journal of accounting and finance...one reason students do not major in accounting is the perception...

TRANSCRIPT

Journal of Accounting and Finance

North American Business Press Atlanta – Seattle – South Florida - Toronto

Journal of Accounting and Finance

Dr. Samanthala Hettihewa Co-Editor

Dr. Christopher Wright

Co-Editor

Dr. David Smith, Editor-In-Chief

NABP EDITORIAL ADVISORY BOARD

Dr. Andy Bertsch - MINOT STATE UNIVERSITY Dr. Jacob Bikker - UTRECHT UNIVERSITY, NETHERLANDS Dr. Bill Bommer - CALIFORNIA STATE UNIVERSITY, FRESNO Dr. Michael Bond - UNIVERSITY OF ARIZONA Dr. Charles Butler - COLORADO STATE UNIVERSITY Dr. Jon Carrick - STETSON UNIVERSITY Dr. Mondher Cherif - REIMS, FRANCE Dr. Daniel Condon - DOMINICAN UNIVERSITY, CHICAGO Dr. Bahram Dadgostar - LAKEHEAD UNIVERSITY, CANADA Dr. Deborah Erdos-Knapp - KENT STATE UNIVERSITY Dr. Bruce Forster - UNIVERSITY OF NEBRASKA, KEARNEY Dr. Nancy Furlow - MARYMOUNT UNIVERSITY Dr. Mark Gershon - TEMPLE UNIVERSITY Dr. Philippe Gregoire - UNIVERSITY OF LAVAL, CANADA Dr. Donald Grunewald - IONA COLLEGE Dr. Russell Kashian - UNIVERSITY OF WISCONSIN, WHITEWATER Dr. Jeffrey Kennedy - PALM BEACH ATLANTIC UNIVERSITY Dr. Jerry Knutson - AG EDWARDS Dr. Dean Koutramanis - UNIVERSITY OF TAMPA Dr. Malek Lashgari - UNIVERSITY OF HARTFORD Dr. Priscilla Liang - CALIFORNIA STATE UNIVERSITY, CHANNEL ISLANDS Dr. Tony Matias - MATIAS AND ASSOCIATES Dr. Patti Meglich - UNIVERSITY OF NEBRASKA, OMAHA Dr. Robert Metts - UNIVERSITY OF NEVADA, RENO Dr. Adil Mouhammed - UNIVERSITY OF ILLINOIS, SPRINGFIELD Dr. Roy Pearson - COLLEGE OF WILLIAM AND MARY Dr. Veena Prabhu - CALIFORNIA STATE UNIVERSITY, LOS ANGELES Dr. Sergiy Rakhmayil - RYERSON UNIVERSITY, CANADA Dr. Robert Scherer - CLEVELAND STATE UNIVERSITY Dr. Ira Sohn - MONTCLAIR STATE UNIVERSITY Dr. Reginal Sheppard - UNIVERSITY OF NEW BRUNSWICK, CANADA Dr. Carlos Spaht - LOUISIANA STATE UNIVERSITY, SHREVEPORT Dr. Ken Thorpe - EMORY UNIVERSITY Dr. Robert Tian - MEDIALLE COLLEGE Dr. Calin Valsan - BISHOP'S UNIVERSITY, CANADA Dr. Anne Walsh - LA SALLE UNIVERSITY Dr. Thomas Verney - SHIPPENSBURG STATE UNIVERSITY

Volume 13(4) ISSN 2158-3625 Authors have granted copyright consent to allow that copies of their article may be made for personal or internal use. This does not extend to other kinds of copying, such as copying for general distribution, for advertising or promotional purposes, for creating new collective works, or for resale. Any consent for republication, other than noted, must be granted through the publisher:

North American Business Press, Inc. Atlanta – Seattle – South Florida - Toronto

©Journal of Accounting and Finance 2013 For submission, subscription or copyright information, contact the editor at: [email protected] Subscription Price: US$ 310/yr Our journals are indexed by UMI-Proquest-ABI Inform, EBSCOhost, GoogleScholar, and listed with Cabell's Directory, Ulrich's Listing of Periodicals, Bowkers Publishing Resources, the Library of Congress, the National Library of Canada. Our journals have been accepted through precedent as scholarly research outlets by the following business school accrediting bodies: AACSB, ACBSP, & IACBE.

This Issue

Return Attribution: A Modified Bootstrapping Approach ................................................................... 11 John M. Geppert, Donna M. Dudney The return to an investment strategy results from the combined effect of three types of decisions: (1) which assets to consider (selection), (2) the proportion of wealth to allocate to each asset (allocation) and (3) when to rebalance the portfolio (rebalancing). In this paper, we develop an easy to implement, bootstrapping procedure which can disentangle the total ex-post investment return into its component parts. Rebalancing results in transactions cost that partially offset returns. Our procedure allows one to assess ex-post whether the additional cost of rebalancing is justified by higher returns. Exploring the Cognitive Effects of Persuasive Messaging on Students’ Perceptions about Accounting ................................................................................................................. 23 Joseph C. Ugrin, Darla Honn, Heber Garcia, Richard L. Ott One reason students do not major in accounting is the perception that accounting is dull and boring. Through the lens of media richness theory, this study explores how perceptions can be changed by promotional media. The results show that promotional media aimed at perception change can influence perceptions about accounting if the message is presented with rich media that incorporates auditory and visual stimuli. Positive changes in perception occurred through an affective response which influenced perception directly, and influenced perception indirectly through increased involvement with the details of the message. The results of the study offer theoretical and practical contributions. Decoupled or Not? What Drives Chinese Stock Markets: Domestic or Global Factors? .................. 40 Priscilla Liang A Vector Error Correction Model (VECM) is used in this paper to identify the factors that affect Chinese stock returns. Test results show that Chinese stock performance has long run equilibrium relationships with both its domestic economic fundamentals and foreign national stock indices. Chinese stocks are sensitive to policy driven economic variables such as exchange rate and bank loans and deposits, but not to real economic forces such as the industrial production. Stock performance in China is closely “coupled” with that in India, Russia, the U.S., Germany, Japan, South Korea, and Mexico. The U.S. has the most influence on China. Reciprocal Cost Allocations for Many Support Departments Using Spreadsheet Matrix Functions ...................................................................................................... 55 Dennis Togo The reciprocal method for allocating costs of support departments is the only method that recognizes all services provided to other departments. Yet, even as the number of support departments and their costs increase, the adoption of the reciprocal method has been hampered since it requires solving simultaneous equations for reciprocated costs of each support department. Matrix functions in spreadsheets will solve for reciprocated costs of many support departments. The Sasha Case illustrates the use of matrices to model services among support and operating departments, to solve simultaneous equations for the reciprocated costs of support departments, and to allocate the reciprocated costs to other departments.

Is the Loss of Tax-Exempt Status For Previous Filers Related to Indicators of Financial Distress? ........................................................................................... 60 John M. Trussel The US Congress passed the Pension Protection Act of 2006 (PPA) that automatically revokes the tax-exempt status of any organization that does not file with the IRS for three consecutive years. This study focuses on charities that previously filed with the IRS, and it examines whether or not the loss of tax-exempt status is related to indicators of financial distress. The results show that charities that lost their tax-exempt status have smaller equity reserves, higher revenue concentration, lower operating margins, more debt (relative to assets) and are younger and smaller than their counterparts. Analysis of REITs and REIT ETFs Cointegration during the Flash Crash ........................................ 74 Stoyu I. Ivanov In this study I revisit the “disintegration hypothesis” of financial assets around a major crisis event. I examine whether the Vanguard Real Estate Investment Trust and iShares Dow Jones US Real Estate Index Fund exchange traded funds disintegrate from the ten largest Real Estate Investment Trusts during the 14:45 Flash Crash on May 6, 2010. I find that six of the ten largest REITs are not cointegrated with the Vanguard Real Estate Investment Trust prior to the Flash Crash and that five of the ten largest REITs are not cointegrated with iShares Dow Jones US Real Estate Index Fund prior to the Flash Crash. After the Flash Crash all REITs are cointegrated with the two REIT ETFs. This clearly refutes the “disintegration hypothesis” of REITs and REIT ETFs. ROE and Corporate Social Responsibility: Is There a Return On Ethics? ......................................... 82 Omid Sabbaghi, Min Xu In light of the financial crisis of 2008, this study examines the return performance of U.S. companies that exhibit high ratings for ethics and corporate social responsibility (CSR). The highly rated CSR firms are identified via Corporate Responsibility (CR) Magazine’s Best 100 Corporate Citizens list for 2010, known as one of the world’s top corporate responsibility ranking. We employ traditional event study methodology to assess the effects of the CSR news announcement. In our study, we find that the return performance of socially responsible firms exhibits similar time-series dynamics to that of a broad market portfolio comprising of all NYSE, Nasdaq, and AMEX stocks. While several CSR firms may provide exceptionally high returns, we find that on average, the socially responsible portfolio’s risk-return profile does not differ significantly from that of the broad-based market portfolio. While we document a rise in the cumulative abnormal return for the CSR portfolio prior to the news announcement, we find that the upward drift in asset prices disappears following the announcement date and after controlling for market-wide sources of risk. This study is one of the first investigations that focuses on the return performance of CSR firms in the aftermath of the global financial crisis of 2008. Our results collectively provide evidence in support of the Efficient Markets Hypothesis and suggest that the CSR rankings announcement provided by Corporate Responsibility Magazine is indicative of good news for these firms.

Private Equity Firms: Decisions Influenced by Time and the Implications for Value Harvesting .......................................................................................................... 96 Lachlan R. Whatley, Bill Doucette This paper combines existing theory on approaches to organizational change interventions and links this theory to the price earnings ratio method of valuation. In doing so, this paper introduces levers for value creation that are determined by the appropriate change intervention typology and are influenced by the constraint of time. This paper then takes this new theory and applies it to a case study1. As a result, this theoretical paper seeks to showcase the importance of time and the possible implications for the chosen intervention method, which ultimately influence value harvesting for private equity firms. Is Community Bank Creating Value for Shareholders? ..................................................................... 107 John S. Walker, Victoria Geyfman The questions posed by the CEO of Community Bank were quite direct: “Is our bank creating value for shareholders?” Mindful of recent industry consolidation, he also asked, “Should the board consider selling the bank to another bank?” Many banks are asking the same questions now that the operating environment for banks has changed. Prior to the credit crisis, banks had to implement new regulatory procedures prompted by the passage of Sarbanes-Oxley. Since the crisis, the Dodd-Frank Act and Basel III are keeping bankers awake at night wondering if the community bank model can survive the added regulations and weak economy.

GUIDELINES FOR SUBMISSION

Journal of Accounting and Finance (JAF)

Domain Statement The Journal of Accounting and Finance (JAF) is dedicated to the advancement and dissemination of research across all the leading fields of financial inquiry by publishing, through a blind, refereed process, ongoing results of research in accordance with international scientific or scholarly standards. Articles are written by business leaders, policy analysts and active researchers for an audience of specialists, practitioners and students in all areas related to financial and accounting in business and education. Studies reflecting issues concerning budgeting, taxation, process, investments, regulatory procedures, and business financial analysis are suitable themes. JAF also covers theoretical and empirical analysis relating to financial reporting, asset pricing, financial markets and institutions, corporate finance, and corporate governance. Articles of regional interest are welcome, especially those dealing with lessons that may be applied in other regions around the world. Submission Format Articles should be submitted following the American Psychological Association format. Articles should not be more than 30 double-spaced, typed pages in length including all figures, graphs, references, and appendices. Submit two hard copies of manuscript along with a disk typed in MS-Word. Make main sections and subsections easily identifiable by inserting appropriate headings and sub-headings. Type all first-level headings flush with the left margin, bold and capitalized. Second-level headings are also typed flush with the left margin but should only be bold. Third-level headings, if any, should also be flush with the left margin and italicized. Include a title page with manuscript which includes the full names, affiliations, address, phone, fax, and e-mail addresses of all authors and identifies one person as the Primary Contact. Put the submission date on the bottom of the title page. On a separate sheet, include the title and an abstract of 100 words or less. Do not include authors’ names on this sheet. A final page, “About the Authors,” should include a brief biographical sketch of 100 words or less on each author. Include current place of employment and degrees held. References must be written in APA style. It is the responsibility of the author(s) to ensure that the paper is thoroughly and accurately reviewed for spelling, grammar and referencing.

Review Procedure Authors will receive an acknowledgement by e-mail including a reference number shortly after receipt of the manuscript. All manuscripts within the general domain of the journal will be sent for at least two reviews, using a double blind format, from members of our Editorial Board or their designated reviewers. In the majority of cases, authors will be notified within 45 days of the result of the review. If reviewers recommend changes, authors will receive a copy of the reviews and a timetable for submitting revisions. Papers and disks will not be returned to authors. Accepted Manuscripts When a manuscript is accepted for publication, author(s) must provide format-ready copy of the manuscripts including all graphs, charts, and tables. Specific formatting instructions will be provided to accepted authors along with copyright information. Each author will receive two copies of the issue in which his or her article is published without charge. All articles printed by JAF are copyrighted by the Journal. Permission requests for reprints should be addressed to the Editor. Questions and submissions should be addressed to:

North American Business Press 301 Clematis Street, #3000

West Palm Beach, FL USA 33401 [email protected]

866-624-2458

Return Attribution: A Modified Bootstrapping Approach

John M. Geppert University of Nebraska- Lincoln

Donna M. Dudney

University of Nebraska- Lincoln

The return to an investment strategy results from the combined effect of three types of decisions: (1) which assets to consider (selection), (2) the proportion of wealth to allocate to each asset (allocation) and (3) when to rebalance the portfolio (rebalancing). In this paper, we develop an easy to implement, bootstrapping procedure which can disentangle the total ex-post investment return into its component parts. Rebalancing results in transactions cost that partially offset returns. Our procedure allows one to assess ex-post whether the additional cost of rebalancing is justified by higher returns. INTRODUCTION The question of whether markets price assets in an efficient manner is of primary importance in financial theory and has considerable implications for practitioners. While the exact definition of an “efficient” market may differ depending on the context, Fama (1991) organizes tests for market efficiency into three categories: 1) tests for return predictability, 2) event studies, and 3) tests for market responses to private information. Many tests of strategies designed to exploit possible market inefficiencies are based upon the application of a trading rule whereby investors buy or sell based upon some signal (e.g., a technical trading rule or earnings surprises). Often, the metric of a strategy’s success is simply whether it results in more accumulated wealth than some reference strategy. The reference strategy is typically the performance of some benchmark or likely investment alternative such as a risk-free asset or an unmanaged market index (see for example Andrade, Babenko and Tserlukevich, (2006)). Various return performance measures are reported, but often the emphasis is on total return with perhaps some risk adjustment. Alternately, profits from the trading strategy may be compared to profits from applying the same trading rule to data created using a bootstrapping procedure that simulates a random walk, AR(1), GARCH or similar return process (see for example Brock, Lakonisok and LeBaron, (1992); Osler and Chang, (1995); Marshall, Cahan, and Cahan, (2008); and Park and Irwin, (2008)). The bootstrap approach is an improvement over simple t-tests of differences in mean profits between a trading strategy and a strategy of buying and holding a benchmark asset. The t-test assumes normal, stationary and time independent distributions, whereas the bootstrap methodology allows modeling of a wide range of distributions that capture the leptokurtosis, autocorrelation, and conditional heteroskedasticity documented in stock market returns. Return differences between the trading strategy and a bootstrapped or benchmark strategy may be due to either investing in assets that differ from the benchmark (selection), investing in the same assets as

Journal of Accounting and Finance vol. 13(4) 2013 11

the benchmark but in different proportions (allocation) or shifting the composition of the assets in a manner different from the benchmark (rebalancing). Previous approaches do not allow decomposition of returns into these component parts. However, disentangling the impact on return of these three components provides insight into the economic value of the trading strategy. For example, if the majority of the strategy’s returns were derived from allocation and selection, then the rebalancing activity simply resulted in excessive transactions costs. This paper introduces a new procedure for measuring the performance of a wide range of investment strategies. Our bootstrap procedure allows ex-post returns from an investment strategy to be separated into rebalancing and allocation components. By holding constant the allocation decision, our approach ensures that benefits from allocation are not falsely attributed to rebalancing (timing) efforts1. Since many trading strategies (particularly technical trading rules), are essentially timing strategies, this separation is critical. Our approach is particularly useful in evaluating the performance of portfolio managers, and in determining whether efforts expended on portfolio rebalancing produce incremental returns in excess of the incremental costs. Our approach is described intuitively below, followed by an application of our technique to a trading rule based on Federal Reserve discount rate signals. EXPLANATION OF OUR APPROACH We consider the sources of return as selection, allocation and rebalancing. The allocation decision is simply the proportion of one’s wealth in each of the portfolio’s assets. For simplicity, we can subsume the selection decision into the allocation decision by defining the investment choice set as all conceivable assets and then assigning a portfolio weight of zero to those assets not selected. With this convention, any ex-post investment strategy can be decomposed into allocation and rebalancing decisions. This approach is illustrated in Figure 1.

FIGURE 1 DEFINING AN INVESTMENT STRATEGY

Time Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12

Stock Index Monthly Return 0.25% 0.42% 0.58% 0.33% -0.17% 0.08% 0.08% -0.17% -0.25% -0.25% 0.33% 0.42%Bond Index Monthly Return 0.08% 0.17% 0.08% 0.08% 0.08% 0.04% 0.08% 0.17% 0.08% 0.08% 0.08% 0.08%

INITIAL INVESTMENT STRATEGY

END OF MONTH BALANCE

The top panel gives the ex-post monthly returns from the stock and bond indices used in the investment strategy. The middle panel gives the allocation and rebalancing decisions that constitute the initial investment strategy. There are six “allocation/buy-and-hold” blocks A1-A6 and five rebalancing decisions. The bottom panel indicates the wealth accumulation resulting from the allocation and rebalancing decisions. Figure 1 shows an example investment strategy that spans twelve months and considers only stock and bond indices as possible assets. The top panel of Figure 1 shows the ex-post monthly returns from the stock and bond indices over the twelve month horizon considered. The middle panel shows the allocation

Time Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12Stock Index Proportion 0.8 0.75 0.8 0.75 0.85 0.6Bond Index Proportion 0.2 0.25 0.2 0.25 0.15 0.4

A1 A2 A3 A4 A5 A6

Time Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12Stock Account 0.8020$ 0.8053$ 0.8100$ 0.7606$ 0.7593$ 0.8106$ 0.7605$ 0.8605$ 0.8583$ 0.6050$ 0.6070$ 0.6095$ Bond Account 0.2002$ 0.2005$ 0.2007$ 0.2529$ 0.2531$ 0.2026$ 0.2535$ 0.1524$ 0.1525$ 0.4047$ 0.4050$ 0.4053$ Total Wealth 1.0022$ 1.0058$ 1.0107$ 1.0134$ 1.0124$ 1.0131$ 1.0140$ 1.0128$ 1.0108$ 1.0096$ 1.0120$ 1.0148$

12 Journal of Accounting and Finance vol. 13(4) 2013

and rebalancing decisions that constitute the initial investment strategy. The initial allocation decision is to apportion 80 percent of the investment into the stock index and 20 percent into the bond index (A1 in Figure 1). No further action is taken by the investor until the end of month three. Note that the portfolio weights in months two and three are likely to passively change as market values of the asset classes fluctuate. However, no active allocation changes are initiated by the investor during this period. This mimics a buy-and-hold strategy until the end of month three. Because it is common to think of buy-and-hold as “unmanaged,” we define the first three months to be one allocation decision, since after the initial allocation no action is taken by the investor. We call each string of non-trading a “buy-and-hold” block. At the end of month three, there is a rebalancing decision that downplays the stock index and rebalances toward bonds (A2 in Figure 1). The second rebalancing decision allocates 75 percent to stocks and 25 percent to bonds. This starts the second buy-and-hold block which remains through month five at which time the third rebalancing decision is made. The allocation and rebalancing continues through month twelve. Using this convention, Figure 1 shows that there are six active allocation decisions (six buy-and-hold blocks labeled A1 through A6) and five rebalancing decisions (A2 through A6). The pattern of allocation and rebalancing in Figure 1 fully characterizes the ex-post decisions used in our example investment strategy and the resulting return path. The wealth accumulation over the twelve month period is shown in the third panel of Figure 1 and is illustrated graphically in Figure 2.

FIGURE 2 INITIAL INVESTMENT STRATEGY WEALTH ACCUMULATION

Figure 2 shows the wealth accumulation from a one dollar investment in the initial investment strategy shown in Figure 1. The investment strategy shown in Figure 1 is just one of a large number of possible allocation and rebalancing strategies for a twelve month investment horizon with stock and bond indices. We want to compare it to other possible strategies that one might have taken over the same twelve month period. Each other alternative strategy would in general have resulted in a different cumulative twelve-month return. In addition, the source of each strategy’s return (from allocation or from rebalancing), would also differ. For the investment strategy illustrated in Figure 1, our objective is to isolate the returns derived from allocation from those derived from rebalancing by holding constant the impact of allocation decisions. We accomplish this by randomly shuffling the buy-and-hold allocation blocks, a process we refer to as a bootstrap shuffle.

$0.9900

$0.9950

$1.0000

$1.0050

$1.0100

$1.0150

$1.0200

Journal of Accounting and Finance vol. 13(4) 2013 13

To understand the intuition behind our shuffle process, we need to highlight when rebalancing affects returns. Profitable rebalancing is predicated on variation in asset return distributions. To see this, consider a world where the distribution of asset returns is fixed for all time. Also assume that an investor alternates between two possible investment allocations, A1 and A2 over a two month horizon. With fixed return distributions, the statistical properties of the two investment alternatives shown below would be identical, in spite of the different time periods associated with each allocation: PDF[(1 + Rt

A1)(1 + Rt+1A2)] = PDF[(1 + Rt

A2)(1 + Rt+1A1)], where PDF is the probability density function

of the associated accumulated wealth distributions. On the left-hand side of the equation the investor first invests with allocation A1 in period t and then rebalances to allocation A2 in period t+1. On the right-hand side, the time periods for allocations A1 and A2 are reversed. The ordering of the allocations is irrelevant when the return distributions are fixed; only the amount of time in each allocation is relevant, not when the allocations are implemented. It is important to note that the ex-post results for the two alternatives will not in general be the same - only the expected values and other statistical properties of the two strategies will be identical. Figure 3 illustrates the concept with our twelve-period example from Figure 1.

FIGURE 3 SHUFFLING ILLUSTRATION

The initial investment strategy consists of six allocation buy-and-hold blocks. The first block, A1, has an initial allocation of 80 percent of wealth to the stock index and 20 percent in the bond index. This buy-and-hold position remains through month three. The corresponding allocation buy-and-hold block in the alternative investment strategy is in month eleven. Because we are trying to separate the effects of rebalancing from allocation, the alternative investments we consider preserve the allocation proportions and buy-and-hold block lengths, but alter the timing of the rebalancing. We call these “allocation preserving strategies.” For ease of comparison, the top two panels of Figure 3 repeat the pattern of allocation and rebalancing of the initial investment strategy shown in Figure 1. In the third panel, we show one possible allocation preserving strategy alternative where the allocation decisions remain unaltered, while the location of the rebalancing decisions is changed. For example, the allocation decision A5, was located in month 8 in the Figure 1 strategy. For the alternative strategy, A5 has been moved to month 11. Similarly, the two month block labeled A2 in the Figure 1 strategy has been moved to month 8 in the alternative strategy. With a fixed

Initial Investment Strategy from Figure 1Time Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12

Stock Index Proportion 0.8 0.75 0.8 0.75 0.85 0.6Bond Index Proportion 0.2 0.25 0.2 0.25 0.15 0.4

A1 A2 A3 A4 A5 A6

Initial Investment Strategy End of Month BalanceTime Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12

Stock Account 0.8020$ 0.8053$ 0.8100$ 0.7606$ 0.7593$ 0.8106$ 0.7605$ 0.8605$ 0.8583$ 0.6050$ 0.6070$ 0.6095$ Bond Account 0.2002$ 0.2005$ 0.2007$ 0.2529$ 0.2531$ 0.2026$ 0.2535$ 0.1524$ 0.1525$ 0.4047$ 0.4050$ 0.4053$ Total Wealth 1.0022$ 1.0058$ 1.0107$ 1.0134$ 1.0124$ 1.0131$ 1.0140$ 1.0128$ 1.0108$ 1.0096$ 1.0120$ 1.0148$

Alternative StrategyTime Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12

Stock Index Proportion 0.6 0.8 0.8 0.75 0.75 0.85Bond Index Proportion 0.4 0.2 0.2 0.25 0.25 0.15

A6 A1 A3 A2 A4 A5

Alternative Strategy End of Month BalanceTime Line Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12

Stock Account 0.6015$ 0.6040$ 0.6075$ 0.8098$ 0.8084$ 0.8091$ 0.8097$ 0.7578$ 0.7559$ 0.7541$ 0.8596$ 0.8632$ Bond Account 0.4003$ 0.0401$ 0.4013$ 0.2019$ 0.2021$ 0.2022$ 0.2024$ 0.2535$ 0.2537$ 0.2539$ 0.1513$ 0.1514$ Total Wealth 1.0018$ 1.0050$ 1.0089$ 1.0117$ 1.0105$ 1.0113$ 1.0121$ 1.0113$ 1.0096$ 1.0079$ 1.0109$ 1.0146$

14 Journal of Accounting and Finance vol. 13(4) 2013

return distribution for stocks and bonds, the Figure 1 strategy and the alternative investment panel strategies would have the same twelve month cumulative distribution, however if the return distribution is not fixed, the timing of the allocation blocks will affect the cumulative wealth distribution. We use the term “shuffling” to describe how we reorder the buy-and-hold blocks to different time periods, while simultaneously preserving their length. It is important to note that we are not shuffling returns. In each month, the stock and bond returns used to calculate the twelve-month cumulative returns are the same for each investment strategy. What changes across strategies is the allocation to stocks and bonds in a particular month. Figure 4 shows how the accumulated wealth for the initial and alternative investment strategy differ over the twelve month horizon.

FIGURE 4 MONTHLY WEALTH ACCUMULATION OF INITIAL INVESTMENT STRATEGY AND ON POSSIBLE ALTERNATIVE ALLOCATION PRESERVING THE INVESTMENT STRATEGY

The figure shows two possible ex-post wealth accumulation paths derived from the ex-post stock and bond return series. Both investment alternatives consist of six buy-and-hold blocks with identical initial allocation proportions and investment lengths. The investment strategies differ only in the timing of rebalancing decisions. See Figure 3 for details on the initial allocations and block lengths. Because the allocation effects of the alternative investment strategy are identical to the initial investment strategy shown in Figure 1, the difference in accumulated wealth between the initial investment strategy and the alternative strategy must be due solely to the timing effect and not an allocation effect. This isolating consequence is the basis of the bootstrap shuffling approach. This approach is different from the bootstrapping procedure used by Brock, Lakonishok and LeBaron (1992) that generates a return series based upon an underlying return process such as a random walk, AR(1), or GARCH. Bootstrapping procedures generally do not assure that investors are in or out of the market for the same number of periods, and the bootstrapping procedures do not preserve the length of the allocation blocks. Because of this, standard bootstrapping procedures blur the distinction between allocation and timing effects and may falsely attribute excess returns to superior timing ability. The particular randomization of the allocation block shown in Figure 4 is just one of many. The bootstrap shuffle repeats this randomization a large number of times and records the distribution of wealth

Journal of Accounting and Finance vol. 13(4) 2013 15

across the various simulations.2 Figure 5 gives a hypothetical result of the shuffling process. To construct the 5th and 95th percentile bands, the buy-and-hold allocation blocks are randomly shuffled and accumulated wealth is calculated for each random shuffle. This process is repeated to generate a distribution of accumulated wealth values associated with alternative rebalancing (timing) decisions. Note that by construction, all of the alternate investment strategies have the same allocation decisions (i.e., all have the same number of allocation blocks of the same lengths), so any differences in wealth are a result of when the rebalancing occurred.

FIGURE 5 ACCUMULATED WEALTH OF INITIAL INVESTMENT STRATEGY VERSUS BOOTSTRAP

SHUFFLE DISTRIBUTION OF ACCUMULATED WEALTH

$0.7000 $0.7500 $0.8000 $0.8500 $0.9000 $0.9500 $1.0000 $1.0500 $1.1000 $1.1500

Initial InvestmentStrategy

95th Percentile ofBootstrap ShuffleDistribution

Median of BootstrapShuffle Distribution

5th Percentile ofBootstrap ShuffleDistribution

The bootstrap shuffle distribution of accumulated wealth was calculated by randomly shuffling the buy-and-hold allocation blocks shown in Figure 1. The accumulated wealth associated with each random shuffle is calculated using the monthly returns for the stock and bond indices shown in Figure 1. This process is repeated 1,000 times to generate the bootstrap shuffle distribution. The accumulated wealth value associated with the initial investment strategy from Figure 1 falls above the mean of the bootstrap distribution, but below the 95th percentile of the distribution. We interpret this to mean that, holding the allocation decisions constant, the profits from the particular rebalancing decisions made in the initial investment strategy are not statistically different from the profits associated with a random assignment of the rebalancing decisions. Consequently the rebalancing decisions in the initial investment strategy were not value adding and resulted in unnecessary transactions costs. To summarize, we can decompose the ex-post profits/returns from any investment strategy by breaking the profit/return sequence into allocation buy-and-hold blocks and rebalancing decisions. We generate an empirical distribution by shuffling the allocation decisions many times in such a way as to preserve the allocation decisions and holding period lengths. The 5th and 95th percentile bounds for this distribution give the confidence interval for the null that the initial investment strategy’s rebalancing decisions are superior to random rebalancing. The mean of this distribution gives the amount of the initial investment strategy’s accumulated wealth that derives from allocation. The difference between the initial investment strategy’s accumulated wealth and the mean of the distribution is attributed to rebalancing (timing). The bootstrap shuffle technique has broad applicability to many tests of market efficiency, including technical trading rules based on past price or volume patterns and trading rules based on public

16 Journal of Accounting and Finance vol. 13(4) 2013

information signals such as phases of the business cycle, the weak dollar/strong dollar cycle, or disclosures of officer and director trading activity. If a market efficiency test can be characterized by a change in portfolio composition based upon a signal, our method can be used to separate the ex-post return into allocation and rebalancing components. AN EMPIRICAL APPLICATION OF THE BOOTSTRAP SHUFFLE TECHNIQUE We illustrate our technique using a trading rule based on the monetary policy environment. Research by Johnson and Jensen (1998) and Conover, Jensen, Johnson and Mercer (2005) finds that periods of decreasing discount rates (an expansive monetary policy) are associated with higher stock market returns and lower variability of returns. This finding implies that investors should be able to earn superior returns by using monetary policy signals to time stock market purchases. Specifically, when monetary policy shifts from restrictive to expansionary, investors should shift from bonds into stocks, and conversely should shift from stocks into bonds when monetary policy shifts from expansionary to restrictive. We use our bootstrap shuffle technique to determine whether profits from this trading rule are attributable to timing or asset allocation. For our trading strategy we use the value weighted CRSP index cum-dividends as a proxy for a stock portfolio that mimics the market portfolio. We use the CRSP 30-year bond return for our bond portfolio. The data are monthly and run from October of 1957 to December of 2009. The timing strategy we examine is based on whether the monetary environment is expansive or restrictive as defined by Johnson and Jensen (1998) and Conover, Jensen, Johnson and Mercer (2005). In their definition, an expansionary period begins when the Federal Reserve Bank (Fed) lowers the discount rate and continues until the Fed raises the discount rate, at which point a restrictive period begins. The restrictive period lasts until the Fed again lowers the discount rate. If we code a restrictive monetary regime as 1 and an expansive regime as 0, we have a trading signal just as described in our original example. In the first monetary timing strategy, the investor starts with $1. At the beginning of each month he observes whether the monetary environment is expansive or restrictive. He then invests the dollar and any subsequent accumulated wealth in a stock portfolio if the monetary environment is expansionary and in a bond portfolio if the monetary environment is restrictive. In each subsequent month he switches his entire wealth between the stock and bond portfolio depending on the monetary environment. Figures 6 and 7 show the accumulated wealth from such a strategy and its resulting bootstrap attribution to timing and allocation.

Journal of Accounting and Finance vol. 13(4) 2013 17

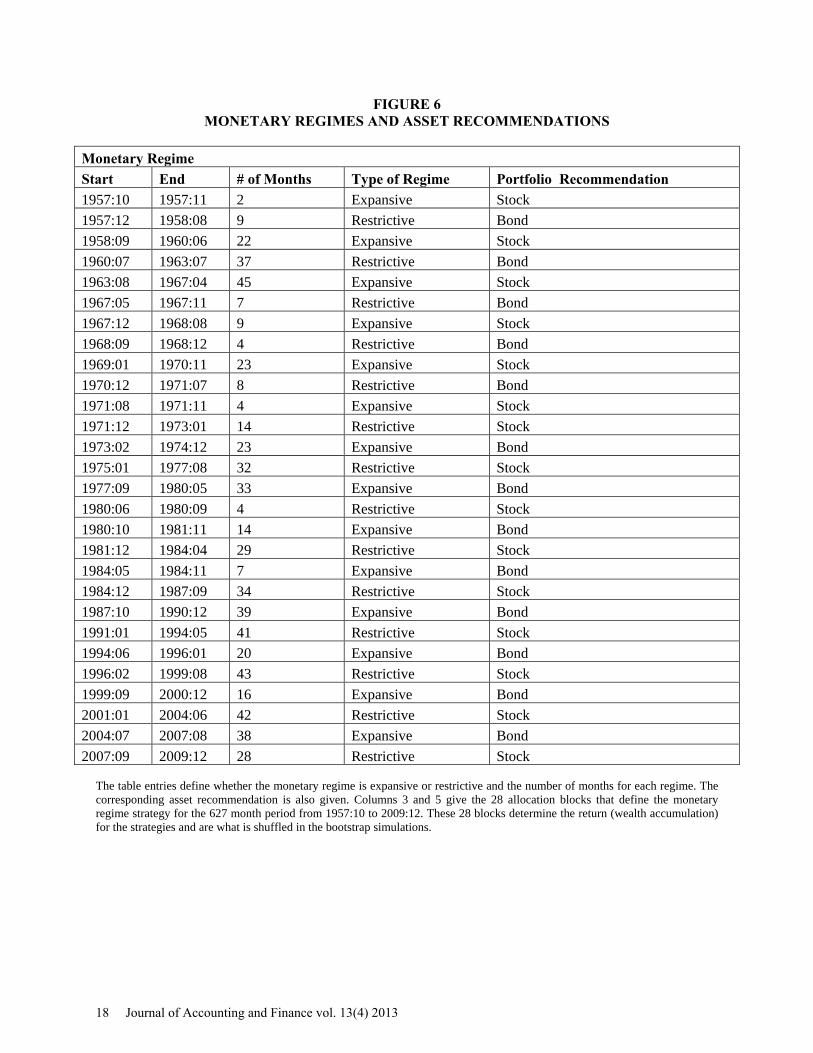

FIGURE 6 MONETARY REGIMES AND ASSET RECOMMENDATIONS

Monetary Regime Start End # of Months Type of Regime Portfolio Recommendation 1957:10 1957:11 2 Expansive Stock 1957:12 1958:08 9 Restrictive Bond 1958:09 1960:06 22 Expansive Stock 1960:07 1963:07 37 Restrictive Bond 1963:08 1967:04 45 Expansive Stock 1967:05 1967:11 7 Restrictive Bond 1967:12 1968:08 9 Expansive Stock 1968:09 1968:12 4 Restrictive Bond 1969:01 1970:11 23 Expansive Stock 1970:12 1971:07 8 Restrictive Bond 1971:08 1971:11 4 Expansive Stock 1971:12 1973:01 14 Restrictive Stock 1973:02 1974:12 23 Expansive Bond 1975:01 1977:08 32 Restrictive Stock 1977:09 1980:05 33 Expansive Bond 1980:06 1980:09 4 Restrictive Stock 1980:10 1981:11 14 Expansive Bond 1981:12 1984:04 29 Restrictive Stock 1984:05 1984:11 7 Expansive Bond 1984:12 1987:09 34 Restrictive Stock 1987:10 1990:12 39 Expansive Bond 1991:01 1994:05 41 Restrictive Stock 1994:06 1996:01 20 Expansive Bond 1996:02 1999:08 43 Restrictive Stock 1999:09 2000:12 16 Expansive Bond 2001:01 2004:06 42 Restrictive Stock 2004:07 2007:08 38 Expansive Bond 2007:09 2009:12 28 Restrictive Stock

The table entries define whether the monetary regime is expansive or restrictive and the number of months for each regime. The corresponding asset recommendation is also given. Columns 3 and 5 give the 28 allocation blocks that define the monetary regime strategy for the 627 month period from 1957:10 to 2009:12. These 28 blocks determine the return (wealth accumulation) for the strategies and are what is shuffled in the bootstrap simulations.

18 Journal of Accounting and Finance vol. 13(4) 2013

FIGURE 7 ATTRIBUTING WEALTH ACCUMULATION TO TIMING OR ALLOCATION

The table gives the accumulated wealth from following the monetary timing rule and a stock only buy-and-hold strategy. In addition, the 5th and 95th percentiles for accumulated wealth are given for a bootstrap simulation that preserves the allocation of the timing strategy. If the timing strategy accumulated wealth falls within the 5th to 95th bounds, the timing strategy is not statistically different from a random strategy with the same allocation blocks. Statistically significant timing results are shaded. The mean of the bootstrap distribution gives the expected wealth accumulation for the strategy allocation blocks. The difference between the actual strategy accumulated wealth and the average is the dollar return attributed to timing. Accumulated wealth for various sub-periods is shown for holding periods of 60, 120 and 180 months. Figure 6 shows 627 months of the “signal” for the monetary regime timing strategy. The Fed alters its posture between restrictive and expansive over this 52-year period in durations from 2 to 45 months as shown. For example, with a 10 year (120-month) horizon beginning in 1957:10, the trading strategy would have recommended an initial allocation of $1 into the stock portfolio. The funds would remain there for two months at which time the Fed would have altered its posture from expansive to restrictive and the investor would rebalance his initial $1 investment and proceeds to the bond portfolio. The funds would remain in the bond portfolio for 9 months and then get rebalanced back into stocks. The process

Mean Accumulated Wealth Bootstrap

Accumulated Wealth from a Buy-and-Hold 5th Percentile 95th Percentile (Allocation Timing Holding Period Number of Months from Trading Strategy Stock Only Strategy Bootstrap Bootstrap Effect) Effect

1957:10 - 1962:09 60 $1.32 $1.65 $1.02 $1.58 $1.31 0.01 $ 1957:10 - 1969:09 120 $2.04 $3.45 $1.60 $2.57 $2.05 (0.01) $ 1957:10 - 1972:09 180 $3.49 $4.54 $1.67 $3.80 $2.67 0.82 $

1962:10 - 1967:09 60 $1.54 $2.09 $1.40 $1.70 $1.52 0.02 $ 1962:10 - 1972:09 120 $2.64 $2.75 $1.47 $2.70 $2.10 0.54 $ 1962:10 - 1977:09 180 $5.29 $2.88 $1.54 $4.83 $2.94 2.34 $

1967:10 - 1972:09 60 $1.76 $1.35 $0.94 $1.84 $1.38 0.38 $ 1967:10 - 1977:09 120 $3.53 $1.41 $1.30 $3.33 $2.11 1.41 $ 1967:10 - 1982:09 180 $6.02 $2.49 $1.63 $4.89 $2.96 3.06 $

1972:10 - 1977:09 60 $1.99 $1.04 $1.24 $2.08 $1.78 0.21 $ 1972:10 - 1982:09 120 $3.39 $1.81 $1.27 $3.23 $2.22 1.17 $ 1972:10 - 1987:09 180 $10.43 $5.72 $2.60 $7.44 $4.77 5.65 $

1977:10 - 1982:09 60 $1.70 $1.84 $1.39 $2.07 $1.74 (0.04) $ 1977:10 - 1987:09 120 $5.22 $5.58 $3.00 $5.56 $4.28 0.94 $ 1977:10 - 1992:09 180 $8.91 $8.28 $3.76 $6.97 $5.23 3.68 $

1982:10 - 1987:09 60 $2.75 $2.71 $2.22 $2.75 $2.40 0.34 $ 1982:10 - 1992:09 120 $4.69 $4.03 $2.30 $3.81 $2.95 1.74 $ 1982:10 - 1997:09 180 $9.04 $10.11 $4.34 $8.61 $6.15 2.88 $

1987:10 - 1992:09 60 $1.70 $1.92 $1.64 $1.70 $1.67 0.02 $ 1987:10 - 1997:09 120 $3.27 $4.81 $2.08 $3.81 $3.00 0.27 $ 1987:10 - 2002:09 180 $3.03 $4.31 $1.83 $5.99 $3.49 (0.46) $

1992:10 - 1997:09 60 $1.91 $2.48 $1.78 $2.25 $1.98 (0.07) $ 1992:10 - 2002:09 120 $1.77 $2.22 $1.29 $3.62 $2.21 (0.44) $ 1992:10 - 2007:09 180 $3.09 $4.98 $2.15 $4.78 $3.03 0.06 $

1997:10 - 2002:09 60 $0.96 $0.93 $0.74 $1.40 $1.06 (0.10) $ 1997:10 - 2007:09 120 $1.68 $2.08 $1.14 $2.04 $1.40 0.28 $ 1997:10 - 2009:09 147 $1.25 $1.64 $0.89 $3.17 $1.59 (0.34) $

Journal of Accounting and Finance vol. 13(4) 2013 19

would continue until 1967:09. Figure 7 gives the accumulated wealth for the trading positions in Figure 6. Accumulated wealth is calculated for holding periods of 5 years (60 months), 10 years (120 months) and 15 years (180 months) for various data sub-periods. As seen in row 2 of Figure 7, from 1957:10 to 1969:09 the strategy of rebalancing wealth between a stock portfolio in expansive monetary regimes and a bond portfolio in restrictive regimes would have accumulated $2.04 for every dollar invested. Randomly shuffling the six trading blocks associated with the 120 month horizon in Table 7 results in 5th and 95th percentile values of $1.60 and $2.57 respectively. Because the realized wealth accumulation of $2.04 lies within these bounds, we can conclude that with this horizon and over this time period, the monetary regime timing strategy is not statistically different from a random timing strategy with the same allocation blocks. The mean bootstrap value indicates that the allocation blocks given by the 120 month monetary regime timing strategy would be expected to earn $2.05, which is close to the $2.04 actually earned. This implies that the realized strategy’s earnings are substantially due to allocation and not timing. Finally, we see that a simple buy-and-hold stock investment would have earned $3.45 over the same investment horizon. Statistically significant timing results are shown by the shaded cells in Figure 7. The monetary regime timing strategy generally fares better for longer investment horizons and also for time periods beginning in the late 1960’s to the mid 1980’s. For example, following the trading strategy of rebalancing wealth between a stock portfolio in expansive monetary regimes and a bond portfolio in restrictive regimes for the 180-month holding period beginning 1982:10 and ending 1997:09 would have accumulated $9.04 for every dollar invested. This is well outside the 5th and 95th percentile bounds of $4.35 and $8.61 calculated by applying the block shuffling procedure. The expected wealth accumulation from the bootstrapped block shuffling strategy is $6.15. As a result, for this period and investment horizon, the timing implied by the monetary regime adds an additional $2.88 to the wealth accumulation for every dollar invested. The trading strategy has been less successful for the most recent sub-periods beginning in the late 1980’s and thereafter as the accumulated wealth from the trading strategy in these periods is generally well below the mean of the bootstrapped distributions. For comparative purposes, the accumulated wealth from a stock-only buy-and-hold strategy is also shown in Figure 7. This comparison highlights the dangers of confounding the effects of allocation and timing decisions on returns. To see this, consider the 60-month holding period from 1972:10 to 1977:09. The accumulated wealth from the trading strategy for this period was $1.99 per $1.00 invested. This is substantially higher than the $1.04 accumulated wealth from a buy-and-hold investment in the stock index. However, the $1.99 in accumulated wealth from the trading strategy is below the 95th percentile of the bootstrap shuffle distribution of $2.08 and is only slightly above the mean of the bootstrap shuffle distribution of $1.78. In this case, the superior performance of the trading strategy was due to allocation, not timing effects, yet a comparison to the buy-and-hold result would have falsely presumed that the trading rule was a successful strategy for timing investments. INCORPORATING TRANSACTIONS COSTS Figure 7 shows that a monetary regime timing strategy generated statistically significant timing returns in several sub-periods of the data set. However, the rebalancing from stocks to bonds was done disregarding transactions costs which would certainly be present. In addition, the presence of transactions costs biases the choice of investment strategy toward buy-and-hold since buy-and-hold incurs only the initial investing and liquidation fees. Figure 8 repeats the investment strategy shown in Figure 7, but each time the portfolio switches from stocks to bonds or from bonds to stocks, the accumulated wealth is reduced by 2 percent as a transactions fee. The transaction fee is also incorporated into the bootstrapping 5th and 95th percentiles and the bootstrap mean to make a fair comparison. While the dollar amounts in Figure 8 are necessarily lower than those in Figure 7, we see that the pattern of statistically significant timing returns is persistent even with a 2 percent transactions cost for 6 of the 8 sub-periods identified in Table 7.

20 Journal of Accounting and Finance vol. 13(4) 2013

FIGURE 8 ATTRIBUTION WEALTH ACCUMULATION TO TIMING OF ALLOCATION

2 PERCENT REBALANCING COSTS

The table shows the effect of a 2 percent rebalancing cost for the trades in Figure 7 that were statistically significant assuming zero transactions costs. The table figures show the accumulated wealth starting from a $1 investment at the beginning date and following a rebalancing strategy based on the monetary regime, either expansive or restrictive. In a given month if the monetary regime is expansive, the portfolio is invested in the CRSP value-weighted portfolio. If the monetary regime is restrictive, the portfolio is invested in a 30-year Treasury bond portfolio. The entire accumulated wealth is switched from the stock to bond portfolio with each change in monetary regime. For comparison, the 5th and 95th percentiles give the accumulated values of rebalancing in a random fashion that exactly mimics the percentage of time the funds are in the stock and bond portfolios given by the strategy, but “shuffles” the timing. In this way allocation decisions are preserved and the only difference is timing. Shaded cells indicate a statistically significant timing strategy. Six of the eight significant trading periods remain significant even with a 2 percent rebalancing cost. CONCLUSION Standard tests of trading strategies designed to exploit market inefficiencies typically compare the profits from implementation of the trading strategy to profits from a buy and hold strategy or a reference strategy calculated using bootstrapping techniques. Higher profits for the trading strategy are attributed to timing, but may in fact be caused by asset allocation differences between the trading strategy and the reference strategy. We propose a modification of the bootstrapping simulation technique that allows a decomposition of trading profit into allocation and timing components. This approach holds constant the allocation decision by ensuring that the reference strategy incorporates the same allocation decisions as the timing strategy (both in terms of the total length of time in the market and the length of each allocation block). The decomposition technique is illustrated using a monetary policy timing strategy, however, the approach can be applied to a wide variety of trading strategies based on technical trading rules or trading rules designed to exploit semi-strong form market inefficiencies. Use of this technique allows a more accurate measurement of the true profit to these trading strategies, and allows portfolio managers to determine whether efforts expended on rebalancing (timing) activities are justified by higher portfolio returns. ENDNOTES

1. Our use of the term “timing” indicates a rebalancing event triggered by some observed signal. 2. In the actual applications of our technique, we repeat the bootstrapping 1,000 times.

Mean Accumulated Wealth Bootstrap

Accumulated Wealth from a Buy-and-Hold 5th Percentile 95th Percentile (Allocation Timing Holding Period Number of Months from Trading Strategy Stock Only Strategy Bootstrap Bootstrap Effect) Effect

1962:10 - 1977:09 180 $4.23 $2.88 $1.39 $4.05 $2.56 1.68 $

1967:10 - 1977:09 120 $2.94 $1.41 $1.18 $3.01 $1.87 1.07 $ 1967:10 - 1982:09 180 $4.63 $2.49 $1.37 $4.20 $2.55 2.08 $

1972:10 - 1982:09 120 $2.94 $1.81 $1.19 $2.94 $2.03 0.91 $ 1972:10 - 1987:09 180 $8.69 $5.72 $2.30 $6.85 $4.29 4.40 $

1977:10 - 1992:09 180 $7.58 $8.28 $3.33 $6.35 $4.73 2.85 $

1982:10 - 1992:09 120 $4.24 $4.03 $2.12 $3.59 $2.75 1.49 $ 1982:10 - 1997:09 180 $7.84 $10.11 $3.88 $8.10 $5.64 2.21 $

Journal of Accounting and Finance vol. 13(4) 2013 21

REFERENCES Andrade, S., Babenko, I., Tserlukevich, Y. (2006). Market timing with CAY: Using deviation from the long-run aggregate log consumption-wealth ratio. Journal of Portfolio Management 32, 70-80. Brock, W., Lakonishok J., LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. Journal of Finance 47, 1731-1764. Conover, C. M., Jensen G., Johnson R., Mercer J. (2005). Is Fed policy still relevant for investors? Financial Analysts Journal 61, 70-79. Fama, E. (1991). Efficient capital markets II. Journal of Finance 46, 1575-1617 Johnson, R., Jensen, G. (1998). Stocks, bonds, bills and monetary policy. Journal of Investing 7, 30-37. Marshall, B., Cahan, R. Cahan, J. (2008). Does intraday technical analysis in the U.S. equity market have value? Journal of Empirical Finance 15, 199-210. Osler, C.L., Chang, P.H. K. (1995). Head and shoulders: Not just a flaky pattern. Federal Reserve Bank of New York Staff Report No. 4, 1-67. Available at SSRN: http://ssrn.com/abstract=993938. Park, C., Irwin, S. (2008). The profitability of technical trading rules in U.S. futures markets: A data snooping free test,” SSRN Working Paper available at SSRN: http://ssrn.com/abstract=722264

22 Journal of Accounting and Finance vol. 13(4) 2013

Exploring the Cognitive Effects of Persuasive Messaging on Students’ Perceptions about Accounting

Joseph C. Ugrin

Kansas State University

Darla Honn University of Central Missouri

Heber Garcia

Kansas State University

Richard L. Ott Kansas State University

One reason students do not major in accounting is the perception that accounting is dull and boring. Through the lens of media richness theory, this study explores how perceptions can be changed by promotional media. The results show that promotional media aimed at perception change can influence perceptions about accounting if the message is presented with rich media that incorporates auditory and visual stimuli. Positive changes in perception occurred through an affective response which influenced perception directly, and influenced perception indirectly through increased involvement with the details of the message. The results of the study offer theoretical and practical contributions. INTRODUCTION

Students’ general perceptions about the accounting profession are a significant factor in their decision to select accounting as a major (Simons, Lowe and Stout, 2003). Unfortunately, the majority of prospective students harbor negative perceptions about accounting and these negative perceptions are an impediment to the recruitment of students into the accounting profession (Taylor, 2000). In recent years, the academic and professional communities have become increasingly concerned about the impact of student perceptions on recruitment, particularly in light of expected supply and demand changes in the job market (Pathways, 2012).

The Bureau of Labor Statistics predicts employment growth for accountants and auditors will be higher than average through 2008-2018 (BLS, 2010), while at the same time, over 75% of accounting professionals are expected to reach retirement in the next 15 years (Trabulsi, 2008). Unfortunately, there are indications that fewer new accounting graduates will be available to fill those vacancies. Although current enrollments in collegiate accounting programs are at record high levels, the Department of Education projects that overall high school enrollments will decline in the next decade (Hussar, 2011).

Journal of Accounting and Finance vol. 13(4) 2013 23

These projections suggest that accounting will be challenged to compete with other professions for the diminishing supply of high school graduates while trying to satisfy an increasing demand for entry level accountants.

It is clear that effective recruitment is critical to the future of the accounting profession and students’ perceptions are an important ingredient in recruitment success. However, literature suggests that prospective students’ perceptions about accounting are generally negative (e.g. Simons, Lowe, and Stout, 2003), and targeted recruitment efforts have little impact on reversing the makeup of accounting students and their preferences (Kovar et al., 2003). These findings are clearly impediments to successful recruitment, yet there has been little research to determine what can be done to effectively change students’ perceptions. Currently, there is no framework in the accounting literature which explains how persuasive messaging can be used to induce perception change. This void in the literature provides the motivation for the current study.

The current study applies theories from the literature on persuasive messaging and cognitive processing that have not previously been used in the context of understanding students’ perceptions of accounting. These theories suggest that the extent to which a persuasive message changes perception largely depends on the richness of the media (Daft and Lengle, 1986, 1987), the affective response induced by the message (Petty et al., 1981; Forgas, 1995), and the individual’s level of cognitive involvement in the message (Petty et al., 1983). The current research extends existing accounting literature by developing a model that explains the cognitive processes that underlie successful persuasive messaging. This model can be used by the profession to design recruitment strategies that are more effective in changing students’ negative perceptions of accounting.

The professional accounting community has been keenly aware of the difficulties involved with recruiting top talent into the field. In response, over the last two decades the American Institute of Certified Public Accountants (AICPA) has invested considerable resources into endeavors aimed at attracting students through use of advertising campaigns comprised of brochures, videos, and online media. The AICPA’s current recruiting effort is the Start Here Go Places initiative, a campaign designed to positively influence prospective students’ perceptions of the accounting profession and increase the number of students majoring in accounting and ultimately pursuing CPA certification. The nucleus of Start Here Go Places is an interactive website that rebukes the stereotype that accounting profession is dull and repetitive, and highlights the challenging and rewarding opportunities available to accounting professionals.

The AICPA has described the Start Here Go Places campaign as highly successful overall (AICPA, 2010), and the website is the most innovative, large scale persuasive messaging tool used to date in the context of student recruitment. Yet, existing literature provides no empirical evidence of the effectiveness of persuasive messaging used in the website. Thus, the website and the content within it provide an ideal platform to test the model presented in this study, and the results provide practical feedback to the developers of the Start Here Go Places campaign.

In an experimental analysis, 87 non-accounting college students were randomly exposed to persuasive content from the Start Here Go Places website in one-way communication exchanges (e.g., the students received communication, the students did not offer return communication) under four different audio/visual treatment conditions. Pre and post-tests of students’ perceptions of accounting were collected and the findings show that the message within the Start Here Go Places website can change students’ perceptions about accounting, but the effect is highly contingent on the mode in which the message is presented and the affective response the message creates. Perception change occurred when media rich presentations of the web content included both auditory and visual components of communication. The presence of richer media induced a stronger affective response which influenced students’ perceptions directly and indirectly by increasing the students’ involvement with the message.

The current study makes important theoretical and practical contributions. It introduces a theoretical framework that explains the cognitive processes through which perception change occurs, and it tests that framework using content from the accounting professions’ most significant investment in student

24 Journal of Accounting and Finance vol. 13(4) 2013

recruitment, the Start Here Go Places website. The outcomes of the current research can be used by the accounting profession to improve the efficacy of persuasive messaging within its recruitment campaigns.

The remainder of the paper begins with a review of the literature and development of the hypotheses. The research design is presented and results from the hypotheses testing are reported. The paper concludes with a discussion of the results and their implications for the accounting profession. BACKGROUND AND HYPOTHESES DEVELOPMENT

A large body of accounting literature directed toward understanding students’ choice of accounting as a major has emerged over the last two decades (see Simons et al., 2003), and a significant factor that has received considerable attention is potential students’ (mis)perceptions of the accounting field. The literature suggests that students’ (mis)perceptions about accounting, and the nature of accounting work, make it difficult to recruit top talent into the field (Albrecht and Sack, 2000; Kreiser, McKeon, and Post, 1990; Nouri, Parker, and Sumanta, 2005; Simons, Lowe, and Stout, 2003). Prospective students typically perceive accountants’ work as boring, tedious and monotonous “number-crunching” and they often believe the profession offers a work environment that is orderly and predictable (Taylor, 2000). Research also shows it is difficult to reverse students’ preferences. For example, over an eight-year period, Kovar et al (2003), implemented targeted recruitment efforts designed to change student’s personality preferences. They found, however, that the recruitment efforts did not result in attracting a more diverse student population which they attribute, in part, to negative mis-perceptions of the accounting profession.

Other studies on student perceptions of accounting show that students are more likely to major in accounting when they perceive the field to be interesting (Seamann and Crooker, 1999; Taylor, 2000). This conclusion continues to be supported by more recent literature (e.g. Byrne and Willis, 2005; Sugahara, Boland, and Cilloni, 2008), including a study by Allen (2004) that found that the primary benefit students found in majoring in a field other than accounting was that other fields are not as boring. Although prior research has established that students’ perceptions of accounting tend to be generally negative, none of these studies have explained why even targeted recruitment strategies seem to have little success in changing those perceptions.

Although there has been little research on perception change in the accounting literature, the AICPA been proactive in its efforts to influence perceptions since the early 1990s. Their efforts have evolved through a number of iterations to the current version, the Start Here Go Places campaign. The showcase of the current campaign is a website designed to appeal to a web-savvy generation of prospective students. In a one-way exchange of information, the website allows students to point and click through a visually based media presentation which highlights the positive aspects of various accounting careers. Even though the visual information is specifically designed to portray accounting work as interesting, exciting and non-repetitive, preliminary survey results suggest the website’s message may have limited persuasive appeal1. A possible explanation can be found using theories from the communications and cognitive psychology literature. Using Media to Change Perceptions: A Theoretical Model

Media Richness Theory (MRT) provides a basis for understanding how various modes of communication influence perceptions differently. MRT is one of the most widely used theories for explaining the effects of communication media (Kinney, Watson, and El-Shinnawy, 1998). The theory was originally used to explain traditional forms of media, but continues to be widely accepted as researchers have found it applicable to newer forms of communication including websites (e.g. Brunelle, 2009). According to the hierarchy of media richness by Daft et al. (1987), general face-to-face verbal communication provides the richest communication, with written documents such as bulletins, fliers, and standard reports providing the lowest. Based on MRT and the hierarchy of media richness within it, computer-based communication mediums like websites should provide minimal communication quality if they are purely visual and lack a more rich combination of auditory and visual stimuli.

Journal of Accounting and Finance vol. 13(4) 2013 25

MRT suggests that less rich media are relatively less effective than more rich media at conveying a persuasive message because less rich media create ambiguity and confusion about what the message intends to convey (Daft and Lengle, 1986; Daft et al., 1987). Similarly, the research on web-based media shows that websites with richer media are more appealing to users and more effective at persuading individuals to purchase a product (Sewak et al., 2005; Brunelle, 2009). From a practical perspective, making the Start Here Go Places message available online may increase students’ motivation to view the information, but the richness of media used to convey the online message will determine its degree of persuasiveness. In its current form, the website contains only text and still photos, which ranks the persuasive message near the bottom of the MRT hierarchy. The same message delivered with audio and video components, similar to a face-to-face delivery would rank the message higher on the MRT hierarchy, increasing its persuasiveness.

H1: The effectiveness of the persuasive message in changing students’ perceptions about accounting varies directly with the media richness.

According to MRT, using more rich media in online persuasive messaging will increase the

likelihood that the information presented will induce a positive change in students’ perceptions about accounting. However, this knowledge alone does not completely explain why researchers have found it so difficult to influence students’ perceptions about accounting. A more comprehensive approach requires also understanding the cognitive processes that underlie students’ evaluation of persuasive messages. A clear model of these processes will help developers improve the efficacy of persuasive messaging, regardless of type of media used to deliver the message. Affective Response

Individuals’ emotions, or affective responses, play an important role in the cognitive processing of a persuasive message, particularly when individuals are not motivated to process the persuasive message (Petty, Desteno, and Rucker, 2001). Since the majority of the potential student population harbor negative perceptions about accounting, they are highly susceptible to implications of affect as they cognitively process messages aimed at inducing perception change. According to Forgas’ (1995) Affect Infusion Model, the impact of affect on decision making becomes amplified in complex situations that demand substantial cognitive processing. In cases where information is lacking, the affective response to the available information, rather than details within the information, can strongly influence an individual’s attitude and perception. This would suggest that the degree of richness of the media used to deliver a persuasive message has a direct link to the intensity and nature (positive vs. negative) of affect induced.

Recall that under MRT, communication levels and richness vary across different delivery mediums. Face-to-face verbal communication provides the highest communication richness while other mediums, such as text based messages, provide comparatively lower communication richness. As the richness of communication decreases within the hierarchy, informational cues become more ambiguous and confusing. As a result, the recipient is more likely to experience cognitive overload. Cognitive overload can be induced by the structure and design of the informational delivery system (Rose, 2002; Rose and Wolfe, 2000) and although most research shows that too much information induces overload, other literature suggests overload can also be induced by too little information. When presented with low quality information, individuals tend to search for missing informational cues, amplifying the extraneous portion of cognitive overload. By contrast, media that include both auditory and visual components can reduce overload (Leahy, Chandler, and Sweller, 2003; Mousavi, Low, and Sweller, 1995). Cognitive overload makes it difficult to focus on the important details of the message and induces a negative affective response (Bohner, Shaiken, and Piroska, 2006; Barta and Stephens, 1994). Thus, it is proposed that the richness of media used to deliver a persuasive message will contribute to the positive or negative nature of an individual’s affective response.

H2: Affective response varies directly with media richness.

26 Journal of Accounting and Finance vol. 13(4) 2013

It is clear that a student’s affective response to a persuasive message is largely determined by the richness of media used to deliver the message. However, a complete model of perceptional change must also consider the conditions under which affective response actually induces a change in perception. Theories suggest affective response induced by a persuasive message has both a direct and an indirect influence on perceptional change, depending upon the individual’s level of involvement with the message. The Relationship between Affect and Perception Change

A model of perceptional change must also consider how affective response induces a change in perception. Theories suggest that affective responses induced by persuasive messages have both a direct and indirect influence on perceptional change. The direct influence is a “peripheral route” where external cues surrounding the message, such as music or background, shape attitudes and perceptions (Petty et al., 1983). In the peripheral route, affective response directly influences perception change, at the subconscious level, without requiring the individual to become actively involved with the details of the message.

H3: Participants’ perceptions of accounting vary directly with their affective response.

In addition to a direct relationship between affect and perception change, research indicates there is also an indirect path that is a function of how deeply recipients consider the arguments presented to them. According to the cognitive response approach to persuasion (e.g., Petty, Ostrom, and Brock, 1981), a persuasive message is one that motivates a receiver to carefully consider the content of an idea or argument and analytically reason through it, and this involvement is piqued by the individual’s emotional response to the message. Petty, Cacioppo, and Schumann (1983), describe this as the “central route” to attitude change; a state in which attitude change is a reaction to a persuasive message and a function of cognitive responses to external information, justification, comprehension, and preexisting beliefs. Others also note that this type of persuasion occurs through attention, involvement, and assimilation of information (Johnson and Eagly, 1989; Buck et al., 2004). An individual is more likely to become involved with a message when the message has “greater personal relevance and consequences or elicits more personal connections” (Petty et al., 1983, pg. 136)

As individuals become more involved with a persuasive message, they tend to pay more attention to the details within the message. In a high-involvement state, persuasion occurs through a “central route” where the informational cues (e.g. details) within the persuasive message are more salient and influential in shaping attitudes (Petty et al., 1983). In the “central route,” emotional response indirectly influences perception change, but only to the extent the individual becomes actively involved in the processing details of the message. Therefore, in persuasive messaging, involvement works as a mediating factor in the relationship between affective response and perceptional change.

H4: Students’ level of involvement with the persuasive message will determine the extent to which affective response influences their perceptions of accounting.

The hypothesized relationships are presented in Figure 1.

Journal of Accounting and Finance vol. 13(4) 2013 27

FIGURE 1 HYPOTHESIZED MODEL

METHODOLOGY Participants

The sample was comprised of 87 college students who were not intending to major in accounting. Non-accounting college students are appropriate participants for several reasons. First, most students that major in accounting do not decide on the major until they reach the university (Mauldin, Crain, and Mounce, 2000; Geiger and Ogilby, 2000). Second, the objective is to influence the perceptions of and recruit students who are intending to choose majors other than accounting. Finally, the baseline perceptions of these participants are less likely to be biased by an existing interest in the profession and all of students in our sample indicated they did not have a preexisting interest in accounting. The participants’ primary academic interests represented a wide range of majors including engineering, pre-medicine, textile design, and education. Demographic information is presented in Table 1. Experimental Procedures and Variables

Prior to starting the experimental task, each participant completed a questionnaire designed to capture his or her perceptions about the accounting profession (hereafter PRE_PERCEPT). Perceptions were measured using a composite of four questions taken from a 36-item seven-point, likert-scaled instrument originally introduced by Seamann and Crooker (1999). The instrument has been widely used in the accounting literature to measure perception (e.g. Byrne and Willis, 2005; Sugahara et al., 2008). The four questions used from the instrument measure the degree to which individuals perceive the accounting profession to be interesting; these scales have also been shown to correlate with an individual’s tendency to major in accounting (Seamann and Crooker, 1999). The Cronbach alpha values for the four items measuring perception were .766 for PRE_PERCEPT.

For the experimental task, participants were randomly assigned to one of four treatment groups with low (1) to high (4) richness of media (hereafter TREATMENTS): 1) Self-Directed Group; 2) Website Group; 3) Multi-Media Group; 4) Face-to-Face Group. All four treatments were administered in controlled group settings and required approximately 40 minutes to complete. Participants in the Self-Directed Group used the Start Here Go Places website, without guidance. Treatment groups 2, 3 and 4 were exposed only to specific pages of the Start Here Go Places website which focused directly on persuasive reasons for choosing a career in accounting2. Participants in the Website Group viewed the specific pages, as prompted by written instructions, by clicking through the presentation and reading the on-screen text3. The Multi-Media treatment group viewed the specific website pages in an online video format. In the video presentation, visuals of the specific website pages were incorporated into a PowerPoint presentation narrated by an actual accounting professional who could be seen in a box on the screen. The Face-to-Face group viewed/listened to the exact same information as the Multi-Media group, except the PowerPoint was delivered in-person by the accounting professional. To eliminate potential presenter bias, the same presenter was used for the Multi-Media and Face-to-Face groups, and the presenter did not interact with the Face-to-Face participants during the PowerPoint presentation (see Appendix E for an example PowerPoint Slide and Appendix F for an example screenshot of the

Involvement with the message (INVOLVEMENT)

Affective Response (AFFECT)

Message Presentations (TREATMENT)

Change in Perception (PERCEPTDIF)

28 Journal of Accounting and Finance vol. 13(4) 2013

multimedia presentation). As a manipulation control, participants in groups two, three and four completed a 23-item quiz (hereafter QUIZ) which asked about the content of the specific website pages.

Immediately following the experimental task, the perception scale was administered as a post-test (hereafter POST_PERCEPT). The Chronbach alpha for POST_PERCEPT was .828 indicating reliability. A difference between participants’ PRE_PERCEPT and POST_PERCEPT was computed (hereafter PERCEPT_DIF). Participants then completed questions related to their affective response (hereafter AFFECT) and their level of involvement with the details of the presentation (hereafter INVOLVEMENT). AFFECT was measured using composite of three seven-point likert type scale items introduced by Kim, Allen, and Kardes (1996) (Appendix B). INVOLVEMENT was measured using composite of five seven-point likert type scale questions introduced by Laczniak, Muehling, and Grossbart (1989) (Appendix C). The Cronbach alpha was calculated for AFFECT and INVOLVEMENT and the alpha values were .897 and .907 respectively, indicating both are reliable measures of their respective underlying constructs.

Data for a number of other factors was also collected to control for possible bias. Prior research has shown that an individual’s relationship with someone in the accounting profession can influence their choice of accounting as a major (Leppel, Williams, and Waldauer, 2001), and by extension influence their perception of accounting. Therefore, participants were also asked, with dichotomous (yes/no) questions, whether they personally know an accountant (hereafter KNOWACCT) and whether they have accountants in their family (hereafter ACCTFAMILY). Finally, additional demographic variables including GENDER, AGE, ETHNICITY and MAJOR were reported by the participants.

TABLE 1 DESCRIPTIVE STATISTICS BY TREATMENT CONDITION

Self-Directed Website (n = 22)

Directed Website

(n = 21)

Multimedia Presentation

(Online Video) (n = 23)

Face-to-Face Presentation (PowerPoint)

(n = 21)

Overall

(n = 87)

Group Diff(e)