kenanga oneprs moderate fund - kenanga investors filekenanga oneprs moderate fund annual report for...

TRANSCRIPT

KENANGA ONEPRS MODERATE FUND

ANNUAL REPORT

For the Financial Period 20 November 2013 (Date of Commencement) to 31 July 2014

Investor Services CenterToll Free Line: 1 800 88 3737Fax: +603 2057 3722Email: [email protected]

Head Office, Kuala LumpurSuite 12.02, 12th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia.Tel: 03-2057 3688 Fax: 03-2161 8807

Kenanga Investors Berhad (353563-P)

KENANGA ONEPRS MODERATE FUND

Contents Page

Corporate Directory iiDirectory of PRS Provider’s Offices iiiiFund Information 1PRS Provider’s Report 2-6Fund Performance 7-9Trustee’s Report 10Independent Auditor’s Report 11-12Statement by the PRS Provider 13Financial Statement 14-31

ii Kenanga OnePRS Moderate Fund Annual Report

CORPORATE DIRECTORY

Private Retirement Scheme (PRS) Provider: Kenanga Investors Berhad (Company No. 353563-P)Registered office

Kenanga Investors Berhad (KIB)8th Floor, Kenanga International, Jalan Sultan Ismail,50250 Kuala Lumpur, Malaysia.Tel: 03-2162 1490 Fax: 03-2161 4990

Business OfficeSuite 12.02, 12th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia.Tel: 03-2057 3688 Fax: 03-2161 8807E-mail: [email protected] Website: www.KenangaInvestors.com.my

Board Of DirectorsDatuk Syed Ahmad Alwee Alsree (Chairman)Syed Zafilen Syed Alwee (Independent Director)YM Raja Dato’ Seri Abdul Aziz bin Raja Salim (Independent Director)Vivek Sharma (Independent Director)Peter John Rayner (Independent Director)Bruce Kho Yaw HuatIsmitz Matthew De Alwis

Investment Committee Bruce Kho Yaw Huat (Chairman) Syed Zafilen Syed Alwee (Independent Member)Vivek Sharma (Independent Member)Peter John Rayner (Independent Member)Ismitz Matthew De Alwis

Company Secretary: Norliza Abd Samad (MAICSA 7011089)9th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia.Tel: 03-2162 1490 Fax:03-2161 4990

Scheme Trustee (“Trustee”): Maybank Trustees Berhad (5004-P)Registered Office

8th Floor, Menara Maybank, 100, Jalan Tun Perak, 50050 Kuala Lumpur. Tel:03-2078 8363 / 8833 Email: [email protected]

Auditor: Ernst & Young (AF: 0039)Level 23A, Menara Milenium, Jalan Damanlela, Pusat Bandar Damansara, 50490 Kuala Lumpur.Tel: 03-7495 8000 Fax: 03-2095 5332

Tax Adviser: Ernst & Young Tax Consultants Sdn Bhd (Company No. 179793-K)Level 23A, Menara Milenium, Jalan Damanlela, Pusat Bandar Damansara, 50490 Kuala Lumpur.Tel: 03-7495 8000 Fax: 03-2095 5332

Administrator: Private Pension Administrator Malaysia (PPA)Level 6, Menara Mudajaya, Jalan PJU 7/3, Mutiara Damansara, 47180 Kuala Lumpur. Tel: 03-6204 8990 Fax: 03-6204 8995 Website: www.ppa.my Email: [email protected]

Membership: Federation Of Investment Managers Malaysia (FIMM)19-06-1, 6th Floor, PNB Damansara, 19, Lorong Dungun, Damansara Heights,50490 Kuala Lumpur, Malaysia. Tel: 03-2093 2600 Fax: 03-2093 2700 Website: www.fimm.com.my

Kenanga OnePRS Moderate Fund Annual Report iii

DIRECTORY OF PRS PROVIDER’S OFFICES

REGIONAL BRANCH OFFICES:

Kuala LumpurSuite 12.02, 12th Floor, Kenanga InternationalJalan Sultan Ismail,50250 Kuala Lumpur, MalaysiaTel: 03-2057 3688Fax: 03-2161 8807

Johor BahruLot 11.03, 11th Floor, Menara MSC Cyberport5 Jalan Bukit Meldrum80300 Johor Bahru, JohorTel: 07-223 7505/4798 Fax: 07-223 4802

MelakaNo. 25-1 Jalan Kota Laksamana 2/17Taman Kota Laksamana Seksyen 275200 MelakaTel: 06-281 8913, 282 0518 Fax: 06-281 4286

Kuching1st Floor, No 71, Lot 7Lot 10900, Jalan Tun Jugah93350 Kuching, SarawakTel: 082-572 228 Fax: 082-572 229

KlangNo. 12 Jalan Batai Laut 3, Taman Intan41300 Klang, Selangor Darul EhsanTel:03-3341 8818, 3348 7889 Fax:03-3341 8816

Kota KinabaluA-03-11, 3rd FloorBlock A Warisan SquareJalan Tun Fuad Stephens88000 Kota Kinabalu, SabahTel: 088-447 089/448 106 Fax: 088-447 039

Penang16th Floor , Menara Boustead Penang 39 , Jalan Sultan Ahmad Shah 10050 Penang. Tel : 04 227 3788 Fax : 04 210 6644

IpohSuite 1, 2nd Floor,63 Persiaran Greenhill,30450 Ipoh, Perak, MalaysiaTel: 05-254 7573/7570 Fax: 05-254 7606

Seremban 2nd Floor , No. 1D-2 Jalan Tuanku Munawir 70000 Seremban, Negeri Sembilan . Tel : 06 761 5678 Fax : 06 761 2242

Kenanga OnePRS Moderate Fund Annual Report 1

1. FUND INFORMATION

1.1 Fund Name

Kenanga OnePRS Moderate Fund (the Fund)

1.2 Fund Category

Core (Moderate)

1.3 Investment Objective

The Fund aims to achieve returns over the long-term through investments in equities and/or bonds.

1.4 Investment Strategy

The Fund seeks to achieve its objective by investing a maximum of 60% of the Fund’s NAV in equities and at least 40% of the Fund’s NAV in fixed income instruments and/or money market instruments.

However, at the launch of the Fund, the Fund aims to meet its objective and asset allocation by investing up to 95% of the Fund’s NAV in any one collective investment scheme managed by the PRS Provider that is in line with the Fund’s asset allocation. Such investment shall be for a period of five (5) years from the launch of the Fund or upon the Fund reaching RM200 million NAV (whichever is earlier).

1.5 Performance Benchmark

A composite of All MGS Index (40%) and FBM 100 (60%).

The risk profile of the Fund is not the same as the risk profile of the performance benchmark.

1.6 Distribution Policy

Distribution (if any) will be declared annually and reinvested into the Fund.

Members who have reached their retirement age can opt to have the distribution paid to them by cheque or to their bank account.

1.7 Breakdown of unit holdings of the Fund as at 31 July 2014

Size of holdings No. of members No. of units held5,000 and below 43 85,9415,001 - 10,000 73 492,98210,001-50,000 2 45,20950,001-500,000 0 0500,001 and above 0 0Total 118 624,132

2 Kenanga OnePRS Moderate Fund Annual Report

2. PRS PROVIDER’S REPORT

2.1 Explanation on whether the Fund has achieved its investment objective.

During the period under review, the Fund fulfilled its investment objective, having invested in a balanced fund which has investments in fixed income, money market and equity securities. Currently, the Fund invests in Kenanga Balanced Fund (KBF) which has the mandate to invest up to 60% of Net Asset Value (NAV) in equity and a minimum of 40% in fixed income and money market instruments. KBF has track record to distribute its income annually. As such it meets the objective of the Fund to achieve returns over the long-term through investments in equities and/or bonds.

2.2 Comparison between the Fund’s performance and performance of the benchmark

Performance Chart Since Launch (20/11/2013 – 31/07/2014)Kenanga OnePRS Moderate Fund vs Benchmark*

% Cumulative Return, Launch to 31/07/2014

1.00

3.002.00

4.00

-3.00

-1.00-2.00

0.00

5.006.007.00

Kenanga OnePRS Moderate : 5.8060% FTSE BM Top 100 + 40% quantshop MGS All Index : 3.19

31/1

2/20

13

31/1

/201

4

28/2

/201

4

31/3

/201

4

30/4

/201

4

31/5

/201

4

30/6

/201

4

31/7

/201

4

31/1

1/20

13

20/1

1/20

13

Source: Novagni Analytics and Advisory Sdn Bhd* A composite of All MGS Index (40%) and FBM 100 (60%).

2.3 Investment strategies and policies employed during the period under review

Since the size of the Fund is below RM200 mil, it is currently invested in a collective investment schemes managed by the PRS provider which is in line with the Fund’s asset allocation.

As at 31 July 2014, the Fund had invested 93.98% of its NAV in KBF, and 6.02% in cash and money market instrument. KBF is a portfolio of investments, which gives a lower risk and a lower volatility for investors as compared to a pure equity fund. It provides to unitholders with long term capital growth and income ranging from 3 to 5 years and has a moderate risk profile with tolerance for short term periods of volatility.

During the period under review, the KBF invested mainly in the Malaysian equities ranging from 50% to 58% of the Fund’s NAV.

Kenanga OnePRS Moderate Fund Annual Report 3

2.3 Investment strategies and policies employed during the period under review (Contd.)

Towards the end of the reporting period, the manager engaged in bigger profit taking in order to capture a higher realised return in order to distribute income for the financial year. The manager was encouraged to redeploy the cash into the stocks that they favoured strongly. The manager maintained a barbell strategy of holding a good balance of high yielding/defensive stocks and beta stocks. The former allows them to reduce the portfolio volatility during the uncertain period, whilst the latter captures extra performance when risk appetite return. The manager liked companies in the banking, oil and gas, consumer, and property/REITs.

2.4 The Fund’s asset allocation as at 31 July 2014

Asset 31 July 2014Unquoted collective investment schemes 94.0%Cash 6.0%

Reason for the differences in asset allocation

A comparison between the Fund’s asset allocation is not available as this is the Fund’s first report.

2.5 Fund performance analysis based on NAV per unit (adjusted for income distribution; if any) since last review period

Period under review 20 Nov 13 – 31 Jul 14

Kenanga OnePRS Moderate Fund 5.80%A composite of All MGS Index (40%) and FBM 100 (60%). 3.19%

Source: Lipper & Novagni Analytics and Advisory Sdn Bhd

For the period under review, the Fund has appreciated 5.8%, outperforming the 3.19% increase in its Benchmark (60% FBM100 Index + 40% All MGS Index rate). The out-performance was mainly due to increase in strength in stock picking strategy in KBF.

2.6 Review of the market

Market Review

Bursa Malaysia staged a rebound, alongside regional bourses in 4Q 2013, cheered by the US Congress’ decision to pass a budget bill avoiding a debt default. Meanwhile, the capital flows adjustment started to stabilize as QE tapering was expected to only begin in 2014. On the other hand, the Malaysia 2014 Budget was unveiled in 4Q 2013 with special emphasis on fiscal consolidation through prudent expenditure. The better than expected 3Q 2013 GDP growth and buying interest in selected blue chip stocks helped the FTSE KLCI rally to closed at 1,866.96 levels, representing a gain of 5.2% for the 6 months ended 31st December 2013.

Moving into 2014, sentiment took a dive in January after the US Fed officially announced the QE reduction programme starting in January 2014, whilst keeping interest rates low. On the other hand, China saw sharp increase in interbank rates, as concerns over liquidity and rising credit spooked investors. As a result, most regional markets experienced a sell-off as capital was flowing out from the emerging markets. On the local front, the FBM KLCI was down 3.4% month-on-month in January 2014.

4 Kenanga OnePRS Moderate Fund Annual Report

2.6 Review of the market (Contd.)

Market Review (Contd.)

However, equity markets were quick to recover in February 2014, driven by rising optimism of US growth, coupled with further financial stimulus from European Central Bank (ECB) and Japan to stimulate their respective economies. India was the biggest gainer as it benchmark index rose 20% during the first half of 2014 after the Bharatiya Janata Party won with the biggest majority in the last 30 years to provide optimism of a good and stable government. Philippine was the second best performer during first half of 2014, the benchmark rose 16.2% after S&P raised Philippine credit rating to another notch above investment grade.

On the local front, the FBM KLCI Index remained flat despite the strong performance in the region. The FBM KLCI closed at 1,882.7 or up by 0.8% during the first half of 2014, as foreigners net buying in since April 2014 was not sufficient to offset the net sale of RM5.8 billion worth of equities in 1Q 2014. Meanwhile, Malaysia posted a strong first quarter GDP growth of 6.2% y-o-y but the recently concluded corporate results season came in below market expectation, limiting further price gains.

Global bond markets benefited strongly at the start of 2014, as weaker economic data from the US and China in January combined with the implementation of the Fed’s tapering of its bond purchases led to a sharp sell-off in global equity markets and other risky assets. However, generally better US data in February and March reversed some of the negative sentiment caused by the weather-depressed January figures.

Locally, MGS market was range trading for much of the first half of 2014. Yields for MGS increased across the curve in May 2014 as BNM’s statement signaled the possibility of interest rate normalization to manage the risks posed by financial imbalances to Malaysia’s growth prospects. Over the period under review, the 3-year MGS rose by 11bps and 10-year MGS yields decreased by 14bps to close at 3.552% and 4.039% respectively. The selling pressure in 2013 saw foreign holdings of MGS declining to 42.7% in July and August from its peak of 49.5% in May, but foreign investors subsequently re-entered the MGS market with a 46.7% holding of total MGS as at end June 2014.

The US economy rebounded strongly in the second quarter, expanding by 4.0% on an annualised basis, and the Q1 GDP growth figure was revised higher to -2.1% from -2.9%. A strong reading in the Employment Cost Index also added to the concern that US wage growth may finally accelerate, although this was somewhat offset by slightly weaker unemployment and wage growth data. At the July policy meeting, the Fed continued to trim another $10 billion worth of monthly bond purchases, and the accompanying statement noted that whilst downside risk to inflation had lessened, the labour market slack favoured continued accommodation.

The MGS yield curve flattened in July with the short-end yield falling by 2bps whilst the long-end yield fell by 13bps. The short-end under-performed as the market remained cautious following the OPR hike in July. BNM raised the OPR by 25bps as widely expected, but the accompanying statement reiterated that the basis of any further adjustment on the OPR will be the outlook on growth and inflation. Market is divided on another 25bps OPR hike by H1 2015 in order to manage domestic inflationary pressures and financial imbalances. The corporate bond yield curve flattened and saw yields of 3-years and above falling by 2-15bps. Trading volume on corporate bonds increased by 28% month-on-month to RM8.9 billion in July.

Kenanga OnePRS Moderate Fund Annual Report 5

2.6 Review of the market (Contd.)

Market Outlook

We remain optimistic on equities as prospects are for global economic growth to gain momentum in the period ahead. Although the US QE3 programme will end by 4Q 2014, we expect policies worldwide to remain largely supportive so as not to derail the slow and uneven recovery thus far. However, interest rates globally are likely to trend up after staying at record lows for an extended period, with Malaysia possibly announcing another rate hike of 25bp, after the first one (in 3 years) on 11 July 2014. Against a largely positive external backdrop, Malaysia is on track to register stronger GDP growth of more than 5% in 2014 (2013:4.7%), helped by improving exports and resilient domestic spending. Corporate earnings, however, are likely to stayed muted this year as rising costs partially negates topline expansion. Pegging the FMBKLCI at 16.5x FY15 EPS, we believe the market has an upside potential to end the year higher with an index target of 1980.

In the near-term, however, based on historical statistics, third quarter equity performances are not among the most exciting periods – Since 2000 to 2013 they performed by -0.4% on average. We are currently experiencing toppish market valuation, threat of an interest rate hike, creeping inflation but the good news is there is still ample liquidity in the system supporting equity prices. Put together, we believe market would be lackluster with range bound trading in 3Q until corporate earnings catches up with the current premium valuations. As we expect a stronger 4Q, we will add on current market weakness to take advantage of a rebound in the subsequent months.

Market participants are fairly divided on whether BNM will deliver another OPR hike of 25bps in the next few months in order to manage domestic inflationary pressures and financial imbalances. BNM will likely monitor the impact of the first OPR hike on the real economy, as well as the global economic and financial conditions before making any changes to its policy settings. Local investors may stay cautious, while foreign investors’ positions in MYR bonds are likely to be driven by MYR/USD expectations.

Strategy

The manager will continue to adopt a bar-bell strategy of beta and defensive stocks while adding positions on any market weakness. Their stock selection remains to favour sectors that will benefit from being the main economic drivers particularly oil & gas, construction, exporters and manufacturers. The oil & gas sector continues to benefit from Petronas robust capital expenditure to develop the local oil & gas sector, whilst infrastructure development under the Economic Transformation Programme (ETP) will benefit the construction sector. The exporters/manufacturers will benefit from improved external demand such as technology counters, gloves and materials.

The manager maintain a cautious stance ahead of the potential OPR hike next year, but remain invested in corporate bonds to take on credit risk for the yield enhancement without taking too much duration risk. If market yields rise, they will take the opportunity to increase duration risk.

2.7 Income Distribution

For the financial period under review, the Fund did not declare any income distribution.

6 Kenanga OnePRS Moderate Fund Annual Report

2.8 Details of any unit split exercise

The Fund did not carry out any unit split exercise during the financial period under review.

2.9 Significant changes in the state of affair of the Fund during the period

There were no significant changes in the state of affair of the Fund during the period and up until the date of the PRS Provider’s report, not otherwise disclosed in the financial statements.

2.10 Circumstances that materially affect any interests of the members

During the period under review, there were no circumstances that materially affected any interests of the members.

2.11 Rebates & Soft commissions

Any rebates received are channeled back to the Fund. On the other hand, soft commissions received from the stockbrokers for goods and services such as technical analysis software, fundamental database, financial wire services, stock quotation system and portfolio management software incidental to investment management of the Fund shall be retained by the PRS Provider. For the period under review, the PRS Provider did not receive any rebates or soft commissions from stockbrokers.

Kenanga OnePRS Moderate Fund Annual Report 7

3. FUND PERFORMANCE

3.1 Details of portfolio composition of Kenanga OnePRS Moderate Fund (“the Fund”) for the financial period as at 31 July 2014 are as follows:

a. Distribution among industry sectors and category of investments:

As at31.7.2014

%

Unquoted collective investment schemes 94.0Cash 6.0

100.0

Note: The above mentioned percentages are based on total investment market value plus cash.

b. Distribution among markets

The Fund invested in unquoted collective investment scheme and cash instruments only.

8 Kenanga OnePRS Moderate Fund Annual Report

3.2 Performance details of the Fund for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 are as follows:

Period20.11.2013

to 31.7.2014

Net asset value (“NAV”) (RM Million) 0.33 Units in circulation (Million) 0.62 NAV per unit (RM) 0.5290 Highest NAV per unit (RM) 0.5302 Lowest NAV per unit (RM) 0.4892 Total return (%) 5.80 - Capital growth (%) 5.80 - Income growth (%) - Gross distribution per unit (sen) - Net distribution per unit (sen) - Management expense ratio (“MER”) (%)1 - Portfolio turnover ratio (“PTR”) (times)2 0.71

Note:TotalreturnistheactualreturnoftheFundforthefinancialperiod,computedbasedonNAVper unit and net of all fees.

MER is computed based on the total fees and expenses incurred by the Fund divided by the average fund size calculated on a daily basis. PTR is computed based on the average of the total acquisitions and total disposals of investment securities of the Fund divided by the average fund size calculated on a daily basis.

AboveNAVandNAVperunitarenotshownasex-distributionastherewerenodistributiondeclaredbytheFundinthecurrentfinancialperiodunderreview.

1MERforthefinancialperiodunderreviewisnilastheexpensesoftheFundisbornebythePRSProvider.

2PTRforthefinancialperiodunderreviewis0.71times.

Kenanga OnePRS Moderate Fund Annual Report 9

3.3 Average total return of the Fund

Since Commencement

20 Nov 13 - 31 Jul 14Kenanga OnePRS Moderate Fund 5.80%A composite of All MGS Index (40%) and FBM 100 (60%). 3.19%

Source: Lipper & Novagni Analytics and Advisory Sdn Bhd

3.4 Annual total return of the Fund

Period under review 20 Nov 13 - 31 Jul 14

Kenanga OnePRS Moderate Fund 5.80%A composite of All MGS Index (40%) and FBM 100 (60%). 3.19%

Source: Lipper & Novagni Analytics and Advisory Sdn Bhd

Investors are reminded that past performance is not necessarily indicative of future performance. Unit prices and investment returns may fluctuate.

10 Kenanga OnePRS Moderate Fund Annual Report

4 TRUSTEE’S REPORT TO THE MEMBERS OF KENANGA ONEPRS MODERATE FUND

We have acted as Trustee of Kenanga OnePRS Moderate Fund (“the Fund”) for the first financial period from 20 November 2013 (date of commencement) to 31 July 2014. In our opinion, Kenanga Investors Berhad, (“the PRS Provider”) has managed the Fund in the financial period under review in accordance with the following:

1. The limitations imposed on the investment powers of the PRS Provider and the Trustee under the Deed, the Securities Commission’s Guidelines on Private Retirement Schemes, the Capital Markets and Services Act 2007 and other applicable laws;

2. The valuation or pricing of the Fund is carried out in accordance with the Deed and relevant regulatory requirements; and

3. The creation and cancellation of units of the Fund are carried out in accordance with the Deed and relevant regulatory requirements.

For Maybank Trustees Berhad (Company No.: 5004-P)

Lim San San Head, Unit Trust

Kuala Lumpur, Malaysia

23 September 2014

Kenanga OnePRS Moderate Fund Annual Report 11

5. INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF KENANGA ONEPRS MODERATE FUND

Report on the financial statements

We have audited the financial statements of Kenanga OnePRS Moderate Fund (“the Fund”), which comprise the statement of financial position as at 31 July 2014 and the statement of comprehensive income, statement of changes in net asset value and statement of cash flows for the financial period from 20 November 2013 (date of commencement) to 31 July 2014, and a summary of significant accounting policies and other explanatory information, as set out on pages 14 to 31.

PRSProvider’sandTrustee’sresponsibilityforthefinancialstatementsandfairpresentation

The PRS Provider of the Fund is responsible for the preparation of financial statements so as to give a true and fair view in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards. The PRS Provider is also responsible for such internal control as the PRS Provider determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. The Trustee is responsible for ensuring that the PRS Provider maintains proper accounting and other records as are necessary to enable true and fair presentation of these financial statements.

Auditors’ responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with approved standards on auditing in Malaysia. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the Fund’s preparation of financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of accounting estimates made by the PRS Provider, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

12 Kenanga OnePRS Moderate Fund Annual Report

5. INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF KENANGA ONEPRS MODERATE FUND (CONTD.)

Opinion

In our opinion, the financial statements give a true and fair view of the financial position of the Fund as at 31 July 2014 and of its financial performance, changes in net asset value and cash flows of the Fund for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards.

Other matters

This report is made solely to the members of the Fund, as a body, in accordance with the requirements of Securities Commission Malaysia’s Guidelines on Private Retirement Scheme, and for no other purpose. We do not assume responsibility to any other person for the content of this report.

Ernst & Young Chan Hooi LamAF: 0039 No. 2844/02/16(J)Chartered Accountants Chartered Accountant

Kuala Lumpur, Malaysia

23 September 2014

Kenanga OnePRS Moderate Fund Annual Report 13

6. STATEMENT BY THE PRS PROVIDER

I, Ismitz Matthew De Alwis, being the director of Kenanga Investors Berhad, do hereby state that, in the opinion of the PRS Provider, the accompanying statement of financial position as at 31 July 2014 and the related statement of comprehensive income, statement of changes in net asset value and statement of cash flows for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 together with notes thereto, are drawn up in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards so as to give a true and fair view of the financial position of Kenanga OnePRS Moderate Fund as at 31 July 2014 and of its financial performance and cash flows for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 and comply with the requirements of the Deed.

For and on behalf of the PRS ProviderKenanga Investors Berhad

Ismitz Matthew De Alwis

Kuala Lumpur, Malaysia

23 September 2014

14 Kenanga OnePRS Moderate Fund Annual Report

7. FINANCIAL STATEMENT

7.1 STATEMENT OF COMPREHENSIVE INCOMEFOR THE FIRST FINANCIAL PERIOD FROM 20 NOVEMBER 2013 (DATE OF COMMENCEMENT) TO 31 JULY 2014

Note

20.11.2013 (date of commencement

to 31.7.2014RM

INVESTMENT INCOMEDistribution income 16,263Net loss from investments:

- Financial assets at fair value through profit or loss (“FVTPL”) 8 (243) 16,020

NET INCOME BEFORE TAX 16,020

Income tax expense 7 -

NET INCOME AFTER TAX, REPRESENTING TOTAL COMPREHENSIVE INCOME FOR THE PERIOD 16,020

Net income after tax is made up as follows:Realised gain 16,163Unrealised gain (143)

16,020

The accompanying notes form an integral part of the financial statements.

Kenanga OnePRS Moderate Fund Annual Report 15

7.2 STATEMENT OF FINANCIAL POSITIONAS AT 31 JULY 2014

Note 31.7.2014RM

INVESTMENTSFinancial assets at FVTPL 8 310,263

OTHER ASSETSCash at bank 77,865Amount due from PRS Provider 149

19,894

TOTAL ASSETS 330,157

EQUITYMember’s contribution 314,137 Retained earnings 16,020 NET ASSET VALUE (“NAV”) ATTRIBUTABLE TO MEMBERS 9 330,157

TOTAL EQUITY AND LIABILITIES 330,157

NUMBER OF UNITS IN CIRCULATION 9(a) 624,133

NET ASSET VALUE PER UNIT (RM) 0.5290

The accompanying notes form an integral part of the financial statements.

16 Kenanga OnePRS Moderate Fund Annual Report

7.3 STATEMENT OF CHANGES IN NET ASSET VALUEFOR THE FIRST FINANCIAL PERIOD FROM 20 NOVEMBER 2013 (DATE OF COMMENCEMENT) TO 31 JULY 2014

NoteMembers’

contributionRetained earnings Total NAV

RM RM RM

20.11.2013 (date of commencement) to 31.7.2014

Total comprehensive income - 16,020 16,020 Creation of units 9(a) 322,004 - 322,004 Cancellation of units 9(a) (7,867) - (7,867)At end of the period 314,137 16,020 330,157

The accompanying notes form an integral part of the financial statements.

Kenanga OnePRS Moderate Fund Annual Report 17

7.4 STATEMENT OF CASH FLOWSFOR THE FIRST FINANCIAL PERIOD FROM 20 NOVEMBER 2013 (DATE OF COMMENCEMENT) TO 31 JULY 2014

20.11.2014 (date of commencement)

to 31.7.2014RM

CASH FLOWS FROM OPERATING AND INVESTING ACTIVITIESProceeds from sale of financial assets at FVTPL 19,794 Purchase of financial assets at FVTPL (313,643)Net cash used in operating and investing activities (293,849)

CASH FLOWS FROM FINANCING ACTIVITIESCash received from units created 321,461 Cash paid on units cancelled (7,867)Net cash generated from financing activities 313,594

NET INCREASE IN CASH AND CASH EQUIVALENTS 19,745CASH AND CASH EQUIVALENTS AT DATE OF COMMENCEMENT - CASH AND CASH EQUIVALENTS AT END OF THE PERIOD 19,745

Cash and cash equivalents comprise:Cash at bank 19,745

The accompanying notes form an integral part of the financial statements.

18 Kenanga OnePRS Moderate Fund Annual Report

7.5 NOTES TO THE FINANCIAL STATEMENTSFOR THE FIRST FINANCIAL PERIOD FROM 20 NOVEMBER 2013 (DATE OF COMMENCEMENT) TO 31 JULY 2014

1. THE FUND, THE PROVIDER AND THEIR PRINCIPAL ACTIVITIES

Kenanga OnePRS Moderate Fund (the “Fund”) was constituted pursuant to the executed Deed dated 29 August 2013 (“the Deed”) between the Private Retirement Scheme Provider (“PRS Privider”), Kenanga Investors Berhad and Maybank Trustees Berhad as the Trustee. The Fund commenced operations on 20 November 2013 and will continue to be in operation until terminated as provided under PART 16 of the Deed.

Kenanga Investors Berhad is a wholly-owned subsidiary of Kenanga Investment Bank Berhad, which in turn is a wholly-owned subsidiary of K & N Kenanga Holdings Berhad, listed on the Main Board of Bursa Malaysia Securities Berhad. All of these companies are incorporated in Malaysia.

The principal place of business of the Provider is Suite 12.02, 12th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur.

The Fund seeks to provide members returns over the long term through investments in equities and/or bonds. The Fund seeks to achieve its objective by investing a maximum of 60% of the Fund’s NAV in equities and at least 40% of the Fund’s NAV in fixed income instruments and/or money market instruments. However, at the launch of the Fund, the Fund aims to meet its objective and asset allocation by investing up to 95% of the Fund’s NAV in any one collective investment scheme managed by the PRS Provider that is in line with the Fund’s asset allocation. Such investment shall be for a period of five (5) years from the launch of the Fund or upon the Fund reaching RM200 million NAV (whichever is earlier).

The financial statements were authorised for issue by the Interim Chief Executive Officer of the PRS Provider on 23 September 2014.

2. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

The Fund is exposed to a variety of risks including market risk (which includes interest rate risk and price risk), credit risk and liquidity risk. Whilst these are the most important types of financial risks inherent in each type of financial instruments, the PRS Provider would like to highlight that this list does not purport to constitute an exhaustive list of all the risks inherent in an investment in the Fund.

The Fund has an approved set of investment guidelines and policies as well as internal controls which sets out its overall business strategies to manage these risks to optimise returns and preserve capital for the members, consistent with the long term objectives of the Fund.

Kenanga OnePRS Moderate Fund Annual Report 19

2. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONTD.)

a. Market Risk

Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices. Market risk includes interest rate risk and price risk.

Market risk arises when the value of the financial instruments fluctuate in response to the activities of individual companies, general market or economic conditions. It stems from the fact that there are economy-wide perils, which threaten all businesses. Hence, investors are exposed to market uncertainties. Fluctuation in the investments’ prices caused by uncertainties in the economic, political and social environment will affect the fair value of the Fund.

The PRS Provider manages the risk of unfavorable changes in prices by cautious review of the financial instruments and continuous monitoring of their performance and risk profiles.

i. Interest rate risk

The Fund is not exposed to interest rate risk as it does not hold any interest-bearing assets and liabilities. However, the Fund has indirect exposure to interest rate risk through its investment in the unquoted collective investment schemes.

ii. Price risk

Price risk is the risk of unfavorable changes in the fair values of unquoted collective investment schemes. The Fund invests in unquoted collective investment schemes which are exposed to price fluctuations. This may then affect the unit price of the Fund.

Price risk sensitivity

The PRS Provider’s best estimate of the effect on the profit for the period due to a reasonably possible change in investments in unquoted collective investment schemes with all other variables held constant is indicated in the table below:

Effect on profit Change in price for the period

Increase/(Decrease) Increase/(Decrease) Basis points RM

31.07.2014Financial assets at FVTPL 5/(5) 155/(155)

In practice, the actual trading results may differ from the sensitivity analysis above and the difference could be material.

20 Kenanga OnePRS Moderate Fund Annual Report

2. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONTD.)

a. Market Risk (Contd.)

ii. Price risk (Contd.)

Price risk concentration

The following table sets out the Fund’s exposure and concentration to price risk based on its portfolio as at the reporting date.

Percentage Fair Value of NAV

RM % 31.07.2014Financial assets at FVTPL 310,263 94.0

b. Credit Risk

Credit risk is the risk that the counterparty to a financial instrument will cause a financial loss to the Fund by failing to discharge an obligation. The PRS Provider manages the credit risk by undertaking credit evaluation to minimise such risk.

i. Credit risk exposure

At the reporting date, the Fund’s maximum exposure to credit risk is represented by the carrying amount of each class of financial assets recognised in the statement of financial position.

ii. Financial assets that are either past due or impaired

As at reporting date, there are no financial assets that are either past due or impaired.

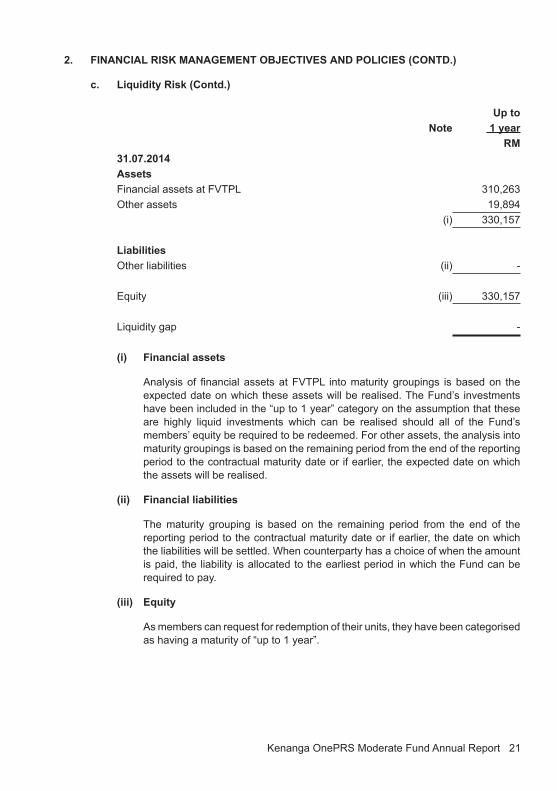

c. Liquidity Risk

Liquidity risk is defined as the risk that the Fund will encounter difficulty in meeting obligations associated with financial liabilities that are to be settled by delivering cash or another financial asset. Exposure to liquidity risk arises because of the possibility that the Fund could be required to pay its liabilities or cancel its units earlier than expected. The Fund is exposed to cancellation of its units on a regular basis. Units sold to members by the PRS Provider are cancellable at the member’s option based on the Fund’s NAV per unit at the time of cancellation calculated in accordance with the Deed.

The liquid assets comprise cash, deposits with licensed financial institutions and other instruments, which are capable of being converted into cash within 7 days.

The following table analyses the maturity profile of the Fund’s financial assets and financial liabilities in order to provide a complete view of the Fund’s contractual commitments and liquidity.

Kenanga OnePRS Moderate Fund Annual Report 21

2. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES (CONTD.)

c. Liquidity Risk (Contd.)

Up to Note 1 year

RM31.07.2014AssetsFinancial assets at FVTPL 310,263 Other assets 19,894

(i) 330,157

LiabilitiesOther liabilities (ii) -

Equity (iii) 330,157

Liquidity gap -

(i) Financial assets

Analysis of financial assets at FVTPL into maturity groupings is based on the expected date on which these assets will be realised. The Fund’s investments have been included in the “up to 1 year” category on the assumption that these are highly liquid investments which can be realised should all of the Fund’s members’ equity be required to be redeemed. For other assets, the analysis into maturity groupings is based on the remaining period from the end of the reporting period to the contractual maturity date or if earlier, the expected date on which the assets will be realised.

(ii) Financial liabilities

The maturity grouping is based on the remaining period from the end of the reporting period to the contractual maturity date or if earlier, the date on which the liabilities will be settled. When counterparty has a choice of when the amount is paid, the liability is allocated to the earliest period in which the Fund can be required to pay.

(iii) Equity

As members can request for redemption of their units, they have been categorised as having a maturity of “up to 1 year”.

22 Kenanga OnePRS Moderate Fund Annual Report

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a. Basis of Accounting

The financial statements of the Fund have been prepared in accordance with Malaysian Financial Reporting Standards (“MFRS”) as issued by Malaysian Accounting Standards Board (“MASB”) and International Financial Reporting Standards (“IFRS”) issued by International Accounting Standards Board (“IASB”).

The financial statements have been prepared on the historical cost basis except as disclosed in the accounting policies below.

b. Standards and Interpretations Issued But Not Yet Effective

As at the date of authorisation of these financial statements, the following Standards and Amendments have been issued by MASB but are not yet effective and have not been adopted by the Fund.

Description

Effective for financial period

beginning on or after

Amendments to MFRS 132: Offsetting Financial Assets and Financial Liabilities 1 January 2014

Amendments to MFRS 10, MFRS 12, and MFRS 127: Investment Entities 1 January 2014

Amendments to MFRS 136: Recoverable Amount Disclosure for Non-Financial Assets 1 January 2014

IC Interpretation 21 Levies 1 January 2014Amendments to MFRSs contained in the documents entitled

Annual Improvements 2010 - 2012 cycle 1 July 2014Amendments to MFRSs contained in the documents entitled

Annual Improvements 2011 - 2014 cycle 1 July 2014MFRS 14: Regulatory Deferral Accounts 1 January 2016Amendments to MFRS 116 and MFRS 138: Property, Plant

and Equipment and Intangible Assets 1 January 2016Amendments to MFRS 11: Joint Arrangements 1 January 2016MFRS 9: Financial Instruments (IFRS 9 Issued by IASB in

November 2009) To be announced MFRS 9: Financial Instruments (IFRS 9 Issued by IASB in

October 2010) To be announced MFRS 9: Financial Instruments: Hedge Accounting and

amendments to MFRS 9, MFRS 7 and MFRS 139 To be announced

The Fund will adopt the above pronouncements when they become effective in the respective financial periods. These pronouncements are not expected to have any significant impact to the financial statements of the Fund upon their initial application, other than MFRS 9.

Kenanga OnePRS Moderate Fund Annual Report 23

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTD.)

b. Standards and Interpretations Issued But Not Yet Effective (Contd.)

MFRS 9 reflects the first phase of work on the replacement of MFRS 139 and applies to classification and measurement of financial assets and financial liabilities as defined in MFRS 139. The standard was initially effective for annual periods beginning on or after 1 January 2013, but Amendments to MFRS 9: Mandatory Effective Date of MFRS 9 and Transition Disclosures, issued in March 2012, moved the mandatory effective date to 1 January 2015. Subsequently, on 14 February 2014, it was announced that the new effective date will be decided when the project is closer to completion. The adoption of the first phase of MFRS 9 will have an effect on the classification and measurement of the Fund’s financial assets, but will not have an impact on classification and measurements of the Fund’s financial liabilities. The Fund will quantify the effect in conjunction with the other phases, when the final standard including all phases is issued by MASB. The final standard of IFRS 7 has been issued by IASB on 24 July 2014.

c. Financial Assets

Financial assets are recognised in the statement of financial position when, and only when, the Fund becomes a party to the contractual provisions of the financial instrument.

When financial assets are recognised initially, they are measured at fair value, plus, in the case of financial assets not at FVTPL, directly attributable transaction costs.

The Fund determines the classification of its financial assets at initial recognition, which are receivables.

i. Financial assets at FVTPL

Financial assets are classified as financial assets at FVTPL if they are held for trading or are designated as such upon initial recognition.

Financial assets held for trading include unquoted collective investment schemes acquired principally for the purpose of selling in the near term.

Subsequent to initial recognition, financial assets at FVTPL are measured at fair value. Changes in the fair value of those financial instruments are recorded in profit or loss.

Interest earned and distribution revenue elements of such instruments are recorded separately in “interest income” and “distribution income” respectively.

ii. Receivables

Financial assets with fixed or determinable payments that are not quoted in an active market are classified as receivables.

Subsequent to initial recognition, receivables are measured at amortised cost using the effective interest method. Gain or loss is recognised in profit or loss when the receivable is derecognised or impaired, and through the amortisation process.

24 Kenanga OnePRS Moderate Fund Annual Report

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTD.)

c. Financial Assets (Contd.)

A financial asset is derecognised when the contractual right to receive cash flows from the asset has expired. On derecognition of a financial asset, the difference between the carrying amount and the sum of the consideration received is recognised in profit or loss.

d. Impairment of Financial Assets

The Fund assesses at each reporting date whether there is any objective evidence that a financial asset is impaired.

To determine whether there is objective evidence that an impairment loss on financial assets has been incurred, the Fund considers factors such as the probability of insolvency or significant financial difficulties of the debtor and default or significant delay in payments.

If any such evidence exists, the amount of impairment loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original effective rate of return. The impairment loss is recognised in profit or loss.

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets, with the exception of receivables, where the carrying amount is reduced through the use of an allowance account. When a receivable becomes uncollectible, it is written off against the allowance account.

If in a subsequent year, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed to the extent that the carrying amount of the asset does not exceed its amortised cost at the reversal date. The amount of reversal is recognised in profit or loss.

e. Income

Income is recognised to the extent that it is probable that the economic benefits will flow to the Fund and the income can be reliably measured. Income is measured at the fair value of consideration received or receivable.

Interest income is recognised using the effective interest method. Distribution income is recognised on declared basis, when the right to receive the distribution is established.

f. Cash and Cash Equivalents

For the purposes of the statement of cash flows, cash and cash equivalents include cash at bank and short term deposits with financial institutions.

Kenanga OnePRS Moderate Fund Annual Report 25

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTD.)

g. Income Tax Expense

Income tax on the profit or loss for the financial period comprises current tax. Current tax is the expected amount of income taxes payable in respect of the taxable profit for the financial period.

h. Unrealised Reserves

Unrealised reserves represent the net gain or loss arising from carrying investments at their fair values at reporting date. This reserve is not distributable.

i. Financial Liabilities

Financial liabilities are classified according to the substance of the contractual arrangements entered into and the definitions of a financial liability.

Financial liabilities are recognised in the statement of financial position when, and only when, the Fund becomes a party to the contractual provisions of the financial instrument. The Fund’s financial liabilities are classified as other financial liabilities. The Fund’s financial liabilities are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method.

A financial liability is derecognised when the obligation under the liability is extinguished. Gains and losses are recognised in profit or loss when the liabilities are derecognised, and through amortisation process.

j. Members’ Contribution

The members’ contribution to the Fund is classified as equity instruments.

Distribution equalisation represents the average amount of undistributed net income included in the creation or cancellation price of units. This amount is either refunded to members by way of distribution and/or adjusted accordingly when units are released back to the Trustee.

k. Functional and Presentation Currency

The financial statements of the Fund are measured using the currency of the primary economic environment in which the Fund operates (“the functional currency”). The financial statements are presented in Ringgit Malaysia (“RM”), which is also the Fund’s functional currency.

l. Distribution

Distributions are at the discretion of the PRS Provider. A distribution to the Fund’s members is accounted for as a deduction from retained earnings.

26 Kenanga OnePRS Moderate Fund Annual Report

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTD.)

m. Significant Accounting Judgments and Estimates

The preparation of financial statements requires the use of certain accounting estimates and exercise of judgment. Estimates and judgments are continually evaluated and are based on past experience, reasonable expectations of future events and other factors.

i. Critical judgments made in applying accounting policies

There are no major judgments made by the PRS Provider in applying the Fund’s accounting policies.

ii. Key sources of estimation uncertainty

There are no key assumptions concerning the future and other key sources of estimation uncertainty at the reporting date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial period.

4. PRS PROVIDER’S REMUNERATION

PRS Provider’s remuneration is computed on a daily basis at a rate up to 5.00% per annum of the NAV of the Fund as provided under Division 17.1 of the Deed. The PRS Provider did not charge any fee for the financial period from 20 November 2013 (date of commencement) to 31 July 2014.

5. TRUSTEE’S FEE

The Trustee’s fee is computed on a daily basis at a rate not exceeding 0.20% per annum of the NAV of the Fund and subject to a minimum fee of RM60,000 per annum for the OnePRS Scheme which consist of Kenanga OnePRS Conservative Fund, Kenanga OnePRS Moderate Fund and Kenanga OnePRS Growth Fund as provided under Division 17.2 of the Deed.

The Trustee’s fee is currently computed at 0.015% per annum of the NAV of the Fund. The Trustee’s fee for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 was borne by the PRS Provider.

6. PRIVATE PENSION ADMINISTRATOR (PPA) ADMINISTRATION FEE AND OTHER EXPENSES

PPA administrative fee is computed on a daily basis at a rate of 0.04% per annum of the NAV of the Fund.

PPA administration fee, auditor’s remuneration, tax agent fees and other administration expenses for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 were borne by the PRS Provider.

Kenanga OnePRS Moderate Fund Annual Report 27

7. INCOME TAX EXPENSE

Income tax is calculated at the Malaysian statutory tax rate of 25% of the estimated assessable income for the financial period. The statutory tax rate will be reduced to 24% effective from year of assessment 2016.

Income tax is calculated on investment income less partial deduction for permitted expenses as provided for under Section 63B of the Income Tax Act, 1967.

A reconciliation of income tax expense applicable to net income before tax at the statutory income tax rate to income tax expense at the effective income tax rate of the Fund is as follows:

20.11.2013 (date of commencement)

to 31.07.2014 RM

Net income before tax 16,020

Tax at Malaysian statutory tax rate of 25% 4,005 Tax effect of:

Income not subject to tax (4,066)Loss not subject to tax 61

Tax expense for the period -

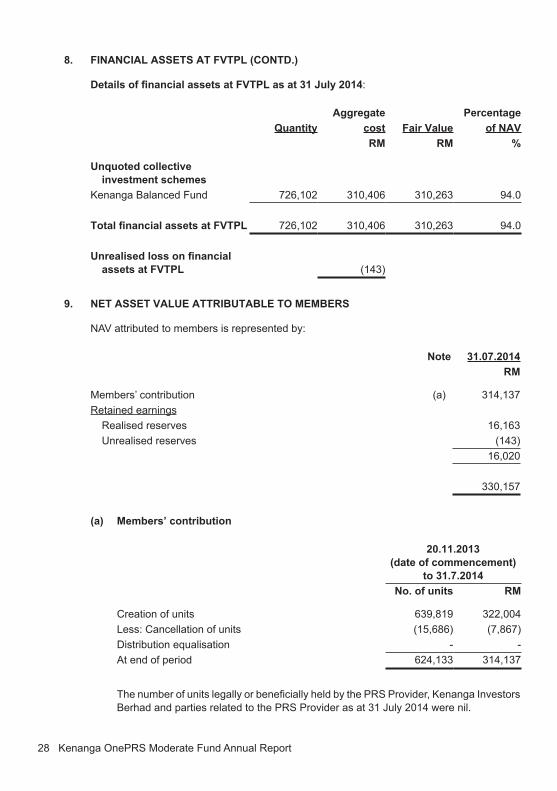

8. FINANCIAL ASSETS AT FVTPL

31.7.2014RM

Financial assets held for trading, at FVTPL:Unquoted collective investment schemes 310,263

20.11.2013 (date of commencement)

to 31.7.2014RM

Net loss on financial assets at FVTPL comprised:Realised loss on disposals (100)Unrealised changes in fair values (143)

(243)

28 Kenanga OnePRS Moderate Fund Annual Report

8. FINANCIAL ASSETS AT FVTPL (CONTD.)

Details of financial assets at FVTPL as at 31 July 2014:

Aggregate PercentageQuantity cost Fair Value of NAV

RM RM %

Unquoted collective investment schemes

Kenanga Balanced Fund 726,102 310,406 310,263 94.0

Total financial assets at FVTPL 726,102 310,406 310,263 94.0

Unrealised loss on financial assets at FVTPL (143)

9. NET ASSET VALUE ATTRIBUTABLE TO MEMBERS

NAV attributed to members is represented by:

Note 31.07.2014RM

Members’ contribution (a) 314,137 Retained earnings

Realised reserves 16,163 Unrealised reserves (143)

16,020

330,157

(a) Members’ contribution

20.11.2013 (date of commencement)

to 31.7.2014No. of units RM

Creation of units 639,819 322,004 Less: Cancellation of units (15,686) (7,867)Distribution equalisation - - At end of period 624,133 314,137

The number of units legally or beneficially held by the PRS Provider, Kenanga Investors Berhad and parties related to the PRS Provider as at 31 July 2014 were nil.

Kenanga OnePRS Moderate Fund Annual Report 29

10. PORTFOLIO TURNOVER RATIO

The portfolio turnover ratio (“PTR”) for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 is 0.71 times.

PTR is the ratio of the average acquisitions and disposals of investments of the Fund for the period to the average NAV of the Fund, calculated on a daily basis.

11. MANAGEMENT EXPENSE RATIO

The management expense ratio (“MER”) for the financial period from 20 November 2013 (date of commencement) to 31 July 2014 is nil.

MER is the ratio of total fees and recovered expenses of the Fund expressed as a percentage of the Fund’s average NAV, calculated on a daily basis.

12. TRANSACTIONS WITH UNIT TRUST FUND MANAGER

Transaction Percentage value of total

RM %

Kenanga Investors Berhad* 310,251 100.0

The above transaction values were in respect of investments in unquoted collective investment schemes. Transactions in these securities do not involve any commission or brokerage fees.

* Kenanga Investors Berhad is the Manager of Kenanga Balanced Fund, the unquoted collective invesment scheme that the Fund invested in during the financial period.

The directors of the PRS Provider are of the opinion that the transactions with Kenanga Investors Berhad have been entered into in the normal course of business and have been established on terms and conditions that are not materially different from that obtainable in transactions with unrelated parties. The PRS Provider is of the opinion that the above dealings have been transacted on an arm’s length basis.

13. SEGMENTAL REPORTING

As the Fund invests primarily in the unquoted collective investment schemes, it is not possible or meaningful to classify its investments by separate business or geographical segments. A summary of the investments portfolio of the unquoted collective investment schemes are disclosed in Note 8.

14. FINANCIAL INSTRUMENTS

a. Classification of financial instruments

The Fund’s financial assets and financial liabilities are measured on an ongoing basis at either fair value or at amortised cost based on their respective classification. The significant accounting policies in Note 3 describe how the classes of financial instruments are measured, and how income and expenses, including fair value gain and loss, are recognised.

30 Kenanga OnePRS Moderate Fund Annual Report

14. FINANCIAL INSTRUMENTS (CONTD.)

a. Classification of financial instruments (Contd.)

The following table analyses the financial assets and liabilities of the Fund in the statement of financial position by the class of financial instrument to which they are assigned and therefore by the measurement basis.

Financialassets at

FVTPL Receivables Total RM RM RM

31.07.2014AssetsUnquoted collective investment schemes 310,263 - 310,263 Cash at bank - 19,745 19,745 Amount due from PRS Provider - 149 149 310,263 19,894 330,157

b. Financial instruments that are carried at fair value

The Fund’s financial assets at FVTPL are carried at fair value. The fair values of these financial assets were determined using prices in active markets.

The following table shows the fair value measurements by level of the fair value measurement hierarchy:

Level 1 Level 2 Level 3 Total RM RM RM RM

Investments:31.07.2014- Unquoted collective investment

schemes - 310,263 - 310,263

Level 1: Quoted prices in active marketLevel 2: Model with all significant inputs which are observable market dataLevel 3: Model with inputs not based on observable market data

The fair value of unquoted collective investment schemes is stated based on the NAV of those unquoted collective investment schemes at reporting date.

c. Financial instruments not carried at fair value and whose carrying amounts are reasonable approximations of fair value

The carrying amounts of the Fund’s other financial assets and liabilities that are not carried at fair value approximate fair values due to the relatively short term maturity of these financial instruments.

Kenanga OnePRS Moderate Fund Annual Report 31

15. CAPITAL MANAGEMENT

The capital of the Fund can vary depending on the demand for creation and cancellation of units to the Fund.

The Fund’s objectives for managing capital are:

a. To invest in investments meeting the description, risk exposure and expected return indicated in its prospectus;

b. To maintain sufficient liquidity to meet the expenses of the Fund, and to meet cancellation requests as they arise; and

c. To maintain sufficient fund size to make the operation of the Fund cost-efficient.

No changes were made to the capital management objectives, policies or processes during the current financial period.

16. COMPARATIVES

There are no comparative amounts presented as this is the Fund’s first set of financial statements since its commencement date.

This page has been intentionally left blank

KENANGA ONEPRS CONSERVATIVE FUND

ANNUAL REPORT

For the Financial Period 20 November 2013 (Date of Commencement) to 31 July 2014

Investor Services CenterToll Free Line: 1 800 88 3737Fax: +603 2057 3722Email: [email protected]

Head Office, Kuala LumpurSuite 12.02, 12th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia.Tel: 03-2057 3688 Fax: 03-2161 8807

Kenanga Investors Berhad (353563-P)