Kenneth Haman Managing Director, The Advisor Institute Fall 2011 Words That Change Minds: Keys to Managing Client Emotions There is no guarantee that any forecasts or opinions in this material will be realized. Information should not be construed as investment advice. Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed Investment Products Offered: For financial representative use only. Not for inspection by, distribution or quotation to, the general public.

Kenneth Haman Managing Director, The Advisor Institute

Fall 2011

Words That Change Minds: Keys to Managing Client Emotions

There is no guarantee that any forecasts or opinions in this material will be realized. Information should not be construed as investment advice.

Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed

Investment Products Offered:

For financial representative use only. Not for inspection by, distribution or quotation to, the general public.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 2

A Different Kind of Volatility: Understanding Client Emotions

Presenter

Presentation Notes

In this presentation, we will be considering a kind of volatility that is different from the usual concept that we talked about in financial services. Every financial advisor is involved in navigating the capital markets and one of the key issues that the advisor must cope with in the capital markets is the issue of volatility, how the value of various investments fluctuates over time. Volatility creates emotional reactions in clients. When investments increase in value, clients experience pleasure and when investments decrease, clients experience distress. The bigger the decrease, the greater the distress and so in a very highly-correlated way, financial volatility corresponds to emotional volatility. In this presentation we will consider ways a financial advisor can understand and then act to manage client emotional volatility. We will look at three different approaches: a long-term strategy, a more mid-term or short-term strategy and an immediate strategy for intervening with a highly-emotional client. The prudent financial advisor will integrate all three strategies into their business management activities.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 3

Understanding Human Behavior: The Basics

Source: Natalie Angier, The Canon: A Whirligig Tour of the Beautiful Basics of Science, “Evolutionary Biology: The Theory of Every Body”. P. 147.

Presenter

Presentation Notes

The biological human being evolved in an environment full of attractive stimulus. There was food to be found, other resources to be gathered and needs to be met through the various resources in the environment and so the human brain evolved with the ability to perceive these resources through the various senses, perceive and understand them and then decide based on motivations and emotions what to do about them. This is the most basic understanding of how the human central nervous systems functions to help the human being navigate in the world. An important awareness needs to be made about the nature of the information that the environment provides for the human being. Information provides insights into not only attractive resources in the environment but also to threats in the environment and so the human being had to evolve various mechanisms within their brain for interpreting both attractive and distressing information and reacting appropriately to it.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 4

The Oldest Part of the Brain Controls “Fight or Flight”…

Sources: George Loewenstein, “Out of Control: Visceral Influences on Behavior,” Organizational Behavior and Human Decision Processes (1996) Dan Ariely, Predictably Irrational: The Hidden Forces that Shape our Decisions, 2008. pp. 89–108.

Presenter

Presentation Notes

If you look at a human brain and dissect it, you’ll find that it’s made-up of many different components, each involved with a different kind of management system for the organism. The brain in fact evolved through several stages as did most of the organs within the human body using evolutionary solutions that were developed earlier and building upon them. The oldest part of the brain is the lower part, that part of the brain that connects with the rest of the body. This is called the brain stem and limbic system and this part of the brain is involved in very instinctive fight-or-flight or very basic functions of motivation. It is this part of the brain where activity is generated, where motion is created. This is a survival mechanism that doesn’t involve a lot of higher-order thinking that other parts of the brain are involved in. The simple way to understand this is to observe how similar this part of the brain is to the brain of a crocodile or a frog or an alligator; very primitive, very much involved in simply eating and/or protecting itself from dangers. This is the part of the brain that it gets activated to get us out of trouble.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 5

…and a Younger Part Controls Language and Rational Thought

Range of Potential Market Returns

Source: “Neo-cortex size as a constraint on group size in primates,” Journal of Human Evolution (1992), Volume 20, pp. 469–493.

Presenter

Presentation Notes

The brain evolved higher-order functions to cope with more complex issues. The neo-cortex or new brain which is located at the top of the head and in front of the skull is involved with the processing of information that is received by the senses. This part of the brain controls rational thought and language. It’s an important piece of information for financial advisors to hold onto, the idea that rational thought and language are highly-related and controlled in the neo cortex. Rational thought, language, long-term planning, the ability to sort out information is all located here and is a critically important part of understanding the importance of controlling emotions or volatility or reactivity with a more rational approach to decision-making.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 6

Language Cause-Effect Relationships Future and Planning Self-Awareness & Observation

Feelings Physical Actions Impulsivity Fight or Flight Instinct

Taking a Closer Look: Two Very Different Structures

Presenter

Presentation Notes

At this point we have enough information to make a basic observation on behalf of a financial advisor. When looking at a human being, you really do need to see the human being as functioning with two different types of thinking patterns, essentially two different brains. There’s the rational brain that processes language, cause-effect or planning relationships, future orientation and also self-awareness and observation. It’s truly the rational operation centers of the brain. And then there is the lower, more instinctive brain that controls emotions, feeling, physical activity, impulsitivity, fight or flight. This part of the brain has no language skills. Now this is an important concept and deserves repetition. No language skills are located here. When this part of the brain is thoroughly activated, the human being is in a completely instinctive, completely impulsive state of mind for the language, rational thought. All of the dynamics that we use to help humans navigate decisions have been significantly impaired and this is the key to understanding what we need to do to help clients manage their volatility.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 7

What Happens When a Client Becomes Anxious or Afraid?

Three strategies can help you manage emotional volatility

Presenter

Presentation Notes

This key insight - the idea of the two brains - helps us understand what we’re looking at when we see a distressed client. The client perceives information in the environment, and then based on the human being’s understand and interpretation of that information, which is a combination of that information and their personal experiences, the human being begins to create a reaction. Essentially that information is processed in the neo-cortex and then the lower portion of the brain gets involved to decide what actions should be taken. For benign information or attractive information, the central nervous system may decide that there’s no great need to take strong emotional action but for threats, it’s a different story. A threat will create an immediate instinctive and impulsive reactivity and cause the client to seek to protect him or herself with the fight-or-flight instinct and this reactivity - this emotion volatility - results in terrible investment decisions and actually interrupts the ability of the client to navigate the capital markets successfully. Fortunately there are strategies that a financial advisor can effect to interrupt this process and restore the rational thinking process to a highly emotional and volatile individual. Let’s take a look at these strategies now.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 8

Strategy #1: Publish Your Principles

Presenter

Presentation Notes

As we mentioned at the beginning of the presentation, we’ll be looking at three different strategies that a financial advisor can combine together for an effective process of managing client emotions. The first is a long-term strategy - something that should be effected on a regular basis - a series of interventions with clients that should be done consistently as part of the management of the client relationship. It will have its greatest effect the longer this strategy is employed with clients.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 9

Strategy #1: “Principles” Can Over-ride Natural Reactions

Fearful/Greedy

“The time to get greedy is when everyone else is fearful; the time to get fearful is when everyone else is greedy.” Warren Buffett

“Regression to the mean is one of the most powerful forces in the universe.” Rod Smith

Regression to the Mean

“Good investment decisions are never based on fear, and are never made impulsively.” Ken Haman

Good Investment Decisions

Presenter

Presentation Notes

One of the wonderful aspects of working with human beings is their ability to take-in information from the perceptions and process it in the neo-cortex. Through interactions, conversations, through the delivery of information to clients over time, the financial advisor can literally install thinking patterns that can be used by the client to make sense of and interpret the world. One source of information for clients to use are the principles that financial advisors use to make decisions about the markets. These are principles that can function as a filter of information that the client can use to navigate decisions in the world. There are many different principles that are involved in investing and each financial advisor will use a cluster of these principles as part of their professional navigation of the markets. We offer a few here and suggest that over time and through repetition, a financial advisor can actually install these principles in the mind of the client and the client can begin to use these principles to navigate the world in a different way than they would without those principles with just their natural reactivity to the world around them.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 10

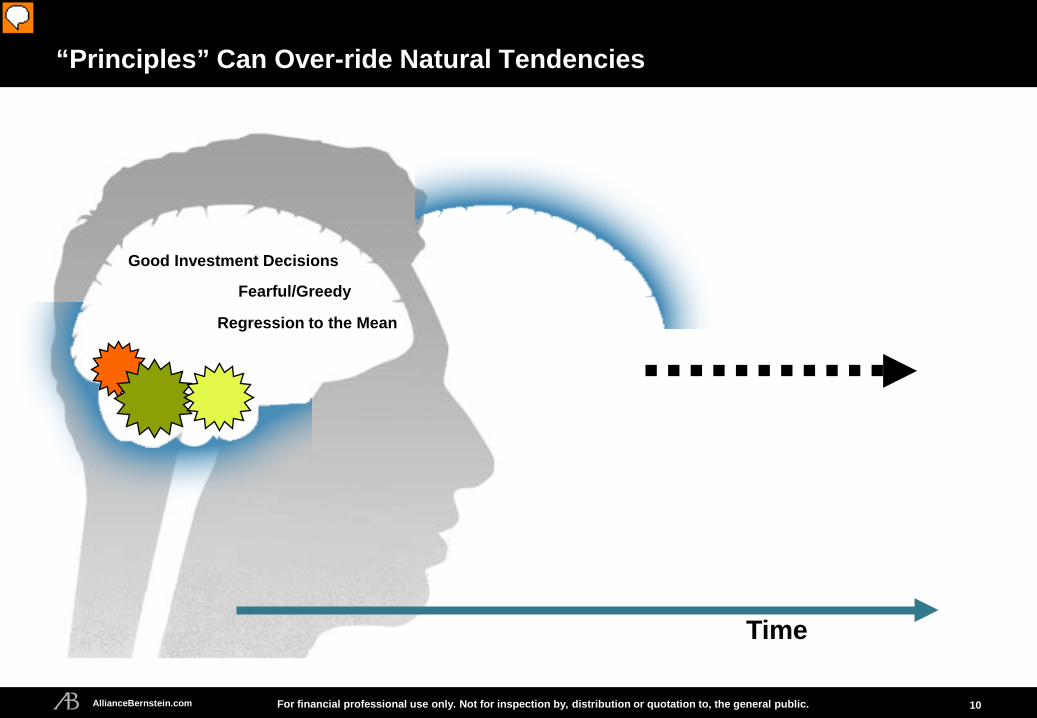

“Principles” Can Over-ride Natural Tendencies

Fearful/Greedy

Regression to the Mean

Good Investment Decisions

Time

Presenter

Presentation Notes

The idea here is actually quite simple. The client, having installed these principles, will continue to navigate over time. And through repetition, these principles can become more and more important in their thinking patterns. As events happen in the marketplace, these principles are activated and essentially provide a way to think about what’s going on so that instead of a decrease in the valuation of an investment being seen by the client as a devastating or frightening experience, the client may be able to actually see that information differently and see it as an opportunity to increase their investment well-being through purchasing more of what is in essence a discounted investment. The role of principles to help a client understand the world around them and become a more effective investor is critically important and while it doesn’t function in the short term to bring a client back into rational thinking, it does function in the long term to inoculate the client from highly-emotional decision-making.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 11

Human beings tend to misperceive risks

Economic processes tend to regress to a mean

Investors tend to extrapolate current trends forward

The time to get greedy is when others are fearful and the time to get fearful is when others are greedy

The investor is always exposed to risk. Investing well is being paid properly for the risk you decide to take

Owning non-correlating assets reduces volatility risk during most market conditions

In stock selection the business model, corporate leadership and qualitative fundamentals matter

Derived investments tend to magnify risk in order to increase returns

“Timeless Principles of Investing”—Your Professional Convictions

Presenter

Presentation Notes

The place for the financial advisor to start in creating an understanding about principles is with his or her own professional principles, those ideas that the financial advisor uses to navigate the capital markets. This is in fact what it means to be a professional, to have studied and experienced the discipline that they’re practicing and having erected a reliable set of guiding ideas or principles for their decision-making. The idea here is to start by extracting clearly-defined principles from the decisions that you make so that you can use these concepts verbally with clients to help them create a more rational approach to investing.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 12

Defining Your Principles: Resources for More Confident Investors

Step One: Define 7–10 Core Principles Look at the key investment decisions that you have made over the past two years

Step Two: Define the Principle that Informed Each Decision At the root of each decision was a principle that guided your decision; write it down

in a sentence or two

Step Three: Refine Each Principle Edit each principle down to a short phrase or a single sentence Create at least seven but no more than 10 “core principles” for your practice

Step Four: Inoculate Your Clients with a Shared Vocabulary Install these principles into your clients through constant repetition:

During Annual Client Reviews

When Markets Become Volatile

During Regular Market Updates

Presenter

Presentation Notes

As an exercise, let’s consider this process of defining principles. We’ll consider a four-step exercise that any financial advisor can pursue. First, look back over the key investment decisions you’ve made over the past two years. Analyze each of these decisions and look for the core guiding idea that you use to inform that decision, an idea that would inform many decisions of a similar type. At the root of each decision, you’ll find that idea. You didn’t use your instincts, you didn’t use your “gut.” What you used was an idea, a principle that you wanted as you’ve mastered your craft. So take Step 2, take all of these ideas and begin to look at them not just from the concept of the decision you made but as an idea that can be communicated. So edit the idea down into a tight, single sentence of even a phrase. We’ve given you some examples in previous slides but the idea here is not so much to copy those examples but to find your own core principles that you believe in and trust. As each principle in Step 3 begins to emerge and become a tighter, more clear, easy-to-understand expression, burn that list down to at least seven but no more than 10 core principles that you will embrace as guiding the decisions of your practice. Having at least seven principles allows for an adequate sense of the complexity and sophistication of your process but trying to work with more than 10 will become overwhelming to your clients. Finally resolve to inoculate your clients with this shared vocabulary. In essence the idea is to repeat these principles in so many times and places and through so many media that the client begins to take these principles on to essentially internalize them and by internalizing them begin to use them themselves without you needing to be there to remind them. This is the essential strategy for using principles to manage client volatility over time and while it is a long-term process, it is a very effective way of creating more cooperative and effective clients.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 13

Strategy #2: Provide a Point of View

Presenter

Presentation Notes

In the second strategy, we’ll look at a more near-term process, moving away from the big guiding principles and timeless ideas in investing to a more immediate intervention with the client’s thinking patterns about the markets.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 14

Strategy #2: Helping Clients Make Sense of the Capital Markets

Presenter

Presentation Notes

As a quick review of the ideas behind these strategies, let’s revisit again what happens to a client neurologically when they see something in the environment that distresses them. First there is the perception of the information, the observation of the dynamics going on in the environment. There is a brief pattern internally of interpreting that information and then the brain decides if this is a distressing piece of information and that it needs to activate the impulsive protective fight-or-flight instincts to cope with it. This is a process that happens in all human beings. It happens quite automatically and unfortunately it can lead to a tremendous amount of emotionalism, impulsivity and bad investment decision-making.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 15 15

Assigning Labels Creates Meaning: New Labels = New Meanings

One part of the brain uses information to make sense of an investment

A different part of the brain decides to take action based on feelings

For illustrative purposes only.

What does this mean? What do we think is going to happen next? What is the right thing to do?

Presenter

Presentation Notes

New labels equal new meanings. In this short-term strategy we’re talking about, we need to remember that there are two parts of the brain operating, one to make sense of what’s going on in the world - in this case the world of investing - and the other making a decision to take a particular kind of action and that action will be based on the feelings that get stirred-up. So it’s essentially a two-part process of perception and then generating feelings. The perceptions have to assign a meaning to the event so the brain is always asking the question, “What does this information mean? What do we think is going to happen next and what’s the right thing to do? Based on what the brain concludes is going to happen next, and this is critical so I’ll repeat it again, based on what the brain thinks is going to happen next, the brain decides whether this is a good thing or a bad thing. If it decides it’s a bad thing, the brain gets activated with a threat, the client decides the right thing to do is to either fight it or flee from it, the fight-or-flight reaction. And this is the key to understanding the second strategy which is called Providing a Point of View - essentially helping the client make a different kind of meaning than their natural tendencies will make of what’s going on in the world.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 16

Changing the Way Clients Think: The Power of a “Point of View”

The rational brain processes information and makes meanings

The primitive brain reacts to meanings emotionally

Without a “point of view” about the Capital Markets, the primitive

brain decides impulsively according to instincts

Through constant education, your professional “Point of View” can

become the perspective from which the client views Market behavior.

Over time the client becomes less impulsive

and more thoughtful: “I know what this means!”

Time

Presenter

Presentation Notes

This creates a very dynamic experience within the client that the financial advisor can manage. First, the rational brain is processing the information and making a meaning. Then the primitive brain is activated by the meanings that the rational brain makes and the impulsive actions are decided upon and that the body then just gets activated. As these two things come together, there is a constant conflict between the two. Without a point of view, without a thoughtful perspective on the markets, the brain will decide frequently that threats are occurring and that these threats must be dealt with instinctively. This is a natural occurrence. It’s well-studied in the disciple of behavioral finance. If however the financial advisor can provide education and a constant reflection of meaning about the markets, talking about what’s going on in the markets and what’s likely to happen next, the client can begin to see the patterns of positive opportunity. The can stop believing that these things are threatening and start making the meaning that there’s positive future outcomes available. As that happens over time, those meanings become more apparent and the client becomes less impulsive. Essentially the client can say I know what this pattern means. The client makes a different meaning and can actually become excited about shifts in the marketplace rather than distressed by them.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 17

Providing a Point of View: Explaining Mechanisms Creates New Labels

Step One: Define 5–7 key aspects of the Capital Markets What are the important Mechanisms of the Capital Markets that you monitor on an ongoing basis? 5–7 will be most influential on your thinking:

Monetary Policy/Inflation Domestic/Global GDP Equity Valuations Fixed Income-Global Bond Markets Currency Market Fluctuations Growth Investing Trends Value Investing Trends Large, Mid- and Small-Cap Trends Global Investment Dynamics Real Estate/Housing Oil and Other Commodities Sector Dynamics Trends in Corporate Profitability Consumer Sentiment Major Political Events Natural Disasters with Global Impact

Step Two: What are the cause-effect mechanisms involved?

Step Three: What “causes” are currently happening?

Step Four: For each cause—what is likely to happen next?

Presenter

Presentation Notes

Just as before, we suggested an exercise for the financial advisor to grapple more effectively with this issue, so in this regard, we suggest that a financial advisor considers a very systematic approach to this kind of educational process. In this four-step exercise we suggest you look at the capital markets and at any given time, perhaps helped by this list of issues that are common to capital markets, pick at least five but no more than seven of these areas as being those parts of the markets that we need to pay special attention to and understand in order to make effective investment decisions. For each of those five to seven aspects of the markets, the financial advisor can pull apart and create an understanding of the cause-effect mechanisms involved. What are the processes involved in the sense of let’s say fixed income investing, the global bond markets in this marketplace or the impacts of oil price fluctuation or commodity pricing at this time in the market cycle? How does this part of the marketplace usually work. This is an attempt to help the client understand the mechanisms of this part of the marketplace. Then in Step 3 we look to understand the mechanism, what’s going on in this part of the market right now that will lead to future outcomes. And then finally in Step 4 the financial advisor can offer his or her point of view and personal convictions, those convictions they are personally operating with. What he or she thinks about what is going to happen next in this important part of the marketplace. In this regard in a very simple way, over time again the client can be helped to understand what’s going on. This intervention can work virtually immediately if the brain understands what this information means. If so, the brain can come to a different sort of conclusion.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 22

2

4

6

8

60 70 80 90 00 10

Perc

ent

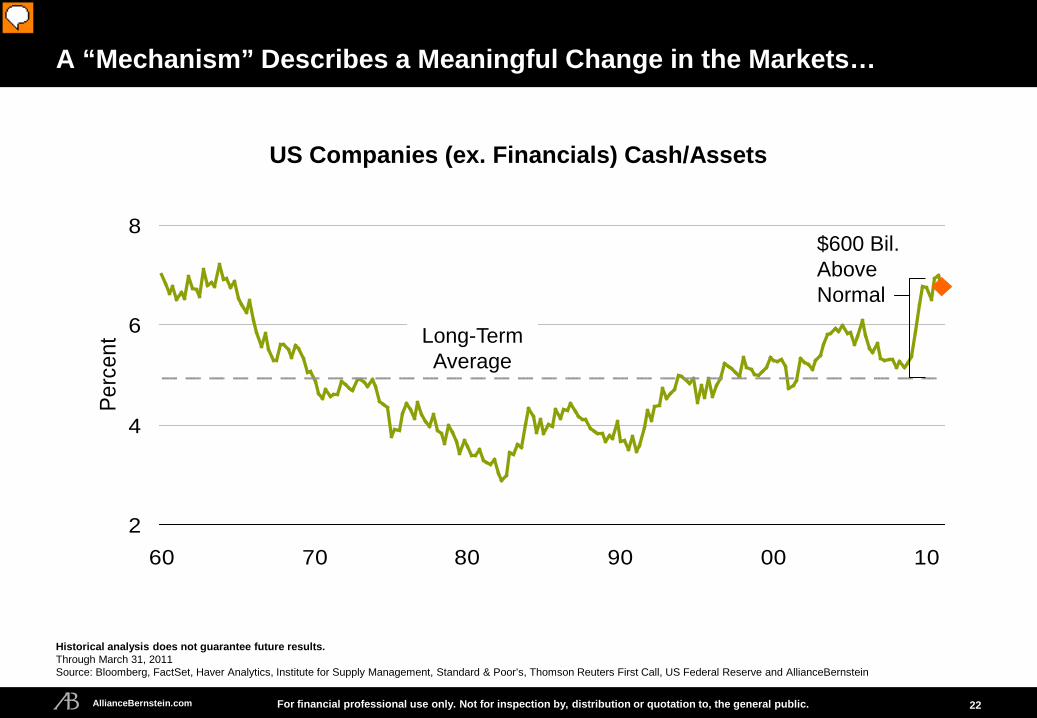

$600 Bil. Above Normal

Long-Term Average

Historical analysis does not guarantee future results. Through March 31, 2011 Source: Bloomberg, FactSet, Haver Analytics, Institute for Supply Management, Standard & Poor’s, Thomson Reuters First Call, US Federal Reserve and AllianceBernstein

US Companies (ex. Financials) Cash/Assets

A “Mechanism” Describes a Meaningful Change in the Markets…

Presenter

Presentation Notes

So while the client can become concerned and take action to protect themselves, we want to promote rational action rather than emotional impulsive action so a client can see where there are opportunities to take advantage of volatility. For example in a market cycle in which corporations have growing cash or assets in excess of the long-term average, the cause-effect mechanism is setup and historical analysis can confirm that this could be advantageous for particular types of investments.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 23

0

5

10

15

20

25

05 06 07 08 09 10 11

…And Experience Over Time Suggests a Possible Future Result

Historical analysis does not guarantee future results. As of June 30, 2011 Based on the Bernstein US stock universe Source: Standard & Poor’s and AllianceBernstein

Ratio of Dividend Increases/Decreases

Presenter

Presentation Notes

This observation in research over time showing how a correlation between excess cash and assets on hand for corporations translates into increasing dividends. This suggests to a client that this may be an opportune time to consider investment into dividend-paying stocks that may benefit from this type of activity in the market cycle. This creates a rational decision platform for the client but it’s only available to the client if the client has the information and the interpretation from the advisor.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 27

Strategy #3: Put it Into Practice

Presenter

Presentation Notes

In our last strategy, we will consider a virtually immediate or interventionary strategy for a highly-distressed client. Unfortunately a financial advisor must accept that even a well-trained client who has been exposed to and has fully embraced a set of meaningful principles for navigating investing and is using a more professional, more well-informed point of view to make sense of the world can become distressed by events in the marketplace. And so in that case the financial advisor should be prepared to have a very particular kind of conversation with the client in order to bring them back to a more rational state of mind so that a well-formed decision can be made.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 28

Step One: Listen Actively and Engage Language Skills

“How are you feeling about things? Say more…”

Get the client to speak (use language) for several minutes

This activates the rational part of the brain and inhibits the impulsive part

Listen attentively Ask for more information but do not try to

address issues or concerns—your rational ideas will not be heard or understood

Presenter

Presentation Notes

We’re back to our original model again and in this case showing the central nervous system of the client fully activated and in an impulsive state of mind. The client comes in very distressed. A financial advisor must remember that with that impulsive primitive brain fully in charge of the client’s functioning, the client is in a full fight-or-flight activation and no use of language will be able to penetrate and inform the way that client’s navigating at this point in time. Therefore this being true, the task of the financial advisor is to get the rational brain turned on. So the key strategy to start this process is to ask the client to talk about how they’re feeling about things, to say more about what’s distressing them once they come in and start the meaning. The key idea here is this. Once the client starts speaking they have to use their rational brain to form the words and deliver the sentences in the conversation. So if the financial advisor will simply listen and encourage the client to keep speaking, gradually the rational brain turns on and the impulsivity within the primitive brain begins to become less controlling of the human’s behavior.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 29

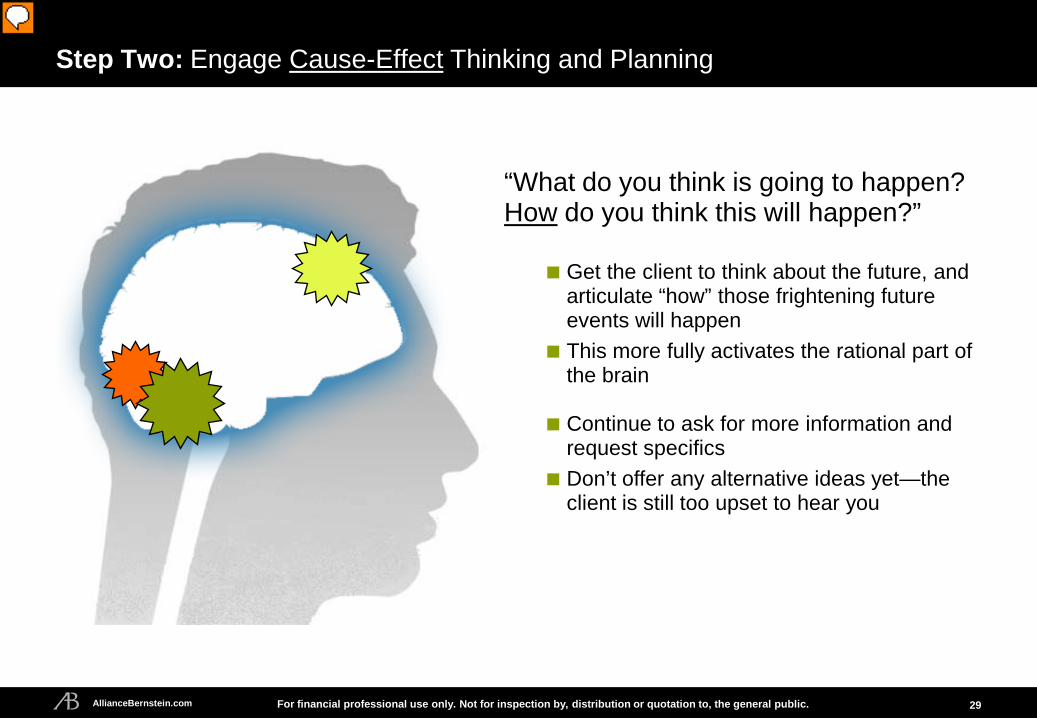

Step Two: Engage Cause-Effect Thinking and Planning

“What do you think is going to happen? How do you think this will happen?”

Get the client to think about the future, and articulate “how” those frightening future events will happen

This more fully activates the rational part of the brain

Continue to ask for more information and

request specifics Don’t offer any alternative ideas yet—the

client is still too upset to hear you

Presenter

Presentation Notes

This conversation therefore starts with the question, “How are you feeling?” but after a few minutes as the client begins to use well-formed sentences and engages their language skills, the financial advisor needs to move the process along to the next stage and that is to get the client’s planning functions activated as well. Language is key but planning is the destination and so the second question the advisor should ask after a few minutes have elapsed is to get the client to say what they think is going to happen and more importantly to ask the question, “Okay, I hear you think that this is going in this direction and something terrible is going to happen; how is that going to happen?” This forces the client to analyze their own conclusions and more fully activates the rational brain. Continue to ask this question, “Well, how’s that going to happen? What’s going to cause that?” and get the client to think very, very concretely and rationally about the conclusions they’ve come to. An important piece of guidance here is that the financial advisor should simply continue asking questions and never offer any ideas to the client. It’s too soon. They won’t be able to use them.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 30

Step Three: Engage the Client’s Self-Awareness and Rational Thought

“Is that what you think? Or, is that just how it feels right now?”

Clients do not fear what has already happened—they feel loss and sadness

Clients become fearful of the mental images of what might happen

Invite the client to observe the difference between thinking and feeling

Allow him to discover how the fears are not based on rational thoughts—to shift gears mentally

It still isn’t time to offer a perspective

Presenter

Presentation Notes

So at this point after five or 10 minutes in the conversation, the client will be clearly less emotionally-activated and far more rationally-activated and this is time to finish the process of activating the neo-cortex by getting the client to self-observe. Remember, the neo-cortex - the new brain, the more rational part of the brain - is the place where critical thinking, rational analysis, language patterns and self-observation are located and so in this regard, you know, you need to understand that the client is not fearing what’s already happened. They’re fearful of the images they’re making in their mind of what might happen so the client can be invited to observe the difference between thinking patterns and feeling patterns. And so if you can ask the client, “Is this what you really think of what’s going to happen or are you just feeling frightened right now and reacting to those mental images? Is that what you think or is that just how it feels right now?” is the question to allow the client to discover, you know, it is how they are feeling. Allow the client to look at themselves in terms of the way they’re making decisions because the advisor can say to the client, “Well, of course you’re upset. I totally understand that but I really don’t want us to use emotions and impulsive thinking patterns to make an investment decision that may have tremendous impacts on your future well-being.”

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 31

Step Four: Normalize and Then Provide Resources

“I understand how you feel–many people have felt that way. But, we have found…”

When the rational part of the brain is fully activated a more thoughtful and less impulsive decision can be made

The client is now able to hear and make

sense of the ideas and information you have to offer

Only offer your insights when the client is

calm and more thoughtful

Presenter

Presentation Notes

This allows the client to finally activate the full rational thinking patterns. There may still be fears and emotionality but the neo-cortex is now more fully-activated. And so it’s time to make a shift at this point and only at this point to begin providing the thoughtful resources and ideas, to return to the point of view conversation that you’ve had at other times because the client now can understand that their feelings are normal but they shouldn’t become the controlling force of the investment decisions. The way to do that is simply to say this: “Hey, I understand how you feel. Many people have felt that way. Hey, I feel that way from time to time but I have to remind myself” and then proceed to unpack part of your point of view about the markets and help the client think about the cause-effect dynamics. This will not work with every client every time and there’s no way to protect yourself totally from client emotionality but after many repetitions of your point of view and especially if you’ve been engaged in sharing your principles, a client can be brought back to a more rational frame of mind using this pattern when they’re highly emotional and you can save the client from impulsive decision-making that yields bad long-term investment results.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis 32

Publish Your Principles - Constantly Provide a Point of View - Regularly Put It Into Practice - When Needed

Review: Three Strategies for Managing Client Emotions

Presenter

Presentation Notes

The idea here is to think about managing client emotions on the long term with three distinct strategies that give you tools for intervening reliably with your clients. First and constantly, publish your principles. Give your clients an opportunity to see how the principles that you use work to validate your professionalism and to internalize those principles and make them their own. By using principles as a common vocabulary, you create a more resilient client. Secondly on an ongoing and quite regularly, provide a point of view. As markets shift, shift when them and offer new insights. Return to the cause-effect relationships that the client needs to use. Help the client be able to look at the markets and understand what’s going on there. This is essential for financial advisors and while it does it take time, the benefits of it over time far outweigh the cost of the investment and finally when needed, intervene effectively with your clients by helping them activate their rational thinking. Reduce their impulsive thinking and be able to use the point of view information you give them about the capital markets.

AllianceBernstein.com For financial professional use only. Not for inspection by, distribution or quotation to, the general public. Never Waste a Good Crisis

Important Disclosure Information

This material was created for informational purposes only. It is important to note that not all Financial Advisors are consultants or investment managers; consulting and investment management are advisory activities, not brokerage activities, and are governed by different securities laws and also by different firm procedures and guidelines. For some clients, only brokerage functions can be performed for a client, unless the client utilizes one or more advisory products. Further, Financial Advisors must follow their firm’s internal policies and procedures with respect to certain activities (e.g. advisory, financial planning) or when dealing with certain types of clients (e.g. trusts, foundations). In addition, it is important to remember that any outside business activity including referral networks be conducted in accordance with your firm’s policies and procedures. Contact your branch manager and/or compliance department with any questions regarding your business practices, creating a value proposition or any other activities (including referral networks.)

Presenter

Presentation Notes

READ SLIDE

AllianceBernstein® and the AB Logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P.