johnathon davis – proactive advisor magazine – volume 6, issue 2

TRANSCRIPT

April 9, 2015 | Volume 6 | Issue 2

Active investment management’s weekly magazine

Will weak jobs numbersdelay Fed rate hike?

9 types ofultra-HNWclients

Building a “niche” into a practice focus

Do you have too much invested in U.S. stocks?

Johnathon Davis

Kentucky blue is seeing green

403(b) plans at UK aim for growth and

risk management

Advisor perspectives on active investment management

- A custodian that makes your life as an RIA simpler.

Partnering with the expertsI want to surround myself with the people and products that are at the top of the class, the best in the business. I have always operated that way and that carries over to the area of active management. Third-party managers have complete focus on the markets every day and the expertise to build strategies that can react favorably to changes in market conditions.

LOUD & CLEARAngela Sloan • Clover, SC Sloan Financial Group LLC • Madison Avenue Securities Inc.

3April 9, 2015 | proactiveadvisormagazine.com

LOUD & CLEAR

By Katie Kuehner-Hebert

Active investment management may help address many of the financial concerns of UHNW clients, including their desire to leave a legacy to heirs and charitable causes.

Profiling ultra-high-net-worth clients

4 proactiveadvisormagazine.com | April 9, 2015

hile ultra-high-net-worth clients (UHNW) may not have to worry about living paycheck-to-paycheck or saving for their kids’ college educations, the very rich do have

concerns for which an active portfolio manage-ment strategy might prove beneficial.

UHNW clients who have more than five million in assets want to ensure they will leave enough money to their beneficiaries and, in many cases, to their favorite charities. As such, engaging the services of an advisor practicing active portfolio management may make a great deal of sense. A properly allocated, active management approach can achieve the goal of capital appreciation over time while employing defensive mechanisms in turbulent markets. The resultant smoothing-out of returns is well suited to maintaining and growing assets for family generations to come.

While many ultra-high-net-worth clients may ostensibly be in a position to be more aggressive in their investment styles due to their overall wealth, active portfolio management can accommodate all types of risk profiles, from the most conservative to the most aggressive. Advisors who have the ability to manage port-folio strategies across the risk spectrum will be able to better serve clients with differing invest-ment attitudes and objectives.

Personality types of the ultra-high-net-worth client

Advisors should never assume that all UHNW clients are of the same mindset. Indeed, Russ Alan Prince, president of R.A. Prince & Associates Inc., and Brett Van Bortel, director of consulting services for Invesco Consulting, contend there are actually nine personality types among the very affluent that advisors should take under consideration:

Family StewardsConservative, “hands-off” investors who mainly want to take care of their families and are not very interested in the mechanics of investments

IndependentsBelieve investing is a necessary means to an end to gain personal financial freedom

PhobicsMay have inherited their assets but are confused and frustrated by the responsibility

of wealth and generally avoid focusing on investing

AnonymousValue privacy, concentrate their assets, and have a few close relationships with profes-sional services firms

MogulsCare most about controlling the asset management process and can present a challenge to advisors

VIPsValue prestige and prefer to affiliate with advisors with leading public reputations

AccumulatorsKnowledgeable and involved clients whose only goal for investing is to grow their assets

GamblersHigh risk tolerance, relish the process of investing, and feel they have the ability to discern the “next great” investment trend or stock InnovatorsTechnically savvy and very interested in companies with leading-edge products and services

Within these profiles, a wide disparity exists with regard to interest and involvement with

investments, their risk profiles, and their atti-tudes surrounding various types of investment asset classes. Advisors may need to adjust their communication styles for these nine personality types, as well as have access to a wide array of broad investment approaches and specific in-vestment strategies.

“One size fits all” certainly does not hold true for the ultra-high-net-worth client. Advisors who employ third-party asset managers, partic-ularly active managers, may have a competitive edge with their diverse array of strategies, the highly sophisticated nature of those strategies, and the ability to formulate portfolio approach-es that can work for a wide variety of client risk profiles and behavioral tendencies.

Charitable focus, worry lists, and challenges for heirs

UHNW clients, no matter their individ-ual investment outlook, also typically want to continue to allocate a significant portion of their money to charities. According to a 2012 Bank of America Study of High-Net-Worth Philanthropy, 95% of high-net-worth households donate regularly to at least one charity—compared to roughly 65% of the general population. The share of total charitable contributions made by the upper 5% of U.S. wealth holders is staggering.

And then there are the affluent clients who still worry whether or not they will outlive their money in retirement. According to a Lincoln

continue on pg. 13

W

58%

3%

13%

26%

One generation

Two generations

Three generations

Four generationsor more

Generations of sustained family wealth58% of high-net-worth individuals are the first generation in their family to be wealthy,while 26% have sustained wealth for two generations.

Source: 2014 U.S. Trust Study: “Insights on Wealth and Worth”

5April 9, 2015 | proactiveadvisormagazine.com

0

600k

400

200

-200

-400

-600

-800

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

{

Longest streak of monthly job gainssince WWII: 54 months.Previous best was 49 monthsending June 1990.

126

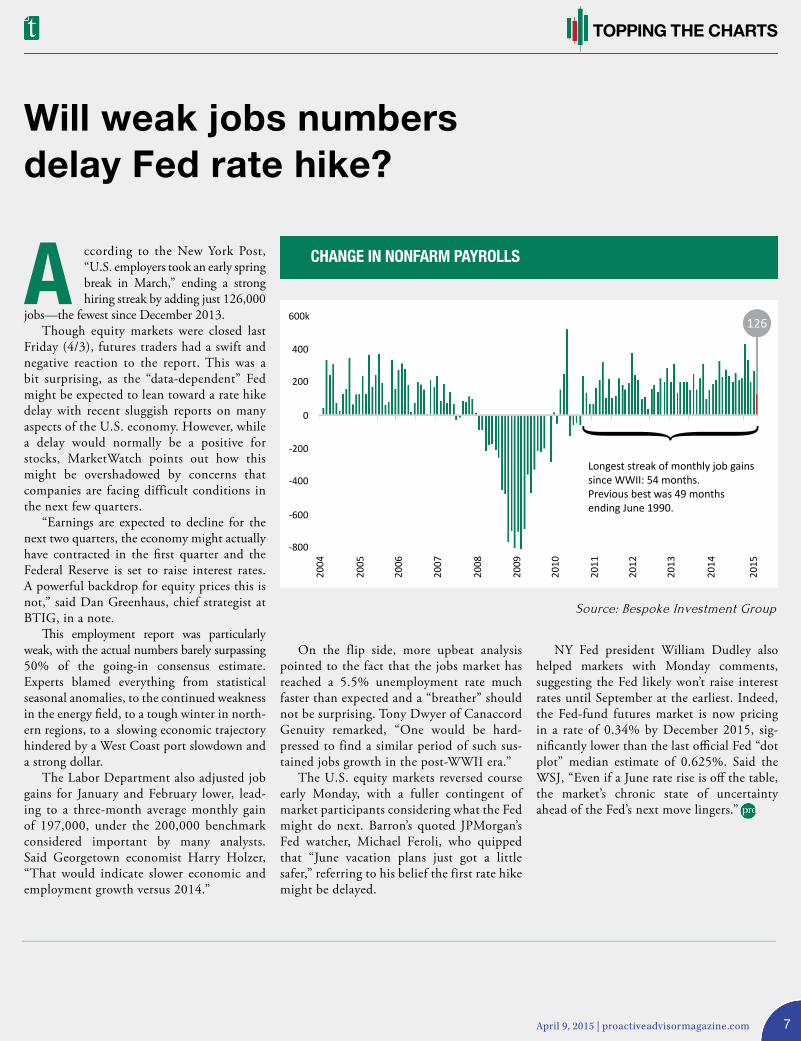

Will weak jobs numbers delay Fed rate hike?

ccording to the New York Post, “U.S. employers took an early spring break in March,” ending a strong hiring streak by adding just 126,000

jobs—the fewest since December 2013.Though equity markets were closed last

Friday (4/3), futures traders had a swift and negative reaction to the report. This was a bit surprising, as the “data-dependent” Fed might be expected to lean toward a rate hike delay with recent sluggish reports on many aspects of the U.S. economy. However, while a delay would normally be a positive for stocks, MarketWatch points out how this might be overshadowed by concerns that companies are facing difficult conditions in the next few quarters.

“Earnings are expected to decline for the next two quarters, the economy might actually have contracted in the first quarter and the Federal Reserve is set to raise interest rates. A powerful backdrop for equity prices this is not,” said Dan Greenhaus, chief strategist at BTIG, in a note.

This employment report was particularly weak, with the actual numbers barely surpassing 50% of the going-in consensus estimate. Experts blamed everything from statistical seasonal anomalies, to the continued weakness in the energy field, to a tough winter in north-ern regions, to a slowing economic trajectory hindered by a West Coast port slowdown and a strong dollar.

The Labor Department also adjusted job gains for January and February lower, lead-ing to a three-month average monthly gain of 197,000, under the 200,000 benchmark considered important by many analysts. Said Georgetown economist Harry Holzer, “That would indicate slower economic and employment growth versus 2014.”

A

Source: Bespoke Investment Group

On the flip side, more upbeat analysis pointed to the fact that the jobs market has reached a 5.5% unemployment rate much faster than expected and a “breather” should not be surprising. Tony Dwyer of Canaccord Genuity remarked, “One would be hard-pressed to find a similar period of such sus-tained jobs growth in the post-WWII era.”

The U.S. equity markets reversed course early Monday, with a fuller contingent of market participants considering what the Fed might do next. Barron’s quoted JPMorgan’s Fed watcher, Michael Feroli, who quipped that “June vacation plans just got a little safer,” referring to his belief the first rate hike might be delayed.

NY Fed president William Dudley also helped markets with Monday comments, suggesting the Fed likely won’t raise interest rates until September at the earliest. Indeed, the Fed-fund futures market is now pricing in a rate of 0.34% by December 2015, sig-nificantly lower than the last official Fed “dot plot” median estimate of 0.625%. Said the WSJ, “Even if a June rate rise is off the table, the market’s chronic state of uncertainty ahead of the Fed’s next move lingers.”

CHANGE IN NONFARM PAYROLLS

April 9, 2015 | proactiveadvisormagazine.com 7

TOPPING THE CHARTS

Proactive Advisor Magazine: Johnathon, tell me about your practice.

Johnathon Davis: I have developed a very significant practice in the 403(b) area. Having at-tended the University of Kentucky, I have a great affinity for the university and do a lot of work with several employee groups there.

The university has an excellent benefits plan and matching contribution schedule for employ-ees. UK employees have the option of two differ-ent custodians and over 100 investment choices. This is great, and it is coordinated with simple

is more or less a pretty random process with people hoping it will all work out in the end. This is where I come in.

How does your process usually work?

I am 100% focused on the financial advi-sory side. Many of my current clients are in the medical profession at UK. They are very caring, career-oriented people with demanding schedules. While they are concerned about retirement planning, they have not been able to devote time to really learn about it.

enrollment education on the nature of the 403(b) plans and the investment selection process.

But, frankly, no one is designated to help these employees actively navigate their way through the investment decision-making pro-cess over a 20- to 40-year timeframe, with the goal of achieving a successful retirement. It’s a common refrain that I hear when meeting with employees that there was really no discipline or concrete rationale as to why they made certain investment decisions. It is often based on what they may gather from financial news sources or what they hear from their fellow employees—it

Kentucky blue is seeing greenBy David WismerPhotography by Chris Cone

403(b) plans at UK aim for growth

and risk management with active

investment management strategies.

proactiveadvisormagazine.com | April 9, 20158

Johnathon Davis Retirement Tax Advisory Group

Lexington, KY

Estimated AUM: $35M

Licenses: 6, 26, 63, 65

Education: University of Kentucky, B.A., Business Marketing

“Investors are not aware of how much risk they are assuming in a passive investment strategy.”

continue on pg. 10

Johnathon Davis graduated from the University of Kentucky, where he was a three-year letter winner with the vaunted Wildcat basketball team. While there, he earned a Bachelor of Arts degree in Business Marketing. Mr. Davis has worked in several different financial ser-vices capacities, including vice president of commercial lending with a Fortune 500 bank. His firm, Retirement Tax Advisory Group, is based in Lexington, KY, and Mr. Davis is registered as a Uniform Investment Advisor.

Mr. Davis and his wife Ginger have two children: son Jackson, a collegiate-level basketball player himself, and daughter Clark, an Opera major at the University of Kentucky. When not helping his clients to achieve their financial goals, he watches and cheers for his son’s Butler University team and provides his daughter with the occasional vocal instruction.

A member of Consolidated Baptist Church and Omega Psi Phi Fraternity Inc., Mr. Davis is active in several non-profit groups.

Step one is education on how invest-ments may fit in with their overall retirement planning picture. When we have the basics squared away and I have a fundamental understanding of their investment objec-tives, I explain my use of third-party active investment managers to help in applying a risk-managed approach to investing. This almost always gets a positive response, and for the vast majority of my clients, I am able to manage 100% of their 403(b) assets through third-party managers.

Why does active management work for you and your clients?

Having been a licensed member of the finan-cial services community for more than 20 years, and with apologies to the great James Taylor, I tell clients, “I’ve seen fire, and I’ve seen rain.” What I mean by that is not only the market displace-ments we have seen in the 2000s, but also how emotions come into play for investors, leading them to either poor decision-making or acting like a deer in headlights. Too often paralysis by analysis makes it justifiable to do nothing with one’s investments. And if everyone else is doing nothing, shouldn’t I be doing nothing, too?

The key selling point for active management is its ability to react to current market condi-tions. This is a fresh concept for most of my clients, who have been uncomfortable seeing their accounts move up and down based on the volatility of the markets. Our money managers use a quantitative approach to help smooth out that volatility, which becomes especially import-ant during bear markets such as those in the early 2000s or 2008.

Were you always in the active management camp?

When I first started in the business, I was

indoctrinated into pretty traditional ways of thinking on diversification, rebalancing, and standard asset allocation models.

Modern Portfolio Theory worked for nearly 50 years, but “buy-and-hold” investing is now, in my opinion, an inappropriate investment strategy when clients’ retirement futures are on the line. The average investor is likely not aware of exactly how much risk they are assuming by being passive in their investment strategy. Our mission is to help our clients have access to both growth and defensive tactics in asset management as conditions warrant.

The recent financial crisis showed investors, especially retirees, the dramatic impact a stock market decline can have on their holdings at the time when they need to access their money most. With life expectancy increasing and markets fluctuating, investors need help managing their money in tough times. We use those third-party money managers who diligently practice active

April 9, 2015 | proactiveadvisormagazine.com 9

Retirement Tax Advisory Group Inc. (RTAG) is a Kentucky-based Registered Investment Advisory Firm. Securities offered through American Equity Investments, member FINRA and SIPC.

management. Accounts are monitored daily, and money is moved as deemed appropriate. We are convinced that this is the best strategy to give our clients a chance to reach their goals through both up and down markets.

How do you communicate the active management story to clients?

With active money management, our whole thesis is not about making the most money when the market goes up, but losing the least when the market goes down. I use elementary math to illustrate how this works out over time. The growth of a portfolio is severely hampered by trying to make up for periods of great loss, and that is exactly what we are trying to protect against. But the beauty of active management and trend-following is that when conditions

are in place to be bullish, the strategies we use should take advantage of that.

I also tend to use sports analogies with clients. They can quickly relate to the fact that every successful sports team has to have an equally strong offense and defense. I personally have had the privilege to have been affiliated with some legendary basketball coaches. I use those lessons I learned, as they are timeless and applicable to just about anything in life: Treat people with respect. Be disciplined. Be prepared for any circumstance. Then, put the best talent that you can on the floor and make sure it is well-coached and stays attentive and involved.

You can pretty quickly see how those prin-ciples can apply to working successfully with clients and in providing sound investment management practices.

continued from pg. 9Johnathon Davis

10 proactiveadvisormagazine.com | April 9, 2015

Dubuque, IA 52001 | 800.548.2993 | americantrustretirement.com

A solution different fromany other.

• Open architecture platform

• Active and tactical portfolios

• §3(38) investment management services

• Discretionary trustee services

• 170 PLANSPONSOR Best in Class awards since 2008

Request a copy of Ten Reasons Why You ShouldPartner with American Trust Retirement!

Simply better retirement.

Simply better partner

America’s best TAMPs: 2015A comprehensive guide to turnkey asset management programs: services offered, benefits, and some of the leading providers.

Target-date fund investors face disappointmentInflexible allocations to stocks and bonds could become an issue for pre-retirees and retirees in a lengthy period of lackluster returns.

Stock price path influences investment decisionsInvestors feel better about a loss if it follows a recovery—a behavioral trait that can influence future investment decisions.

L NKS WEEK

April 9, 2015 | proactiveadvisormagazine.com 11

Why you have way too much invested in U.S. stocks

Meb Faber is a co-founder and the chief investment officer of Cambria Investment Management. Faber is the manager of Cambria’s ETFs, separate accounts and private investment funds. Mr. Faber has authored numerous white papers and three books: Shareholder Yield, The Ivy Portfolio, and Global Value. He is a frequent speaker and writer on investment strategies and has been featured in Barron’s, The New York Times and The New Yorker. Mr. Faber graduated from the University of Virginia with a double major in Engineering Science and Biology. www.cambriafunds.com and www.mebfaber.com

Ranking country valuations by CAPE ratios

Least expensive Most expensive GreeceRussiaHungaryAustriaPortugalBrazilCzech

25688910

MexicoSwedenSwitzerlandJapanUSAPhilippinesDenmark

22232326272834

Source: Global financial data, MSCI, Bloomberg. Country valuations based on cyclically adjusted price-earnings (CAPE) ratios.

uick question: How much of your global stock portfolio is in U.S. stocks? Let me guess: 70%? 80%? 100%?

The JPMorgan Guide to the Markets illus-trates the U.S. as a percentage of global market capitalization (52%) and GDP (20%). Even if you are a die-hard Vanguard “Bogelhead” indexer, you should only have about half of your equity allocation in U.S. stocks.

But few do. Most investors around the world invest

the majority of their assets in their own stock market. This is called the home-country bias, and it occurs everywhere. Vanguard details the effect in the U.S., the U.K., Australia, and Canada. U.S. investors have approximately 72% invested in the U.S. market. It isn’t just retail investors—professional investors allocate most of their assets to their home countries as well.

A home-country bias is compounded by an-other unfortunate tendency that most investors exhibit: favoring market indices weighted by market capitalization. Why is market-cap weight-ing so problematic? Market-cap weighted indexes are constructed using only one variable—size—which is determined by price.

When overvalued assets grow to be bigger and bigger parts of a market—or become the market—you no longer want to invest in that market or stock. That’s the beauty of capitalism and creative destruction. When a company grows to be one of the most successful companies in the world, that success places a large target on its back. When Apple made the world-changing iPhone, companies began to seriously compete with it.

Japan’s stock market rose to account for nearly half of the world’s market cap in the

Q

1980s. And if you believed in the efficient market, you would have invested half of your equity allocation in Japan. But Japan returned approximately -2% per year from 1990-2010, including more than 20 years of negative re-turns. A value-driven approach works not just by investing in the cheapest markets, but also by avoiding the most expensive.

What is the biggest country in the world by market cap now? The U.S.—with nearly half of global stock-market capitalization. The figure above shows the cheapest and most expensive countries in the world. Notice that the U.S. is one of the most expensive countries in the world.

The U.S. was cheap relative to the rest of the world in the early 1980s, which also happened to be the start of the long bull market. The late 1990s saw the U.S. near the top of the range, which preceded the bear market that began in 2000. Will the current overvaluation signal

another bear or perhaps a time to shift more assets to foreign markets? Time will tell.

The bad news is that U.S. stocks are expen-sive, although not in bubble territory. I expect U.S. stocks to return about 2% per annum for the next 10 years. The good news is that most of the rest of the world is quite cheap.

Here are a few actions investors can take to improve the future returns of their equity port-folio: 1) allocate your portfolio reflecting global market-cap weightings; 2) consider also weight-ing along global GDP, avoiding market-cap-con-centration risk; and 3) consider more of a value global approach, overweighting a basket of cheaper countries and lowering weight to the most overpriced. For those heavily allocated to the U.S., this might mean a significant reduction in relative percentage weight.

Proactive Advisor Magazine presents weekly commentary provided by well-known market analysts, financial authors, investment newsletter publishers, and economists. The opinions expressed each week represent their personal perspectives and not necessarily those of the magazine.

proactiveadvisormagazine.com | April 9, 201512

HOW I SEE IT

Rydex FundsA Comparison of ETFs and Mutual Funds—The True Cost of Investing

continued from pg. 5

Financial survey, nearly half (48%) of wealthy Baby Boomers who have saved more than $1 million for retirement feared their money would not last until their death. Many of the superrich also worry about the prospect of losing significant portions of their wealth. According to Prince & Associates, more than 80% of those worth $20 million or more are deeply concerned about being the target of lawsuits from plaintiff lawyers who seek out deep pockets. Others cite “medical crises,” “family disputes,” and “changes in the family dynamic” as top worry points potentially affecting their wealth.

Advisors can help foster relationships with the children of UHNW clients by engendering trust that their wealth is being proactively managed and protected. Such strategies would also be effective for those heirs who might have very different attitudes about money than their parents, particularly children of parents who were not born into wealth, but accumulated it through hard work and perseverance (see exhibit: more than 50% of UHNW are first generation).

Through education on the long-term market cycles of economies and investments, where active management can shine, many heirs may learn that they cannot assume their money will

always be there for them without proper and continual management. They would benefit greatly from a financial advisor or wealth man-ager who employs active investment strategies that can be adjusted as market or economic conditions fluctuate.

On the flip side, proactive advisors may be able to attract young high-net-worth clients who seek an alternative to their parents’ advisors by demonstrating the superiority of active port-folio management over what may have been a multi-generational static relationship with an-other advisory firm. Roughly half of rich heirs under the age of 40 say that they are willing to shop for another advisor, according to a recent survey by Morgan Stanley and Campden Research.

Then there are heirs whose families have never used the services of a wealth manager—preferring instead to rely on their own real estate,

stock market, or business investment prowess. Unfortunately, in more cases than not, such acumen is not necessarily passed down to the next generation. In fact, according to a 2014 U.S. Trust study, “the majority of wealthy parents question whether their children will be adequately prepared to handle the inheritance planned for them.”

Financial advisors or wealth managers with a true point of difference—skilled in employing the services of third-party active managers—may be able to demonstrate the prudence of working with a professional who has the expertise to handle the ever-increasing sophistication and complexities of the investment environment. The children of ultra-high-net-worth clients, who stand to inherit an unprecedented amount of wealth over the next 30 years, would be well-served by a proactive investment approach—instead of falling back on what may be an outdated and dangerous family philosophy that their “wealth will last forever.”

UHNW Clients

Katie Kuehner-Hebert is an award-winning journalist with more than two decades of experience writing about the financial services industry. She has expertise in the banking, insurance, financial planning, economic develop-ment, and employee benefits areas and her work has appeared in many leading publications.

Advisors may attract young HNW clientsby demonstrating the benefits of activeportfolio management.

13April 9, 2015 | proactiveadvisormagazine.com

Advertising proactiveadvisormagazine.com/advertising

Reprintsproactiveadvisormagazine.com/reprints

Copyright 2015© Dynamic Performance Publishing Inc. All rights reserved. Reproduction of printed form, whole or in part, without permission is prohibited.

EditorDavid Wismer

Associate EditorElizabeth Whitley

Contributing WritersMeb Faber

Katie Kuehner-HebertDavid Wismer

Graphic DesignerTravis Bramble

Contributing PhotographerChris Cone

April 09, 2015Volume 6 | Issue 2

Proactive Advisor Magazine is dedicated to promoting and educating on active investment management. Distribution reaches a wide audience of financial professionals who advise clients on investments and portfolio management. Each issue features an experienced investment advisor who offers insights on active money management, client service, and investment approaches. Additionally, Proactive Advisor Magazine offers an up-close look at a topic with current relevance to the field of active management.

The opinions and forecasts expressed herein are those of the author and may not actually come to pass. Any opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. The analysis and information in this edition and on our website is for informational purposes only. No part of the material presented in this edition or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any portfolio constitutes a solicitation to purchase or sell securities or any investment program.

Building a “niche” into a practice focus

Phylyp Wagner, CFP®

McLean, VAH. BeckFounder

Wagner Resource Group Inc.

Securities and investment advisory services offered through H. Beck Inc., member FINRA/SIPC and an SEC-registered investment advisor. H. Beck Inc. and Wagner Resource Group Inc. are not affiliated. Investments will fluctu-ate and when redeemed may be worth more or less than when originally invested.

hile we will gladly work with clients from any walk of life, we have found a niche target segment

that has expanded to become the bulk of our client roster. Attorneys are excellent prospects for forward-thinking financial planning. They are affluent, consumed with their professional lives, and appreciate the principles of risk management in planning for their financial futures.

Targeting attorneys came about by a little bit of luck and a lot of hard work. It started with a thorough investigation of SIC codes to see what might be good target segments in the Washington, D.C., metro area. It became obvious that the legal profession was one of the dominant segments, with over 25,000 attorneys in the area.

We have developed several marketing and database methods to identify specific law firms and attorneys, and have developed a commu-nications plan to reach out to them. After many years of doing this, we have some expertise in what works and have a very good response rate leading to initial meetings. We average two or three new prospect appointments a week, plus additional follow-up meetings coming from contacts in our existing client base.

In addition to the marketing side of the equation, our core competencies as a firm are appealing to this audience. Attorneys can appreciate the sophisticated active investment management strategies that we employ. They are also very receptive to messages around risk management, for both their investments and their insurance needs. They like our focus on tax-advantaged financial planning and expertise in alternative investments. They also represent a good target for 401(k) investment management and generally have substantial assets in their plans.

This has become a very successful marketing focus so the legal profession really no longer qualifies as a niche for us—it represents the bulk of our client roster. Other firms certainly target this segment, but we believe we do it exceptionally well by drilling into and understanding all aspects of their firms’ benefits and qualified plans.

W

Matt Quattlebaum, CFP®

McLean, VAH. Beck

Senior Financial PlannerWagner Resource Group Inc.

This enables us to assist our attorney clients in many more aspects of their lives. As such we have become the “go-to” financial planning firm for many of the law firms in our region. Currently we are represented in over 60 law firms and have multiple clients in many of those.

14

TIPS & TOOLS

Active ManagementThere is a great deal of confusion surrounding the term “active

management” created by the business press. When one reads a headline in any given year that “active managers” are underperforming or overper-forming their benchmarks, this typically is referring to “active” managers of a mutual fund—who are being measured against a specific index or competing funds within that style.

Within the field of true active portfolio management, this narrow and misleading definition really has little significance.

Active investment management is not about exceeding a specific benchmark or “beating the market.” Active management seeks favorable risk-adjusted returns in any market environment, generally employing sophisticated algorithms and models to capture gains and protect against losses in a wide variety of sectors, asset classes, and geographies.

It is about controlling risk in the markets, finding new ways to dynamically diversify, and smoothing out the long-term volatility typically found in any asset class. Active managers tend to rely on quantitative approaches for asset allocation, exposure to the market, and adjustments to portfolios based on current market conditions. When it comes to evaluating returns, they generally will not compare to the S&P 500 or global total market indexes, but are far more interested in risk-adjusted returns and in meeting their portfolio objectives.

In theory, it is fundamentally about a long-term approach to portfolio management that is diametrically opposed to “buy-and-hold.”

Fee-based assets continue to grow among advisors

101

DynamicStrategic

Diversification

Tools Models

Strategies

5 reasons to consider active management

Buy and hold is dead(ly)—While bull market runs are impressive, history shows it is not a matter of “if ” but more a matter of

“when” for the next bear market. Investment expert Kenneth Solow sums it up: “Patiently waiting for stocks to deliver historical average returns does not rise to the level of an investment strategy.”

Bear market math is daunting—It takes longer than most in-vestors think to recover from bear markets—a gain of 50% is

needed to overcome a 33% portfolio loss.

Risk first: always—As one prominent active manager has said, “No one would ever jump into a car without brakes, so why

would investors even consider having an investment strategy that did not have a strong defense?”

Active management aligns with investor psychology—Behavioral finance studies have documented the tendencies of investors to

operate on the destructive principles of “fear and greed.” Disciplined active management takes emotion out of the equation.

Does “set it and forget it” really make sense?—For retirees or those approaching it, the “sequence of returns” dilemma can

have a devastating effect on future income needs. Active management offers a prudent path to achieving the twin goals of asset preservation and compounded capital growth.

Resources for AdvisorsWebsitesProactive Advisor Magazine: Active investment management’s weekly magazine, providing advisor perspectives, topical issues in active management and commentary on strategy and tactical tools. www.proactiveadvisormagazine.com

National Association of Active Investment Managers (NAAIM): Peer-to-peer networking in the active investment management community, providing best practices among successful advisors and advisory firms. www.naaim.org

Market Technicians Association (MTA): Leading national organization of investment analysts, stock market analysis professionals and certified market technicians. www.mta.org

Advisor Perspectives: Audience-generated and vendor-neutral forum where fund companies, wealth managers and financial advisors share their views on the market, the economy and investment strategy. www.advisorperspectives.com

Whitepapers“Bucket Investing with Dynamic Risk-Managed Portfolios,” Flexible Plan Investmentsgoto.flexibleplan.com/download/whitepaper-bucket-investing.pdf

“Comparison of ETFs and Mutual Funds—The True Cost of Investing,” Guggenheim Investments guggenheiminvestments.com/rydex

“Understanding Leveraged Exchange Traded Funds,” Direxion Investmentswww.direxioninvestments.com

“Small Accounts, Big Opportunities,” Trust Company of America www.trustamerica.com/resources

“Why Gold? Seven Enduring Reasons,” Flexible Plan Investments goldbullionstrategyfund.com

“The State of Retail Wealth Management, 4th Annual Report,” PriceMetrixwww.pricemetrix.com

2011 2012 2013

Fee-Based Assets (% of Total Assets) 25% 28% 31%

Fee-Based Revenue (% of Total Revenue) 43% 45% 47%

Fee Accounts per Advisor 85 92 101

Average Fee Account Assets ($000s) $240 $258 $293

Source: PriceMetrix Insights – The State of Retail Wealth Management 2013 – 4th Annual Report (Aggregated data representing 7 million retail investors and over $3.5 trillion in investment assets.)