key concepts = “level 0” - unsd — welcome to unsd of environmental-economic accounting key...

TRANSCRIPT

System of Environmental-Economic Accounting

Key Concepts = “Level 0”

Project: Advancing the SEEA

Experimental Ecosystem Accounting

System of Environmental-Economic Accounting

Overview

1. SEEA-EEA Training (Level 0)

• Overview of training modules

• Basic concepts:

▫ Ecosystems as “Assets”

▫ Ecosystem Services Cascade

▫ Accounting Principles

▫ Ecosystem Accounting is Spatial

• Accounts

• Tools

System of Environmental-Economic Accounting

SEEA-EEA Training

• Concepts, Accounts and Tools

• Flexible and modular (don’t need all Accounts and Tools)

• Three levels:

• Level 0 (All participants)

• Level 1 (Compiling)

• Level 2 (Providing data, country examples)

• Links to related training materials:

• Secretariat for the Convention on Biological Diversity (SCBD)

• Quick Start Package (QSP): includes GIS exercises

• World Bank WAVES

3

System of Environmental-Economic Accounting

SEEA-EEA Training Level 0

• Learning objectives

• Understand the basic concepts in ecosystem

accounting

• Understand the structure, data requirements and

uses of the SEEA-EEA accounts

• Understand the basic tools used to compile the

SEEA-EEA accounts

• For technical and scientific experts, this is:

• Preparation for Levels 1 & 2

• For policy experts and supporters you will:

• Understand how to use the accounts and who to

engage in the discussion

4

System of Environmental-Economic Accounting

SEEA-EEA Training Level 0

• Basic concepts and definitions

• Ecosystems as “Assets”

• The Ecosystem Services “Cascade” • Ecosystem structure and processes, function,

services, benefits and values

• Accounting (not just “counting”) Principles • Assets, stocks and flows

• Balancing the books

• Ecosystem Accounting is Spatial • Geographic information systems (GIS)

5

System of Environmental-Economic Accounting

Ecosystem assets, a definition

Ecosystem assets are spatial areas containing

a combination of biotic and abiotic components

and other characteristics that function together

(SEEA-EEA Sections 2.31, 4.1)

A forest is an area that: • Can be located on a map (spatial)

• Contains trees, shrubs, grasses, soil biota, birds,

mammals, insects… functioning together with

• The soil, water, geology (rocks), sunlight, wind…

6

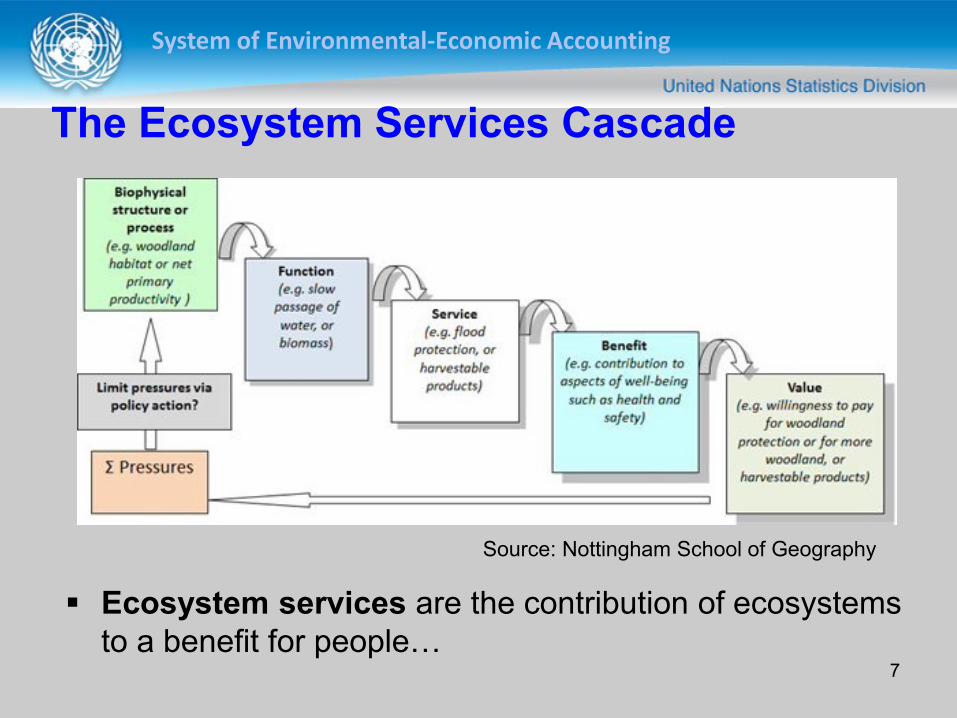

System of Environmental-Economic Accounting

The Ecosystem Services Cascade

7

Ecosystem services are the contribution of ecosystems

to a benefit for people…

Source: Nottingham School of Geography

System of Environmental-Economic Accounting

Accounting principles…

Apply to environmental data, too… Double entry accounting:

Beginning & end of time period reconcile changes

Compare two sources reconcile and find errors

Time of recording: Referring to same time period (accounting period)

Unit of measurement: Same units (physical or monetary)

Reconciliation and aggregation

Consistent valuation rules: Market price: Basic, producer, purchaser

Consistent concepts and classifications

Stock Flow (Asset Service)

8

System of Environmental-Economic Accounting

Balancing the books of environmental assets

9

Assets Services

Waste & degradation

Economy and

well-being Regeneration

Time 1

System of Environmental-Economic Accounting

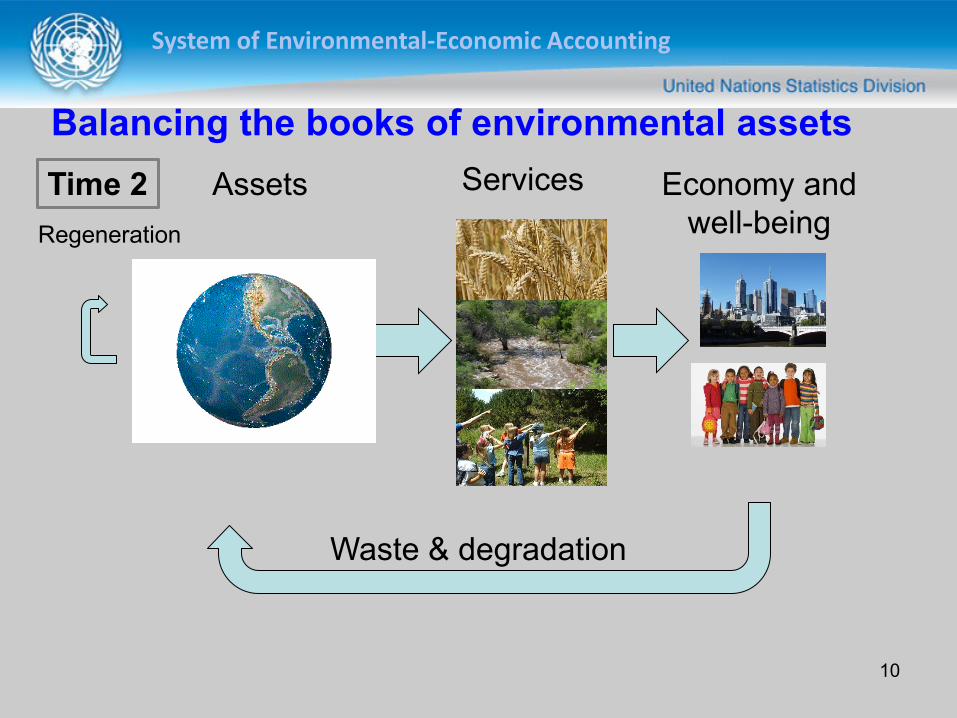

Balancing the books of environmental assets

10

Assets Services

Waste & degradation

Economy and

well-being Regeneration

Time 2

System of Environmental-Economic Accounting

Ecosystem accounting is spatial

Ecosystems are different and function differently

depending on where they are

Their capacity to supply services depends on

their location

The benefits of many services depends on

whether or not the ecosystems are accessible

Therefore…Ecosystem accounting needs to

integrate spatial and non-spatial data

For example, wetlands in northern Canada may

have the capacity to purify water, but there is no

population there to benefit from it. 11

System of Environmental-Economic Accounting

Ecosystem accounting is spatial

Geographic information systems (GIS) • Manage spatial information as layers

• Have tools to integrate spatial information: ▫ Overlay different data where space is the common

denominator

▫ Aggregate point information (e.g., water sampling station) to

larger areas (polygons)

▫ Attribute information from larger areas to smaller ones

(downsampling)

▫ Geospatial statistics (interpolation, modelling)

• Generate tables based on common properties (e.g.,

land cover and land cover change)

12

System of Environmental-Economic Accounting

Pop quiz!

What is an important ecosystem type in your

country and what services does it provide?

What are examples of spatial data that you may

wish to integrate into ecosystem accounting?

Why is GIS a useful tool for ecosystem

accounting?

13

System of Environmental-Economic Accounting

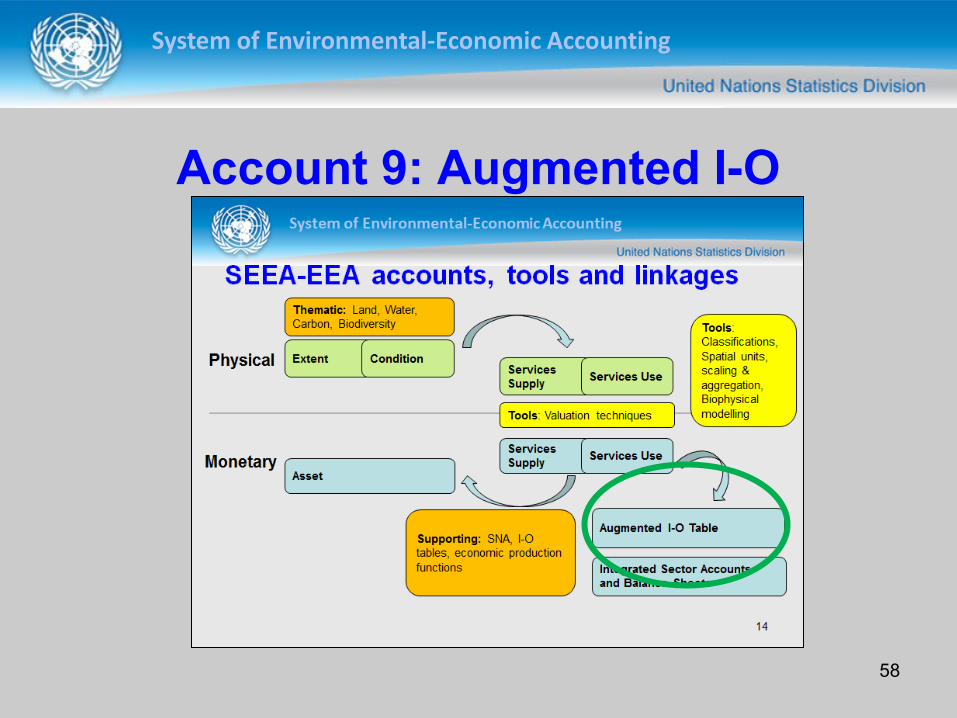

SEEA-EEA accounts, tools and linkages

14

Extent Condition Services

Supply Services Use

Services

Supply Services Use

Asset

Augmented I-O Table

Integrated Sector Accounts

and Balance Sheets

Tools:

Classifications,

Spatial units,

scaling &

aggregation,

Biophysical

modelling

Thematic: Land, Water,

Carbon, Biodiversity

Tools: Valuation techniques

Supporting: SNA, I-O

tables, economic production

functions

Physical

Monetary

System of Environmental-Economic Accounting

SEEA-EEA Accounts and Tools Today’s session presents 2-4 slides on each topic:

15

Tools • Classifications

• Spatial units, scaling and

aggregation

• Biophysical modelling

• Valuation

Accounts • Ecosystem Extent Account

• Ecosystem Condition Account

• Thematic Accounts:

• Water Account

• Carbon Account

• Biodiversity Account

• Ecosystem Services Supply Account

• Ecosystem Services Use Account

• Ecosystem Capacity

• Augmented I-O Tables

• Integrated Sector Accounts and Balance Sheet

• Supporting information

System of Environmental-Economic Accounting

Account 1: Extent

16

System of Environmental-Economic Accounting

Level 0: Account 1: Extent

• What? • Ecosystem assets are spatial areas containing a combination

of biotic and abiotic components and other characteristics that

function together (SEEA-EEA Sections 2.31, 4.1)

• National coverage of land cover, land use, ownership

(terrestrial, freshwater, coastal and marine areas)

• Why? • Land management, conservation policies

• Spatial foundation for other accounts

basis for allocating macro data to spatial units

• Builds on SEEA-CF (land, forest, water)

• Indicators:

• Land cover change where changes occurring

• Land cover/use intensity who owns it

17

System of Environmental-Economic Accounting

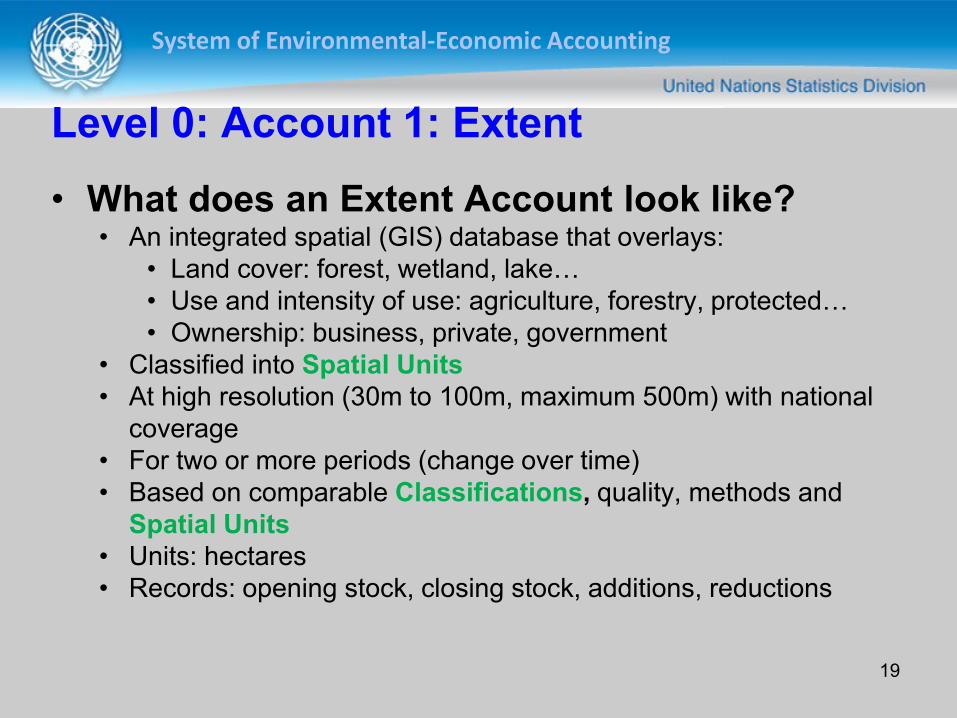

Level 0: Account 1: Extent

What does an Extent Account look like?

18

Cover

Ownership

Use

Maps Tables

Cover

Open

wetlands Total

Use Infrastructure Residential

Permananet

crops Maintenance Forestry Protected Infrastructure Aquaculture Maintenance

Ownership Government Private Private Private Private Government Government Private Government

Units

Opening Stock

Additions to Stock

Managed expansion

Natural expansion

Reductions to stock

Managed regression

Natural regression

Closing stock

Urban and associated

Rainfed herbaceous

cropland Forest tree cover Inland water bodies

hectares

Spatial units

Classifications

System of Environmental-Economic Accounting

Level 0: Account 1: Extent

• What does an Extent Account look like? • An integrated spatial (GIS) database that overlays:

• Land cover: forest, wetland, lake…

• Use and intensity of use: agriculture, forestry, protected…

• Ownership: business, private, government

• Classified into Spatial Units

• At high resolution (30m to 100m, maximum 500m) with national

coverage

• For two or more periods (change over time)

• Based on comparable Classifications, quality, methods and

Spatial Units

• Units: hectares

• Records: opening stock, closing stock, additions, reductions

19

System of Environmental-Economic Accounting

Level 0: Account 1: Extent

• What do you need to compile an Extent

Account? • GIS platform: software, protocols, spatial units

• Classifications: land cover, land use, ownership

• National level data:

• Existing land account would be useful

• Satellite: land cover, aerial photography

• Census: agriculture, population, settlements

• Forest inventories

• Hydrological, topographic (rivers, drainage areas, elevation,

coastlines)

• Cadastral (ownership, tax)

• Expertise:

• Land managers, ecologists, geographers (GIS, satellite

imagery, integration)

20

System of Environmental-Economic Accounting

Account 2: Condition

21

System of Environmental-Economic Accounting

Level 0: Account 2: Condition

• What? • Ecosystem condition reflects the overall quality of an

ecosystem asset, in terms of its characteristics. (SEEA EEA

paragraph 2.34)

• Why? • Policies to limit degradation of natural heritage, rehabilitation of

degraded ecosystems

• Links to capacity to produce services (Services Supply)

• Indicators:

• Indices of condition change over time where changes

• Good/bad condition (exceeding “safe” levels) where

22

System of Environmental-Economic Accounting

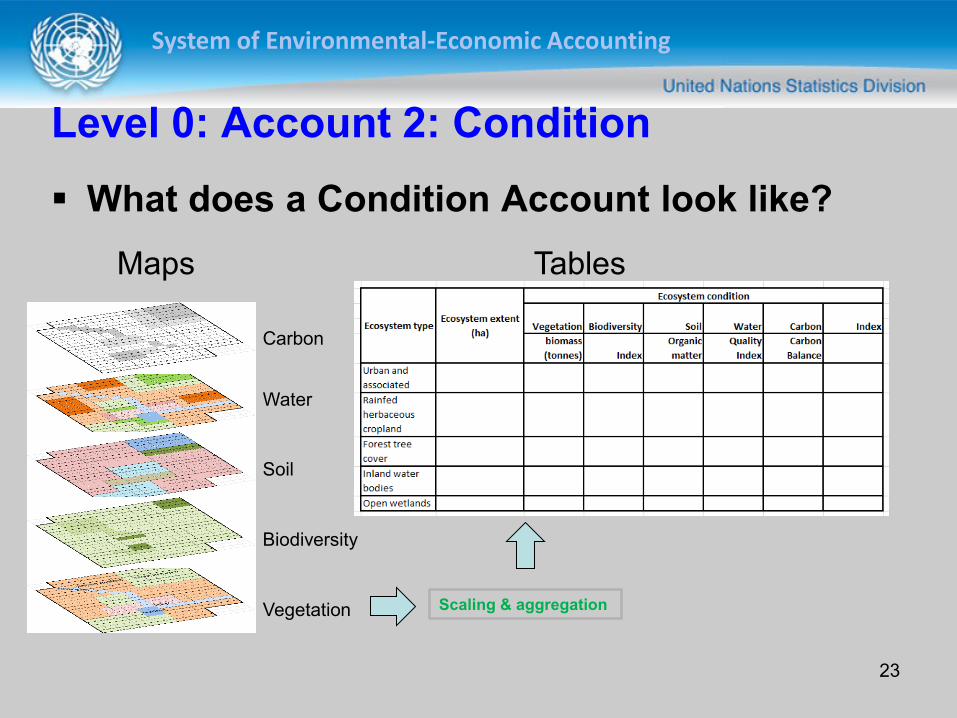

Level 0: Account 2: Condition

What does a Condition Account look like?

23

Maps Tables

Vegetation

Soil

Biodiversity

Water

Carbon

Scaling & aggregation

System of Environmental-Economic Accounting

Level 0: Account 2: Condition

• What does a Condition Account look like? • Spatially-detailed condition measures (quality or biophysical) for

each characteristic: • Vegetation

• Biodiversity (species abundance, diversity indices)

• Soil

• Water

• Carbon

• Air

• Overall measures (e.g., heterogeneity)

• Selected to reflect an area’s capacity to generate services

• Summarized in terms of an index

• Accounts for changes over time (accounting period)

• Attributes changes to drivers (natural and human) 24

System of Environmental-Economic Accounting

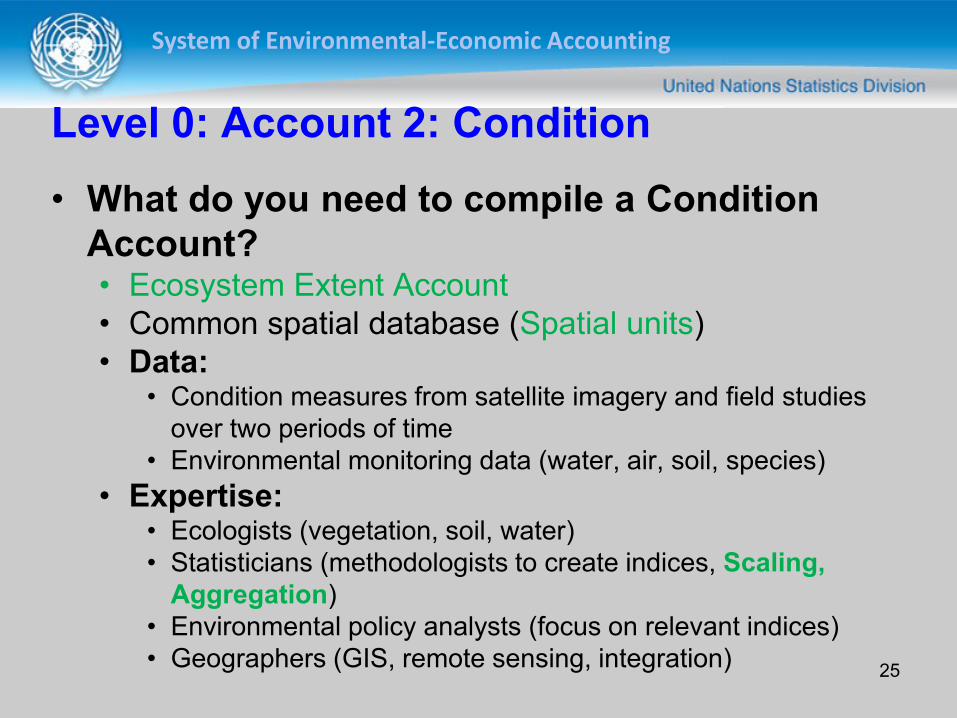

Level 0: Account 2: Condition

• What do you need to compile a Condition

Account? • Ecosystem Extent Account

• Common spatial database (Spatial units)

• Data: • Condition measures from satellite imagery and field studies

over two periods of time

• Environmental monitoring data (water, air, soil, species)

• Expertise: • Ecologists (vegetation, soil, water)

• Statisticians (methodologists to create indices, Scaling,

Aggregation)

• Environmental policy analysts (focus on relevant indices)

• Geographers (GIS, remote sensing, integration)

25

System of Environmental-Economic Accounting

Account 3: Water

26

System of Environmental-Economic Accounting

Level 0: Account 3: Water

• What? • Spatially-detailed version of SEEA-CF Water Account to capture:

• Inter-ecosystem flows of water (SEEA-EEA 4.62),

• Water quality and

• Supply/use for ecosystems

• Why? • Policies on water security, water quality, impacts of water

abstraction on ecosystems

• Links to other accounts (Condition, Services Supply & Use)

• Links to SEEA-CF; SEEA-WATER

• Indicators: • Local water supply/use, quality (use > supply?)

• Variability in supply, trends (droughts, floods)

27

System of Environmental-Economic Accounting

Level 0: Account 3: Water

What does a Water Account look like?

28

Maps Tables

Use

Rainfall

Hydrology

Spatial units

Classifications

Biophysical modelling

Socio-economic data

Agriculture,

forestry and

fishing

Mining &

quarrying,

manufacturing

and

construction

Electricity,

gas, steam

and air

conditioning

supply

Water

collection,

treatment and

supply Sewerage

Other

industries Households Total use

Source of abstracted water

Inland water resources

Surface water

Goundwater

Soil water

Total

Other water sources

Precipitation

Sea water

Total

Total use of abstracted water

Abstracted water

Distributed water

Own use

Use of water

mill ions m3

System of Environmental-Economic Accounting

Level 0: Account 3: Water

• What does a Water Account look like? • Spatially-detailed data on:

• Stock

• Supply, and

• Use including soil moisture & groundwater

• Water quality measures (contribution to Condition Account)

29

System of Environmental-Economic Accounting

Level 0: Account 3: Water

• What do you need to compile a Water

Account? • Ecosystem Extent Account

• SEEA-CF Water Account (national level)

• Common spatial infrastructure (Spatial Units)

• Data: • Spatially-detailed supply (rainfall, transfers)

• Use (abstraction, inter-ecosystem transfers);

• Water quality measures

• Expertise: • Geographers (GIS and remote sensing)

• Hydrologists

• Ecologists

• Climatologists

30

System of Environmental-Economic Accounting

Account 4: Carbon

31

System of Environmental-Economic Accounting

Level 0: Account 4: Carbon

• What? • Accounts for biocarbon as an asset (e.g., soil carbon)

• Carbon-related services (sequestration and storage)

• Carbon as a characteristic of ecosystem condition (productivity)

• Why? • Policies on climate change, low-carbon economy

• Assess changes in land cover and land use on carbon stocks

and sequestration

• Links to other SEEA accounts (Condition, Services Supply)

• Links to SEEA-CF (timber, soil, materials)

• Links to international guidelines (IPCC and REDD+)

• Indicators:

• Natural and human additions to carbon stock where

• Natural and human removals from carbon stock where

32

System of Environmental-Economic Accounting

Level 0: Account 4: Carbon

What does a Carbon Account look like?

33

Soil

Vegetation

Hydrology

Removals

Maps Tables

Scaling

Biophysical modelling

Geocarbon Biocarbon Oceans Atmosphere

Opening stock 10,000 400 20,000 100

Additions - 4 10 24

Reductions 10 5 9 14

Closing stock 9,990 399 20,001 110

billion tonnes C

System of Environmental-Economic Accounting

Level 0: Account 4: Carbon

• What does a Carbon Account look like? • Spatially detailed in terms of:

• Stock

• Additions and reductions of biocarbon

• Natural & human additions and removals

34

System of Environmental-Economic Accounting

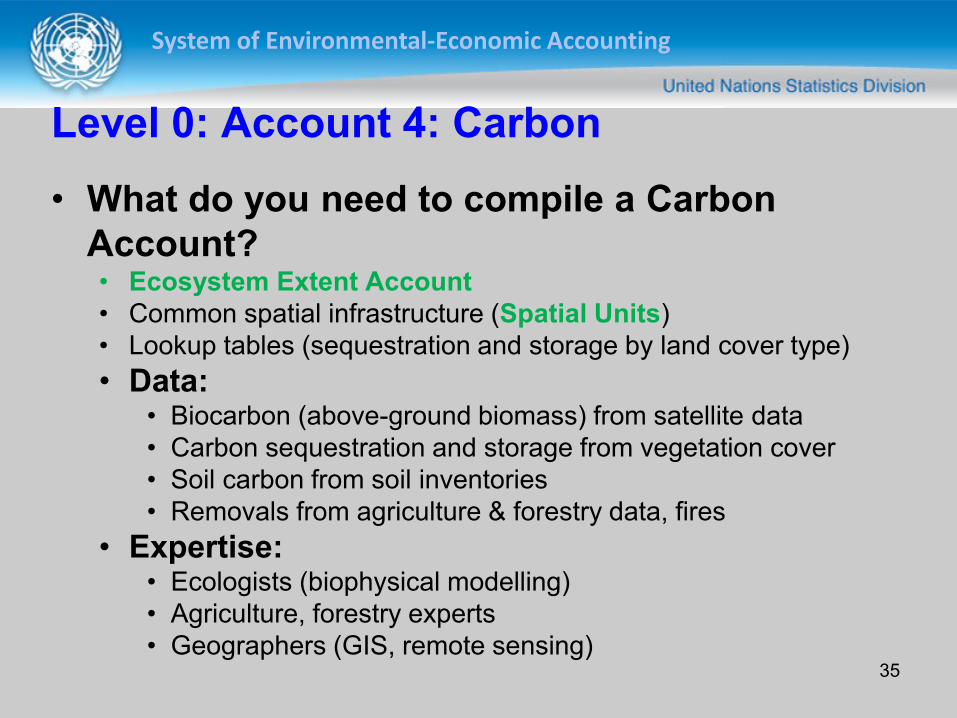

Level 0: Account 4: Carbon

• What do you need to compile a Carbon

Account? • Ecosystem Extent Account

• Common spatial infrastructure (Spatial Units)

• Lookup tables (sequestration and storage by land cover type)

• Data: • Biocarbon (above-ground biomass) from satellite data

• Carbon sequestration and storage from vegetation cover

• Soil carbon from soil inventories

• Removals from agriculture & forestry data, fires

• Expertise: • Ecologists (biophysical modelling)

• Agriculture, forestry experts

• Geographers (GIS, remote sensing) 35

System of Environmental-Economic Accounting

Account 5: Biodiversity

36

System of Environmental-Economic Accounting

Level 0: Account 5: Biodiversity

What do Biodiversity Accounts contain?

• Biodiversity information linked to areas of ecosystems

(from Extent Account)

• Spatially detailed information on key species:

• Abundance,

• Richness

• Conservation status

• Other characteristics (e.g., health)

• Spatially detailed summary statistics (index) on

species diversity (used in Condition Account)

37

System of Environmental-Economic Accounting

Level 0: Account 5: Biodiversity

Why would you create Biodiversity Accounts?

• To compare trends in biodiversity with economic and

social activity in a spatially explicit manner

• To link biodiversity information with other SEEA

accounts (Condition, Ecosystem Services

Generation)

• To meet global commitments under the Convention

on Biological Diversity’s Strategic Plan for Biodiversity

(2011-2020)

• To support sustainable development

38

System of Environmental-Economic Accounting

Level 0: Account 5: Biodiversity

What does a Biodiversity Account look like?

39

Maps Tables

Species 2

Species 1

Species 3

Ecosystems

Species data:

- abundance

- richness

- classification

- conservation status

- characteristics

- health

Priority species and ecosystems

Index

Species 1 Species 2 Species 1 Species 2

Pop. Ecosys.

Area

Pop. Ecosys.

Area

Pop. Ecosys.

Area

Pop. Ecosys.

Area

Reference

Opening

Closing

Net

change

System of Environmental-Economic Accounting

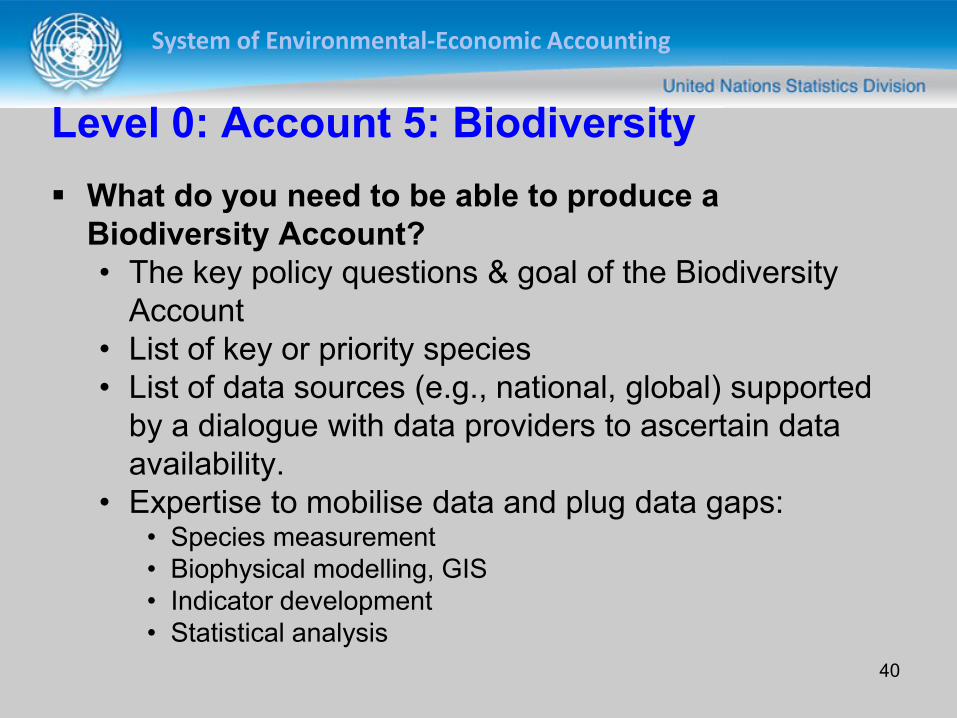

Level 0: Account 5: Biodiversity

What do you need to be able to produce a

Biodiversity Account?

• The key policy questions & goal of the Biodiversity

Account

• List of key or priority species

• List of data sources (e.g., national, global) supported

by a dialogue with data providers to ascertain data

availability.

• Expertise to mobilise data and plug data gaps: • Species measurement

• Biophysical modelling, GIS

• Indicator development

• Statistical analysis

40

System of Environmental-Economic Accounting

Level 0: Account 5: Biodiversity

What do you need to produce a Biodiversity

Account?

• Information on key or priority species • Species classifications (family, genus)

• Species measures (ranges, richness, population counts over

time)

• Characteristics (e.g., habitat, specialist/generalist, health)

• Conservation status

• Extent Account or some form of spatial infrastructure

for ecosystems (spatial units)

41

System of Environmental-Economic Accounting

Account 6: Services Supply

42

System of Environmental-Economic Accounting

Level 0: Account 6: Services Supply

• What? • Physical and monetary flows of “final” ecosystem services from

ecosystems to beneficiaries

• Directly used by (or affect) people

• Why? • Inform policies of contribution of ecosystems to human

well-being

• Assess trade-offs between development and conservation

• Link to standard economic production measures in SNA

• Link to other SEEA-EEA accounts (Condition, Services Use,

Monetary Asset valuation)

• Indicators: • Flows of individual services (physical and monetary) change

• Indices of aggregated services by ecosystem type change

43

System of Environmental-Economic Accounting

Level 0: Account 6: Services Supply

44

• What does a Services Supply Account look like?

Regulating

Provisioning

Cultural

Land cover

Maps Tables

Lookup tables

Biophysical modelling

Urban and

associated Forest tree cover Agricultural land Open wetlands

Provisioning

e.g., tonnes of

timber

e.g., tonnes of

wheat

Regulating

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

P absorbed

Cultural

e.g., hectares of

parkland

e.g., number of

visitors / hikers

e.g., hectares

of duck habitat

Ecosystem type

Type of service

Valuation

Monetary Services Supply

System of Environmental-Economic Accounting

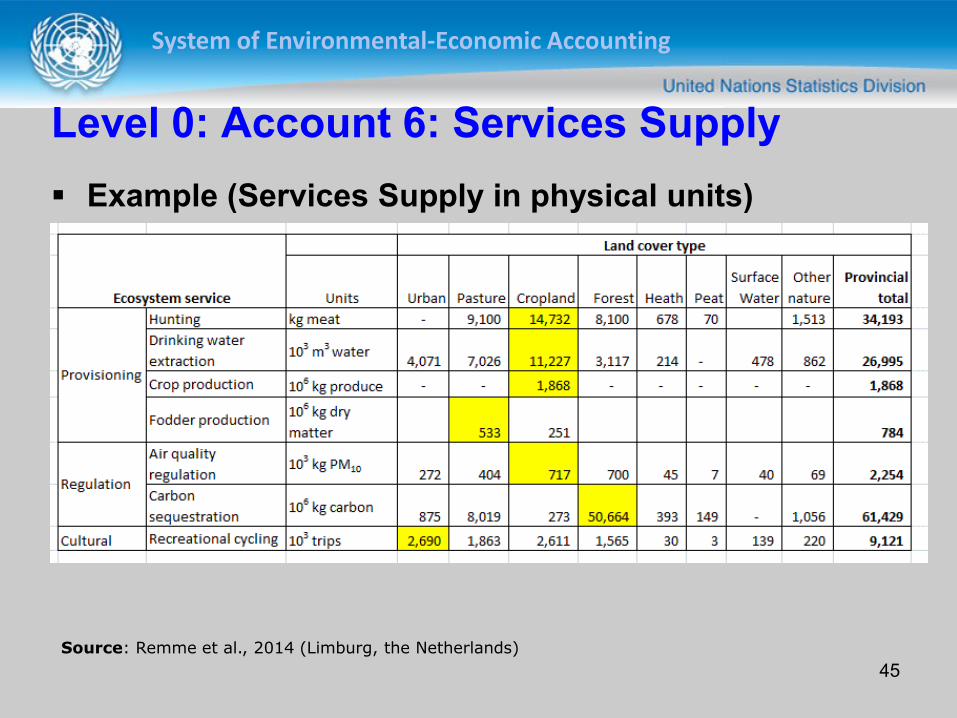

Level 0: Account 6: Services Supply

Example (Services Supply in physical units)

Source: Remme et al., 2014 (Limburg, the Netherlands)

45

System of Environmental-Economic Accounting

Level 0: Account 6: Services Supply

• What does a Services Supply Account look like?

• Spatially-detailed physical measures of “final” services according

to common Classification:

• Provisioning

• Regulating

• Cultural

• Physical measures (crops, flood control, clean drinking water,

carbon sequestration, recreation, …)

• Valuation where appropriate and available

Monetary Services Supply

46

System of Environmental-Economic Accounting

Level 0: Account 6: Services Supply

• What do you need to create a Services

Supply Account? • Ecosystem Extent, Ecosystem Condition

• Common spatial infrastructure (Spatial Units)

• Common Classification of services

• Data: • Field studies

• Transfer from other locations (benefits transfer, valuation)

• Economic production (agriculture, forestry, fisheries, water)

• Biophysical modelling

• Expertise: ecologists, geographers (GIS),

economists, policy analysts, statisticians

47

System of Environmental-Economic Accounting

Account 7: Services Use

48

System of Environmental-Economic Accounting

Level 0: Account 7: Services Use

• What? • Physical and monetary flows from ecosystems to beneficiaries

• Why? • Social, economic and environmental policies:

• Who benefits from ecosystem services?

• Who is dependent on ecosystem services?

• Link to consumption accounts in SNA (Augmented I-O…)

• Link to other SEEA-EEA accounts (Services Supply)

• Indicators:

• Dependence on ecosystem services where and whom

• Public goods from private ecosystems

49

System of Environmental-Economic Accounting

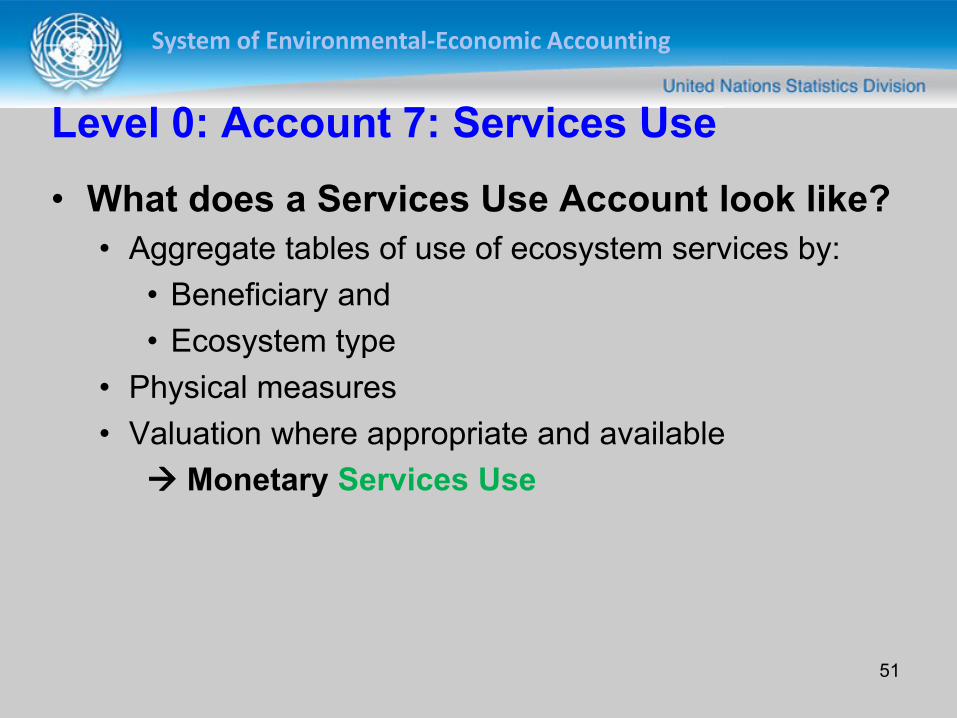

• What does a Services Use Account look like?

Level 0: Account 7: Services Use

50

Services Supply Account

Tables

Urban and

associated Forest tree cover Agricultural land Open wetlands

Provisioning

e.g., tonnes of

timber

e.g., tonnes of

wheat

Regulating

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

P absorbed

Cultural

e.g., hectares of

parkland

e.g., number of

visitors / hikers

e.g., hectares

of duck habitat

Ecosystem type

Type of service

Allocation Valuation

Monetary Services Use

System of Environmental-Economic Accounting

Level 0: Account 7: Services Use

• What does a Services Use Account look like?

• Aggregate tables of use of ecosystem services by:

• Beneficiary and

• Ecosystem type

• Physical measures

• Valuation where appropriate and available

Monetary Services Use

51

System of Environmental-Economic Accounting

Level 0: Account 7: Services Use

• What do you need to compile a Services Use

Account?

• Services Supply Account

• Data:

• Beneficiaries of ecosystem services by:

• service

• type of beneficiary and

• type of asset

• Expertise: Ecosystem accounting

52

System of Environmental-Economic Accounting

Account 8: Capacity

53

System of Environmental-Economic Accounting

Level 0: Account 8: Capacity

• What? • Expected flows of services

• Modeled using Ecosystem Condition Account

• Current and future capacity to supply services

• Why? • Policies related to changing land use, land use intensity,

environmental quality, population distribution

• Ecosystem assessments: Trade-off scenarios of services for

different future conditions

• Estimate Services Supply if little data available

• Calculate Ecosystem Asset Account

• “Value” is Net Present Value of future flows of services

• Indicators: • Services in physical and monetary terms

54

System of Environmental-Economic Accounting

Level 0: Account 8: Capacity

What do Capacity Accounts look like?

55

Urban and

associated Forest tree cover Agricultural land Open wetlands

Provisioning

e.g., tonnes of

timber

e.g., tonnes of

wheat

Regulating

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

P absorbed

Cultural

e.g., hectares of

parkland

e.g., number of

visitors / hikers

e.g., hectares

of duck habitat

Ecosystem type

Type of service

Area

Urban and

associated

Rainfed

herbaceous

cropland

Forest tree

cover

Inland water

bodies

Open wetlands

hectares

Ecosystem typeEcosystem extent

Ecosystem condition

Vegetation Biodiversity Soil Water Carbon Index

Condition Account (Current) Capacity (Current)

Assumptions about future

Condition Account (Future)

Area

Urban and

associated

Rainfed

herbaceous

cropland

Forest tree

cover

Inland water

bodies

Open wetlands

hectares

Ecosystem typeEcosystem extent

Ecosystem condition

Vegetation Biodiversity Soil Water Carbon Index

Biophysical

Modelling

Capacity (Future)

Urban and

associated Forest tree cover Agricultural land Open wetlands

Provisioning

e.g., tonnes of

timber

e.g., tonnes of

wheat

Regulating

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

P absorbed

Cultural

e.g., hectares of

parkland

e.g., number of

visitors / hikers

e.g., hectares

of duck habitat

Ecosystem type

Type of service

Biophysical

Modelling

System of Environmental-Economic Accounting

Level 0: Account 8: Capacity

• What do Capacity Accounts look like?

• Spatially-detailed: by ecosystem and service type

• Looks the same as the Services Supply Account

• But: Services are modelled

• Biophysical models estimate Capacity from Condition

• Capacity Accounts record “hypothetical” flow of services

• e.g., water purification potential of wetlands if there is no

pollution or beneficiaries

• Assumptions about the future are used to generate a

future Conditions Account

• Biophysical models estimate Future Capacity Account

56

System of Environmental-Economic Accounting

Level 0: Account 8: Capacity

• What do you need to compile a Capacity

Account? • Extent Account and Condition Account

• Ecosystem services classification

• Scenarios: assumptions about the future

• Data: • Ecological production functions

• Models may be generic or calibrated to local conditions

• Expertise: • Ecologists (modelling & production functions)

• Spatial analysts (many models are linked to GIS packages)

• Ecosystem accounting (to ensure coherence)

• Stakeholders (to agree on future scenarios)

57

System of Environmental-Economic Accounting

Account 9: Augmented I-O

58

System of Environmental-Economic Accounting

Level 0: Account 9: Augmented I-O

• What? • Addition to standard Input-Output tables to take into

account ecosystems (producers) and ecosystem

services (commodities)

• Why? • Show contribution of ecosystems and services to the

economy (direct and indirect)

• Support decisions about the economic impacts of

ecosystem change

• Link to SNA

• Use I-O methods to balance production and

consumption 59

System of Environmental-Economic Accounting

Level 0: Account 9: Augmented I-O

What do Augmented I-O Accounts look like?

60

Urban and

associated Forest tree cover Agricultural land Open wetlands

Provisioning

e.g., tonnes of

timber

e.g., tonnes of

wheat

Regulating

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

CO2 stored /

released

e.g., tonnes of

P absorbed

Cultural

e.g., hectares of

parkland

e.g., number of

visitors / hikers

e.g., hectares

of duck habitat

Ecosystem type

Type of service

Services Supply

Augmented I-O

Services Use

System of Environmental-Economic Accounting

Level 0: Account 9: Augmented I-O

• What do you Augmented I-O Accounts look

like?

• National level I-O tables (provincial or state if available)

• Rows added for commodities (ecosystem services)

• Columns added for producers (ecosystems)

• Physical or monetary

• Need monetary to balance

61

System of Environmental-Economic Accounting

Level 0: Account 9: Augmented I-O

• What do you need to compile Augmented I-O

Accounts? • Services Supply Account (physical and monetary)

• Services Use Accounts (physical and monetary)

• Data:

• Economic production functions including

ecosystem services • e.g., crop = f(ecosystem services, capital, labour…)

• Expertise:

• Input-Output experts (set up and operation)

• Productivity experts (production functions)

• Ecological economists (production functions)

62

System of Environmental-Economic Accounting

Account 10: Integrated Sector Accounts and

Balance Sheet

63

System of Environmental-Economic Accounting

Level 0: Account 10: Integrated Sector

Accounts and Balance Sheet

• What? • Economic sector level summary accounts

• Standard aggregates adjusted for degradation

• Why? • Augment the economic accounts of the SNA by integrating

into the sequence of accounts

• Integrated Sector Accounts produce aggregate

measures of economic activity, such as national income

and saving, which are adjusted for ecosystem degradation.

• Balance Sheets compare the values of ecosystem assets

with values of produced assets, financial assets (and

liabilities) and other economic assets.

64

System of Environmental-Economic Accounting

Level 0: Account 10: Integrated Sector

Accounts and Balance Sheet

What do Integrated Sector Accounts and

Balance Sheet look like?

65

Asset

Services

Supply

Services

Use

SNA

System of Environmental-Economic Accounting

Level 0: Account 10: Integrated Sector

Accounts and Balance Sheet

What do Integrated Sector Accounts and

Balance Sheet look like? • For example, the Production Account takes

▫ Total Output

Less: Intermediate consumption

= Gross Value Added

Less: Consumption of Fixed Capital

= Net Value Added

Less Depletion/Degradation of natural resources

= Depletion-adjusted Net Value Added

• Similar calculations result in other important

indicators: ▫ Depletion-adjusted Net Saving

66

System of Environmental-Economic Accounting

Level 0: Account 10: Integrated Sector

Accounts and Balance Sheet

What do you need to compile Integrated

Sector Accounts and Balance Sheet? • Asset Account

• Services Supply Account

• Services Use Account

• SNA

Data: • Monetary value of assets, services

Expertise: • National accounting

• Ecosystem accounting

67

System of Environmental-Economic Accounting

Supporting information: Socio-economic

68

System of Environmental-Economic Accounting

Level 0: Supporting Information: Socio-economic

• What? • Socio-economic data and other drivers of change

• Why? • People, governments and businesses are drivers of change and

beneficiaries of Ecosystem Services

• Understand why a change occurred (natural or human?)

• Support scenarios of future (Capacity)

• Links to SEEA-EEA accounts (Extent, Condition, Water,

Carbon, Biodiversity, Services Supply, Services Use, Asset)

• Indicators: • Allocate changes in assets to local, national and global drivers

• Allocate supply of services to beneficiaries

• Estimate dependence of population and business on ecosystems

(food security, water security, flood risks)

69

System of Environmental-Economic Accounting

Level 0: Supporting Information: Socio-economic

What does Socio-economic Information look like?

• Drivers of change: ▫ Maps or tables to explain changes in Extent, Conditions and

Services Supply

– e.g., changes in land-use

– e.g., trends in rainfall

• Socio-economic data: ▫ Maps or tables to explain business and population drivers

– e.g., changes in commodity prices

– e.g., trends in population growth

▫ Maps or tables to calculate beneficiaries

– e.g., population distribution

70

System of Environmental-Economic Accounting

Level 0: Supporting Information: Socio-economic

• What do you need to compile Socio-economic

information?

• Common spatial infrastructure (Spatial Units)

• Drivers of change data: • Local, global climate

• Global, national, local economic conditions (GDP,

employment, growth rates)

• Local activities (agriculture intensity, forestry intensity,

recreation intensity)

• Local development plans (land use, urban expansion)

• Expertise: Economists, climate specialists,

sociologists, regional planners

71

System of Environmental-Economic Accounting

Level 0: Supporting Information: Socio-economic

• What do you need to compile Socio-economic

information?

• Socio-economic data:

• Local population distribution (Census, surveys, case studies):

• Income

• Industry of employment

• Dependence on nature (Case studies)

• Business types by location (surveys, Business Register)

• Environmental protection expenditures

• Dependence on nature (biomass, energy, water,

pollution regulation…)

• Expertise: Economists, sociologists, statisticians,

geographers (GIS, integration) 72

System of Environmental-Economic Accounting

End of Accounts…

Questions?

Discussion

Prepare for group exercise…think about: • What are your priority accounts?

• What are the opportunities to produce them? ▫ Stakeholders?

▫ Institutional mechanisms?

▫ Current activities?

• What are the constraints? ▫ Data?

▫ Capacity?

Next up: Tools 73

System of Environmental-Economic Accounting

Level 0: Tools

Classifications

Spatial units, scaling & aggregation

Biophysical modelling

Valuation

Other tools: • Statistical quality guidelines

• Interdisciplinary teams

• Case studies and surveys

Not discussed: GIS (spatial analysis), data

analysis, communications, engagement, data

management, project planning and evaluation…

74

System of Environmental-Economic Accounting

Tools 1: Classifications

75

System of Environmental-Economic Accounting

Level 0: Tools 1: Classifications

What? • From SEEA-CF:

▫ Land Cover, Land Use

▫ Economic units, industry sectors

• New: ▫ Final ecosystem services

Why? • Accounting needs Consistent and Coherent and

Comprehensive: Classifications ▫ Consistent: use same classification for same concept

▫ Coherent: with other classifications

▫ Comprehensive: “Classifications Certify Complete Coverage”

76

System of Environmental-Economic Accounting

Level 0: Tools 1: Classifications

Land Cover • From SEEA-CF (p.276)

• Uses FAO LCCS3

(Food and Agriculture

Organization – Land

Cover Classification

System v3) definitions

• High-level aggregate: • May adapt to local

situations

• Used as basis for

“ecosystem type”

77

01 Artificial surfaces (including urban and associated

areas)

02 Herbaceous crops

03 Woody crops

04 Multiple or layered crops

05 Grassland

06 Tree covered areas

07 Mangroves

08 Shrub covered areas

09 Shrubs and/or herbaceous vegetation, aquatic or

regularly flooded

10 Sparsely natural vegetated areas

11 Terrestrial barren land

12 Permanent snow and glaciers

13 Inland water bodies

14 Coastal water bodies and inter-tidal areas

System of Environmental-Economic Accounting

Level 0: Tools 1: Classifications

Land Use From SEEA-CF (p. 266)

Detailed (4-digit level)

78

1.0 Land 1.1 Agriculture

1.2 Forestry

1.3 Aquaculture

1.4 Built up and related areas

1.5 Maintenance and restoration of environmental functions

1.6 Other uses of land

1.7 Land not in use

2.0 Inland waters 2.1 Aquaculture and holding facilities

2.2 Maintenance and restoration of environmental functions

2.3 Other uses of inland waters

2.4 Inland waters not in use

3.0 Coastal waters 3.1 Aquaculture and holding facilities

3.2 Maintenance and restoration of environmental functions

3.3 Other uses of coastal waters

3.4 Coastal waters not in use

4.0 Exclusive Economic Zone (EEZ) 4.1 Aquaculture and holding facilities

4.2 Maintenance and restoration of environmental functions

4.3 Other uses of coastal waters

4.4 Coastal waters not in use

System of Environmental-Economic Accounting

Level 0: Tools 1: Classifications

Services • Based on Common

International

Classification of

Ecosystem Services

(CICES)

• Not mutually exclusive

• A list of “final”

services

• More detail (4-digit)

• Does not include

“supporting services”

(= ecosystem

functions)

79

Section Division Group

01.01.01 Biomass

01.01.02 Water

01.02.01 Biomass

01.02.02 Water

01.03.01 Biomass-based energy sources

01.03.02 Mechanical energy

02.01.01 Mediation by biota

02.01.02 Mediation by ecosystems

02.02.01 Mass flows

02.02.02 Liquid flows

02.02.03 Gaseous / air flows

02.03.01 Lifecycle maintenance, habitat and gene pool

protection

02.03.02 Pest and disease control

02.03.03 Soil formation and composition

02.03.04 Water conditions

02.03.05 Atmospheric composition and climate

regulation

03.01.01 Physical and experiential interactions

03.01.02 Intellectual and representative interactions

03.02.01 Spiritual and/or emblematic

03.02.02 Other cultural outputs

01. Provisioning

02. Regulation &

Maintenance

03. Cultural

01.01 Nutrition

01.02 Materials

01.03 Energy

02.01 Mediation of waste,

toxics and other nuisances

02.02 Mediation of flows

02.03 Maintenance of

physical, chemical,

biological conditions

03.01 Physical and

intellectual interactions

with biota, ecosystems, and

land-/seascapes

[environmental settings]

03.02 Spiritual, symbolic

and other interactions with

biota, ecosystems, and land-

/seascapes [environmental

settings]

System of Environmental-Economic Accounting

Level 0: Tools 1: Classifications

From SEEA-CF: Economic Units - Enterprises (business industry)

- Households (people and non-corporate business)

- Government

- Rest of the world

SEEA-EEA adds a spatial dimension: • Local

• Regional

• National

• Global

80

System of Environmental-Economic Accounting

Tools 2: Spatial units

81

System of Environmental-Economic Accounting

Level 0: Tools 2: Spatial units

What? • A common definition of Spatial Units for all accounts

• Based on surface characteristics (terrestrial, freshwater, coastal

and marine)

Why? • Accounting needs statistical units about which information is

compiled, derived, reported and compared ▫ e.g., business statistics are built on locations, establishments,

companies and enterprises

• Information is collected on many spatial levels ▫ Needs to be consolidated within a GIS or spatial model

• First step in tabulating & aggregating more detailed data ▫ Not everybody is a GIS expert

• Links accounts together:

▫ (Extent, Condition, Services Supply…) 82

System of Environmental-Economic Accounting

Recommended three levels: hierarchical and mutually exclusive: 1. Basic Spatial Unit (BSU)

• Pixel or grid cell 2. Ecosystem Unit (EU)

• Homogenous according to criteria (cover, slope, drainage area, elevation…)

• Consolidate for tables by EU type 3. Ecosystem Reporting Area (ERA)

• For reporting (sub-drainage area, administrative area…)

Establishes Ecosystem Extent Account

Source: Statistics Canada, 2013

Level 0: Tools 2: Spatial units

83

System of Environmental-Economic Accounting

Level 0: Tools 2: Scaling

What? • Converting information from one scale to another (spatial,

temporal, thematic)

Why? • Information exists in various types:

▫ Point (water quality monitoring, “study sites”, etc.)

▫ Area (land cover, protected area, species range, etc.)

▫ Network (roads, streams, corridors, etc.)

• Need to understand how and when to attribute information from

one scale to another

84

System of Environmental-Economic Accounting

Level 0: Tools 2: Scaling

Main approaches • Downscaling

▫ Attributing information from larger areas to smaller areas contained

within them

▫ Caution: Data need to be evenly distributed

• Upscaling ▫ Attributing information from smaller areas to larger areas

▫ Caution: Data need to be representative

• Transfer ▫ Transferring information measured in one location to another

▫ Often used in terms of Benefits Transfer

▫ Caution: Locations need to be very similar

85

System of Environmental-Economic Accounting

Level 0: Tools 2: Aggregation

What?

• Combining many measures into simpler ones

• Dissimilar measures may be aggregated using:

▫ Indices (e.g., water quality index)

▫ Conversion to common units (e.g., CO2 equivalents)

Why?

• Accounting requires aggregates (of dollars, business

types, sub-populations, regional summaries, national

indicators…)

• Summary indicators for dashboards, linking to

economic accounts

86

System of Environmental-Economic Accounting

Level 0: Tools 2: Aggregation

Aggregating dissimilar biophysical measures:

• Requires indexing (comparison with reference)

• Example: ecosystem condition measures, service measures

• Caution: Requires understanding of relative importance of

component measures (weighting)

Final aggregates

• e.g., total value of ecosystem services, total asset value

• Require many assumptions (relative importance, methods…)

• Services can be competing, complementary or independent

• Caution: Monetary valuation is often applied inappropriately

Valuation results can be misleading

87

System of Environmental-Economic Accounting

Tools 3: Biophysical modelling

88

System of Environmental-Economic Accounting

Level 0: Tools 3: Biophysical modelling

What? • Four main approaches:

Why? • Estimate Ecosystem Services across spatial units and time

• Estimate Ecosystem Capacity from Ecosystem Condition

• Combine data from various sources and scales (e.g., point field

data and satellite data)

• Estimate unknown data values

• GIS-based spatial modelling approaches have methods built-in

89

1. Look-up tables

2. Statistical approaches

3. Geostatistical interpolation

4. Process-based modelling

System of Environmental-Economic Accounting

Level 0: Tools 3: Biophysical modelling

Approaches: 1. Look-up tables 2. Statistical approaches 3. Geostatistical interpolation 4. Process-based modeling

90

Attribute values for an ecosystem service (or other measure) to every Spatial Unit in the same class (e.g., a land cover class).

Example: Benefits Transfer

one ha of forest = $5000 attribute to each ha of forest

error rate: 60-70%

System of Environmental-Economic Accounting

Level 0: Tools 3: Biophysical modelling

Approaches: 1. Look-up tables 2. Statistical approaches 3. Geostatistical interpolation 4. Process-based modeling

91

Estimate ecosystem services, asset or condition based on known explanatory variables such as soils, land cover, climate, distance from a road, etc., using a statistical relation.

Example: Function Transfer

Value = f(land cover, population, roads, climate)

Error rate = 40-50%

System of Environmental-Economic Accounting

Level 0: Tools 3: Biophysical modelling

Approaches: 1. Look-up tables 2. Statistical approaches 3. Geostatistical interpolation 4. Process-based modeling

92

Use algorithms to predict the measure of unknown locations on the basis of measures of nearby known measures:

Example: Kriging

Error rate = ?

Known

Unknown

System of Environmental-Economic Accounting

Level 0: Tools 3: Biophysical modelling

Approaches: 1. Look-up tables 2. Statistical approaches 3. Geostatistical interpolation 4. Process-based modeling

93

Predict ecosystem services based on a set of future condition or management scenarios:

Example: Scenario for future services based on expected changes in land cover, demand and management

Error rate = 100%

System of Environmental-Economic Accounting

Tools 4: Valuation techniques

94

System of Environmental-Economic Accounting

Level 0: Tools 4: Valuation

What? • Attributing economic or social value to assets

& services

• Ecosystem services valuation produces:

95

▫ Average values (per hectare, under specific conditions)

▫ Or Marginal values (change in value of converting one hectare)

• Asset valuation: ▫ Scenarios of future Conditions and demand net present value of

Ecosystem Asset

Why? • Integrate with SNA

▫ Augmented I-O, Integrated Sector Accounts and Balance Sheet

• Assessing trade-offs: Convert or protect?

• Monetary valuation is embedded in many: ▫ National plans: cost/benefit, payment & compensation schemes

▫ Research approaches: contingent valuation, choice modelling

System of Environmental-Economic Accounting

Level 0: Tools 4: Valuation

Approaches (non-market): • Revealed preferences:

▫ Production function: (resource rent)

• value = f(ecosystem, produced capital, labour)

▫ Replacement cost: produce service with another ecosystem/asset

▫ Hedonic pricing: real-estate prices, wages with respect to distance

▫ Averting behaviour: expenditures to avoid degradation

▫ Travel cost: expenditures to enjoy a service (e.g., recreation)

• Stated preference: ▫ Contingent valuation, choice modelling: willingness to pay

• Simulated exchange values: model supply/demand

• Payments for ecosystem services (PES): ▫ Carbon, biodiversity markets

• Payments made to improve condition: Rehabilitation costs

96

System of Environmental-Economic Accounting

Level 0: Tools 4: Valuation

Measurement challenges • More challenging for Regulating and Cultural Services

• How to measure monetary value of regulating services? ▫ Spatial dependencies (downstream, species/habitat)

▫ Multiple beneficiaries

▫ Risks (e.g., flood control, climate regulation)

• Non-linear responses ▫ Thresholds/resilience, climate change, refuge areas

• Aggregating values of different services ▫ Services can be competing, complementary or independent

• Transferring measured values from one site to another ▫ (Discussed under Biophysical Modelling & Scaling)

• Highly dependent on decision context ▫ Project assessment: trade-offs

▫ Long-term sustainable use of ecosystems: high-level indicators

▫ Payments and compensation: needs to have precise values

97

System of Environmental-Economic Accounting

Tools 5: Other tools

98

System of Environmental-Economic Accounting

Level 0: Tools 5: Other tools

What? • Statistical quality guidelines

Why? • Need a common concept of quality, uncertainty and “fitness for

use”

How? • Apply national or international guidelines

▫ UN National Quality Assurance Framework (NQAF)

▫ International Monetary Fund – Data Quality Assessment

Framework (IMF-DQAF)

▫ Disciplinary “accepted methods” are less-well documented

• Build a culture of quality:

▫ Metadata, process documentation, strategic planning…

• Work within accepted statistical processes (e.g., Generic

Statistical Business Processing Model – GSBPM) 99

System of Environmental-Economic Accounting

Level 0: Tools 5: Other tools

Why? • No single discipline can do it alone

Need a shared “language”

Need to become transdisciplinary

How? • Agree on common objectives and approaches

• Work together to avoid disciplinary “stovepipes”

• Engage experts, data providers, users and supporters

100

What? • Interdisciplinary teams (ecology,

economics, geography, policy, sociology,

statistics…)

System of Environmental-Economic Accounting

Level 0: Tools 5: Other tools

What? • Case studies & surveys linking services with benefits

Why? • In some countries, there is a close relationship between

ecosystem services and poverty, water security, food security,

employment…

• Link ecosystem condition, services with socio-economic priorities

(well-being, health, income, employment…)

How? • Local surveys for priority stakeholders (e.g., dependent on

ecosystem services)

• National sample surveys (e.g., water use, importance of nature,

expenditures on environmental protection…)

101

System of Environmental-Economic Accounting

Other related training materials

Secretariat for the Convention on Biological

Diversity (SCBD) • Quick Start Package (QSP) (Weber, 2014)

▫ Available online at www.ecosystemaccounting.net

▫ Includes free GIS software and tutorials

• National Biodiversity Strategies and Action Plans ▫ Training modules at www.cbd.int/nbsap/training/

World Bank WAVES

Statistics Canada: • Measuring Ecosystem Goods and Services Teacher’s Kit

102

System of Environmental-Economic Accounting

Evaluation of the training module

Please complete the online evaluation form for this

module: http://tinyurl.com/pbopmy2

For this module

• What did you learn that you could apply in your work?

• Was the presentation clear and informative?

• Was it too simple? Too complex?

• Was there anything you did not understand?

• What additions or deletions would you suggest (recognizing that

the unit is intended for a general audience)?

• Do you have any suggestions as to how the SEEA-EEA may be

improved (concepts, principles) in this area?

System of Environmental-Economic Accounting

References

SNA 2008

SEEA Central Framework, SEEA-EEA, Applications and Extensions

SCBD Quick Start Package

World Bank WAVES: Designing Pilots for Ecosystem Accounting

International Monetary Fund: DQAF

UN: NQAF

UNECE: GSBPM Australian Bureau of Statistics, 2013. Land Account: Queensland, Experimental

Estimates, 2013

Eigenraam, M., Chua, J. and HASKER, J., 2013. Environmental-Economic Accounting:

Victorian Experimental Ecosystem Accounts, Version 1.0. Melbourne, Australia:

Department of Sustainability and Environment, State of Victoria.

Remme, Roy P., Matthias Schröter, and Lars Hein. "Developing spatial biophysical

accounting for multiple ecosystem services." Ecosystem Services 10 (2014): 6-18.

Statistics Canada, 2013. Human Activity and the Environment: Measuring Ecosystem

Goods and Services 2013. 16-201-XWE. Ottawa: Government of Canada.

Weber, J., 2014. Ecosystem Natural Capital Accounts: A Quick Start Package. 77

(Technical Series). Montreal: Secretariat of the Convention on Biological Diversity. 104

System of Environmental-Economic Accounting

Acknowledgements

This project is a collaboration between The United

Nations Statistics Division (UNSD), United Nations

Environment Programme (UNEP) and the Secretariat of

the Convention on Biological Diversity (CBD) and is

supported by the Government of Norway.

Contact: [email protected]

105