lakeshore subdivision sewerage districtapp1.lla.state.la.us/publicreports.nsf/a4765c859bb... ·...

TRANSCRIPT

303.1 1

LAKESHORE SUBDIVISIONSEWERAGE DISTRICT

Ouachita Parish Police JuryMonroe, Louisiana

Report on the Audit of theComponent Unit

Basic Financial StatementsAs of and For the Year Ended December 31,2005

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the officgof ttye parish clerk of court.

Release Date IT

Jimmie Self, CPAA Professional Accounting Corporation

2908 Cameron Street, Suite CMonroe, LA 71201

Phone (318) 323-4656 • Fax (318) 388-0724

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1Component Unit of the

Ouachita Parish Polke Jury

Basic Financial StatementsAs of and For the Year Ended

December 31,2005With Supplemental Information Schedules

TABLE OF CONTENTS

STATEMENT PAGE

Independent Auditor's Report 1 - 2

Required Supplementary Information (Part D

Management Discussion and Analysis 4-7

Basic Financial Statements

Statement of Net Assets - Proprietary Funds A 9

Statement of Revenues, Expenses, and Changes in Fund Net Assets -Proprietary Funds Type B 10

Statement of Cash Flows - Increase (Decrease) In Cash andCash Equivalents - Proprietary Fund C 11

Notes to the Financial Statements

Notes 13-20

Required Supplementary Information (Part II)

Independent Auditor's Report on Compliance and on Internal ControlOver Financial Reporting based on an Audit of Financial StatementsPerformed in Accordance With Government Auditing Standards 22 - 23

Schedule of Compensation Paid Board of Commissioners 24

Schedule of Findings and Questioned Costs 25

LAKEOSContents

JIMMIE SELF, CPAA PROFESSIONAL ACCOUNTING CORPORATION

2908 Cameron Street, Suite CMonroe, Louisiana 71201

Phone (318) 323^656 Fax (318) 388-0724

INDEPENDENT AUDITOR'S REPORT

Board of CommissionersLakeshore Subdivision Sewerage District #1Monroe, LA 71203

I have audited the accompanying basic financial statements of the business-type activitiesof Lakeshore Subdivision Sewerage District #1, a component unit of The Ouachita ParishPolice Jury, as of and for the year ended, December 31,2005, which comprise the District'sbasic financial statements as listed in the table of contents. These financial statements arethe responsibility of the District's management. My responsibility is to express an opinionon these basic financial statements based on my audit.

I conducted my audit in accordance with auditing standards generally accepted in theUnited States of America and the standards applicable to financial audits contained inGovernment Auditing Standards issued by the Comptroller General of the United Statesand the Louisiana Governmental Audit Guide. Those standards require that I plan andperform the audit to obtain reasonable assurance about whether the general purposefinancial statements are free of material misstatement. An audit includes examining, on atest basis, evidence supporting the amounts and disclosures in the financial statements. Anaudit also includes assessing the accounting principles used and significant estimates madeby management, as well as evaluating the overall general purpose financial statementpresentation. I believe that my audit provides a reasonable basis for my opinion.

In my opinion, the basic financial statements referred to above present fairly, in all materialrespects, the financial position of the Lakeshore Subdivision Sewerage District #1 as ofDecember 31, 2005, and the changes in financial position and cash flows of its proprietaryfund types for the year then ended in conformity with accounting principles generallyaccepted in the United States of America.

The Management's Discussion and Analysis is not a required part of the basic financialstatements but is supplementary information required by accounting principles generallyaccepted in the United States of America. I have applied certain limited procedures, whichconsisted principally of inquiries of management regarding the methods of measurementand presentation of the supplementary information. However, I did not audit theinformation and express no opinion on it.

In accordance with Government Auditing Standards, I have also issued my report datedJune 15,2006, on my consideration ofthe District's internal control over financialreporting and a report dated June 15, 2006, on its compliance with certain provisions of

LAKEOSIndAudRep

laws, regulations, and grants. That report is an integral part of an audit performed inaccordance with Government Auditing Standards, and should be read in conjunction withthis report in considering the results of my audit.

Jimmie Self, CPAMonroe, LouisianaJune 15,2006

LAKE05IndAudRep

REQUIRED SUPPLEMENTARY INFORMATION(PART I)

Management Discussion and Analysis

LAKESHORE SUBDIVISION SEWERAGE DISTRICT No. 1Monroe, Louisiana

MANAGEMENT'S DISCUSSION AND ANALYSIS

Our discussion and analysis of the financial performance of the Lakeshore SubdivisionSewerage District No. 1 (the District) provides an overview of the District's financialactivities for the fiscal year that ended December 31,2005. Please read it in conjunctionwith the financial statements.

The annual financial report has taken on a new form and includes new component partsin compliance with the Governmental Accounting Standards Board Statement 34 (GASB34). The District is considered a Phase 3 governmental entity with annual revenues ofless than $10 million and as such was required to comply with GASB 34 for the first timein 2004.

FINANCIAL HIGHLIGHTS

During the past year ended December 31, 2004, the District's net assets were reported tobe $975,985. The District's total operating revenues were $235,924. The District hadtotal expenses, excluding depreciation, of $320,719.

During the current year ended December 31,2005, the District's net assets were$951,684. The District's total operating revenues were $232,333. The District had totalexpenses, excluding depreciation, of $149,260.

OVERVIEW OF THE FINANCIAL STATEMENTS

This annual report consists of three parts - Management's Discussion and Analysis (thissection), the Basic Financial Statements, and Other Supplementary Information. TheBasic Financial Statements include government - wide enterprise fund financialstatements (business-type activities) about the District's overall financial status.

The financial statements also include notes that explain some of the information in thefinancial statements and provide more detailed data. The statements are followed by asection of other supplementary information that further explains and supports theinformation in the financial statements.

ENTERPRISE FUND FINANCIAL STATEMENTS (GOVERNMENT- WIDE)

The Statement of Net Assets and the Statement of Revenue, Expenses, and Changes inFund Net Assets provide information in a way that shows the change in the District'sfinancial condition resulting from the current year's activities. These statements includeall assets and liabilities using the accrual basis of accounting, which is similar to theaccounting used by most businesses. All of the current year's revenues and expenses aretaken into account regardless of when cash is received or paid.

These two statements report the District's net assets and the changes in them. Net Assets,the difference between assets (what the District owns) and liabilities (what the District

LAKE05MD&A

LAKESHORE SUBDIVISION SEWERAGE DISTRICT No. 1Monroe, Louisiana

MANAGEMENT'S DISCUSSION AND ANALYSIS

owes), is a way to measure the financial position of the District. Over time, increases ordecreases in the District's net assets are an indicator of whether the District's financialposition is improving or deteriorating.

The Statement of Cash Flows provides information on the changes in cash during theyear. This statement reports the net cash provided or used by operating activities, capitaland related financing activities, and investing activities.

FINANCIAL ANALYSIS

The information in the table below is found in the "Statements of Net Assets" located inthe section of this report entitled "Basic Financial Statements." The followingrestatement of those figures is offered to aid the reader of this report in understanding theintent and meaning of the figures contained in the Statement of Net Assets.

Net Assets. The District's Total Net Assets for the prior year ended December 31,2004were in the amount of $975,985. The District's Total Net Assets for the year endedDecember 31,2005 were in the amount of $951,684.NET ASSETS - BUSINESS TYPE ACTIVITIES 2004 2005

Current and Other Assets 637,559 621,411Capital Assets 958,293 893,926Unamortized Bond Discount 2,796 2,695

Total Assets 1,598,648 1,518,032

Accounts payable and Accrued Expenses 9,528 8,213Other Liabilities 118,135 123,135Revenue Bonds Payable 495,000 435,000

Total Liabilities 622,663 566,348

Net AssetsInvested in Capital Assets, net of Related Debt 563,864 403,926Unreserved Designated for Capital Assets 412,121 547,760

Total Net Assets 975,985 951,684

The information in the table below is found in the "Statement of Revenues, Expenses,and Changes in Fund Net Assets" located in the section of this report entitled "BasicFinancial Statements." The following restatement of these figures is offered to aid thereader of this report in understanding the meaning of those figures.

LAKE05MD&A

LAKESHORE SUBDIVISION SEWERAGE DISTRICT No. 1Monroe, Louisiana

MANAGEMENT'S DISCUSSION AND ANALYSIS

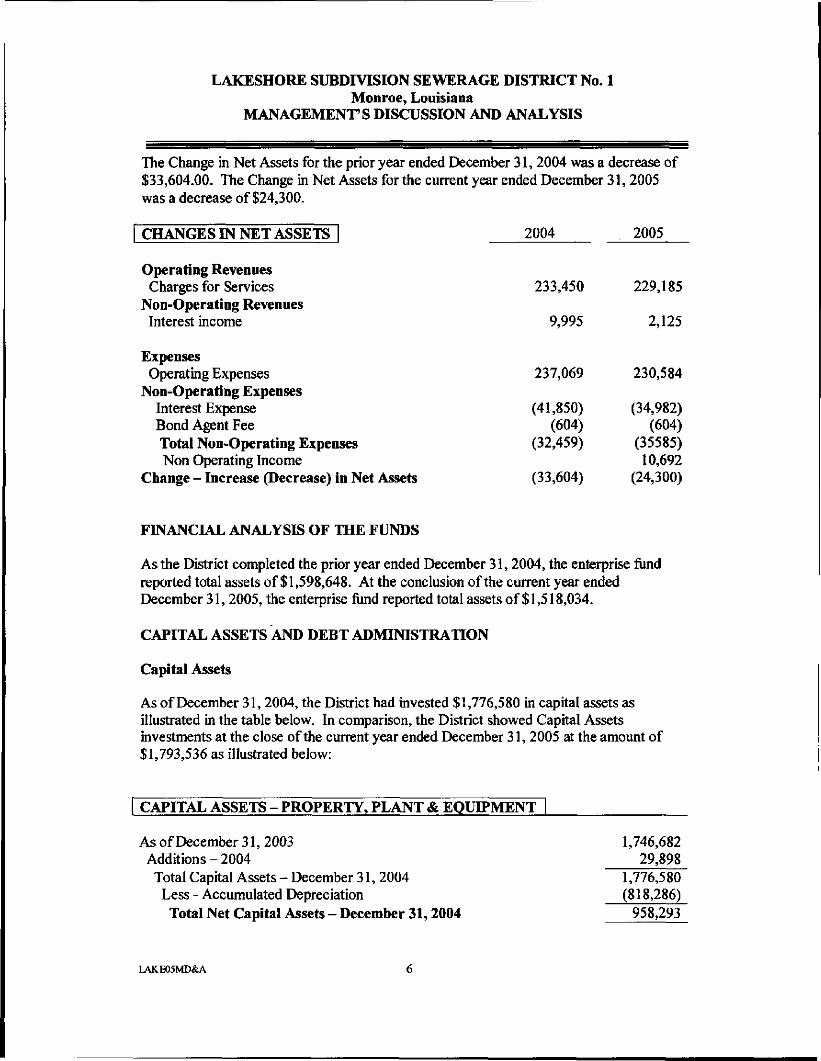

The Change in Net Assets for the prior year ended December 31, 2004 was a decrease of$33,604.00. The Change in Net Assets for the current year ended December 31,2005was a decrease of $24,300.

CHANGES IN NET ASSETS 2004 2005

Operating RevenuesCharges for Services 233,450 229,185

Non-Operating RevenuesInterest income 9,995 2,125

ExpensesOperating Expenses 237,069 230,584

Non-Operating ExpensesInterest Expense (41,850) (34,982)Bond Agent Fee (604) (604)Total Non-Operating Expenses (32,459) (35585)Non Operating Income 10,692

Change - Increase (Decrease) in Net Assets (33,604) (24,300)

FINANCIAL ANALYSIS OF THE FUNDS

As the District completed the prior year ended December 31,2004, the enterprise fundreported total assets of $1,598,648. At the conclusion of the current year endedDecember 31,2005, the enterprise fund reported total assets of $1,518,034.

CAPITAL ASSETS AND DEBT ADMINISTRATION

Capital Assets

As of December 31, 2004, the District had invested $1,776,580 in capital assets asillustrated in the table below. In comparison, the District showed Capital Assetsinvestments at the close of the current year ended December 31, 2005 at the amount of$1,793,536 as illustrated below:

CAPITAL ASSETS - PROPERTY, PLANT & EQUIPMENT |

As of December 31, 2003 1,746,682Additions-2004 29,898Total Capital Assets - December 31, 2004 1,776,580

Less - Accumulated Depreciation (818,286)Total Net Capital Assets - December 31,2004 958,293

LAKE05MD&A

LAKESHORE SUBDIVISION SEWERAGE DISTRICT No. 1Monroe, Louisiana

MANAGEMENT'S DISCUSSION AND ANALYSIS

Additions - 2005 16,956Total Capital Assets - December 31, 2005 975,249Less - Accumulated Depreciation (81,324)Total Net Capital Assets - December 31,2005 893,926

Debt

As of December 31, 2004, the District had Sewer Revenue Bonds payable in the amountof $545,000. The portion due and payable for the current year was made on April 1,2005 in the amount of $55,000. The District is required by the bond agreement tomaintain a sufficient amount in the Revenue Bond Sinking Fund to pay promptly andfully the principal and interest on the bonds as they come due and payable by transferringfrom the Sewer System Fund to the Sinking Fund monthly in advance on or before the20* day of each month 176th of the interest on bonds falling due on the next interestpayment date and 1/12* of the principal of the bonds falling due on the next principalpayment date. As of December 31,2005, the District had Sewer Revenue Bonds payablein the amount of $490,000. The next payment date shall be April 1,2006 for the amountof $55,000.

ECONOMIC FACTORS AFFECTING THE UPCOMING YEAR'S BUSINESS

Management of the District foresees no major changes in economic factors which willaffect the upcoming year's business climate. The ongoing threat of rising fuel and utilitycosts are always a concern whose effect to expenses must be factored in as they occur.Substantial changes in fuel and utility fees and other equipment and repair expenses on anaging sewer system could always bring about an adjustment in monthly sewerage servicerates.

CONTACTING THE DISTRICT'S FINANCIAL MANAGEMENT

The District is a component unit of the Ouachita Parish Police Jury and as such, isultimately under the supervision of the Police Jury. The Jury has appointed a board ofcommissioners to oversee the operations of the District. Mr. Leon Sivils serves as theSecretary-Treasurer of the board of commissioners and may be contacted by mail atLakeshore Subdivision Sewerage District, P. O. Box 7237, Monroe, LA 71211.

LAKE05MD&A

BASIC FINANCIAL STATEMENTS

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OUACHITA PARISH POLICE JURYMonroe, LouisianaSTATEMENT OF NET ASSETS - PROPIETARY FUNDSDECEMBER 31,2005

ASSETSCurrent Assets:Cash and Cash EquivalentsAccounts Receivable, NetBilled Sewerage Charges - 38660

N on cur rent Assets:Restricted AssetsInvestmentsCapital assets, Net (See Note 5)Unamortized Bond Discount

TOTAL ASSETS

LIABILITIESCurrent Liabilities:Accrued Interest PayableCurrent Portion of Bonds PayableTotal Current Liabilities

Non-current Liabilities:Due to Louisiana DOTDSewer Revenue Bonds PayableTotal Long-term Liabilities

TOTAL LIABILITIES

NET ASSETSInvested in Capital Assets Net of Related DebtRestricted net assetsUnreserved

TOTAL NET ASSETS

STATEMENT A

187,269

38,660

294,224

101,258893,926

2,6951,518,032

8,213

55,00063,213

68,135435,000503,135566348

403,926294,224253,534951,684

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS.

LAKEOSStmtFndNelAssets

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OUACHITA PARISH POLICE JURY

Monroe, Louisiana

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET ASSETS

PROPRIETARY FUNDS TYPE

For the Year Ended December 31,2005

OPERATING REVENUES:

Charges for Services

Miscellaneous

Interest

Total Operating Revenues

STATEMENT B

229,185

1,023

2,125

232,333

OPERATING EXPENSES:

Chemicals

Depreciation Expense

Electric Expense

Insurance

Lab Fees

Legal & Professional

Office Expense

Plumbing Supplies & Maintenance

Supervisory

Repairs and Maintenance

Total Operating Expenses

NON-OPERATING REVENUES (Expenses):

Interest Income

Interest Expense

Bond Agent Fee

Total Non-Operating Revenues (Expenses)

CHANGE IN NET ASSETS

NET ASSETS BEGINNING OF YEAR,

NET ASSETS END OF YEAR

1,7988132423,711

5^07

2,5214,518

3,225

160

107,295

726230,584

1,749

9436

(34^83)

(603)(26,050)

(24301)

975,985

S 951,684

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS

LAKEOSStmtRevExpChngFndNelAssetsPropFnd 10

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OUACHTTA PARISH POLICE JURYMonroe, LouisianaSTATEMENT OF CASH FLOWSINCREASE (DECREASE) IN CASH AND CASH EQUIVALENTSPROPRIETY FUNDDecember 31,2005

Cash Flows from Operating Activities:Receipts from CustomersCash Paid to SuppliersOther expensesOther incomeNet Cash provided by Operating Activities

Cash Flows from Capital and Related Financing Activities:Acquisition of Capital AssetsPrincipal paid on bondsInterest and other fees paid on bondNet cash provided (used) by capital and related financing activities

Cash flows from investing activities:Investment income

Net increase (decrease) in cash and cash equivalentsCash and Cash Equivalents at beginning of YearCash and Cash Equivalents at end of year

Reconciliation of Operating Income (Loss) to Net CashProvided (Used) by Operatng Activities:Operating Income (Loss)DepreciationIncrease (Decrease) in Accounts ReceivableIncrease (Decrease) in Accounts Payable

Non operating Revenues/EXPNet Cash provided by Operating Activities

STATEMENT C

Operating Acct.

$ 238,261(147,945)

(1,607)2,125

90,834

(16,956)(55,000)(36,437)

(108393)

(17,559)

204.828S 187,269

1,749813249,076(1315)

90,834

THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS

Disclosure of accounting policy:For purposes of the statement of cash flows, the Company considers all highly liquid debt instrumentspurchased with a maturity of three months or less to be cash equivalents.

The balance in cash and cash equivalents accounts is as follows:Checking account #1050 $ 1,636Restricted bond acct # 1130 185,633

Total S 187,269

LAKE05 StmtCashFlowPropFnd 11

NOTES

TO THE

FINANCIAL STATEMENTS

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

INTRODUCTION

The Lakeshore Subdivision Sewerage District #1, Monroe, Louisiana, (serving approximately4000 people) was established by the Ouachita Parish Police Jury in the early 1970's and is acomponent unit of the Police Jury. The District is operated by a board of four Commissioners,which is appointed by the Ouachita Parish Police Jury. The Commissioners receive nocompensation. The District is managed by an independent contractor, hence no payrolls. Theactual footage for the lines is not known.

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. BASIS OF PRESENTATION

The accompanying component unit financial statements of the Lakeshore SubdivisionSewerage District of Ouachita Parish have been prepared in conformity with generallyaccepted accounting principles (GAAP) as applied to governmental units. TheGovernmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles.

B. REPORTING ENTITY

As the governing authority of the parish, for reporting purposes, the Ouachita ParishPolice Jury is the financial reporting entity for Ouachita Parish. The financial reporting entity

consists of (a) the primary government (police jury), (b) organizations for which theprimary government is financially accountable, and (c) other organizations for whichnature and significance of their relationship with the primary government are such thatexclusion

would cause the reporting entity's financial statements to be misleading or incomplete.

Governmental Accounting Standards Board Statement No. 14 established criteria fordetermining which component units should be considered part of the Ouachita Parish

Police Jury for financial reporting purposes. The basic criterion for including a potentialcomponent unit within the reporting entity is financial accountability. The GASB has setforth criteria to be considered in determining financial accountability. This criteriaincludes:

1. Appointing a voting majority of an organization's governing body, and

a. The ability of the police jury to impose its will on that organizationand/or

b. The potential for the organization to provide specific financialbenefits to or impose specific financial burdens on the police jury.

2. Organizations for which the police jury does not appoint a voting majoritybut are fiscally dependent on the police jury.

LAKE05Notes 13

LAKESHORE SUBDIVISION SEWERAGE DISTRICTSOF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

3. Organizations for which the reporting entity financial statements would bemisleading if data of the organization is not included because of the nature

or significance of the relationship.

Because the police jury has the authority to perform the above three steps, the districtwas determined to be a component unit of the Ouachita Parish Police Jury, the financialreporting entity. The accompanying financial statements present information only on thefunds maintained by the district and do not present information on the police jury, thegeneral government services provided by that governmental unit, or the othergovernmental units that comprise the financial reporting entity.

C. FUND ACCOUNTING

The Lakeshore Subdivision Sewerage District #1 of Ouachita Parish is organized andoperated on a fund basis whereby a self-balancing set of accounts (Enterprise Fund) ismaintained that comprises its assets, liabilities, fund equity, revenues, and expenses. Theoperations are financed and operated in a manner similar to a private business enterprise,where the intent of the governing body is that the cost (expenses, including depreciation)of providing services on a continuing basis be financed or recovered primarily throughuser charges.

D. BASIS OF ACCOUNTING

The accounting and financial reporting treatment applied to a fund is determined by itsmeasurement focus. The Enterprise Fund statements (government-wide) were accountedfor on a flow of economic resources measurement focus and a determination of netincome and capital maintenance. With this measurement focus, all assets and allliabilities associated with the operation of this fund is included on the balance sheet. TheEnterprise Fund uses the accrual basis of accounting. Revenues are recognized whenearned and expenses are recognized at the time liabilities are incurred. The EnterpriseFund uses the following practices in recording certain revenues and expenses:

Revenues

Revenues consist of income from users of the sewer line in the district. Billing isdone monthly, and the payments are collected and deposited. Interest income is a

result of bank accounts bearing interest.

Expenses

Expenses are reported when the liability occurs. Major expenses are:

Electricity 23,711Supervisory/Accounting 107,295

LAKEOSNotes 14

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

Depreciation 81,324Interest 35,834

E. USE OF ESTIMATES

The preparation of financial statements in conformity with accounting principals generallyaccepted in the United States of America requires management to make estimates andassumptions that affect the reported amounts of assets and liabilities and disclosure ofcontingent assets and liabilities at the date of the financial statements and the reportedamounts of revenues and expenses during the reporting period. Actual results could differfrom those estimates.

F. CASH AND CASH EQUIVALENTS AND INVESTMENTS

Cash includes amounts in demand deposits, interest-bearing demand deposits, and othermoney market accounts. Cash equivalents include amounts in time deposits and thoseinvestments with original maturities of 90 days or less. Under state law, the district maydeposit funds in demand deposits, interest-bearing demand deposits, money marketaccounts, or time deposits with state banks organized under Louisiana law and nationalbanks having their principal offices in Louisiana.

Under state law, the district may invest in United States bonds, treasury notes, orcertificates. These are classified as investments if their original maturities exceed 90

days; however, if the original maturities are 90 days or less, they are classified as cashequivalents. The district has no investments.

G. RESTRICTED ASSETS

Certain proceeds of the enterprise fund's resources are set aside for specific paymentsand are classified on the balance sheet as restricted assets because their use is limited byapplicable requirements. Restricted assets include the "customer deposits" account,which is used to segregate water meter deposits used to pay any outstanding water billswhen customers discontinue service.

H. FIXED ASSETS

Fixed assets of the district are valued at historical cost and are included on the balancesheet of the fund, net of accumulated depreciation. Construction period interest isimmaterial and is not capitalized. Depreciation of all exhaustible fixed assist is charged asan expense against operations. Depreciation is computed using the straight-line methodover the estimated useful lives of periods from 5 to 50 years.

I. COMPENSATED ABSENCES

The district does not have a formal leave policy.

LAKE05Notes 15

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

J. LONG - TERM LIABILITIES

Long-term liabilities are recognized within the enterprise fond.

K. FUND EQUITY

Contributed Capital

Grants, entitlements, or shared revenues received that are restricted for theacquisition or construction of capital assets are recorded as contributed

capital. Contributed capital is not amortized.

Reserves

Reserves represent those portions of fond equity legally segregated for a specificfuture use.

L. ENCUMBRANCES

Encumbrance accounting is not used.

NOTE 2. CASH AND CASH EQUIVALENTS

At December 31, 2005, the district has cash and cash equivalents (book balances) totaling$187,269 as follows:

Cash and Cash Equivalents $ 187,269

TOTAL $ 187,269

These deposits are stated at cost, which approximates market. Under state law, these depositsmust be secured by federal deposit insurance and/or the pledge of securities owned by the fiscalagent bank. The market value of the pledged securities plus the federal deposit insurance must atall times equal the amount on deposit with the fiscal agent. These securities are held in the nameof the pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable toboth parties. At December 31,2005, the district has $187,269 on deposit (checking) with theOuachita Independent Bank and CD's in the amount of $395,482 (OIB - $441,742, Chase -$139,373). The deposits held by the OIB and Chase Banks are insured by FDIC and SecurityPledges (Market Value) for a total of $602,542.

PLEDGED SECURITIES CHASE OIB TOTALCash and Cash Equivalents - 187,269 187,269

LAKEOSNotes 16

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

CD's 139,373 256,109 395,482Totals 139,373 443,378 582,751

FDIC Insurance 100,000 100,000 200,000Security Pledge (Market Value) 44,041 358,501 402,542

Total Insurance and Security Pledge 144,041 458,501 602,542Collateralized above requirement 4,668 15,124 19,792

ADEQUATELY COLLATERALIZED.

Even though the pledged securities are considered uncollateralized (Category 3) under theprovisions of GASB Statement 3, Louisiana Revised Statute 39:1229 imposes a statutoryrequirement on the custodial bank to advertise and sell the pledged securities within 10 days ofbeing notified by the district that the fiscal agent has failed to pay deposited funds upon demand.

NOTE 3. RECEIVABLES

The following is a summary of receivables at December 31, 2005:

Class of Receivable Current Assets Total

Accounts Receivable 38,662 38,662

No allowance for bad debts is used since bad debts are offset by utility deposits or written off.

NOTE 4. RESTRICTED ASSETS

RESTRICTED ASSETSOperating Fund Savings 154,851Bond Reserve Fund 139,373

TOTAL 294,224

These assets are restricted to pay bond indebtedness and a contingency fund for repairs. Theoutstanding bond indebtedness @ 12/31/2005 was $490,000.

NOTE 5. FIXED ASSETS

A summary of fixed assets at December 31, 2005, follows:

Property, Plant & Equipment - December 31, 2004 1,776,580

Additions-2005 16,956

LAKEOSNotes 17

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

Total Capital (Fixed) Assets December 31, 2005 1,793,537

Less Accumulated Depreciation (899,611)Total Net Capital Assets 893,926

NOTE 6. LONG - TERM LIABILITIES

On April 1,1992, Sewer Revenue Bonds, Series 1992, were issued to Lakeshore SewerageSubdivision District #1. The following are descriptions of the bonds:

Sewer Revenue Bonds 765,000Form Fully RegisteredDate 04/01/92Denomination 5,000Payment to Trust Co. of LAMaturity 20 YearsInterest Rate Varies 4-7.1 %

The following restrictions apply:

Revenue Bond Sinking Fund

1. Maintain a sufficient amount to pay promptly and fully the principal of and theinterest on the bonds as they severally become due and payable by transferring fromthe Sewer System Fund to the Sinking Fund monthly in advance on or before the 20*day of each month of

2. Each year, one sixth (1/6) of the interest on the Bonds falling due on the next InterestPayment Date and One - Twelfth (1/12) of the principal of the Bonds falling due onthe next principal payment date, together with such additional proportionate sum asmay be required so that sufficient moneys will be available in the Sinking Fund to paysaid principal and interest as the same respectively become due.

3. The establishment and maintenance of a "Revenue Bond Reserve Fund" (the ReserveFund) with the Fiscal Agent Bank by depositing from Bond proceeds upon delivery ofthe Bonds, a sum equal to the Reserve Fund Requirement, and by making any furtherdeposits as provided in the Bond resolution so that there will be on deposit in theReserve Fund an amount equal to the Reserve Fund Requirement. The money in theReserve fund shall be retained solely for the purpose of paying the principal of andinterest on bonds payable from the Sinking Fund as to which there would otherwise bedefault (except such amounts, if any, as may be payable to the United States ofAmerica as a rebate of arbitrage pursuant to Section 148(f) of the Code.

3. The establishment and maintenance of a "Capital Additions and Contingencies Fund"(the Contingencies Fund") to care for additions and improvements, renewals,

LAKEOSNotes 18

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

replacements and emergency repairs or operational costs necessary to properlyoperate the System. In addition to caring for extensions, additions, improvements,renewals and replacements or emergency operation and maintenance expendituresnecessary to properly operate the System, the money in the Contingencies Fund shallbe used to pay the principal of and the interest on the bonds, including any additionalparipassu bonds issued in the manner provided by the Bond Resolution, for thepayment of which there is not sufficient money in the Sinking and or Reserve Fund,but the money in the Contingencies Fund shall never be used for the making ofextensions, additions, improvements, renewals and replacements to the System if suchuse of said money will leave in the Contingencies fund for making emergency repairsor replacements or paying emergency operational costs less than the sum of TenThousand Dollars ($10,000.00). Upon a finding of the Governing Authority thatmoneys in the Contingencies Fund are not required for the above - stated purposes, ofthe fund, such moneys may also be used to retire by purchase or call for redemptionOutstanding Bonds or outstanding pan passu bonds payable from the Net SewerRevenues (as defined in the Bond Resolution) at prices not exceeding 105% of theface value thereof plus accrued interest; provided such purchase would not leaveremaining in the Contingencies Fund less than the amount of Fifty Thousand Dollars($50,000.00). If at any time it shall be necessary to use moneys in the Reserve Fundor the Contingencies Fund for the purpose of paying principal or interest on bondspayable from the Sinking Fund as to which there would otherwise be default, then themoneys so used shall be replaced from the revenues of the system first thereafterreceived, not required for the purposes described in the Bond Resolution it being theintention that there shall as nearly as possible be at all times in the Reserve Fund andthe Contingencies Fund the amounts specified.

The following is a summary of bond transactions of the District for the fiscal year endedDecember 31,2005.

Total Long-Term Debt at December 31, 2004 545,000Less Current Portion - April 1, 2005 55,000Total Long-Term Debt at December 31,2005 490,000

The annual requirements to amortize bonds outstanding at December 31, 2004, is as follows:

Due April 12006200720082009

Amount55,00060,00065,00070,000

Interest Rate7.107.107.007.00

Price or Yield7.107.107.107.10

LAKEOSNotes 19

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1OF OUACHITA PARISH

Notes to the Financial StatementsAs of and for the Year Ended December 31,2005

2010 75,000 7.00 7.102011 80,000 7.00 7.102012 85,000 7.00 7.10

NOTE 7. PENSION PLAN

None.

NOTE 8. RELATED PARTY TRANSACTIONS

None.

NOTE 9. LITIGATION AND CLAIMS

None.

NOTE 10. SUBSEQUENT EVENTS

None.

NOTE 11. OTHER SUPPORT

None.

LAKEOSNotes 20

REQUIRED SUPPLEMENTARY INFORMATION(PART II)

JIMMIE SELF, CPAA PROFESSIONAL ACCOUNTING CORPORATION

2908 Cameron Street, Suite CMonroe, Louisiana 71201

Phone (318) 323-4656 Fax (318) 388-0724

INDEPENDENT AUDITOR'S REPORT ON COMPLIANCE AND ON INTERNAL CONTROL OVERFINANCIAL REPORTING BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED

IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Board of CommissionersLakeshore Subdivision Sewerage District #1Monroe, Louisiana

I have audited the basic financial statements of the Lakeshore Subdivision Sewerage District #1,a component unit of the Ouachita Parish Police Jury, State of Louisiana, as of and for the yearended December 31, 2005, and have issued my report thereon dated June 15,2006. I conductedmy audit in accordance with auditing standards generally accepted in the United States ofAmerica and the standards applicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States, and the LouisianaGovernmental Audit Guide issued by the Louisiana Legislative Auditor and the LouisianaSociety of Certified Public Accountants.

Compliance

As part of obtaining reasonable assurance about whether the District's financial statements arefree of material misstatement, I performed tests of its compliance with certain provisions of laws,regulations, contracts and grants, noncompliance with which could have a direct and materialeffect on the determination of financial statement amounts. However providing an opinion oncompliance with those provisions was not an objective of my audit and, accordingly, I do notexpress such an opinion. The results of my tests disclosed no instances of noncompliance thatare required to be reported under Government Auditing Standards.

Internal Control Over Financial Reporting

In planning and performing my audit, I considered the District's internal control over financialreporting in order to determine my auditing procedures for the purpose of expressing my opinionon the financial statements and not to provide assurance on the internal control over financialreporting. My consideration of the internal control over financial reporting would not necessarilydisclose all matters in the internal control over financial reporting that might be materialweaknesses. A material weakness is a condition in which the design or operation of one or moreof the internal control components does not reduce to a relatively low level the risk thatmisstatements in amounts that would be material in relation to the financial statements beingaudited may occur and not be detected within a timely period by employees in the normal course

LAKE05Com>lianceGAS 22

of performing their assigned functions. I noted no matters involving the internal control overfinancial reporting and its operation that I consider to be material weaknesses.

This report is intended for the information and use of the management of the District and theLouisiana Legislative Auditor and is not intended to be and should not be used by anyone otherthan these specified parties. Under Louisiana Revised Statute 24:513, this report is distributed bythe Louisiana Legislative Auditor as a public document.

Jimmie Self, CPAMonroe, LouisianaJune 15,2006

LAKEOSComplianceGAS 23

LAKESHORE SUBDIVISION SEWERAGE DISTRICT #1Monroe, Louisiana

Supplemental Information ScheduleAs of and for the Year Ended December 31,2005

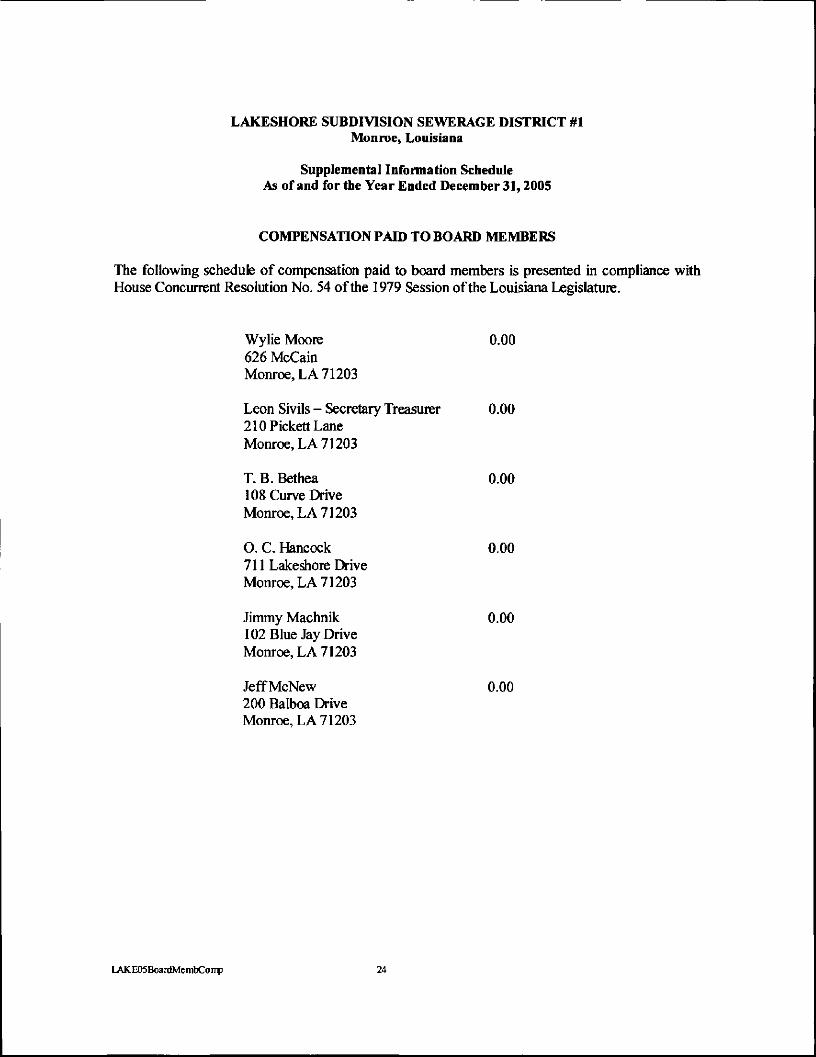

COMPENSATION PAID TO BOARD MEMBERS

The following schedule of compensation paid to board members is presented in compliance withHouse Concurrent Resolution No. 54 of the 1979 Session of the Louisiana Legislature.

Wylie Moore 0.00626 McCainMonroe, LA 71203

Leon Sivils - Secretary Treasurer 0.00210 Pickett LaneMonroe, LA 71203

T. B. Bethea 0.00108 Curve DriveMonroe, LA 71203

O. C. Hancock 0.00711 Lakeshore DriveMonroe, LA 71203

Jimmy Machnik 0.00102 Blue Jay DriveMonroe, LA 71203

JeffMcNew 0.00200 Balboa DriveMonroe, LA 71203

LAKEGSBoardMembConp 24

LAKESHORE SUBDIVISION SEWERAGE DISTRICT No. 1A Component Unit Of The

OUACHITA PARISH POLICE JURYMonroe, Louisiana

SCHEDULE OF FINDINGS AND QUESTIONED COSTSFor the Year Ended December 31, 2005

Summary of Audit Results

• The auditor's report expresses an unqualified opinion on the basic financial statementsof the Lakeshore Subdivision Sewerage District No. 1 of Ouachita Parish, State ofLouisiana.

• There were no reportable conditions in internal control disclosed during the audit ofthe basic financial statements which were required to be reported in the Report OnCompliance And On Interned Control Over Financial Reporting Based On An Audit OfFinancial Statements Performed In Accordance With Government Auditing Standards.

• The results of my tests disclosed no instances of noncompliance material to the basicfinancial statements which were required in the Report On Compliance And On InternalControl Over Financial Reporting Based On An Audit Of Financial StatementsPerformed In Accordance With Government Auditing Standards.

LAKEOSSchFindAndQuestCosts 25