kpmg financial reporting insights · pdf fileof cases, these reportable ... kpmg financial...

TRANSCRIPT

August 2016

kpmg.com.au

KPMG FinancialReporting InsightsKPMG’s review of 45 ASX200 entities Operating Segment disclosures

2 | KPMG Financial Reporting Insights: Operating Segment disclosures

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

The headlines

91 percent of entities reviewed disclosed multiple reportable segments

81 percent of entities used a non-IFRS measure when measuring segment performance

91%

81%

Entities on average disclosed three to four reportable segments with the majority of entities using products and services to determine their segments

In 81 percent of cases cash generating units with goodwill allocated to them aligned with or were at a lower level than the reportable segments

Wide range of interpretations as to what is required to comply with the entity wide disclosure requirements on revenue by product and service type, geographical location and major customers

In 78 percent of cases the reportable segments were consistent with how the performance of the business was disaggregated and discussed in the Operating and Financial Review

$

3 | KPMG Financial Reporting Insights: Operating Segment disclosures

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

IntroductionSegment information is required to be disclosed in general purpose financial reports of listed entities1 in accordance with AASB 8 Operating Segments. Apart from being required, these disclosures provide users with the information they need to evaluate an entity’s business activities and the economic environment in which it operates and provides insights into how management assess the performance of and makes decisions about the business.

The importance of segment disclosures is further highlighted by the links that exist between these disclosures and information provided in an operating and financial review (OFR) forming part of a listed entities directors’ report2 and the requirements of AASB 136 Impairment of Assets.

Although not an ASIC focus area, ASIC has definitely been paying more attention to the segment disclosures in recent times and especially how they interact with the impairment assessments entities are making for goodwill and the identification of cash generating units.

Given the significance of segment disclosures, KPMG have undertaken a review of 45 ASX200 entities annual reports for the 2015 reporting period, focusing on the segment report and its interactions with the impairment disclosures and the OFR.

What we have seen in the 2015 reporting periodOur review identified that 91 percent of entities have more than one reportable segment, with entities averaging between three to four reportable segments each. Further, in 78 percent of cases, these reportable segments were consistent with how the performance of the business was disaggregated and discussed in the OFR and in 81 percent of cases, the cash generating units with goodwill allocated to them aligned with or were at a lower level than the reportable segments.

Purpose of publicationThis publication is intended to assist listed entities assess how their segment discloses compare to other entities in the ASX200. This publication provides insights into:

• the basis on which entities determine their segments• the common measures of segment profit or loss• other common items of income and expense reported by

entities for each segment• how entities interpret and address the entity wide

disclosures required by AASB 8• the interactions between segment disclosures, the OFR

and the impairment requirements, and• the relationship between segments and Integrated

Reporting.

1. ‘listed entities’ under AASB 8, paragraphs Aus2.1(d) & (e) are entities: (i) whose debt or equity instruments are traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local and regional markets); or (ii) that file, or are in the process of filing, their financial statements with a securities commission or other regulatory organisation for the purpose of issuing any class of instruments in a public market.2. Corporations Act 2001, section 299A.

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

4 | KPMG Financial Reporting Insights: Operating Segment disclosures

General disclosuresAASB 8 Operating Segments defines an operating segment as a component of an entity:

• that engages in business activities from which it may earn revenues and incur expenses

• who’s operating results are regularly reviewed by the chief operating decision maker (CODM) to make decisions about resources to be allocated to the segment and assess performance, and

• for which discrete financial information is available.³

Number of segments reported in reviewed population

Source: KPMG

0 2 4 6 8 10 12 14

Number of entities

Num

ber

of s

egm

ents

1

2

3

4

5

6

7

10

Our review showed the number of segments disclosed by entities varied from one to as many as 10, with the majority of entities (55 percent) disclosing – three to four segments in their segment note. All the following discussion focuses on the sub-sample of 41 entities that disclosed more than one segment, unless noted otherwise.

How has the entity determined its segments?

Source: KPMG

Mix of geographic regions and products & servcies

Products and services

Geographical regions

Other

Mix of geographic regions and products & servcies

Products and services

Geographical regions

5%

32%

27%

36%

3. AASB 8, paragraph 5.

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

5 | KPMG Financial Reporting Insights: Operating Segment disclosures

Of the 41 entities disclosing more than one reportable segment, 36 percent used product and service lines as the basis for determining segments and a further 32 percent used a combination of product and service lines and geographical regions to determine segments. This combined approach was principally applied in one of two ways:

1. Segments were first determined by product line, and then the predominate product line was broken down further by country.

2. Segments were first determined by country or region in which the entity operated, and then the largest market (typically Australia) was disaggregated further into smaller segments identified by product lines.

Only 27 percent of entities used purely a geographical basis for determining their segments.

Corporate segmentsAASB 8 indicates that not every part of an entity is necessarily a segment or part of an operating segment, drawing out corporate headquarters as an example of such a component. This is due to the fact that the specific part of the business may not earn revenues or may earn revenues that are only incidental to the activities of the entity.4

Seven of the 41 entities disclosing more than one reportable segment (17 percent) reported a corporate segment with only three of these disclosing revenue from that segment. However, for one of these three entities, the corporate segment was combined with other non-reportable segments and the revenue in another was minimal. It would therefore appear that for the majority of these seven entities, the corporate segment may not have necessarily represented an operating segment as defined by the standard.

For entities in similar situations it may be worth reconsidering whether their corporate segments are in fact an operating segment or whether it would be more appropriate to rename them as unallocated or other items used to reconcile the total segment results back to the consolidated result disclosed in the financial report.

Aggregating Segments AASB 8 require entities disclose whether they have aggregated any operating segments into reportable segments. Although it would appear to be best practice to make a statement where there has been no aggregation, only 39 percent of entities explicitly stated that they did not aggregate any segments. 20 percent of entities disclosed they had aggregated segments while 41 percent of the entities were silent on whether they had aggregated any segments or not.

Operating vs Reportable segmentsAlthough an entity may have a specific number of operating segments, AASB 8 only requires segments meeting specific quantitative thresholds to be separately reported (reportable segments).5 AASB 8 requires reportable segments to be identified until at least 75 percent of external revenues have been allocated to these segments.

Segment revenue as % of consolidated revenue

Source: KPMG

120+%

100-120%

100%

75% - 100%

<75%

120+%

100-120%

100%

75% - 100%

<75%

56%

5%5%2%

32%

Of the 41 entities disclosing more than one reportable segment, the majority reported total segment revenues representing at least 75 percent of total consolidated revenues. There was one entity that reported total segment revenue below the 75 percent threshold (representing 68 percent of total revenue), however given this particular entity’s basis for measuring segment revenue was different to the IFRS basis used for measuring consolidated revenue, this outcome is reasonable.

For the 15 entities where segment revenues were higher than consolidated revenue, this was typically attributable to inter-segment sales that eliminated on consolidation.

Accounting for transactions between segmentsAASB 8 requires entities to disclose the basis of accounting for any transaction between reportable segments.6

Basis for accounting for transactions between segments

Source: KPMG

Other

Undisclosed

Arms length

Other

Undisclosed

Arms length

63%

32%

5%

Of the entities reviewed, 32 percent disclosed that transactions between segments were undertaken on an arm’s length basis, with 63 percent remaining silent on the basis for accounting. Although some of these entities may not have had significant transactions between their segments, it would appear that describing the basis for accounting between segments is an area where entities could look to improve their disclosures.

4. AASB 8, paragraph 6.

5. AASB 8, paragraph 13 requires an entity to report separate information for an operating segment meeting any of the following criteria: a) Its reported revenues are 10 percent or more of combined revenues; b) The absolute amount of reported profit or loss is 10 percent or more of the greater in absolute amount of (i) the combined reported profit of all operating segments that did not report a loss and (ii) the combined reported loss of all operating segments that reported a loss; or c) Its assets are 10 percent of more of the combined assets of all operating segments.6. AASB 8, paragraph 27(a).

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

6 | KPMG Financial Reporting Insights: Operating Segment disclosures

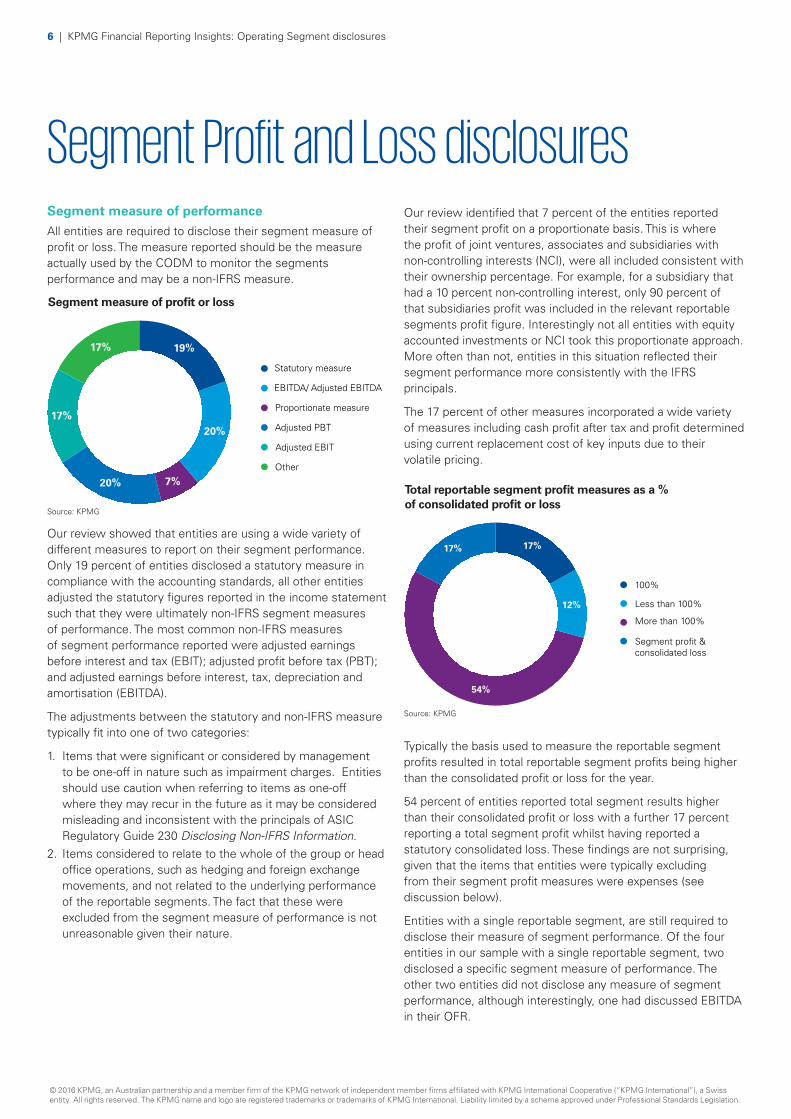

Segment Profit and Loss disclosuresSegment measure of performanceAll entities are required to disclose their segment measure of profit or loss. The measure reported should be the measure actually used by the CODM to monitor the segments performance and may be a non-IFRS measure.

Segment measure of profit or loss

Source: KPMG

Other

Adjusted EBIT

Adjusted PBT

Proportionate measure

EBITDA/ Adjusted EBITDA

Statutory measure

Other

Adjusted EBIT

Adjusted PBT

Proportionate measure

EBITDA/ Adjusted EBITDA

Statutory measure

17% 19%

20%

20% 7%

17%

Our review showed that entities are using a wide variety of different measures to report on their segment performance. Only 19 percent of entities disclosed a statutory measure in compliance with the accounting standards, all other entities adjusted the statutory figures reported in the income statement such that they were ultimately non-IFRS segment measures of performance. The most common non-IFRS measures of segment performance reported were adjusted earnings before interest and tax (EBIT); adjusted profit before tax (PBT); and adjusted earnings before interest, tax, depreciation and amortisation (EBITDA).

The adjustments between the statutory and non-IFRS measure typically fit into one of two categories:

1. Items that were significant or considered by management to be one-off in nature such as impairment charges. Entities should use caution when referring to items as one-off where they may recur in the future as it may be considered misleading and inconsistent with the principals of ASIC Regulatory Guide 230 Disclosing Non-IFRS Information.

2. Items considered to relate to the whole of the group or head office operations, such as hedging and foreign exchange movements, and not related to the underlying performance of the reportable segments. The fact that these were excluded from the segment measure of performance is not unreasonable given their nature.

Our review identified that 7 percent of the entities reported their segment profit on a proportionate basis. This is where the profit of joint ventures, associates and subsidiaries with non-controlling interests (NCI), were all included consistent with their ownership percentage. For example, for a subsidiary that had a 10 percent non-controlling interest, only 90 percent of that subsidiaries profit was included in the relevant reportable segments profit figure. Interestingly not all entities with equity accounted investments or NCI took this proportionate approach. More often than not, entities in this situation reflected their segment performance more consistently with the IFRS principals.

The 17 percent of other measures incorporated a wide variety of measures including cash profit after tax and profit determined using current replacement cost of key inputs due to their volatile pricing.

Total reportable segment profit measures as a % of consolidated profit or loss

Source: KPMG

Segment profit & consolidated loss

More than 100%

Less than 100%

100%

Segment profit & consolidated loss

More than 100%

Less than 100%

100%

17% 17%

12%

54%

Typically the basis used to measure the reportable segment profits resulted in total reportable segment profits being higher than the consolidated profit or loss for the year.

54 percent of entities reported total segment results higher than their consolidated profit or loss with a further 17 percent reporting a total segment profit whilst having reported a statutory consolidated loss. These findings are not surprising, given that the items that entities were typically excluding from their segment profit measures were expenses (see discussion below).

Entities with a single reportable segment, are still required to disclose their measure of segment performance. Of the four entities in our sample with a single reportable segment, two disclosed a specific segment measure of performance. The other two entities did not disclose any measure of segment performance, although interestingly, one had discussed EBITDA in their OFR.

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

7 | KPMG Financial Reporting Insights: Operating Segment disclosures

Reconciliations of segment disclosures to consolidated resultsEntities are required under AASB 8 to provide a reconciliation between the total reportable segments measures of profit or loss to the entity’s consolidated profit or loss before tax and discontinued operations.7

Consolidated profit that the Segment results were reconciled to

Source: KPMG

EBITDA

EBIT

Statutory profit attributable to members of the parent entity

Profit after tax from continuing operations

Profit before tax from continuing operations

EBITDA

EBIT

Statutory profit attributable to members of the parent entity

Profit after tax from continuing operations

Profit before tax from continuing operations

7%

47%

34%

5%

7%

Our review identified a number of different statutory measures being used as the basis for the reconciliation. In particular, 39 percent reconciled back to an after tax measure whilst 14 percent reconciled back to either EBIT or EBITDA.

The choice of consolidated profit that entities reconciled their segment result to also had a significant impact on the reconciling items that were presented. The graph below outlines the most common reconciling items that the entities disclosed.

Common reconciling items between segment results and consolidated profit

Source: KPMG

0 5 10 15 20

Claims and legal proceedings

Gains and losses on purchases or sale of investments

Share of profits of equity accounted investments

Remuneration

Elimination of discontinued operations

General net eliminations

Unallocated amounts

Derivatives and hedging

Transaction and restructuring costs

Corporate expenses

Depreciation and amortisation

Tax

Impairment

Interest

Number of entities disclosing these reconciling items

It appears that most entities did not consider the financing of their segment operations to be a reflection of the segments performance with 20 entities excluding interest from their segment result and including it as a reconciling item between the segment result and the statutory consolidated profit.

A description of each reconciling item identified in the table above is provided in the Appendix of this report.

Entities are also required to reconcile their segment revenue back to the consolidated statutory revenue. As discussed above (see Operating vs Reportable segments) the most common reconciling item from total segment revenue to consolidated revenue was the elimination of inter-segment sales with 46 percent of entities including this in their reconciliations.

7. AASB 8, paragraph 28(b).

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

8 | KPMG Financial Reporting Insights: Operating Segment disclosures

Material items In addition to the segment profit, entities are required to disclose a number of prescribed income statement line items or any other material income or expense items for each segment if the specified amounts are included in the segment measure of profit or loss or otherwise regularly reported to the CODM (even if not included in the measure of segment profit or loss).8

Material items specifically prescribed by AASB 8 disclosed by segment

All of the 41 entities disclosing more than one reportable segment disclosed their revenue from external customers with depreciation and amortisation and revenues from other operating segments rounding out the top three most commonly reported material items. A direct comparison of the number of entities making these disclosures is not considered relevant as not all entities would have recognised these items in their income statement e.g. not all entities recognised impairment losses in the period.

It was interesting to note that although 13 entities reported their share of equity accounted profits, only 46 percent of these entities proceeded to disclose the carrying amount of their equity accounted investment for each segment which is a required disclosure if the amount is reported to the CODM.9

On top of the prescribed disclosure highlighted above, 62 percent of entities included disclosures in relation to 75 other material items as part of their segment disclosures. On average these entities disclosed an additional three other material items.

The types of other material items disclosed generally depended on the industry that the entity operated in. For example, an insurance business disclosed underwriting profit or loss by reportable segment, whilst a mining company disclosed exploration expenses for each reportable segment. Five entities disclosed share-based payment expenses related to each reportable segment and a number of entities disclosed fair value gains and losses on either investment properties, derivatives or foreign exchange gains or losses.

For the 75 other material items disclosed, in 52 percent of instances the value of the material item disclosed in the segment note was the same as the corresponding statutory consolidated amount. However, in 43 percent of cases these amounts were different to the statutory consolidated amounts and in 5 percent of cases these specific material items were not disclosed elsewhere in the financial report. For those 43 percent where the segment total differed to the statutory consolidated amount, only 69 percent were reconciled back to the statutory consolidated figure. Given AASB 8 requires all items disclosed for reportable segments to be reconciled back to the consolidated amounts10, entities should ensure where individually material items are disclosed by segment they provide adequate reconciliations.

8. AASB 8, paragraph 23.9. AASB 8, paragraph 24.10. AASB 8, paragraph 28.

0 5 10 15 20 25 30 35 40 45

Net interest income

Reversal of impairment losses

Impairment losses

Interest revenue

Income tax expense/ income

Share of P&L of associates and JVs (equity accounted)

Interest expense

Revenues from transaction with other operating segments

Depreciation and amortisation

Revenues from external customers

Number of entities disclosing this itemSource: KPMG

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

9 | KPMG Financial Reporting Insights: Operating Segment disclosures

Balance Sheet disclosuresEntities are only required to disclose information about their segment assets and liabilities if this data is included in the information regularly provided to the CODM.11 Of the 41 entities with segment disclosures, only 46 percent disclosed their segment assets and out of those entities 68 percent disclosed their segment liabilities.

There was a wide variety of reconciling items between segment assets and liabilities and the consolidated balance sheet balances including tax assets and liabilities, cash accounts and interest bearing liabilities.

Entity wide disclosuresIn addition to the segment disclosures discussed above, AASB 8 also requires a number of entity wide disclosures that should be made regardless of whether an entity has one or more reportable segments. These disclosures relate to sales by product line; local and international sales and major customers.

Of the four entities with only one segment, none made any disclosures regarding revenue by product lines. As they all operated in a single country the disclosures related to geographical areas was not relevant and only one entity made any disclosure regarding major customers that contribute to more than 10 percent of their revenue.

Any entity with a single segment should be aware of the additional entity wide disclosures required by AASB 8 and ensure that they are appropriately included in their financial reports where material.

Products and servicesAASB 8 requires that an entity report the revenues from external customers for each product and service, or each group of similar products and services.12

For the 41 entities disclosing more than one reportable segment, there appeared to be significant inconsistencies in the way that this requirement was interpreted. Some entities that determined their segments based on products and services provided no additional disclosures whilst other entities provided additional break downs of their revenue to individual product lines.

For example, one company in the oil and gas industry disclosed two segments determined by product/service line, one related to refining and the other to retail and wholesale. The entity then included an additional breakdown of revenues by each type of product such as crude, petrol and diesel.

Whether or not the disclosures made by an entity at a segment level are adequate for the specific product entity wide disclosures would depend on the following:

• where an entity has aggregated segments, whether these aggregated segments reflect individual product lines

• the level of disaggregation used to determine segments by product or service, and whether they truly reflect individual product lines or a broader product type

• if revenue disclosed in the segment note has been determined on a non-IFRS basis this would not satisfy the entity wide disclosure requirements which are required to be based on the statutory consolidated revenue numbers.

Information about geographical areasAASB 8 requires an entity to disclose revenue and non-current assets at a minimum from their country of domicile and the rest of the world, including the basis for attributing revenues from customers to individual countries.13

Inconsistencies similar to those noted in the product and service disclosures above were observed in the disclosures regarding geographical areas. Many entities that prepared their segment report based on geographical location did not provide any additional information regarding their revenue or non-current assets by geography.

Two key observations were identified from the approach taken by entities:

1. In some instances the reportable segment disclosed would be Australia & New Zealand. Strictly speaking, for an Australian domiciled entity, this would not satisfy the requirement to disclose the revenues and non-current assets from Australia separately to those internationally.

2. In some instances entities may have a single international reportable segment that aggregated the results of numerous countries. This international segment would often represent a significant proportion of sales yet no further breakdown was provided under these geographical disclosure requirements, even though the standard requires individual country disclosures where revenues or non-current assets attributable that country are material.

11. AASB 8, paragraph 23.12. AASB 8, paragraph 32. 13. AASB 8, paragraph 33.

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

10 | KPMG Financial Reporting Insights: Operating Segment disclosures

Major customersAASB 8 requires an entity to disclose the extent of its reliance on its major customers. Where revenue from a single customer amounts to 10 percent or more of total revenues this fact is required to be disclosed along with the amount of revenue from each such customer and the segment or segments reporting this revenue.14

Number of customers entity disclosed with revenues > 10% of the entity’s total revenue

Source: KPMG

Other

Not disclosed

1 - 2

0

Other

Not disclosed

1 - 2

0

69%

20%

7%

4%

Of the 45 entities reviewed, 69 percent did not include any disclosures regarding their reliance on major customers and 20 percent disclosed that there were no individual customers contributing to more than 10 percent of their revenues. Only 7 percent disclosed the number of entities that generated more than 10 percent of revenue and the amount of that revenue. The remaining 4 percent disclosed the total amount or percentage of revenue that came from their major customers, but did not identify how many customers this represented.

ImpairmentA relationship exists between operating segments and impairment assessments and disclosures in financial reports as goodwill cannot be allocated to a cash generating unit (CGU) larger than an operating segment before aggregation. AASB 136 Impairment of Assets requires an entity with goodwill to disclose the carrying amount of goodwill allocated to each CGU or group of CGUs.

Relationship between CGUs and segments

Source: KPMG

Unable to determine the relationship between CGU and segment

CGU at a lower level of aggregation than a segment

CGU same level as segment

Did not disclose allocation of Goodwill to CGU

Unable to determine the relationship between CGU and segment

CGU at a lower level of aggregation than a segment

CGU same level as segment

Did not disclose allocation of Goodwill to CGU

16%3%

29%

52%

Of the 45 entities reviewed, 38 had goodwill. Of these, six did not disclose the amount of goodwill that was allocated to individual CGUs, however two of these entities did provide a narrative description of their CGUs. 52 percent disclosed CGUs or groups of CGUs consistent with their segments and 29 percent of entities disclosed CGUs that were at a lower level than their segments. One entity had allocated goodwill to individual subsidiaries and it was not clear how these related to their segments which were determined based on their product lines.

Given ASIC’s continuing focus on impairment and impairment disclosures15 it would be advisable to ensure the allocation of goodwill to CGUs is appropriately disclosed and how that allocation interacts with the segments is clear to reduce potential questions from the regulator.

14. AASB 8, paragraph 34. 15. ASIC 16-174MR ASIC calls on directors to apply realism and clarity to financial reports

RU-004 ASIC focuses for 30 June 2016

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

11 | KPMG Financial Reporting Insights: Operating Segment disclosures

Operating and Financial Review required by the Corporations ActSection 299A of the Corporations Act requires a listed entity’s directors’ report to include information that members of the entity would reasonably require to make an informed assessment of the entity’s operations, financial position, business strategies and prospects for future financial years. This information is normally contained in what is referred to as an operating and financial review (OFR) or management commentary forming part of the directors’ report. The OFR provides an entity the opportunity to tell their story and focus a user’s attention on the contributing factors to their performance as seen through management’s eyes.

An operating or reportable segment as defined by AASB 8 is a representation of how the CODM views an entity and assesses its performance to make decisions about the allocation of resources.

Consequently, there are clearly similarities between the definition of a segment and what would be discussed in an OFR. As part of our review we have compared the disclosures made in the segment report to the discussion and analysis in the OFR in the directors’ report. Our findings were mixed as noted in the graph below.

Comparision of OFR analysis and segment notes

Source: KPMG

OFR analysis consistent with segment note

OFR analysis based on different disaggregation to segments

OFR analysis based on whole of business

OFR analysis consistent with segment note

OFR analysis based on different disaggregation to segments

OFR analysis based on whole of business

78%

13%

9%

In line with our expectations, 78 percent of entities provided an analysis in their OFR consistent with the segments disclosed in the financial report. Of these, four provided additional analysis on a different basis with:

• Three providing additional details, for example, a mining company providing analysis on individual mine sites where their segments were by country.

• One providing analysis based on their geographical segments and then also providing additional analysis based on the product type.

It is not unusual to see additional analysis to that contained in the segment report in the OFR as although the CODM may focus on one particular way of analysing the business, other methods may also be relevant and beneficial in assisting a user to understand the key drivers of performance in the period.

Of the entities reviewed, 13 percent discussed their performance in the OFR only on a consolidated group basis. They did not discuss the business performance at a segment level. This suggests that although they provide the analysis in their segment note to comply with the accounting standards, this is not how management view the business or consider it more relevant for the users of the financial report to understand the performance and operations of the entity in its entirety.

In 9 percent of cases entities did not discuss their segments in the OFR as disclosed in the segment note. Instead they disaggregated their business on a different basis and discussed the performance of the business based on this different disaggregation. Using an inconsistent basis between the segment note and OFR for analysing an entities performance could raise questions on the appropriateness of an entities identification of their reportable segments. We expect how the CODM views and assesses the business would also be relevant to a members or users understanding of the business’ performance.

Of the 35 entities that analysed the performance of their business in their OFR consistent with their segment note, 85 percent used a consistent measure of profit in the OFR compared to the segment note. Given the measure used in the segment note is meant to reflect the measure that is regularly reported to the CODM and is used to monitor performance and make decisions about resource allocation, we would expect similar measures to be the focus of discussion in the OFR, otherwise this may raise questions on the appropriateness of the disclosures made in the segment note.

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

12 | KPMG Financial Reporting Insights: Operating Segment disclosures

Integrated ReportingSegment reporting by geography and/or product is important for companies as they start to explain their value story using the IIRC’s integrated reporting framework.

The integrated report starts by explaining the company’s business model, the markets in which it operates and its strategy to create and preserve value for its shareholders and other stakeholders. The discussion in the integrated report then focuses on explaining value creation at the group level, including why certain segments are important for ongoing growth, risk mitigation etc. For example, in GE’s 2015 Integrated Summary Report, we clearly see Jeffrey Immelt, the Chairman and Chief Executive Officer, explain how the group has been transformed, at the group and segment level, to create value for shareholders. He explains why GE has exited most of the financial services business segment and re-focused as a high-tech leader, selling more than half the company in the process.

As more companies develop their integrated reports, the importance of business segments to long term business value will be more clearly explained, not in tables, but more around their importance to the business model and long term creation of value.

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

13 | KPMG Financial Reporting Insights: Operating Segment disclosures

MethodologyTo provide observations relevant across a broader cross section of entities, we focused this review on 45 companies across the ASX200. These 45 entities were randomly selected for a review from a list of ASX200 entities that was determined based on their market capitalisation as at 31 May 2016.

ASX ranking Year end GIC Industry Group

ASX50: 8 companies

• June (5)• September (1)• December (2)

• Banks (1)• Energy (2)• Insurance (1)• Real Estate (2)• Transportation (1)• Materials (1)

ASX51-100: 15 companies

• March (1)• June (8)• July (1)• August (1)• September (2)• December (2)

• Banks (1)• Consumer Services (1)• Diversified Financials (2)• Energy (1)• Food, Beverage & Tobacco (1)• Materials (2)• Real Estate (1)• Retailing (1)• Software & Services (1)• Telecommunication Services (1)• Utilities (3)

ASX101-150: 12 companies

• March (2)• April (1)• June (7)• December (2)

• Commercial & Professional Services (1)• Consumer Services (1)• Food & Staples Retailing (1)• Health Care Equipment & Services (1)• Household & Personal Products (1)• Insurance (1)• Materials (2)• Media (1)• Retailing (2)• Software & services (1)

ASX151-200: 10 companies

• June (8)• July (1)• December (1)

• Commercial & Professional Services (1)• Consumer Durables & Apparel (1)• Consumer Services (2)• Energy (1)• Media (1)• Pharmaceuticals, Biotechnology & Life Sciences (1)• Software & Services (1)• Telecommunication Services (1)• Transportation (1)

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

14 | KPMG Financial Reporting Insights: Operating Segment disclosures

Reconciling item Description

Interest Interest expense on borrowings, the unwind of discounts on provisions, and interest income on deposits.

Impairments Impairments relating to property, plant and equipment; goodwill and other intangibles; equity accounted investments; and write downs of inventories.

Depreciation and amortisation Adjustments relate to excluding specific items of depreciation or amortisation such as amortisation on acquired intangibles.

Tax Tax on significant/adjusting items; recognition of deferred tax assets; costs/benefits associated with resolution of uncertain tax positions with the tax office; or total tax expense/benefit for the period.

Transaction and restructure costs Costs relating to acquisitions of businesses, disposals, business restructures, initial public offerings and takeover defence.

Corporate Expenses Costs relating to the head office function, in some instances it may have included central funding costs and investor relation costs. Entities provided minimal to no details of the composition of corporate costs.

Derivatives and hedging Gains and losses relating to fair value adjustments on derivative financial instruments and the impacts of economic hedges (accounting for derivatives that do not qualify for hedge accounting as if they did qualify).

Remuneration Adjustments relating to voluntary redundancies; share based payment expenses – excluding all share based payments expenses or reflecting cash cost; and remuneration adjustments associated with IPO’s.

Elimination of discontinued operations

Discontinued operations as disclosed on the income statement are eliminated to reconcile back to profit from continuing operations.

General net eliminations Entities provided one overarching reconciling item, with no further break down or explanation.

Unallocated amounts Amounts not attributable to a reportable segment, this may have been from other operating segments or corporate operations.

Claims and legal proceedings Costs associated with court cases or other legal proceedings and the costs attributable to recognising provisions in relation to legal proceedings.

Gains and losses on purchase or sale of investments

Gains and losses on sale of assets, businesses, subsidiaries and associates; gains on business combinations (bargain purchases); and gains on the acquisition of equity accounted investments.

Share of profits of equity accounted investments

Profits of associates or joint ventures as disclosed on the face of the income statement.

AppendixDetails of the types of reconciling items discussed in the Reconciliations of segment disclosures to consolidated results section above.

The information contained in this document is of a general nature and is not intended to address the objectives, financial situation or needs of any particular individual or entity. It is provided for information purposes only and does not constitute, nor should it be regarded in any manner whatsoever, as advice and is not intended to influence a person in making a decision, including, if applicable, in relation to any financial product or an interest in a financial product. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

To the extent permissible by law, KPMG and its associated entities shall not be liable for any errors, omissions, defects or misrepresentations in the information or for any loss or damage suffered by persons who use or rely on such information (including for reasons of negligence, negligent misstatement or otherwise).

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Liability limited by a scheme approved under Professional Standards Legislation.

July 2016. NSW N14318AUD

Contact us

For more information on this publication please contact:

Zuzana PaulechPartnerDepartment of Professional Practice Audit & Assurance+61 2 9335 7329 [email protected]

Kristen HainesManagerDepartment of Professional Practice Audit & Assurance+61 3 9288 5184 [email protected]

For more information on integrated reporting please contact:

Nick RidehalghPartnerAudit & Assurance+61 2 9455 9312 [email protected]

Simon DuboisPartnerAudit & Assurance+61 3 9288 6927 [email protected]

kpmg.com.au