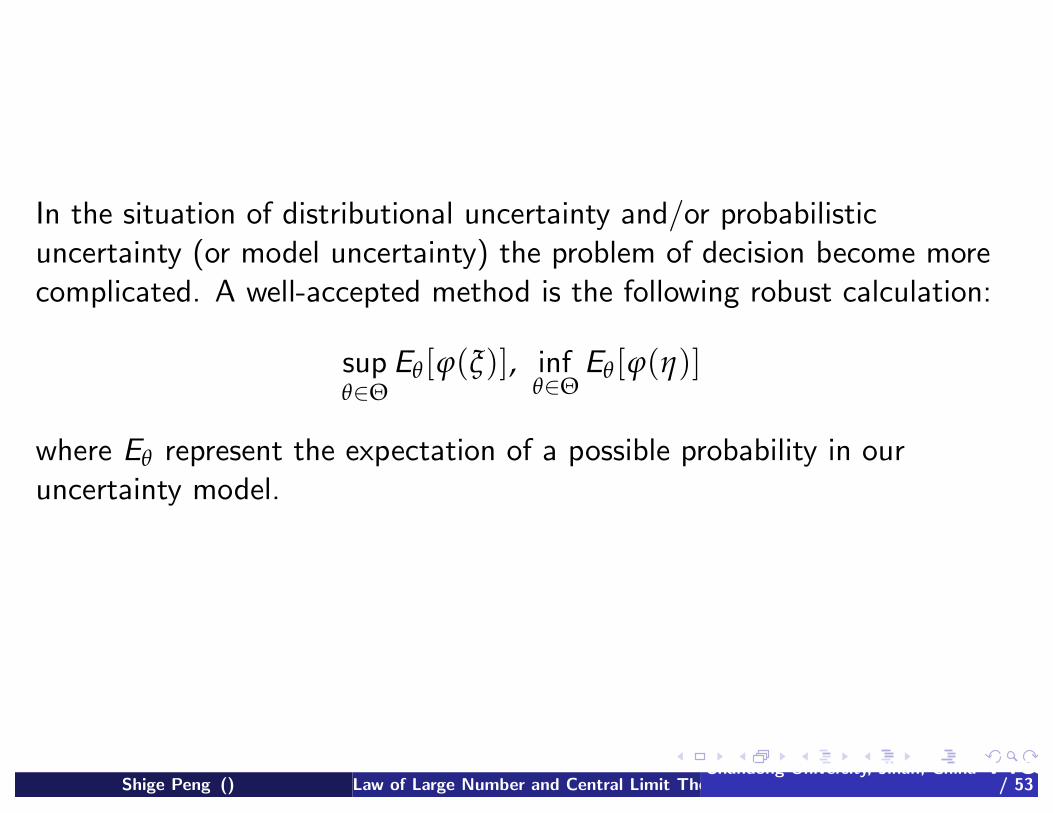

In the situation of distributional uncertainty and/or probabilistic

uncertainty (or model uncertainty) the problem of decision become more

complicated. A well-accepted method is the following robust calculation:

sup

θ∈ΘEθ [ϕ(ξ)], inf

θ∈ΘEθ [ϕ(η)]

where Eθ represent the expectation of a possible probability in our

uncertainty model.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 16

/ 53

But this turns out to be a new and basic mathematical tool:

E[X ] = sup

θ∈ΘEθ [X ]

The operator E has the properties:

a) X ≥ Y then E[X ] ≥ E[Y ]b) E[c ] = c

c) E[X + Y ] ≤ E[X ] + E[Y ]d) E[λX ] = λE[X ], λ ≥ 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 17

/ 53

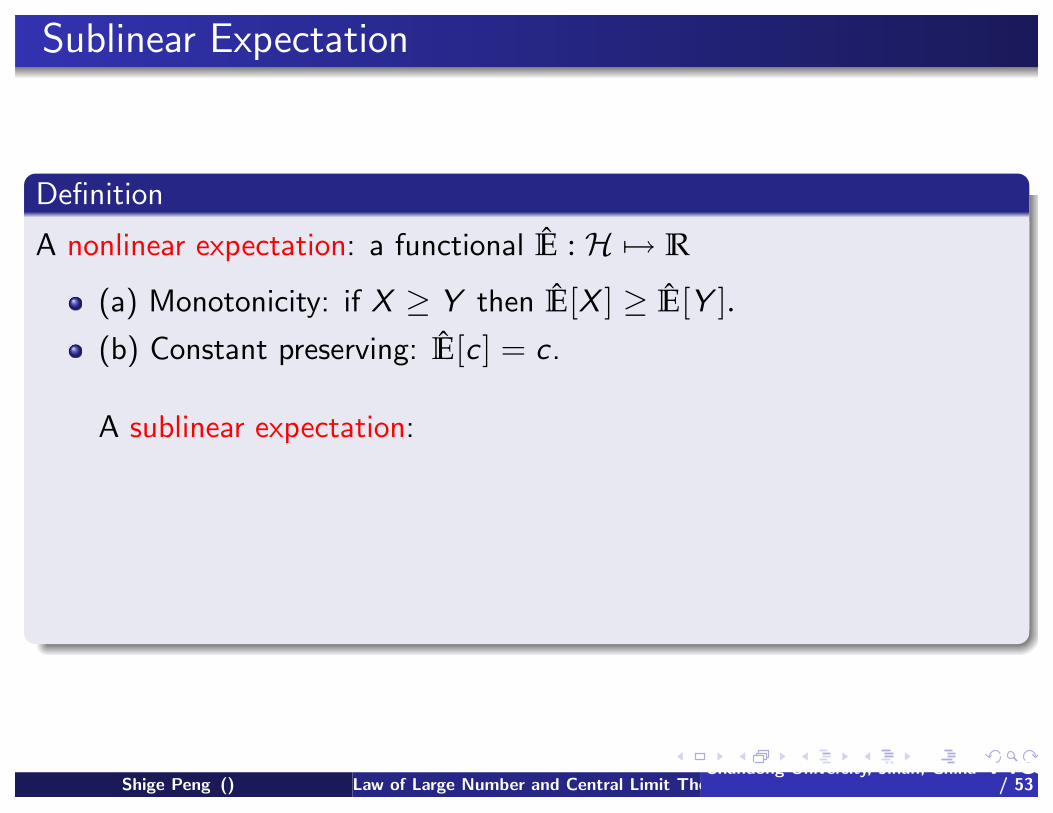

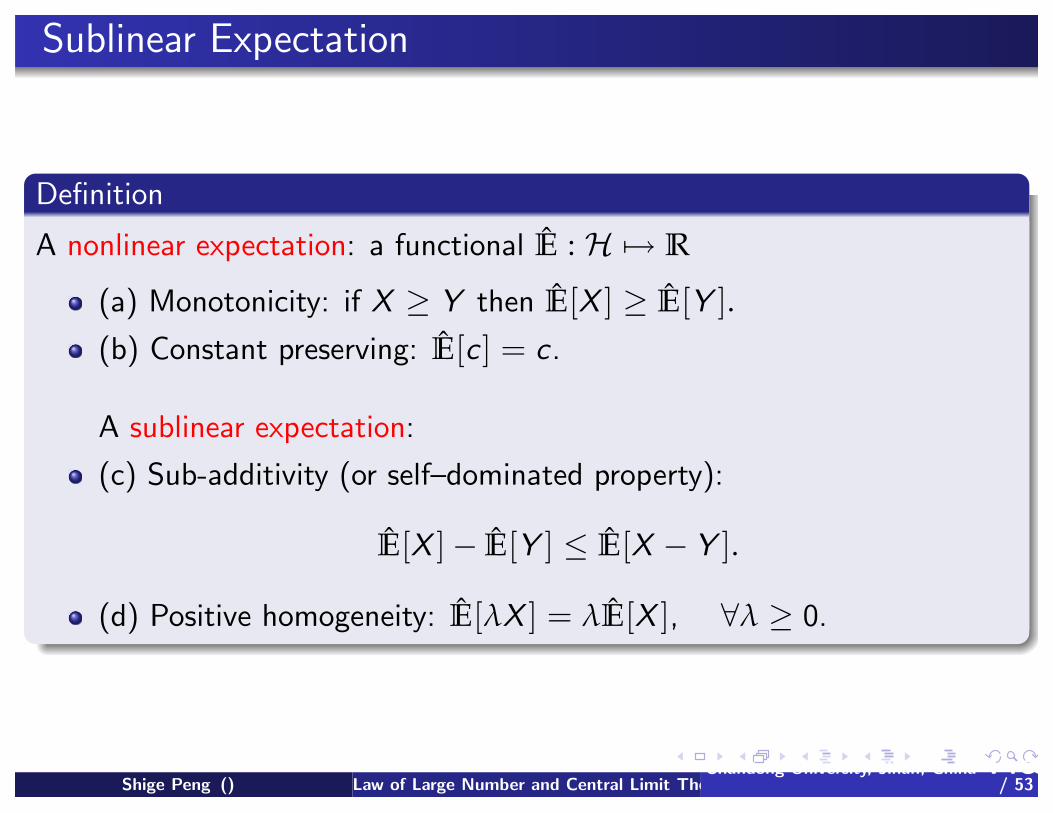

Sublinear Expectation

Definition

A nonlinear expectation: a functional E : H → R

(a) Monotonicity: if X ≥ Y then E[X ] ≥ E[Y ].(b) Constant preserving: E[c ] = c .

A sublinear expectation:

(c) Sub-additivity (or self–dominated property):

E[X ]− E[Y ] ≤ E[X − Y ].

(d) Positive homogeneity: E[λX ] = λE[X ], ∀λ ≥ 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 18

/ 53

Sublinear Expectation

Definition

A nonlinear expectation: a functional E : H → R

(a) Monotonicity: if X ≥ Y then E[X ] ≥ E[Y ].

(b) Constant preserving: E[c ] = c .

A sublinear expectation:

(c) Sub-additivity (or self–dominated property):

E[X ]− E[Y ] ≤ E[X − Y ].

(d) Positive homogeneity: E[λX ] = λE[X ], ∀λ ≥ 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 18

/ 53

Sublinear Expectation

Definition

A nonlinear expectation: a functional E : H → R

(a) Monotonicity: if X ≥ Y then E[X ] ≥ E[Y ].(b) Constant preserving: E[c ] = c .

A sublinear expectation:

(c) Sub-additivity (or self–dominated property):

E[X ]− E[Y ] ≤ E[X − Y ].

(d) Positive homogeneity: E[λX ] = λE[X ], ∀λ ≥ 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 18

/ 53

Sublinear Expectation

Definition

A nonlinear expectation: a functional E : H → R

(a) Monotonicity: if X ≥ Y then E[X ] ≥ E[Y ].(b) Constant preserving: E[c ] = c .

A sublinear expectation:

(c) Sub-additivity (or self–dominated property):

E[X ]− E[Y ] ≤ E[X − Y ].

(d) Positive homogeneity: E[λX ] = λE[X ], ∀λ ≥ 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 18

/ 53

Sublinear Expectation

Definition

A nonlinear expectation: a functional E : H → R

(a) Monotonicity: if X ≥ Y then E[X ] ≥ E[Y ].(b) Constant preserving: E[c ] = c .

A sublinear expectation:

(c) Sub-additivity (or self–dominated property):

E[X ]− E[Y ] ≤ E[X − Y ].

(d) Positive homogeneity: E[λX ] = λE[X ], ∀λ ≥ 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 18

/ 53

Coherent Risk Measures and Sunlinear Expectations

H is the set of bounded and measurable random variables on (Ω,F ).

ρ(X ) := E[−X ]

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 19

/ 53

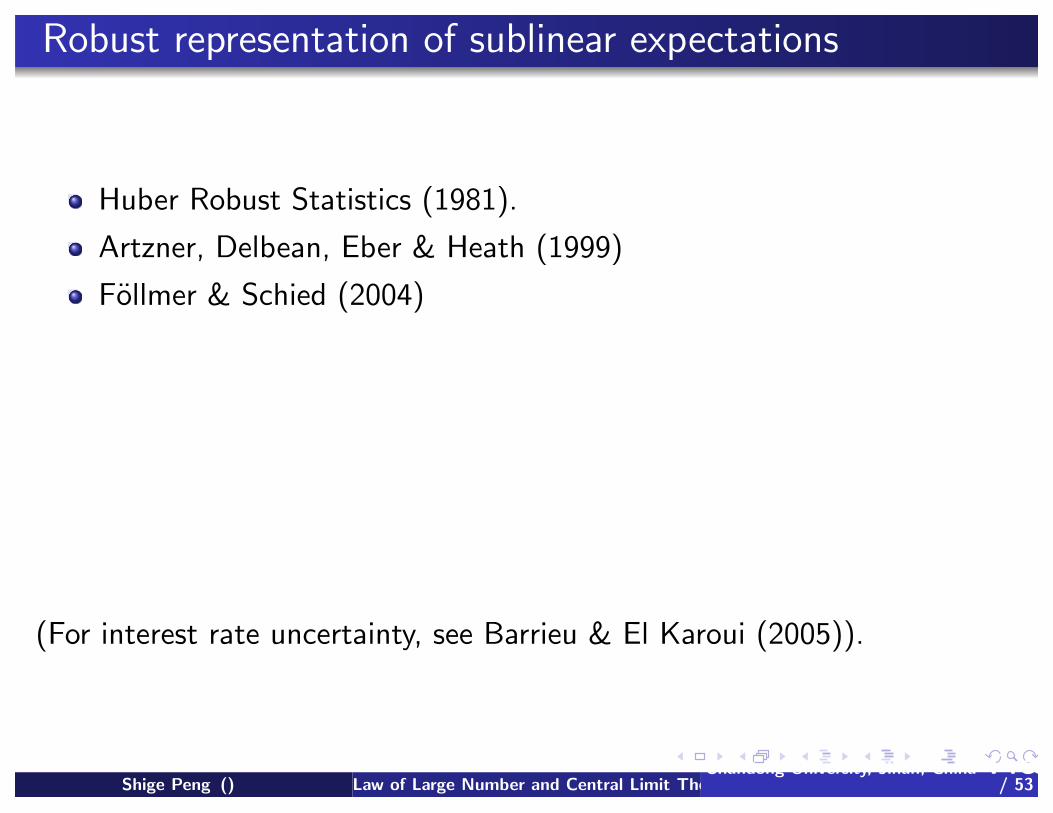

Robust representation of sublinear expectations

Huber Robust Statistics (1981).

Artzner, Delbean, Eber & Heath (1999)

Follmer & Schied (2004)

Theorem

E[·] is a sublinear expectation on H if and only if there exists a subset

P ∈M1,f (the collection of all finitely additive probability measures) such

that

E[X ] = sup

P∈PEP [X ], ∀X ∈ H.

(For interest rate uncertainty, see Barrieu & El Karoui (2005)).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 20

/ 53

Robust representation of sublinear expectations

Huber Robust Statistics (1981).

Artzner, Delbean, Eber & Heath (1999)

Follmer & Schied (2004)

Theorem

E[·] is a sublinear expectation on H if and only if there exists a subset

P ∈M1,f (the collection of all finitely additive probability measures) such

that

E[X ] = sup

P∈PEP [X ], ∀X ∈ H.

(For interest rate uncertainty, see Barrieu & El Karoui (2005)).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 20

/ 53

Meaning of the robust representation:Statistic model uncertainty

E[X ] = sup

P∈PEP [X ], ∀X ∈ H.

The size of the subset P represents the degree of

model uncertainty: The stronger the E the more the uncertainty

E1[X ] ≥ E2[X ], ∀X ∈ H ⇐⇒ P1 ⊃ P2

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 21

/ 53

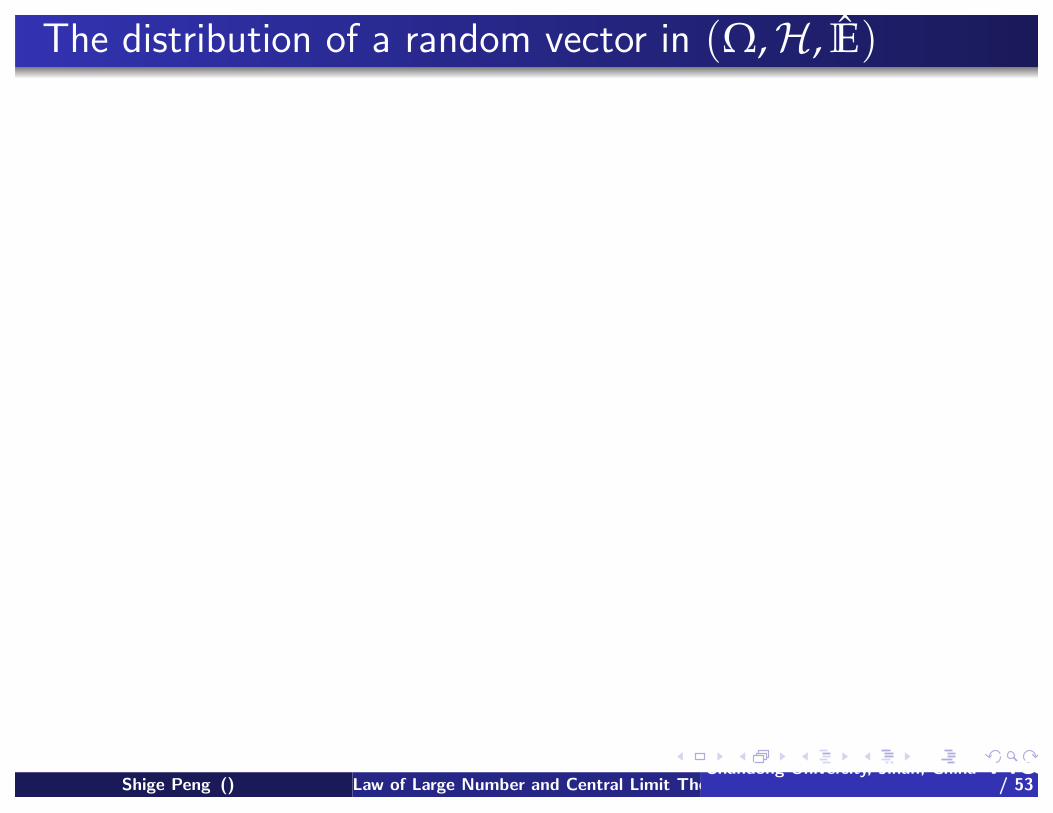

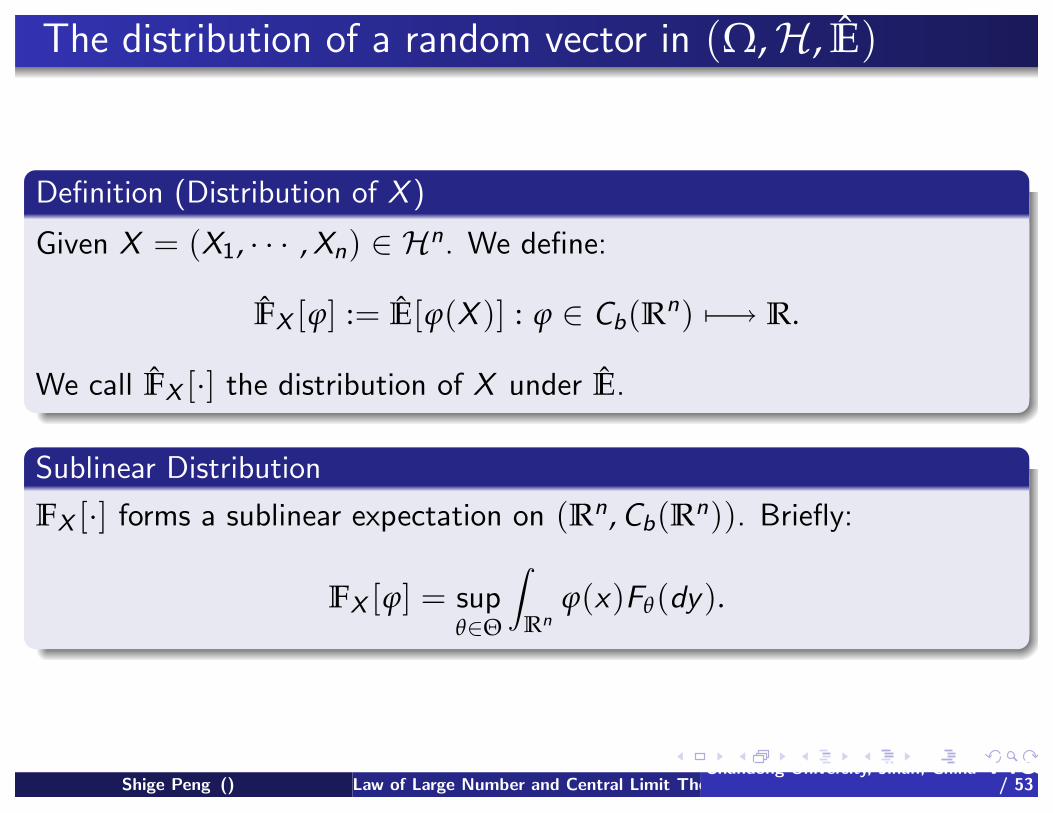

The distribution of a random vector in (Ω,H, E)

Definition (Distribution of X )

Given X = (X1, · · · , Xn) ∈ Hn. We define:

FX [ϕ] := E[ϕ(X )] : ϕ ∈ Cb(Rn) −→ R.

We call FX [·] the distribution of X under E.

Sublinear Distribution

FX [·] forms a sublinear expectation on (Rn, Cb(Rn)). Briefly:

FX [ϕ] = sup

θ∈Θ

Rnϕ(x)Fθ(dy).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 22

/ 53

The distribution of a random vector in (Ω,H, E)

Definition (Distribution of X )

Given X = (X1, · · · , Xn) ∈ Hn. We define:

FX [ϕ] := E[ϕ(X )] : ϕ ∈ Cb(Rn) −→ R.

We call FX [·] the distribution of X under E.

Sublinear Distribution

FX [·] forms a sublinear expectation on (Rn, Cb(Rn)). Briefly:

FX [ϕ] = sup

θ∈Θ

Rnϕ(x)Fθ(dy).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 22

/ 53

The distribution of a random vector in (Ω,H, E)

Definition (Distribution of X )

Given X = (X1, · · · , Xn) ∈ Hn. We define:

FX [ϕ] := E[ϕ(X )] : ϕ ∈ Cb(Rn) −→ R.

We call FX [·] the distribution of X under E.

Sublinear Distribution

FX [·] forms a sublinear expectation on (Rn, Cb(Rn)). Briefly:

FX [ϕ] = sup

θ∈Θ

Rnϕ(x)Fθ(dy).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 22

/ 53

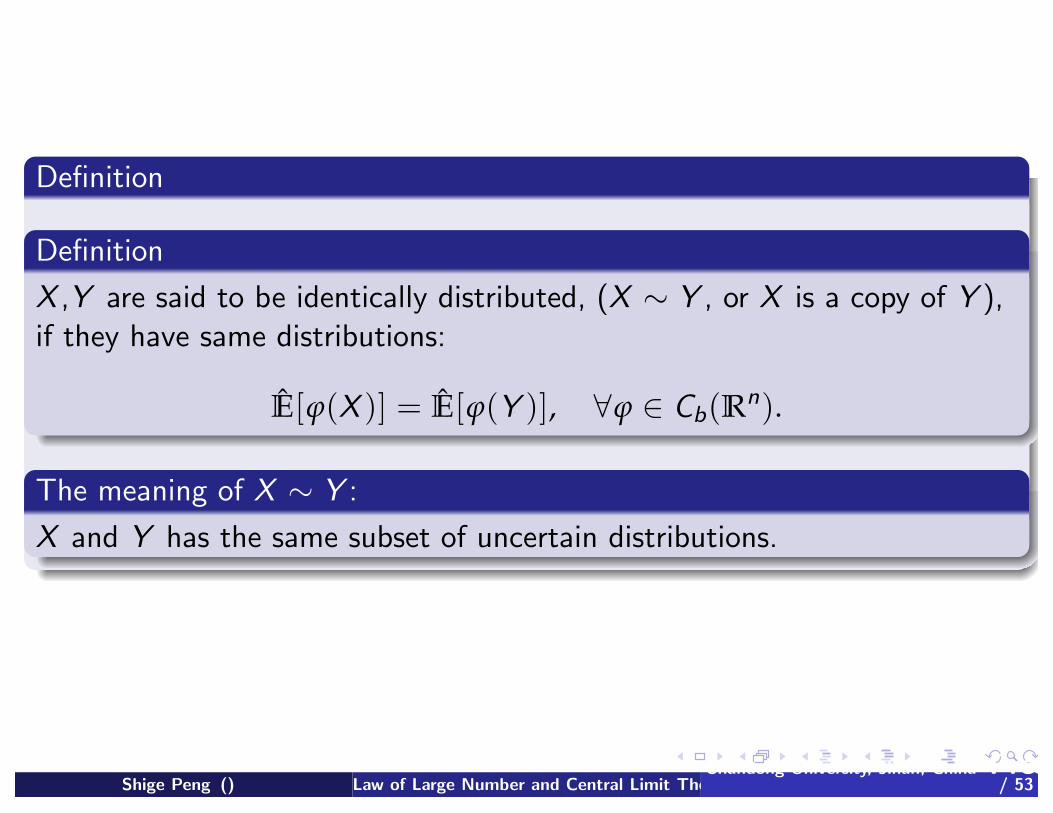

Definition

Definition

X ,Y are said to be identically distributed, (X ∼ Y , or X is a copy of Y ),

if they have same distributions:

E[ϕ(X )] = E[ϕ(Y )], ∀ϕ ∈ Cb(Rn).

The meaning of X ∼ Y :

X and Y has the same subset of uncertain distributions.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 23

/ 53

Definition

Definition

X ,Y are said to be identically distributed, (X ∼ Y , or X is a copy of Y ),

if they have same distributions:

E[ϕ(X )] = E[ϕ(Y )], ∀ϕ ∈ Cb(Rn).

The meaning of X ∼ Y :

X and Y has the same subset of uncertain distributions.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 23

/ 53

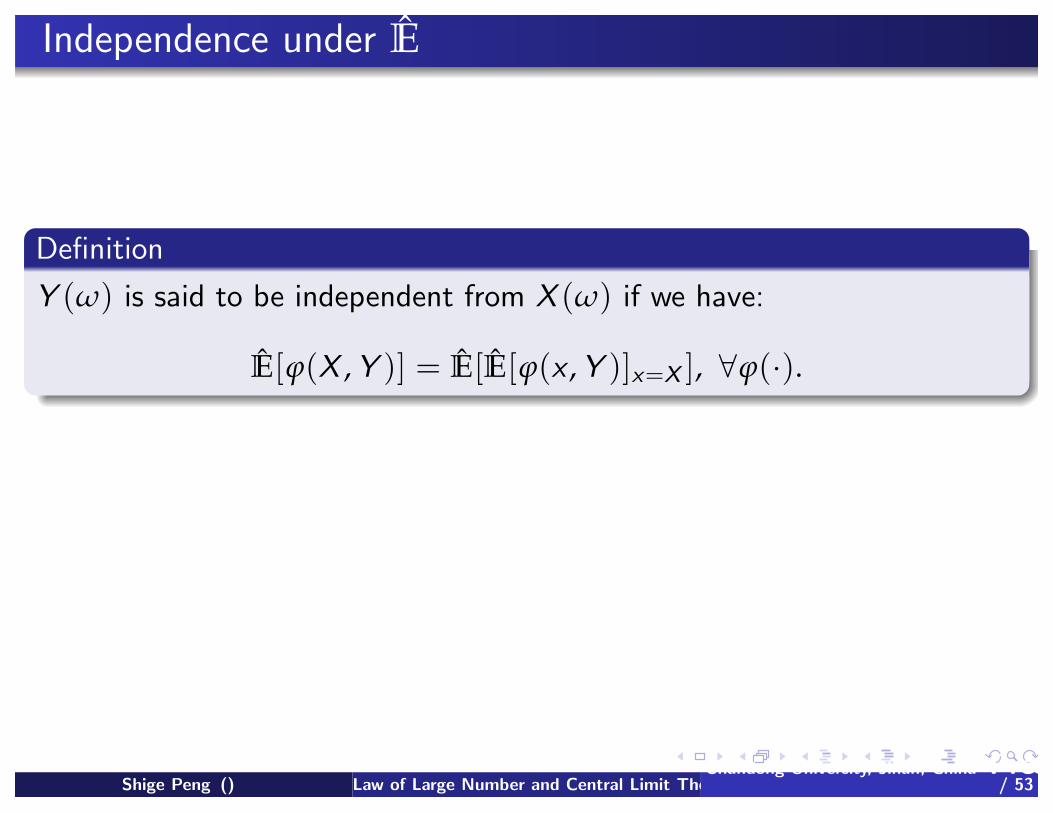

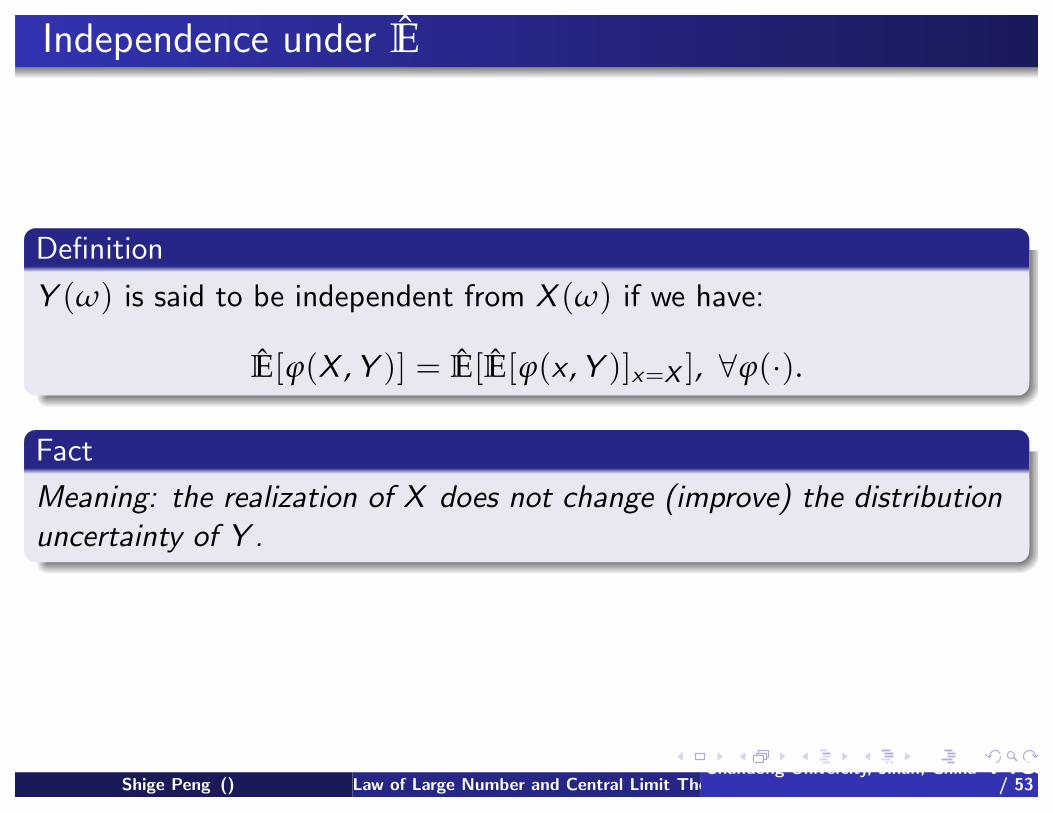

Independence under E

Definition

Y (ω) is said to be independent from X (ω) if we have:

E[ϕ(X , Y )] = E[E[ϕ(x , Y )]x=X ], ∀ϕ(·).

Fact

Meaning: the realization of X does not change (improve) the distribution

uncertainty of Y .

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 24

/ 53

Independence under E

Definition

Y (ω) is said to be independent from X (ω) if we have:

E[ϕ(X , Y )] = E[E[ϕ(x , Y )]x=X ], ∀ϕ(·).

Fact

Meaning: the realization of X does not change (improve) the distribution

uncertainty of Y .

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 24

/ 53

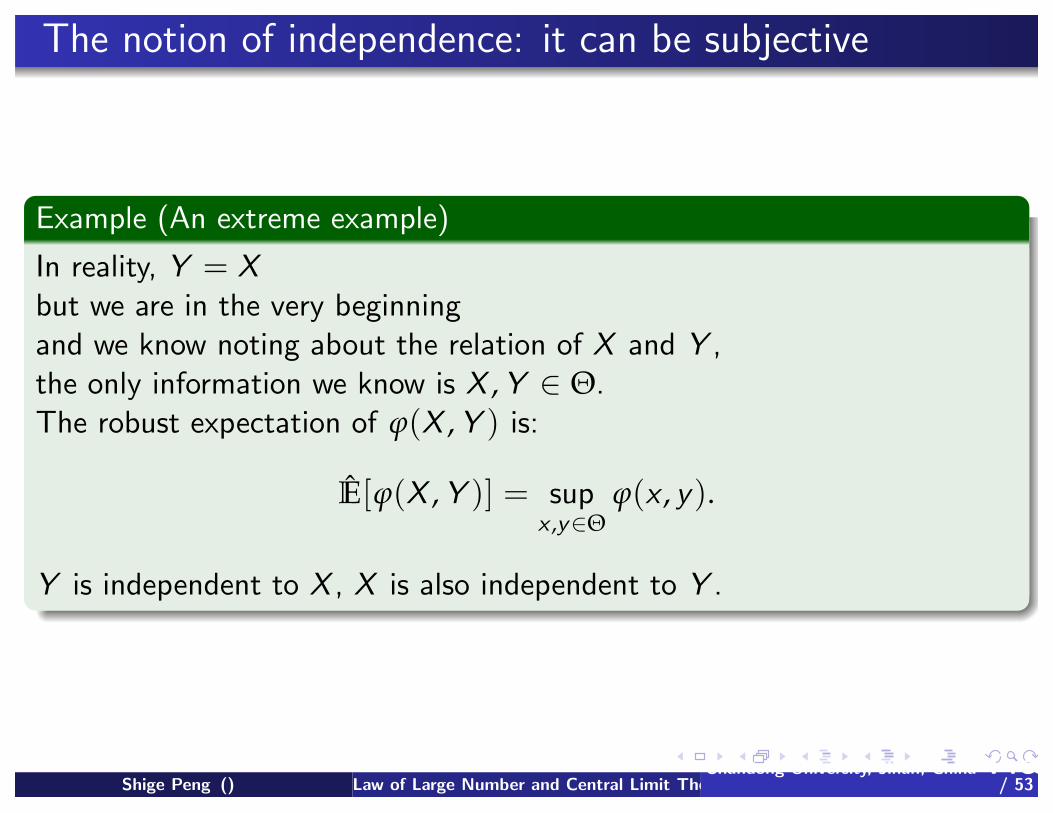

The notion of independence: it can be subjective

Example (An extreme example)

In reality, Y = X

but we are in the very beginning

and we know noting about the relation of X and Y ,

the only information we know is X , Y ∈ Θ.

The robust expectation of ϕ(X , Y ) is:

E[ϕ(X , Y )] = sup

x ,y∈Θϕ(x , y).

Y is independent to X , X is also independent to Y .

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 25

/ 53

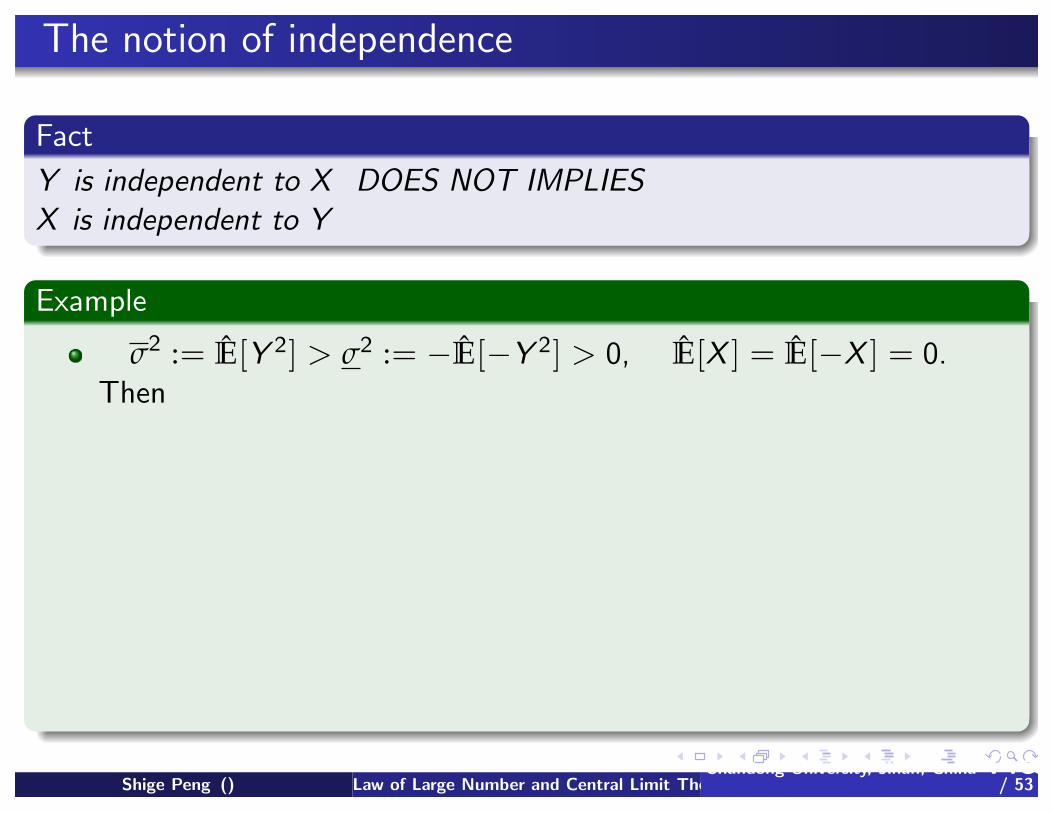

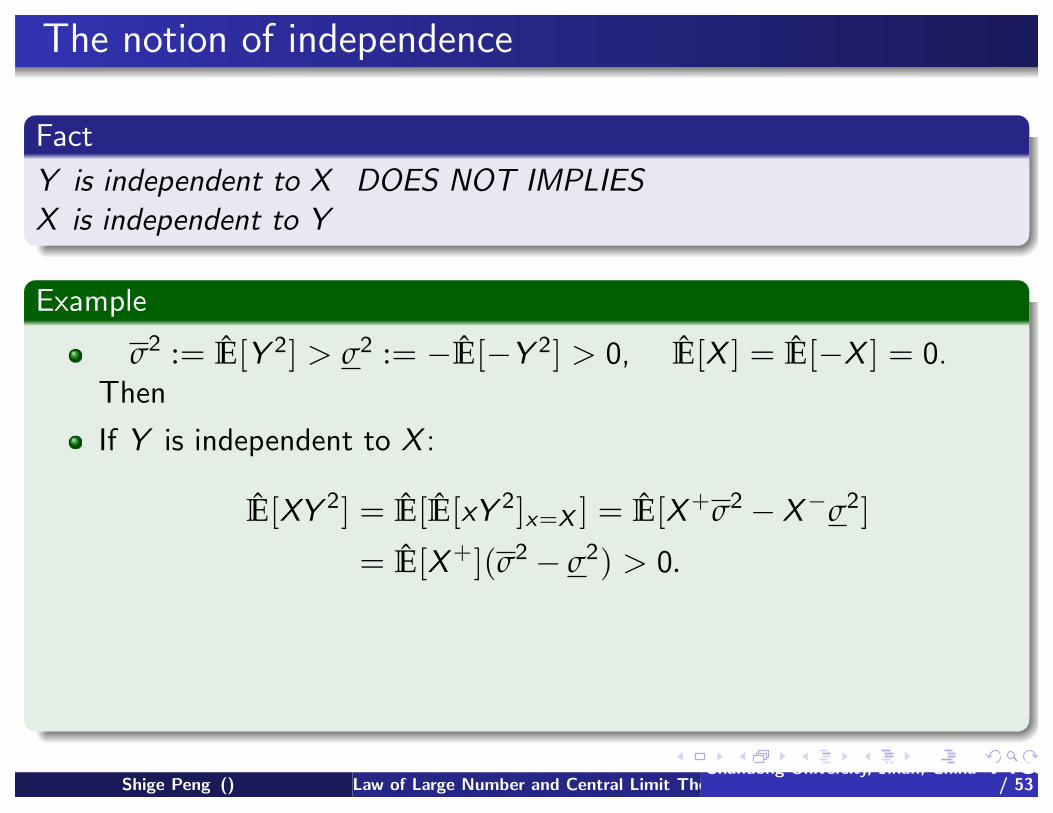

The notion of independence

Fact

Y is independent to X DOES NOT IMPLIES

X is independent to Y

Example

σ2 := E[Y 2] > σ2 := −E[−Y 2] > 0, E[X ] = E[−X ] = 0.

Then

If Y is independent to X :

E[XY2] = E[E[xY 2]x=X ] = E[X+σ2

− X−σ2]

= E[X+](σ2− σ2) > 0.

But if X is independent to Y :

E[XY2] = E[E[X ]Y 2] = 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 26

/ 53

The notion of independence

Fact

Y is independent to X DOES NOT IMPLIES

X is independent to Y

Example

σ2 := E[Y 2] > σ2 := −E[−Y 2] > 0, E[X ] = E[−X ] = 0.

Then

If Y is independent to X :

E[XY2] = E[E[xY 2]x=X ] = E[X+σ2

− X−σ2]

= E[X+](σ2− σ2) > 0.

But if X is independent to Y :

E[XY2] = E[E[X ]Y 2] = 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 26

/ 53

The notion of independence

Fact

Y is independent to X DOES NOT IMPLIES

X is independent to Y

Example

σ2 := E[Y 2] > σ2 := −E[−Y 2] > 0, E[X ] = E[−X ] = 0.

Then

If Y is independent to X :

E[XY2] = E[E[xY 2]x=X ] = E[X+σ2

− X−σ2]

= E[X+](σ2− σ2) > 0.

But if X is independent to Y :

E[XY2] = E[E[X ]Y 2] = 0.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 26

/ 53

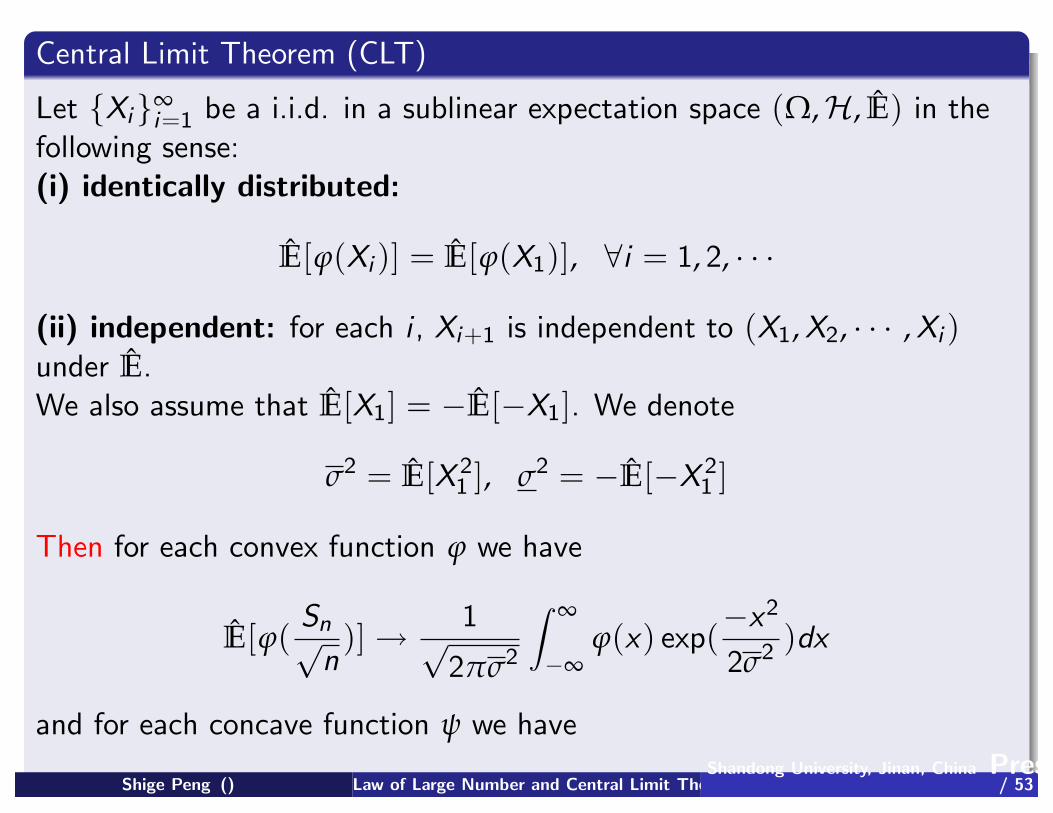

Central Limit Theorem (CLT)

Let Xi∞i=1 be a i.i.d. in a sublinear expectation space (Ω,H, E) in the

following sense:

(i) identically distributed:

E[ϕ(Xi )] = E[ϕ(X1)], ∀i = 1, 2, · · ·

(ii) independent: for each i , Xi+1 is independent to (X1, X2, · · · , Xi )under E.

We also assume that E[X1] = −E[−X1]. We denote

σ2 = E[X 21 ], σ2 = −E[−X

21 ]

Then for each convex function ϕ we have

E[ϕ(Sn√

n)] →

1√

2πσ2

∞

−∞ϕ(x) exp(

−x2

2σ2 )dx

and for each concave function ψ we have

E[ψ(Sn√

n)] →

12πσ2

∞

−∞ψ(x) exp(

−x2

2σ2)dx .

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 27

/ 53

Theorem ( CLT under distribution uncertainty)

Let Xi∞i=1 be a i.i.d. in a sublinear expectation space (Ω,H, E) in the

following sense:

(i) identically distributed:

E[ϕ(Xi )] = E[ϕ(X1)], ∀i = 1, 2, · · ·

(ii) independent: for each i , Xi+1 is independent to (X1, X2, · · · , Xi )under E.

We also assume that E[X1] = −E[−X1]. Then for each convex function

ϕ we have

E[ϕ(Sn√

n)] → E[ϕ(X )], X ∼ N (0, [σ2, σ2])

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 28

/ 53

Normal distribution under Sublinear expectation

An fundamentally important sublinear distribution

Definition

A random variable X in (Ω,H, E) is called normally distributed if

aX + bX ∼

a2 + b2X , ∀a, b ≥ 0.

where X is an independent copy of X .

We have E[X ] = E[−X ] = 0.

We denote X ∼ N (0, [σ2, σ2]), where

σ2 := E[X 2], σ2 := −E[−X2].

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 29

/ 53

Normal distribution under Sublinear expectation

An fundamentally important sublinear distribution

Definition

A random variable X in (Ω,H, E) is called normally distributed if

aX + bX ∼

a2 + b2X , ∀a, b ≥ 0.

where X is an independent copy of X .

We have E[X ] = E[−X ] = 0.

We denote X ∼ N (0, [σ2, σ2]), where

σ2 := E[X 2], σ2 := −E[−X2].

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 29

/ 53

Normal distribution under Sublinear expectation

An fundamentally important sublinear distribution

Definition

A random variable X in (Ω,H, E) is called normally distributed if

aX + bX ∼

a2 + b2X , ∀a, b ≥ 0.

where X is an independent copy of X .

We have E[X ] = E[−X ] = 0.

We denote X ∼ N (0, [σ2, σ2]), where

σ2 := E[X 2], σ2 := −E[−X2].

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 29

/ 53

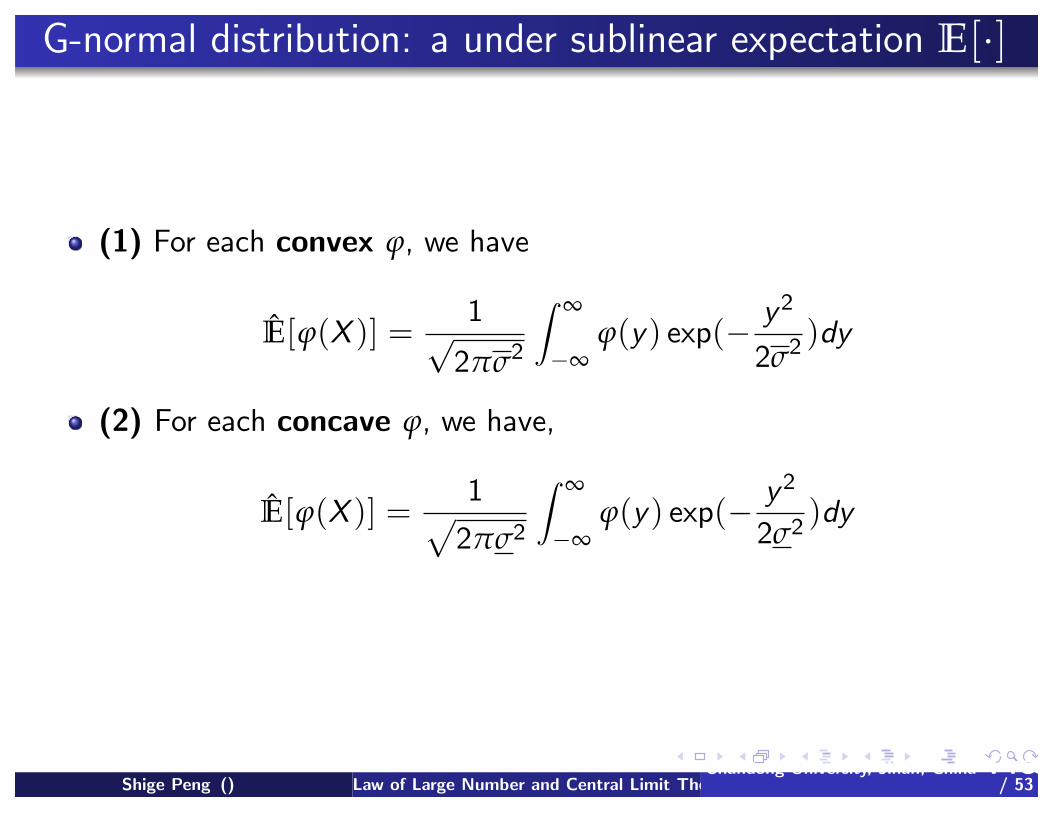

G-normal distribution: a under sublinear expectation E[·]

(1) For each convex ϕ, we have

E[ϕ(X )] =1

√

2πσ2

∞

−∞ϕ(y) exp(−

y2

2σ2 )dy

(2) For each concave ϕ, we have,

E[ϕ(X )] =1

2πσ2

∞

−∞ϕ(y) exp(−

y2

2σ2)dy

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 30

/ 53

G-normal distribution: a under sublinear expectation E[·]

(1) For each convex ϕ, we have

E[ϕ(X )] =1

√

2πσ2

∞

−∞ϕ(y) exp(−

y2

2σ2 )dy

(2) For each concave ϕ, we have,

E[ϕ(X )] =1

2πσ2

∞

−∞ϕ(y) exp(−

y2

2σ2)dy

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 30

/ 53

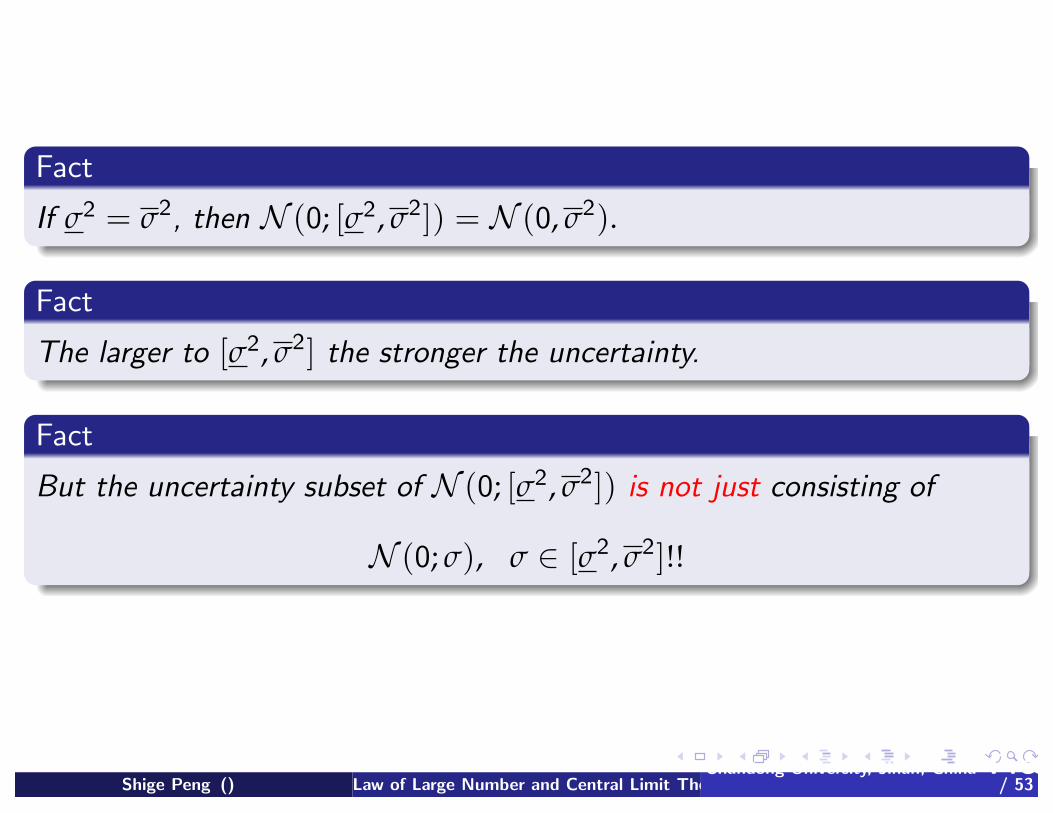

Fact

If σ2 = σ2, then N (0; [σ2, σ2]) = N (0, σ2).

Fact

The larger to [σ2, σ2] the stronger the uncertainty.

Fact

But the uncertainty subset of N (0; [σ2, σ2]) is not just consisting of

N (0; σ), σ ∈ [σ2, σ2]!!

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 31

/ 53

Theorem

X ∼ N (0, [σ2, σ2]) in (Ω,H, E) iff for each ϕ ∈ Cb(R) the function

u(t, x) := E[ϕ(x +√

tX )], x ∈ R, t ≥ 0

is the solution of the PDE

ut = G (uxx ), t > 0, x ∈ R

u|t=0 = ϕ,

where G (a) = 12 (σ2

a+ − σ2a−)(= E[ a2X 2]). G-normal distribution.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 32

/ 53

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 33

/ 53

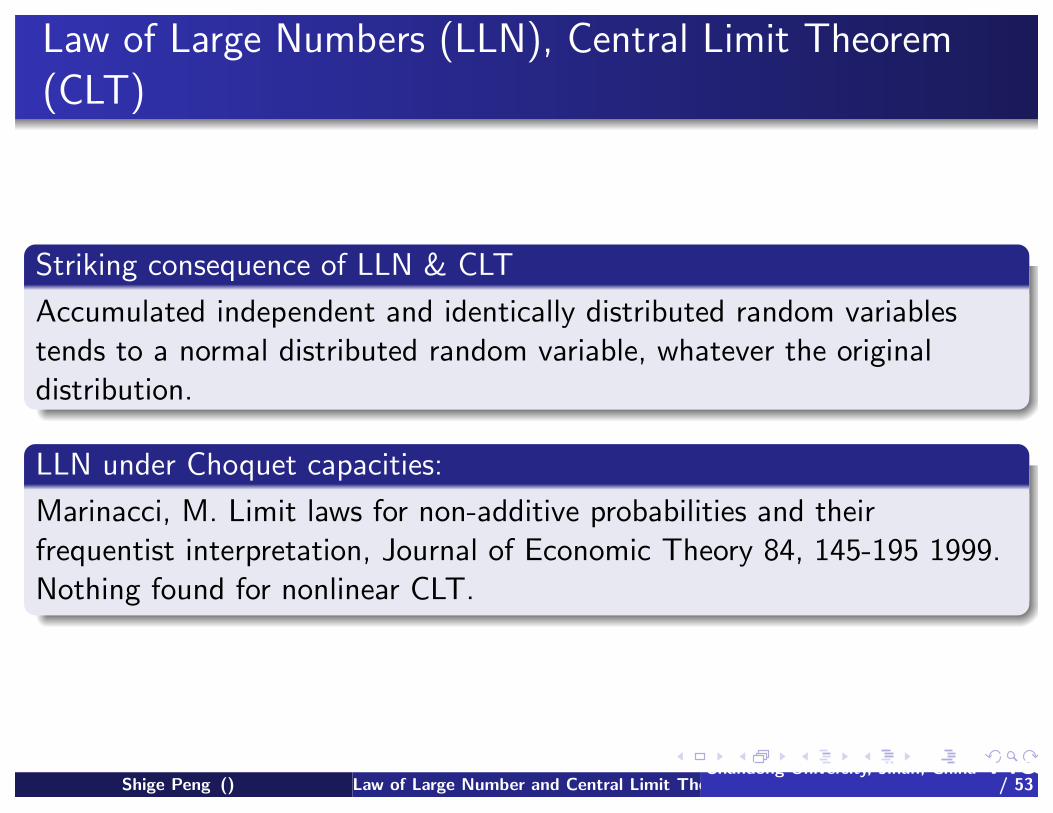

Law of Large Numbers (LLN), Central Limit Theorem(CLT)

Striking consequence of LLN & CLT

Accumulated independent and identically distributed random variables

tends to a normal distributed random variable, whatever the original

distribution.

LLN under Choquet capacities:

Marinacci, M. Limit laws for non-additive probabilities and their

frequentist interpretation, Journal of Economic Theory 84, 145-195 1999.

Nothing found for nonlinear CLT.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 33

/ 53

Law of Large Numbers (LLN), Central Limit Theorem(CLT)

Striking consequence of LLN & CLT

Accumulated independent and identically distributed random variables

tends to a normal distributed random variable, whatever the original

distribution.

LLN under Choquet capacities:

Marinacci, M. Limit laws for non-additive probabilities and their

frequentist interpretation, Journal of Economic Theory 84, 145-195 1999.

Nothing found for nonlinear CLT.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 33

/ 53

Definition

A sequence of random variables ηi∞i=1 in H is said to converge in law

under E if the limit

limi→∞

E[ϕ(ηi )], for each ϕ ∈ Cb(R).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 34

/ 53

Central Limit Theorem under Sublinear Expectation

Theorem

Let Xi∞i=1 in (Ω,H, E) be identically distributed: Xi ∼ X1, and each

Xi+1 is independent to (X1, · · · , Xi ). We assume furthermore that

E[|X1|2+α] < ∞ and E[X1] = E[−X1] = 0.

Sn := X1 + · · ·+ Xn. Then Sn/√

n converges in law to N (0; [σ2, σ2]):

limn→∞

E[ϕ(Sn√

n)] = E[ϕ(X )], ∀ϕ ∈ Cb(R),

where

where X ∼ N (0, [σ2, σ2]), σ2 = E[X 21 ], σ2 = −E[−X

21 ].

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 35

/ 53

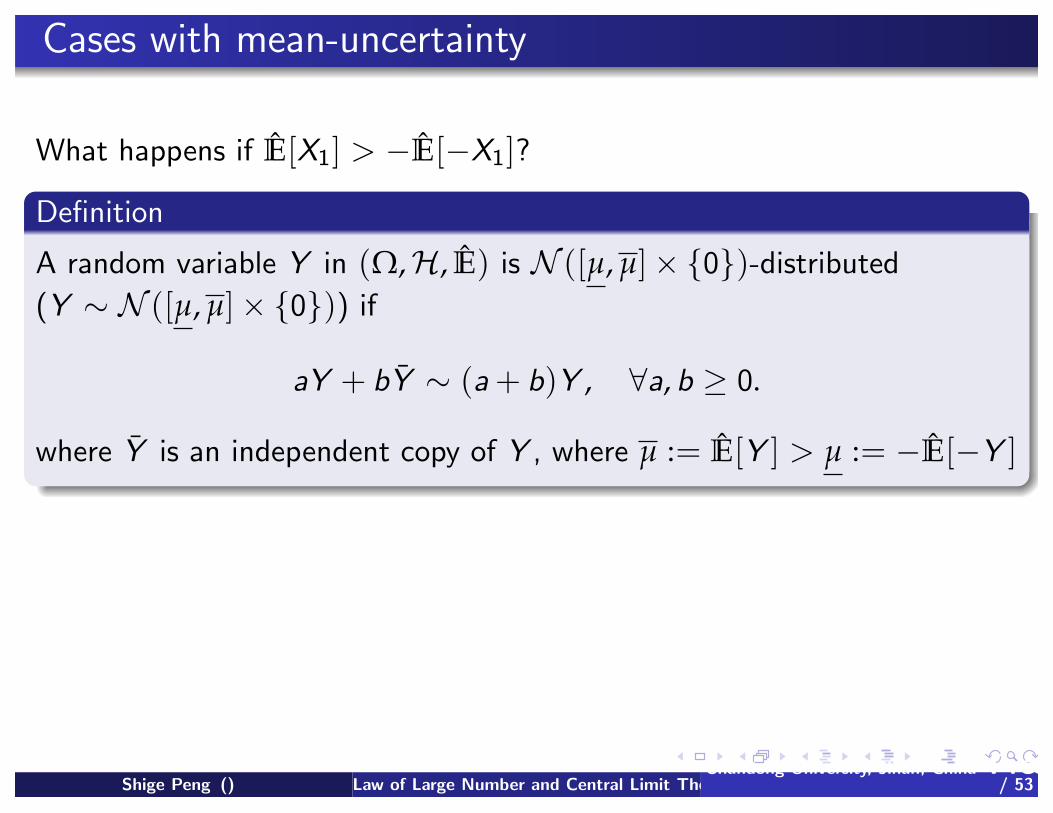

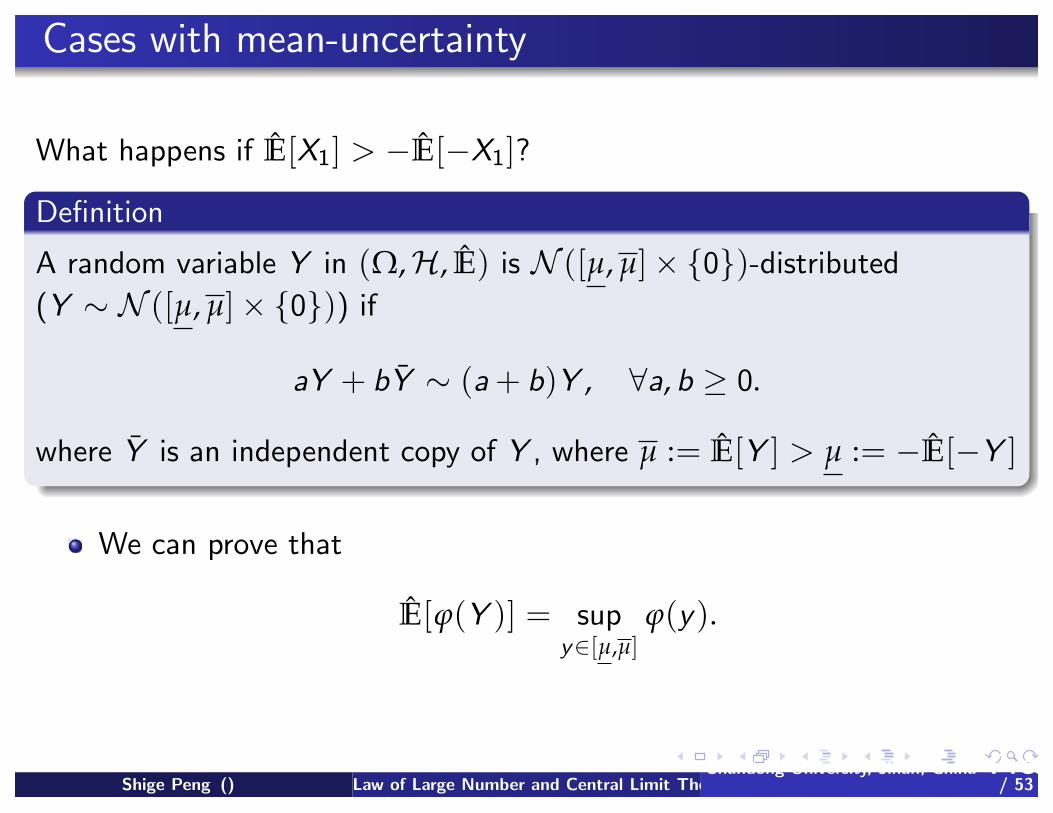

Cases with mean-uncertainty

What happens if E[X1] > −E[−X1]?

Definition

A random variable Y in (Ω,H, E) is N ([µ, µ]× 0)-distributed

(Y ∼ N ([µ, µ]× 0)) if

aY + bY ∼ (a + b)Y , ∀a, b ≥ 0.

where Y is an independent copy of Y , where µ := E[Y ] > µ := −E[−Y ]

We can prove that

E[ϕ(Y )] = sup

y∈[µ,µ]ϕ(y).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 36

/ 53

Cases with mean-uncertainty

What happens if E[X1] > −E[−X1]?

Definition

A random variable Y in (Ω,H, E) is N ([µ, µ]× 0)-distributed

(Y ∼ N ([µ, µ]× 0)) if

aY + bY ∼ (a + b)Y , ∀a, b ≥ 0.

where Y is an independent copy of Y , where µ := E[Y ] > µ := −E[−Y ]

We can prove that

E[ϕ(Y )] = sup

y∈[µ,µ]ϕ(y).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 36

/ 53

Case with mean-uncertainty E[·]

Definition

A pair of random variables (X , Y ) in (Ω,H, E) is

N ([µ, µ]× [σ2, σ2])-distributed ((X , Y ) ∼ N ([µ, µ]× [σ2, σ2])) if

(aX + bX , a2Y + b

2Y ) ∼ (

a2 + b2X , (a2 + b

2)Y ), ∀a, b ≥ 0.

where (X , Y ) is an independent copy of (X , Y ),

µ := E[Y ], µ := −E[−Y ]

σ2 := E[X 2], σ2 := −E[−X ], (E[X ] = E[− X ] = 0).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 37

/ 53

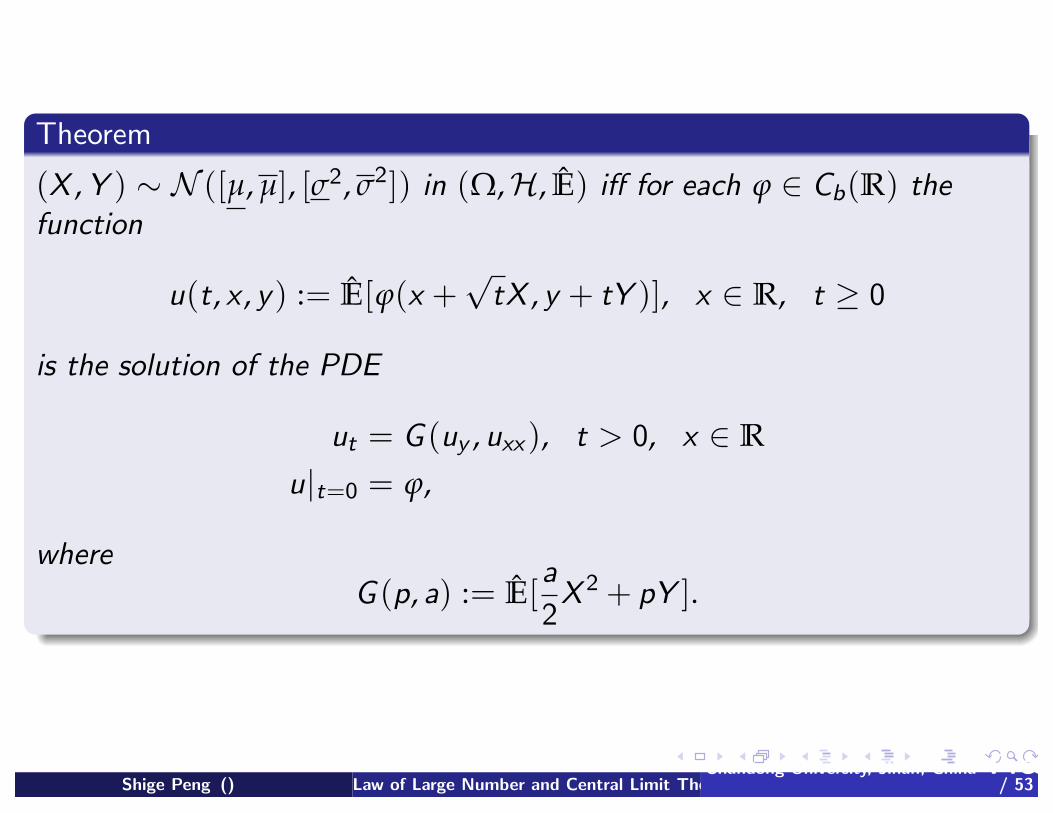

Theorem

(X , Y ) ∼ N ([µ, µ], [σ2, σ2]) in (Ω,H, E) iff for each ϕ ∈ Cb(R) the

function

u(t, x , y) := E[ϕ(x +√

tX , y + tY )], x ∈ R, t ≥ 0

is the solution of the PDE

ut = G (uy , uxx ), t > 0, x ∈ R

u|t=0 = ϕ,

where

G (p, a) := E[a

2X

2 + pY ].

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 38

/ 53

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 39

/ 53

Central Limit Theorem under Sublinear Expectation

Theorem

Let Xi + Yi∞i=1 be an independent and identically distributed sequence.

We assume furthermore that

E[|X1|2+α] + E[|Y1|

1+α] < ∞ and E[X1] = E[−X1] = 0.

SXn := X1 + · · ·+ Xn, SY

n := Y1 + · · ·+ Yn. Then Sn/√

n converges in

law to N (0; [σ2, σ2]):

limn→∞

E[ϕ(SX

n√

n+

SYn

n)] = E[ϕ(X + Y )], ∀ϕ ∈ Cb(R),

where (X , Y ) is N ([µ, µ], [σ2, σ2])-distributed.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 39

/ 53

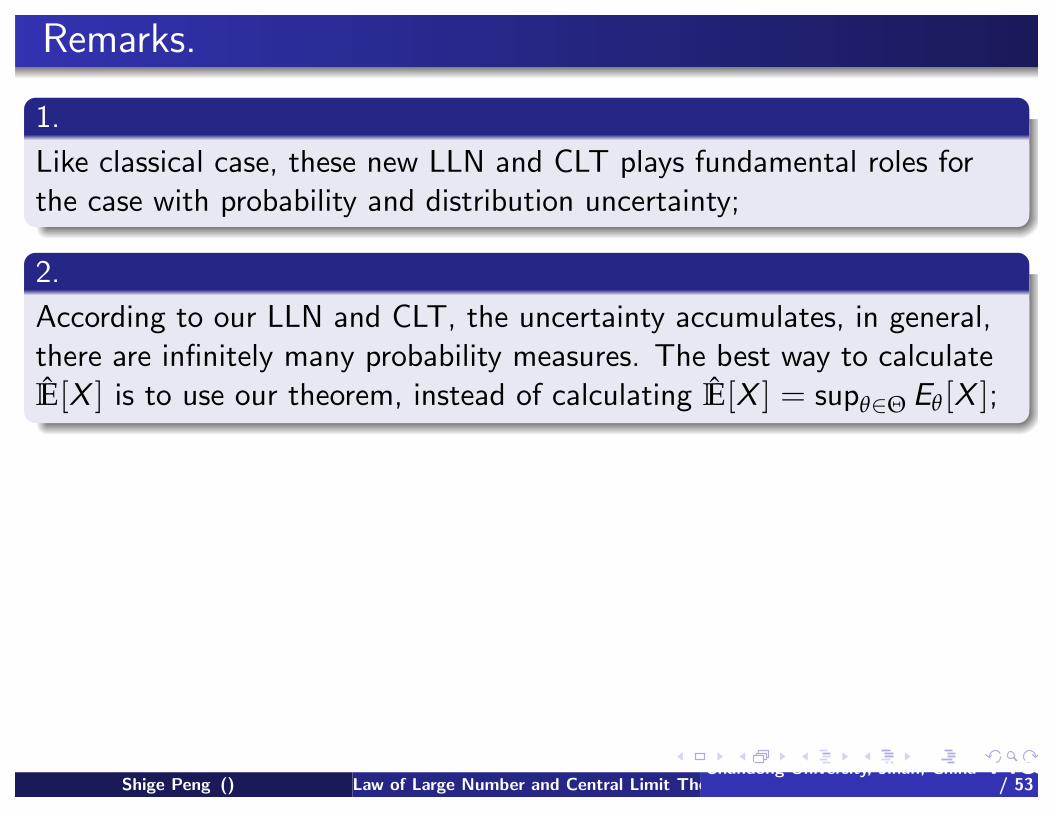

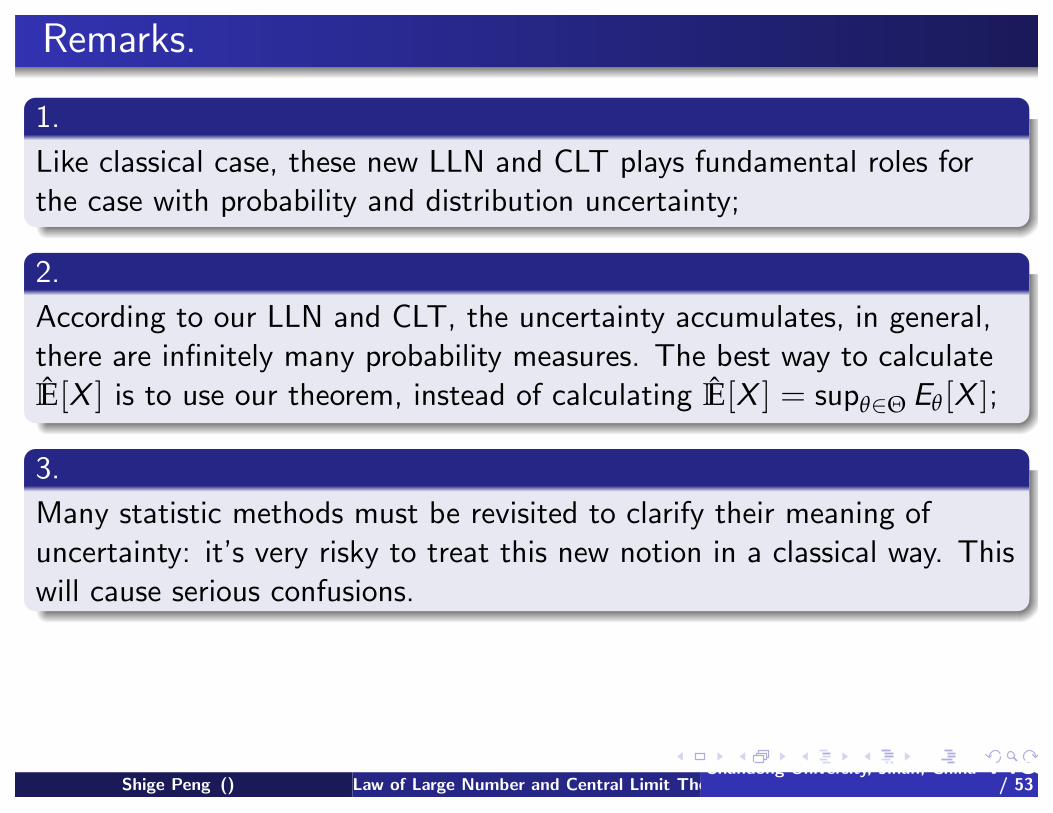

Remarks.

1.

Like classical case, these new LLN and CLT plays fundamental roles for

the case with probability and distribution uncertainty;

2.

According to our LLN and CLT, the uncertainty accumulates, in general,

there are infinitely many probability measures. The best way to calculate

E[X ] is to use our theorem, instead of calculating E[X ] = supθ∈Θ Eθ [X ];

3.

Many statistic methods must be revisited to clarify their meaning of

uncertainty: it’s very risky to treat this new notion in a classical way. This

will cause serious confusions.

4.

The third revolution: Deterministic point of view =⇒ Probabilistic point

of view =⇒ uncertainty of probabilities.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 40

/ 53

Remarks.

1.

Like classical case, these new LLN and CLT plays fundamental roles for

the case with probability and distribution uncertainty;

2.

According to our LLN and CLT, the uncertainty accumulates, in general,

there are infinitely many probability measures. The best way to calculate

E[X ] is to use our theorem, instead of calculating E[X ] = supθ∈Θ Eθ [X ];

3.

Many statistic methods must be revisited to clarify their meaning of

uncertainty: it’s very risky to treat this new notion in a classical way. This

will cause serious confusions.

4.

The third revolution: Deterministic point of view =⇒ Probabilistic point

of view =⇒ uncertainty of probabilities.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 40

/ 53

Remarks.

1.

Like classical case, these new LLN and CLT plays fundamental roles for

the case with probability and distribution uncertainty;

2.

According to our LLN and CLT, the uncertainty accumulates, in general,

there are infinitely many probability measures. The best way to calculate

E[X ] is to use our theorem, instead of calculating E[X ] = supθ∈Θ Eθ [X ];

3.

Many statistic methods must be revisited to clarify their meaning of

uncertainty: it’s very risky to treat this new notion in a classical way. This

will cause serious confusions.

4.

The third revolution: Deterministic point of view =⇒ Probabilistic point

of view =⇒ uncertainty of probabilities.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 40

/ 53

Remarks.

1.

Like classical case, these new LLN and CLT plays fundamental roles for

the case with probability and distribution uncertainty;

2.

According to our LLN and CLT, the uncertainty accumulates, in general,

there are infinitely many probability measures. The best way to calculate

E[X ] is to use our theorem, instead of calculating E[X ] = supθ∈Θ Eθ [X ];

3.

Many statistic methods must be revisited to clarify their meaning of

uncertainty: it’s very risky to treat this new notion in a classical way. This

will cause serious confusions.

4.

The third revolution: Deterministic point of view =⇒ Probabilistic point

of view =⇒ uncertainty of probabilities.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 40

/ 53

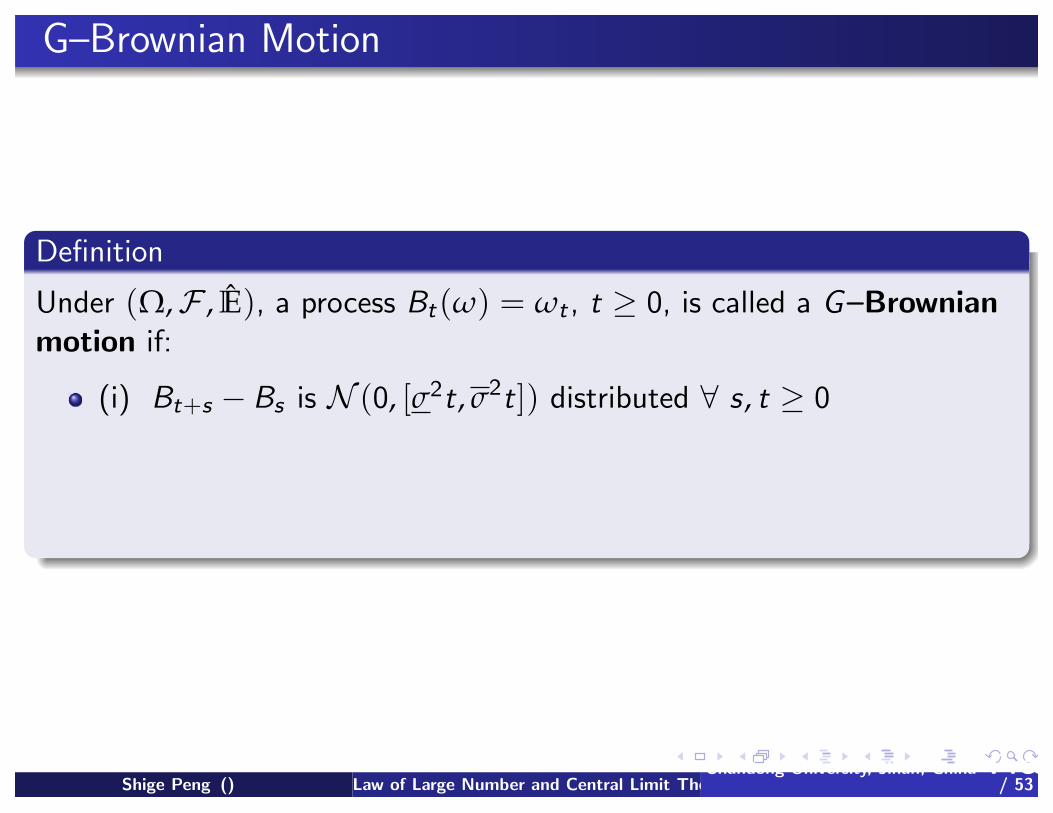

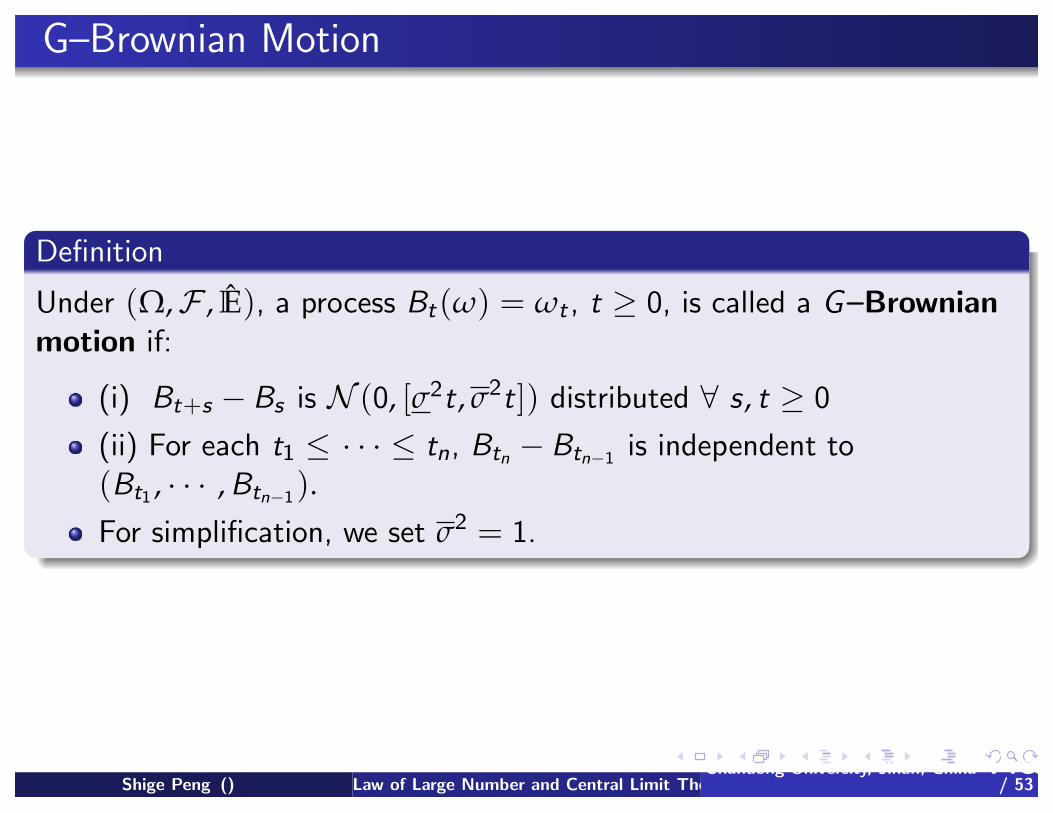

G–Brownian Motion

Definition

Under (Ω,F , E), a process Bt(ω) = ωt , t ≥ 0, is called a G–Brownianmotion if:

(i) Bt+s − Bs is N (0, [σ2t, σ2t]) distributed ∀ s , t ≥ 0

(ii) For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).For simplification, we set σ2 = 1.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 41

/ 53

G–Brownian Motion

Definition

Under (Ω,F , E), a process Bt(ω) = ωt , t ≥ 0, is called a G–Brownianmotion if:

(i) Bt+s − Bs is N (0, [σ2t, σ2t]) distributed ∀ s , t ≥ 0

(ii) For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).

For simplification, we set σ2 = 1.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 41

/ 53

G–Brownian Motion

Definition

Under (Ω,F , E), a process Bt(ω) = ωt , t ≥ 0, is called a G–Brownianmotion if:

(i) Bt+s − Bs is N (0, [σ2t, σ2t]) distributed ∀ s , t ≥ 0

(ii) For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).For simplification, we set σ2 = 1.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 41

/ 53

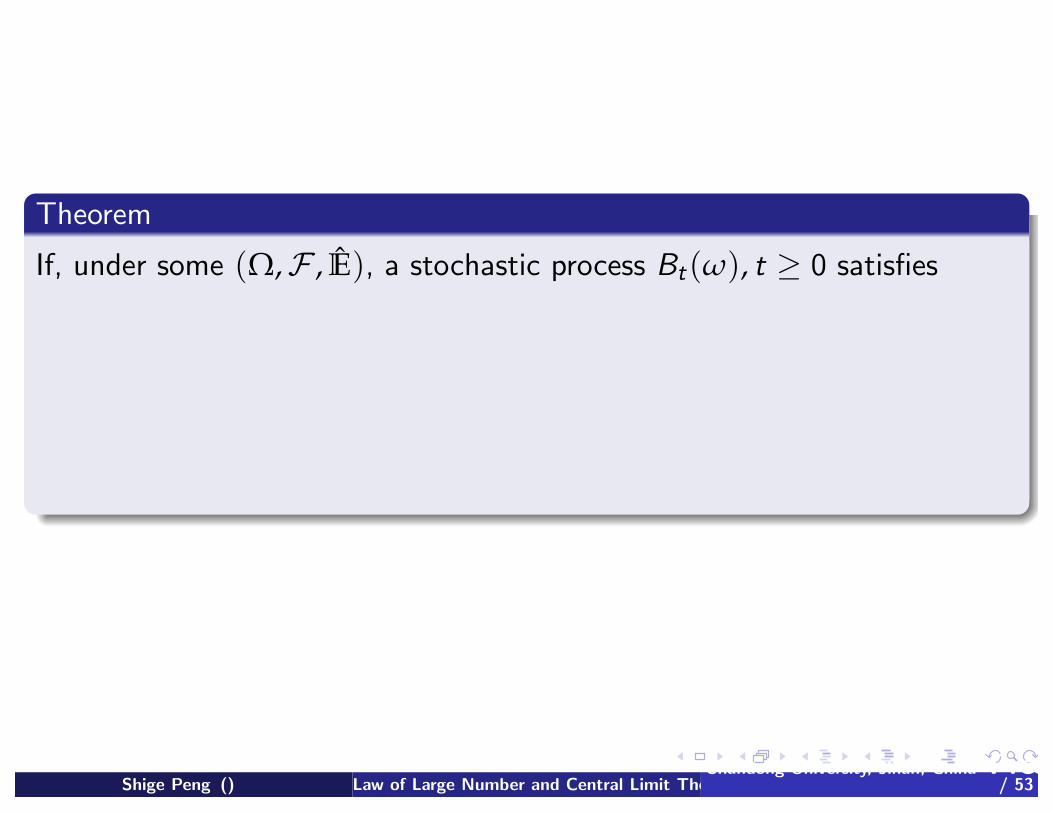

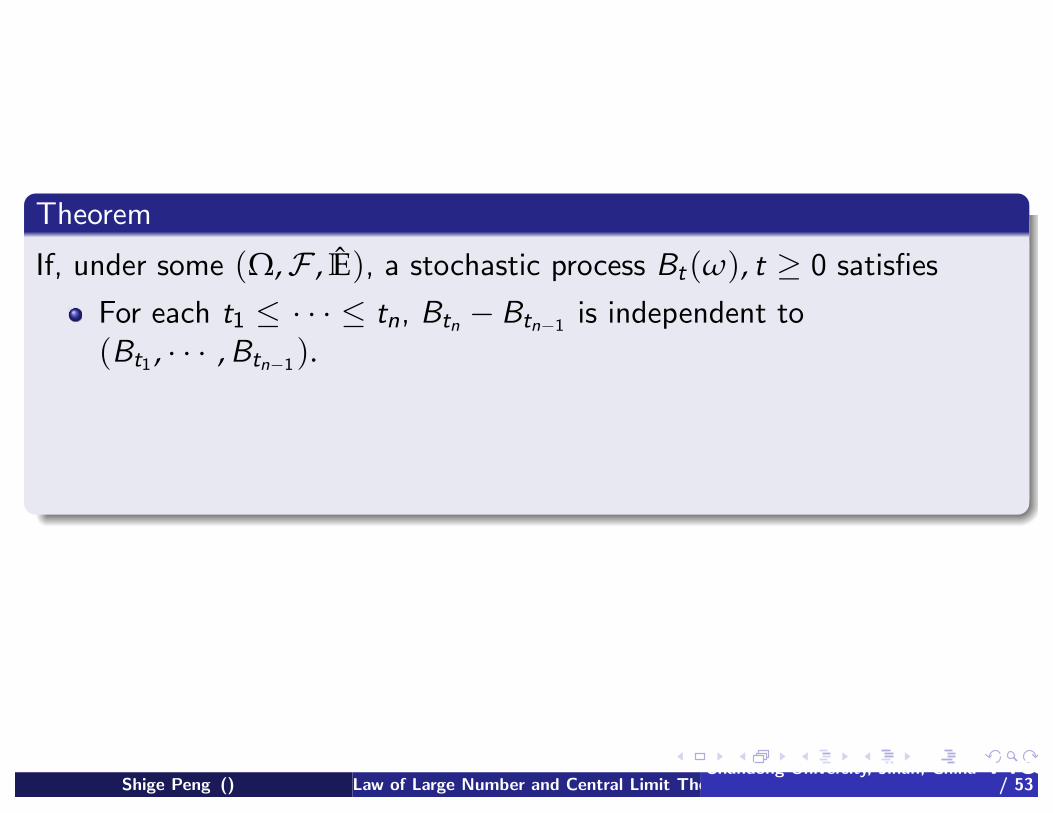

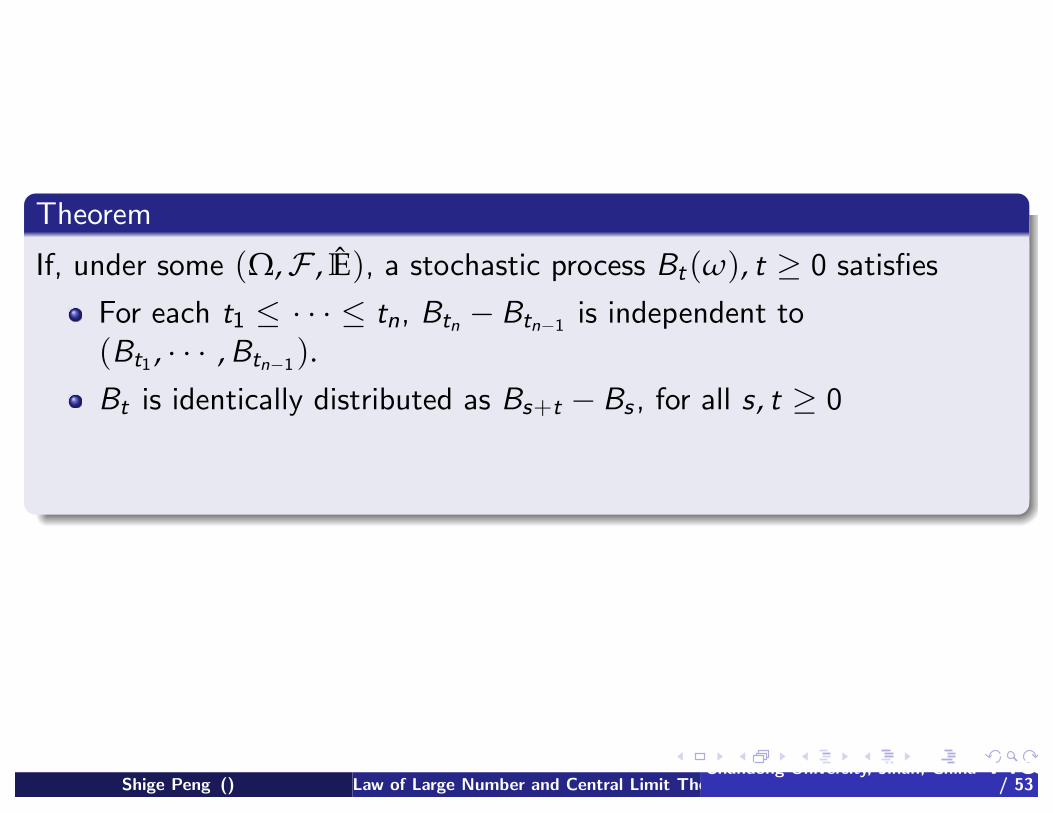

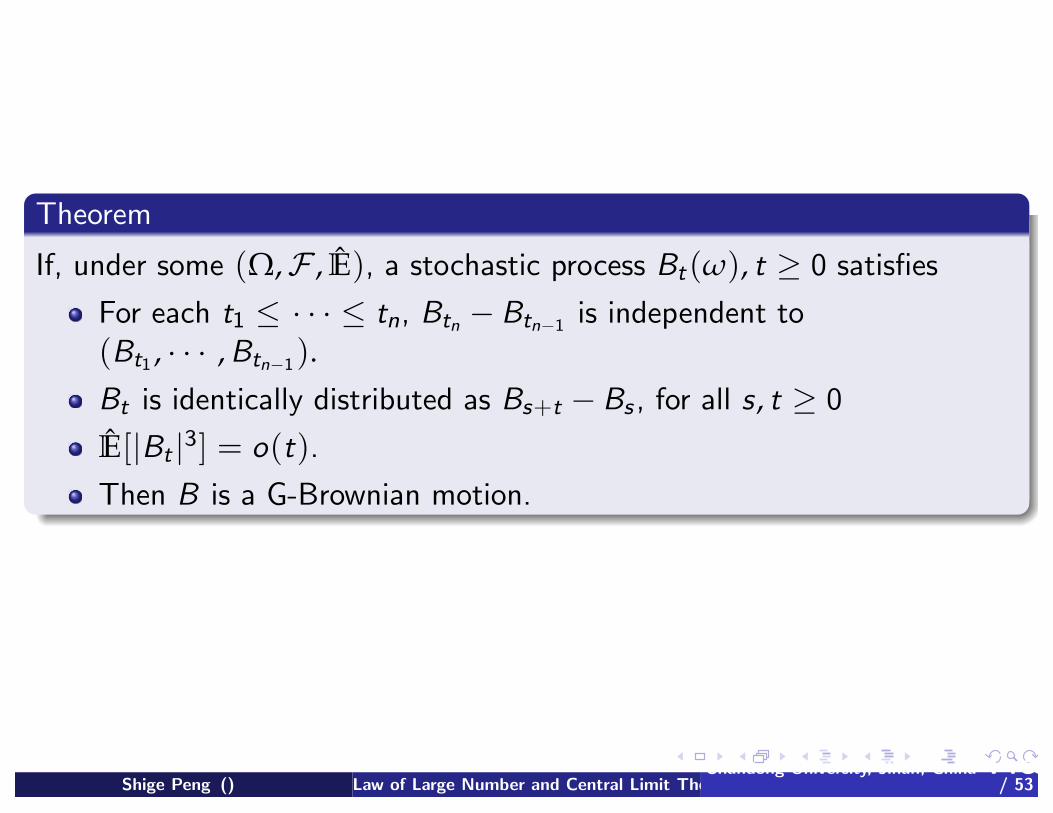

Theorem

If, under some (Ω,F , E), a stochastic process Bt(ω), t ≥ 0 satisfies

For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).Bt is identically distributed as Bs+t − Bs , for all s , t ≥ 0

E[|Bt |3] = o(t).

Then B is a G-Brownian motion.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 42

/ 53

Theorem

If, under some (Ω,F , E), a stochastic process Bt(ω), t ≥ 0 satisfies

For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).

Bt is identically distributed as Bs+t − Bs , for all s , t ≥ 0

E[|Bt |3] = o(t).

Then B is a G-Brownian motion.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 42

/ 53

Theorem

If, under some (Ω,F , E), a stochastic process Bt(ω), t ≥ 0 satisfies

For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).Bt is identically distributed as Bs+t − Bs , for all s , t ≥ 0

E[|Bt |3] = o(t).

Then B is a G-Brownian motion.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 42

/ 53

Theorem

If, under some (Ω,F , E), a stochastic process Bt(ω), t ≥ 0 satisfies

For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).Bt is identically distributed as Bs+t − Bs , for all s , t ≥ 0

E[|Bt |3] = o(t).

Then B is a G-Brownian motion.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 42

/ 53

Theorem

If, under some (Ω,F , E), a stochastic process Bt(ω), t ≥ 0 satisfies

For each t1 ≤ · · · ≤ tn, Btn − Btn−1 is independent to

(Bt1 , · · · , Btn−1).Bt is identically distributed as Bs+t − Bs , for all s , t ≥ 0

E[|Bt |3] = o(t).

Then B is a G-Brownian motion.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 42

/ 53

G–Brownian

Fact

Like N (0, [σ2, σ2])-distribution, the G-Brownian motion Bt(ω) = ωt ,

t ≥ 0, can strongly correlated under the unknown ‘objective probability’, it

can even be have very long memory. But it is i.i.d under the robust

expectation E. By which we can have many advantages in analysis,

calculus and computation, compare with, e.g. fractal B.M.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 43

/ 53

Ito’s integral of G–Brownian motion

For each process (ηt)t≥0 ∈ L2,0F

(0, T ) of the form

ηt(ω) =N−1

∑j=0

ξj (ω)I[tj ,tj+1)(t), ξj ∈L2(Ftj ) (Ftj -meas. & E[|ξj |2] < ∞)

we define

I (η) = T

0η(s)dBs :=

N−1

∑j=0

ξj (Btj+1 − Btj ).

Lemma

We have

E[ T

0η(s)dBs ] = 0

and

E[( T

0η(s)dBs)2] ≤

T

0E[(η(t))2]dt.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 44

/ 53

Ito’s integral of G–Brownian motion

For each process (ηt)t≥0 ∈ L2,0F

(0, T ) of the form

ηt(ω) =N−1

∑j=0

ξj (ω)I[tj ,tj+1)(t), ξj ∈L2(Ftj ) (Ftj -meas. & E[|ξj |2] < ∞)

we define

I (η) = T

0η(s)dBs :=

N−1

∑j=0

ξj (Btj+1 − Btj ).

Lemma

We have

E[ T

0η(s)dBs ] = 0

and

E[( T

0η(s)dBs)2] ≤

T

0E[(η(t))2]dt.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 44

/ 53

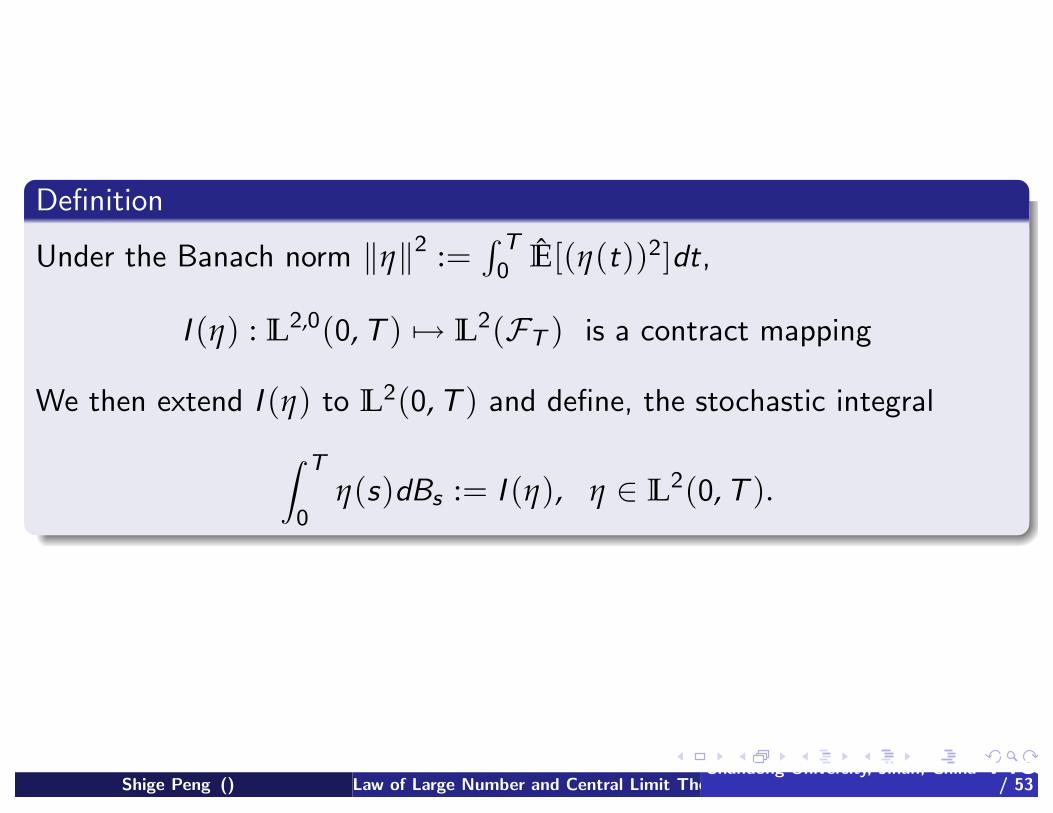

Definition

Under the Banach norm η2 := T0 E[(η(t))2]dt,

I (η) : L2,0(0, T ) → L2(FT ) is a contract mapping

We then extend I (η) to L2(0, T ) and define, the stochastic integral

T

0η(s)dBs := I (η), η ∈ L2(0, T ).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 45

/ 53

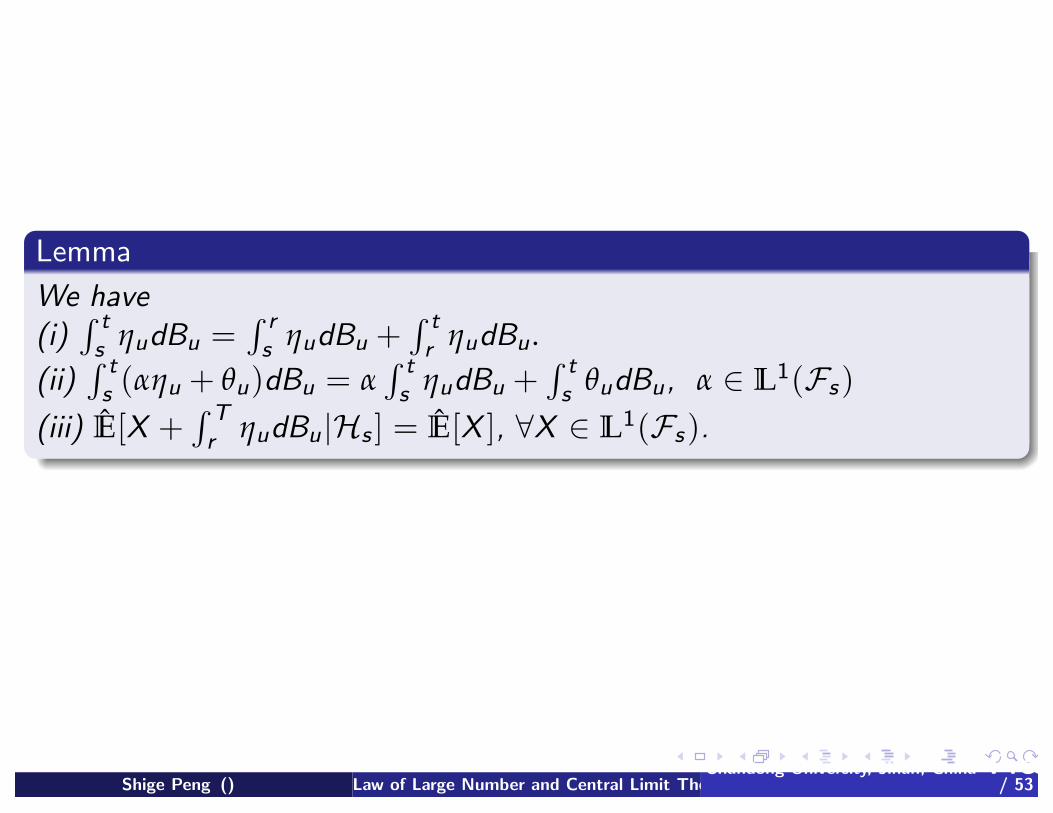

Lemma

We have

(i) ts ηudBu =

rs ηudBu +

tr ηudBu .

(ii) ts (αηu + θu)dBu = α

ts ηudBu +

ts θudBu, α ∈ L1(Fs)

(iii) E[X + Tr ηudBu |Hs ] = E[X ], ∀X ∈ L1(Fs).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 46

/ 53

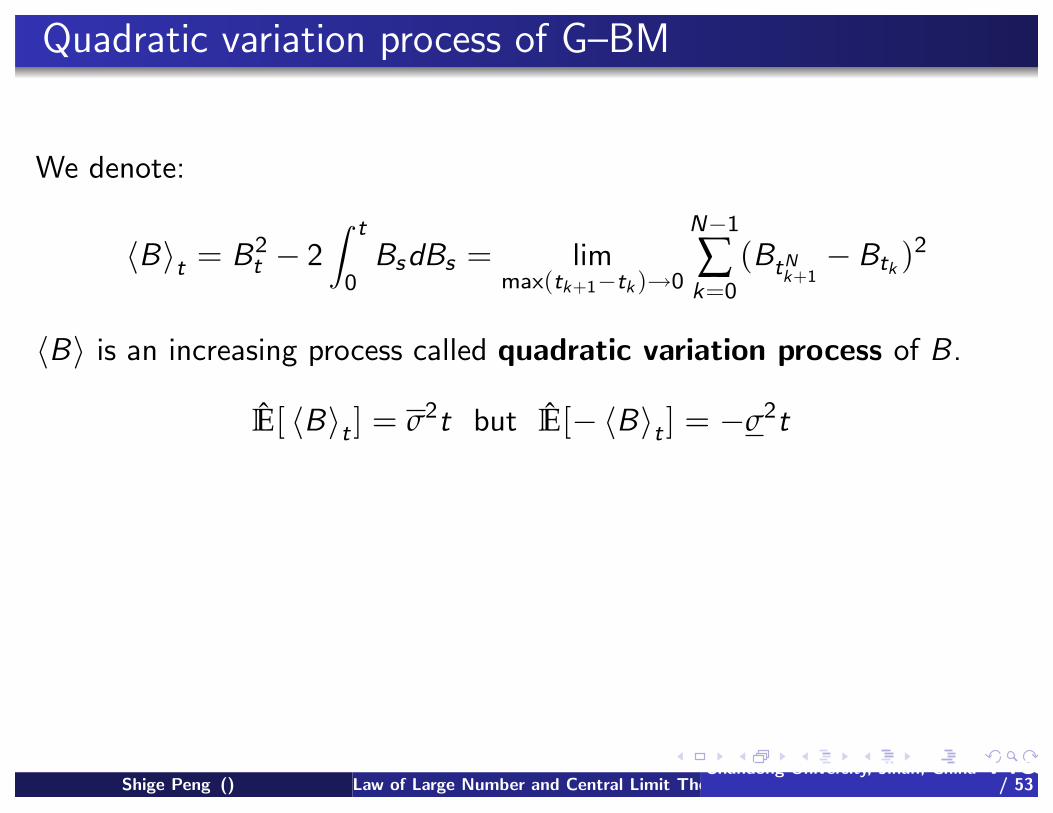

Quadratic variation process of G–BM

We denote:

Bt = B2t − 2

t

0BsdBs = lim

max(tk+1−tk )→0

N−1

∑k=0

(BtNk+1− Btk )

2

B is an increasing process called quadratic variation process of B.

E[ Bt ] = σ2t but E[− Bt ] = −σ2

t

Lemma

Bst := Bt+s − Bs , t ≥ 0 is still a G-Brownian motion. We also have

Bt+s − Bs ≡ Bst ∼ U ([σ2

t, σ2t]).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 47

/ 53

Quadratic variation process of G–BM

We denote:

Bt = B2t − 2

t

0BsdBs = lim

max(tk+1−tk )→0

N−1

∑k=0

(BtNk+1− Btk )

2

B is an increasing process called quadratic variation process of B.

E[ Bt ] = σ2t but E[− Bt ] = −σ2

t

Lemma

Bst := Bt+s − Bs , t ≥ 0 is still a G-Brownian motion. We also have

Bt+s − Bs ≡ Bst ∼ U ([σ2

t, σ2t]).

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 47

/ 53

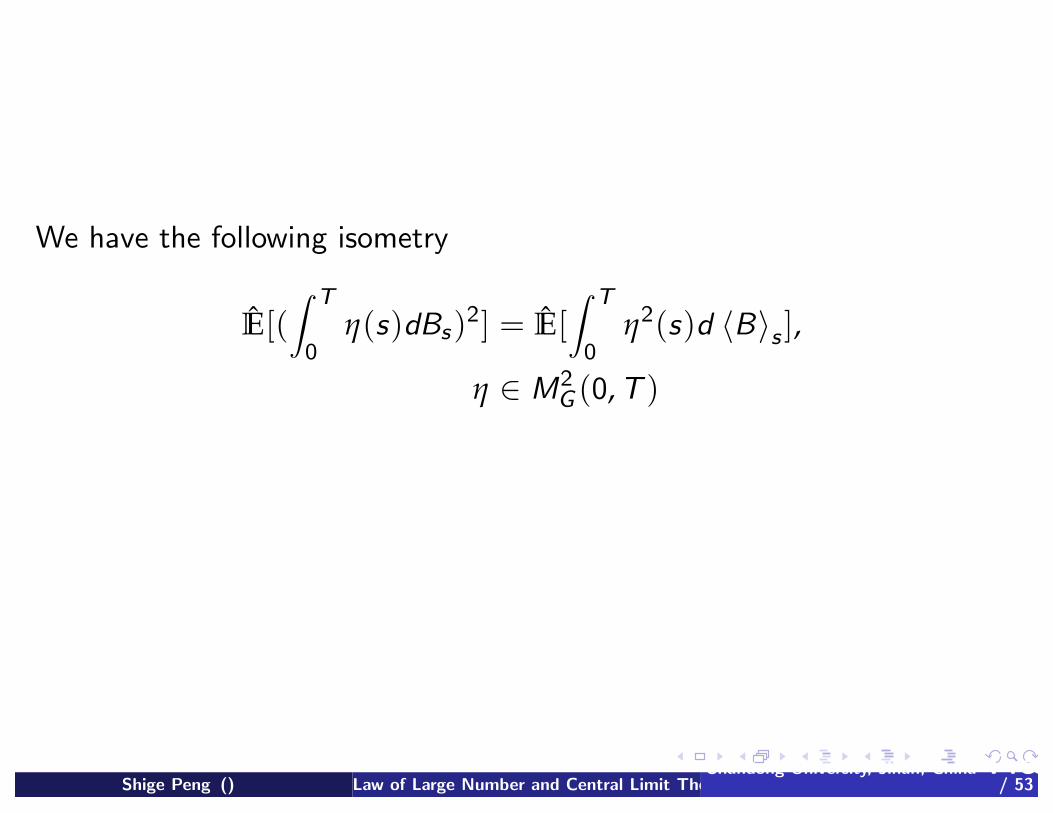

We have the following isometry

E[( T

0η(s)dBs)2] = E[

T

0η2(s)d Bs ],

η ∈ M2G (0, T )

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 48

/ 53

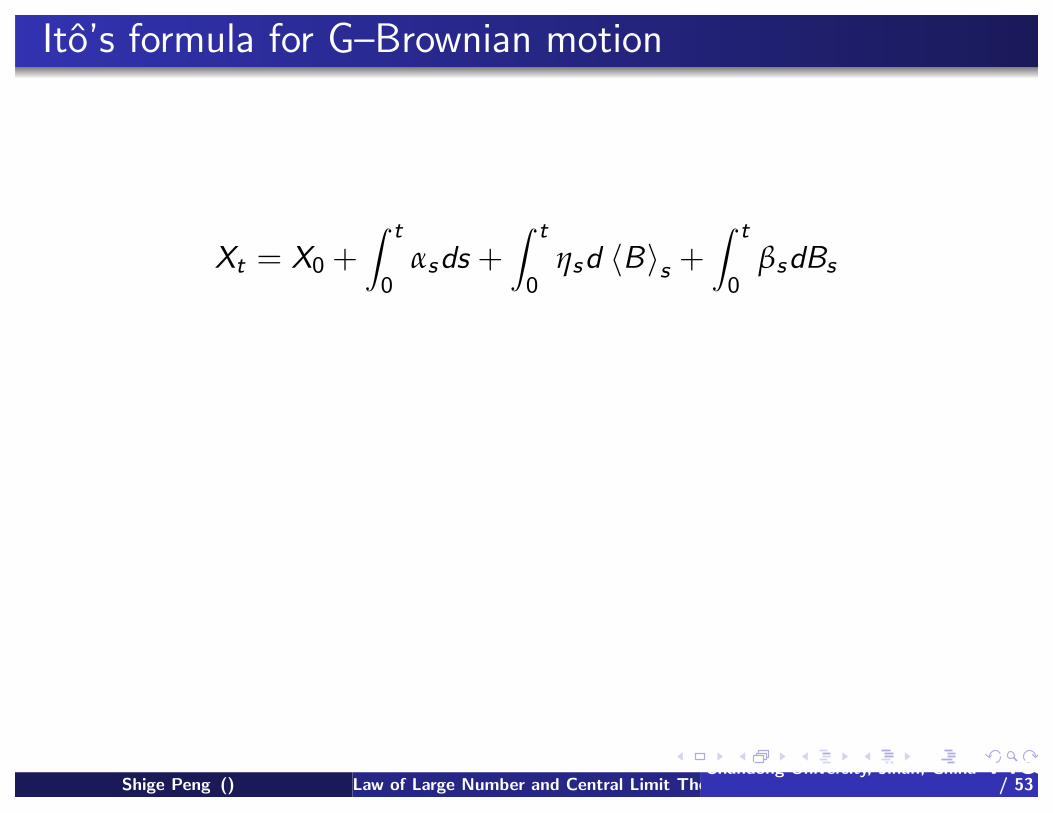

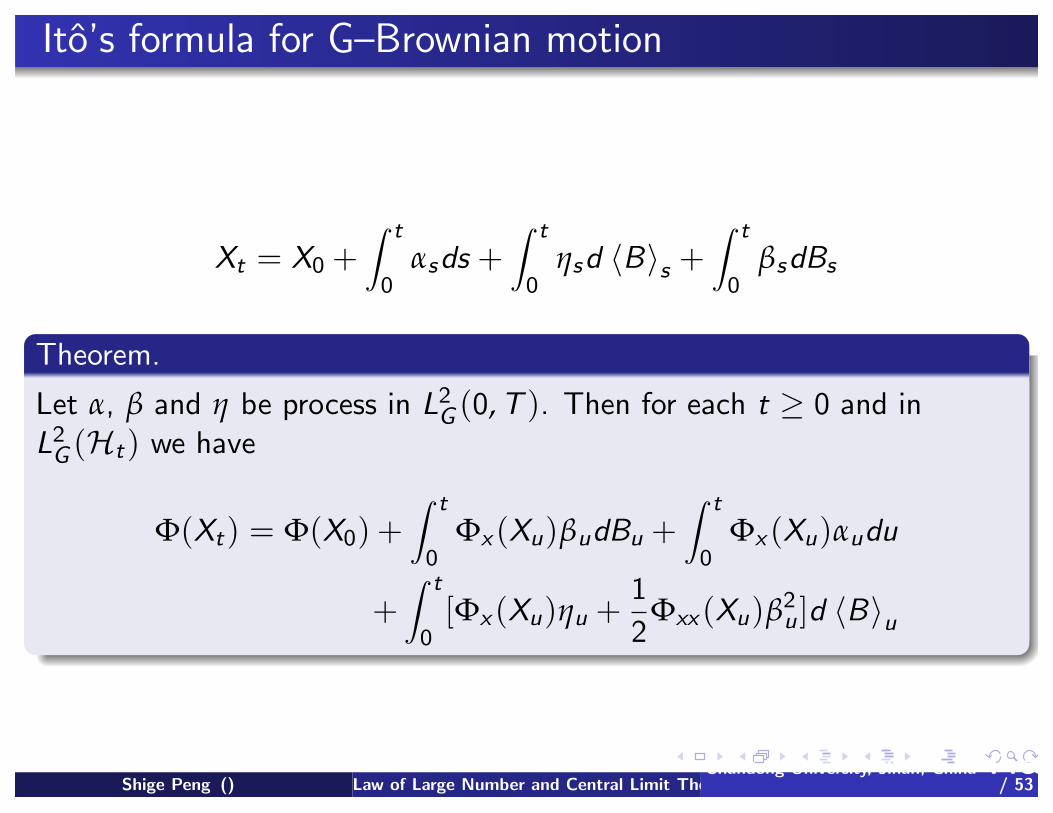

Ito’s formula for G–Brownian motion

Xt = X0 + t

0αsds +

t

0ηsd Bs +

t

0βsdBs

Theorem.

Let α, β and η be process in L2G (0, T ). Then for each t ≥ 0 and in

L2G (Ht) we have

Φ(Xt) = Φ(X0) + t

0Φx (Xu)βudBu +

t

0Φx (Xu)αudu

+ t

0[Φx (Xu)ηu +

1

2Φxx (Xu)β2

u ]d Bu

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 49

/ 53

Ito’s formula for G–Brownian motion

Xt = X0 + t

0αsds +

t

0ηsd Bs +

t

0βsdBs

Theorem.

Let α, β and η be process in L2G (0, T ). Then for each t ≥ 0 and in

L2G (Ht) we have

Φ(Xt) = Φ(X0) + t

0Φx (Xu)βudBu +

t

0Φx (Xu)αudu

+ t

0[Φx (Xu)ηu +

1

2Φxx (Xu)β2

u ]d Bu

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 49

/ 53

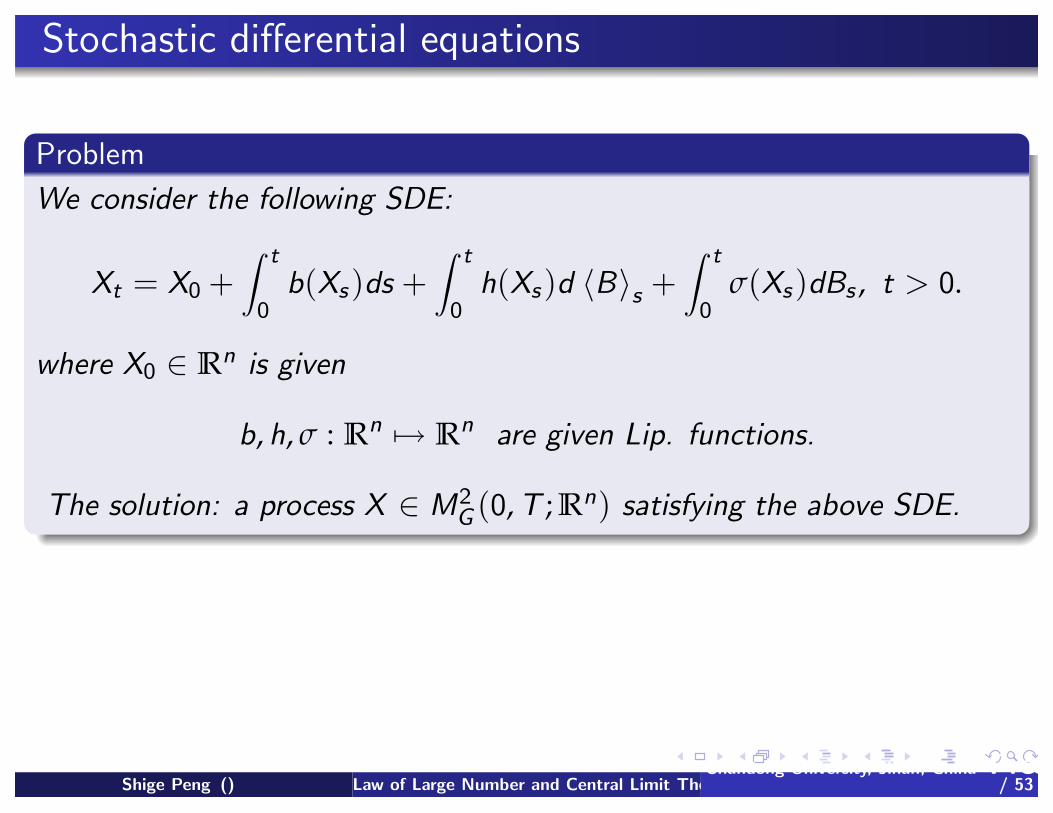

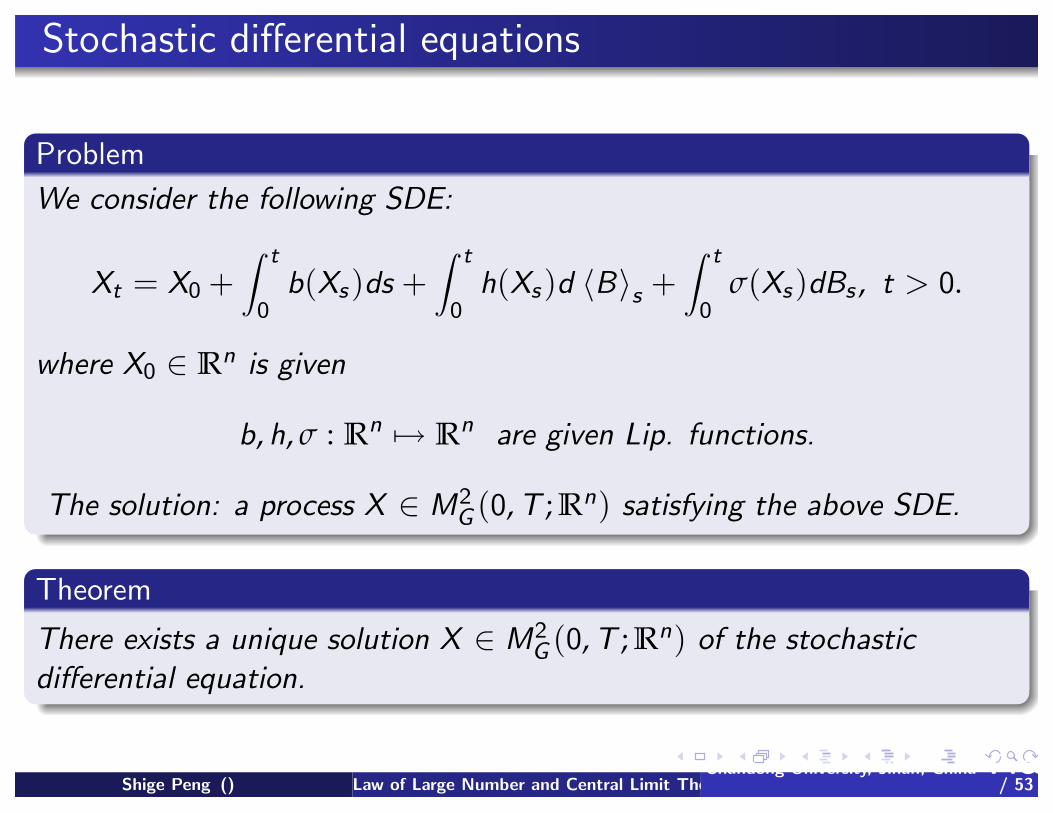

Stochastic differential equations

Problem

We consider the following SDE:

Xt = X0 + t

0b(Xs)ds +

t

0h(Xs)d Bs +

t

0σ(Xs)dBs , t > 0.

where X0 ∈ Rn is given

b, h, σ : Rn→ Rn

are given Lip. functions.

The solution: a process X ∈ M2G (0, T ; Rn) satisfying the above SDE.

Theorem

There exists a unique solution X ∈ M2G (0, T ; Rn) of the stochastic

differential equation.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 50

/ 53

Stochastic differential equations

Problem

We consider the following SDE:

Xt = X0 + t

0b(Xs)ds +

t

0h(Xs)d Bs +

t

0σ(Xs)dBs , t > 0.

where X0 ∈ Rn is given

b, h, σ : Rn→ Rn

are given Lip. functions.

The solution: a process X ∈ M2G (0, T ; Rn) satisfying the above SDE.

Theorem

There exists a unique solution X ∈ M2G (0, T ; Rn) of the stochastic

differential equation.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 50

/ 53

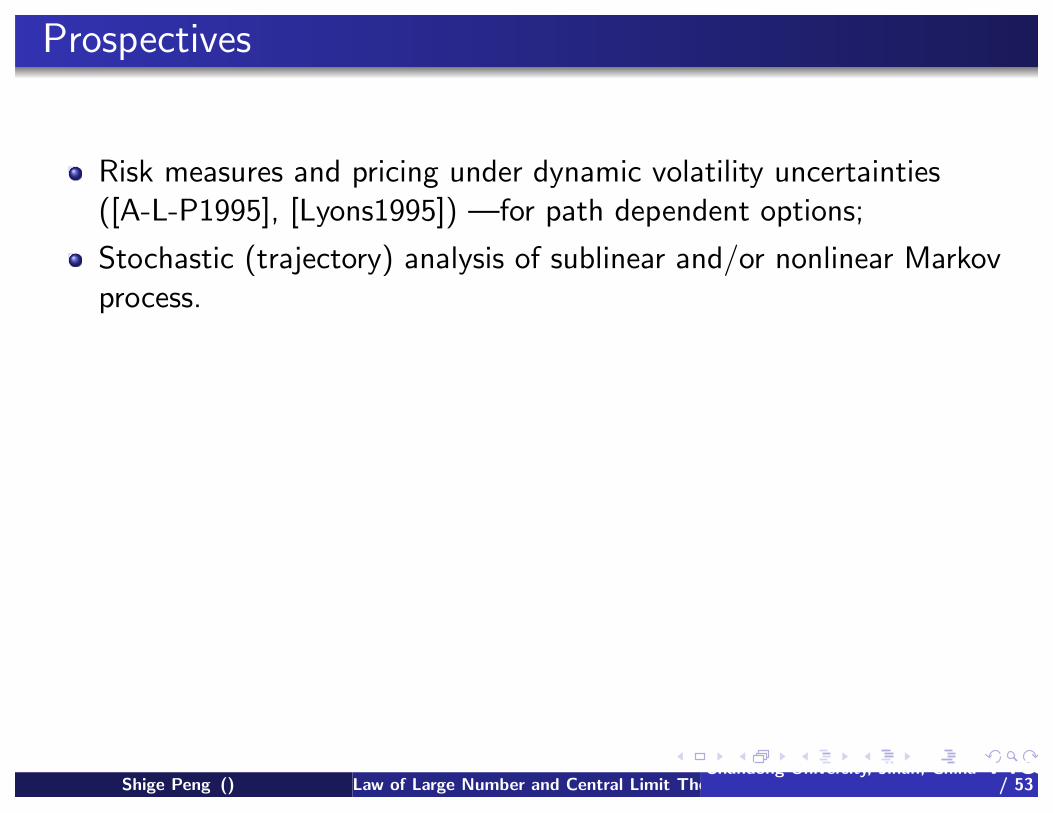

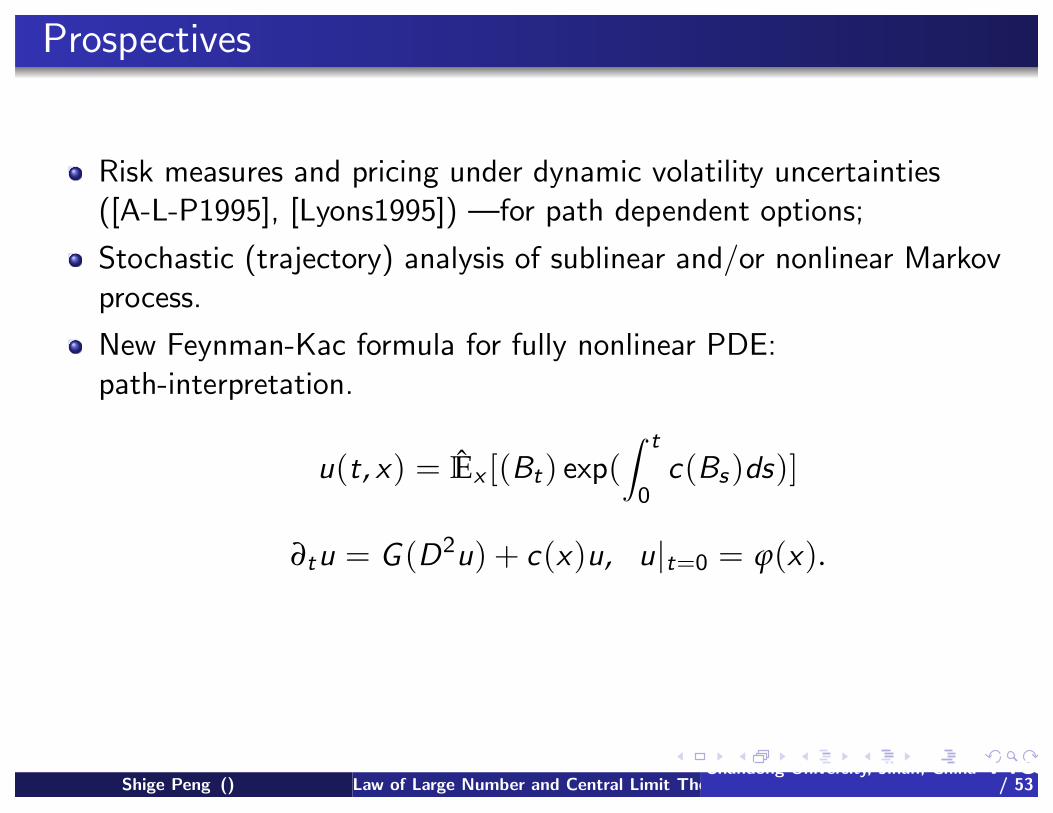

Prospectives

Risk measures and pricing under dynamic volatility uncertainties

([A-L-P1995], [Lyons1995]) —for path dependent options;

Stochastic (trajectory) analysis of sublinear and/or nonlinear Markov

process.

New Feynman-Kac formula for fully nonlinear PDE:

path-interpretation.

u(t, x) = Ex [(Bt) exp( t

0c(Bs)ds)]

∂tu = G (D2u) + c(x)u, u|t=0 = ϕ(x).

Fully nonlinear Monte-Carlo simulation.

BSDE driven by G -Brownian motion: a challenge.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 51

/ 53

Prospectives

Risk measures and pricing under dynamic volatility uncertainties

([A-L-P1995], [Lyons1995]) —for path dependent options;

Stochastic (trajectory) analysis of sublinear and/or nonlinear Markov

process.

New Feynman-Kac formula for fully nonlinear PDE:

path-interpretation.

u(t, x) = Ex [(Bt) exp( t

0c(Bs)ds)]

∂tu = G (D2u) + c(x)u, u|t=0 = ϕ(x).

Fully nonlinear Monte-Carlo simulation.

BSDE driven by G -Brownian motion: a challenge.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 51

/ 53

Prospectives

Risk measures and pricing under dynamic volatility uncertainties

([A-L-P1995], [Lyons1995]) —for path dependent options;

Stochastic (trajectory) analysis of sublinear and/or nonlinear Markov

process.

New Feynman-Kac formula for fully nonlinear PDE:

path-interpretation.

u(t, x) = Ex [(Bt) exp( t

0c(Bs)ds)]

∂tu = G (D2u) + c(x)u, u|t=0 = ϕ(x).

Fully nonlinear Monte-Carlo simulation.

BSDE driven by G -Brownian motion: a challenge.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 51

/ 53

Prospectives

Risk measures and pricing under dynamic volatility uncertainties

([A-L-P1995], [Lyons1995]) —for path dependent options;

Stochastic (trajectory) analysis of sublinear and/or nonlinear Markov

process.

New Feynman-Kac formula for fully nonlinear PDE:

path-interpretation.

u(t, x) = Ex [(Bt) exp( t

0c(Bs)ds)]

∂tu = G (D2u) + c(x)u, u|t=0 = ϕ(x).

Fully nonlinear Monte-Carlo simulation.

BSDE driven by G -Brownian motion: a challenge.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 51

/ 53

The talk is based on:

Peng, S. (2006) G–Expectation, G–Brownian Motion and Related

Stochastic Calculus of Ito’s type, in arXiv:math.PR/0601035v2 3Jan

2006, to appear in Proceedings of 2005 Abel Symbosium, Springer.

Peng, S. (2006) Multi-Dimensional G-Brownian Motion and Related

Stochastic Calculus under G-Expectation, in

arXiv:math.PR/0601699v2 28Jan 2006.

Peng, S. Law of large numbers and central limit theorem under

nonlinear expectations, in arXiv:math.PR/0702358v1 13 Feb 2007

Peng, S. A New Central Limit Theorem under Sublinear Expectations,

arXiv:0803.2656v1 [math.PR] 18 Mar 2008

Peng, S.L. Denis, M. Hu and S. Peng, Function spaces and capacity

related to a Sublinear Expectation: application to G-Brownian Motion

Pathes, see arXiv:0802.1240v1 [math.PR] 9 Feb 2008.

Song, Y. (2007) A general central limit theorem under Peng’s

G-normal distribution, Preprint.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 52

/ 53

The talk is based on:

Peng, S. (2006) G–Expectation, G–Brownian Motion and Related

Stochastic Calculus of Ito’s type, in arXiv:math.PR/0601035v2 3Jan

2006, to appear in Proceedings of 2005 Abel Symbosium, Springer.

Peng, S. (2006) Multi-Dimensional G-Brownian Motion and Related

Stochastic Calculus under G-Expectation, in

arXiv:math.PR/0601699v2 28Jan 2006.

Peng, S. Law of large numbers and central limit theorem under

nonlinear expectations, in arXiv:math.PR/0702358v1 13 Feb 2007

Peng, S. A New Central Limit Theorem under Sublinear Expectations,

arXiv:0803.2656v1 [math.PR] 18 Mar 2008

Peng, S.L. Denis, M. Hu and S. Peng, Function spaces and capacity

related to a Sublinear Expectation: application to G-Brownian Motion

Pathes, see arXiv:0802.1240v1 [math.PR] 9 Feb 2008.

Song, Y. (2007) A general central limit theorem under Peng’s

G-normal distribution, Preprint.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 52

/ 53

The talk is based on:

Peng, S. (2006) G–Expectation, G–Brownian Motion and Related

Stochastic Calculus of Ito’s type, in arXiv:math.PR/0601035v2 3Jan

2006, to appear in Proceedings of 2005 Abel Symbosium, Springer.

Peng, S. (2006) Multi-Dimensional G-Brownian Motion and Related

Stochastic Calculus under G-Expectation, in

arXiv:math.PR/0601699v2 28Jan 2006.

Peng, S. Law of large numbers and central limit theorem under

nonlinear expectations, in arXiv:math.PR/0702358v1 13 Feb 2007

Peng, S. A New Central Limit Theorem under Sublinear Expectations,

arXiv:0803.2656v1 [math.PR] 18 Mar 2008

Peng, S.L. Denis, M. Hu and S. Peng, Function spaces and capacity

related to a Sublinear Expectation: application to G-Brownian Motion

Pathes, see arXiv:0802.1240v1 [math.PR] 9 Feb 2008.

Song, Y. (2007) A general central limit theorem under Peng’s

G-normal distribution, Preprint.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 52

/ 53

The talk is based on:

Peng, S. (2006) G–Expectation, G–Brownian Motion and Related

Stochastic Calculus of Ito’s type, in arXiv:math.PR/0601035v2 3Jan

2006, to appear in Proceedings of 2005 Abel Symbosium, Springer.

Peng, S. (2006) Multi-Dimensional G-Brownian Motion and Related

Stochastic Calculus under G-Expectation, in

arXiv:math.PR/0601699v2 28Jan 2006.

Peng, S. Law of large numbers and central limit theorem under

nonlinear expectations, in arXiv:math.PR/0702358v1 13 Feb 2007

Peng, S. A New Central Limit Theorem under Sublinear Expectations,

arXiv:0803.2656v1 [math.PR] 18 Mar 2008

Peng, S.L. Denis, M. Hu and S. Peng, Function spaces and capacity

related to a Sublinear Expectation: application to G-Brownian Motion

Pathes, see arXiv:0802.1240v1 [math.PR] 9 Feb 2008.

Song, Y. (2007) A general central limit theorem under Peng’s

G-normal distribution, Preprint.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 52

/ 53

The talk is based on:

Peng, S. (2006) G–Expectation, G–Brownian Motion and Related

Stochastic Calculus of Ito’s type, in arXiv:math.PR/0601035v2 3Jan

2006, to appear in Proceedings of 2005 Abel Symbosium, Springer.

Peng, S. (2006) Multi-Dimensional G-Brownian Motion and Related

Stochastic Calculus under G-Expectation, in

arXiv:math.PR/0601699v2 28Jan 2006.

Peng, S. Law of large numbers and central limit theorem under

nonlinear expectations, in arXiv:math.PR/0702358v1 13 Feb 2007

Peng, S. A New Central Limit Theorem under Sublinear Expectations,

arXiv:0803.2656v1 [math.PR] 18 Mar 2008

Peng, S.L. Denis, M. Hu and S. Peng, Function spaces and capacity

related to a Sublinear Expectation: application to G-Brownian Motion

Pathes, see arXiv:0802.1240v1 [math.PR] 9 Feb 2008.

Song, Y. (2007) A general central limit theorem under Peng’s

G-normal distribution, Preprint.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 52

/ 53

Thank you,

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 53

/ 53

In the classic period of Newton’s mechanics, including A. Einstein, people

believe that everything can be deterministically calculated. The last

century’s research affirmatively claimed the probabilistic behavior of our

universe: God does plays dice!

Nowadays people believe that everything has its own probability

distribution. But a deep research of human behaviors shows that for

everything involved human or life such, as finance, this may not be true: a

person or a community may prepare many different p.d. for your selection.

She change them, also purposely or randomly, time by time.

Shige Peng () Law of Large Number and Central Limit Theorem under Uncertainty, the Related New Ito’s Calculus and Applications to Risk MeasuresShandong University, Jinan, China Presented at 1st PRIMA Congress, July 06-10, 2009 UNSW, Sydney, Australia 53

/ 53