latin america shines: is it for real this time? - bbva research · static conceptstatic concept...

TRANSCRIPT

Latin America shines: Is it for real this time?Latibex

November, 2010

José Luis Escrivá│Chief Economist BBVA Research │

Page 2Page 2Page 2

Main Messages

• Latin America has changed, both politically and economically

• A great deal of macroeconomic stability has been achieved: inflation has been conquered in most countries and fiscal discipline is now widespread

• These changes, together with external factors such as growing ties with Asia and benign terms of trade, have contributed to sustained growth in the region

• The region has passed major economic and political tests, and is emerging stronger from the current financial crisis: higher credit ratings and lower risk premiums are evidence of this

• There have been a few setbacks, but we believe they will be temporary

• Major challenges remain, but growing middle classes with an stake in the good performance of the economic system is a major source of stability

• There is room for further increases in potential growth if reforms materialize in microeconomic issues, investments in infra-structure and education

• We are convinced that this time is for real: Latin America is entering a path of sustained progress

Page 3

Index

Latin America

shines: Is it for real this

time?Latibex

Section I

Global OutlookSection II Latin America breaks with the past

Section III Latin America passes the “stress test”

Section IV A bright future, if the right road is taken

Section V

Latin America: Investment possibility

Page 4

Section I

Global Outlook

Global OutlookEconomic growth in 2010 across key geographical areas will be above expected one year ago. We expect positive growth for BBVA´s key markets, significantly higher in Emerging Markets.

2011 GDP growth revision Source: BBVA Research Forecasts. *Latin America: Arg, Bra, Chi, Col, Mex, Per and Ven.

Latin America Economic Growth:

• Breaks with the past

• Passes the “stress test”

• A bright future:

– Capital inflows

– Commodity Prices

– Asian Dynamism

– Potential Growth0123456789

10

USA Alabama Texas EMU Spain China LatinAmerica

Advanced Economies EmergingEconomies

Page 5

Note: 45 Emerging Markets– Argentina, Bahrain, Bangladesh, Brazil, Bulgaria, Chile, China, Colombia, Czech Rep., Egypt, Estonia, Hungary, India, Indonesia, Iran, Jordan, Korea, Kuwait, Latvia, Lithuania, Malaysia, Mauritius, Mexico, Morocco, Nigeria, Oman, Pakistan, Peru, Philippines, Poland, Qatar, Romania, Russia, Slovak Rep., South Africa, Sri Lanka, Sudan, Taiwan, Thailand, Tunisia, Turkey, Ukraine, UAE, Venezuela, Vietnam.

Section I

Global Outlook

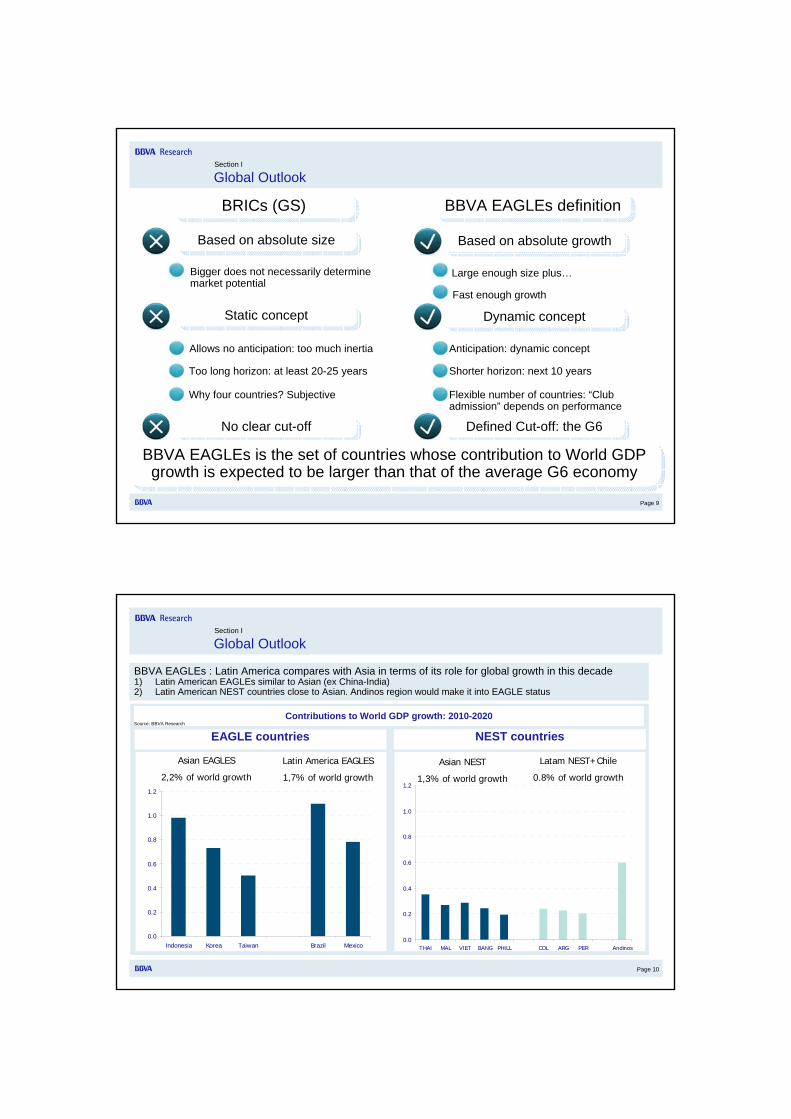

Towards a two speed WorldG7 countries’ growth is expected to remain below 2% for the next 10 yearsEmerging markets growth will outpace the G7 average by 4pp including China and 2,5pp excluding the Asian giant

GDP adjusted by PPP: growth rateSource: BBVA Research and IMF

0

1

2

3

4

5

6

7

8

9

10

2003-2007 2011-2020

BRICs BRICs without China EM without BRICs G7

Page 6

Section I

Global Outlook

Everybody is looking at Asia, but the strength of Latin America can stand up to comparison

The recovery has been as strong, taking into account a deeper impact of the crisis

GDP growth rateSource: BBVA Research and IMF

-4

-2

0

2

4

6

8

10

2006

2007

2008

2009

2010

2011

LATAM* Emerging Asia* (ex. China)

+7.5 %

+4.7%

Page 7

Section I

Global Outlook

Excluding China, the growth differential is moderate (1pp) and…

0

1

2

3

4

5

6

7

8

9

10

LATAM* Emerging Asia* (ex.China)

China

Average2010-2015

LATAM vs. ASIA: Potential GDP growth between 2010-2015Source: BBVA Research

LATAM: Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela

Emerging Asia: Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand

Page 8

Section I

Global Outlook

Moreover, since Latin American countries are more developed, their growth rates look very attractive

LATAM vs. ASIA: Potential GDP growth and income per capitaSource: BBVA Research

Mexico

Brazil Argentina

ChileColombia

Peru

Venezuela

Hong Kong

India

Indonesia

Korea

Malaysia

PhilippinesSingaporeTaiwanThailand

China

0

1

2

3

4

5

6

7

8

9

8.0 8.5 9.0 9.5 10.0 10.5 11.0

GDP per capita: logarithme (average 2010-2015)

Pote

ntia

l GD

P gr

owth

: (av

erag

e 20

10-

2015

)

Page 9

Based on absolute sizeBased on absolute size Based on absolute growthBased on absolute growth

Allows no anticipation: too much inertia

Bigger does not necessarily determine market potential

Too long horizon: at least 20-25 years

Anticipation: dynamic concept

Large enough size plus…

Shorter horizon: next 10 years

BRICs (GS)BRICs (GS) BBVA EAGLEs definitionBBVA EAGLEs definition

Static conceptStatic concept Dynamic conceptDynamic concept

No clear cut-offNo clear cut-off Defined Cut-off: the G6Defined Cut-off: the G6

Why four countries? Subjective Flexible number of countries: “Club admission” depends on performance

BBVA EAGLEs is the set of countries whose contribution to World GDP growth is expected to be larger than that of the average G6 economy

BBVA EAGLEs is the set of countries whose contribution to World GDP growth is expected to be larger than that of the average G6 economy

Fast enough growth

Section I

Global Outlook

Page 10

Section I

Global Outlook

BBVA EAGLEs : Latin America compares with Asia in terms of its role for global growth in this decade1) Latin American EAGLEs similar to Asian (ex China-India)2) Latin American NEST countries close to Asian. Andinos region would make it into EAGLE status

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Indonesia Korea Taiwan Brazil Mexico

Contributions to World GDP growth: 2010-2020Source: BBVA Research

EAGLE countries

Asian EAGLES

2,2% of world growth

Latin America EAGLES

1,7% of world growth

0.0

0.2

0.4

0.6

0.8

1.0

1.2

THAI MAL VIET BANG PHILL COL ARG PER Andinos

Asian NEST

1,3% of world growth

Latam NEST+Chile

0.8% of world growth

NEST countries

Page 11

Section I

Global Outlook

High liquidity and low interest rates, at least for a whileWhile the long-term benchmark rate in USA is at record low levels due to high and rising liquidity to revive lending in the Advanced Economies, Latin America (as most Emerging Markets) has seen risk premiums fall, creating very favorable financial conditions and pressures for their currencies to appreciate

Benchmark Rate US Treasury Bond (10 Y)Source: BBVA Research Forecasts.

Spread CDS Latin America vs. Germany. Source: BBVA Research Forecasts. *Latin America: Bra, Chi, Col, Mex and Per.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Average 2004-2008 Now

0

20

40

60

80

100

120

140

160

180

Average 2004-2008 Now

Page 12

Index

Latin America

shines: Is it for real this

time?Latibex

Section IGlobal Outlook

Section II

Latin America breaks with the pastSection III Latin America passes the “stress test”

Section IV A bright future, if the right road is taken

Section VLatin America: Investment possibility

Page 13

Section II

Latin America breaks with the past

LatAm, GDP per capita, relative performance to US, decade average. 70’s=100Source: BBVA Research

Latam is beginning to close the Income Gap after decades of disappointmentThe financial crisis has not stopped the convergence process. In the past, recessions meant long periods of divergence

LatAm, GDP per capita, relative performance to US, crisis(*) comparison. (*) US recession in terms of GDP pc. Source: BBVA Research

90

95

100

105

110

-2 -1 0 1 2 3 4Years since the Crisis

90

95

100

105

110

Current, 2008 Average, 1980-1991-2002

0

20

40

60

80

100

120

70's 80's 90's 00's 10's (2010-12)0

20

40

60

80

100

120

Page 14

Section II

Latin America breaks with the past

While taming inflation in the late 90s, the region made sustained progress in external and public solvency over the years

LatAm, External DebtAs % of the GDPSource: BBVA Research

LatAm, External and Fiscal Balance. As % of the GDPSource: BBVA Research

LatAm, InflationCPI, %, yearly averageSource: BBVA Research

0

50

100

150

200

250

300

350

80's 90's 00's 10's (2010-12)0

50

100

150

200

250

300

350

0

5

10

15

20

25

30

35

40

45

50

80's 90's 00's 10's (2010-12)0

5

10

15

20

25

30

35

40

45

50

-16

-14

-12

-10

-8

-6

-4

-2

0

2

80's 90's 00's 10's (2010-12)-16

-14

-12

-10

-8

-6

-4

-2

0

2

Current Account Balance Fiscal Balance

Page 15

Section II

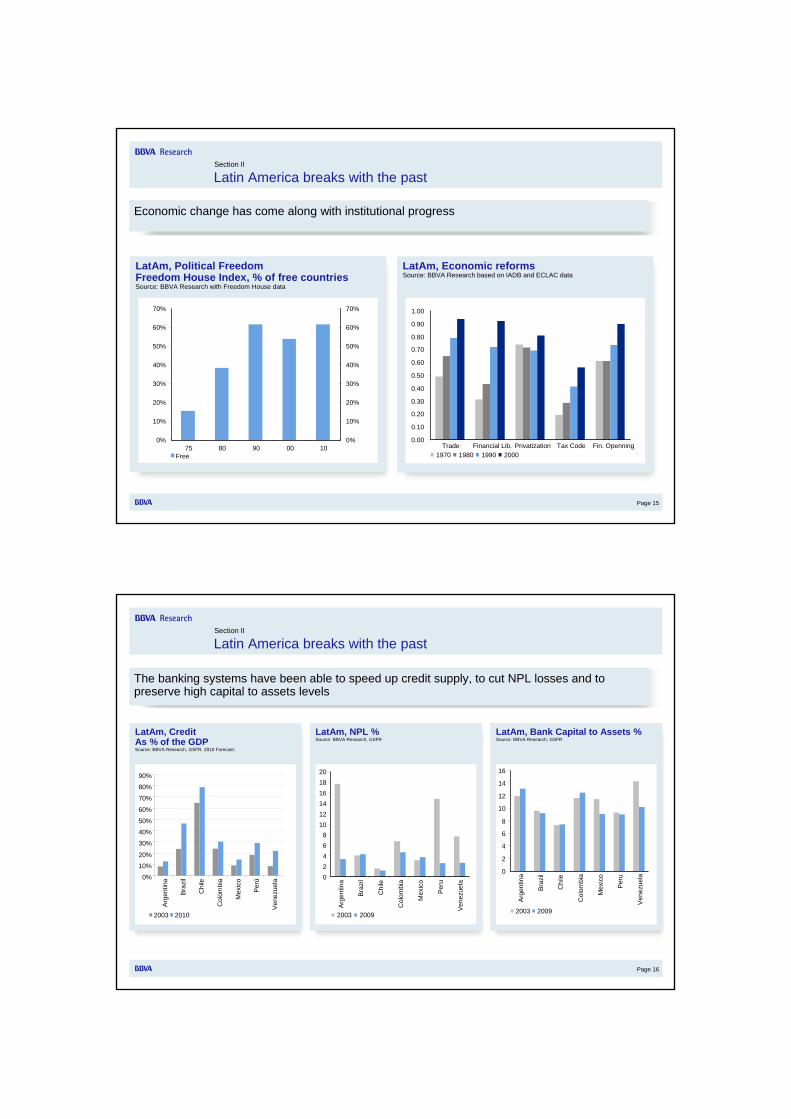

Latin America breaks with the past

LatAm, Political FreedomFreedom House Index, % of free countriesSource: BBVA Research with Freedom House data

LatAm, Economic reformsSource: BBVA Research based on IADB and ECLAC data

0%

10%

20%

30%

40%

50%

60%

70%

75 80 90 00 100%

10%

20%

30%

40%

50%

60%

70%

Free

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Trade Financial Lib. Privatization Tax Code Fin. Openning1970 1980 1990 2000

Economic change has come along with institutional progress

Page 16

Section II

Latin America breaks with the past

The banking systems have been able to speed up credit supply, to cut NPL losses and to preserve high capital to assets levels

LatAm, Bank Capital to Assets %Source: BBVA Research, GSFR

LatAm, NPL %Source: BBVA Research, GSFR

LatAm, Credit As % of the GDPSource: BBVA Research, GSFR. 2010 Forecast.

02468

101214161820

Arge

ntin

a

Braz

il

Chi

le

Col

ombi

a

Mex

ico

Peru

Vene

zuel

a

2003 2009

0

2

4

6

8

10

12

14

16

Arge

ntin

a

Braz

il

Chi

le

Col

ombi

a

Mex

ico

Peru

Vene

zuel

a

2003 2009

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Arge

ntin

a

Braz

il

Chi

le

Col

ombi

a

Mex

ico

Perú

Vene

zuel

a

2003 2010

Page 17

Index

Latin America

shines: Is it for real this

time?Latibex

Section IGlobal Outlook

Section II Latin America breaks with the past

Section III

Latin America passes the “stress test”Section IV A bright future, if the right road is taken

Section VLatin America: Investment possibility

Page 18

The second test, the “Election cycle”

Section III

The region has passed a demanding sequence of tests since the 90s

Rob

ustn

ess

test

s

The first test, a hike in interest rates in the US

´

The current“twin test”

The region made substantial economic and institutional reforms, but also enjoyed a benign favorable environment in the second half of the 00sBut the region also confronted – and passed -severe tests, including the global financial crisis of 08

Early 2000’s Mid 2000’s Late 2000’s

The third test, global financial turbulences

The fourth test, commodity prices and global recession

Page 19

Response to an increase on global interest rates: decoupling based on enhanced financial soundness

Section III

First test: increase on global interest rates

Spread EMBI Latam vs. US 3 month interest rateSource: JP Morgan, Datastream and BBVA Research

Spread EMBI Latam vs. US 3 month interest rateSource: JP Morgan, Datastream and BBVA Research

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Jan-

92M

ar-9

2M

ay-9

2Ju

l-92

Sep-

92N

ov-9

2Ja

n-93

Mar

-93

May

-93

Jul-9

3Se

p-93

Nov

-93

Jan-

94M

ar-9

4M

ay-9

4Ju

l-94

Sep-

94N

ov-9

4Ja

n-95

Mar

-95

May

-95

Jul-9

5Se

p-95

Nov

-95 400

600

800

1000

1200

1400

1600

1800

2000

US 3 month interest rate Spread Embi+ Latam (right axis)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-

02M

ar-0

2M

ay-0

2Ju

l-02

Sep-

02N

ov-0

2Ja

n-03

Mar

-03

May

-03

Jul-0

3Se

p-03

Nov

-03

Jan-

04M

ar-0

4M

ay-0

4Ju

l-04

Sep-

04N

ov-0

4Ja

n-05

Mar

-05

May

-05

Jul-0

5Se

p-05

Nov

-05 0

200

400

600

800

1000

1200

1400

1600

US 3 month interest rate Spread Embi+ Latam (right axis)

1994 2004

Page 20

Uncertainty during Electoral Periods Embi spread Latin America, bpsSource: JP Morgan and BBVA Research

Presidential elections are losing their negative impact on risk premium they used to have in the past

Section III

Second test: the “Election cycle”

Sovereign spreads in Latin America (EMBI+, bps)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

sep-

92

jun-

93

mar

-94

dic-

94

sep-

95

jun-

96

mar

-97

dic-

97

sep-

98

jun-

99

mar

-00

dic-

00

sep-

01

jun-

02

mar

-03

dic-

03

sep-

04

jun-

05

mar

-06

dic-

06

sep-

07

jun-

08

mar

-09

dic-

09

sep-

10

Lehman Brothers Crisis

Mexico andBrasil's elections

Brasil'selections

Currentelections

Page 21

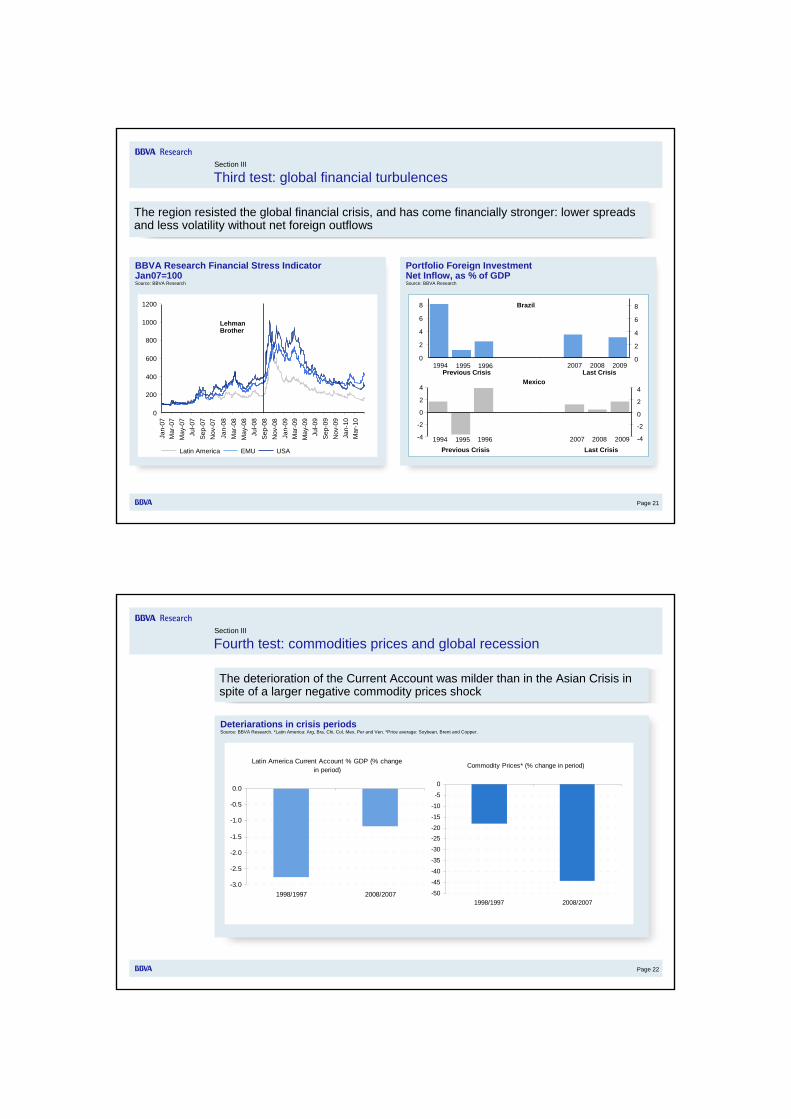

BBVA Research Financial Stress IndicatorJan07=100Source: BBVA Research

Portfolio Foreign InvestmentNet Inflow, as % of GDPSource: BBVA Research

The region resisted the global financial crisis, and has come financially stronger: lower spreads and less volatility without net foreign outflows

Section III

Third test: global financial turbulences

0

200

400

600

800

1000

1200

Jan-

07M

ar-0

7M

ay-0

7Ju

l-07

Sep-

07N

ov-0

7Ja

n-08

Mar

-08

May

-08

Jul-0

8Se

p-08

Nov

-08

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep-

09N

ov-0

9Ja

n-10

Mar

-10

Latin America EMU USA

LehmanBrother

Mexico

-4

-2

0

2

4

1994 1995 1996 2007 2008 2009 -4

-2

0

2

4

Previous Crisis Last Crisis

Brazil

0

2

4

6

8

1994 1995 1996 2007 2008 20090

2

4

6

8

Previous Crisis Last Crisis

Page 22

Deteriarations in crisis periods Source: BBVA Research. *Latin America: Arg, Bra, Chi, Col, Mex, Per and Ven. *Price average: Soybean, Brent and Copper.

Section III

Fourth test: commodities prices and global recession

The deterioration of the Current Account was milder than in the Asian Crisis in spite of a larger negative commodity prices shock

Latin America Current Account % GDP (% change in period)

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

1998/1997 2008/2007

Commodity Prices* (% change in period)

-50

-45

-40

-35

-30

-25-20

-15

-10

-5

0

1998/1997 2008/2007

Page 23

Interest Rate changes during crises (2002 compared to 2009)Source: BBVA Research

LatAm, Fiscal Stimulus as % of the GDPSource: BBVA Research

In this cycle fiscal and monetary policies were expansionary, marking a major break with previous cycles when financial constraints did not allowed them

Section III

New resilience allows countercyclical policies

-800

-600

-400

-200

0

200

400

600

800

Brazil Chile Colombia Mexico Peru

May02-Apr03 Jan09-current

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Brazil Chile Colombia Mexico Peru

Temporary Permanent

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Page 24

Index

Latin America

shines: Is it for real this

time?Latibex

Section IGlobal Outlook

Section II Latin America breaks with the past

Section III Latin America passes the “stress test”

Section IV

A bright future, if the right road is takenSection VLatin America: Investment possibility

Page 25

Emerging Asia: share in world imports (%)Source: BBVA Research

Latin America Exports’s to Asia (US$ M)Source: BBVA Research.

A more open region, both to trade and investment, is benefiting from Asian dynamism

Section IV

A bright future, if the right road is taken

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

0

5

10

15

20

25

30

1980 2009Agricultural products Fuels and mining products Manufactures

Page 26

Asian imports from Latin America (% over total Asian imports)Source: MF and BBVA Research

Concentration of the main product's exports to Asia from Latin America (% over total exports in each country). Source: BBVA Research.

The region has increased significantly its trade integration with Emerging Asia during the last decade, mainly at the expense of traditional trade partners (U.S.).

Section IV

A bright future, if the right road is taken

Initially Latam’s exports to Asia have been biased towards commodities and are benefiting from high prices

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2002 2003 2004 2005 2006 2007 2008 2009Brazil Chile Rest

0

10

20

30

40

50

60

70

Arg

entin

a

Bra

zil

Chi

le

Col

ombi

a

Mex

ico

Per

u

Ven

ezue

la

Minerals

Minerals

Agricultura

Copper

Crude Petroleum

Crude Petroleum

Crude Petroleum

Page 27

Rising incomes, urbanization and fast industrialization in China put a lot of pressure on all kind of commodity markets. India is just at the beginning of a similar process

Section IV

A bright future, if the right road is taken

Commodity prices have been resilient to the financial crisis. A new cycle of high prices seem to be starting, fueled by fast Asian development. There is a similarity with the post WWII reconstruction in Europe and Japan

Long-term trends in commodity prices (US cents 2009/pound)Source: IADB (2010) and BBVA Research

Agricultural Metals Brent

0

50

100

150

200

250

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

Agricultural Average 1957-2009Average 1973-2009

0

50

100

150

200

250

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

Metals Average 1957-2009Average 1973-2009

0

50

100

150

200

250

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

Brent Average 1957-2009

Average 1973-2009

Page 28

Strong growth, (relative) high yields and (relative) low risk is prompting capital inflows in the region

Emerging Markets Net Equity Inflows (Yearly Flows as % of Total Regional Assets)Source: EPFR and BBVA Research. *EMEA: Emerging Europe, Middle East and Africa

Section IV

A bright future, if the right road is taken

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

Latin America Emerging Asia EMEA*

2002 2009 1H2010 3Q2010

Page 29

Real Commodities Price (Respect US CPI, base 2005=100)Source: IMF and BBVA Research.

Foreign Direct Investment to the region (US$ bn)Source: BBVA Research. *Forecast BBVA Research.

Section IV

A bright future, if the right road is taken

Some new policy dilemmas: Stronger fundamentals means more appreciated currencies – in real terms – over the long – run

0

50

100

150

200

250

Soybean Brent CopperAverage 2000-2006 Average 2007-2012

0

10

20

30

40

50

60

70

80

90

100

Average 2000-2006 Average 2007-2012*

Page 30

Monetary Policy Rates (%)Source: BBVA Research

0

2

4

6

8

10

12

Brazil Mexico Colombia Peru Chile

Monetary Policy Reference Rate Monetary Policy Neutral Rate

GDP and Domestic Demand Forecast(% y/y, average 2010-2011)Source: BBVA Research

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

3.0 4.0 5.0 6.0 7.0 8.0 9.0 10.0GDP Forecast (% y/y, average 2010-2011)

Dom

estic

Dem

and

Fore

cast

(% y

/y,

aver

age

2010

-201

1)

Mexico

Chile Peru

Brazil

Colombia

Section IV

A bright future, if the right road is taken

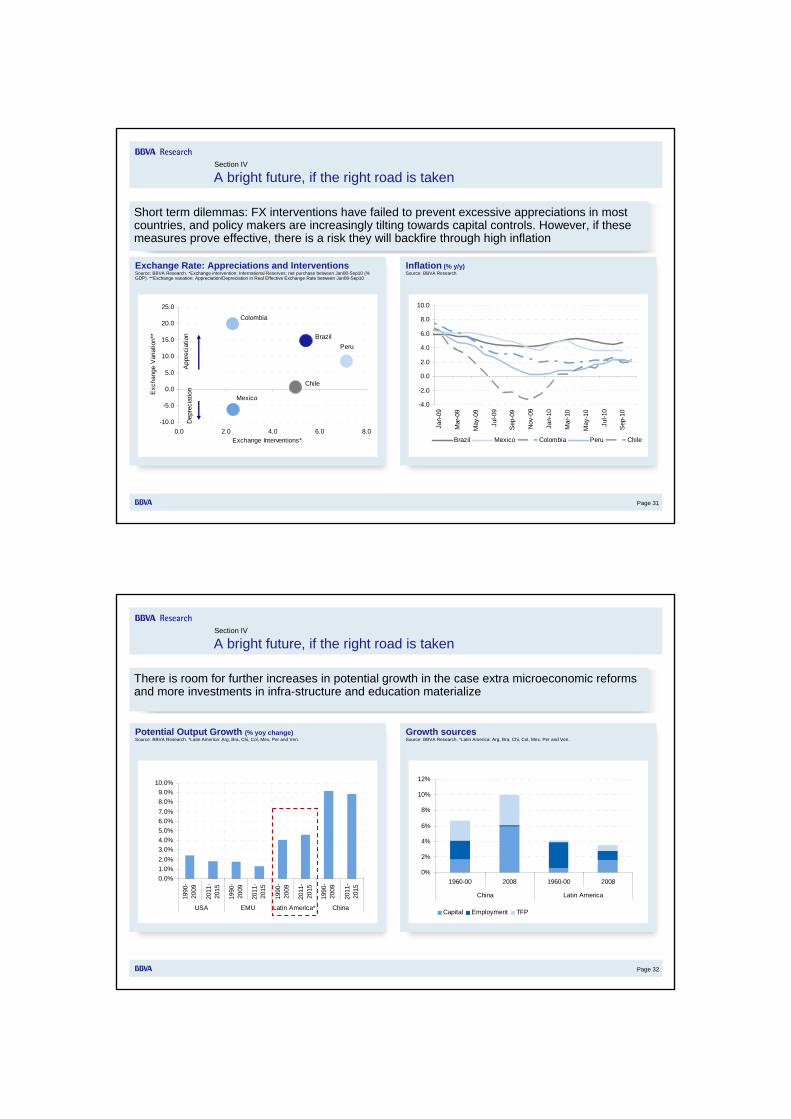

Short term dilemmas: Domestic demand growth is outperforming GDP growth in almost all countries (Mexico is the exception) with significant risks of overheating, while policy interest rates are well below neutral levels in most countries

Neutral Interest rates

Domestic Demand grow faster than GDP in 10-11

Page 31

Exchange Rate: Appreciations and InterventionsSource: BBVA Research. *Exchange intervention: International Reserves: net purchase between Jan08-Sep10 (% GDP). **Exchange variation: Appreciation/Depreciation in Real Effective Exchange Rate between Jan08-Sep10

Inflation (% y/y)Source: BBVA Research

Section IV

A bright future, if the right road is taken

Short term dilemmas: FX interventions have failed to prevent excessive appreciations in most countries, and policy makers are increasingly tilting towards capital controls. However, if these measures prove effective, there is a risk they will backfire through high inflation

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep

-10

Brazil Mexico Colombia Peru Chile

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

0.0 2.0 4.0 6.0 8.0Exchange Interventions*

Exc

hang

e V

aria

tion*

*

Mexico

Chile

PeruBrazil

Colombia

App

reci

atio

nD

epre

ciat

ion

Page 32

Potential Output Growth (% yoy change)Source: BBVA Research. *Latin America: Arg, Bra, Chi, Col, Mex, Per and Ven.

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

10.0%

1990

-20

09

2011

-20

15

1990

-20

09

2011

-20

15

1990

-20

09

2011

-20

15

1990

-20

09

2011

-20

15

USA EMU Latin America* China

Growth sources Source: BBVA Research. *Latin America: Arg, Bra, Chi, Col, Mex, Per and Ven.

Section IV

A bright future, if the right road is taken

There is room for further increases in potential growth in the case extra microeconomic reforms and more investments in infra-structure and education materialize

0%

2%

4%

6%

8%

10%

12%

1960-00 2008 1960-00 2008

China Latin America

Capital Employment TFP

Page 33

Section IV

A bright future, if the right road is taken

2003-2008* 2009 2010 2011-2012*Argentina 8.2 -2.1 8.0 4.8Brazil 4.2 -0.2 7.5 4.4Chile 4.7 -1.5 5.4 5.5Colombia 5.0 0.8 4.8 5.5Mexico 3.1 -6.6 4.5 3.5Peru 7.0 0.9 8.5 6.3Venezuela 7.3 -3.3 -2.3 1.5LATAM 4.7 -2.4 5.8 4.2

GDP (% y/y)2003-2008* 2009 2010 2011-2012*

Argentina 9.5 6.3 10.5 12.0Brazil 7.0 4.9 4.8 4.7Chile 3.9 0.4 1.5 3.0Colombia 5.8 4.2 2.2 3.3Mexico 4.3 5.3 4.5 3.8Peru 2.9 3.0 1.7 2.6Venezuela 22.1 28.6 30.0 26.8LATAM 7.1 6.4 6.5 6.4

Inflation CPI (% y/y, average)

2003-2008* 2009 2010 2011-2012*Argentina 3.3 3.5 1.2 -0.3Brazil 0.6 -1.6 -2.4 -3.0Chile 1.7 2.5 -0.4 -1.7Colombia -1.8 -2.1 -2.7 -3.0Mexico -0.8 -0.6 -1.2 -2.1Peru 0.1 0.1 -1.3 -2.5Venezuela 13.4 2.4 9.9 11.8LATAM 1.2 -0.3 -0.7 -1.4

Current Account (% GDP)

Latin America Forecast

Source: BBVA Research

Source: BBVA Research

Source: BBVA Research

Source: BBVA Research

2003-2008* 2009 2010 2011-2012*Argentina 1.5 -0.6 0.3 -0.4Brazil -3.2 -3.3 -2.6 -2.2Chile 4.6 -4.6 0.5 -0.1Colombia -3.5 -4.1 -4.2 -3.6Mexico -1.3 -2.7 -2.3 -1.8Peru 0.8 -1.9 -1.4 -0.6Venezuela -0.5 -5.1 -3.0 -0.7LATAM -1.5 -3.0 -2.2 -1.7

Fiscal Balance (% GDP)

Page 34

Index

Latin America

shines: Is it for real this

time?Latibex

Section IGlobal Outlook

Section II Latin America breaks with the past

Section III Latin America passes the “stress test”

Section IV A bright future, if the right road is taken

Section V

Latin America: Investment possibility

Page 35

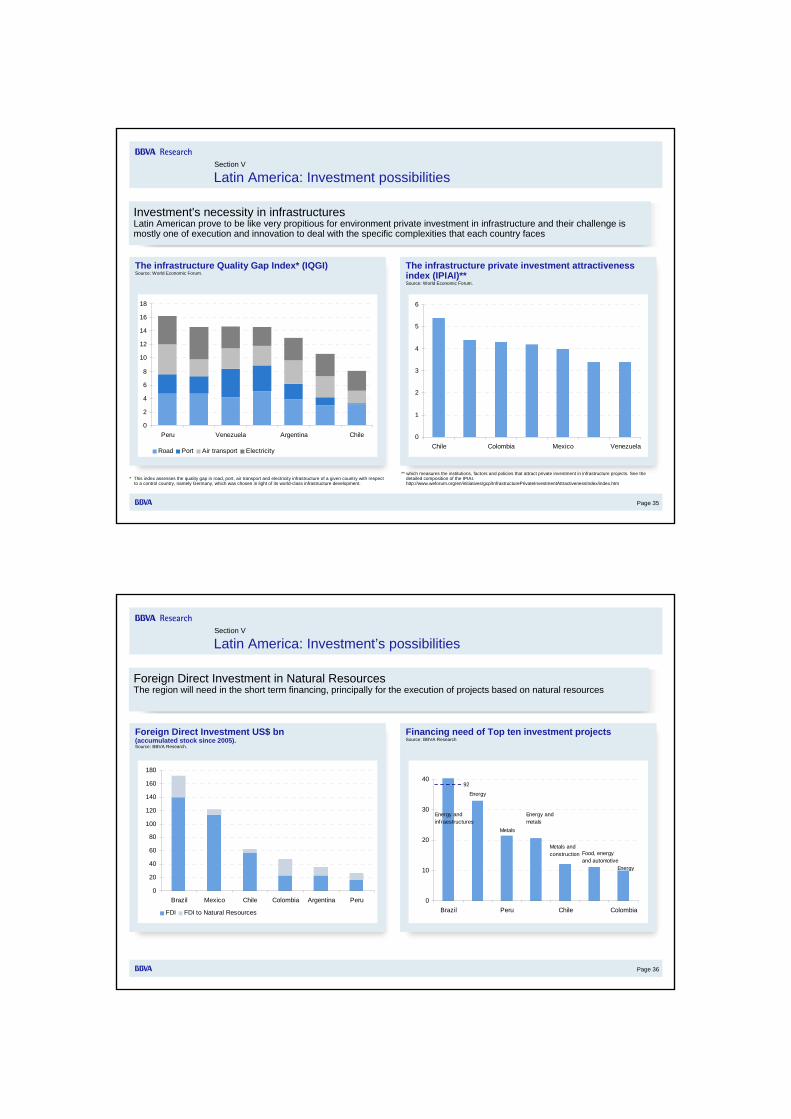

The infrastructure Quality Gap Index* (IQGI)Source: World Economic Forum.

The infrastructure private investment attractiveness index (IPIAI)**Source: World Economic Forum.

Section V

Latin America: Investment possibilities

Investment's necessity in infrastructuresLatin American prove to be like very propitious for environment private investment in infrastructure and their challenge is mostly one of execution and innovation to deal with the specific complexities that each country faces

* This index assesses the quality gap in road, port, air transport and electricity infrastructure of a given country with respect to a control country, namely Germany, which was chosen in light of its world-class infrastructure development.

** which measures the institutions, factors and policies that attract private investment in infrastructure projects. See the detailed composition of the IPIAI. http://www.weforum.org/en/initiatives/gcp/InfrastructurePrivateInvestmentAttractivenessIndex/index.htm

0

2

4

6

8

10

12

14

16

18

Peru Venezuela Argentina Chile

Road Port Air transport Electricity

0

1

2

3

4

5

6

Chile Colombia Mexico Venezuela

Page 36

Foreign Direct Investment US$ bn(accumulated stock since 2005).Source: BBVA Research.

Financing need of Top ten investment projectsSource: BBVA Research

Section V

Latin America: Investment’s possibilities

Foreign Direct Investment in Natural ResourcesThe region will need in the short term financing, principally for the execution of projects based on natural resources

0

20

40

60

80

100

120

140

160

180

Brazil Mexico Chile Colombia Argentina Peru

FDI FDI to Natural Resources

0

10

20

30

40

Brazil Peru Chile Colombia

92

Energy and infraestructures

Energy

Metals

Metals and construction

Energy and metals

Energy

Food, energy and automotive

Page 37

Section V

Latin America: Investment’s possibilities

Diversity in the region (GDP and CPI forecast)Source: BBVA Research. *Price Stability: CPI 2010-2012 (spread % y/y average latam vs. average country). **Economic Growth: GDP 2010-2012 (spread % y/y average country vs. average latam) Bubble size: Total GDP based on purchasing-power-parity (PPP).

• The “two giants” (BRA, MEX)

• Medium Size Emerging South America: medium size countries combine good performance both in inflation and growth (CHL, COL, PER)

• The “heterodox”countries: most countries have achieved low inflation, but it remains a problem in ARG and VEN

But Latin America is not one entity: there is diversity in the region

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

-6.0 -5.0 -4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0Economic Growth**

Pric

e st

abili

ty*

CHL PERMEX

BRA

ARG

VEN

COL PAN

URU PAR

Maj

or p

rice'

s st

abilit

y

Major economic growth's stability

Page 38Page 38

Section V

Argentina

• The economy will grow strongly in 2010, in spite of a slowdown in 2H. Higher political uncertainty and lower growth are expected in 2011, which, together with less expansionary demand policies in 2012-13 will lead to the output gap closing towards 2014

• Positive growth surprises in 1H10: the recovery in confidence, low interest rates and exchange rate stability are boosting consumption. Better than expected investment performance.

• When faced with supply constraints, expansionary fiscal and monetary policies are increasing inflationary pressures. A credible anti-inflation plan is required to put a cap on 2 digit price increases.

• In spite of rising imports and real exchange rate appreciation, the current account is expected to remain in surplus until 2012

• Improving fiscal solvency, although doubts about 2011 financing and the possibility of tapping credit markets remain

• The banking system remains solid, but size is an issue

An economy at full speed

Page 39

GDP – II Quarter 2010 Seasonally Adjusted Source: BBVA Research based on Indec.

Página 39

Section V

Argentina

The economy will grow vigorously in 2010 (8 %) led by domestic demandPositive growth surprises in 1H10 have led to continuous upward revisions in GDP forecasts

Some favorable shocks in 2010:

• Record soy harvest due to end of drought

• Strong demand for industrial exports stemming from above average growth in the region, particularly Brazil which is our main trading partner

• Higher than expected agricultural commodity prices.

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

GD

P

Impo

rts

Priv

ate

Com

sum

ptio

n

Pub

licC

omsu

mpt

ion

Inve

stm

ent

Exp

orts

Forecast Actual

Page 40

Inflation (% y/y) Source: BBVA Research

Section V

Argentina

Página 40

Inflation is the main problem, but is not expected to get out of controlInflation expectations are not anchored and even during the 2009 recession, CPI increased by 17% yoyExpansionary fiscal and monetary policies face growing supply constraints, increasing inflationary pressures.The FX rate continues to act as a nominal anchor

Inflation is end 2010 at 25%, edging up in 2011:

• Impact of wage agreements signed in 2Q10 granting increases of 30-35% y/y

• Fiscal policies: increases in pensions, childhood subsidies and Income Tax deductions

• Monetary policy: external surplus plus monetization of Central Bank 2009 quasi fiscal results

0%

5%

10%

15%

20%

25%

30%

35%

Dec

-08

Feb-

09

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb-

10

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

BBVA ResearchINDECDi Tella University Expectation Survey

Page 41

Term of TradeSource: BBVA Research based on Indec.

Trade BalanceSource: BBVA Research.

Section V

Argentina

The external sector remains strong New set of international commodity prices maintains terms of trade above historical averages

The trade surplus will fall to USD 13 billion in 2010 due to rising imports (+42% e y/y), but the current account will remain in surplus until 2012

Página 41

7585

95105

115125

135145

155165

175

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

e

2011

e

2012

e

Base

199

3 =

100

Export Price Index Import Price Index Term of Trade Index

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2008

2009

2010

e

2011

e

2012

e

mill

ions

u$d

Exports Imports Trade Balance

Page 42

Section V

Argentina

Página 42

Principal investment projects Financing needs (US$ M)

Cóndor Cliff Hidroeléctrica 4000

Yacimiento Pascua Lama (Oro y plata) 3000

Agua Rica (cobre y oro) 2300

Gasoducto del Noreste Argentino 1000

Financing Needs (US$ M) 10300

Financing Needs: Argentina

Source: BBVA Research.

Page 43

Inflation and interest rates (average %)Source: BBVA Research.

GDP and domestic demand growth (%)Source: BBVA Research

Section V

Brazil

Robust domestic demandGDP to grow more than 7% in 2010, especially supported by domestic demand, and to near potential pace in 2011-12 following the reversal of monetary and fiscal policies and in line with global slowdown

Inflation under controlInterest rates to remain at current levels (10.75%) in 2011. FX concerns could prevent authorities to adopt a more tight monetary policy but inflation should remain under control due to activity moderation

-2

0

2

4

6

8

10

12

2008 2009 2010 2011 2012GDP Domestic Demand

5.704.90 4.85 4.54 4.92

12.00

10.10 10.0010.75

10.25

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012

Inflation SELIC

Page 44

Fiscal and Current account deficitsSource: BBVA Research.

Exchange rate: BRL / USD Source: BBVA Research

Section V

Brazil

Strong currencyGrowth and interest rate differentials will continue to pressure the real which however is expected to depreciate slightly in nominal terms due to inflation differential and current account pressures

Current account deterioration Robust growth is expected to support a reduction of fiscal deficits and also a continuous deterioration of the current account

1.60

1.65

1.70

1.75

1.80

1.85

1.90

1.95

2.00

2.05

2008 2009 2010 2011 2012

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2008 2009 2010 2011 2012

Fiscal Deficit Current Account Deficit

Page 45

Exports and imports (USD millions)Source: BBVA Research.

Exports and Imports (USD millions)Source: BBVA Research

Section V

Brazil

Trade recoveryExports and imports continue to recover and pre-crisis levels are expected to be soon reached. Exports are being supported by commodity prices and Asian growth and imports by domestic dynamism

Narrowing trade surplusTrade surplus is expected to drop from USD 25 bi in 2009 to USD 16 bi in 2010, USD 7 in 2011 and slightly more than zero in 2012 following the dynamism of the domestic demand and a relatively appreciated real

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

23,000

Jan-

08

Apr-

08

Jul-0

8

Oct

-08

Jan-

09

Apr-

09

Jul-0

9

Oct

-09

Jan-

10

Apr-

10

Jul-1

0

Exports Imports

0

50,000

100,000

150,000

200,000

250,000

300,000

2008 2009 2010 2011 2012

Exports Imports

Page 46

Section V

Brazil

Página 46

Principal investment projects Financing needs (US$ M)

Tren Alta Velocidad Rio - Sao Paulo 20000

Refinaria Abreu Lima 13529

Refinaria COMPERJ 11294

Generación Energia Eletrica - Usina Hidrelectrica Belo Monte 11176

Generación Energia Eletrica - Usina Hidrelectrica Santo Antonio 8235

Ferrovia Norte-Sur 7647

Generación Energia Eletrica - Jirau 5471

Usina Termonuclear Angra III 4882

Plataforma de Petroleo - Campo Marlim 4882

Pre Sal - Piloto de Produccion Tupi 4706

Financing Needs (US$ M) 91822

Financing Needs: Brazil

Source: BBVA Research.

Page 47

GDP and domestic demand growth (%)Source: BBVA Research

Inflation and interest rates (average %)Source: BBVA Research.

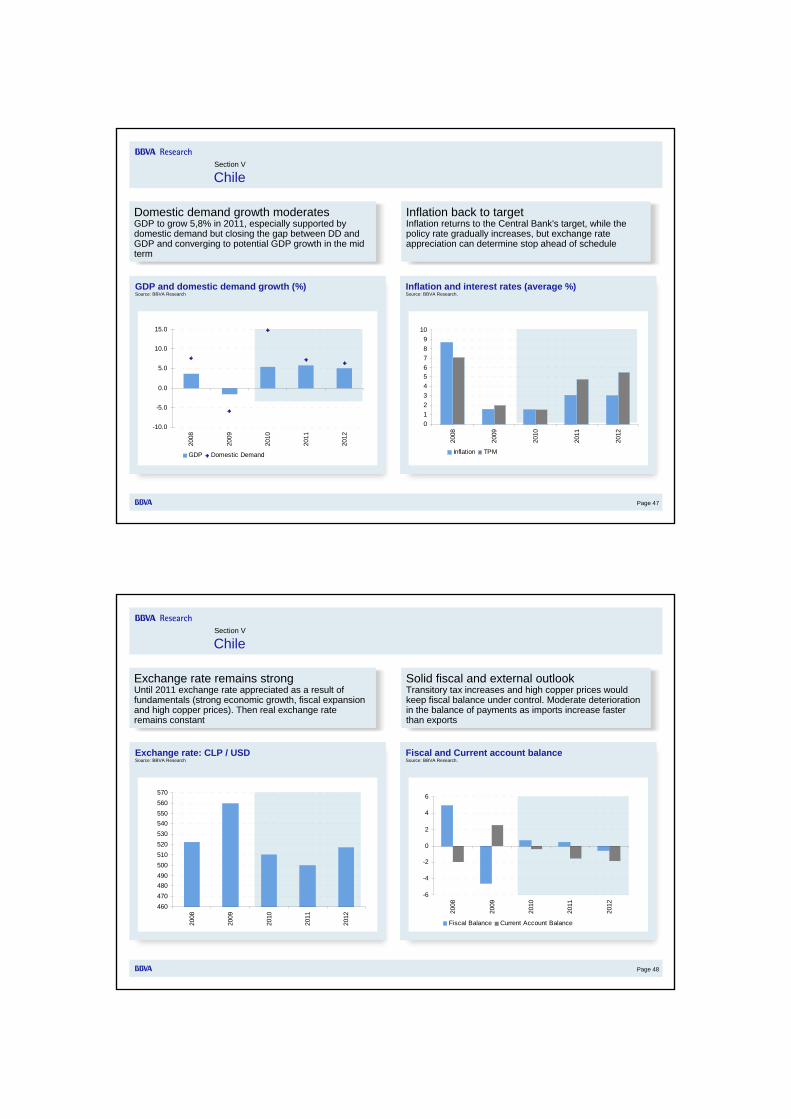

Section V

Chile

Domestic demand growth moderatesGDP to grow 5,8% in 2011, especially supported by domestic demand but closing the gap between DD and GDP and converging to potential GDP growth in the mid term

Inflation back to targetInflation returns to the Central Bank's target, while the policy rate gradually increases, but exchange rate appreciation can determine stop ahead of schedule

-10.0

-5.0

0.0

5.0

10.0

15.0

2008

2009

2010

2011

2012

GDP Domestic Demand

0123456789

10

2008

2009

2010

2011

2012

Inflation TPM

Page 48

Exchange rate: CLP / USD Source: BBVA Research

Fiscal and Current account balanceSource: BBVA Research.

Section V

Chile

Exchange rate remains strongUntil 2011 exchange rate appreciated as a result of fundamentals (strong economic growth, fiscal expansion and high copper prices). Then real exchange rate remains constant

Solid fiscal and external outlook Transitory tax increases and high copper prices would keep fiscal balance under control. Moderate deterioration in the balance of payments as imports increase faster than exports

460470480490500510520530540550560570

2008

2009

2010

2011

2012

-6

-4

-2

0

2

4

6

2008

2009

2010

2011

2012

Fiscal Balance Current Account Balance

Page 49

Section V

Chile

Página 49

Principal investment projects Financing needs (US$ M)

Cerro Casale, Minería-cobre 4200

El Morro, Minería-cobre 2500

Caserones, Minería-cobre 1997

Cochrane, Central terrmoeléctrica a carbón 1100

Santa María 2, Central termoeléctrica a carbón 650

Plan de renovación de flota LAN, Transporte aéreo 520

Altos de Lampa, proyecto inmobiliario 320

Modernización Planta Laja, Celulosa 295

Tercera Planta Gran Santiago, Procesamiento de aguas 250

Central Hidroeléctrica Ñuble 240

Financing Needs (US$ M) 12072

Financing Needs:Chile

Source: BBVA Research.

Page 50

GDP growth (%)Source: BBVA Research

Inflation and interest rates (average %)Source: BBVA Research.

Section V

Colombia

GDP growth near potentialEconomy expands at a sustainable pace, based on strong consumption dynamics and a slower recovery of investment. Exports and industrial production affected by trade restrictions with Venezuela.

Inflation remains well anchoredBenign behavior of inflation and exchange rate concerns will post-pone normalization of the monetary policy stance until 1H11. High liquidity sets a limit to stronger exchange rate intervention

0

2

4

6

8

2006 2007 2008 2009 2010 20110

2

4

6

8

0

2

4

6

8

10

2008 2009 2010 20110

2

4

6

8

10

Inflation Interest rate

Page 51

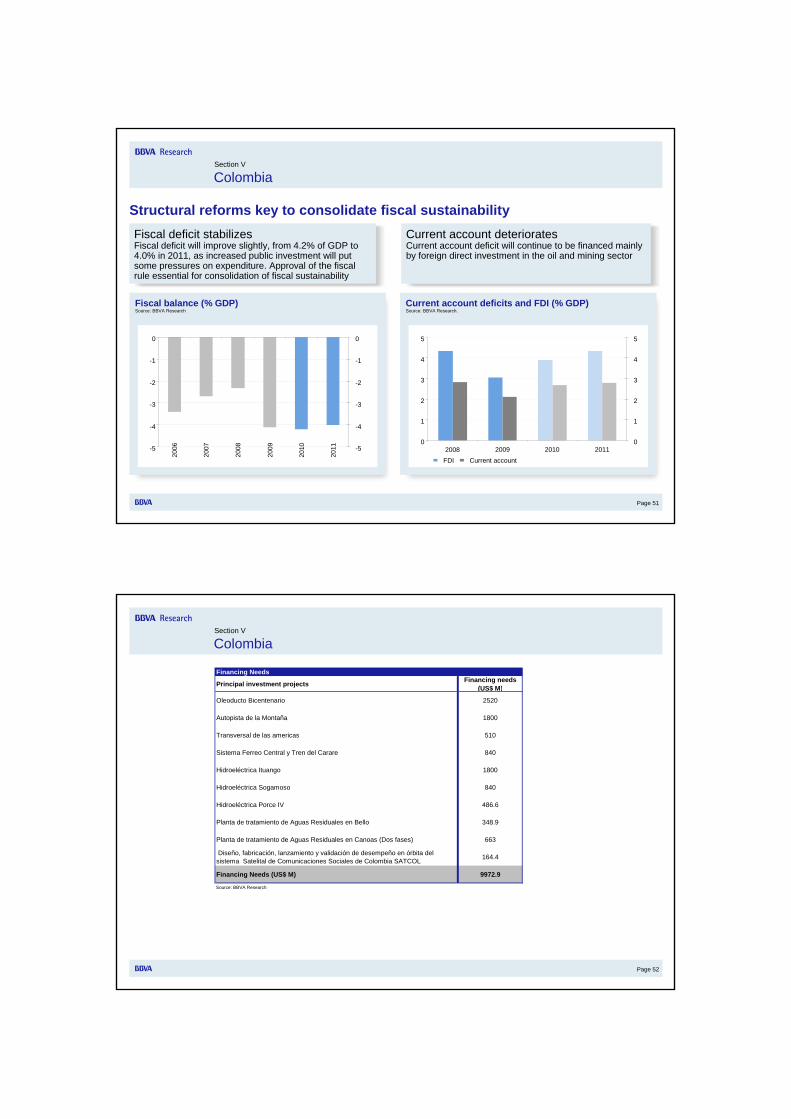

Fiscal balance (% GDP)Source: BBVA Research

Current account deficits and FDI (% GDP)Source: BBVA Research.

Section V

Colombia

Fiscal deficit stabilizesFiscal deficit will improve slightly, from 4.2% of GDP to 4.0% in 2011, as increased public investment will put some pressures on expenditure. Approval of the fiscal rule essential for consolidation of fiscal sustainability

Current account deterioratesCurrent account deficit will continue to be financed mainly by foreign direct investment in the oil and mining sector

Structural reforms key to consolidate fiscal sustainability

-5

-4

-3

-2

-1

0

2006

2007

2008

2009

2010

2011 -5

-4

-3

-2

-1

0

0

1

2

3

4

5

2008 2009 2010 20110

1

2

3

4

5

FDI Current account

Page 52

Section V

Colombia

Principal investment projects Financing needs (US$ M)

Oleoducto Bicentenario 2520

Autopista de la Montaña 1800

Transversal de las americas 510

Sistema Ferreo Central y Tren del Carare 840

Hidroeléctrica Ituango 1800

Hidroeléctrica Sogamoso 840

Hidroeléctrica Porce IV 486.6

Planta de tratamiento de Aguas Residuales en Bello 348.9

Planta de tratamiento de Aguas Residuales en Canoas (Dos fases) 663

Diseño, fabricación, lanzamiento y validación de desempeño en órbita del sistema Satelital de Comunicaciones Sociales de Colombia SATCOL 164.4

Financing Needs (US$ M) 9972.9

Source: BBVA Research

Financing Needs

Page 53

Mexico, GDP (2003=100)Source: BBVA Research

Bank System External Position (Foreign currency, % GDP)Source: BBVA Research.

Section V

Mexico

Page 53

Large impact of external shock As soon as global demand came back, Mexico resumed its recovery path. It is foreseeable a GDP higher than previous peak in the first half of 2011

But a strong financial sectorA free exchange rate and a revamped banking system allowed a depreciation to act as a shock absorber without pass through on inflation or credit channel interruption

95

100

105

110

115

120

Sep

-02

Sep

-03

Sep

-04

Sep

-05

Sep

-06

Sep

-07

Sep

-08

Sep

-09

Sep

-10

95

100

105

110

115

120

0.0

0.5

1.0

1.5

2.0

2.5

2006

2007

2008

2009

Jun-

10

0.0

0.5

1.0

1.5

2.0

2.5

Assets Liabilities

Page 54

Mexico, Corporate Credit in USD (%)Source: BBVA Research

Inflation and interest rates (average and eop)Source: BBVA Research.

Section V

Mexico

Page 54

Financial resilienceCost and access to funding have improved in Mexico during 2010. In 2011, global liquidity, (moderated) growth and sound financial situation of corporate sector should give support to low and stable capital cost

Inflation and rates well anchoredDisinflationary process during the forecast horizon and inflation expectative anchorage will produce an ever longer monetary policy pause

3.0

6.0

9.0

12.0

15.0

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Corporate Issuance, México, mill USD, right axisRate, Mexico

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2007 2008 2009 2010 (p) 2011 (p)0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Inflation Fondeo Rate

Page 55

México: manufactures exports to USA(Change in sectoral shares & competitive advantages 1998-2000 vs 2007-2009)Source: BBVA Research

Mexico: Market Share (as % of total manufacture exports)Source: BBVA Research.

Section V

Mexico

Page 55

Mexican competitiveness …Mexican comparative advantage is not just a matter of price, instead there is a variety of differences in productivity among industries…

… has contributed to resilience of the Mexican market share in the US

0

5

10

15

20

25

2007 2008 2009 Jun-100

5

10

15

20

25

China Canada Mexico

-50

-40

-30

-20

-10

0

10

20

30

40

50

-3 -2 -1 0 1 2 3 4Change in Comparative Advantage Index

Cha

nge

in s

ecto

rals

hare

TransportationequipementGold

Tractors

Autoparts

Processing data machines

Telephones

Electric conductors

TV receivers

Page 56

Comparative Advantage Index:Transport EquipmentSource: BBVA Research

Comparative Advantage Index:Electricity AppliancesSource: BBVA Research

Comparative Advantage Index:TV ReceiversSource: BBVA Research

Section V

Mexico

Page 56

Mexican competitivenessVery diverse performance considering sector breakdown persist: those products in which the advantage revealed grows are those that have increased their penetration in the US market

* Basket includes the following countries: China, Taiwan, Tailandia, Corea del Sur, Malasia, Hong Kong, Singapur, Turquía, Filipinas, Indonesia, Hungría, Polonia and Portugal.

0

1

2

3

4

5

6

7

8

9

10

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

3Q08

0

1

2

3

4

5

6

7

8

9

10

Basket Brazil Mexico China

0

1

2

3

4

5

6

7

8

9

10

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

3Q08

0

1

2

3

4

5

6

7

8

9

10

Basket Brazil Mexico China

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

3Q08

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Basket Brazil Mexico China

Page 57

Section V

Mexico

Principal investment projects Financing needs (US$ M)

Coca Cola Alimentos 5000

IDESA (Mex) Braskem (Bra) Energía 2500

NIHD Telecomunicaciones 970

Volkswagen Automotriz 550

General Motors Automotríz 500

Mitsui Energía 480

Nestle Alimentos 400

Telefónica Telecomunicaciones 300

Bombardier Aeronáutica 250

Pepsico Alimentos 245

Financing Needs (US$ M) 11195

Source: BBVA Research

Financing Needs

Page 58

Peru: GDP (yoy % change)Source: Central Bank of Peru and BBVA Research Peru

Peru: private consumption and investment(yoy % change)Source: Central Bank of Peru

Section V

Peru

Strong rebound in 2010, driven by private demandThe economy has grown at a pace close to 8,5% yoy up to 3Q10This is supported by high business and consumers confidence, as well as by improving jobs creation conditions

Strong and sustainable

economic growth

-30

-20

-10

0

10

20

30

40

08Q

1

08Q

2

08Q

3

08Q

4

09Q

1

09Q

2

09Q

3

09Q

4

10Q

1

10Q

2

0

2

4

6

8

10

12

Investment (left) Consumption (right)

10.5

12.1

10.5

6.2

2.3

-1.2-0.2

3.0

6.4

10.18.9

-2

0

2

4

6

8

10

12

14

08Q

1

08Q

2

08Q

3

08Q

4

09Q

1

09Q

2

09Q

3

09Q

4

10Q

1

10Q

2

0Q3(

e)

Page 59

Peru: public debt(% of GDP) Source: Central Bank of Peru and BBVA Research Peru

Peru: net international reserves(% of GDP) Source: Central Bank of Peru and BBVA Research Peru

Section V

Peru

Strong growth (6%) in the medium termPublic debt resumes its downward trend. Net international reserves have reached almost 30% of GDP, an important buffer stock against eventual future external shocks. Pace of cyclical recovery and solid macro foundations anticipate an improvement in Peru’s credit rating in 2011

Healthy macro foundations

support high growth rates in

the coming years

The public sector has currently PEN 46 billion (13% of GDP) deposited in the Peruvian financial system

0

5

10

15

20

25

30

35

40

45

50

2002 2003 2004 2005 2006 2007 2008 2009 2010(f)

10

12

14

16

18

20

22

24

26

28

30

2002 2003 2004 2005 2006 2007 2008 2009 2010 (f)

Page 60

Section V

Peru

Página 60

Source: BBVA Research

Principal investment projects Financing needs (US$ M)

Las Bambas (Minería - Cobre) 4200

Quellaveco (Minería - Cobre) 3000

Minas Conga (Minería - Oro) 3000

Galeno (Minería - Cobre) 2500

Toromocho (Minería - Cobre) 2500

Antapaccay (Minería - Cobre) 1500

Rio Blanco (Minería - Cobre) 1440

Los Chancas (Minería - Cobre) 1200

Ampliación de tajo Antamina (Minería - Cobre) 1100

Ampliación minera Cerro Verde (Minería - Cobre) 1000

Financing Needs (US$ M) 21440

Financing Needs

Page 61

Section V

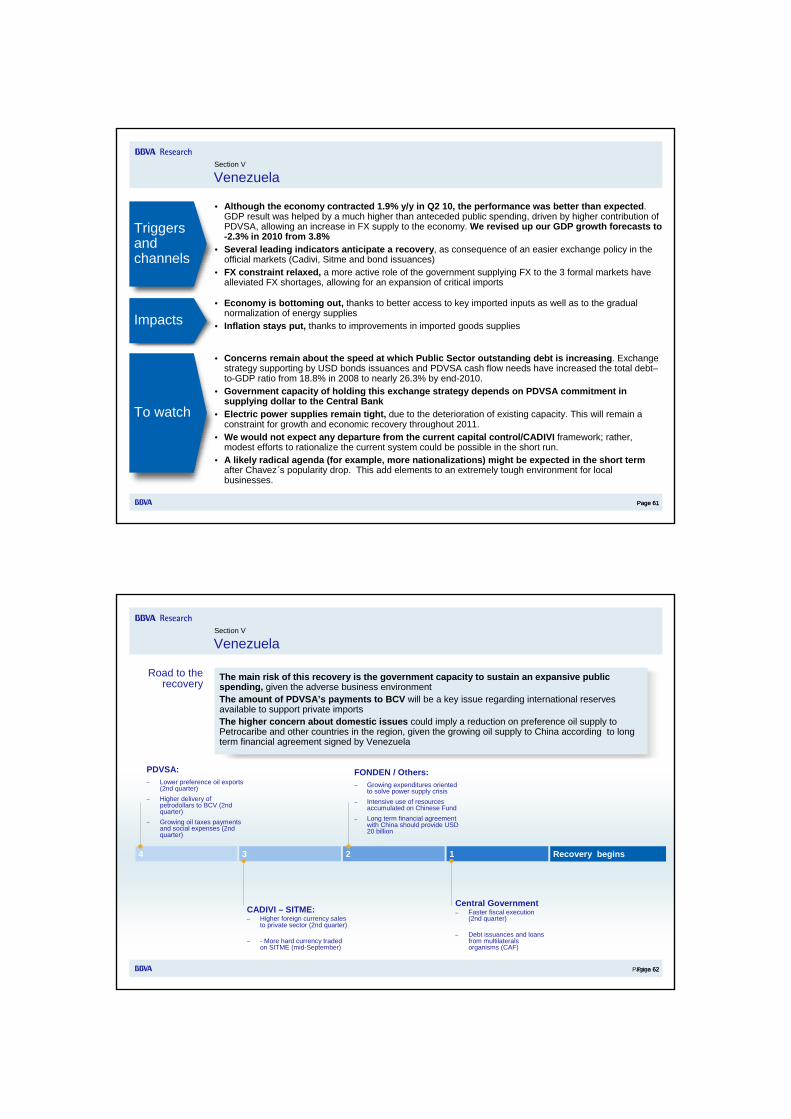

Venezuela

Page 61

• Although the economy contracted 1.9% y/y in Q2 10, the performance was better than expected. GDP result was helped by a much higher than anteceded public spending, driven by higher contribution of PDVSA, allowing an increase in FX supply to the economy. We revised up our GDP growth forecasts to -2.3% in 2010 from 3.8%

• Several leading indicators anticipate a recovery, as consequence of an easier exchange policy in the official markets (Cadivi, Sitme and bond issuances)

• FX constraint relaxed, a more active role of the government supplying FX to the 3 formal markets have alleviated FX shortages, allowing for an expansion of critical imports

Triggers and channels

Impacts

To watch

• Economy is bottoming out, thanks to better access to key imported inputs as well as to the gradual normalization of energy supplies

• Inflation stays put, thanks to improvements in imported goods supplies

• Concerns remain about the speed at which Public Sector outstanding debt is increasing. Exchange strategy supporting by USD bonds issuances and PDVSA cash flow needs have increased the total debt–to-GDP ratio from 18.8% in 2008 to nearly 26.3% by end-2010.

• Government capacity of holding this exchange strategy depends on PDVSA commitment in supplying dollar to the Central Bank

• Electric power supplies remain tight, due to the deterioration of existing capacity. This will remain a constraint for growth and economic recovery throughout 2011.

• We would not expect any departure from the current capital control/CADIVI framework; rather, modest efforts to rationalize the current system could be possible in the short run.

• A likely radical agenda (for example, more nationalizations) might be expected in the short term after Chavez´s popularity drop. This add elements to an extremely tough environment for local businesses.

Page 62

Section V

Venezuela

Página 62

4 3 2 1

PDVSA:– Lower preference oil exports

(2nd quarter) – Higher delivery of

petrodollars to BCV (2nd quarter)

– Growing oil taxes payments and social expenses (2nd quarter)

CADIVI – SITME:– Higher foreign currency sales

to private sector (2nd quarter)

– - More hard currency traded on SITME (mid-September)

FONDEN / Others:– Growing expenditures oriented

to solve power supply crisis– Intensive use of resources

accumulated on Chinese Fund– Long term financial agreement

with China should provide USD 20 billion

Central Government – Faster fiscal execution

(2nd quarter)

– Debt issuances and loans from multilaterals organisms (CAF)

Recovery begins

Road to the recovery

The main risk of this recovery is the government capacity to sustain an expansive public spending, given the adverse business environmentThe amount of PDVSA’s payments to BCV will be a key issue regarding international reserves available to support private importsThe higher concern about domestic issues could imply a reduction on preference oil supply to Petrocaribe and other countries in the region, given the growing oil supply to China according to long term financial agreement signed by Venezuela

Page 63

Section V

Venezuela

Source: BBVA Research

Principal investment projects Financing needs (US$ M)

Proyectos de recuperación secundaria Distrito Norte Oriente - Sector Petróleo y Gas 9737

Proyecto Gas Delta Caribe Oriental - Sector Petróleo y Gas 8811

Central Hidroelectrica Tocoma - Sector Eléctrico 3060

Complejo Criogénico de Occidente - Sector Petróleo y Gas 2659

Construcción Complejo Generador Termocentro - Sector Eléctrico 2187

Modernización Central Hidroeléctrica de Guri - Sector Eléctrico 2106

Construcción Planta Termoeléctrica A. J. Sucre - Sector Eléctrico 1472

Tercer puente sobre el Rio Orinoco - Sector Vialidad 1000

Modernización Planta Centro - Sector Eléctrico 978

Interconexión de transmisión de gas Centro Oriente-Occidente - Sector Petróleo y Gas 884

Financing Needs (US$ M) 32894

Financing Needs

Latin America shines: Is it for real this time?Latibex

November, 2010

José Luis Escrivá│Chief Economist BBVA Research │[email protected]