jll riyadh real estate market overview q1 2011...

TRANSCRIPT

RiyadhReal Estate Market Overview Q1 2011Riyadh

Market Highlights – Q1 2011

Land trading remains the most active sector of the real estate investment market in Saudi Arabia. Trading volumes have increased in the Riyadh market, driving up land prices during Q1 2011.

Owners have begun to recognise the importance of property/facility management and are preparing new strategies.

Public companies and agencies leading investment and development. Plans to construct a further 500,000 residential units and major investment in infrastructure, transport, health and education sectors will further reinforce this position.

The office market continues to see new supply entering the market pushing CBD vacancies up to 18%. While demand is strong, it is unlikely to offset additional supply levels, resulting in a further decline in average rentals during 2011.

The office market will remain tenant favourable during the next three years. There will be opportunities to ‘trade up’ from existing facilities and improve workplaces, enhance security and increase parking.

While retail sales have increased on the back of the government stimulus package, rents are generally stable and vacancies have increased in secondary centres during Q1 2011.

Development opportunities remain for community retail centres because city limits are expanding and new residential areas are being developed.

Residential rents and sale prices are increasing and should continue to do so for the rest of 2011. Mortgage and off plan sale reforms should augment demand next year.

Developers now recognize affordable housing demand, but high land prices and a reliance upon traditional construction techniques remain significant hurdles to private sector delivery of affordable housing in Riyadh.

The Riyadh hotel market has moved into the recovery stage of the property cycle in Q1 2011, with increasing ADR’s and Rev PAR compared to the same period of 2010.

Market Milestones – Q1 2011Economic News

More than 50% of this stimulus package is directed towards housing, with an objective to

create 500,000 additional housing units for Saudi families. To support this target, the loan

limit of the Real Estate Development Fund was

increased from SAR 300,000 to SAR 500,000.

A new Ministry of Housing has been established to assume

the authority and responsibilities

of the General Housing Authority.

Real GDP growth for 2011 is currently forecast at

5.7%, with Saudi Arabia being one of very few countries in the MENA

region to have experienced an upward revision of

economic growth projections since the beginning of 2011.

These projections are underpinned by the oil price

remaining consistently at more than USD 100 per

barrel

The largest ever government budget (SAR 580 billion) has

been augmented by King Abdullah’s recent

announcement of one-time stimulus measures worth SAR 500 billion to be realised over

the next few years.

The Shura Council has approved the long-awaited mortgage laws. The

Shura Council has also waived the requirement for expatriate residents to secure approval from the Ministry

of Interior in order to purchase a home.

Market Milestones – Q1 2011Property & Project News

Parastatal entities such as GOSI, PPA and the National Guard have announcedresidential projects which will deliver more than 40,000 units in the coming few years.

The Ministry of Transport has allocated SAR 11 billion to develop new road networks. Riyadh will receive the lion’s share of this total, with plans including King Abdullah Road and the extension of SitteenStreet to the North Ring Road

Kingdom Holdings has announced the development of the second “Kingdom City” on 1 million sq m of land to the north east of Riyadh. This will be a mixed use project including residential villas, hotels and all support facilities.

Rafal has launched Al Rabiah - a new 500 villa semi-gated community located to the west of Riyadh. Rafal has also completed registration to conduct off plan sales in their 62 storey Rafal Tower project.

Fairmont Raffles Holdings has signed an agreement to manage two new hotels in the Riyadh Business Gate project.

MODON has signed agreements with different contractors to develop the infrastructure for an additional 1.5 million sq m of industrial land located in Al Kharj.

Riyadh Rental Clock – Q1 2011

5

Rental GrowthSlowing

RentsFalling

Rental GrowthAccelerating

RentsBottoming Out

Office

RetailHotel** Hotel Sector reflects the movement of RevPARSource: Jones Lang LaSalle

Residential

Riyadh Market Overview

Office

DEMAND

SUPPLY PERFORMANCE

OUTLOOK

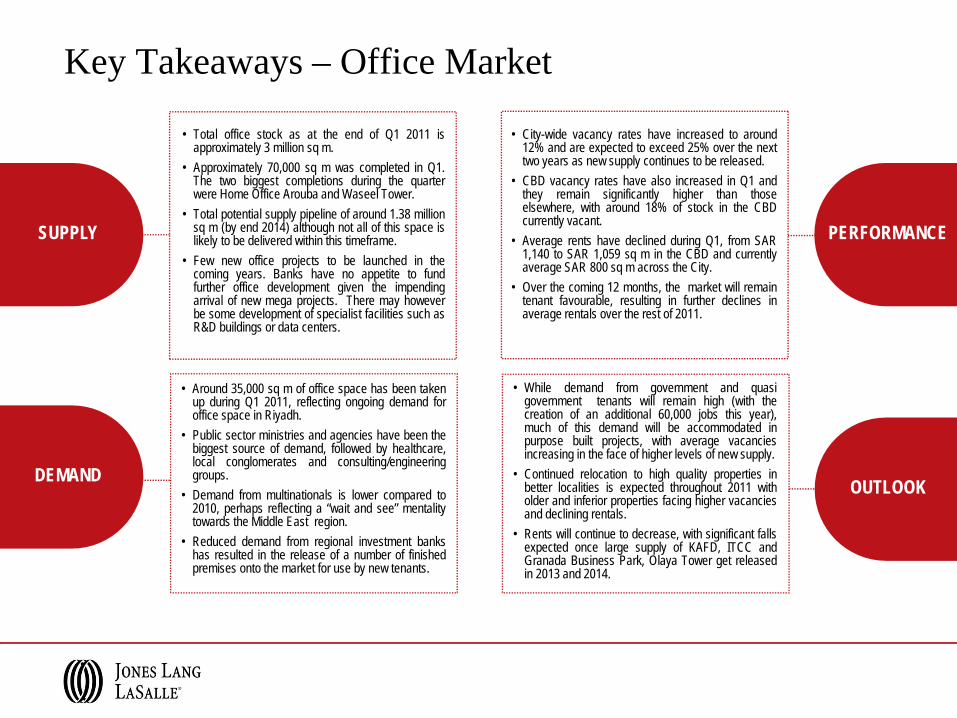

Key Takeaways – Office Market

• Total office stock as at the end of Q1 2011 isapproximately 3 million sq m.

• Approximately 70,000 sq m was completed in Q1.The two biggest completions during the quarterwere Home Office Arouba and Waseel Tower.

• Total potential supply pipeline of around 1.38 millionsq m (by end 2014) although not all of this space islikely to be delivered within this timeframe.

• Few new office projects to be launched in thecoming years. Banks have no appetite to fundfurther office development given the impendingarrival of new mega projects. There may howeverbe some development of specialist facilities such asR&D buildings or data centers.

• Around 35,000 sq m of office space has been takenup during Q1 2011, reflecting ongoing demand foroffice space in Riyadh.

• Public sector ministries and agencies have been thebiggest source of demand, followed by healthcare,local conglomerates and consulting/engineeringgroups.

• Demand from multinationals is lower compared to2010, perhaps reflecting a “wait and see” mentalitytowards the Middle East region.

• Reduced demand from regional investment bankshas resulted in the release of a number of finishedpremises onto the market for use by new tenants.

• City-wide vacancy rates have increased to around12% and are expected to exceed 25% over the nexttwo years as new supply continues to be released.

• CBD vacancy rates have also increased in Q1 andthey remain significantly higher than thoseelsewhere, with around 18% of stock in the CBDcurrently vacant.

• Average rents have declined during Q1, from SAR1,140 to SAR 1,059 sq m in the CBD and currentlyaverage SAR 800 sq m across the City.

• Over the coming 12 months, the market will remaintenant favourable, resulting in further declines inaverage rentals over the rest of 2011.

• While demand from government and quasigovernment tenants will remain high (with thecreation of an additional 60,000 jobs this year),much of this demand will be accommodated inpurpose built projects, with average vacanciesincreasing in the face of higher levels of new supply.

• Continued relocation to high quality properties inbetter localities is expected throughout 2011 witholder and inferior properties facing higher vacanciesand declining rentals.

• Rents will continue to decrease, with significant fallsexpected once large supply of KAFD, ITCC andGranada Business Park, Olaya Tower get releasedin 2013 and 2014.

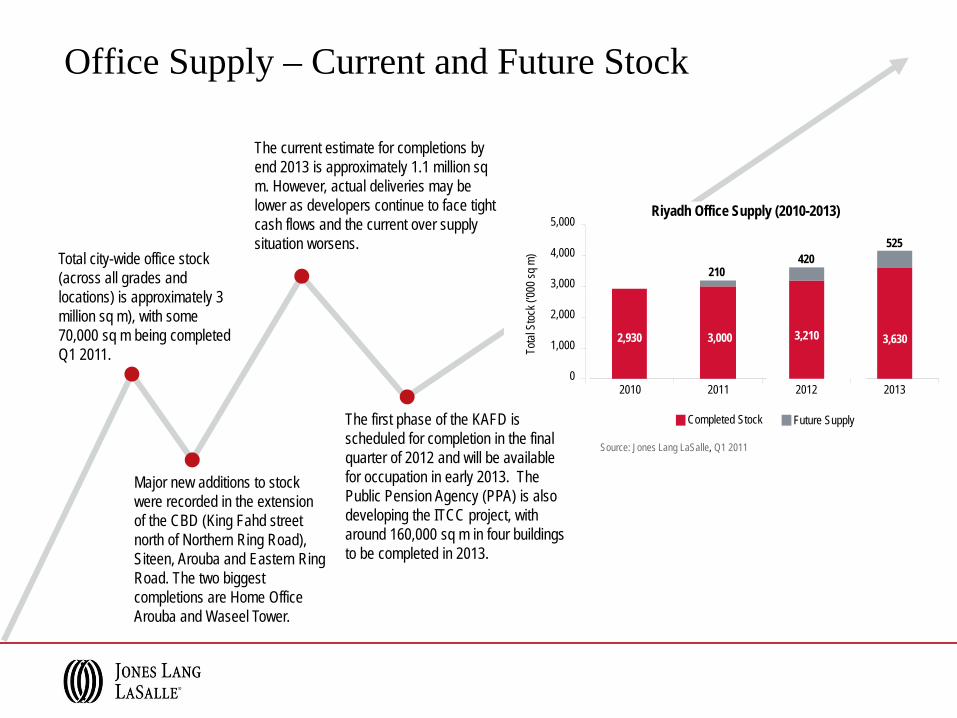

Total city-wide office stock (across all grades and locations) is approximately 3 million sq m), with some 70,000 sq m being completed Q1 2011.

Office Supply – Current and Future Stock

Major new additions to stock were recorded in the extension of the CBD (King Fahd street north of Northern Ring Road), Siteen, Arouba and Eastern Ring Road. The two biggest completions are Home Office Arouba and Waseel Tower.

The current estimate for completions by end 2013 is approximately 1.1 million sq m. However, actual deliveries may be lower as developers continue to face tight cash flows and the current over supply situation worsens.

The first phase of the KAFD is scheduled for completion in the final quarter of 2012 and will be available for occupation in early 2013. The Public Pension Agency (PPA) is also developing the ITCC project, with around 160,000 sq m in four buildings to be completed in 2013.

Source: Jones Lang LaSalle, Q1 2011

Riyadh Office Supply (2010-2013)

210420

525

2,930 3,000 3,210 3,630

0

1,000

2,000

3,000

4,000

5,000

2010 2011 2012 2013

Total

Stoc

k ('00

0 sq m

)

Completed Stock Future Supply

Rental Performance

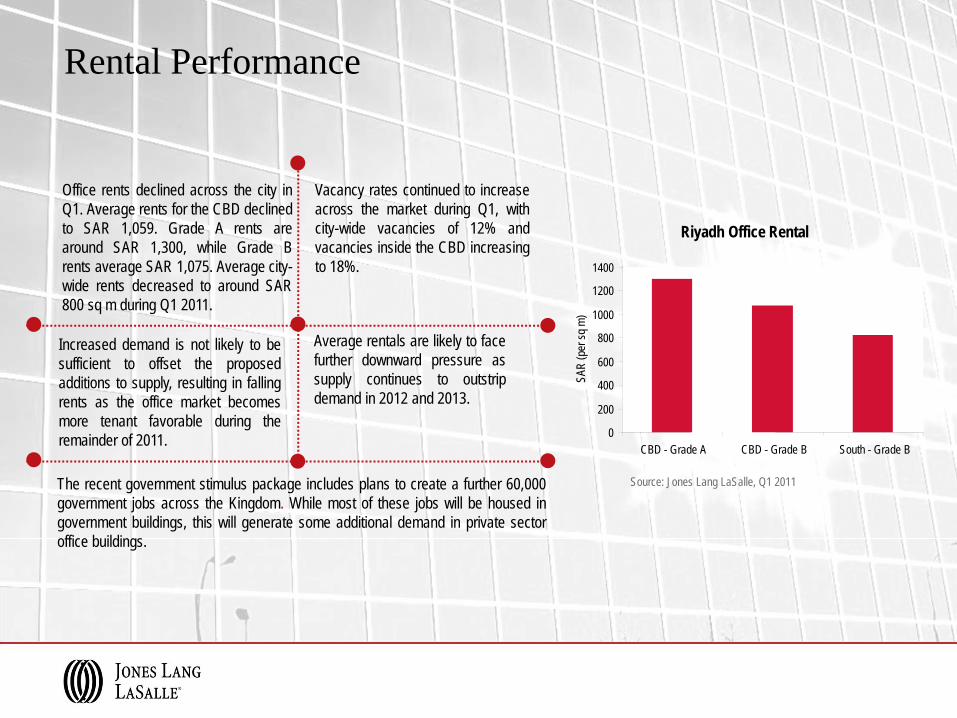

Office rents declined across the city inQ1. Average rents for the CBD declinedto SAR 1,059. Grade A rents arearound SAR 1,300, while Grade Brents average SAR 1,075. Average city-wide rents decreased to around SAR800 sq m during Q1 2011.

Vacancy rates continued to increaseacross the market during Q1, withcity-wide vacancies of 12% andvacancies inside the CBD increasingto 18%.

The recent government stimulus package includes plans to create a further 60,000government jobs across the Kingdom. While most of these jobs will be housed ingovernment buildings, this will generate some additional demand in private sectoroffice buildings.

Increased demand is not likely to besufficient to offset the proposedadditions to supply, resulting in fallingrents as the office market becomesmore tenant favorable during theremainder of 2011.

Average rentals are likely to facefurther downward pressure assupply continues to outstripdemand in 2012 and 2013.

Source: Jones Lang LaSalle, Q1 2011

Riyadh Office Rental

0

200

400

600

800

1000

1200

1400

CBD - Grade A CBD - Grade B South - Grade B

SAR

(per

sq m

)

Indicator Level Comment / Outlook

Current Office Stock 3 million sq m Includes all grades and all locations.

Future Supply (2011–2014) 1.38 million sq m Riyadh market will face a major supply shock when Granada Business Park, KAFD and Olaya Towers complete in 2013 and 2014.

City-wide VacancyCBD Vacancy

12%18%

Average CBD RentalAverage – Citywide Rental

SAR 1,059 sq mSAR 800 sq m

Office Market Summary

10

Riyadh Market Overview

Residential

Key Takeaways – Residential Market

• The total residential stock in Riyadh was around857,800 units according to the National HousingCensus (Aug 2010).

• Vast majority of existing stock is in small schemesrather than those by large, professional developers.

• In Q1 2011, approximately 3,000 units werecompleted within major projects monitored by JLL.

• Around 24,000 units are expected to be completed(across all projects) during 2011.

• Supply figures for 2012 and beyond will increasedue to new projects announced by the Ministry ofHousing.

• Increase in the loan limit of REDF from SAR300,000 to SAR 500,000 will encourage theconstruction of more houses on a DIY basis.

SUPPLY PERFORMANCE

DEMAND

• Major demand for sales market from a growingyoung local population.

• Demand for leasing properties (especiallyapartments and compounds) is driven by theincreasing number of expatriates working in Riyadh.

• Duplexes have become popular among thoseunable to afford a villa but not wanting to live in anapartment.

• There is continued strong demand from both endusers and investors in the compound sector.

• Off plan sales for Rafal and Nasamat Al-Riyadhhave resulted in increased sales activity.

• Villa prices have increased in all areas of Riyadhover the past quarter, driven in part by higherland prices.

• Apartment prices have increased in the East andNorth over the past quarter, while remainingunchanged in the South

• Average apartment rents continued to increase(12% Y-o-Y), with the greatest increase in themiddle and lower end segment.

• Average villa rents have increased by 10%Y-o-Y.

OUTLOOK

• With growing population and increasing number ofexpatriates, demand for housing will continue togrow during 2011 and beyond.

• Demand is particularly robust for middle incomehousing and prices are expected to increase through2011.

• The availability of long term housing finance remainsa key factor in driving demand and prices. Finalapproval of the mortgage law and implementationwill act as a major stimulus to demand.

• Rents are likely to continue their upward trendduring 2011 as new expatriates are entering themarket.

857,764 857,764881,851

909,980

24,087

28,129

29,163

800,000

820,000

840,000

860,000

880,000

900,000

920,000

940,000

960,000

2010 2011 2012 2013

Numb

er of

Unit

s

Completed Stock Future Supply

Source: Jones Lang LaSalle, Q1 2011

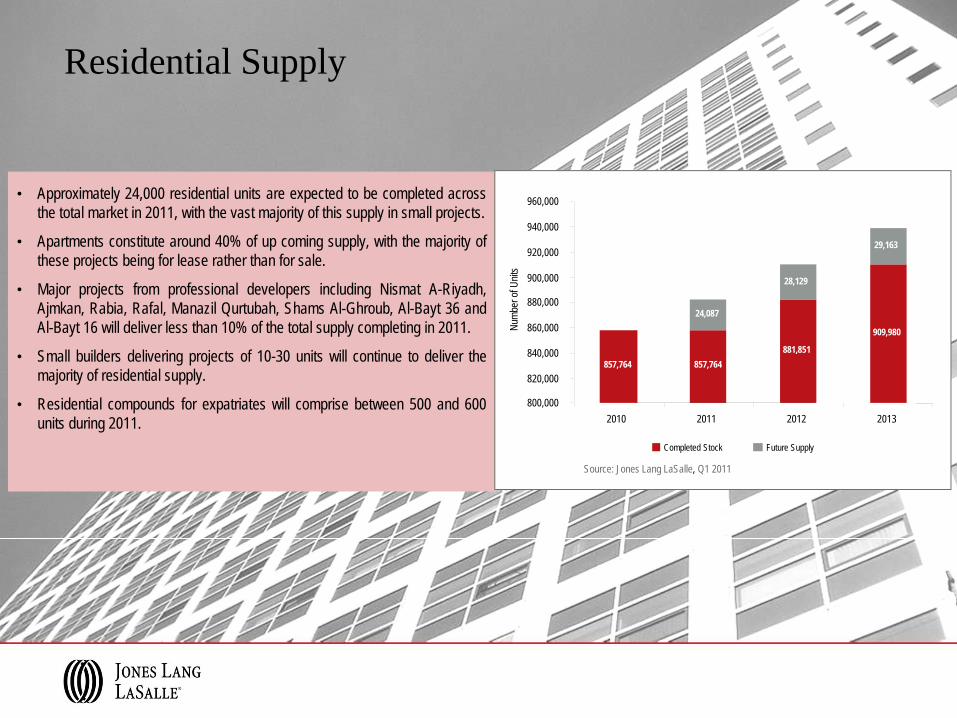

Residential Supply

• Approximately 24,000 residential units are expected to be completed acrossthe total market in 2011, with the vast majority of this supply in small projects.

• Apartments constitute around 40% of up coming supply, with the majority ofthese projects being for lease rather than for sale.

• Major projects from professional developers including Nismat A-Riyadh,Ajmkan, Rabia, Rafal, Manazil Qurtubah, Shams Al-Ghroub, Al-Bayt 36 andAl-Bayt 16 will deliver less than 10% of the total supply completing in 2011.

• Small builders delivering projects of 10-30 units will continue to deliver themajority of residential supply.

• Residential compounds for expatriates will comprise between 500 and 600units during 2011.

Residential Sale Prices

• The average sales price of apartments has increasedduring Q1 2011 in East and North Riyadh, while prices inthe South remained unchanged.

• The average asking price for apartments as at Q1 2011stood at SAR 2,300 per square meter.

• Average villa prices have increased across all districts ofRiyadh during Q1 2011.

• Increasing land prices have played a major role in liftingaverage villa prices to around SAR 3,000 sq m.

• During the last two quarters, investors have shown moreinterest in acquiring residential compounds, but few dealshave been completed due to very high asking prices.

0

500

1,000

1,500

2,000

2,500

3,000

North South East

SAR

per s

q m

Apartment – Average Sales Prices

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

North South East West

SAR pe

r sq m

Source: Jones Lang LaSalle, Q1 2011

Villa – Average Sales Prices

Residential Rentals

• Villa rents increased by 10% in Q1 2011 on a Y-o-Y basis. Rentsfor high end villas in Waroud, Nakheel, Nuzha and Ishbiliah haveincreased more than in other districts.

• Villa rents in residential communities such as Sindad, Palenisaand Al-Qasar are higher than those in surrounding neighborhoods.

• Many of the villas currently available for rent are located in lowerpriced areas such as Wadi Laban and Areja.

• Y-o-Y increase of 12% from Q1 2010 to Q1 2011.

• Rents in low income apartments such as Malaz, Suleimania,and Wazarat continue to grow at higher rates compared toother districts as these areas have low vacancy levels.

• The absence of rental caps means landlords can increaserentals at their discretion. The greatest increases have occurredfor apartments occupied by lower income expatriates.

0100002000030000400005000060000700008000090000

100000

North South East West

Annu

al Re

nt (S

AR)

Villa - Average Annual Rent

0

5000

10000

15000

20000

25000

30000

North South East West

Annu

al Re

nt (S

AR)

Apartment - Average Annual Rent

Mid to high-end villa rents have increased at a rapid rate Low to mid-end apartment rents continue to increase

Source: Jones Lang LaSalle, Q1 2011

Residential Market Summary

16

Indicator Level Comment / Outlook

Current Residential Stock 857,764 units Based on National Housing Census (2010) 40% Apartment, 60%Villas

Future Supply (2011–2012) 52,000 additional units in all projects New stock built by Ministry of Housing may increase this figure.

Average 2 Bed Apartment Rent SAR 26,000 p.a. Apartment rents expected to increase. Further in 2011 due to high demand

Average 2 Bed Apartment Sale Price SAR 2,300 / sq m Increases in lower priced units will increase average.

Average 4 Bed Villa Rent SAR 90,000 p.a. Rents are expected to grow.

Average 4 Bed Villa Sale Price SAR 3,000 / sq m Average price within the range will increase further in 2011.

Riyadh Market Overview

Retail

Key Takeaways – Retail Market

DEMAND

SUPPLY PERFORMANCE

OUTLOOK

• As of Q1 2011, there was a total of 1.07 million sqm of retail space in malls (over 10,000 sq m)across Riyadh.

• No new major mall supply is expected to bereleased during the remainder of 2011. The nextcompletion being the Swaidi Mall in 2012.

• Super regional and regional malls currently accountfor around 61% of total mall based retail space inRiyadh.

• Retail sales continued to increase with the point ofsale transaction values growing 23% during March.

• Retailers are generally aggressive in theirexpansion plans and remain keen to explore newopportunities.

• FG4 and Pottery Barn are two new additions toretailers operating in Riyadh while DQ restaurant isalso fitting out its first outlet.

• Lulu has opened their second outlet in Riyadh.• Further growth in retail sales is likely due to the

recent stimulus package which included salaryincreases for government employees, payment ofone-off bonuses and creation of new governmentsector jobs.

• Average estimated rental values (ERV’s) remainedstable at SAR 2,136 per sq m over Q1 2011.

• Retailers are currently able to negotiate moreeffective lease deals than those previously available.Stepped rental rates and greater incentives for newoutlets are now available in the market.

• Vacancies have remained largely unchanged overQ1 2011, ranging from 0% to over 30%, with anaverage of around 16% in major existing malls.Vacancies are being well disguised in most retailenvironments.

• Average rents are expected to remain stable overthe remainder of 2011 in the absence of anyadditional supply.

• More non performing retail space is likely to beconverted into office space.

• Retail environments catering to the requirements offamilies (particularly children) are expected toperform well.

• The key ingredients for success of these centers willbe good access, ample parking and a strong tenantmix of retailers and restaurants.

Retail Mall Supply

• Approximately 30,000 sq m of retail space wascompleted in Q1 2011, bringing the total supply inmajor retail malls (those over 10,000 sq m in size)across Riyadh to approximately 1.07 million sq m.

• The major completion in Q1 2011 was the RiyadhAvenue Mall on Olaya Street (King Faisal Road),anchored by a Lulu supermarket.

• No further major malls are expected to completeuntil 2012, with the opening of the much delayedSwaidi Mall.

• Total mall based retail supply is expected to reacharound 1.25 million sq m by the end of 2014, withthe completion of a number of small centres andadditions to existing malls.

Riyadh Retail Supply (2010-2013)

1,0731,043 1,073 1,183

61

110

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

2010 2011 2012 2013

Supp

ly ('0

00 sq

m)

Completed Stock Future Supply

Source: Jones Lang LaSalle, Q1 2011

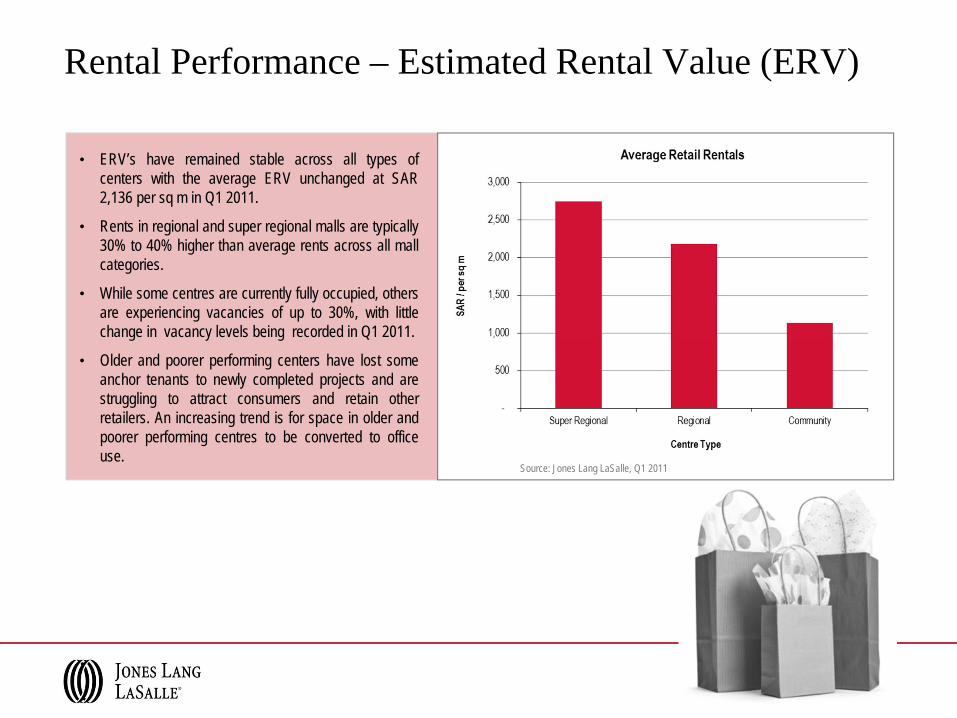

Rental Performance – Estimated Rental Value (ERV)

• ERV’s have remained stable across all types ofcenters with the average ERV unchanged at SAR2,136 per sq m in Q1 2011.

• Rents in regional and super regional malls are typically30% to 40% higher than average rents across all mallcategories.

• While some centres are currently fully occupied, othersare experiencing vacancies of up to 30%, with littlechange in vacancy levels being recorded in Q1 2011.

• Older and poorer performing centers have lost someanchor tenants to newly completed projects and arestruggling to attract consumers and retain otherretailers. An increasing trend is for space in older andpoorer performing centres to be converted to officeuse.

Source: Jones Lang LaSalle, Q1 2011

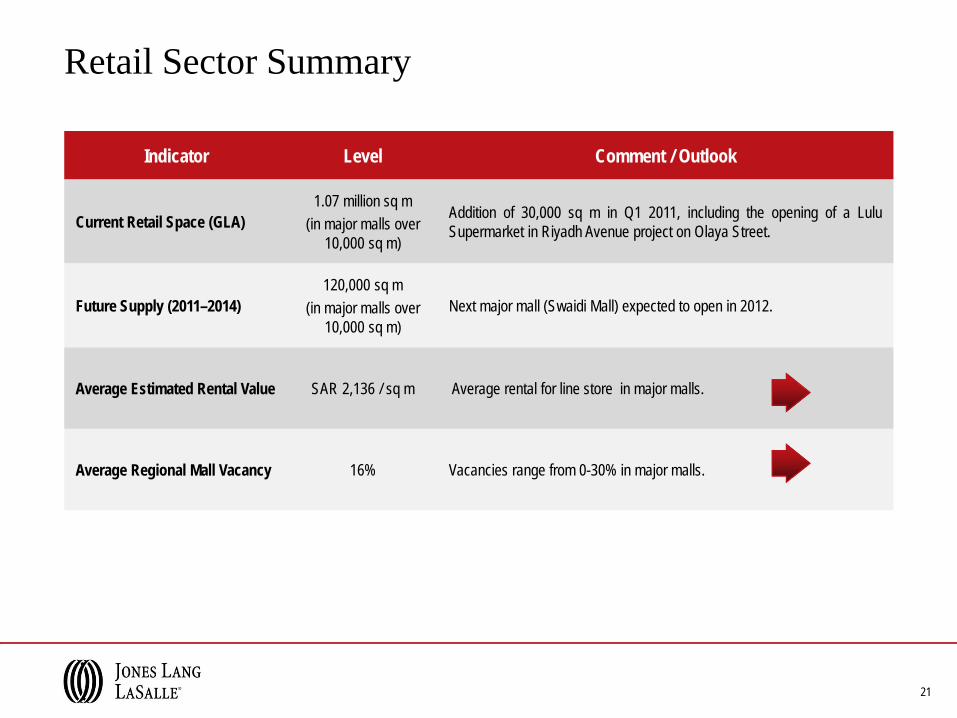

Retail Sector Summary

21

Indicator Level Comment / Outlook

Current Retail Space (GLA)1.07 million sq m

(in major malls over 10,000 sq m)

Addition of 30,000 sq m in Q1 2011, including the opening of a LuluSupermarket in Riyadh Avenue project on Olaya Street.

Future Supply (2011–2014)120,000 sq m

(in major malls over 10,000 sq m)

Next major mall (Swaidi Mall) expected to open in 2012.

Average Estimated Rental Value SAR 2,136 / sq m Average rental for line store in major malls.

Average Regional Mall Vacancy 16% Vacancies range from 0-30% in major malls.

Riyadh Market Overview

Hospitality

Key Takeaways – Hospitality Market

DEMAND

SUPPLY PERFORMANCE

OUTLOOK

• Riyadh has approximately 9,000 rooms and has notwitnessed any notable addition to its hotel supplysince the last quarter of 2009.

• The four and five star segments together account forapproximately 35% of the overall room supply in thecity. A large proportion of these 4 and 5 star hotelsare internationally branded.

• There are currently about 3,000 hotel rooms in thepipeline for the city over the next 3 – 4 years. Thebulk of the supply pipeline is positioned in the 4 and5 star segment.

• The quality hotel segment in Riyadh is drivenprimarily by business travellers and corporateguests.

• The Government sector forms an important sourceof demand for hotel rooms in the city.

• Domestic business guests comprise about 65% ofthe overall room demand in Riyadh.

• While leisure represents a fairly small segment ofcurrent demand in Riyadh, the authorities endeavourto develop the tourism offering.

• In Q1 2011, the Riyadh market moved into therecovery stage of the property cycle.

• Occupancy levels have increased marginallycompared to those reported in the same period of2010.

• The average daily room rate (ADR) also increasedby 3% in Q1 2011.

• A marginal increase in occupancy and the notablerise in ADRs resulted in a 5% growth in RevPARduring Q1 2011 over the same period in 2010.

• Future hotel developments in Riyadh CBD areexpected to induce demand through their offering.

• A major proportion of the future hotel supply formspart of larger mixed use projects. The performanceof these hotels will be highly dependent on that ofthe overall project.

• Summer is traditionally the weakest season for hotelperformance in Riyadh. With Ramadan moving backto August, an earlier recovery can be expected forSeptember and Q4, leading to a stronger annualperformance in 2011.

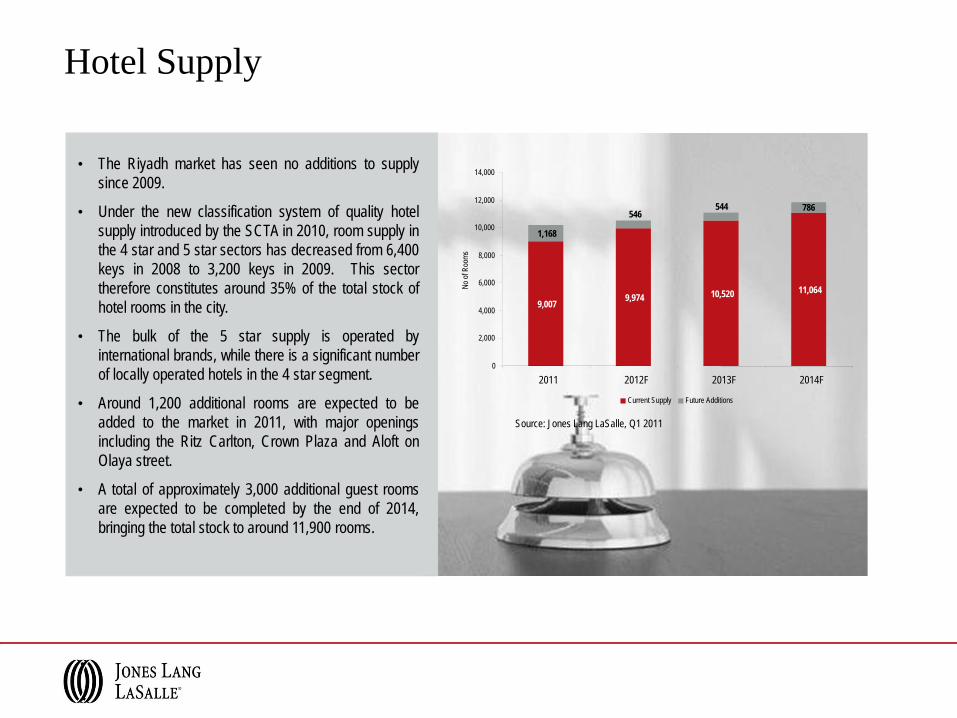

Hotel Supply

• The Riyadh market has seen no additions to supplysince 2009.

• Under the new classification system of quality hotelsupply introduced by the SCTA in 2010, room supply inthe 4 star and 5 star sectors has decreased from 6,400keys in 2008 to 3,200 keys in 2009. This sectortherefore constitutes around 35% of the total stock ofhotel rooms in the city.

• The bulk of the 5 star supply is operated byinternational brands, while there is a significant numberof locally operated hotels in the 4 star segment.

• Around 1,200 additional rooms are expected to beadded to the market in 2011, with major openingsincluding the Ritz Carlton, Crown Plaza and Aloft onOlaya street.

• A total of approximately 3,000 additional guest roomsare expected to be completed by the end of 2014,bringing the total stock to around 11,900 rooms.

9,007 9,974 10,520 11,064

1,168

544 786546

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2011 2012F 2013F 2014F

No of

Roo

ms

Current Supply Future Additions

Source: Jones Lang LaSalle, Q1 2011

Hotel Performance

• Occupancy rates for quality hotels in Riyadh increasedmarginally to 70% during the first quarter of 2011,compared with 69% in Q1 2010.

• This represents a reversal of the previous period ofdeclining occupancy rates, which had fallen from 71%in 2008 to just 60% for the full year of 2010. Thissuggests that business travel to Riyadh has nowstarted to increase again, following the fallsexperienced in the aftermath of the global economiccrisis.

• After average room rates declined - 5% in 2010, thefirst quarter of 2011 saw a 3% rise in average ratesover the same period last year.

• With increased occupancy and ADRs in Q1 2011,RevPAR levels grew to USD 193 and registered a 5%growth over Q1 2010. Source: STR Global

Hotel Market Summary

26

Indicator Level Comment / Outlook

Current Hotel Supply 9,007 rooms There have been no major additions to the Riyadh hotel supply since Q42009.

Future Supply (2011–2014) 3,044 units

While the bulk of the future supply is concentrated in the existing CBD(along King Fahd Road and Olaya Street), new developments such asKing Abdullah Financial District, Granada Centre and Riyadh BusinessGate will add inventory in more peripheral locations

2011 YTD Occupancy 70% Slight increase in YTD levels of occupancy. Positive trend after significantdrop in occupancy levels from 2008.

2011 YTD ADR SAR 1,038 Notable increase in Q1 ADRs, with a marginal increase in occupancydriving up RevPAR levels in the city.

www.joneslanglasalle-mena.comCOPYRIGHT © JONES LANG LASALLE IP, INC. 2011This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the priorwritten consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation ismade, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not acceptany liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Contacts:John HarrisCo-Head, Riyadh [email protected]

Soraka Al KhatibCo-Head, Jeddah [email protected]

David DudleyRegional [email protected]

David MacadamHead of Retail, [email protected]

Chiheb Ben-MahmoudExecutive VP, [email protected]

Craig PlumbHead of Research, [email protected]

Fayyaz AhmadResearch Manager, [email protected]

Diyaa AyoubMarket Intelligence [email protected]