june 2008 republic of portugal the next step in the development of the ot benchmark curve

TRANSCRIPT

June 2008June 2008June 2008June 2008

Republic of Portugal

The Next Step The Next Step

in the Development of the OT Benchmark Curvein the Development of the OT Benchmark Curve

2

Section 1: New issue summary

• Section 2: Portugal’s Public Finance Reform Programme

• Section 3: Debt management and funding

CONTENTS:CONTENTS:

3

A new OT Oct 2023A new OT Oct 2023OT/PGB yield curve

OT issuance in 2008OT issuance in 2008 € 10 - 12 billion (gross) to be issued through government bonds (OT)

• Two new benchmarks to be launched through syndication

• 10yr benchmark already launched in February – OT Jun 2018

• Reopening of OT previously issued

• € 4.5 billion (gross) already issued

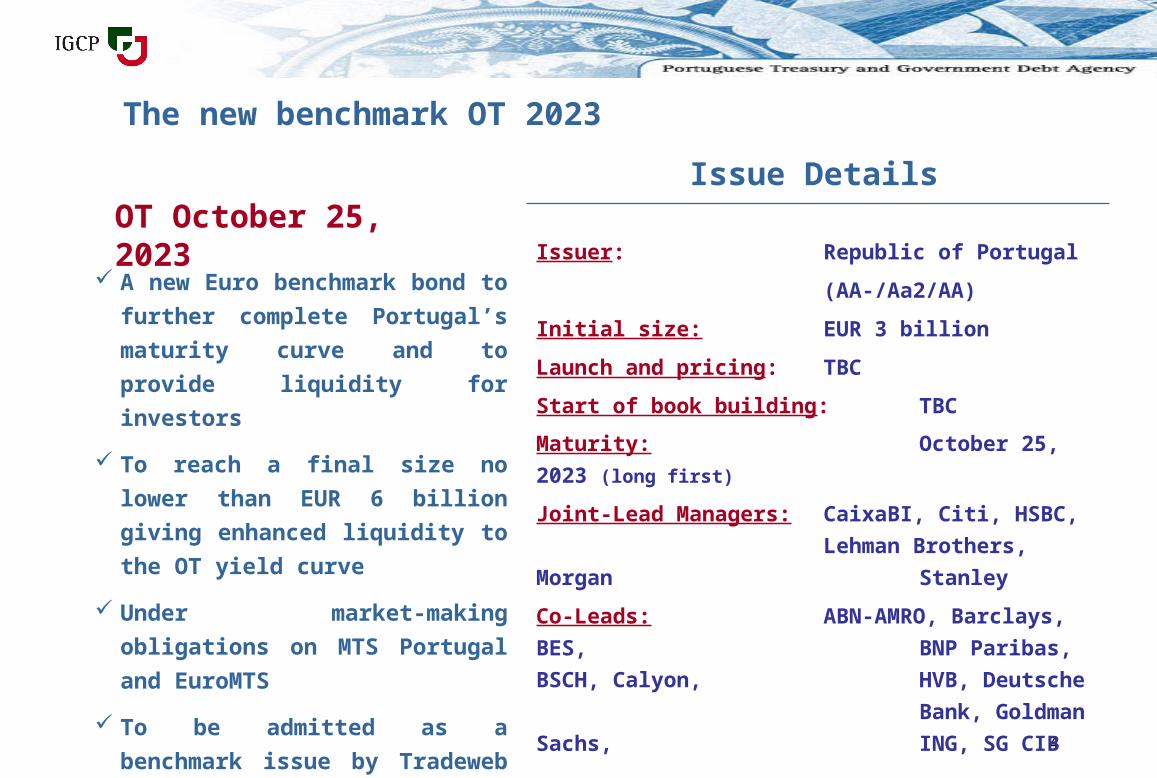

THE NEXT STEP: The new OT October 2023

4

Issuer: Republic of Portugal

(AA-/Aa2/AA)

Initial size: EUR 3 billion

Launch and pricing: TBC

Start of book building: TBC

Maturity: October 25, 2023 (long first)

Joint-Lead Managers: CaixaBI, Citi, HSBC,

Lehman Brothers, Morgan

Stanley

Co-Leads: ABN-AMRO, Barclays, BES,

BNP Paribas, BSCH, Calyon,

HVB, Deutsche

Bank, Goldman Sachs,

ING, SG CIB

Issue DetailsOT October 25, 2023

A new Euro benchmark bond to

further complete Portugal’s

maturity curve and to provide

liquidity for investors

To reach a final size no lower than

EUR 6 billion giving enhanced

liquidity to the OT yield curve

Under market-making obligations

on MTS Portugal and EuroMTS

To be admitted as a benchmark

issue by Tradeweb and Bondvision

The new benchmark OT 2023The new benchmark OT 2023

5

• Section 1: New issue summary

Section 2: Portugal’s Public Finance Reform Programme

• Section 3: Debt management and funding

CONTENTS:CONTENTS:

6

• The two main political parties have the backing of roughly 80% of the

Portuguese voters and share the objective of budgetary consolidation

• A government with absolute majority in the Parliament since February 2005

• A new President of the Republic was elected in January 2006

• There will be no elections until 2009 for Central and Local Government and

2011 for the Presidency

• A high degree of social consensus

Portuguese public finance reform programmePortuguese public finance reform programme

A stable political and social environment

7

Portugal’s public finance reform programmePortugal’s public finance reform programme

The Portuguese government has a strong mandate to put public finances

on a sustainable footing

The Stability and Growth Programme (SGP), 2007 - 2011 (December

2007) includes a comprehensive set of measures consistent with a

correction of the prevailing deficit and a progress towards the medium-term

objective, including the following:

Central Government restructuring

Reform of the social security and health systems

Improvement in the use of public resources

Strengthen the tax system’s effectiveness

2008 Budget Law approved by the Parliament reaffirms the

Government’s commitments and objectives included in the SGP

8

Public finances in the medium-term: SGP 2007-2011

Government committed to reduce budget deficit over the coming years

Deficit reduction based on structural measures rather than on one-off and

temporary measures

Between 2005 and 2007 the deficit was reduced from 6.1% to 2.6% of GDP

In 2008 the deficit is expected to achieve 2.2% of GDP

The Stability and Growth ProgrammeThe Stability and Growth Programme

9

Public finances in the medium-term: SGP 2007-2011

The performance in 2007 allowed the Government to attain the Stability and

Growth Pact’s reference value, one year ahead of schedule

“Portugal is to be praised for bringing its deficit to 3%, and possibly less, in 2007,

one year before the deadline. The recent pension reforms also significantly improve

the long-term outlook of its finances. It is encouraged to pursue its budgetary

strategy to help put the Portuguese economy back on a sustainable and dynamic

catching-up path.” – Recommendation from the EC on February 13th, 2008

The Stability and Growth ProgrammeThe Stability and Growth Programme

10

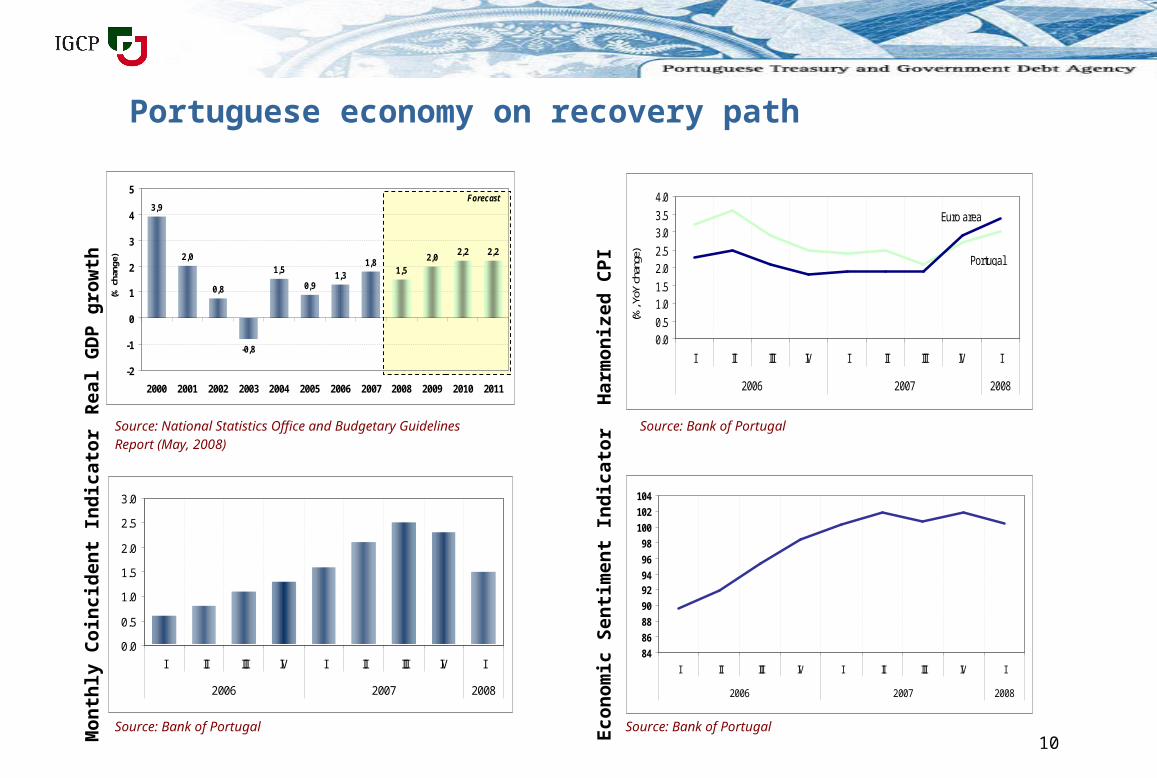

Portuguese economy on recovery pathR

eal

GD

P g

row

thM

on

thly

Co

inc

iden

t In

dic

ato

r

Eco

no

mic

Sen

tim

ent

Ind

icat

or

Source: Bank of Portugal

Source: National Statistics Office and Budgetary Guidelines Report (May, 2008)

Source: Bank of Portugal

Har

mo

niz

ed

CP

I

Source: Bank of Portugal

3,9

2,0

0,8

-0,8

1,5

0,91,3

1,81,5

2,02,2 2,2

-2

-1

0

1

2

3

4

5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

(% c

hang

e)

Forecast

0.0

0.5

1.0

1.5

2.0

2.5

3.0

I II III IV I II III IV I

2006 2007 2008

0.00.5

1.01.5

2.02.5

3.03.5

4.0

I II III IV I II III IV I

2006 2007 2008

(%, Y

oY c

hang

e) Portugal

Euro area

84

86

88

90

9294

96

98

100

102

104

I II III IV I II III IV I

2006 2007 2008

11

Structural reforms…Structural reforms…

Measures to reduce public expenditure

• Reorganisation of the State’s local services (PRACE)

• Development of shared services

• Keeping staff costs growth under strict control

• New rules and guidelines to improve human resources management

Reforming the Public Administration

Promotion of the sustainability of the social security system, through

fundamental changes on the applicable rules, in line with major

demographic trends

12

Improving the use of public resources

• Streamlining of the fundamental public services (education, healthcare, justice and local

Government), including the harmonization of public health protection systems in line with

the private sector regime

• Efficient allocation of public real-estate

Structural reforms…Structural reforms…

Measures to reduce public expenditure

13

… underpinning fiscal consolidation … underpinning fiscal consolidation

Some measures already implemented to increase tax revenue

Fight against tax fraud and evasion and abusive tax planning

• Use of information as a lever in the fight against fraud and tax evasion shall continue to be stimulated

• The dissuasive effect resultant from the new debt recovery instruments and mechanisms, and the significant worsening of sanctions for non-compliance with tax obligations, in addition to the revenue achieved, has been the greatest benefit of these actions

Reduction of tax benefits and exemptions

14

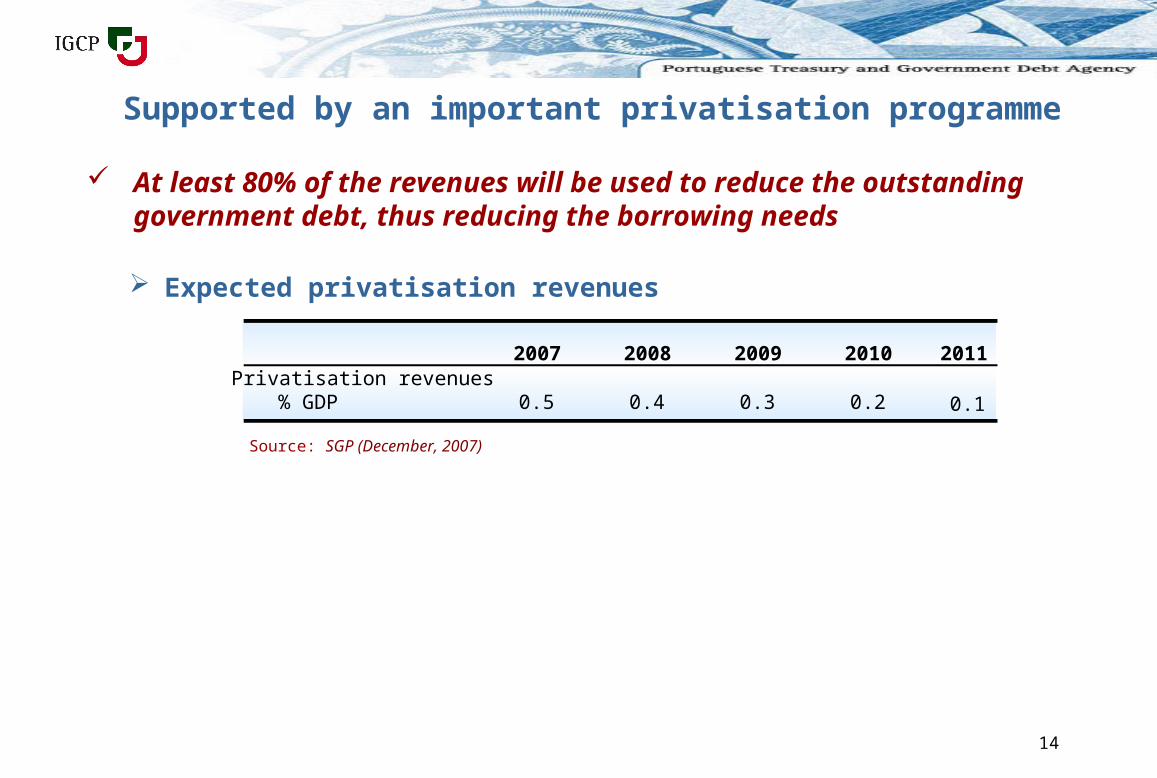

At least 80% of the revenues will be used to reduce the outstanding government debt, thus reducing the borrowing needs

Expected privatisation revenues

2007 2008 2009 2010Privatisation revenues% GDP 0.5 0.4 0.3 0.2

Supported by an important privatisation programmeSupported by an important privatisation programme

2011

0.1

Source: SGP (December, 2007)

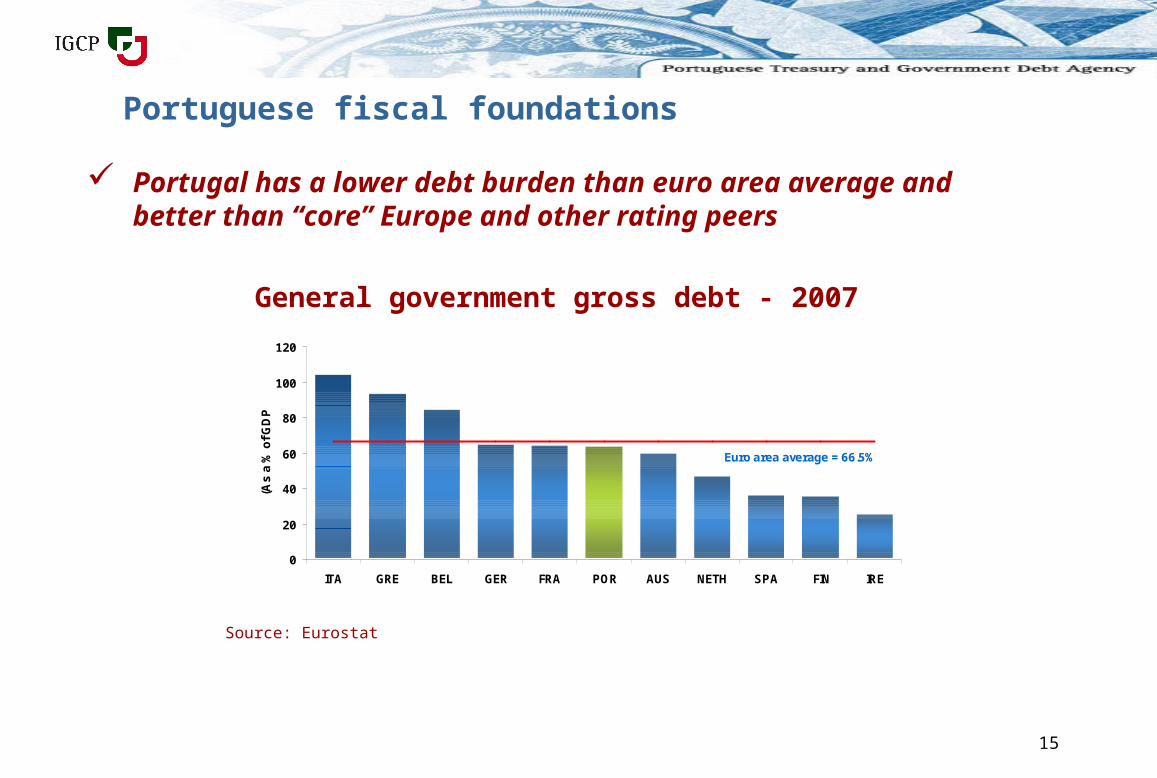

15

General government gross debt - 2007

Portuguese fiscal foundationsPortuguese fiscal foundations

Portugal has a lower debt burden than euro area average and better than “core” Europe and other rating peers

Source: Eurostat

0

20

40

60

80

100

120

ITA GRE BEL GER FRA POR AUS NETH SPA FIN IRE

(As

a %

of

GD

P)

Euro area average = 66.5%

16

CONTENTS:CONTENTS:

• Section 1: New issue summary

• Section 2: Portuguese Public Finance Reform Programme

Section 3: Debt management and funding

17

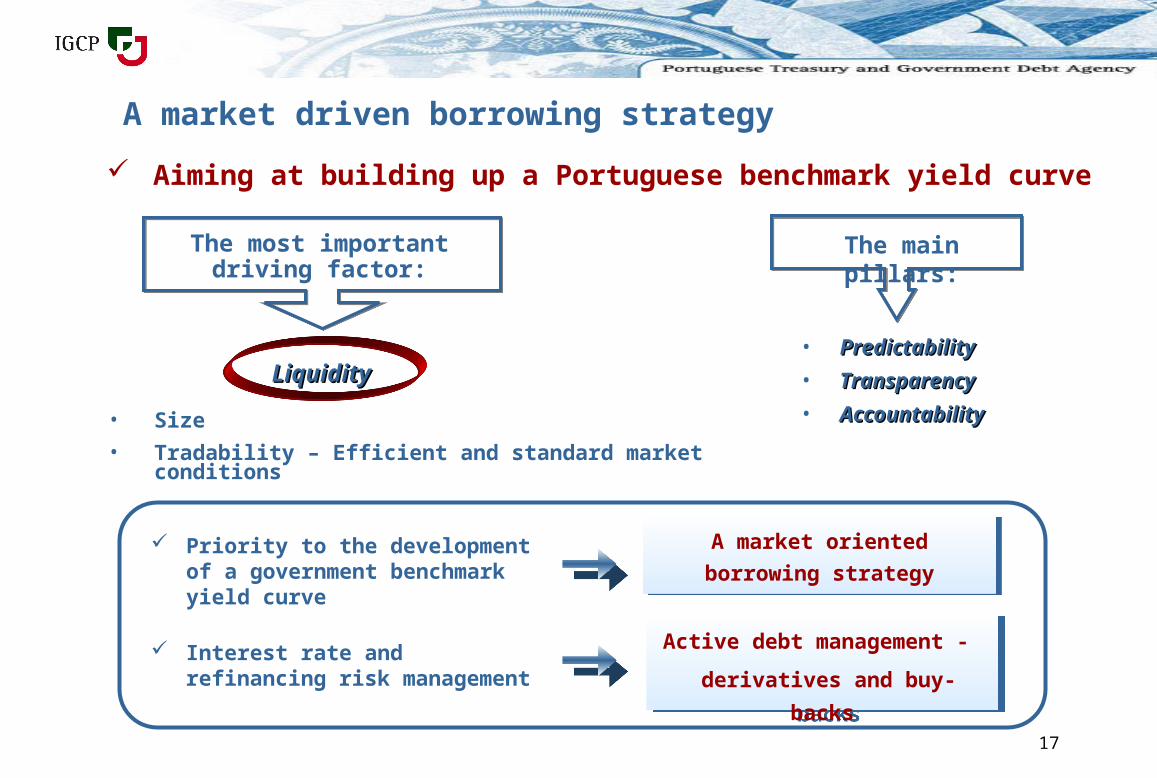

Aiming at building up a Portuguese benchmark yield curve

A market driven borrowing strategyA market driven borrowing strategy

• Size

• Tradability – Efficient and standard market conditions

The most important driving factor:

LiquidityLiquidity

A market oriented borrowing

strategy

A market oriented borrowing

strategy

Active debt management -

derivatives and buy-backs

Active debt management -

derivatives and buy-backs

Priority to the development of a government benchmark yield curve

Interest rate and refinancing risk management

• Predictability Predictability

• TransparencyTransparency

• AccountabilityAccountability

The main pillars:

18

OT launched through syndication…

Building up an international and diversified investor base

Benchmark size: € 3 billion

Allowing the benchmark OT to be traded in MTS Portugal with quoting obligations from start

…and increased through auctions up to € 6 billion

OT syndication process

PD are the only underwriters

PD committed to place bonds in high quality investors

IGCP is the active manager

E-book building

OT issuance processOT issuance process

Syndicate +1stauction

+2ndauction

+3rdauction

EU

R b

illi

on

1 bln

1 bln

1 bln

3 bln

Co-Leads

Joint-Leads

Full pot

Retention+

Co-lead pot

19

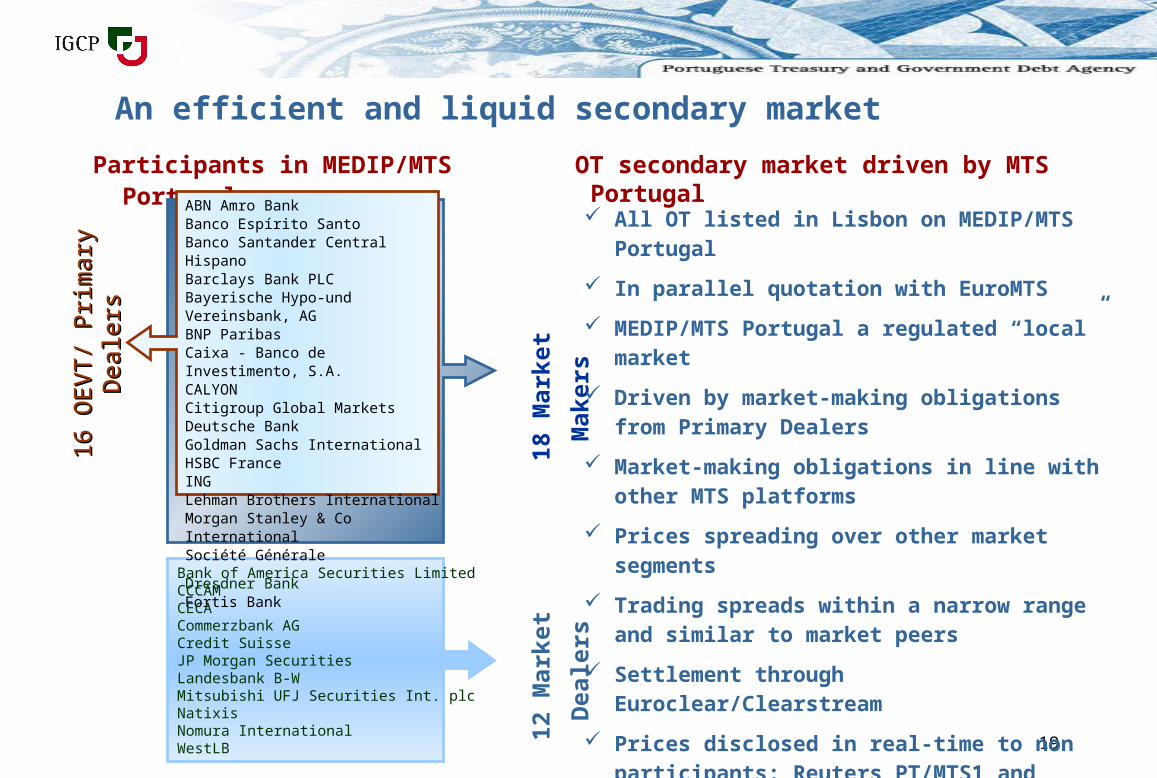

Participants in MEDIP/MTS Portugal

An efficient and liquid secondary marketAn efficient and liquid secondary market

ABN Amro Bank Banco Espírito SantoBanco Santander Central HispanoBarclays Bank PLCBayerische Hypo-und Vereinsbank, AGBNP Paribas Caixa - Banco de Investimento, S.A.CALYONCitigroup Global Markets Deutsche BankGoldman Sachs InternationalHSBC FranceINGLehman Brothers InternationalMorgan Stanley & Co InternationalSociété Générale

Dresdner BankFortis Bank

Bank of America Securities LimitedCCCAMCECACommerzbank AGCredit SuisseJP Morgan SecuritiesLandesbank B-WMitsubishi UFJ Securities Int. plcNatixisNomura InternationalWestLB

18 M

arke

t M

aker

s12

Mar

ket

Dea

lers

16 O

EV

T/

Prim

ary

16 O

EV

T/

Prim

ary

Dea

lers

Dea

lers

All OT listed in Lisbon on MEDIP/MTS Portugal

In parallel quotation with EuroMTS

MEDIP/MTS Portugal a regulated “local” market

Driven by market-making obligations from Primary Dealers

Market-making obligations in line with other MTS platforms

Prices spreading over other market segments

Trading spreads within a narrow range and similar to market peers

Settlement through Euroclear/Clearstream

Prices disclosed in real-time to non participants: Reuters PT/MTS1 and Bloomberg

Daily turnover, reference prices and a daily fixing

in www.mtsportugal.com

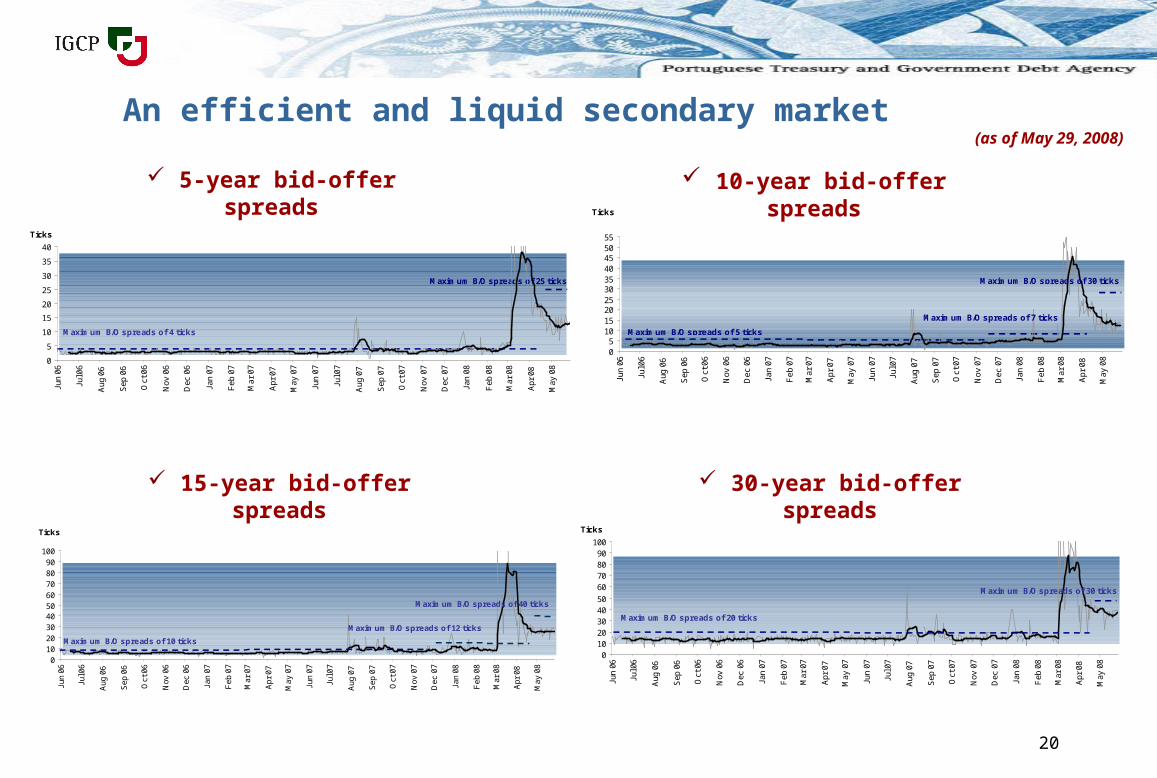

OT secondary market driven by MTS Portugal

20

10-year bid-offer spreads

An efficient and liquid secondary marketAn efficient and liquid secondary market(as of May 29, 2008)

5-year bid-offer spreads

30-year bid-offer spreads 15-year bid-offer spreads

Maximum B/O spreads of 25 ticks

0

5

10

15

20

25

30

35

40

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

Dec

06

Jan

07

Feb

07

Mar

07

Apr

07

May

07

Jun

07

Jul 0

7

Aug

07

Sep

07

Oct

07

Nov

07

Dec

07

Jan

08

Feb

08

Mar

08

Apr

08

May

08

Ticks

Maximum B/O spreads of 4 ticks

01020304050

60708090

100

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

Dec

06

Jan

07

Feb

07

Mar

07

Apr

07

May

07

Jun

07

Jul 0

7

Aug

07

Sep

07

Oct

07

Nov

07

Dec

07

Jan

08

Feb

08

Mar

08

Apr

08

May

08

Ticks

Maximum B/O spreads of 20 ticks

Maximum B/O spreads of 30 ticks

0102030405060708090

100

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

Dec

06

Jan

07

Feb

07

Mar

07

Apr

07

May

07

Jun

07

Jul 0

7

Aug

07

Sep

07

Oct

07

Nov

07

Dec

07

Jan

08

Feb

08

Mar

08

Apr

08

May

08

Ticks

Maximum B/O spreads of 10 ticks

Maximum B/O spreads of 12 ticks

Maximum B/O spreads of 40 ticks

Maximum B/O spreads of 5 ticks

05

10152025303540455055

Jun

06

Jul 0

6

Aug

06

Sep

06

Oct

06

Nov

06

Dec

06

Jan

07

Feb

07

Mar

07

Apr

07

May

07

Jun

07

Jul 0

7

Aug

07

Sep

07

Oct

07

Nov

07

Dec

07

Jan

08

Feb

08

Mar

08

Apr

08

May

08

Maximum B/O spreads of 7 ticks

Ticks

Maximum B/O spreads of 30 ticks

21

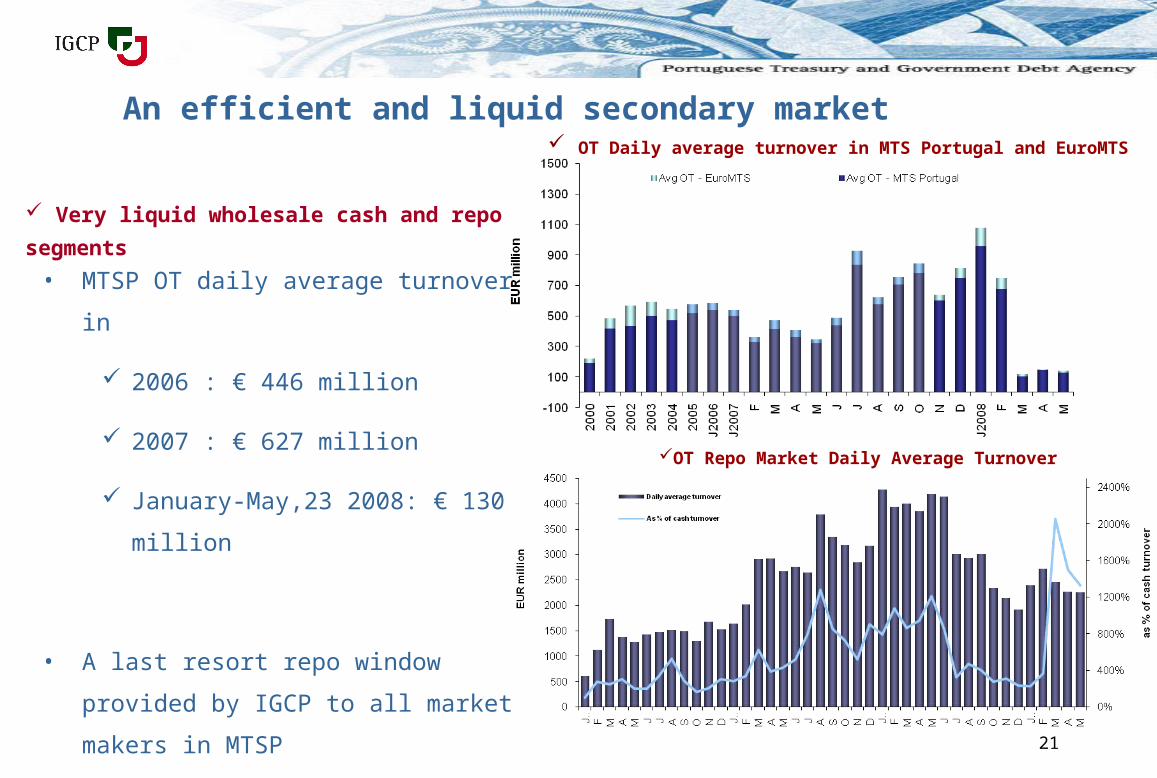

An efficient and liquid secondary marketAn efficient and liquid secondary market OT Daily average turnover in MTS Portugal and EuroMTS

OT Repo Market Daily Average Turnover

• MTSP OT daily average turnover in

2006 : € 446 million

2007 : € 627 million

January-May,23 2008: € 130 million

• A last resort repo window provided by

IGCP to all market makers in MTSP

Very liquid wholesale cash and repo segments

22

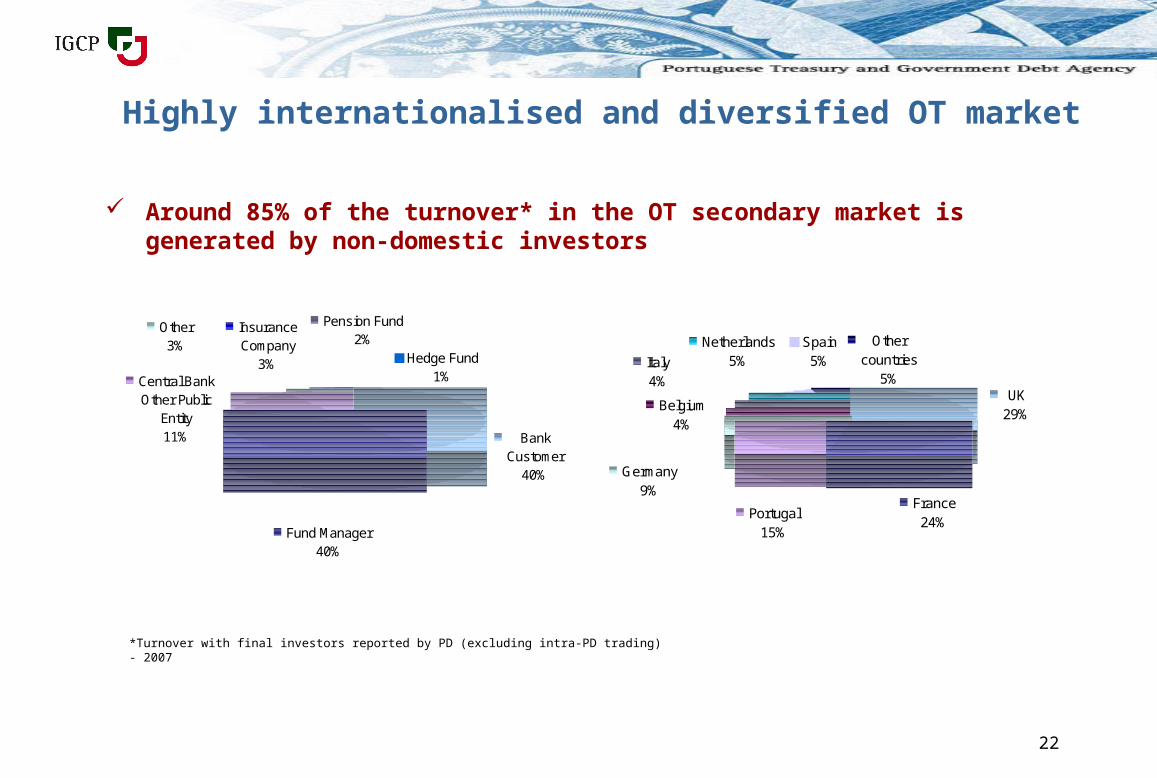

Highly internationalised and diversified OT marketHighly internationalised and diversified OT market

*Turnover with final investors reported by PD (excluding intra-PD trading) - 2007

Around 85% of the turnover* in the OT secondary market is generated by non-domestic investors

Other3%

Pension Fund2%

Insurance Company

3% Hedge Fund1%

Bank Customer

40%

Fund Manager40%

Central Bank Other Public

Entity11%

UK29%

Other countries

5%

Belgium4%

Germany9%

Portugal15%

France24%

Netherlands5%Italy

4%

Spain5%

23

Further information on the Portuguese economy can be obtained from:

Tel: +351 21 792 33 00Fax: +351 21 799 37 95E-mail:[email protected]

Budget Department

National Statistics Office

Banco de Portugal (Central bank)

Web site: igcp.ptReuters pages: IGCP01

Bloomberg pages: IGCP

Further information on the Portuguese secondary market can be obtained from:

MTS Portugal: www.mtsportugal.com

Reuters pages: PT/MTS1

www.dgo.pt

www.ine.pt

www.bportugal.pt

IGCP:

DISCLAIMERThe information and opinions contained in this document have been compiled or arrived at from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. All opinions and estimates contained in this document are published for the assistance of recipients, but is not to be relied upon as authoritative or taken in substitution for the exercise or judgment by a recipient and, therefore, does not form the basis of any contract or commitment whatsoever. IGCP does not accept any liability whatsoever for any direct or consequential loss arising from any use of this document or its contents.