john aldersley, executive chairman direct portfolio services limited 22 november 2006

TRANSCRIPT

John Aldersley, Executive Chairman

Direct Portfolio Services Limited

22 November 2006

MANAGED ACCOUNTS:

Latest fad or simply evolution?

Disclaimer

This presentation has been prepared by Direct Portfolio Services Limited (DPSL), ABN 18 072 262 312, AFSL 245525. DPSL’s contact details can be found on www.shareinvest.com.au. Our address is Level 5, 2 Bulletin Place SYDNEY NSW 2000.

DPSL believes the information contained in this document to be accurate at the date of the presentation. But to the extent permissible by law DPSL makes no express warranties and excludes all implied warranties in relation to the information contained in this document.

This document does not purport to be comprehensive or to provide legal, financial or any other professional advice and should not be relied as such. To the extent permissible by law, DPSL excludes all liability for any loss or damage whether direct, indirect or consequential arising in any way out of the use of the information contained in this document or results obtained from the use of it.

Agenda

• The marketplace opportunity• An evolutionary view of discretionary portfolios • IMA, SMA & MDA – explained• SMA Features

USA SMA growth projection

-

500

1,000

1,500

2,000

2,500

SM

A A

sset

s U

S$

mil

-

3

6

9

12

Nu

mb

er o

f Acc

ou

nts

(m

il)SMA Assets US$ (billions)

Number of Accounts (millions)

Source: Money Management Institute, FRC, 2005

51% of Australians own shares 44% directly

Trend of Australian Share Ownership

0%

10%

20%

30%

40%

50%

60%

1997 1998 1999 2000 2001 2002 2003 2004

Indirect Both Direct/Indirect Direct Only

Share Ownership rising in all age groups

Direct Share Ownership - Age% owning shares directly

16

30

4247 48

21

35

4652

56

0

10

20

30

40

50

60

18 - 24 years 25 - 35 years 36 - 44 years 45 - 54 years 55 years +

2003 2004

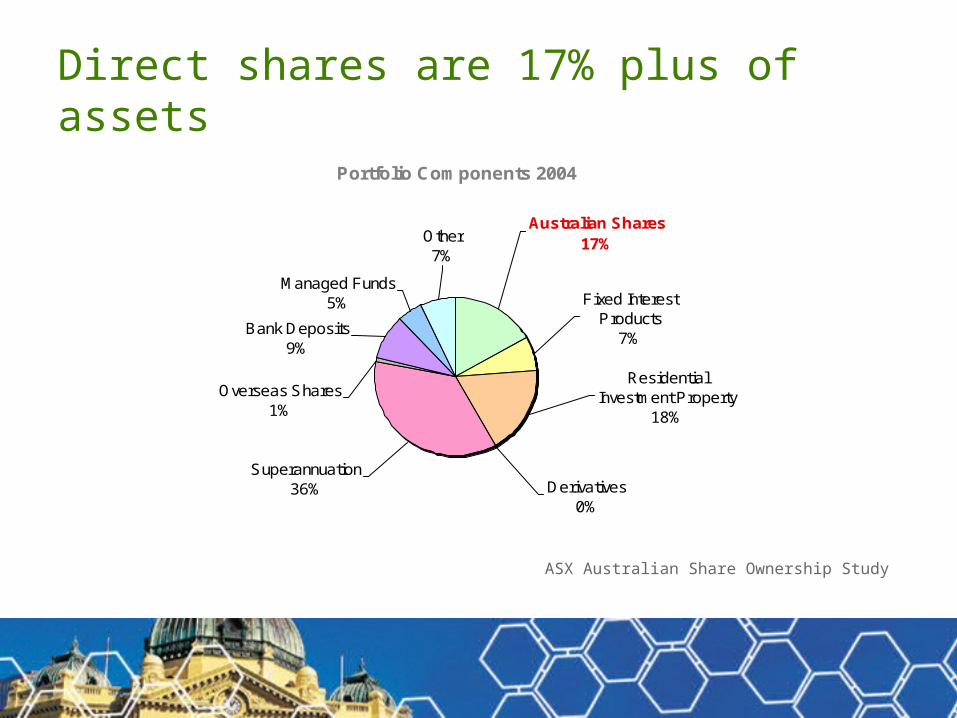

Direct shares are 17% plus of assets

Portfolio Components 2004

Other7%

Managed Funds5%

Bank Deposits9%

Overseas Shares1%

Superannuation36% Derivatives

0%

Residential Investment Property

18%

Fixed Interest Products

7%

Australian Shares17%

ASX Australian Share Ownership Study

Direct equity investors not using planners

Source of Direct Share Ownership 2004

55%

38%

21%

13%

10%

10%

15%

0% 10% 20% 30% 40% 50% 60%

Broker

Prospectus / Float

Float or Privatisation

Financial Planner

Employee Share Scheme

Inheritance or Gift

Bought via Employer

The Australian Marketplace

• 40% of these investors do not use a planner

• Conclusion – passive holdings on Wraps & equity unit trusts are not the solution 40% of share-owning investors are seeking

Differing risk perspectives?

Adviser view of the world

• Inflation is not an issue

• Life expectancy for a 65 year old male is around 86

• Current product range should achieve investment goals

Client view of the world

• Inflation is an issue eg health care,

fuel, etc

• Longevity is seen as a risk –

(a 65 year old has >35% of

becoming a 93 year old)

• Standard industry “unitised”

products not trusted to deliver

sufficient after tax growth

Source: McKinsey Survey 2005 presented at Money

Management Institute conference in USA 2006

Evolution of discretionary managed accounts

For 200 years:• Traditional private bank style discretionary equity portfolios available to

very wealthy & institutional investors only – traditional IMA – 0.05% of population

• Team of adviser, fund manager, brokers, banker, accountant built & managed the investment portfolios

• Private banking arms of banks still operate this way

Unit Trusts took discretionary shares to the masses…

• Commenced pre-computerisation over 40 yrs ago• Pooling of investments in unit trust allowed for

investment & administrative efficiencies• Allowed for low investment minimums• Shift of power from life companies to

funds management companies

Disadvantages of Unit Trusts

• Own units not the underlying shares• Cannot transfer your existing shares in• New investors inherit existing undistributed gains• Deliberate realising of gains each year• Income & realised gains paid six monthly• Any realised losses are trapped in the trust

DIY issues to consider

paperwork hassles

too speculative at highs

sporadic dividends

hard to access growth return

too cautious at lows

Ideal future

• Separately accounted personal portfolios within a managed fund structure

• Full time professional discretionary management• Beneficial ownership & tax effective investment

management• Each client determines a monthly income amount in

conjunction with a professional adviser• Eliminate paperwork & CGT hassles

Everyone told me in 1992 it was impossible

The Lesson:

Technology & human endeavour makes most things possible in time

The “impossible” retail SMA of 1994

• Prospectus based “prescribed interest” retail offer• Single pooled bank account “virtual” client accounts• Single pooled “bare trust” Custodial holdings• Separately accounted portfolios• True investment system (cash and accrual accounting)• Centrally implemented manager models• Ability to transfer existing shares in specie – locked parcels• Derivative overlays on existing shares• Monthly Annuity-style income stream (EasyIncome) nominated by each client• Regular saving & instalment gearing into direct shares

Beneficial ownership

Scheme

Model Portfolio

Investor 1 Investor 2 Investor 3

Securities

Cash

Ownership Tracking to Individual

Scheme

Model Portfolio

Model Manager

Units Units Units

Model Manager

Investor 1 Investor 2 Investor 3

TrustTrust

Unit Trust Structure Separately Managed Account Structure

Trust structure is removed

FSR was a watershed

FSR introduced:• Single Responsible Entity (fiduciary) for financial products

• Distinction between financial products and financial services

• Management of conflicts of interest in discretionary accounts within a regulated compliance setting

• SMA formally recognised by ASIC

• Dec 2004 – ASIC Policy on Managed Discretionary Accounts (PS179 & CO 04/294) allows financial service version

What are Managed Accounts?

Defining features of Managed Accounts• Underlying investment assets are held personally by the investor

• Held either legally & beneficially (IMA) or just beneficially (single HIN SMA)

• Investments managed on a discretionary basis

Individually Managed Accounts (IMA)

Customisation• Tailored to individual wishes

Administration• Individual HINs

• Trades, corporate actions & income/distributions are processed at an individual level

• High administrative overhead hence high fees & minimum investments

• Difficult to scale due to individual nature of portfolio management

Legalities (Retail Clients)• Must be structured as either an Managed Discretionary Account (MDA)

or SMA financial product

Separately Managed Accounts (SMA)

Customisation• Range of model portfolios, each with particular investment process & strategy• Technology can allow for customisation

• Locked existing holdings, exclusion of stocks from a model, min trade sizes

Administration• Single HIN – all securities held by a custodian• Trades, corporate actions & income/distributions by pooled electronic processes• Highly efficient hence becoming cheaper than unit trusts• Highly scaleable so expect further cost reductions

Legalities (Retail Clients)• For pooling benefits must be structured as a Managed Investment

Scheme (MIS) – like a Unit Trust

SMA v MDA • SMA = Financial Product

• Registered Managed Investment Scheme

• PDS disclosure

• No requirement for transaction reports

• No ASIC requirement for personal advice

• No requirement to provide Statement of Advice to RE

• No ASIC requirement for continuing personal advice

• Professional active management

• Suits retail and wholesale clients

MDA = Financial Service

• Governed by PS 179 & CO 04/294

• Individual contracts

• Transactions reports required

• Personal Advice required & linked to

investment program

• Copy of SOA must go to MDA operator

• <13 months confirm advice & investment

program remains in best interests of client

• Mostly broker run portfolios

• Mostly for wholesale clients

Why advisers will go SMA route

• SMAs are financial products – no change to current business model

• PS146 Managed Fund training (& product training)

• Separation of advice from product

• Suit retail as well as wholesale clients

• Great fit with Self-Managed Super Funds

• Good margins available (less competition in retail)

• Efficient scaleable way of providing direct equities for clients

• Will shortly be wholesale product on wraps/desktops

• Adviser can focus on advice & growing client numbers (or construct own models)

• Clients are demanding them

SMA Features

Tax & investment efficiencies• No inheritance of other investor’s capital gains

• In-specie transfers without CGT events enable customisation & flexibility

• “Tax aware” portfolio management & tax planning possible – eg 12 month discount rule on CGT; tax harvesting

• Realised losses available to investors

• Reduced transaction costs (SMAs) – netting of trades

• Enables accumulation & capital drawdown strategies in direct shares

SMA Features

Investment options• Portfolios predominantly built from ASX300 securities

• Some providers offer:• Fixed interest & hybrids• Derivative overlays• Listed property trusts• Margin lending• Managed models of unit trusts

• Soon we will see direct International equity portfolios

SMA Features

Model portfolios• Range of investment strategies, managers

• Internal & external model managers

• As security weightings from model manager change, the SMA provider automatically rebalances each investors portfolio to reflect the changes

SMA Features

Customisation tools• Custody-only style service possible

• Filtering of stocks – exclude stocks/sectors from model portfolios

• “Locking” of particular tax parcels to avoid sales of “existing” shares

• Derivative overlays

• Individual tax parcel management – bed & breakfasting

• Minimum trade sizes

• IMA portfolios for ultra HNW

SMA Features

More transparent than unit trusts• Fees & charges are shown as individual transaction items

• Individual transaction history available

• Individual holdings within a portfolio are visible

• Web based daily valuation reporting the norm

• Allows the adviser/client to be fully informed

Fees & Charges

Administration Fee• Charged by the MA provider for operating the service

• Range from 0.385% to 1.5% pa. Usually scales down for size

• Amount depends on level of individualisation (increased overheads)

• Custodian & audit fees may also be charged

Model Manager Fee (Investment Fee)• Deducted and paid to the model manager

• Range between 0% - 0.6% pa depending on the type of model profile

MER (pre adviser)• Can range between 0.44% - 2.5% pa

SMAs are no fad

Client driven demand• DIY Clients believe SMAs are high touch sophisticated products –

likely to meet their emotional & financial needs

Beliefs depend on perspective…

SMA Opportunities with SMSF

• Treated as a managed fund for compliance purposes:• therefore summary audited data only required by administrator • no need to verify holdings, transactions or corporate actions• can be annual rather than 24/7 super administration• Non-unitised structure appeals to their accountants

• Can establish dollar cost averaging strategies for small DIY funds via regular salary sacrifice• Can organise regular monthly capital drawdown for pension mode members – can combine

with specialist low volatility funds• Can accept existing holdings in specie• S.I.S. exemption for Risk Management Statement for Option overlays when through a

collective financial product• DIY Super Baby-boomers are fast approaching retirement – need strategic financial advice

for the first time (in their view)

SMAs deliver practice efficiencies

Current IDPS (Wrap) structures have efficiency limitations:• Investor discretionary – so SOA based changes, lack of pooling

• Direct share solutions – mainly administration based - active management can be complex & expensive (corporate actions, contract notes, etc)

• Primitive investment systems – lack accrual/cash accounting

Solution• SMA menu of mandates on wrap

• Indirect investment in wholesale SMA via WRAP

• SMA migrate to Unified Managed Accounts

(combine shares & unit trusts)