key findings regulations survey - fund platform...

TRANSCRIPT

Key findingsRegulations Survey

November 2015

Survey realized with and thanks to the

support of SWIFT

Fund Platform Group

Thank you for your participation

Fund Platform Group - SWIFT: Regulation Survey 2

THE FOLLOWING KEY FINDINGS ARE FROM A SURVEY OF FUND PLATFORM GROUP AND THEIR CLIENTS.

This survey is a joint research collaboration between The Fund

Platform Group and SWIFT, the leader in secured financial communication. The survey logistic was

conducted by SWIFT and SWIFT assembled the data results .

The survey was conducted over a 6 weeks period throughout September

and October 2015 among some of the most influential platform groups, fund buyers and fund sellers across Europe.

It sought the opinions of key players in the platform industry, regarding future developments, challenges and growth

outlook.

To learn more about this research, contact us:

Valérie Letellier

Market Manager – [email protected]

Richard Jones

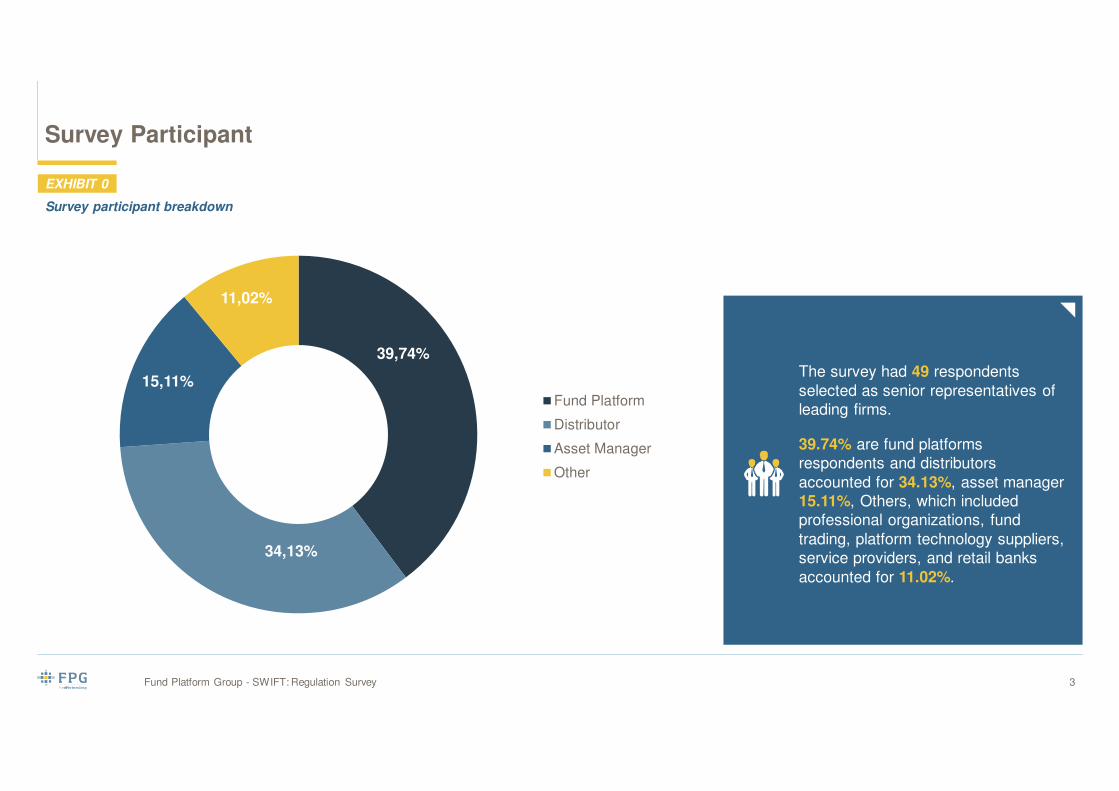

Survey Participant

Fund Platform Group - SWIFT: Regulation Survey 3

EXHIBIT 0

Survey participant breakdown

Fund Platform

Distributor

Asset Manager

Other

39,74%

34,13%

15,11%

11,02%

The survey had 49 respondents

selected as senior representatives of

leading firms.

39.74% are fund platforms

respondents and distributors

accounted for 34.13%, asset manager

15.11%, Others, which included

professional organizations, fund

trading, platform technology suppliers,

service providers, and retail banks

accounted for 11.02%.

Key takeaways – Executive summary

Fund Platform Group - SWIFT: Regulation Survey 4

High impact of MIFID II regulations

MIFID II impacts to the funds industry are so important that they may modify its landscape and

possibly require it to re-invent part of itself. A year before its effective implementation and despite

the fact that it has been around since a few years most of the respondents are still assessing the

impacts or are in the process of defining their strategic axes (94,86%). This is due to some

remaining uncertainties on the final text but most probably to the fact that the consequence are so

wide that they are not totally integrated in the transversal picture across industry actors.

Rebate will continue drive growth in the market

60.56% of the respondents are stating that the rebate will remain the dominant compensation

model for the funds distribution in Europe within the next 3 years. This is slightly lower than last

year’s result that was at 68.8 %. Industry players are assessing alternative remuneration models

and are adapting to the idea that the trend is in favour of transparency on fees and remunerations.

Finally, 49.98% are still stating that banning the rebates will have no financial impact on the cost of

funds for investors. However they are now 30.02% to consider it will make cost of Funds cheaper

for investors. They were 14% only in 2014. This is another clear trend toward the recognition of the

fact that regulation might be meeting its objective to improve the cost of Funds.

Key takeaways – Executive summary

Fund Platform Group - SWIFT: Regulation Survey 5

Due diligence

After the remuneration models, due diligences and legal agreements across the fund distribution

chain are certainly amongst the key considerations derived from MIFID II and fund distribution.

77% are confirming that due diligences are a costly process impacting their profitability and 38,7%

have issues with investing in this process. The due diligence cost is identified as a key challenge to

the industry. Smaller players will not be able to cope with the costs of this requirement. They will

have to rely on partners or on mutualized solutions.

Digital transformation

Innovation and transformation are the only options for the industry players to overcome the

challenges created by MIFID II regulations. D2C and Robot Advisors are 2 innovative solutions

making some buzz in 2015.

D2C: With 57% believing in its emergence, there is no strong consensus on the future success of

D2C solutions promoted directly by AM.

Robot advisors: With close to 95% considering robot advisors will be present in the retail space

and close to 60% in the Wealth Management space, there is a strong consensus that robot-

advisors are the innovative solution for providing low-cost advise to retail investors. It is making

sense, especially considering the UK experience on retrocessions ban. In the UK, for cost reasons

, advisors and banks translated “retrocession ban” into “banning advise to retail customer ”. Robot-

advisors are a low cost solution for addressing the retail advise profitability issue.

Fund Platform Group - SWIFT: Regulation Survey6

Part 1 : MIFID

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 7

EXHIBIT 1

MIFID readiness

HOW PREPARED ARE YOU TO COMPLY WITH MIFID II REQUIREMENTS REGARDING THE DISTRIBUTION OF MUTUAL FUNDS?

0% 20% 40% 60% 80% 100%

We have already adapted our portfolio allocation models

We have already adapted our commercial & remunerationmodels

We will opt for the Independent status (vs tied) under MIFID II

We have already adapted our operational model

We Have already deployed or prepared reporting solutions oncosts and charges

We already offer low fees shares classes

We are defining our strategic axes

We are assessing the impacts

Yes No

The survey confirms that while low fees

share classes are available in

approximately 50% of the platforms,

portfolio allocations and remunerations

models have not yet integrated the use

of these share classes. Less than 25%

will opt for the status of Independent

Adviser that involves a rebate free

model. This explains the standby on

the remuneration model confirmed on

the following page

While MIFID II is seen as one of the

most challenging regulation to the

Fund Industry, 70% of players seem

not to be ready to the coming tsunami.

30% only have already adapted their

operating model.

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 8

EXHIBIT 2

Rebate as compensation model

0%

10%

20%

30%

40%

50%

60%

70%

Insurance Unit Linked Private Banks Retail Bank Intermediating FundPlatforms

Independent FA/RetailPlatforms

Funds of funds

UK

Germany

France

Belgium

Italy

Spain

Netherlands

60.56% of the respondents agree that the rebate will remain the dominant compensation model for the funds distribution in Europe within

the next 3 years, especially in France, UK* and Germany. Moreover, There is a clear consensus (81.32%) on the fact that the AM need to

have formal agreements in place to ensure a proper cascading of responsibilities across the whole distribution value chain. Even with

intermediaries not remunerated by the AM. This confirms last year’s expectation that agreement terms between AM and Fund Buyers will

need to be reviewed. Distribution agreements will have to integrate all stakeholders in the processing chain and/ or new agreements will

have to be signed with intermediaries that were not considered until now. It concerns custodians, ICSDs, order routing platforms

Finally, 49.98% of the respondents stated that banning the rebates will have no financial impact on the cost of funds, whereas 30.02%

(against 14% in 2014) consider that banning the rebates will make it cheaper.

DO YOU THINK REBATES WILL CONTINUE TO BE THE DOMINANT COMPENSATION MODEL FOR DISTRIBUTION IN CONTINENTAL EUROPE WITHIN THE NEXT 3 YEARS?

* Life Funds and discretionary portfolio are not part of RDR

0%

10%

20%

30%

40%

50%

60%

70%

80%

Insurance Unit Linked Private Banks Retail Bank Intermediating FundPlatforms

Independent FA/RetailPlatforms

Funds of funds

UK

Germany

France

Belgium

Italy

Spain

Netherlands

Nordics

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 9

EXHIBIT 3

MIFID towards passive funds?

While last year’s survey was believing at 75% in a moderate switch towards passive funds, this year’s survey has a more mitigated view

that is below 50% in average. The industry has matured on the pro and con’s of passive versus actives and even if the growth of

passives keeps strong, the industry has made his view on where this products are relevant or not. UK, Germany and France are the

countries where passive products are showing the fastest growth trend in average.

DO YOU EXPECT MIFID II TO DRIVE A SWITCH TOWARDS PASSIVE FUNDS?

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Insurance Unit Linked

Private Banks

Retail Bank

Un-intermediated Sales

Intermediating Fund Platforms

Independent FA/Retail Platforms

Funds of funds

Execution-only platform (D2C)

Increase Remain the same Decrease

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 10

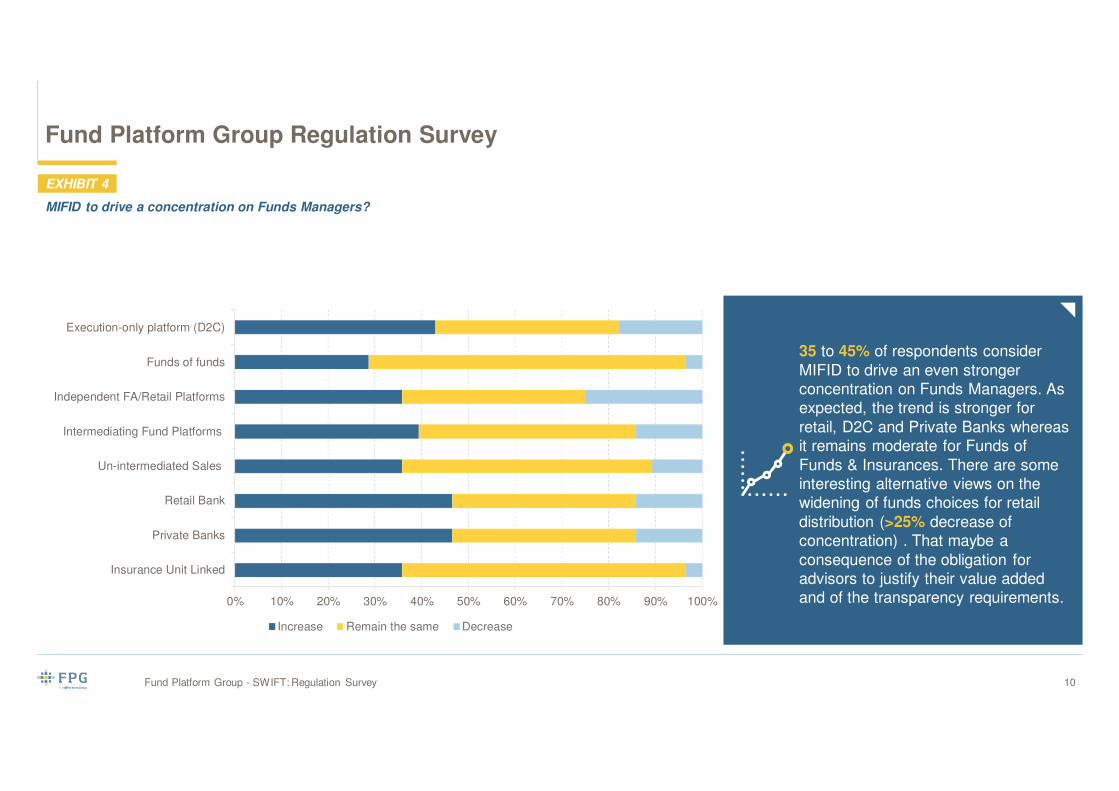

EXHIBIT 4

MIFID to drive a concentration on Funds Managers?

35 to 45% of respondents consider

MIFID to drive an even stronger

concentration on Funds Managers. As

expected, the trend is stronger for

retail, D2C and Private Banks whereas

it remains moderate for Funds of

Funds & Insurances. There are some

interesting alternative views on the

widening of funds choices for retail

distribution (>25% decrease of

concentration) . That maybe a

consequence of the obligation for

advisors to justify their value added

and of the transparency requirements.

Fund Platform Group - SWIFT: Regulation Survey11

Part 2: Due Diligence

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 12

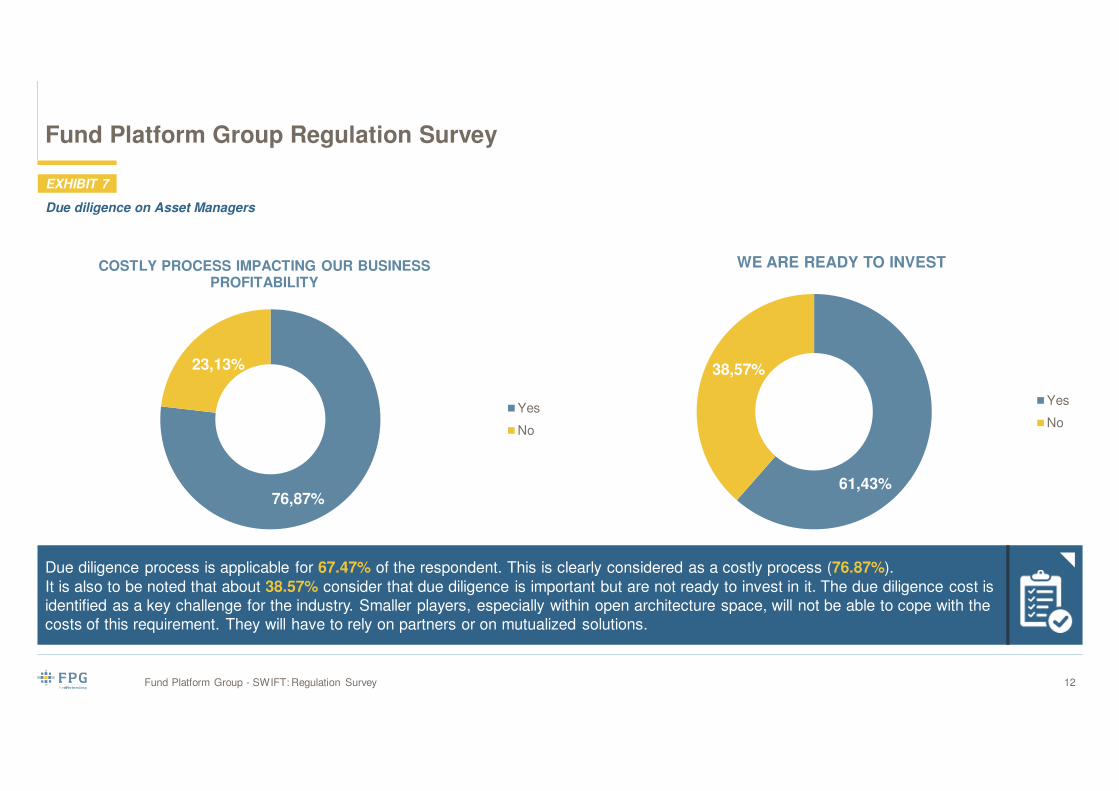

EXHIBIT 7

Due diligence on Asset Managers

COSTLY PROCESS IMPACTING OUR BUSINESS PROFITABILITY

Yes

No

76,87%

23,13%

WE ARE READY TO INVEST

Yes

No

61,43%

38,57%

Due diligence process is applicable for 67.47% of the respondent. This is clearly considered as a costly process (76.87%).

It is also to be noted that about 38.57% consider that due diligence is important but are not ready to invest in it. The due diligence cost is

identified as a key challenge for the industry. Smaller players, especially within open architecture space, will not be able to cope with the

costs of this requirement. They will have to rely on partners or on mutualized solutions.

Fund Platform Group - SWIFT: Regulation Survey13

Part 3: Evolution of the distribution

process

The data are clearly getting more and more important to answer to new regulation hitting the funds industry. The value will come from the

data being managed and the way service provider will use it for the benefits of the funds and its shareholders.

There is certainly opportunity to have new solution that allow to manage complexity.

Impacts for data and services providers...

Fund Platform Group Regulation SurveyAnalysis & restitution of open questions

Fund Platform Group - SWIFT: Regulation Survey 14

Although few answers were considering the fees as being a discouragements for small retail client, respondents view that the overall

costs will remain the same but distributed in other ways or at least to be more justified. The industry players also consider that the model

will continue to be dominated by rebates, especially in the distribution channel related to financial advisors.

Remuneration of the distribution players

For product governance, the trend is clearly towards the need of a strong process to be put in place. Asset managers and distributor will

have to work closer to propose the right fund to each investor.

But so far, the lack of standard practice seems to be the issue that needs to be tackled in priority.

Product governance and its monitoring

The creation of multiple share classes is considered by respondent to be confusing, complicated and further creation could be harmful

due to a lack of clarity. The benefits of creating multiple share classes should be clearly balanced beforehand.

Creation of multiple share classes

Fund Platform Group - SWIFT: Regulation Survey15

Part 4: Digital Transformation

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 16

EXHIBIT

Digital Transformation

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00%

Yes, in Belgium

Yes, In Switzerland

Yes, in Netherlands

Yes, in the UK

Yes, in France

Yes, in Germany

Yes, in Italy

Yes, in Spain

No

No view at all

With only 57% of respondant believing

in its emergence, D2C distribution

solutions promoted directly by AM are

not clearly seen as the innovative

solutions that will arise. UK is the only

country where more than 50% of the

believers in D2C state that D2C will

emerge. The Netherland comes next

with 38,87% only

DO YOU BELIEVE THERE WILL BE AN EMERGENCE OF D2C DISTRIBUTION THROUGH ONLINE SOLUTIONS PROMOTED BY ASSET MANAGERS (SELLING DIRECTLY TO RETAILS)?

Fund Platform Group Regulation Survey

Fund Platform Group - SWIFT: Regulation Survey 17

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

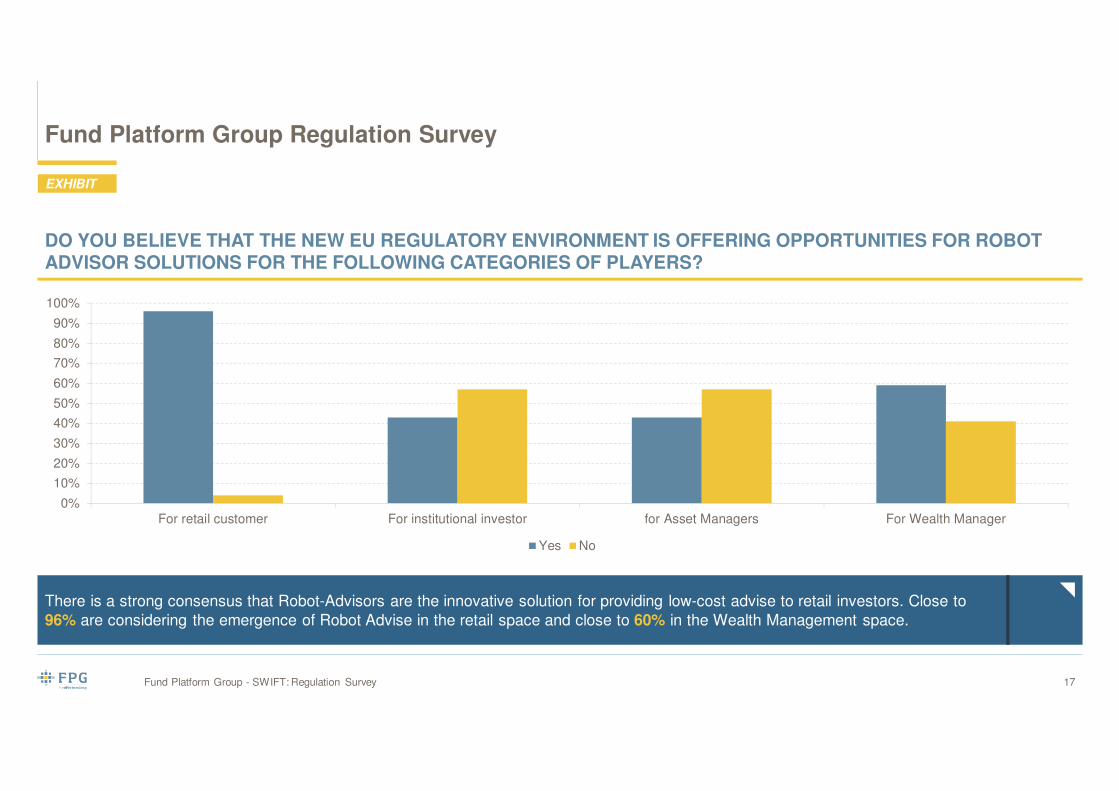

For retail customer For institutional investor for Asset Managers For Wealth Manager

Yes No

EXHIBIT

There is a strong consensus that Robot-Advisors are the innovative solution for providing low-cost advise to retail investors. Close to

96% are considering the emergence of Robot Advise in the retail space and close to 60% in the Wealth Management space.

DO YOU BELIEVE THAT THE NEW EU REGULATORY ENVIRONMENT IS OFFERING OPPORTUNITIES FOR ROBOT ADVISOR SOLUTIONS FOR THE FOLLOWING CATEGORIES OF PLAYERS?

http://fundplatformgroup.com/

12, rue Erasme

L-1468 Luxembourg

Tel: +352 46 36 60 - 210