k+s aktiengesellschaft berenberg food ingredients and ... · k+s aktiengesellschaft. berenberg food...

TRANSCRIPT

K+S Aktiengesellschaft

Berenberg Food Ingredients and Chemicals Conference 201615 September 2016

Martin Heistermann, Senior Investor Relations Manager

K+S Group 2

K+S Group

Investment CaseTwo-pillar strategy

Global Presence

Positioned for growthEarnings-based dividend policy

Attractive mid-term outlookBalanced regional portfolio

Sustainable margin growth through specialisationCost discipline

K+S Group 3

Our ProductsK+S Group

De-icing

Fertilizer

Food processing

Chemicals

Pharma

Oil & Gas

Agriculture(Feed)

~ 10m tons

~ 6m tons

~ 11m tons

K+S Group

Inevitable for life…and for K+SSalt

4

Main Applications: Food processing

industry Baking industry Condiment and

preservative agent

Main Applications: Chemical industry Chlor-Alkali

processes (→ PVC) Polycarbonates ,

MDI (Isocyanat)(→ plastics, synthetic resin)

Synthetic Soda Ash (→ glass)

Main Applications: Winter road

maintenance services

Commercial users Private

households

Main Applications: Water treatment Drilling fluids Animal feed Infusion, dialysis

solutions Pharmaceuticals Preserving of fish Dyeing works Leather treatment

De-Icing Food processing Industrial ChemicalConsumer

Main Applications: Table salt Dishwasher care Water softening Pool chlorination Body care

K+S Group 5

Unrivalled Global Production NetworkSalt

More than 30 assets on 3 continents Ensuring close proximity to customers Best in class supply chain assets and competence Industry best cost production in Chile

Project in Australia launched

K+S Group 6

Balanced FertilizationPotash and Magnesium Products

Plants need sunlight, water and minerals

Only few soils with sufficient availability of plant nutrients

Potash is an indispensablesupplement to natural nutrient content of soils

Potash not substitutable

K+S Group 7

¼ of a Soccer Field Remains to Feed One Person 2050Potash and Magnesium Products

K+S Group 8

Utilizing Entire Range of Minerals in Complex DepositsPotash and Magnesium Products

KCL (MOP)3.1

Industrial products

0.7

Specialties3.0

6.8

SOP

Korn-Kali

Kieserite

Industrial potash

Health Care & Nutrition

K+S Group 9

Q12012

Q12013

Q12014

Q12015

Q12016

Bas

is: Q

120

12

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Basi

s: Q

120

14

K+S average selling price versus selected peers

MOP gran. Europe vs. Brazil (Source: FMB)

200

300

400

500

600

200

300

400

500

600

Europe (€, Granular, cfr)

Brazil(US$/t, Granular, cfr)

US$/t €/t

2011 2012 2013 2014 2015 2016

K+S K+S

Potash and Magnesium ProductsOur Unique Portfolio Makes Us More Robust

K+S Group 10

Strengthening our Global Presence Legacy Project

ChinaIndiaSouth East Asia

North America

South America

K+S Group 11

ValuationLegacy Project

~90

2017 2018 2019 2020 2021 2022 2023

Cost

sper

ton

(CAD

)

Volume ramp-up (m metric tons) /costs per ton (CAD)

Production costs Logistics costs Mining taxes/ royalties

<1 ~2 ~2.1 ~2.3 ~2.4 ~2.6 ~2.9Sales volumes (m metric tons)

Implied Value Per Share (€)

Terminal growth rate

0% 2%

WAC

C

7% ~ 21

8% ~ 11

Volume ramp-up (m metric tons)/ costs per ton (CAD)

Main assumptions:

Unaffected potash production Potash price level of summer 2015

(time of release of guidance)

K+S Group 12

K+S Group

Q2/16 ResultsLower potash prices

Dry weather

Fit for the FutureMild winter weather

Full-year guidanceMissing deep-well injection

High extraordinary impactsCost discipline

K+S Group 13

Weak Second Quarter in Both Business UnitsK+S Group

179

15

Q2/15 Volume/ Price Missing deep-well injection

Fit for the Future Q2/16

EBIT I in € million

• Potash price andproduct mix

• Mild winter in salt

• Werra productionstandstills

K+S Group 14

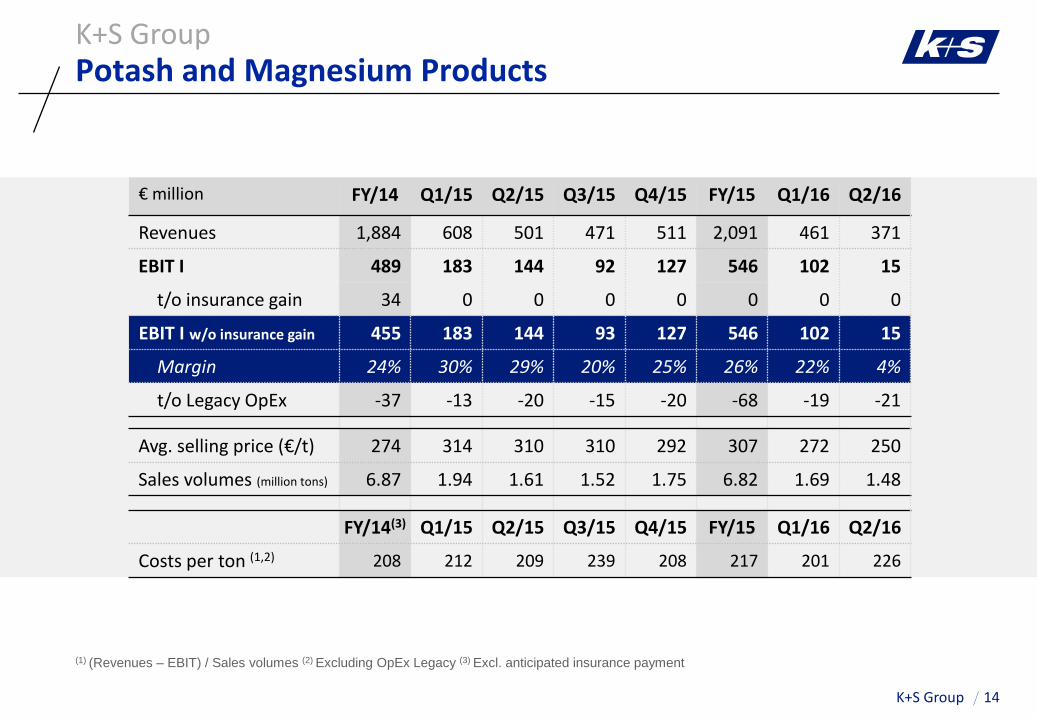

Potash and Magnesium ProductsK+S Group

(1) (Revenues – EBIT) / Sales volumes (2) Excluding OpEx Legacy (3) Excl. anticipated insurance payment

€ million FY/14 Q1/15 Q2/15 Q3/15 Q4/15 FY/15 Q1/16 Q2/16

Revenues 1,884 608 501 471 511 2,091 461 371

EBIT I 489 183 144 92 127 546 102 15

t/o insurance gain 34 0 0 0 0 0 0 0

EBIT I w/o insurance gain 455 183 144 93 127 546 102 15

Margin 24% 30% 29% 20% 25% 26% 22% 4%

t/o Legacy OpEx -37 -13 -20 -15 -20 -68 -19 -21

Avg. selling price (€/t) 274 314 310 310 292 307 272 250

Sales volumes (million tons) 6.87 1.94 1.61 1.52 1.75 6.82 1.69 1.48

FY/14(3) Q1/15 Q2/15 Q3/15 Q4/15 FY/15 Q1/16 Q2/16

Costs per ton (1,2) 208 212 209 239 208 217 201 226

K+S Group 15

SaltK+S Group

€ million FY/14 Q1/15 Q2/15 Q3/15 Q4/15 FY/15 Q1/16 Q2/16

Revenues 1,779 727 374 382 442 1,925 595 319

EBIT I 173 142 43 43 39 266 123 5

Margin 10% 20% 11% 11% 9% 14% 21% 2%

Sales volumes (million tons) 23.6 9.1 3.6 3.8 4.7 21.1 7.1 2.9

De-icing 14.4 6.9 1.2 1.5 2.3 11.9 4.9 0.6

Non de-icing 9.2 2.2 2.4 2.3 2.4 9.2 2.2 2.3

Average selling prices (€)

De-icing 53 65 65 62 67 65 64 53

Non de-icing 104 119 120 124 118 120 122 123

K+S Group

Update on deep-well injection

16

Review of the application is ongoing

Originally expected to be completed in summer 2016

Currently, saline wastewater can only be disposed to a limited extent

Production largely based on water flow rate of the Werra river

Potash and Magnesium Products

Mai Jun Jul Aug

Wat

erflo

wW

erra

May Jun Jul Aug

K+S Group

K+S GroupGuidance 2016: EBIT I also Influenced by Extraordinaries

17

Actual2015

Volume-/price

Missing deep-well injection

permit

Othereffects(net)

Fit for theFuture

2016e

782

€ million

200

300

2016e EBIT I range

Main effects:- OpEx Legacy- Higher D&A

200

K+S Group 18

K+S Group

Management AgendaCommissioning Legacy

Lower CapEx

Fit for the FutureManage environmental challenges

Enhancing portfolio of higher yielding productsSalt 2020

Potash fundamentals to improveCost discipline

K+S Group

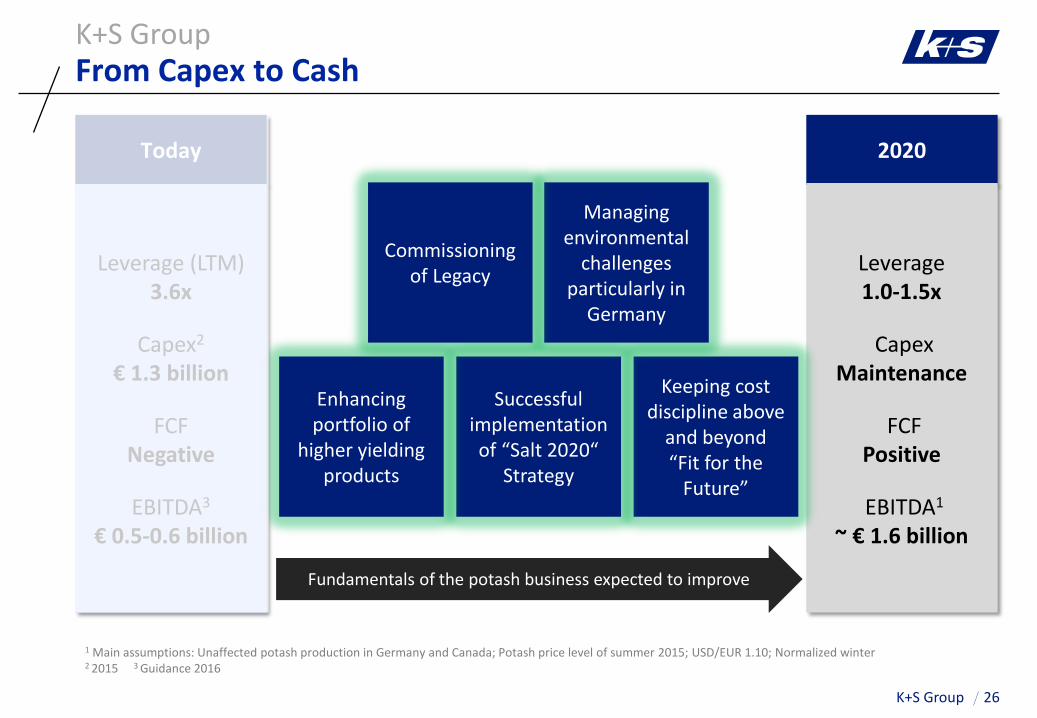

From Capex to CashK+S Group

19

Today 2020

Leverage1.0-1.5x

CapexMaintenance

FCFPositive

EBITDA1

~ € 1.6 billion

Leverage (LTM)3.6x

Capex2

€ 1.3 billion

FCFNegative

EBITDA3

€ 0.5-0.6 billion

Keeping cost discipline above

and beyond “Fit for the

Future”

Successful implementation of “Salt 2020“

Strategy

Enhancing portfolio of

higher yielding products

Managing environmental

challenges particularly in

Germany

Commissioning of Legacy

Fundamentals of the potash business expected to improve

1 Main assumptions: Unaffected potash production in Germany and Canada; Potash price level of summer 2015; USD/EUR 1.10; Normalized winter2 2015 3 Guidance 2016

K+S Group 20

Commissioning Continues Despite Incident in July Commissioning of Legacy

No injuries 1 of 5 crystallizers dropped Impact on ramp-up:

− Commissioning continues− Production of first ton

delayed into Q2/17 − Production volume 2017

below previously planned (up to 1 million tons)

Capacity of 2 million tons p.a. expected to be reached by the end of 2017

K+S Group 21

Deep-well injection: Measures for the short-termManaging Environmental Challenges in Germany

1997 2006 2012 2015 2016 2017 Beyond

Werra + Deep-well injection Measures Gap

20

10

14

7 7 7 5.5

Identification and implementation of measures

to bridge 2016/2017

KCF plant

Million m³

K+S Group 22

Two Bolt-On Acquisitions in Both Business UnitsEnhancing Portfolio of Higher Yielding Products

One of the largest producers of synthetic magnesium sulphate

Oil palms, soybeans and sugar cane and industrial applications

Improved access to growth markets of South-East Asia and China

Scalable low cost production assets

Huludao

Expected capacity of 3.5 million tons of salt for chemical industry in Asia

CapEx of around € 225 million

Possible production start in 2022

K+S Group

250+

2013 2015 2020e

23

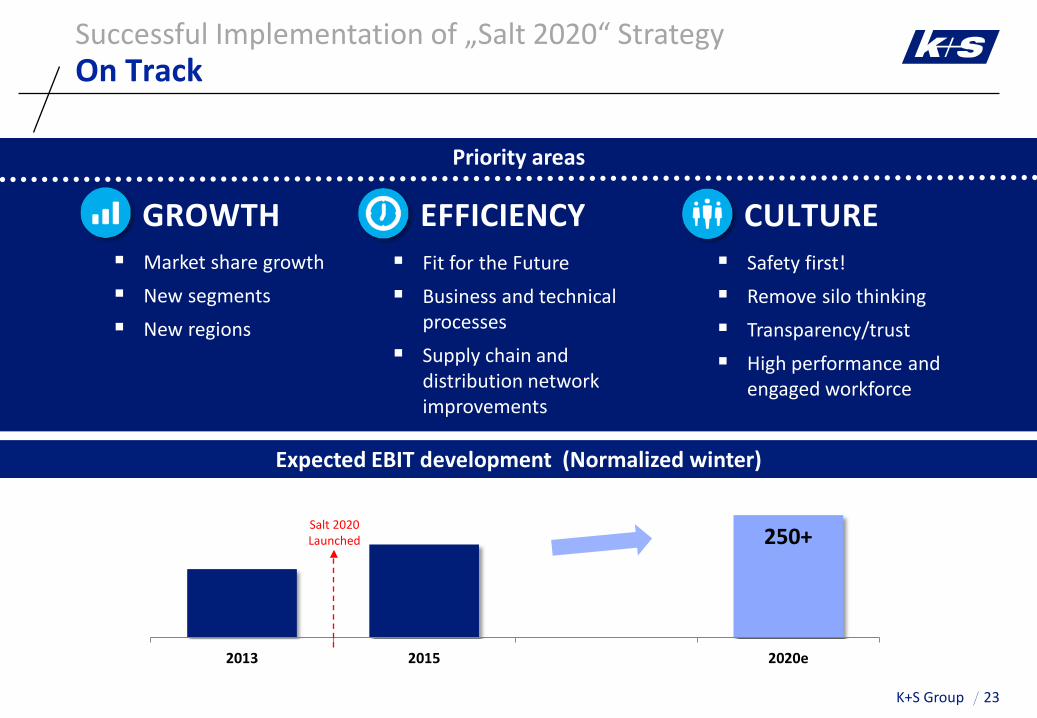

On TrackSuccessful Implementation of „Salt 2020“ Strategy

Expected EBIT development (Normalized winter)

Safety first! Remove silo thinking Transparency/trust High performance and

engaged workforce

Fit for the Future Business and technical

processes Supply chain and

distribution network improvements

Market share growth New segments New regions

Salt 2020 Launched

Priority areas

GROWTH CULTUREEFFICIENCY

K+S Group

2013 2014 2015 2016

>150

30

>180

24

Cost Discipline Will Remain HighKeeping Cost Discipline Above and Beyond ‚Fit for the Future‘

on track

€ million

“Fit for the Future” on track More than 2/3 of total

aspirations achieved Measures implemented will

continue beyond 2016 with full effects until 2018

Further top-down measures beyond “Fit for the Future” initiated Effects coming through in

2017 and 2018

K+S Group 25

Debt ProfileK+S Group

Bond I € 500 million(expn. June 2022; coupon: 3.000%)

Bond II € 500 million(expn. Dec 2021; coupon: 4.125%)

Bond III € 500 million(expn. Dec 2018; coupon: 3.125%)

RCF € 1 billion

Debt Instruments

2016 2017 2018 2019 2020 2021 2022

Schuldschein € 700 million(3-yrs: € 295 million; 5-yrs: € 365 million; 7-yrs: € 40 million)

K+S Group

From Capex to CashK+S Group

26

Today 2020

Leverage1.0-1.5x

CapexMaintenance

FCFPositive

EBITDA1

~ € 1.6 billion

Leverage (LTM)3.6x

Capex2

€ 1.3 billion

FCFNegative

EBITDA3

€ 0.5-0.6 billion

Keeping cost discipline above

and beyond “Fit for the

Future”

Successful implementation of “Salt 2020“

Strategy

Enhancing portfolio of

higher yielding products

Managing environmental

challenges particularly in

Germany

Commissioning of Legacy

Fundamentals of the potash business expected to improve

1 Main assumptions: Unaffected potash production in Germany and Canada; Potash price level of summer 2015; USD/EUR 1.10; Normalized winter2 2015 3 Guidance 2016

K+S Group 27

IR Contact DetailsK+S Group

E-Mail: [email protected]: www.k-plus-s.comIR-website: www.k-plus-s.com/en/ir

K+S AktiengesellschaftBertha-von-Suttner-Str. 734131 Kassel (Germany)

Laura SchumberaJunior Investor Relations ManagerPhone.: +49 561 / 9301-1607Fax: +49 561 / [email protected]

Thorsten BoeckersHead of Investor RelationsPhone: +49 561 / 9301-1460Fax: +49 561 / [email protected]

Andrea RachInvestor Relations AssistantPhone: +49 561 / 9301-1100Fax: +49 561 / [email protected]

Martin HeistermannSenior Investor Relations ManagerPhone.: +49 561 / 9301-1403Fax: +49 561 / [email protected]

Patrick KoflerSenior Investor Relations ManagerPhone.: +49 561 / 9301-1885Fax: +49 561 / [email protected]

K+S Group 28

Forward-Looking StatementsK+S Group

This presentation contains facts and forecasts that relate to the future development of the K+S

Group and its companies. The forecasts are estimates that we have made on the basis of all the

information available to us at this moment in time. Should the assumptions underlying

these forecasts prove not to be correct or should certain risks – such as those referred to in

the Risk Report of the Annual Report – materialize, actual developments and events may deviate

from current expectations. The Company assumes no obligation to update the statements, save

for the making of such disclosures as are required by the provisions of statute.

K+S Group

K+S Group 30

K+S Group

K+S Aktiengesellschaft · Bertha-von-Suttner-Straße 7 · 34131 Kassel | Germany · Internet: www.k-plus-s.comInvestor Relations · phone: +49 (0)561 / 9301-1100 · fax: +49 (0)561 / 9301-2425 · email: [email protected]

Financial Calendar 2016/17: 10 Nov: Q3/16 – 16 Mar: FY/16

K+S Share• WKN: KSAG88• ISIN: DE000KSAG888 • Ticker-Symbols:

Bloomberg SDF / Reuters SDFG

K+S ADR• CUSIP: 48265W108 • ADR Ticker-Symbol:

Bloomberg: KPLUY / Reuters: KPLUY.PK

K+S Bond 06/2022• WKN: A1P GZ8• ISIN: DE000A1PGZ82

K+S Bond 12/2018• WKN: A1Y CR4 • ISIN: XS0997941199

K+S Bond 12/2021• WKN: A1Y CR5• ISIN: XS0997941355