july 2001brent w. ambrose, university of kentucky1 commercial mortgage-backed securities national...

TRANSCRIPT

July 2001 Brent W. Ambrose, University of Kentucky 1

Commercial Mortgage-Backed Securities

National University of Singapore

July 27, 2001

Notes from lecture given by Brent Ambrose at

National University of Singapore – July 2001

July 2001 Brent W. Ambrose, University of Kentucky 2

COMMERICAL MORTGAGE-BACKED SECURITIES

What is a CMBS?

• A commercial mortgage-backed security (CMBS) is a financial asset.– created when an issuer places a commercial

mortgage (or collection of mortgages) into a trust

– the trust issues classes of bonds backed by the underlying principal and interest payments.

July 2001 Brent W. Ambrose, University of Kentucky 3

Objectives for this Session

• This session will cover the following topics:– Differences between CMBS and MBS.

– The anatomy of a CMBS deal.

– Prepayment penalties on commercial mortgages.

– CMBS risks (prepayment & default)

– CMBS underwriting and the role of rating agencies.

– The role of CMBS servicers.

– Empirical studies of CMBS default and loss severity.

– How CMBS deals are rated.

July 2001 Brent W. Ambrose, University of Kentucky 4

CMBS vs. MBS

• Basic difference between residential MBS and commercial MBS:– PREPAYMENT

• Commercial mortgages have prepayment lockouts and penalties.

• This changes the termination options.

• Default is now paramount.

July 2001 Brent W. Ambrose, University of Kentucky 5

U.S. CMBS Legalities

• Real Estate Mortgage Investment Conduits (REMIC)– U.S. tax code provision that allows the pooling

and securitization of mortgages. Once pool is formed, not allowed to substitute mortgages.

July 2001 Brent W. Ambrose, University of Kentucky 6

U.S. CMBS Legalities

• Financial Asset Securitization Investment Trust (FASIT)– created in 1997– allows issuers to substitute and add collateral

after securitization• now issuer can add mortgages to pool as they are

originated

July 2001 Brent W. Ambrose, University of Kentucky 7

U.S. CMBS Legalities

FASIT – Allow securitization of a broader class of assets including:

1. construction loans

2. commercial property bridge loans

3. automobile loans

4. credit card receivables

5. home equity loans

July 2001 Brent W. Ambrose, University of Kentucky 8

CMBS Anatomy• Cash Flows• Subordination• Prepayment Penalties• CMBS Risks• Call Protection• Property Diversification• Credit Enhancements• Underwriting• Role of Servicers

July 2001 Brent W. Ambrose, University of Kentucky 9

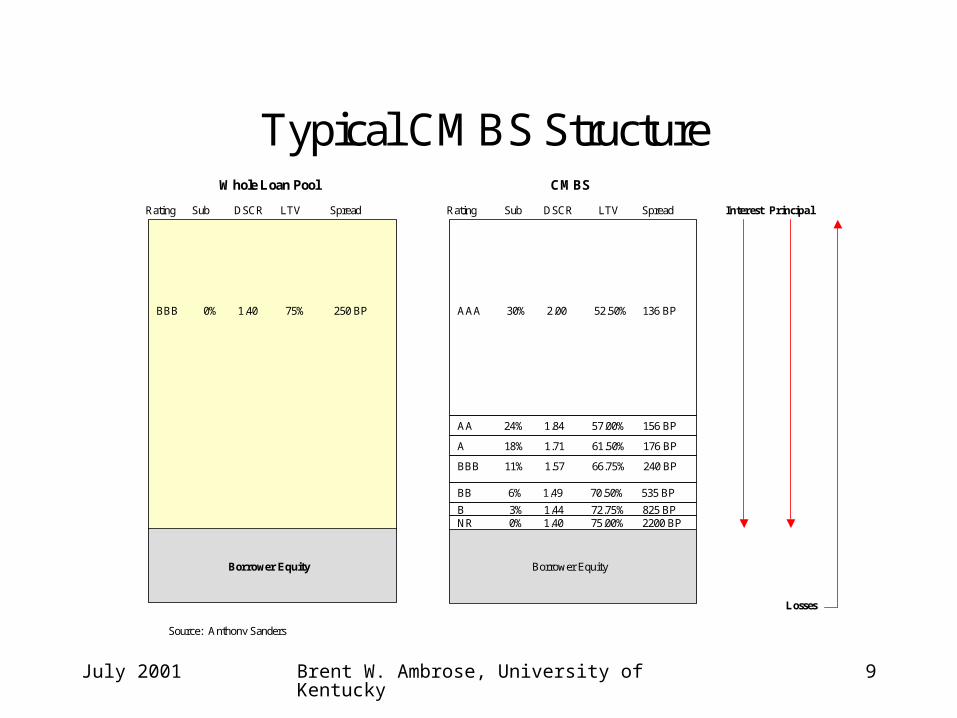

Typical CMBS Structure

Rating Sub DSCR LTV Spread

AAA 30% 2.00 52.50% 136 BP

AA 24% 1.84 57.00% 156 BP

A 18% 1.71 61.50% 176 BP

BBB 11% 1.57 66.75% 240 BP

BB 6% 1.49 70.50% 535 BP

NR 0% 1.40 75.00% 2200 BPB 3% 1.44 72.75% 825 BP

Borrower Equity

Rating Sub DSCR LTV Spread

BBB 0% 1.40 75% 250 BP

Borrower Equity

Whole Loan Pool CMBS

Interest Principal

Losses

Source: Anthony Sanders

July 2001 Brent W. Ambrose, University of Kentucky 10

Actual CMBS Examples

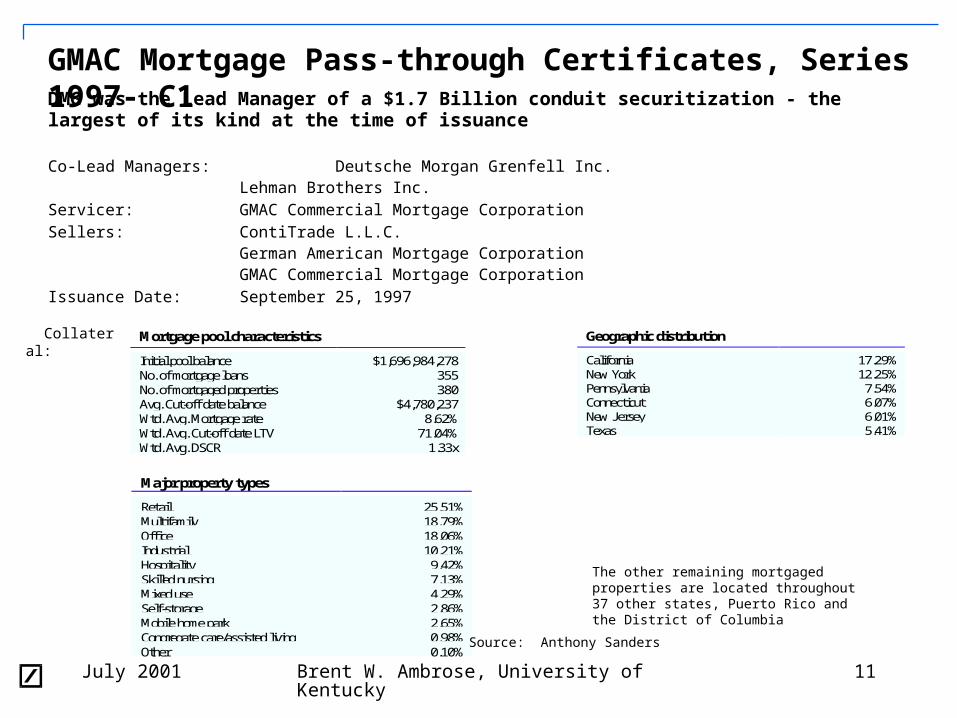

• GMAC Mortgage Pass-through Certificates

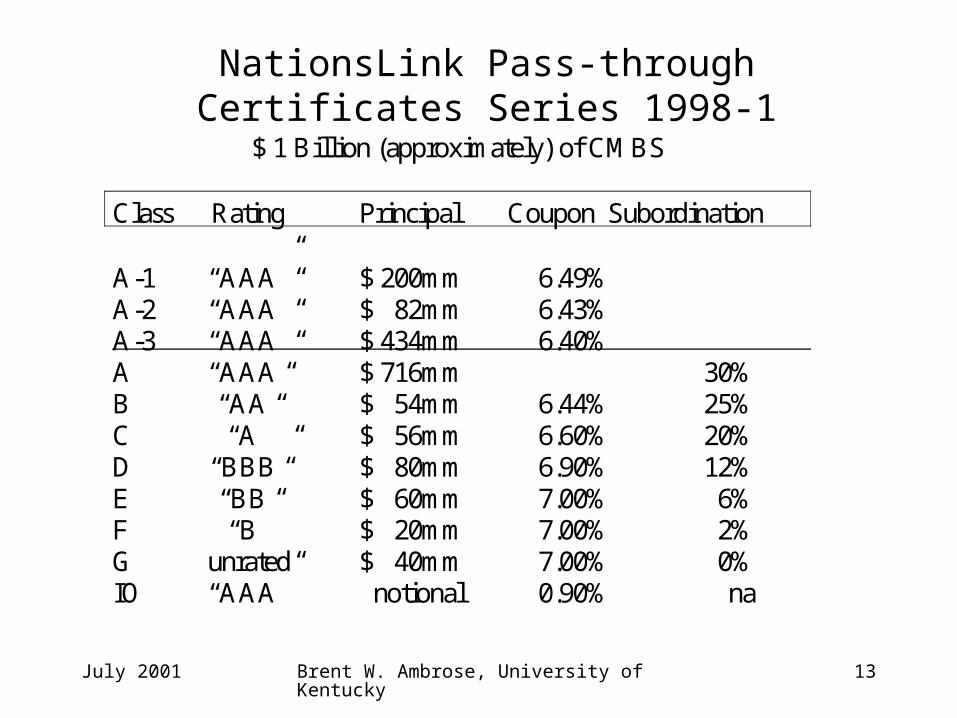

• NationsLink Commercial Mortgage Pass-through Certificates Series 1998-1

July 2001 Brent W. Ambrose, University of Kentucky 11

Geographic distribution

California 17.29%New York 12.25%Pennsylvania 7.54%Connecticut 6.07%New Jersey 6.01%Texas 5.41%

GMAC Mortgage Pass-through Certificates, Series 1997- C1DMG was the Lead Manager of a $1.7 Billion conduit securitization - the largest of its kind at the time of issuance

Co-Lead Managers: Deutsche Morgan Grenfell Inc. Lehman Brothers Inc.

Servicer: GMAC Commercial Mortgage CorporationSellers: ContiTrade L.L.C.

German American Mortgage CorporationGMAC Commercial Mortgage Corporation

Issuance Date: September 25, 1997

Mortgage pool characteristics

Initial pool balance $1,696,984,278No. of mortgage loans 355No. of mortgaged properties 380Avg. Cut-off date balance $4,780,237Wtd. Avg. Mortgage rate 8.62%Wtd. Avg. Cut-off date LTV 71.04%Wtd. Avg. DSCR 1.33x

Major property types

Retail 25.51%Multifamily 18.79%Office 18.06%Industrial 10.21%Hospitality 9.42%Skilled nursing 7.13%Mixed use 4.29%Self-storage 2.86%Mobile home park 2.65%Congregate care/assisted living 0.98%Other 0.10%

The other remaining mortgaged properties are located throughout 37 other states, Puerto Rico and the District of Columbia

Collateral:

Source: Anthony Sanders

July 2001 Brent W. Ambrose, University of Kentucky 12

Class

Initial Cert.Balance or

Notional Amt. Spread

Rating(Moody's/

Fitch)

Percent of Initial Pool Balance Sub-ordination

Initial Pass-Through Rate

(approx.)

WeightedAverage Life

(yrs) Payment Window

A-1 $261, 582,000 48 Ass/AAA 15.4% 28.5% 6.830% 4.00 1 - 75A-2 $227, 661,000 62 Aaa/AAA 13.4% 28.5% 6.853% 7.50 75-108A-3 $724,100,000 65 Aaa/AAA 42.7% 28.5% 6.869% 9.71 108-119B $67,879,000 70 Aa2/AA+ 4.0% 24.5% 6.918% 9.94 119-120C $50,909,000 75 A1/AA 3.0% 21.5% 6.898% 9.96 120-120D $50,909,000 85 A2/A+ 3.0% 18.5% 6.997% 10.01 120-125E $93,334,000 100 Baa2/BBB 5.5% 13.0% 7.085% 11.45 125-158F $25,454,000 118 Baa3/BBB- 1.5% 11.5% 7.222% 13.53 158-170G $84,849,000 BB/BB 5.0% 6.5% 7.414% 14.93 170-195H $59,394,000 B 3.5% 3.0% 6.600% 17.99 195-235J $16,969,000 B- 1.0% 2.0% 6.600% 19.78 235-242K $33,944,278 Unrated 2.0% 0.0% 6.600% 22.0 242-358

X $1,696,984,278 Notional Amt Aaa/AAA N/A N/A 1.629% N/A 1-358

Total $1,696,984,278 Securities

Bonds:

GMAC Mortgage Pass-Through Certificates, Series 1997-C1

Source: Anthony Sanders

July 2001 Brent W. Ambrose, University of Kentucky 13

NationsLink Pass-through Certificates Series 1998-1

$ 1 Billion (approximately) of CMBS

Class Rating Principal Coupon Subordination A-1 “AAA” $ 200mm 6.49% 101.00% A-2 “AAA” $ 82mm 6.43% 101.00% A-3 “AAA” $ 434mm 6.40% 101.00% A “AAA” $ 716mm 30% B “AA” $ 54mm 6.44% 25% 101.00% C “A” $ 56mm 6.60% 20% 100.75% D “BBB” $ 80mm 6.90% 12% 100.50% E “BB” $ 60mm 7.00% 6% 85.00% F “B” $ 20mm 7.00% 2% 75.00% G unrated $ 40mm 7.00% 0% 45.00% IO “AAA” notional 0.90% na 4.75%

July 2001 Brent W. Ambrose, University of Kentucky 14

CMBS Anatomy

• Cash flow prioritization:– 1) Principal repayments (both scheduled amortization

and unscheduled prepayments) go to retire senior class debt first.

• CF go to senior classes AAA through BBB

• Intermediate class

• Junior class

• Unrated

• Equity holder

– 2) Coupon interest paid to all classes

July 2001 Brent W. Ambrose, University of Kentucky 15

CMBS Anatomy

• Loss prioritization:– Principal and interest due the most junior class

bondholder must be completely exhausted before any loss is assigned to the class above it.

July 2001 Brent W. Ambrose, University of Kentucky 16

The Anatomy of a CMBS

Required Subordination

The required level of subordination is computed as the expected lossin the event of a recession in the real property market. Morespecifically,

required subordination = probability of loss (given a recession) x severity of loss (given a default)

The probability of loss varies from small (say 10%) to large (say50%), depending on the magnitude of the real property recession.The severity of loss is the amount of the loss conditional on a default.For example, a “Class B” real property recession will result in loanlosses with a 10% probability. The severity of the loss is typically20% of the loan balance. Therefore, the required subordination for a“Class B” real property recession is 10% x 20% = 2%.

July 2001 Brent W. Ambrose, University of Kentucky 17

The Anatomy of a CMBS

Example of Required Subordination Level Calculation (NationsLink Example)

Type of Probability x Severity = Required Recession of Loss of Loss Subordination “AAA” 50% x 60% 30% “AA” 45% x 55% 25% “A” 40% x 50% 20% “BBB” 30% x 40% 12% “BB” 20% x 30% 6% “B” 10% x 20% 2%

July 2001 Brent W. Ambrose, University of Kentucky 18

The Anatomy of a CMBS

The Unrated Piece

The unrated piece is used to provide subordination for the lowestrated junior piece.

The size of the unrated bond reflects rating agency requirements forloans that are not cross-collateralized and cross-defaulted.

The unrated piece is sold privately and typically purchased by thespecial servicer.

July 2001 Brent W. Ambrose, University of Kentucky 19

The Anatomy of a CMBS

The Interest Only (IO) Piece

The notional balance of the IO piece is initially the aggregate issue amount ($ 1 billion in the example)

The notional balance of the IO piece equals the sum of the

certificate balances for the sequential pay certificates. The IO piece typically pays a small coupon (e.g. 90bp) and sells

at a steep discount.

July 2001 Brent W. Ambrose, University of Kentucky 20

CMBS Anatomy

• Expected Cash Flows – Review– Principal repayment

• Scheduled amortization• Unscheduled prepayment

– Interest– Penalties

• Hyperamortization• Prepayment Penalty• Balloon Default

July 2001 Brent W. Ambrose, University of Kentucky 21

CMBS Anatomy (Penalties)

A. Hyperamortization (cash trap): • all cash flows in excess of operating expenses go

to retire debt.

• Triggered byi. Delinquency

ii. failure to maintain required DSCR

iii. failure to maintain debt rating

iv. failure to maintain adequate reserves

July 2001 Brent W. Ambrose, University of Kentucky 22

CMBS Anatomy (Penalties)

B. Prepayment penalty: » penalty assessed the borrower for early repayment

of debt.

» Penalty may be computed in various ways.

July 2001 Brent W. Ambrose, University of Kentucky 23

CMBS Anatomy (Penalties)

C. Balloon default: • penalty assessed the borrower for failing to

refinance at the end of the loan term.

July 2001 Brent W. Ambrose, University of Kentucky 24

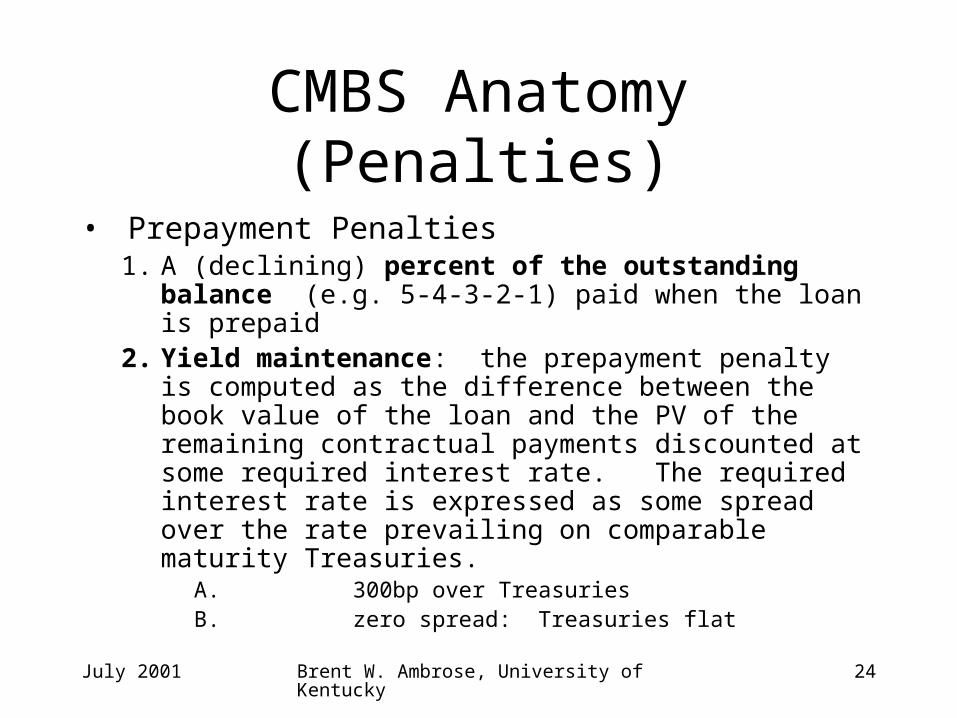

CMBS Anatomy (Penalties)

• Prepayment Penalties1. A (declining) percent of the outstanding balance

(e.g. 5-4-3-2-1) paid when the loan is prepaid2. Yield maintenance: the prepayment penalty is

computed as the difference between the book value of the loan and the PV of the remaining contractual payments discounted at some required interest rate. The required interest rate is expressed as some spread over the rate prevailing on comparable maturity Treasuries.

A. 300bp over TreasuriesB. zero spread: Treasuries flat

July 2001 Brent W. Ambrose, University of Kentucky 25

CMBS Anatomy (Penalties)

• Prepayment Penalties:3. Lockout – complete prohibition of prepayment

of principal. Usually only in effect during the first few years of the mortgage.

July 2001 Brent W. Ambrose, University of Kentucky 26

Simple Prepayment Example

• Mortgage Assumptions:– Two year, $10 million interest only mortgage

• 10% interest rate on the loan at date of issuance

• Loan is repaid after 1 year when interest rates fall to 8%.

July 2001 Brent W. Ambrose, University of Kentucky 27

Simple Prepayment Example

• Prepayment Penalties– Yield Maintenance penalty provision

• Penalty = ($1,000,000 - $800,000) / (1+0.08)

• = $185,185

– Percent of Prepaid Amount penalty provision• Assume 1% penalty in this example

• Penalty = 1% * $10 million = $100,000

July 2001 Brent W. Ambrose, University of Kentucky 28

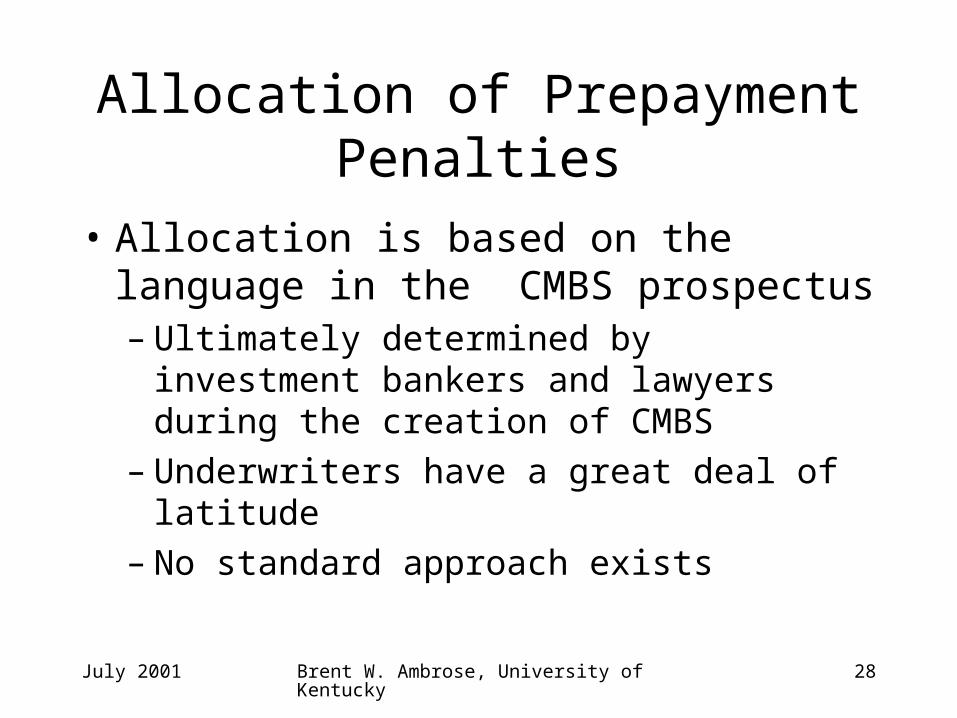

Allocation of Prepayment Penalties

• Allocation is based on the language in the CMBS prospectus– Ultimately determined by investment bankers

and lawyers during the creation of CMBS– Underwriters have a great deal of latitude– No standard approach exists

July 2001 Brent W. Ambrose, University of Kentucky 29

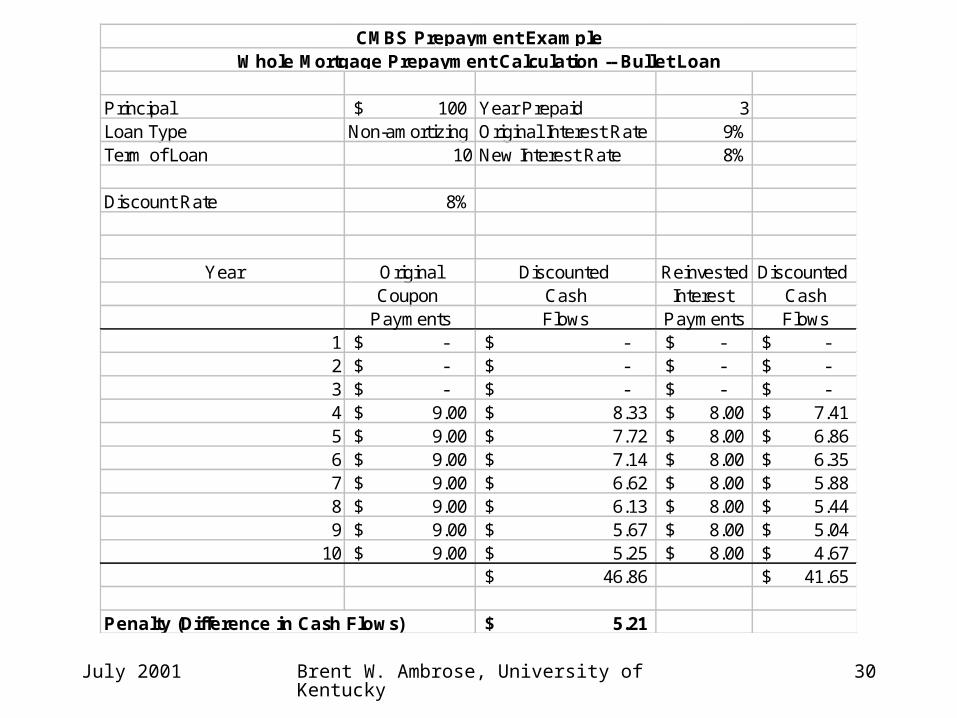

Yield Maintenance Calculations

• One bullet loan tranched into two classes:– Assumptions:

1. Underlying loan is a ten year bullet loan priced at par and pays a 9% coupon

2. Multi-class structure: • Senior class is $90 million and pays an 8% coupon

(priced at par). • Subordinate class is a $10 million classs that pay an 18%

coupon (priced at par).

3. Borrower prepays in full at at year 3. Current interest rates are 100bps lower than in year 0.

July 2001 Brent W. Ambrose, University of Kentucky 30

Principal 100$ Year Prepaid 3Loan Type Non-amortizing Original Interest Rate 9%Term of Loan 10 New Interest Rate 8%

Discount Rate 8%

Year Original Discounted Reinvested Discounted Coupon Cash Interest Cash

Payments Flows Payments Flows1 -$ -$ -$ -$ 2 -$ -$ -$ -$ 3 -$ -$ -$ -$ 4 9.00$ 8.33$ 8.00$ 7.41$ 5 9.00$ 7.72$ 8.00$ 6.86$ 6 9.00$ 7.14$ 8.00$ 6.35$ 7 9.00$ 6.62$ 8.00$ 5.88$ 8 9.00$ 6.13$ 8.00$ 5.44$ 9 9.00$ 5.67$ 8.00$ 5.04$

10 9.00$ 5.25$ 8.00$ 4.67$ 46.86$ 41.65$

Penalty (Difference in Cash Flows) 5.21$

CMBS Prepayment ExampleWhole Mortgage Prepayment Calculation -- Bullet Loan

July 2001 Brent W. Ambrose, University of Kentucky 31

• Allocation of Penalty:

1. Percentage Prepayed Senior Class (90%) 4.69$ Junior Class (10%) 0.52$

5.21$

July 2001 Brent W. Ambrose, University of Kentucky 32

Principal 90$ Year Prepaid 3Loan Type Non-amortizing Original Interest Rate 8%Term of Loan 10 New Interest Rate 7%

Discount Rate 7%

Year Original Discounted Reinvested Discounted Coupon Cash Interest Cash

Payments Flows Payments Flows1 -$ -$ -$ -$ 2 -$ -$ -$ -$ 3 -$ -$ -$ -$ 4 7.20$ 6.73$ 6.30$ 5.89$ 5 7.20$ 6.29$ 6.30$ 5.50$ 6 7.20$ 5.88$ 6.30$ 5.14$ 7 7.20$ 5.49$ 6.30$ 4.81$ 8 7.20$ 5.13$ 6.30$ 4.49$ 9 7.20$ 4.80$ 6.30$ 4.20$

10 7.20$ 4.48$ 6.30$ 3.92$ 38.80$ 33.95$

Penalty (Difference in Cash Flows) 4.85$

Using a Make-whole CalculationSenior Tranche

July 2001 Brent W. Ambrose, University of Kentucky 33

Principal 10$ Year Prepaid 3Loan Type Non-amortizing Original Interest Rate 18%Term of Loan 10 New Interest Rate 17%

Discount Rate 17%

Year Original Discounted Reinvested Discounted Coupon Cash Interest Cash

Payments Flows Payments Flows1 -$ -$ -$ -$ 2 -$ -$ -$ -$ 3 -$ -$ -$ -$ 4 1.80$ 1.54$ 1.70$ 1.45$ 5 1.80$ 1.31$ 1.70$ 1.24$ 6 1.80$ 1.12$ 1.70$ 1.06$ 7 1.80$ 0.96$ 1.70$ 0.91$ 8 1.80$ 0.82$ 1.70$ 0.78$ 9 1.80$ 0.70$ 1.70$ 0.66$

10 1.80$ 0.60$ 1.70$ 0.57$ 7.06$ 6.67$

Penalty (Difference in Cash Flows) 0.39$ Total Penalty Payment (Junior + Senior) 5.24$ Difference in Penalty Payments (0.04)$

Using a Make-whole CalculationJunior Tranche

July 2001 Brent W. Ambrose, University of Kentucky 34

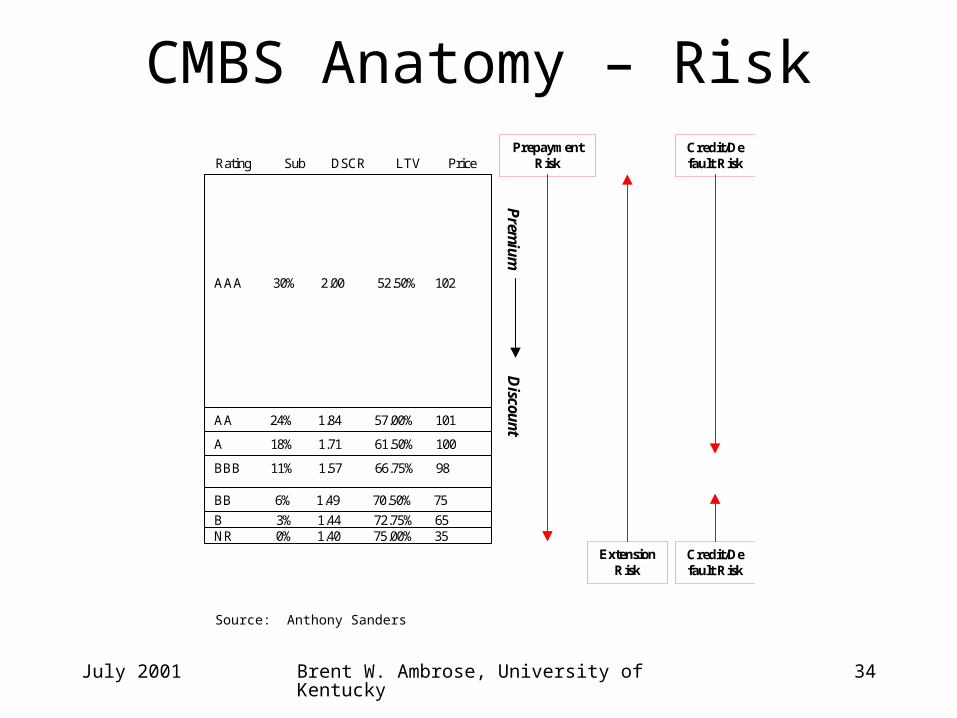

CMBS Anatomy – Risk

Rating Sub DSCR LTV Price

AAA 30% 2.00 52.50% 102

AA 24% 1.84 57.00% 101

A 18% 1.71 61.50% 100

BBB 11% 1.57 66.75% 98

BB 6% 1.49 70.50% 75

NR 0% 1.40 75.00% 35B 3% 1.44 72.75% 65

PrepaymentRisk

ExtensionRisk

Credit/Default Risk

Prem

iumD

iscount

Credit/Default Risk

Source: Anthony Sanders

July 2001 Brent W. Ambrose, University of Kentucky 35

CMBS Anatomy

• CMBS Risk impacted by:– property quality– geographic location– tenant creditworthiness

July 2001 Brent W. Ambrose, University of Kentucky 36

CMBS Risks

• Default risk: – Income property loans are typically

nonrecourse.• Borrower has the financial incentive to default when

the market value of the property falls below the outstanding balance of the loan (negative equity).

• Also referred to as “optimal”, “strategic”, or “financial” default.

July 2001 Brent W. Ambrose, University of Kentucky 37

CMBS Risks

• Balloon risk: – income property mortgages typically have

terms that are less than the loan amortization period, thus the borrower must refinance to continue making mortgage payments.

– Circumstances in the property and capital markets may have changed in ways that make refinancing difficult or even impossible.

• Also referred to as “refinancing risk”

July 2001 Brent W. Ambrose, University of Kentucky 38

CMBS Risks

• Prepayment risk: – Many income property mortgages provide some

call protection.• lock-out provisions

• prepayment penalties

• Treasury defeasance

– Some income property mortgages do not have any of these features.

July 2001 Brent W. Ambrose, University of Kentucky 39

CMBS Call Protection

• Lock-out provisions:– prohibit loan prepayment over given period

• Prepayment penalties: – paid in a lump sum at the time of prepayment; – Cash flows are proportionally allocated to

remaining certificate classes.• See previous examples of a (declining) percent of

the outstanding loan balance or yield maintenance agreements

July 2001 Brent W. Ambrose, University of Kentucky 40

CMBS Call Protection

• Treasury defeasance:– the borrower must purchase a series of

Treasuries that provide the same future cash flows assuming the loan not prepaid.

• Property release provision: – prohibits asset substitution;– prevents the issuer/lender from removing the

stronger properties from the pool.

July 2001 Brent W. Ambrose, University of Kentucky 41

Property Diversification

• Diversification across:– Loan size:

• usually no single loan exceeds 5% of the aggregate issue amount.

• An exception to this is a fusion deal, where a single large loan is packaged with several smaller loans.

– Property type

– Property location• State

• metropolitan area

July 2001 Brent W. Ambrose, University of Kentucky 42

Table 2. The twenty largest loans underlying the GMAC 1999-C3 deal.

Name Location, MSA Category Loan Amount 1 Biltmore Fashion Phoenix, Arizona Retail $80,000,000 2 Prime Outlets Niagara Falls, New York Retail $62,835,426 3 Equity Inns Various Hotel $46,511,317 4 One Colorado Pasadena, California Retail $42,628,093 5 Comerica Bank San Jose, California Office $33,640,510 6 120 Monument Indianapolis, Indiana Office $28,955,362 7 125 Maiden New York, New York Office $28,500,000 8 Texas Development Houston, Texas Apartment $26,926,701 9 Sherman Plaza Van Nuys, California Office $25,984,904 10 Alliance TP Various Apartment $24,888,157 11 Bush Tower New York, New York Office $23,000,000 12 County Line Jackson, Mississippi Retail $20,990,264 13 Sherwood Lakes Schererville, Indiana Apartment $20,162,442 14 Laurel Portfolio Various Apartment $17,950,331 15 Sweet Paper Various Warehouse $17,420,000 16 Sheraton Portsmouth Portsmouth, New Hampshire Hotel $15,949,087 17 Trinity Commons Fort Worth, Texas Retail $15,242,981 18 Village Square Indianapolis, Indiana Apartment $14,993,950 19 Golden Books Fayetteville, North Carolina Warehouse $14,493,350 20 Air Touch Dublin, Ohio Office $13,992,523

Source: Charter Research.

Loan Diversification

July 2001 Brent W. Ambrose, University of Kentucky 43

Table 4. Aggregate loan amounts by state for GMAC 1999-C3 deal.

State Loan Amount No. of Loans % of Pool California $257,522,410 33 22.35% Texas $162,355,125 26 14.09% New York $130,070,471 7 11.29% Arizona $99,942,794 5 8.68% Indiana $68,623,516 5 5.96% Ohio $44,982,528 5 3.90% Mississippi $23,067,864 2 2.00% New Jersey $22,983,973 5 2.00% Other $342,473,371 50 29.73%

Total $1,152,022,052 138 100.00%

Source: Charter Research.

Geographic Diversification

July 2001 Brent W. Ambrose, University of Kentucky 44

Table 5. Aggregate loan amounts by property type for GMAC 1999-C3 deal.

Property Type Loan Amount No. of Loans % of Pool

Apartment $259,779,802 39 22.55% Office $322,053,844 36 27.96% Retail $350,683,062 34 30.44% Warehouse $99,126,075 15 8.60% Hotel $105,832,139 8 9.19% Other $14,547,130 6 1.26%

Total $1,152,022,052 138 100.00%

Source: Charter Research.

Property Type Diversification

July 2001 Brent W. Ambrose, University of Kentucky 45

Credit Enhancements

• Subordination

• Cross collateralization: – properties that collateralize individual loans are

pledged against all loans in the pool

• Cross default:– allows the lender to call ALL LOANS in the

event a single loan is in default.

July 2001 Brent W. Ambrose, University of Kentucky 46

Credit Enhancements• Lock box:

– Gives the trustee control of the property gross revenues. The trustee assigns priority in the following order:

• (1) taxes and insurance;

• (2) operating expenses;

• (3) debt service;

• (4) management fees;

• (5) reserves for replacements;

• (6) equity investor

July 2001 Brent W. Ambrose, University of Kentucky 47

Credit Enhancements

• Overcollateralization: – When the book value of the loans exceed the

par value of the bonds issued.– Most common in residential MBS

• Especially common in CMO structure

July 2001 Brent W. Ambrose, University of Kentucky 48

Reserve Funds

• Established at loan closing to:– Provide liquidity:

• to pay interest for investment grade bonds

– Service the asset: • to pay

– property taxes

– property insurance

– legal fees

– Maintenance

July 2001 Brent W. Ambrose, University of Kentucky 49

Standardized CMBS Underwriting

• Key Underwriting Characteristics– Debt Service Coverage Ratio (DSCR)– Loan to Value Ratio (LTV)– Average loan size– Max loan not to exceed certain percentage (e.g. 5%)– Diversification across

• Property types• Geographic locations

– Prepayment terms– Loan maturities

July 2001 Brent W. Ambrose, University of Kentucky 50

Role of rating agencies

• Establish different rating criteria for various property types.

• Negotiate subordination levels with issuers.• Track property performance/delinquencies• Servicer and trustee report ongoing loan level

performance– Monthly/quarterly DSCRs– occupancy levels– updated bond information

July 2001 Brent W. Ambrose, University of Kentucky 51

Role of Servicers

• Master Servicer:– Oversees the deal and servicing agreements– Facilitates timely payment of principal and

interest– May provide (servicer) advances for

delinquent/defaulted loans

• Sub-Servicer: – loan originator in a conduit deal who retains

servicing

July 2001 Brent W. Ambrose, University of Kentucky 52

Role of Servicers

• Special Servicer:– Becomes engaged when loan more than 60 days

delinquent.– Has the authority to

• Extend the loan

• Modify/restructure the loan (based on an appraisal)

• Foreclose

July 2001 Brent W. Ambrose, University of Kentucky 53

Pricing CMBS

• Unlike residential MBS, the underlying mortgages have little prepayment risk.

• However, default risk is now relevant due to these risks:– Lease termination risk– Lease rollover risk

• Imperative to monitor developments in the overall real estate market.– For example, low vacancy rates may lead to additional construction.

• This additional supply can result in reduced real lease rates in future years.

• Has implications on the ability of the property to service the debt in future years.

July 2001 Brent W. Ambrose, University of Kentucky 54

Pricing CMBS

• Rating agencies play a critical role in the CMBS pricing process.– S&P, Moodys, and Duff & Phelps maintain internal models of

collateral risk in order to rate default risk associated with CMBS deals.

• In addition to having to price deals in accordance with rating agency opinions, it is wise to understand the underlying real estate markets in order to anticipate payments delays or defaults. – Example. Lease rates and vacancy rates may look great at

the moment, but will these indicators prompt developers/banks into another frenzy of construction?

July 2001 Brent W. Ambrose, University of Kentucky 55

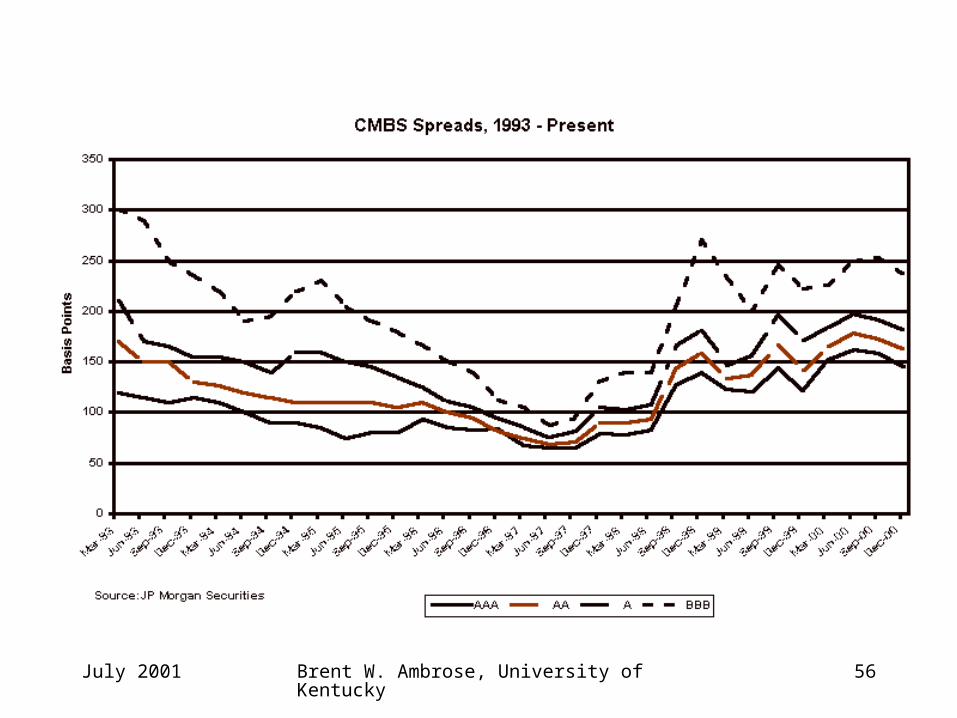

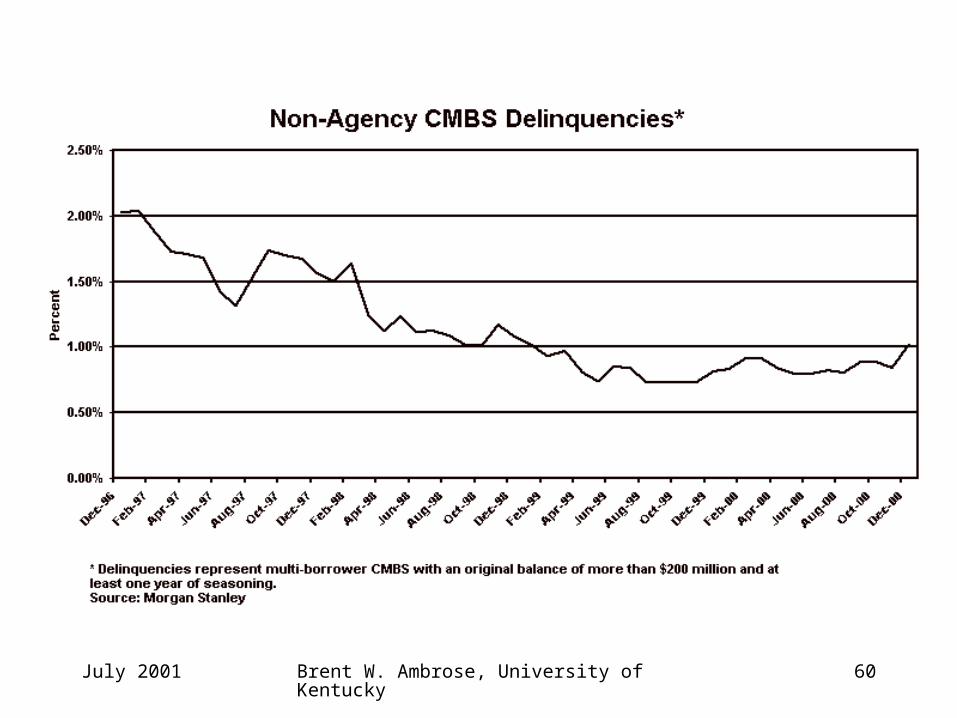

Pricing CMBS

• Remember – CMBS product is part of the fixed-income universe.– Capital markets are linked such that

shocks in one market impact others.• For example – Russian debt crises in

1998– See following charts.

July 2001 Brent W. Ambrose, University of Kentucky 56

July 2001 Brent W. Ambrose, University of Kentucky 57

NCREIF Total Returns

-0.05

-0.04

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

0.04

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Date

Re

turn

July 2001 Brent W. Ambrose, University of Kentucky 58

July 2001 Brent W. Ambrose, University of Kentucky 59

July 2001 Brent W. Ambrose, University of Kentucky 60

July 2001 Brent W. Ambrose, University of Kentucky 61

Bond Market Yields

0

2

4

6

8

10

12

Jan-90 Jan-91 Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01

Date

%

AAA

BBB

Treas

July 2001 Brent W. Ambrose, University of Kentucky 62

Bond SpreadsBond Credit Spreads

0

0.5

1

1.5

2

2.5

3

Jan-90 Jan-91 Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01

Date

Sp

rea

d

AAA

BBB

July 2001 Brent W. Ambrose, University of Kentucky 63

Income Property Debt:Default and Loss Severity

• What do we know about income property default and loss severity?– 1. Fitch ICBA, Inc. (1998)

– 2. Corcoran and Kao (1998)

– 3. Vandell, Barnes, Hartzell, Kraft, and Wendt (1993)

– 4. Snyderman (1994)

*

*-these notes are based on lecture material provided by Thomas Thibodeau at Southern Methodist University.

July 2001 Brent W. Ambrose, University of Kentucky 64

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Study examines Fitch rated transactions between 1991 and 1996

18,839 loans (in 33 CMBS transactions)

total principal $16.1 billion

84% thrift loans (mostly RTC)

16% conduit loans

July 2001 Brent W. Ambrose, University of Kentucky 65

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Examines relationship between default/loss severity and:

Debt service coverage ratio (DSCR) Property type State Loan Size Fixed/floating rate loan Loan type (e.g. amortizing, balloon) Servicer flexibility Foreclosure type

July 2001 Brent W. Ambrose, University of Kentucky 66

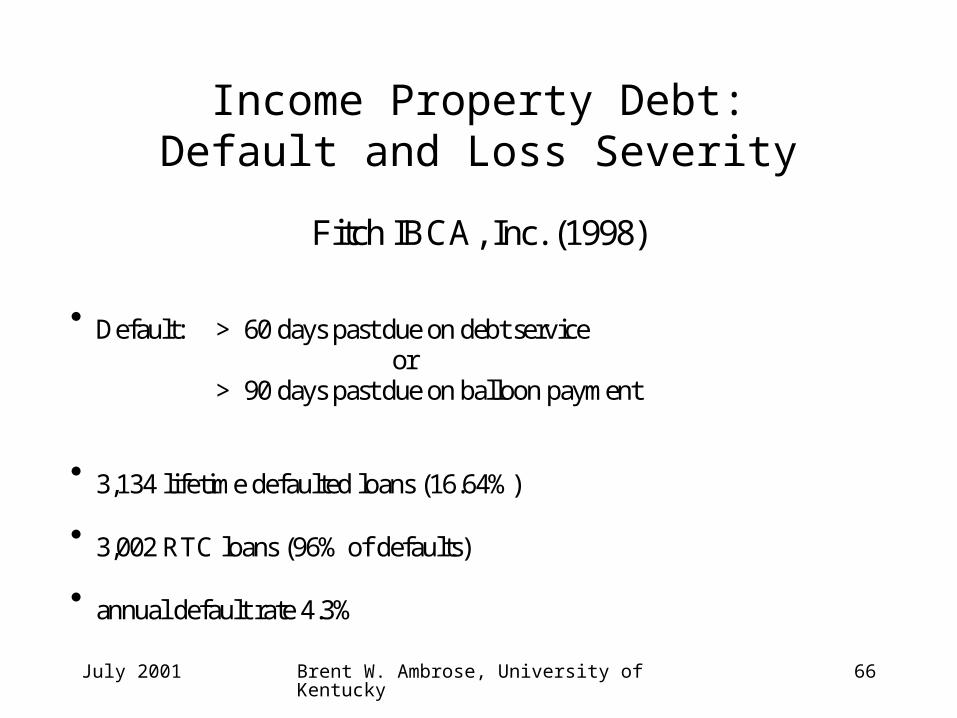

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Default: > 60 days past due on debt service or

> 90 days past due on balloon payment

3,134 lifetime defaulted loans (16.64%)

3,002 RTC loans (96% of defaults)

annual default rate 4.3%

July 2001 Brent W. Ambrose, University of Kentucky 67

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Loss = loan balance at securitization+ interest advanced+ property protection expenses- loan amortization- property income- net sales proceeds

Losses reported as a percent of loan balance at securitization for loansCOMPLETELY resolved (e.g. properties sold).

July 2001 Brent W. Ambrose, University of Kentucky 68

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Source of losses:

Decrease in property value 35.8%+ advanced interest 10.5%+ advanced property protection expenses 7.7%- amortization- property income (combined) 14.9%

Average Loss Rate: 39.1%

July 2001 Brent W. Ambrose, University of Kentucky 69

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

DSCR Default Rate Loss

0.01-0.49 8.0% 47%0.50-0.79 7.0% 52%0.80-0.89 6.6% 42%0.90-0.99 6.5% 41%1.00-1.14 4.4% 29%1.15-1.24 2.6% 48%1.25-1.34 2.4% 27%1.35-1.49 2.8% 36%1.50-1.74 3.1% 41% 1.75+ 2.9% 22%

July 2001 Brent W. Ambrose, University of Kentucky 70

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Property Type Default Rate Loss

Lodging 4.2% 27%Multifamily 3.9% 46%Nursing 4.0% 11%Office 4.8% 38%Industrial 4.7% 27%Other 4.2% 46%Retirement 4.7% 34%Warehouse 2.5% 29%

July 2001 Brent W. Ambrose, University of Kentucky 71

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

State Default Rate Loss

Highest 5: New York 6.8% 32%Louisianna 5.8% 69%New Mexico 5.5% 25%Arizona 5.2% 22%Massachusetts 5.2% 40%

Lowest 5: Iowa 3.5% 65%Florida 3.1% 44%Texas 3.1% 45%Washington 2.4% 25%Oregon 1.9% 34%

July 2001 Brent W. Ambrose, University of Kentucky 72

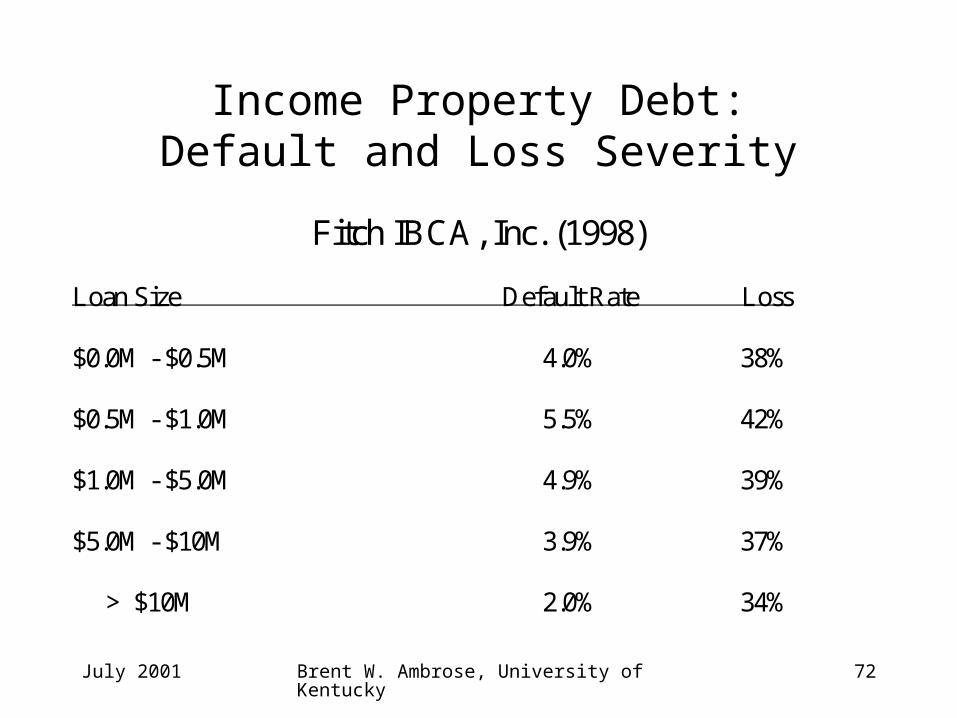

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Loan Size Default Rate Loss

$0.0M - $0.5M 4.0% 38%

$0.5M - $1.0M 5.5% 42%

$1.0M - $5.0M 4.9% 39%

$5.0M - $10M 3.9% 37%

> $10M 2.0% 34%

July 2001 Brent W. Ambrose, University of Kentucky 73

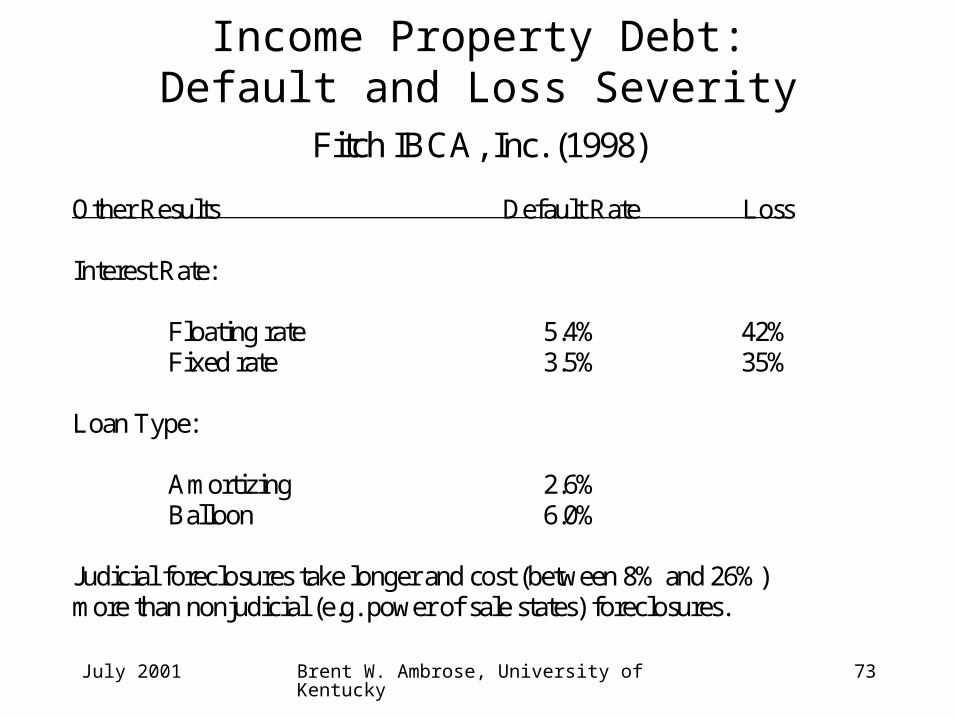

Income Property Debt:Default and Loss Severity

Fitch IBCA, Inc. (1998)

Other Results Default Rate Loss

Interest Rate:

Floating rate 5.4% 42%Fixed rate 3.5% 35%

Loan Type:

Amortizing 2.6%Balloon 6.0%

Judicial foreclosures take longer and cost (between 8% and 26%)more than nonjudicial (e.g. power of sale states) foreclosures.

July 2001 Brent W. Ambrose, University of Kentucky 74

Income Property Debt:Default and Loss Severity

Vandell et. al. (1993)

Use a proportional hazards model to examine the joint effect of loan,borrower, property and market characteristics on the length of time todefault.

The hazard function is the conditional probability of default in the nextperiod given the loan is currently a performing loan.

Data: 2,899 completed loans originated during 1962-1989:3 period175 defaults (6%)

Use the Frank Russell Company Index to market property values tomarket over time.

July 2001 Brent W. Ambrose, University of Kentucky 75

Income Property Debt:Default and Loss Severity

Vandell et. al. (1993) Estimation results: Higher L/V higher default rate Higher interest rate higher default rate DSCR is not a contributing influence All property types have higher default rates RELATIVE TO RETAIL

Greatest risk: hotel, office, apartment Least risk: retail, industrial

Partnerships exhibit greater default risk compared to alternatives

July 2001 Brent W. Ambrose, University of Kentucky 76

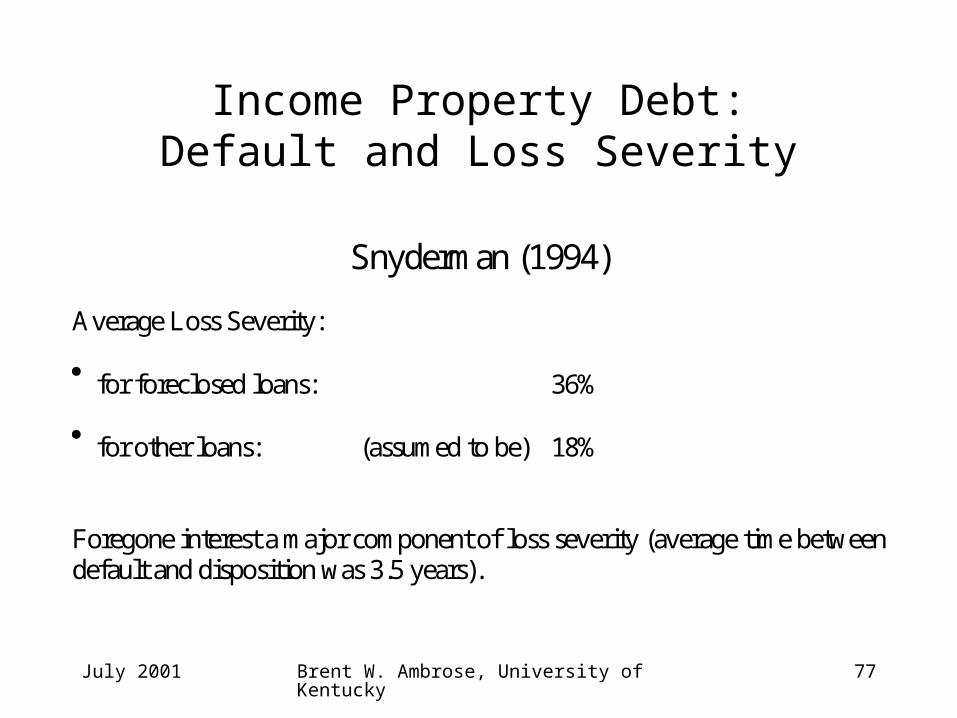

Income Property Debt:Default and Loss Severity

Snyderman (1994)

Snyderman examines:

(1) incidence of lifetime default for 10,955 Insurance Co. loans:a. originated between 1972 and 1989b. tracked over 1972-1991 periodc. 1,512 lifetime defaults (13.8%)

(2) severity of losses:a. defaults that end in foreclosure (46% of defaults)b. defaults resolved some other way (e.g. workout)

(3) estimates “yield cost” of default between 31 and 52 basis points

July 2001 Brent W. Ambrose, University of Kentucky 77

Income Property Debt:Default and Loss Severity

Snyderman (1994)

Average Loss Severity:

for foreclosed loans: 36%

for other loans: (assumed to be) 18%

Foregone interest a major component of loss severity (average time betweendefault and disposition was 3.5 years).

July 2001 Brent W. Ambrose, University of Kentucky 78

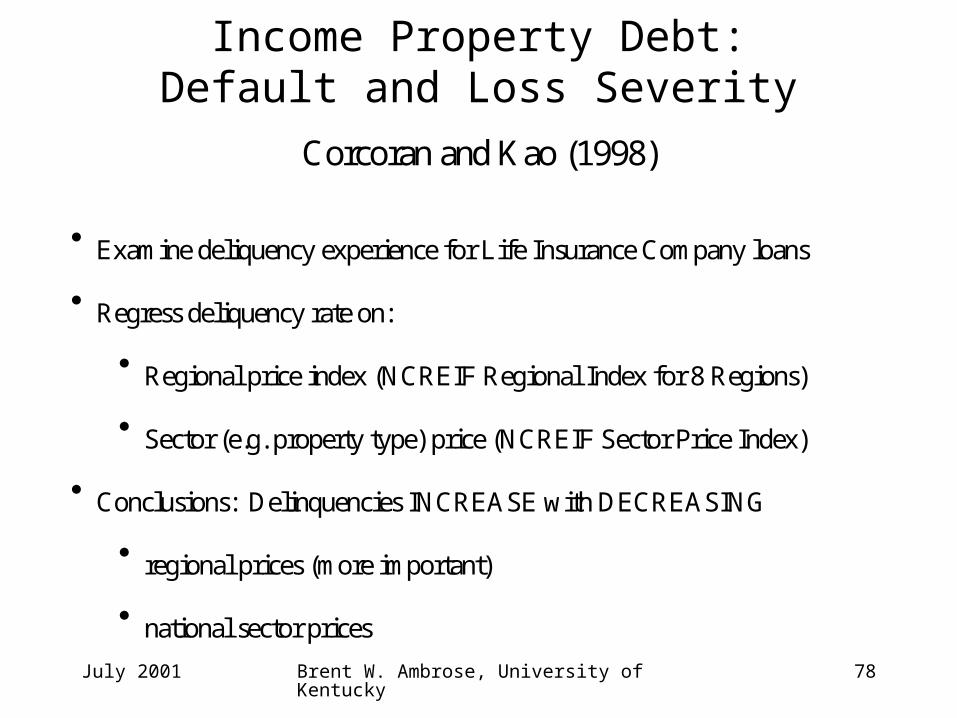

Income Property Debt:Default and Loss Severity

Corcoran and Kao (1998)

Examine deliquency experience for Life Insurance Company loans

Regress deliquency rate on:

Regional price index (NCREIF Regional Index for 8 Regions)

Sector (e.g. property type) price (NCREIF Sector Price Index)

Conclusions: Delinquencies INCREASE with DECREASING

regional prices (more important)

national sector prices

July 2001 Brent W. Ambrose, University of Kentucky 79

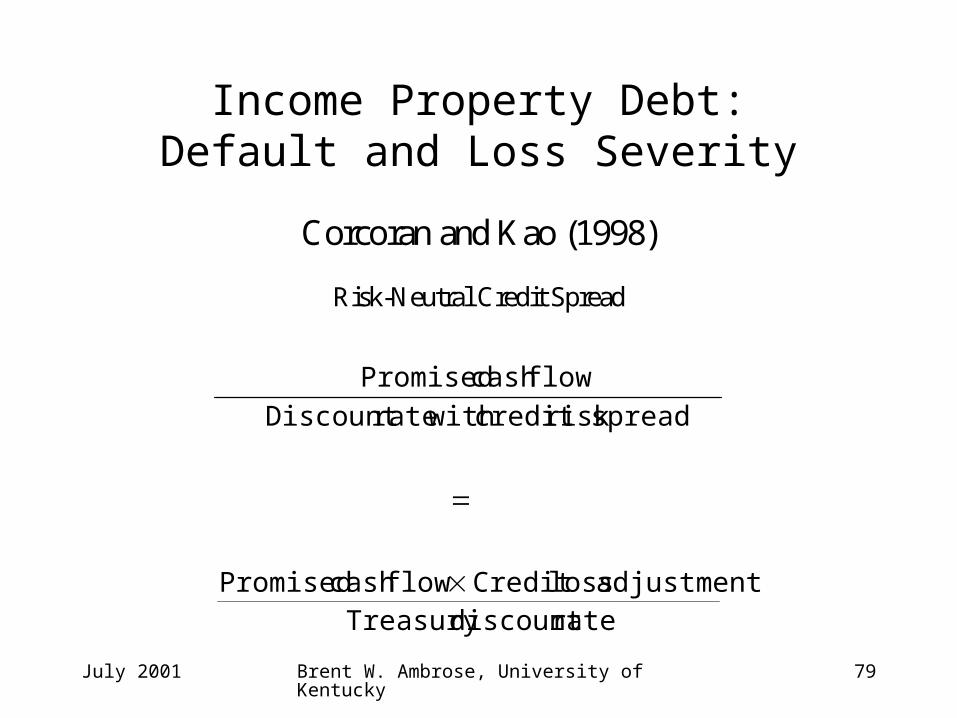

Income Property Debt:Default and Loss Severity

Corcoran and Kao (1998)

Risk-Neutral Credit Spread

ratediscount Treasury adjustment lossCredit flowcash Promised

spreadrisk credit with rateDiscount

flowcash Promised

July 2001 Brent W. Ambrose, University of Kentucky 80

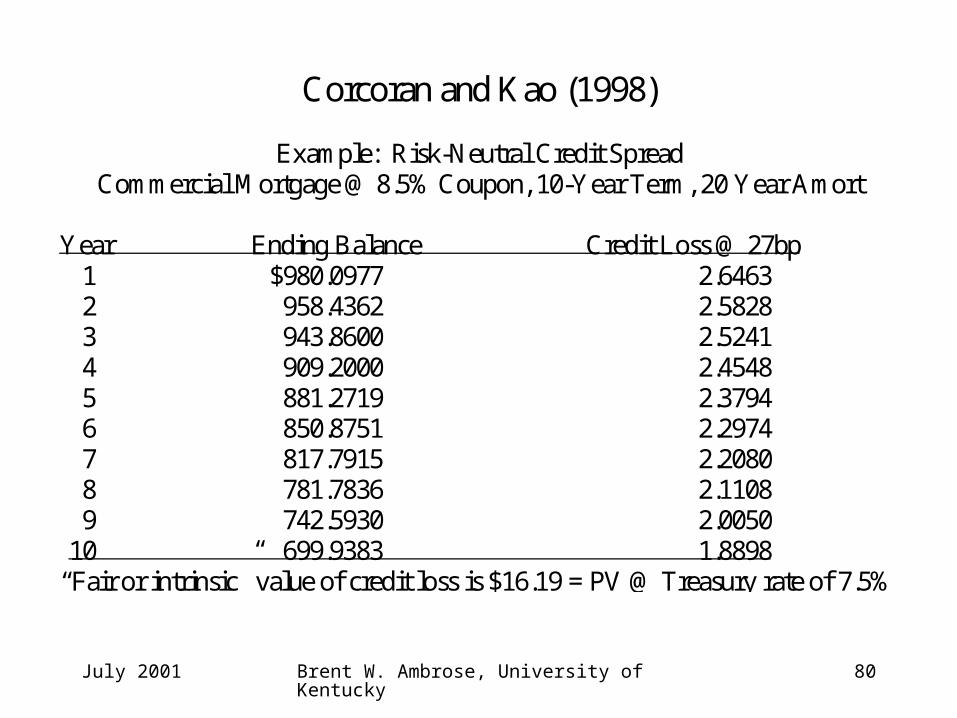

Corcoran and Kao (1998)

Example: Risk-Neutral Credit SpreadCommercial Mortgage @ 8.5% Coupon, 10-Year Term, 20 Year Amort

Year Ending Balance Credit Loss @ 27bp1 $980.0977 2.64632 958.4362 2.58283 943.8600 2.52414 909.2000 2.45485 881.2719 2.37946 850.8751 2.29747 817.7915 2.20808 781.7836 2.11089 742.5930 2.0050

10 699.9383 1.8898“Fair or intrinsic” value of credit loss is $16.19 = PV @ Treasury rate of 7.5%

July 2001 Brent W. Ambrose, University of Kentucky 81

Default and Loss Severity

• To summarize, the studies show that:– Commercial mortgage default estimates are

highly dependent upon the data source.– Most CMBS deals were originated during

period of unprecedented economic growth and expansion.

• Loans have not been tested through full economic cycle.

July 2001 Brent W. Ambrose, University of Kentucky 82

Rating CMBSs

• Property Cash Flow Adjustments

• Capitalization Rate Adjustments

• Pool analysis

• Ideal Pool for Small Income Property Loans

July 2001 Brent W. Ambrose, University of Kentucky 83

Rating CMBSsProperty Cash Flow Adjustments

Rental income = min {contract rent, market rent}

Non-rental income = frequently ignored

Vacancy loss = max {actual, market, 10%}

Operating expenses = max {historical, industry standards, appraisal}

Management fees = max {historical, appraisal, 5% for MF}= max {historical, appraisal, 4% for commercial}

Capital reserves = $250 - $450 per unit for MF= $0.15 - $0.30 per square foot for office= $0.15 - $0.25 psf for retail= 4-5% of Gross Revenues for hotel

July 2001 Brent W. Ambrose, University of Kentucky 84

Rating CMBSs

Property Cash Flow Adjustments

Sources of Information for Industry Standard Operating Expenses

(1) Building Owners and Managers Association (BOMA)

(2) Institute of Real Estate Management (IREM)

(3) Urban Land Institute (ULI)a. Dollars and cents of shopping centersb. Dollars and cents of retailc. Etc.

July 2001 Brent W. Ambrose, University of Kentucky 85

Rating CMBSs

Property Cash Flow Adjustments

Expected property cash flows also adjusted for:

(1) Average lease term (by property type)

(2) Tenant retention (50-60%)a. new tenant improvementsb. renewal tenant improvements

(3) Leasing commissionsa. new leasing commissions (4-6%)b. renewal leasing commissions (varies by property type)

July 2001 Brent W. Ambrose, University of Kentucky 86

Rating CMBSs

Property Cash Flow Adjustments

Financing cash flows adjustments:

(1) below market interest rates increased

(2) loan term adjusted for remaining economic life of the property

July 2001 Brent W. Ambrose, University of Kentucky 87

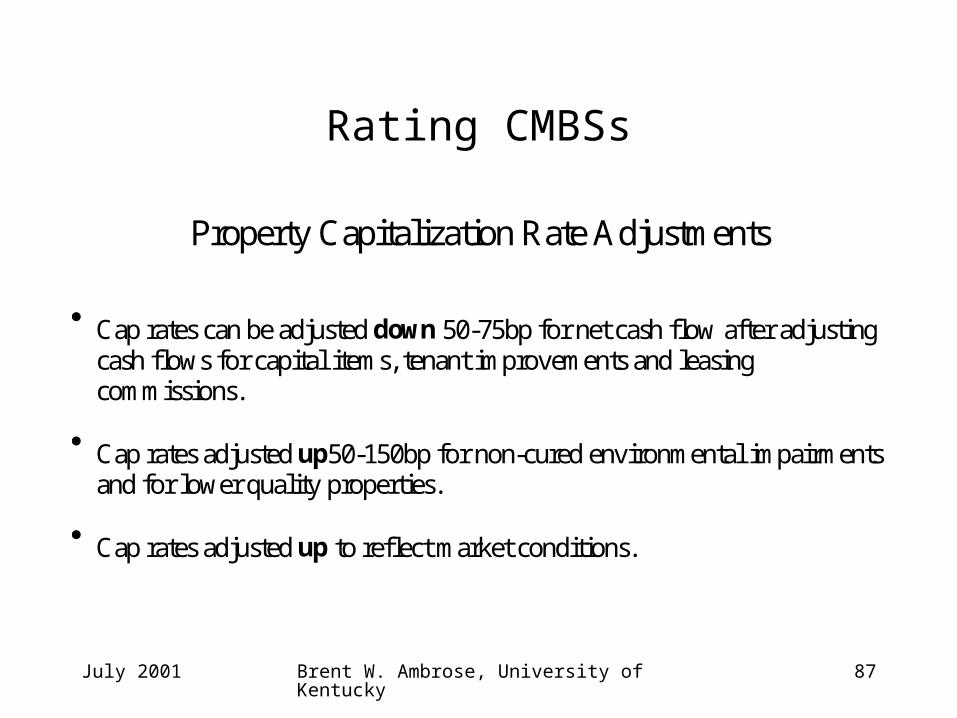

Rating CMBSs

Property Capitalization Rate Adjustments

Cap rates can be adjusted down 50-75bp for net cash flow after adjustingcash flows for capital items, tenant improvements and leasingcommissions.

Cap rates adjusted up50-150bp for non-cured environmental impairmentsand for lower quality properties.

Cap rates adjusted up to reflect market conditions.

July 2001 Brent W. Ambrose, University of Kentucky 88

Rating CMBSs

Pool Analysis

Probability of loss: the probability that any loan will default, beforeclosed on, and be liquidated.

Probability of loss = f(LTV, DSCR, property type, loan structure,fixed/floating rate, loan quality, seasoning,management, ownership structure, barriers toentry (loan to replacement cost, CF volatility,recourse)

Loan loss = f (cost to obtain the asset, time to sell, cost to sell)

July 2001 Brent W. Ambrose, University of Kentucky 89

Rating CMBSs

Ideal Pool for Small Income Property Loans

At least 500 loans

No one loan > 1% of loan balance

Geographically diversified

Taxes, insurance, and capital reserves escrowed

Full recourse

July 2001 Brent W. Ambrose, University of Kentucky 90

CMBS in Singapore

• MAS declared that real estate securitization is a strategic goal.

• Current debt securitization programs:– Mortgage-Backed bonds

• Similar to single mortgage securitization.

• Typical deal will have additional credit enhancements from mortgage borrower.

• Does not have credit rating or credit enhancements from 3rd parties.

– Asset-Backed Securitization• One step further than mortgage-backed bonds in that property securing the

debt is transferred to a “special-purchase vehicle”.