july 13, 2016 - usfia - united states fashion industry ... · trade facilitation and enforcement...

TRANSCRIPT

Trade Facilitation and Enforcement Act of 2015 prepared for the

United States Fashion Industry Association

July 13, 2016

1

1st Reauthorization of CBP since 2003

2

Brief Overview

3

Title 1: Trade Facilitation and Trade Enforcement Title II: Import Health and Safety Title III: Import related Protection of Intellectual Property Rights Title IV: Prevention of Evasion of Antidumping and Countervailing Duty Orders Title V: Small Business Trade Issues and State Trade Coordination Title VI: Additional Enforcement Provisions Title VII: Currency Manipulation Title VIII: Matters Relating to US Customs and Border Protection Title IX: Miscellaneous Provisions

Section 910 Forced Labor

Elimination of consumptive demand “loophole”

CBP actions Issuance of detention or withhold release

orders

4

Withhold release orders The orders require detention at all U.S. ports of

entry of any subject merchandise manufactured by the identified company(ies)

Importers of detained shipments are provided

an opportunity to demonstrate that the merchandise was not produced with forced labor.

5

Forced Labor

6

Order on Chemical, Fiber Products Produced by Forced Labor in China Release Date: March 29, 2016 WASHINGTON — U.S. Customs and Border Protection Commissioner R. Gil Kerlikowske today directed the issuance of a withhold release order against imported soda ash, calcium chloride, caustic soda, and viscose/rayon fiber manufactured or mined by Tangshan Sanyou Group and its subsidiaries in the People’s Republic of China. The order will require detention at all U.S. ports of entry of any of such merchandise manufactured by this company.

Forced Labor

“It is imperative that companies examine their supply chains to understand product sourcing and the labor used to generate their products,” said Commissioner Kerlikowske. “CBP is committed to ensuring U.S. values outweigh economic expediency and as part of its trade enforcement responsibilities, will work to ensure products made with forced labor do not cross our borders.”

7

Title IV: Prevention of Evasion of Antidumping and Countervailing Duty Orders

Deals with the evasion of trade remedy orders (i.e., antidumping and countervailing duties)

Expands the tools that CBP and the Department of Commerce have available to address evasions of trade remedy order duties.

The Act also makes CBP’s civil and criminal investigations more transparent to domestic industry.

8

9

CBP Creates Trade Enforcement Task Force U.S. Customs and Border Protection established a Trade Enforcement Task Force last month within CBP’s Office of Trade to further protect the American economy and domestic industry. The task force is focused on issues related to enforcement of antidumping and countervailing duty laws, and interdiction of imported products using forced labor. Both antidumping and countervailing duty are tariffs imposed on foreign imports priced below fair market value to ensure a level playing field for domestic producers. “This task force strengthens CBP's ability to detect high-risk activity, target illicit trade networks, and work with industry to disrupt evasion of U.S. trade laws,” said CBP Commissioner R. Gil Kerlikowske. “ It focuses expertise and resources to safeguard the U.S. market and ensure a fair and competitive trade environment.“ The task force enables CBP to leverage new enforcement authorities of the Trade Facilitation and Trade Enforcement Act of 2015, which strengthens CBP’s enforcement capabilities and methods to better enforce U.S. trade laws, including antidumping countervailing duty laws. The Act also enhance CBP’s efforts to combat the import of counterfeit goods and protect intellectual property rights holders, and eliminates obstacles to preventing imports made with forced or child labor into the United States. The CBP task force will harness the agency’s collective trade enforcement expertise as a focal point for coordination with other government agency partners, including Department of Commerce and U.S. Immigration and Customs Enforcement’s Homeland Security Investigations. By focusing its combined resources through the enforcement task force, CBP will be able to combat illicit traders that illegally exploit American trade and conduct enforcement operations at and beyond the border to ensure U.S. industry can compete on a level playing field.

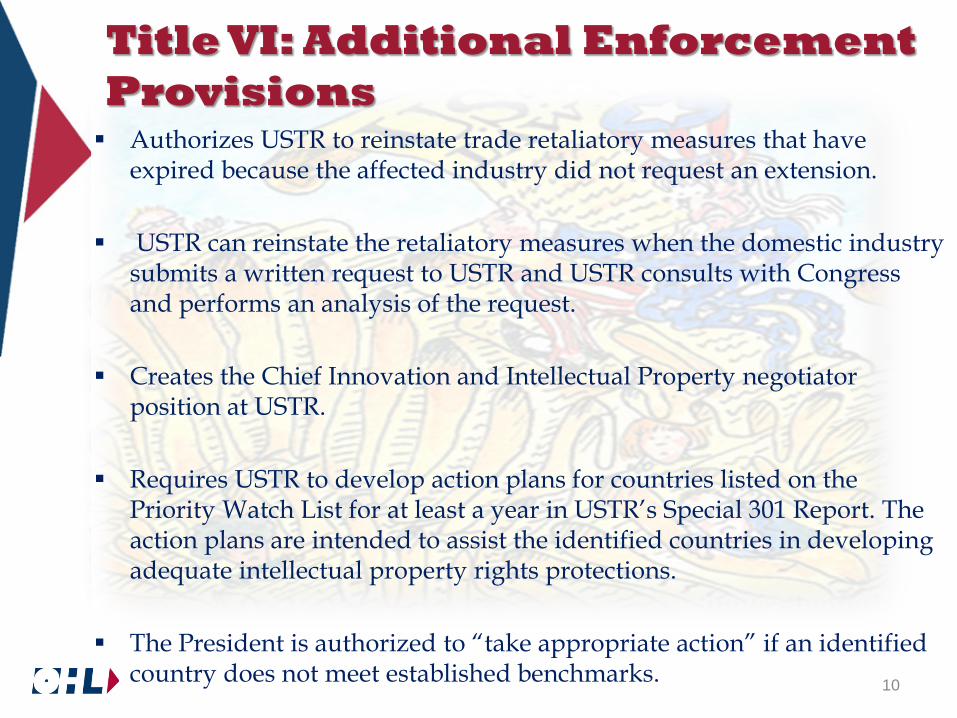

Title VI: Additional Enforcement Provisions Authorizes USTR to reinstate trade retaliatory measures that have

expired because the affected industry did not request an extension.

USTR can reinstate the retaliatory measures when the domestic industry submits a written request to USTR and USTR consults with Congress and performs an analysis of the request.

Creates the Chief Innovation and Intellectual Property negotiator position at USTR.

Requires USTR to develop action plans for countries listed on the Priority Watch List for at least a year in USTR’s Special 301 Report. The action plans are intended to assist the identified countries in developing adequate intellectual property rights protections.

The President is authorized to “take appropriate action” if an identified country does not meet established benchmarks. 10

Title 1:Trade Facilitation and Trade Enforcement

Requires CBP to improves its partnership programs. Codifies the Centers of Excellence and Expertise in order to process

entries more efficiently. Requires the publication of reports or plans.

Requires CBP to develop minimum criteria for an importer to obtain an

importer of record number and maintain a centralized database of importer of record numbers.

Requires CBP to establish a new importer program under which CBP can assess new importers and their imported products.

Requires that CBP implement new minimum requirements for the type of information that customs brokers must obtain from their customers in order to verify the importer’s identity.

11

Title IX- Miscellaneous Provisions

Includes various miscellaneous provisions, such as, but not limited to: • Increase to the de-minimis threshold for low-

value shipments • Amendments to Chapter 98 to address certain

returned goods • Drawback Simplification • Limits CBP’s ability to voluntarily re-liquidate

entries

12

Section 901

Increase to the de-minimis threshold for low-value shipments

Allows the duty-free entry of a shipment valued at $800

(an increase from $200) or less that is imported by one person on one day, with minimal documentation requirements. Also known as a “Section 321” entry which comes from the provision’s statutory source, 19 U.S.C. § 1321(a)(2)(C).

This affects merchandise imported or withdrawn from

warehouse for consumption on, or after March 06, 2016. Contains guidance from Congress that USTR should

encourage foreign countries to establish commercially meaningful de-minimis thresholds for express and postal shipments. 13

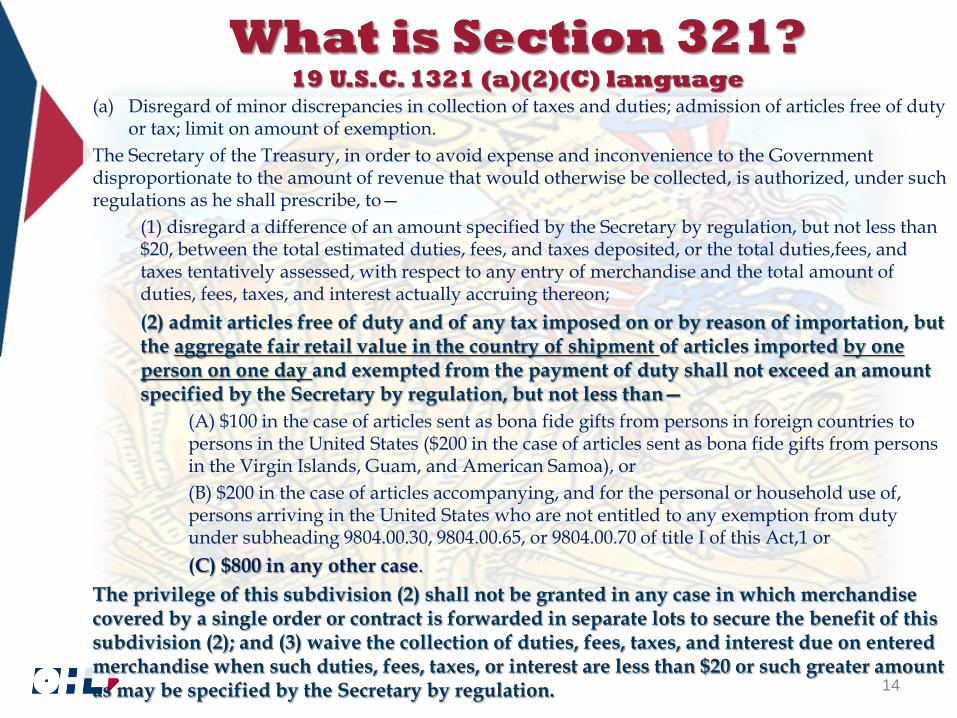

What is Section 321? 19 U.S.C. 1321 (a)(2)(C) language

(a) Disregard of minor discrepancies in collection of taxes and duties; admission of articles free of duty or tax; limit on amount of exemption.

The Secretary of the Treasury, in order to avoid expense and inconvenience to the Government disproportionate to the amount of revenue that would otherwise be collected, is authorized, under such regulations as he shall prescribe, to—

(1) disregard a difference of an amount specified by the Secretary by regulation, but not less than $20, between the total estimated duties, fees, and taxes deposited, or the total duties,fees, and taxes tentatively assessed, with respect to any entry of merchandise and the total amount of duties, fees, taxes, and interest actually accruing thereon; (2) admit articles free of duty and of any tax imposed on or by reason of importation, but the aggregate fair retail value in the country of shipment of articles imported by one person on one day and exempted from the payment of duty shall not exceed an amount specified by the Secretary by regulation, but not less than—

(A) $100 in the case of articles sent as bona fide gifts from persons in foreign countries to persons in the United States ($200 in the case of articles sent as bona fide gifts from persons in the Virgin Islands, Guam, and American Samoa), or (B) $200 in the case of articles accompanying, and for the personal or household use of, persons arriving in the United States who are not entitled to any exemption from duty under subheading 9804.00.30, 9804.00.65, or 9804.00.70 of title I of this Act,1 or (C) $800 in any other case.

The privilege of this subdivision (2) shall not be granted in any case in which merchandise covered by a single order or contract is forwarded in separate lots to secure the benefit of this subdivision (2); and (3) waive the collection of duties, fees, taxes, and interest due on entered merchandise when such duties, fees, taxes, or interest are less than $20 or such greater amount as may be specified by the Secretary by regulation.

14

What Section 321 IS

A vacationer arriving in the U.S. from Ireland while transporting a shawl purchased for $150.00 at a farming mill in Cork, Ireland.

A dress arriving in the U.S. from an online retailer in China pursuant to an individual ecommerce order valued at $575.00

Two Men’s Dress Shirts purchased by a U.S. retailer, from a manufacturer in Vietnam, the retail value of which is $125.00 each in Vietnam, arriving in one shipment into the U.S.

15

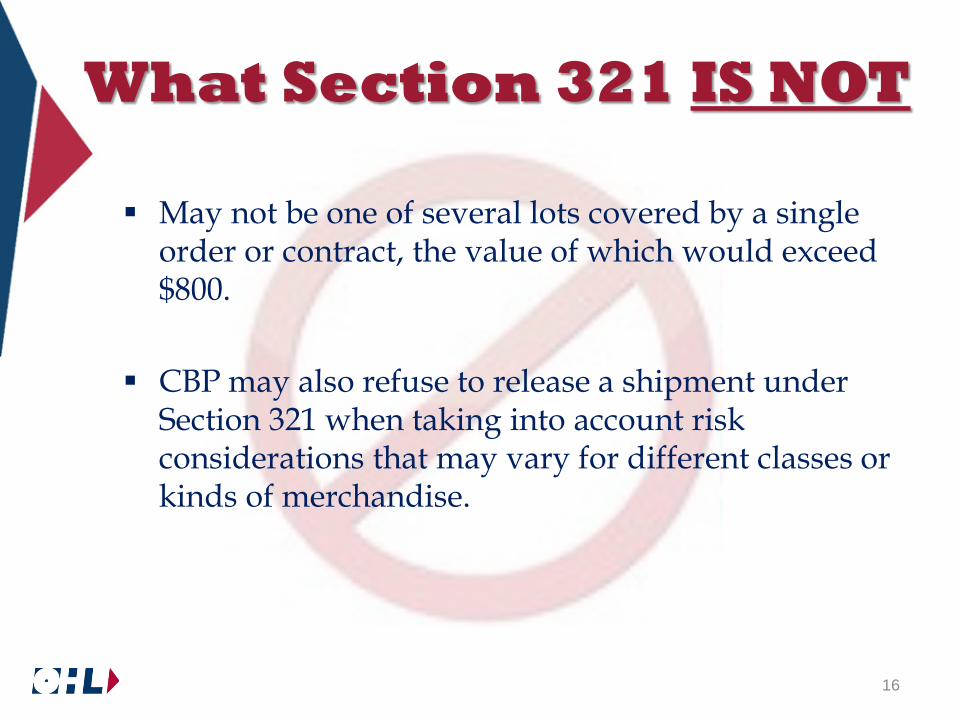

What Section 321 IS NOT

May not be one of several lots covered by a single order or contract, the value of which would exceed $800.

CBP may also refuse to release a shipment under

Section 321 when taking into account risk considerations that may vary for different classes or kinds of merchandise.

16

17

Trade Facilitation and Trade Enforcement Act of 2015 Increase in the De Minimis Value Exemption Background On February 24, 2016, the President signed the Trade Facilitation and Trade Enforcement Act of 2015, strengthening the capabilities of the U.S. Customs and Border Protection (CBP) to enforce U.S. trade laws and regulations, streamline and facilitate the movement of legitimate trade, and interdict non-compliant trade. The Act of 2015 included an amendment of Section 321 of the Tariff Act of 1930, as amended (19 U.S.C. § 1321) to increase the de minimis value exemption from duties and taxes from $200 to $800, which CBP implemented on March 10, 2016. CBP Authority: As a reminder, even in the case of low value shipment, CBP has the right to require a formal entry on any shipment where additional information, bonding, or protection is required. The administrative exemption may be denied if CBP believes that the shipment was sent as a low value shipment for the purpose of avoiding compliance with any pertinent law or regulation. What Changed? The value of a shipment imported by one person on one day that generally may be imported free of duties and taxes has increased from $200 to $800. Shipments valued at $800 or less for the de minimis exemption are eligible for release under the same processes and with the same restrictions that previously applied to shipments valued at $200 or less. Processes: Manual Processing (all modes): Importer may provide oral declaration or evidence document of

fair retail value of $800 or less Land Border Truck: Low value shipments may be released off of the electronic truck manifest by

accepting the release on the primary lane Rail, Sea, and Air (standard and express air): CBP may release low value shipments after

electronic manifest is reviewed in the Automated Commercial Environment (ACE) by manual posting, as appropriate

18

What Remains the Same? All existing processes and restrictions for merchandise shipments remain the same with the exception of increasing the de minimis value exemption. Conditions and Exceptions: Shipment must be imported by one person on one day Consolidated shipments addressed to one ultimate consignee are treated as one

importation No alcoholic beverage, perfume containing alcohol (except where the aggregate

fair retail value in the country of shipment of all merchandise contained in the shipment does not exceed $5), cigars, or cigarettes will be exempted from duty and tax payment

Exemption is not allowed if CBP believes that the shipment is one of several lots covered by a single order or contract, and that it was sent separately for the express purpose of securing free entry or for the purpose of avoiding compliance with any pertinent law or regulation

Exemption is not allowed in the case of any merchandise of a class or kind provided for in any tariff-rate quota

Exemption is not allowed if one or more Partner Government Agencies require information to fulfill their regulatory requirements

Increase in the De Minimis Value Exemption continued

Low Value Shipments

Questions to CBP regarding proper entry of these goods How to properly declare value? How to define ‘country of shipment’? How to monitor daily-use limitation? How to monitor single-order limitation? How to enforce PGA interests?

19

Section 906

Drawback and Refunds Imported goods of one eight-digit HTSUS subheading are

permitted to qualify for duty drawback when goods of the same subheading are exported. For unused Drawback, claimant can use the Schedule B number to determine if the merchandise is classifiable under the same eight digit HTSUS subheading as the imported merchandise.

Extends the time frame for filing drawback from 3 years to 5 years from the date the merchandise was imported

Duties, taxes, and fees are eligible for drawback , instead of just duties in some scenarios

In substitution drawback, claimants may claim the lesser of (1) duties, taxes and fees that are paid on the imported merchandise on the entry-line item level; or (2) the duties, taxes and fees that would have been paid on the export if it had been imported.

20

Section 906

Drawback and Refunds

If drawback is claimed on merchandise that is exported, the record of exportation must be contained in a record kept by the exporter in the normal course of business or be entered into the Automated Export System once it is determined to be a system of record.

Amends CBP’s recordkeeping statute (19 U.S.C. § 1508) to require that records for drawback claims be maintained for three years from liquidation, as opposed to the current date of payment of the claim.

21

Drawback Regulations

Being drafted with input from trade Competing deliverables Drawback filing in ACE TFTEA regulations Process Simplification ideas

22

Title III: Import related Protection of Intellectual Property Rights

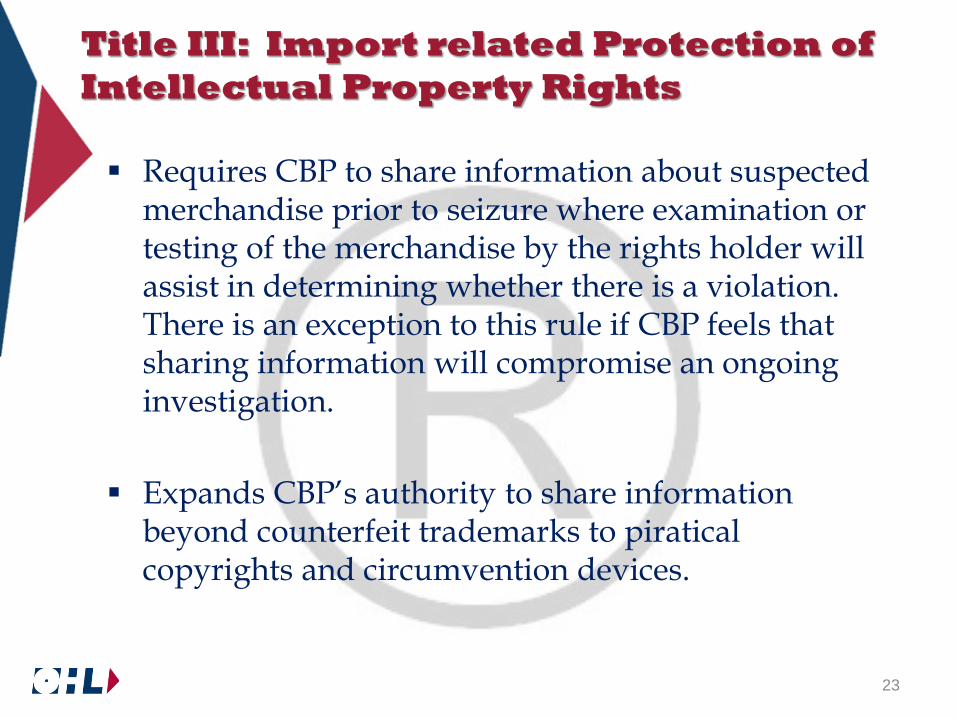

Requires CBP to share information about suspected merchandise prior to seizure where examination or testing of the merchandise by the rights holder will assist in determining whether there is a violation. There is an exception to this rule if CBP feels that sharing information will compromise an ongoing investigation.

Expands CBP’s authority to share information

beyond counterfeit trademarks to piratical copyrights and circumvention devices.

23

Additional Resources

https://www.congress.gov/bill/114th-congress/house-bill/644/text

OHL Trade Services: Mary Jo Muoio @[email protected]

24

Thank You!

25

Title II: Import Health and Safety

Establishes an interagency Import Safety Working Group, to ensure the safety of U.S. imports and to identify best practices to improve a coordinated government response to threats.

Requires CBP to create a joint-response plan to respond to

incoming cargo that poses a health and safety threat. The Group will include representatives from the departments of Health and Human Services, Treasury, Commerce and Agriculture; the Office of the U.S. Trade Representative; the Office of Management and Budget; the Food and Drug Administration ; CBP; and the Consumer Product Safety Commission.

26

Title V: Small Business Trade Issues and State Trade Coordination

Ensures that small businesses have a voice when the U.S. government considers negotiating new free trade agreements (FTAs).

Establishes working groups that are tasked

with reporting on the impact of an FTA on small businesses and coordinating on export promotion and financing.

27

Title VII: Currency Manipulation

Requires the Secretary of the Treasury to submit a report to Congress on the macroeconomic and currency exchange rate policies for major trading partner countries.

The Secretary of the Treasury is required to take action to address currency issues with major trading partners that are subject to enhanced macroeconomic analysis.

In the event that the Secretary of the Treasury is unable to address currency manipulation issues with the major trading partner, the President may take steps to remedy the situation.

The President can waive the remedial actions only if he finds that the action would have an adverse impact on the U.S. economy or would cause serious harm to U.S. national security

28

Title VIII: Establishment of CBP Reauthorizes CBP and formalizes the process for establishing CBP

preclearance facilities at airports in foreign countries.

The purpose of the preclearance facilities is to (1) prevent terrorist attacks in the United States; (2) prevent inadmissible foreigners from entering the United States; (3) ensure that imported merchandise complies with U.S. law; (4) promptly process people entering the United States; and (5) accomplish any other objectives necessary to protect the United States.

Outlines the procedures that CBP must follow to notify Congress before it establishes a preclearance facility. It includes reports on the impact of the facility on U.S. trade and travel, CBP staffing, and potential security vulnerabilities.

CBP is authorized to enter into cost-sharing agreements with airport

authorities and allows airport authorities to make advance payments when establishing new facilities.

29

Section 904: Amendments to Chapter 98

of the HTSUS

Section 904(a) modernizes the rules for goods imported under subheadings 9802.00.40 and 9802.00.50, HTSUS by allowing merchandise to be commingled and by providing that the origin, value and classification of such articles may be accounted for using an inventory management method.

Section 904(b) amends the article description for subheading 9801.00.10, HTSUS so that it includes any other products when returned within three years, after having been exported.

Section 904(c) creates a new heading 9801.00.11, which provides duty-free treatment for certain U.S. government property returned to the United States either by the U.S. government or a U.S. government contractor.

30

Title IX Section 904 (b)Chapter 9801.00.10

Products of the United States when returned after having been exported, without having been advanced in value or improved in condition by any process of manufacture or other means while abroad

Previously excluded textile, apparel, or footwear chapters

Now includes “any other products when returned

within 3 years after having been exported”

31

What Title IX Section 904 IS

Importer shipped apparel to a foreign country to fill an order. Foreign customer has merchandise that they would like to return to the US. Until now, there was no duty free provision afforded to the return to U.S.

Consolidated e-commerce returns

32