latin america unified communications & collaboration solutions market

TRANSCRIPT

Latin America Unified Communications &

Collaboration Solutions Market

Executive Summary

NDEC-64

July 2014

NDEC-64 2

Study Description & Research Methodology

NDEC-64 3

Study Description

Market Scope:

• This study examines the trends in the unified communications and collaboration

solutions market in Latin America.

• It estimates the incomes of the product providers of unified communications in

2013 and projects the revenues up to 2020.

• The study considers incomes provided by product manufacturers

(manufacturing revenue) and excludes revenues generated by indirect channels

of distribution (street revenue).

• It does not consider incomes generated by provision of services, but only

considers products on premise—in other words, this study excludes revenue

generated by hosted products or cloud base.

Source: Frost & Sullivan analysis.

NDEC-64 4

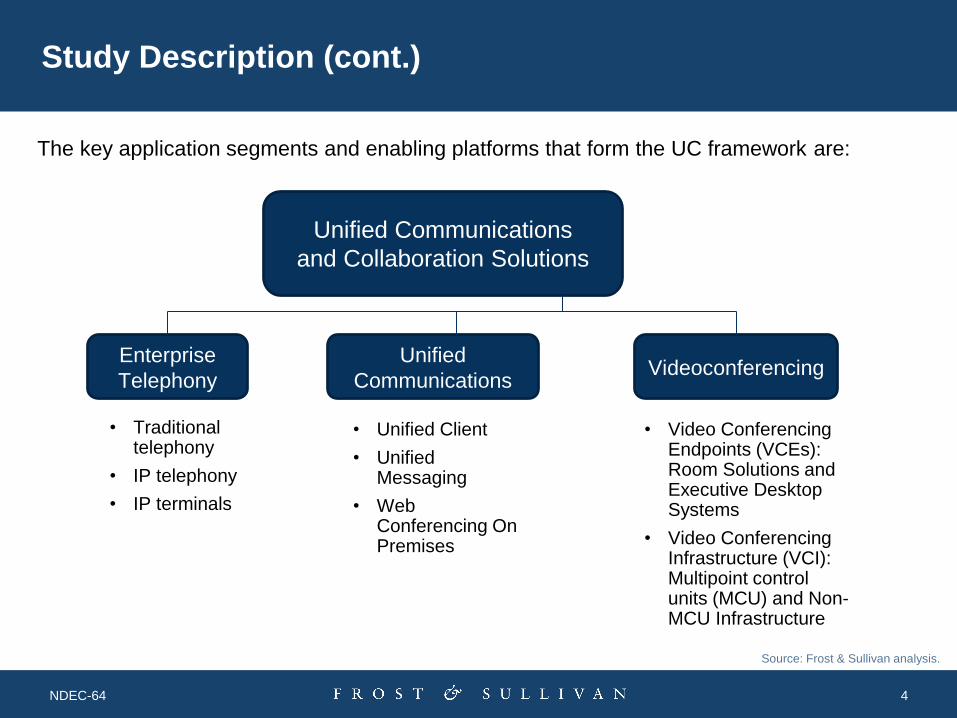

Study Description (cont.)

The key application segments and enabling platforms that form the UC framework are:

Unified Communications

and Collaboration Solutions

Unified

Communications Videoconferencing

Enterprise

Telephony

• Traditional telephony

• IP telephony

• IP terminals

• Video Conferencing Endpoints (VCEs): Room Solutions and Executive Desktop Systems

• Video Conferencing Infrastructure (VCI): Multipoint control units (MCU) and Non-MCU Infrastructure

• Unified Client

• Unified Messaging

• Web Conferencing On Premises

Source: Frost & Sullivan analysis.

NDEC-64 5

Study Description (cont.)

• Enterprise telephony

• Enterprise telephony is an umbrella term used to define traditional telephony, IP

telephony, and IP phones.

•For traditional and IP telephony, this study only considers the line-license component

that provides the end user access to an enterprise telephony system. Revenue from

any hardware or software element necessary for the telephony system to work is not

included. Furthermore, managed services and service fees associated with

maintenance, integration, and installation are not included.

• Time Division Multiplexing (TDM)

• Traditional telephony refers to telephony line licenses that work over private-branch-

exchange (PBX) systems.

• IP Telephony

• Internet protocol (IP) telephony refers to telephony line licenses that work over IP-PBX

systems. The IP-PBX can be a hybrid system (that supports traditional telephony and

IP telephony), but a license must be an IP-line license for consideration in this

category.

Source: Frost & Sullivan analysis.

NDEC-64 6

• IP Terminals

• IP phones are communications endpoints that connect to the company network and

provide the end user access to the enterprise’s IP communications system. This study only

counts desktop IP phones, not multimedia IP phones equipped to support video calling.

• Unified Communications

• UC is an umbrella term that, depending on the source, can cover a wide range of

information and communication technologies (ICTs). For this study, only unified clients and

unified messaging solutions are considered. Furthermore, only client-access license (CAL)

revenue that enables the end user to use the aforementioned solutions is included.

Hardware components necessary for these solutions to work are not included, nor are

managed services or service fees associated with maintenance, integration, and

installation.

• Unified Client

• Unified clients are software-based interfaces that include the following capabilities: PC-

based presence, telephony presence, point-to-point voice calling and PBX call handling,

instant messaging, audio conferencing, application and file sharing, and PC-based video.

Study Description (cont.)

Source: Frost & Sullivan analysis.

NDEC-64 7

• Unified Messaging

• Unified messaging includes applications that integrate storage and accessibility of

voice, fax, and email messages into a single mailbox that can be accessed by email,

telephone, Web browser, or a unified client.

• Web Conferencing On Premises

• Web conferencing on premises is available as a licensed software for installation on

servers; the Web conferencing application is deployed behind the enterprise firewall

and managed by the customer. This product is typically offered as a converged

conferencing of a UC solution.

• Video Conferencing

• In this study, Frost & Sullivan only considers room solutions, executive desktop

systems, and infrastructure systems, within the videoconferencing category.

• Frost & Sullivan counts revenue from the physical component sales of the

aforementioned solutions. All professional and managed services are excluded from

the revenue count.

Study Description (cont.)

Source: Frost & Sullivan analysis.

NDEC-64 8

Study Description (cont.)

• VCE

Within video conferencing endpoints (VCEs), this research service considers room

solutions and executive desktop systems.

• Room Solution

• Room videoconferencing solutions facilitate videoconferencing in a group setting. These

are high-quality systems designed to be used in shared environments such as meeting

rooms, boardrooms, and auditoriums. This category has evolved tremendously over the

last several years. Price points have come down, form factors have become more

diverse, and functionality has improved.

• Executive Desktop Systems

• Executive desktop systems are characterized by fully integrated hardware–based

endpoints with built-in camera, microphone, speakers, and LCD, which can also be

utilized as a PC monitor. These units are primarily designed for personal conferencing.

The smaller form factor makes them well-suited for desktops, executive suites, remote

offices, and doctors’ offices.

Source: Frost & Sullivan analysis.

NDEC-64 9

• VCI

• Within video conferencing infrastructure (VCI), this study considers multipoint control

units and non-multi point control units.

• MCU

• A videoconferencing bridge, also called a multipoint control unit (MCU), allows

videoconferencing endpoints to connect and participate in a multi-point conference.

• Non-MCU Infrastructure

• Infrastructure systems include routers, firewall traversal, gateways, gatekeepers, and

management and scheduling software.

Study Description (cont.)

Source: Frost & Sullivan analysis.

NDEC-64 10

Research Methodology

This strategic analysis is part of Frost & Sullivan’s continued coverage of the Latin

America unified communications and enterprise solutions market.

Geographical Regions Covered:

• The study covers the following regions: Brazil, Mexico, Central America and The

Caribbean, Andean Region (Colombia, Venezuela, Peru, Bolivia, Ecuador),

Southern Cone (Argentina, Chile, Paraguay, Uruguay).

Research Methodology and Scope:

o In order to assess the current LATAM unified communications solutions market, data from

many primary and secondary sources were used, including: Interviews with enterprise

telephony, software, and equipment vendors.

o Frost & Sullivan‘s published research services

o Frost & Sullivan‘s decision support databases

o Company Websites and other secondary sources

The base year for this research service is 2013 and forecast period is 2014 to 2020.

Source: Frost & Sullivan analysis.

NDEC-64 11

Study Description (cont.) - Table of Contents

Source: Frost & Sullivan analysis.

NDEC-64 12

Executive Summary

NDEC-64 13

Executive Summary

• In 2013, the unified communications and collaboration solutions market in Latin America generated a

revenue of $890,386,656 Million, representing a growth of 3.8% from 2012.

• In 2014, market revenue growth is expected to be small. Lack of knowledge about all the benefits of

these services, recession in the economies of the region, depreciation of local currencies, free

solutions as participants of the market, lower prices, and bundle options that included more than one

technology at special rates are the main reasons for this recession.

• However, UC applications, along with IP telephony and videoconferencing, are expected to continue

to grow. The total unified communications and collaboration solutions market is forecast to grow at a

compound annual growth rate (CAGR) of 6.8% during 2013–2020.

• The enterprise telephony segment is forecast to grow at a CAGR of 5.2% due to the decline in IP

prices. While the units are expected to grow, the prices are likely to decline, producing a balance with

a similar revenue scenario as the year before.

• The unified communications segment is expected to grow at a CAGR of 11.4%, considering the

escalating price of its components. This is the highest-growing segment in the market. The products

in this segment are gaining popularity steadily and are known as a software that increases

productivity.

• The video conferencing segment is expected to grow at a CAGR of 8.1%, considering the growing

recognition of these solutions. VCI is likely to stand out within this segment

• In 2013, Brazil was the largest market in Latin America, accounting for 37.4% of total sales, having a

39.3% market share in 2012. Mexico is positioned to get the second place in 2013 of the market

share in Latin America, with 25.0%, owning a 22.8% market share in 2012. Source: Frost & Sullivan analysis.

NDEC-64 14

Market Status by Application

• Enterprise Telephony continues to be the

most important segment in terms of revenues.

• The time-division multiplexing (TDM)

telephony segment decelerated since vendors

are switching focus to increase Internet

protocol (IP) telephony solutions penetration.

• Unified communications demonstrated stable

growth throughout the LATAM region, with the

Mexican market experiencing the highest

growth from 2012, closely followed by the

Andean region and the Southern Cone region

. However, Brazil has the highest investments

in this solution.

• The videoconferencing segment grew at 16.4

percent. Is the smallest segment within the

unified communications and collaboration

solutions market. Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan analysis.

Percent Sales Breakdown

Total UC and Collaboration Solutions Market by Segment: LATAM, 2013

69.5%

17.2%

13.2%

Enterprise Telephony Unified Communications Video Conferencing

NDEC-64 15

Drivers & Restraints M

ark

et

Dri

vers

M

ark

et

Restr

ain

ts

Total UC and Collaboration Solutions Market: Key Market Drivers and Restraints, LATAM, 2012–2020

Government restrictive polices (such as taxes in Brazil and

restriction on import of equipment in Argentina) likely to restrain UC

equipment adoption M M M

Constant development, promotion, and access to cost-free solutions restrains growth.

M L L

Unstable economic scenario in key Latin American countries

slows market growth M L L

Underdeveloped IT infrastructure in Latin America affects technology adoption in secondary cities

M L L

1–2 Years 3–5 Years 6–7 Years

Globalization of Latin American economies likely to generate new opportunities for unified communications

M M L

Low costs of employment and maintenance of new communication solutions to increase implementation of solutions M M L

Conception of new collaborative and multitask jobs, which require secure, rapid feedback would drive the adoption of UC applications

M M L

Arrival of enhanced devices that enable and support UC solutions to allow increase penetration of advanced applications in Latin America

L M M

Impact: H High M Medium L Low Note: Drivers and restraints are ranked in order of impact. Source: Frost & Sullivan analysis.

NDEC-64 16

The Frost & Sullivan Story

NDEC-64 17

Who is Frost & Sullivan

Frost & Sullivan, the Growth Partnership Company, enables clients to accelerate growth and

achieve best-in-class positions in growth, innovation and leadership. The company's Growth

Partnership Service provides the CEO and the CEO's Growth Team with disciplined

research and best-practice models to drive the generation, evaluation, and implementation

of powerful growth strategies. Frost & Sullivan leverages 50 years of experience in

partnering with Global 1000 companies, emerging businesses and the investment

community from more than 40 offices on six continents.

To join our Growth Partnership, please visit http://www.frost.com.

NDEC-64 18

What Makes Us Unique

All services aligned on growth to help clients develop and implement

innovative growth strategies

Continuous monitoring of industries and their convergence, giving clients first

mover advantage in emerging opportunities

More than 40 global offices ensure that clients gain global perspective to

mitigate risk and sustain long term growth

Proprietary TEAM Methodology integrates 7 critical research perspectives to

optimize growth investments

Career research and case studies for the CEOs’ Growth Team to ensure

growth strategy implementation at best practice levels

Close collaboration with clients in developing their research-based visionary

perspective to drive GIL

Focused on Growth

Industry Coverage

Global Footprint

Career Best Practices

360 Degree Perspective

Visionary Innovation Partner

NDEC-64 19

TEAM Methodology

Frost & Sullivan’s proprietary TEAM Methodology ensures that clients have a complete 360 Degree

PerspectiveTM from which to drive decision making. Technical, Econometric, Application, and Market

information ensures that clients have a comprehensive view of industries, markets, and technology.

Technical

Real-time intelligence on technology, including emerging technologies, new

R&D breakthroughs, technology forecasting, impact analysis, groundbreaking

research, and licensing opportunities.

Econometric

In-depth qualitative and quantitative research focused on timely and critical

global, regional, and country-specific trends, including the political,

demographic, and socioeconomic landscapes.

Application

Insightful strategies, networking opportunities, and best practices that can be

applied for enhanced market growth; interactions between the client, peers,

and Frost & Sullivan representatives that result in added value and

effectiveness.

Market

Global and regional market analysis, including drivers and restraints, market

trends, regulatory changes, competitive insights, growth forecasts, industry

challenges, strategic recommendations, and end-user perspectives.

NDEC-64 20

Global Perspective

• 1,700 staff across every major market worldwide

• Over 10,000 clients worldwide from emerging to global 1000 companies

NDEC-64 21

Frost & Sullivan Contacts

Jose Roberto Mavignier

Director of Latin America - ICT

Frost & Sullivan Latin America

+55 11 3065-8463

Juan Manuel Gonzalez

ICT Industry Manager

Frost & Sullivan Latin America

+54 11 4777 0071

Valeria Goldsworthy

Industry Analyst - ICT

Frost & Sullivan Latin America

+55 11 4771 8006