june 2009 cleveland plus economic review (team neo)

DESCRIPTION

Team Northeast Ohio (Team NEO) released the latest edition of the quarterly Cleveland Plus® Economic Review today with a focus on the region’s growing Professional, Scientific and Technical (PS&T) Services sector. GRP for the sector has grown 79% since 1993, outpacing the nation’s average in several industries. Fueling this growth is the region’s strong heritage of invention, a strong base of significant research institutions, and a growing entrepreneurial sector. Also noted in the report: PS&T has added 21,000 new jobs in the Cleveland Plus region since 1993 : 21% of total job creation (1 in 5 new jobs) Scientific Research and Development growth in Northeast Ohio has more than doubled U.S. growth in the same time periodTRANSCRIPT

Our partners include:Greater Cleveland Partnership

Greater Akron ChamberStark Development Board

Team Lorain CountyYoungstown-Warren Regional Chamber

Medina County Economic Development Corporation

Cleveland Plus® Economic ReviewJune 2009Volume 3, Issue 2

Growing Professional, Scientific and Technical Services Sector Generates Opportunity in Cleveland Plus Region

June 2009 | Volume 3, Issue 2

All PS&T Services Industries are Growing

In the September 2007 edition of the Northeast Ohio Economic Review, we reviewed the sectors that accounted for the 30% growth in Gross Regional Product (GRP) from 1992–2007. As evidenced by the chart below, several sectors had significantly grown in that time, including Professional, Scientific and Technical (PS&T) Services, which grew 74%.

While it is expected that PS&T would grow due to global advances in technology, such significant growth in Northeast Ohio may be surprising because of our strong industrial manufacturing base. This prompted further exploration into this sector.

This report investigates this sector to better understand the factors that are driving such remarkable growth in the Cleveland Plus region.

Updated for the fifteen years between 1993 and 2008, the PS&T GRP has grown more than 79%, with growth realized in all segments. Several industries, such as Computer Systems Design, Scientific Research & Develop-ment, Management, Scientific and Technical Services grew by more than 150%. Certainly, these service industries are contributing to diversifying Northeast Ohio’s economy. As the region’s manu-facturing sector is becoming more advanced with robotics and automation, and other sectors, such as Biomedical and Information are growing, technical services are in greater demand.

Legal Services

ComputerSystems Design

Architectural &Engineering

Scientific &Tech Consulting

Accounting &Tax Prep

Other Professional,Scientific & Tech

Advertising

Scientific R&D

$0 $500 $1000 $1500 $2000 $2500

GRP in Professional, Scientific & Technical Industries(1993-2008)

1993 2008(Millions 2008 $)

169%

48%

48%

21%

165%

38%

173%

76%

Source : Moody’s Economy.com

Continued Growth in Professional, Scientificand Technical Services Sector

Information

Management of Companies/Entps

Public Aministration

Manufacturing

Health Care & Social Asst

Prof, Sci & Tech Services

Wholesale Trade

Retail Trade

Finance & Insurance

All Other Industries

Real Estate, Rental & Leasing

$0 $5 $10 $15 $20 $25 $30 $35 $40

Real GRP Change : 1992-2007Billions (2006 Dollars)

2007 GRP 1992 GRP

58%

22%

60%

56%

51%

74%

38%

64%

88%

16%

6%

Source : Moody’s Economy.com and Northeast Ohio Economic Review September 2007

Management, Scientific and Technical Services, and Computer Systems Design have both grown by approximately 170% in Northeast Ohio.

Many industries within the PS&T Services Sector have also realized employment growth throughout the last 15 years. Not only is this sector driving regional growth in GRP, but it also requires a growing, skilled workforce. Scientific and Technical Consulting employment has grown nearly 100%, while Computer Systems Design has grown 129%. In total, increases in employment in the PS&T Services Sector account for more than 21,000, or 21%, of the 99,500 new jobs added to the region between 1993 and 2008.

PS&T Sector has added 21,000 new jobs since 1993.

Significant Employment Growth in Many PS&T Services Sector Industries

Legal Services

Accounting &Tax Prep

ComputerSystems Design

Architectural &Engineering

Scientific &Tech Consulting

Other Professional,Scientific & Tech

Advertising

Scientific R&D

0 2000 4000 6000 8000 10,000 12,000 14,000 16,000 18,000 20,000

Employment in Professional, Scientific & Technical Industries(1993-2008)

1993 2008

81%

5%

30%

98%

-5%

129%

12%

28%

Source : Moody’s Economy.com

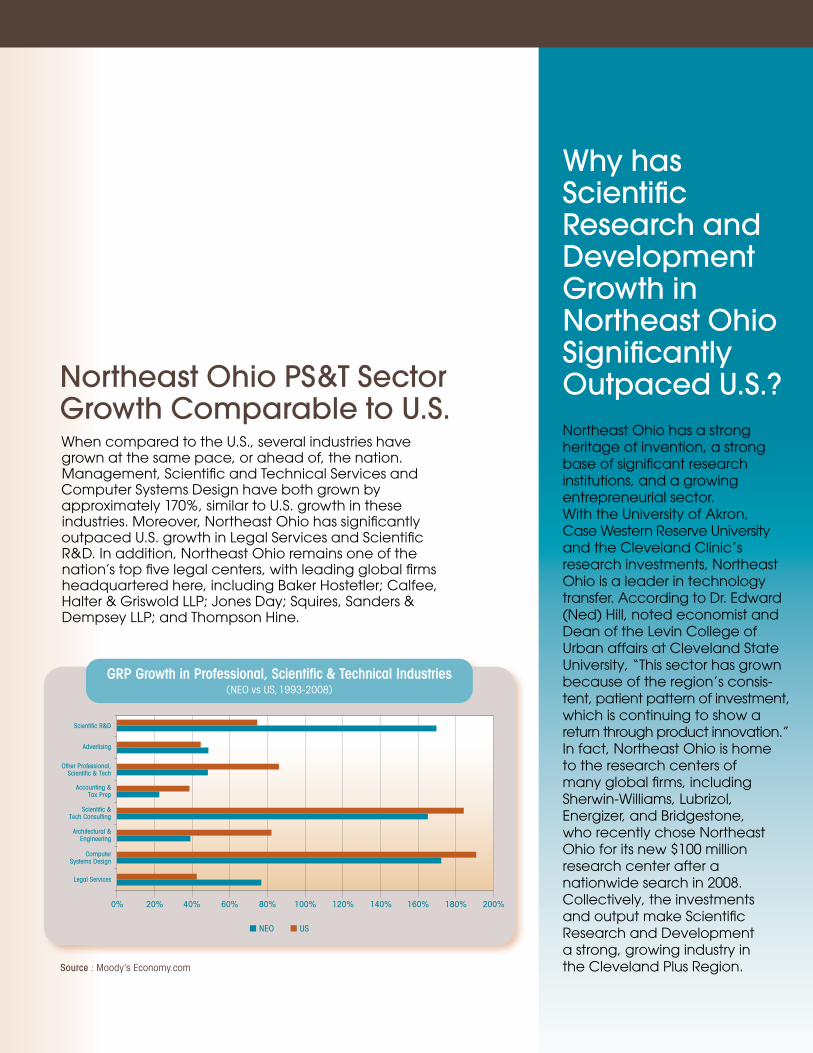

Northeast Ohio PS&T Sector Growth Comparable to U.S.

Source : Moody’s Economy.com

Legal Services

ComputerSystems Design

Architectural &Engineering

Scientific &Tech Consulting

Accounting &Tax Prep

Other Professional,Scientific & Tech

Advertising

Scientific R&D

0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 200%

GRP Growth in Professional, Scientific & Technical Industries(NEO vs US,1993-2008)

NEO US

Why has Scientific Research and Development Growth in Northeast Ohio Significantly Outpaced U.S.?Northeast Ohio has a strong heritage of invention, a strong base of significant research institutions, and a growing entrepreneurial sector. With the University of Akron, Case Western Reserve University and the Cleveland Clinic’s research investments, Northeast Ohio is a leader in technology transfer. According to Dr. Edward (Ned) Hill, noted economist and Dean of the Levin College of Urban affairs at Cleveland State University, “This sector has grown because of the region’s consis-tent, patient pattern of investment, which is continuing to show a return through product innovation.” In fact, Northeast Ohio is home to the research centers of many global firms, including Sherwin-Williams, Lubrizol, Energizer, and Bridgestone, who recently chose Northeast Ohio for its new $100 million research center after a nationwide search in 2008. Collectively, the investments and output make Scientific Research and Development a strong, growing industry in the Cleveland Plus Region.

When compared to the U.S., several industries have grown at the same pace, or ahead of, the nation. Management, Scientific and Technical Services and Computer Systems Design have both grown by approximately 170%, similar to U.S. growth in these industries. Moreover, Northeast Ohio has significantly outpaced U.S. growth in Legal Services and Scientific R&D. In addition, Northeast Ohio remains one of the nation’s top five legal centers, with leading global firms headquartered here, including Baker Hostetler; Calfee, Halter & Griswold LLP; Jones Day; Squires, Sanders & Dempsey LLP; and Thompson Hine.

1.75

1.80

1.85

1.90

1.95

2.00

2.05

2.10

(Mill

ions

)

NEO Total Employment (Not Seasonally Adjusted)

2003

2004

2005

2006

2007

2008

2009

2003

2004

2005

2006

2007

2008

2003

2004

2005

2006

2007

2008

2003

2004

2005

2006

2007

2008

Q1 Q2 Q3 Q4

NEO Total Employment Reflective of World EconomyBecause of seasonal patterns, this chart compares total employment year over year.

There is a typical drop in employment from Q4 to Q1. The decline was 4% from Q4 2008 to Q1 2009, only slightly higher than the decline of 3% that occurred last year. Overall, total employment in Q1 was down about 4% from a year ago.

Soft Economy Reflected in GRP ProjectionsAs expected, GRP for the region in 2009 is estimated to show a moderate decline at 0.7%. In addition, the GRP was revised downward for 2008 (-5.5% growth), putting Northeast Ohio in line with the decline in the nation as a whole. As data are updated, these numbers are subject to revision. Real GRP Average Annual Growth = 0.7%

$120

$130

$140

$150

$160

$170

$180

$190

(-1.1%)0%(-1.0%)0.5%2.4%1.8%

1.2%(-1.9)%0.3%1.2%

2.6%4.8%

3.0%3.8%

5.1%

NEO Real GRP Billions (2008 Dollars)

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

(-5.5%)(-0.7%)

NEO Unemployment Rate Similar to National RateWhile the regional unemployment rate has been following the pattern of both the U.S. and Ohio, most recent figures indicate that the region is continuing to narrow the gap between Northeast Ohio and the U.S. as a whole. The unemployment rate in Northeast Oho increased by 2.85% in Q1 09, bringing the rate to 9.97%. This increase is less than both the state of Ohio (4.03% increase) and the U.S. (3.08% increase).

Source : Ohio Labor Market Information (LAUS Data)

4.0%4.5%5.0%5.5%6.0%6.5%7.0%7.5%8.0%8.5%9.0%9.5%

10.0%10.5%11.0%11.5%12.0%

NEO Quarterly Unemployment Rate

NEO 16 counties Ohio U.S.

Q1

Q2

Q3

Q4

2003

Q1

Q2

Q3

Q4

2004

Q1

Q2

Q3

Q4

2005Q

1

Q2

Q3

Q4

2006

Q1

Q2

Q3

Q4

2007

Q1

Q2

Q3

Q4

Q1

2008

Source : Ohio Labor Market Information (LAUS Data)

Source : Moody’s Economy.com

737 Bolivar Road, Suite 2000, Cleveland, Ohio 44115888.NEO.1411 • www.clevelandplusbusiness.com

375

380

385

390

395

400

405

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

Occ

upie

d Sq

uare

Fee

t (M

illio

ns)

Vaca

ncy

Rate

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q4

Q1

Q1

Q2

Q3

2004 2005 2006 2007 2008 09

NEO Occupied Industrial Space & Vacancy Rate

Vacancy RateOccupied Square Feet

June 2009 | Volume 3, Issue 2

Demand for Industrial Space Remains Strong

This graph shows the total amount of industrial space occupied by quarter between the first quarter of 2005 and the first quarter of 2009. In the first quarter of 2009, Northeast Ohio had a total stock of occupied industrial space greater than 400 million square feet. The Northeast Ohio Industrial vacancy rate was stable at 7.5% in the first quarter of 2009, remaining steady through the current economic downturn.

About Team NEOTeam NEO advances Northeast Ohio’s economy by attracting businesses worldwide to the 16-county Cleveland Plus region. The organization is a joint venture of the region’s largest metro chambers of commerce. Since 2007, the organization has attracted 23 new companies, 2,500 new jobs and more than $75M in annual payroll to Northeast Ohio, leading to a total regional annual impact of $150M. For more information, visit www.clevelandplusbusiness.com.

Data Sources: Team Northeast Ohio uses a number of data sources for the Regional Economic Review. One of the primary sources is the Moody’s Economy.com (www.economy.com) Northeast Ohio modeling system. This firm is the leading independent provider of economic, financial and industry research and data that specializes in national and metropolitan economic growth forecasts. Moody’s Economy.com county level output, employment and payroll historical data are estimated from several publicly available sources and are summarized into the Team NEO regional footprint. It is important to understand data provided by Economy.com are estimates of economic activity.

Team NEO also uses data from federal and state sources as part of the report. As with Economy.com, the information for the Team NEO footprint is derived from data reported at either the county or metropolitan level. We rely heavily on data from the U.S. Bureau of Labor Statistics (www.bls.gov) and Ohio’s Labor Market Information (www.lmi.state.oh.us) for information on wages, unemployment and both general and industry-specific employment. In addition, Team NEO uses data from the Census (www.census.gov) to track housing-related activity including the number of single and multifamily permits, as well as their values.

Industrial real estate data for this edition was derived from the CoStar Group. The CoStar Group is a leading provider of commercial real estate data throughout the United States, covering more than 58 billion square feet of property throughout the country.

Due to market limits within the CoStar database, historic trend data for the Team NEO region is defined as 10 of the 16 counties forming the regional footprint. These counties include Ashtabula, Cuyahoga, Geauga, Lake, Lorain, Medina, Portage, Richland, Stark and Summit.

AshtabulaLake

Cleveland

Akron Youngstown

Canton

Geauga

Trumbull

Portage

Mahoning

Columbiana

Carroll

Stark

Summit

Cuyahoga

Medina

Lorain

WayneAshland

Richland

Cleveland Plus 16-County Region

Source : CoStar Industrial Data

This report made possible through the generous support of Dominion.