jebel ali free zone fze consolidated financial statements...

TRANSCRIPT

Jebel Ali Free Zone FZE

Consolidated financial statementsfor the year ended 31 December 2016

Jebel Ali Free Zone FZE

Consolidated financial statements for the year ended 31 December 2016

Pages

Independent auditor’s report 1 - 3

Consolidated balance sheet 4

Consolidated statement of comprehensive income 5

Consolidated statement of changes in equity 6

Consolidated statement of cash flows 7

Notes to the consolidated financial statements 8 - 38

PricewaterhouseCoopers (Dubai Branch), License no. 102451Emaar Square, Building 4, Level 8, P O Box 11987, Dubai - United Arab EmiratesT: +971 (0)4 304 3100, F: +971 (0)4 346 9150, www.pwc.com/me

Douglas O’Mahony, Paul Suddaby, Jacques Fakhoury and Mohamed ElBorno are registered as practising auditors with the UAE Ministry of Economy (1)

Independent auditor's report to the shareholder ofJebel Ali Free Zone FZE

Report on the audit of the consolidated financial statements

Our opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, theconsolidated financial position of Jebel Ali Free Zone FZE (the “Establishment”) and itssubsidiaries (together, the “Group”) as at 31 December 2016, and its consolidated financialperformance and its consolidated cash flows for the year then ended in accordance withInternational Financial Reporting Standards (“IFRS”).

What we have audited

The Group’s consolidated financial statements comprise:

• the consolidated balance sheet as at 31 December 2016;• the consolidated statement of comprehensive income for the year then ended;• the consolidated statement of changes in equity for the year then ended;• the consolidated statement of cash flows for the year then ended; and• the notes to the consolidated financial statements, which include a summary of

significant accounting policies and other explanatory information.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (“ISAs”).Our responsibilities under those standards are further described in the Auditor’sresponsibilities for the audit of the consolidated financial statements section of our report.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our opinion.

Independence

We are independent of the Group in accordance with the International Ethics Standards Boardfor Accountants’ Code of Ethics for Professional Accountants (IESBA Code) and the ethicalrequirements that are relevant to our audit of the consolidated financial statements in theUnited Arab Emirates. We have fulfilled our other ethical responsibilities in accordance withthese requirements and the IESBA Code.

(2)

Independent auditor's report to the shareholder ofJebel Ali Free Zone FZE (continued)

Responsibilities of management and those charged with governance for the consolidatedfinancial statements

Management is responsible for the preparation and fair presentation of the consolidatedfinancial statements in accordance with IFRS, and for such internal control as managementdetermines is necessary to enable the preparation of consolidated financial statements that arefree from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessingthe Group’s ability to continue as a going concern, disclosing, as applicable, matters related togoing concern and using the going concern basis of accounting unless management eitherintends to liquidate the Group or to cease operations, or has no realistic alternative but to doso. Those charged with governance are responsible for overseeing the Group’s financialreporting process.

Auditor’s responsibilities for the audit of the consolidated financial statements

Our objectives are to obtain reasonable assurance about whether the consolidated financialstatements as a whole are free from material misstatement, whether due to fraud or error, andto issue an auditor’s report that includes our opinion. Reasonable assurance is a high level ofassurance, but is not a guarantee that an audit conducted in accordance with ISAs will alwaysdetect a material misstatement when it exists. Misstatements can arise from fraud or error andare considered material if, individually or in the aggregate, they could reasonably be expectedto influence the economic decisions of users taken on the basis of these consolidated financialstatements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintainprofessional scepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the consolidated financialstatements, whether due to fraud or error, design and perform audit proceduresresponsive to those risks, and obtain audit evidence that is sufficient and appropriate toprovide a basis for our opinion. The risk of not detecting a material misstatementresulting from fraud is higher than for one resulting from error, as fraud may involvecollusion, forgery, intentional omissions, misrepresentations, or the override of internalcontrol.

• Obtain an understanding of internal control relevant to the audit in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose ofexpressing an opinion on the effectiveness of the Group’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness ofaccounting estimates and related disclosures made by management.

Jebel Ali Free Zone FZE

The notes on pages 8 to 38 form an integral part of these consolidated financial statements. (5)

Consolidated statement of comprehensive income

Year ended 31 December2016 2015

Note AED’000 AED’000

Revenue 18 1,936,519 1,857,356Cost of sales 19 (411,915) (392,063)Gross profit 1,524,604 1,465,293

Other operating income 20 43,282 32,035General and administrative expenses 21 (181,886) (182,549)Selling and marketing expenses 22 (58,222) (57,724)Operating profit 1,327,778 1,257,055

Finance income 24 4,593 15,989Finance costs 24 (176,637) (280,440)Finance costs – net 24 (172,044) (264,451)

Profit and total comprehensive income for the year 1,155,734 992,604

Jebel Ali Free Zone FZE

The notes on pages 8 to 38 form an integral part of these consolidated financial statements. (6)

Consolidated statement of changes in equity

Sharecapital

Retainedearnings Total

AED’000 AED’000 AED’000

Balance at 1 January 2015 4,268,000 3,410,288 7,678,288

Total comprehensive income for the year - 992,604 992,604

Balance at 31 December 2015 4,268,000 4,402,892 8,670,892

Total comprehensive income for the year - 1,155,734 1,155,734

Transaction with shareholderDividend (Note 12) - (734,500) (734,500)

Balance at 31 December 2016 4,268,000 4,824,126 9,092,126

Jebel Ali Free Zone FZE

The notes on pages 8 to 38 form an integral part of these consolidated financial statements. (7)

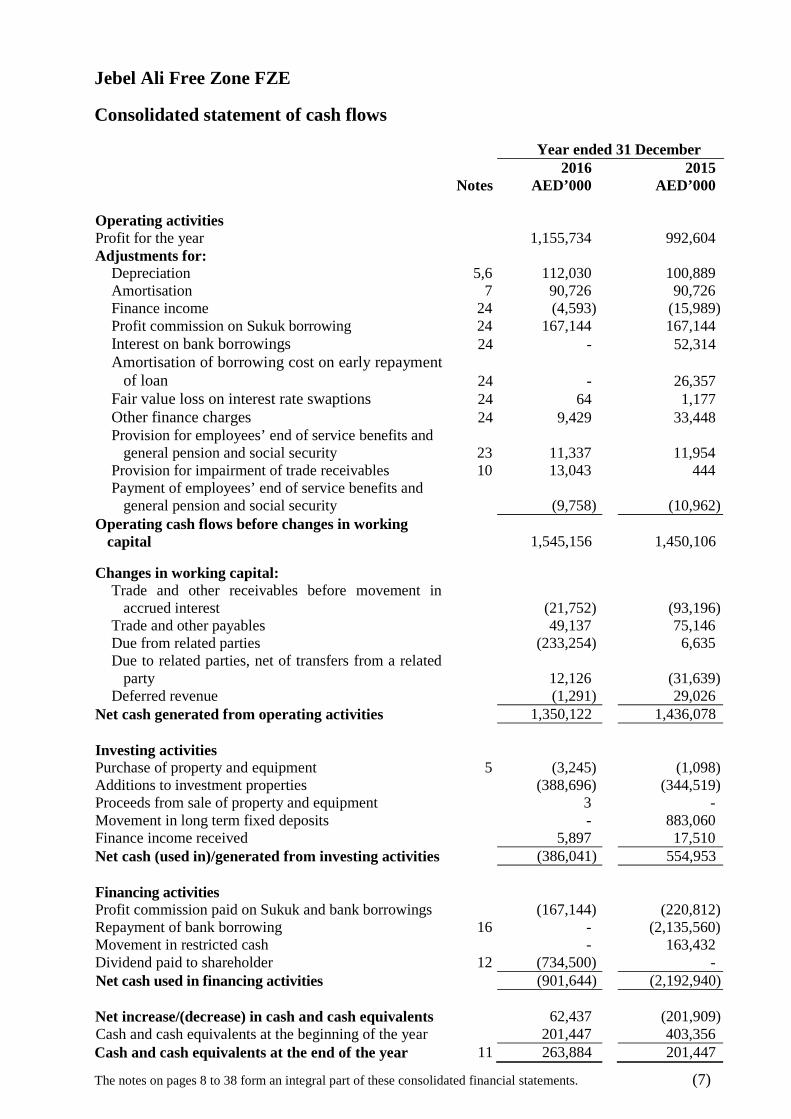

Consolidated statement of cash flows

Year ended 31 December2016 2015

Notes AED’000 AED’000

Operating activitiesProfit for the year 1,155,734 992,604Adjustments for:

Depreciation 5,6 112,030 100,889Amortisation 7 90,726 90,726Finance income 24 (4,593) (15,989)Profit commission on Sukuk borrowing 24 167,144 167,144Interest on bank borrowings 24 - 52,314Amortisation of borrowing cost on early repayment

of loan 24 - 26,357Fair value loss on interest rate swaptions 24 64 1,177Other finance charges 24 9,429 33,448Provision for employees’ end of service benefits and

general pension and social security 23 11,337 11,954Provision for impairment of trade receivables 10 13,043 444Payment of employees’ end of service benefits and

general pension and social security (9,758) (10,962)Operating cash flows before changes in working

capital 1,545,156 1,450,106

Changes in working capital:Trade and other receivables before movement in

accrued interest (21,752) (93,196)Trade and other payables 49,137 75,146Due from related parties (233,254) 6,635Due to related parties, net of transfers from a related

party 12,126 (31,639)Deferred revenue (1,291) 29,026

Net cash generated from operating activities 1,350,122 1,436,078

Investing activitiesPurchase of property and equipment 5 (3,245) (1,098)Additions to investment properties (388,696) (344,519)Proceeds from sale of property and equipment 3 -Movement in long term fixed deposits - 883,060Finance income received 5,897 17,510Net cash (used in)/generated from investing activities (386,041) 554,953

Financing activitiesProfit commission paid on Sukuk and bank borrowings (167,144) (220,812)Repayment of bank borrowing 16 - (2,135,560)Movement in restricted cash - 163,432Dividend paid to shareholder 12 (734,500) -Net cash used in financing activities (901,644) (2,192,940)

Net increase/(decrease) in cash and cash equivalents 62,437 (201,909)Cash and cash equivalents at the beginning of the year 201,447 403,356Cash and cash equivalents at the end of the year 11 263,884 201,447

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016

(8)

1 Legal status and activities

Jebel Ali Free Zone FZE (the “Establishment”) was established as a Jebel Ali Free ZoneEstablishment under registration number 1283 pursuant to Law No 9 of 1992 issued by the Rulerof Dubai and implementing regulations issued by the Jebel Ali Free Zone Authority (“JAFZA”).The Establishment’s registered office is P.O. Box 16888, Jebel Ali, Dubai, United ArabEmirates.

The Establishment and its subsidiary (together, the “Group”) are wholly-owned by EconomicZones World FZE (“EZW”/the “Parent company”).

On 17 March 2015, DP World Limited and its wholly-owned subsidiary, DP World FZE hasacquired 100% shares of the Parent company from Port and Free Zone World FZE (“PFZW”/ the“former intermediate parent”). Accordingly, DP World FZE became the intermediate parentcompany (“DP World”/ the “Intermediate parent”).

The ultimate parent company is Dubai World Corporation (the “Ultimate parent”).

The Establishment develops and manages free zones, develops sells and lease warehouses, andprovide facility management services.

Significant subsidiary Principal activityHolding percentage

2016 2015

United Arab EmiratesJAFZ Sukuk (2019) Limited* Financing (Sukuk borrowing) 100 100

*The Establishment holds 100% beneficial interest in JAFZ Sukuk (2019) Limited, a special-purpose entity incorporated for the execution of AED 2.39 billion Islamic trust certificates (Note14).

On 13 November 2007 and subsequently amended on 22 April 2012, the Establishment enteredinto two agreements with JAFZA, one agreement to acquire a land use right for a period of 99years and another agreement for the purchase of assets. The Establishment paid JAFZA AED 8.9billion and AED 3 billion as consideration for the acquisition of the land use rights and purchaseof assets respectively. Under the land use right agreement, the Group will be liable to payJAFZA a contingent consideration of 2% of revenue (limited to licensing and registrationactivity) earned from the fourth year onward and increases to 50% by the end of the 99th year.

2 Summary of significant accounting policies

The principal accounting policies applied in the preparation of these consolidated financialstatements are set out below. These policies have been consistently applied to all the yearspresented unless otherwise stated.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(9)

2 Summary of significant accounting policies (continued)

2.1 Basis of preparation

The consolidated financial statements of the Establishment have been prepared in accordance withInternational Financial Reporting Standards (“IFRS”) and IFRS interpretations committee (“IFRSIC”) applicable to companies reporting under IFRS. The consolidated financial statements complywith IFRS as issued by the International Accounting Standards Board (“IASB”).

These consolidated financial statements have been prepared under the historical cost convention asmodified by the revaluation of derivative financial instruments.

At 31 December 2016, the current liabilities included deferred revenue amounting to AED 309million (2015: AED 309 million) (Note 15) and customer refundable deposits of AED 698 million(2015: AED 663 million) (Note 17) which is unlikely to require a significant outflow of cashresources in the next 12 months. The Group has a net current assets of AED 262 million as at 31December 2016 (2015: AED 65 million) after adjustment of the deferred revenue and customerrefundable deposits.

The preparation of the consolidated financial statements in conformity with IFRS requires the useof certain critical accounting estimates. It also requires management to exercise its judgement inthe process of applying the Group’s accounting policies. The areas involving a higher degree ofjudgement or complexity, or areas where assumptions and estimates are significant to the financialstatements are disclosed in Note 4.

(a) New standards, amendments and interpretations effective for the financial year beginningafter 1 January 2016 that did not have a material impact on the Group

IAS 1, ‘Presentation of Financial Statements’ (amendment), (effective from 1 January2016);IAS 16, ‘Property, Plant and Equipment’ (amendment), (effective from 1 January 2016);IAS 27, ‘Separate Financial Statements’ (amendment), (effective from 1 January 2016);IAS 28 ‘Investments in associates and joint ventures’ (amendment), (effective from 1January 2016);IAS 38, ‘Intangible Assets (amendment), (effective from 1 January 2016);IFRS 10, ‘Consolidated Financial Statements’ (amendment), (effective from 1 January2016);

There are no other IFRSs or IFRIC interpretations that are effective and would be expected tohave a material impact on the Group.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(10)

2 Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

(b) New and amended standards issued but not effective for the financial year beginning 1January 2016 and not early adopted by the Group

The standards and interpretations that are issued, but not yet effective, up to the date of issuance ofthe Group’s consolidated financial statements are disclosed below. The Group intends to adoptthese standards, if applicable, when they become effective.

IFRS 9 ‘Financial instruments’ (effective annual periods beginning on or after 1 January2018). IFRS 9 addresses the classification, measurement and recognition of financial assetsand financial liabilities. The complete version of IFRS 9 was issued in July 2014. Itreplaces the guidance in IAS 39 that relates to the classification and measurement offinancial instruments. IFRS 9 retains but simplifies the mixed measurement model andestablishes three primary measurement categories for financial assets: amortised cost, fairvalue through other comprehensive income and fair value through profit or loss. The basisof classification depends on the entity’s business model and the contractual cash flowcharacteristics of the financial asset. Investments in equity instruments are required to bemeasured at fair value through profit or loss with the irrevocable option at inception topresent changes in fair value in other comprehensive income with no subsequent recycling.There is now a new expected credit losses model that replaces the incurred loss impairmentmodel used in IAS 39. For financial liabilities there were no changes to classification andmeasurement except for the recognition of changes in own credit risk in othercomprehensive income, for liabilities designated at fair value through profit or loss. IFRS 9relaxes the requirements for hedge effectiveness by replacing the bright line hedgeeffectiveness tests. It requires an economic relationship between the hedged item andhedging instrument and for the ‘hedged ratio’ to be the same as the one managementactually use for risk management purposes. Contemporaneous documentation is stillrequired but is different to that currently prepared under IAS 39. The Group is yet to assessIFRS 9’s full impact.

IFRS 15 ‘Revenue from contracts with customers’ (effective annual periods beginning onor after 1 January 2018). IFRS 15 deals with revenue recognition and establishes principlesfor reporting useful information to users of financial statements about the nature, amount,timing and uncertainty of revenue and cash flows arising from an entity’s contracts withcustomers. Revenue is recognised when a customer obtains control of a good or service andthus has the ability to direct the use and obtain the benefits from the good or service. Thestandard will replace the existing IAS 18 ‘Revenue’ and IAS 11 ‘Construction contracts’and related interpretations.

Amendment to IFRS 15, ‘Revenue from contracts with customers’ (effective annualperiods beginning on or after 1 January 2018). These amendments comprise clarificationsof the guidance on identifying performance obligations, accounting for licences ofintellectual property and the principal versus agent assessment (gross versus net revenuepresentation). New and amended illustrative examples have been added for each of thoseareas of guidance. The IASB has also included additional practical expedients related totransition to the new revenue standard.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(11)

2 Summary of significant accounting policies (continued)

2.1 Basis of preparation (continued)

(b) New and amended standards issued but not effective for the financial year beginning 1January 2016 and not early adopted by the Group (continued)

IFRS 16 ‘Leases’ (effective annual periods beginning on or after 1 January 2019 withearlier application permitted if IFRS 15, ‘Revenue from Contracts with Customers’, is alsoapplied). This standard replaces the current guidance in IAS 17 and is a farreaching changein accounting by lessees in particular.

Under IAS 17, lessees were required to make a distinction between a finance lease (onconsolidated balance sheet) and an operating lease (off consolidated balance sheet). IFRS16 now requires lessees to recognise a lease liability reflecting future lease payments and a‘right-of-use asset’ for virtually all lease contracts. The IASB has included an optionalexemption for certain short-term leases and leases of low-value assets; however, thisexemption can only be applied by lessees.

For lessors, the accounting stays almost the same. However, as the IASB has updated theguidance on the definition of a lease (as well as the guidance on the combination andseparation of contracts), lessors will also be affected by the new standard. At the very least,the new accounting model for lessees is expected to impact negotiations between lessorsand lessees.

Under IFRS 16, a contract is, or contains, a lease if the contract conveys the right to controlthe use of an identified asset for a period of time in exchange for consideration.

IAS Amendments to IAS 7, ‘Statement of cash flows on disclosure initiative consideration’(effective annual periods beginning on or after 1 January 2017). These amendments to IAS7 introduce an additional disclosure that will enable users of financial statements toevaluate changes in liabilities arising from financing activities. The amendment is part ofthe IASB’s Disclosure Initiative, which continues to explore how financial statementdisclosure can be improved.

2.2 Principles of consolidation

(a) Subsidiaries

Subsidiaries are all entities (including structured entities) over which the Group has control. TheGroup controls an entity when the Group is exposed to, or has rights to, variable returns from itsinvolvement with the entity and has the ability to affect those returns through its power over theentity. Subsidiaries are fully consolidated from the date on which control is transferred to theGroup. They are deconsolidated from the date that control ceases.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(12)

2 Summary of significant accounting policies (continued)

2.2 Principles of consolidation (continued)

(a) Subsidiaries (continued)

The Group applies the acquisition method to account for business combinations. The considerationtransferred for the acquisition of a subsidiary is the fair values of the assets transferred, theliabilities incurred to the former owners of the acquiree and the equity interests issued by theGroup. The consideration transferred includes the fair value of any asset or liability resulting froma contingent consideration arrangement. Identifiable assets acquired and liabilities and contingentliabilities assumed in a business combination are measured initially at their fair values at theacquisition date. The Group recognises any non-controlling interest in the acquiree on anacquisition-by-acquisition basis, either at fair value or at the non-controlling interest’sproportionate share of the recognised amounts of acquiree’s identifiable net assets. Acquisition-related costs are expensed as incurred.

If the business combination is achieved in stages, the acquisition date fair value of the acquirer’spreviously held equity interest in the acquiree is remeasured to fair value at the acquisition datethrough profit or loss.

Any contingent consideration to be transferred by the Group is recognised at fair value at theacquisition date. Subsequent changes to the fair value of the contingent consideration that isdeemed to be an asset or liability is recognised in accordance with IAS 39 either in profit or loss oras a change to other comprehensive income. Contingent consideration that is classified as equity isnot remeasured, and its subsequent settlement is accounted for within equity.

(b) Eliminations on consolidation

Inter-company transactions, balances and unrealised gains or losses on transactions betweenGroup companies are eliminated. When necessary amounts reported by subsidiaries have beenadjusted to conform with the Group’s accounting policies.

2.3 Foreign currency translation

(a) Functional and presentation currency

Items included in the financial statements of each of the Group’s entities are measured using thecurrency of the primary economic environment in which the entity operates (‘the functionalcurrency’). The consolidated financial statements are presented in United Arab Emirates Dirham(“AED”), which is the Group’s functional and presentation currency.

(b) Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange ratesprevailing at the dates of the transactions or valuation where items are re-measured. Foreignexchange gains and losses resulting from the settlement of such transactions and from thetranslation at year-end exchange rates of monetary assets and liabilities denominated in foreigncurrencies are recognised in the consolidated statement of comprehensive income, except whendeferred in other comprehensive income as qualifying cash flow hedges.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(13)

2 Summary of significant accounting policies (continued)

2.3 Foreign currency translation (continued)

(b) Transactions and balances (continued)

Balances and transactions denominated in US dollars (“USD”) have been translated into thepresentation currency at a fixed rate as the exchange rate of AED to USD has been pegged since1981.

2.4 Property and equipment

Property and equipment are stated at historical cost less accumulated depreciation. Historical costincludes expenditures that are directly attributable to the acquisition of the asset.

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, asappropriate, only when it is probable that future economic benefits associated with the item willflow to the Group and the cost of the item can be measured reliably. The carrying amount of thereplaced part is derecognised. All other repairs and maintenance are charged to the statement ofcomprehensive income during the financial period in which they are incurred.

Depreciation is calculated using the straight-line method to allocate their cost to their residualvalues over their estimated useful lives, as follows:

YearsMotor and utility vehicles 5-10Furniture and fixtures 5-10Equipment 3-5

The assets’ residual values, useful lives and methods of depreciation, are reviewed and adjustedif appropriate at each financial year end.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’scarrying amount is greater than its estimated recoverable amount.

Gains and losses on disposals are determined by comparing the proceeds with the carryingamount and are recognised within the statement of comprehensive income.

Capital work-in-progress is stated at cost. When commissioned, capital work-in-progress istransferred to the appropriate category of property and equipment and depreciated in accordancewith the Group’s policy.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(14)

2 Summary of significant accounting policies (continued)

2.5 Investment properties

Property that is held for long-term rental yields or for capital appreciation or both, and that is notoccupied by the companies in the consolidated Group, is classified as investment property.Investment property also includes property that is being constructed or developed for future useas investment property.

Investment property is measured initially at its cost, including related transaction costs andwhere applicable borrowing costs. After initial recognition, investment property is carried at costless accumulated depreciation and impairment, if any.

The fair value for disclosure purposes of the investment property is based on active marketprices, adjusted, if necessary, for any difference in the nature, location or condition of thespecific asset. If this information is not available, the Group uses alternative valuation methods,such as recent prices on less active markets or discounted cash flow projections. Valuations areperformed as of the financial position date by an external valuer who hold recognised andrelevant professional qualifications and have recent experience in the location and category ofthe investment property being valued.

Subsequent expenditure is capitalised to the asset’s carrying amount only when it is probable thatfuture economic benefits associated with the expenditure will flow to the Group and the cost ofthe item can be measured reliably. All other repairs and maintenance costs are expensed whenincurred. When part of an investment property is replaced, the carrying amount of the replacedpart is derecognised.

When investment property is sold, gains and losses on disposal are determined by reference to itscarrying amount and are taken into account in determining operating profit.

Investment property under construction is not depreciated until such time as the relevant assetsare completed and commissioned.

Depreciation is calculated using the straight-line method to allocate their cost to their residualvalues over their estimated useful lives, as follows:

YearsBuildings 20-45Infrastructure 5-50

The useful lives and depreciation method are reviewed periodically to ensure that the methodand period of depreciation are consistent with the expected pattern of economic benefits fromthese assets.

2.6 Land use right

The total cost of acquiring land use right is capitalised as a land use right asset and is carried atcost less accumulated amortisation and impairment, if any. Amortisation is calculated using thestraight-line method to allocate the cost over the term of rights of 99 years that is included under‘cost of sales’ in the statement of comprehensive income.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(15)

2 Summary of significant accounting policies (continued)

2.7 Impairment of non-financial assets

Non-financial assets that are subject to amortisation are reviewed for impairment whenever eventsor changes in circumstances indicate that the carrying amount may not be recoverable. Animpairment loss is recognised for the amount by which the asset’s carrying amount exceeds itsrecoverable amount. The recoverable amount is the higher of an asset’s fair value less costs ofdisposal and value in use. For the purposes of assessing impairment, assets are grouped at thelowest levels for which there are separately identifiable cash inflows which are largely independentof the cash inflows from other assets or groups of assets (cash-generating units).

Non-financial assets that suffered an impairment are reviewed for possible reversal of theimpairment at the end of each reporting period. A reversal of an impairment loss for an asset isrecognised immediately in the consolidated statement of comprehensive income under ‘otheroperating income’.

After a reversal of an impairment loss is recognised, the depreciation/amortisation charge of theasset shall be adjusted in future period to allocate the asset’s revised carrying amount, less residualvalue, over the remaining useful life.

2.8 Financial assets

2.8.1 Classification

The Group classifies its financial assets as loans and receivables or as derivatives. Theclassification depends on the purpose for which the financial assets were acquired. Managementdetermines the classification of its financial assets at initial recognition.

Loans and receivables are non-derivative financial assets with fixed or determinable paymentsthat are not quoted in an active market. They are included in current assets, except for maturitiesgreater than 12 months after the end of the reporting period. These are classified as non-currentassets. The Group’s loans and receivables comprise ‘due from related parties’, ‘trade and otherreceivables’ and ‘cash and cash equivalents’ in the consolidated balance sheet (Notes 8, 10 and11).

Derivatives are categorised as held for trading unless they are designated as hedges. Assets in thiscategory are classified as current assets if expected to be settled within 12 months, otherwise theyare classified as non-current.

2.8.2 Recognition and measurement

Regular purchases and sales of financial assets are recognised on the “trade-date” – the date onwhich the Group commits to purchase or sell the asset. Investments are initially recognised atfair value plus transaction costs for all financial assets not carried at fair value through profit orloss. Financial assets are derecognised when the rights to receive cash flows from theinvestments have expired or have been transferred and the Group has transferred substantially allrisks and rewards of ownership.

Loans and receivables are subsequently carried at amortised cost using the effective interestmethod.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(16)

2 Summary of significant accounting policies (continued)

2.9 Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the consolidated balancesheet when there is a legally enforceable right to offset the recognised amounts and there is anintention to settle on a net basis or realise the asset and settle the liability simultaneously.

2.10 Impairment of financial assets

Assets carried at amortised cost

The Group assesses at the end of each reporting period whether there is objective evidence that afinancial asset or Group of financial assets is impaired. A financial asset or a Group of financialassets is impaired and impairment losses are incurred only if there is objective evidence ofimpairment as a result of one or more events that occurred after the initial recognition of theasset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cashflows of the financial asset or Group of financial assets that can be reliably estimated.

Evidence of impairment may include indications that the debtors or a Group of debtors isexperiencing significant financial difficulty, default or delinquency in interest or principalpayments, the probability that they will enter bankruptcy or other financial reorganisation, andwhere observable data indicate that there is a measurable decrease in the estimated future cashflows, such as changes in arrears or economic conditions that correlate with defaults.

For loans and receivables category, the amount of the loss is measured as the difference betweenthe asset’s carrying amount and the present value of estimated future cash flows (excludingfuture credit losses that have not been incurred) discounted at the financial asset’s originaleffective interest rate. The carrying amount of the asset is reduced and the amount of the loss isrecognised in the consolidated statement of comprehensive income. If a loan has a variableinterest rate, the discount rate for measuring any impairment loss is the current effective interestrate determined under the contract. As a practical expedient, the Group may measure impairmenton the basis of an instrument’s fair value using an observable market price.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can berelated objectively to an event occurring after the impairment was recognised (such as animprovement in the debtor’s credit rating), the reversal of the previously recognised impairmentloss is recognised in the consolidated statement of comprehensive income.

2.11 Derivative financial instruments and hedging activities

Derivatives are initially recognised at fair value on the date a derivative contract is entered intoand are subsequently re-measured at their fair value. The method of recognising the resultinggain or loss depends on whether the derivative is designated as a hedging instrument, and if so,the nature of the item being hedged. The Group designates its derivatives as hedges of aparticular risk associated with a recognised asset or liability or a highly probable forecasttransaction (cash flow hedge).

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(17)

2 Summary of significant accounting policies (continued)

2.11 Derivative financial instruments and hedging activities (continued)

The Group documents at the inception of the transaction the relationship between hedginginstruments and hedged items, as well as its risk management objectives and strategy forundertaking various hedging transactions. The Group also documents its assessment, both athedge inception and on an ongoing basis, of whether the derivatives that are used in hedgingtransactions are highly effective in offsetting changes in fair values or cash flows of hedgeditems. A hedge of the foreign currency risk of a firm commitment is accounted for as a cash flowhedge.

The full fair value of a hedging derivative is classified as a non-current asset or liability when theremaining hedged item is more than 12 months, and as a current asset or liability when theremaining maturity of the hedged item is less than 12 months. Trading derivatives are classifiedas a current asset or liability.

The effective portion of changes in the fair value of derivatives that are designated and qualify ascash flow hedges is recognised in other comprehensive income. The gain or loss relating to theineffective portion is recognised immediately in the statement of comprehensive income.

Amounts accumulated in equity are reclassified to profit or loss in the periods when the hedgeditem affects profit or loss (for example, when the forecast sale that is hedged takes place). Thegain or loss relating to the effective portion of interest rate swaps hedging variable rateborrowings is recognised in the consolidated statement of comprehensive income within ‘Financecost - net’. However, when the forecast transaction that is hedged, results in the recognition of anon-financial asset (for example, inventory or fixed assets), the gains and losses previouslydeferred in equity are transferred from equity and included in the initial measurement of the costof the asset. The deferred amounts are ultimately recognised in cost of goods sold in the case ofinventory or in depreciation in the case of fixed assets.

When a hedging instrument expires or is sold, or when a hedge no longer meets the criteria forhedge accounting, any cumulative gain or loss existing in equity at that time remains in equityand is recognised when the forecast transaction is ultimately recognised in the statement ofcomprehensive income. When a forecast transaction is no longer expected to occur, thecumulative gain or loss that was reported in equity is immediately transferred to the statement ofcomprehensive income within ‘other gains/ (losses) – net’.

2.12 Trade receivables

Trade receivables are amounts due from customers for properties sold or services performed in theordinary course of business. If collection is expected in one year or less (or in the normal operatingcycle of the business if longer), they are classified as current assets. If not, they are presented asnon-current assets.

Trade receivables are recognised initially at fair value and subsequently measured at amortised costusing the effective interest method, less provision for impairment.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(18)

2 Summary of significant accounting policies (continued)

2.13 Cash and cash equivalents

Cash and cash equivalents includes cash in hand, deposits held at call with banks, other short-term highly liquid investments with original maturities of three months or less.

2.14 Share capital

Ordinary shares are classified as equity.

2.15 Dividend distribution

Dividend distribution to the Establishment’s shareholder is recognised as a liability in theGroup’s consolidated financial statements in the period in which the dividends are approved bythe Establishment’s shareholder.

2.16 Trade payables

Trade payables are obligations to pay for goods or services that have been acquired in theordinary course of business from suppliers. Trade payables are classified as current liabilities ifpayment is due within one year or less (or in the normal operating cycle of the business iflonger). If not, they are presented as non-current liabilities. Trade payables are recognisedinitially at fair value and subsequently measured at amortised cost using the effective interestmethod.

2.17 Advances from customers

Instalments received from buyers for sales of warehouses and/or service prior to meeting therevenue recognition criteria, are recognised as advances from customers. These are considered acurrent liability as they are repayable on demand on cancellation of the contracts, subject tocertain penalties.

2.18 Borrowings

Borrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings aresubsequently carried at amortised cost; any difference between the proceeds (net of transactioncosts) and the redemption value is recognised in the statement of comprehensive income over theperiod of the borrowings using the effective interest method.

Fees paid on the establishment of loan facilities are recognised as transaction costs of the loan tothe extent that it is probable that some or all of the facility will be drawn down. In this case, thefee is deferred until the draw down occurs. To the extent there is no evidence that it is probablethat some or all of the facility will be drawn down, the fee is capitalised as a pre-payment forliquidity services and amortised over the period of the facility to which it relates.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(19)

2 Summary of significant accounting policies (continued)

2.19 Borrowing costs

General and specific borrowing costs directly attributable to the acquisition, construction orproduction of qualifying assets, which are assets that necessarily take a substantial period of timeto get ready for their intended use or sale, are added to the cost of those assets, until such time asthe assets are substantially ready for their intended use or sale.

Investment income earned on the temporary investment of specific borrowings pending theirexpenditure on qualifying assets is deducted from the borrowing costs eligible for capitalisation.All other borrowing costs are recognised in the consolidated statement of income in the period inwhich they are incurred.

2.20 Employee benefits

(a) End of service benefits to non-UAE nationals – Defined benefit plan

An accrual is made for employees employed in the UAE for estimated liability for employees’entitlement to annual leave as a result of services rendered by the employees up to theconsolidated balance sheet date. Provision is made, using actuarial techniques, for the fullamount of end of service benefits due to the non-UAE Nationals in accordance with the Grouppolicy and UAE labour law, for their periods of service up to the consolidated balance sheet date.The accrual relating to annual leave and leave passage is disclosed as a current liability, whilethe provision relating to end of service benefits is disclosed as a non-current liability.

(b) General pension and social security – Defined contribution plan

The Group joined a pension scheme on 6 March 2006, the date of the Establishment’sincorporation. Any employee transferred from JAFZA will continue their pension scheme withthe Establishment. The scheme is a defined contribution plan, operated by the Federal GeneralPension and Social Security Authority. Contributions for eligible UAE National employees aremade and charged to the statement of comprehensive income, in accordance with the provisionsof Federal Law No. 7 for 1999 relating to Pension and Social Security Law.

2.21 Provisions

Provisions are recognised when the Group has a present legal or constructive obligation as aresult of past events, where it is probable that an outflow of resources embodying economicbenefits will be required to settle the obligation, and a reliable estimate of the amount can bemade. Provisions are not recognised for future operating losses.

Where there are a number of similar obligations, the likelihood that an outflow will be requiredin settlement is determined by considering the class of obligations as a whole. A provision isrecognised even if the likelihood of an outflow with respect to any one item included in the sameclass of obligation may be small.

Provisions are measured at the present value of the expenditures expected to be required to settlethe obligation using a pre-tax rate that reflects current market assessments of the time value ofmoney and risks specific to the obligation. Increases in provisions due to the passage of time arerecognised as interest expense.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(20)

2 Summary of significant accounting policies (continued)

2.22 Revenue recognition

Revenue is measured at the fair value of the consideration received or receivable. The Grouprecognises revenue when the amount of revenue can be reliably measured; when it is probablethat future economic benefits will flow to the entity; and when specific criteria have been met foreach of the Group’s activities, as described below.

(a) Lease rental

Lease rental is recognised on a straight line basis over the lease term. Where the considerationfor the lease is received for subsequent periods, the attributable amount of revenue is deferredand recognised in the subsequent period. Unrecognised revenue is classified as deferred revenueunder liabilities in the consolidated balance sheet.

(b) Administrative services

Revenue from license, registration administration and consultancy service are recognised as theservice is provided.

(c) Other operating income

Other operating income is recognised when the service is provided and right to receive paymentis established.

2.23 Interest income

Interest income is recognised using the effective interest method. When a loan and receivable isimpaired, the Group reduces the carrying amount to its recoverable amount, being the estimatedfuture cash flow discounted at the original effective interest rate of the instrument, and continuesunwinding the discount as interest income. Interest income on impaired loan and receivables isrecognised using the original effective interest rate

2.24 Segment information

The Group is managed as a single business unit and its assets are located in Jebel Ali Free Zone,Dubai, United Arab Emirates. The Chief Executive Officer (“CEO”) is the Group’s chiefoperating decision-maker. Management has determined the operating segments based on theinformation reviewed by the CEO for the purposes of allocating resources and assessingperformance. The CEO considers the business from a service perspective only as the business isgeographically carried out in United Arab Emirates. Apart from lease rental, all other activitiessuch as administrative services and license and registration do not meet the quantitative thresholdrequired by IFRS 8. Accordingly, management has determined that the business is one reportablesegment based on the information reviewed by the Chief Executive Officer for the purposes ofallocating resources and assessing performance.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(21)

3 Financial risk management

3.1 Financial risk factors

The Group’s activities expose it to a variety of financial risks: market risk (including foreignexchange risk, price risk, and cash flow and fair value interest rate risk), credit risk and liquidityrisk. The Group’s overall risk management programme focuses on the unpredictability offinancial markets and seeks to minimise potential adverse effects on the Group’s financialperformance. The Group uses derivative financial instruments to hedge certain risk exposures.

(a) Market risk

(i) Foreign exchange risk

The Group does not have any significant foreign currency exposure, as the majority of itstransactions are denominated in United Arab Emirates Dirham (“AED”).

(ii) Price risk

The Group is not exposed to equity securities or commodity price risk.

(iii) Cash flow and fair value interest rate risk

The Group’s interest rate risk arises from Sukuk borrowing and bank borrowings denominated inAED. Borrowings issued at variable rates expose the Group to cash flow interest rate risk whichis partially offset by cash held at variable rates. Borrowings issued at fixed rates expose theGroup to fair value interest rate risk. The Group management did not set ratio of variable rateborrowings to fixed rate borrowings.

The Group manages its cash flow interest rate risk by using floating-to-fixed interest rateswaption agreements (Note 9). Such interest rate swaptions have the economic effect ofconverting borrowings from floating rates to fixed rates. The Group raised long-term borrowingsat floating rates and should partially purchase swaptions to fixed rates as per terms of the bankborrowing agreement. Under these agreement, the Group has the right but not the obligation onother parties to exchange, at specified intervals (primarily quarterly), the difference betweenfixed contract amounts and floating-rate interest amounts calculated in reference to the agreednotional amounts.

Bank borrowings was settled on 21 December 2015. As at 31 December 2016 and 31 December2015, the Group has no outstanding term facility issued at variable rate and consequently is notexposed to cash flow interest rate risk.

Sukuk borrowings issued at fixed rates expose the Group to fair value interest rate risk. As at 31December 2016, if the interest rate on the of Sukuk borrowing of AED 2,387,320,000 (2015:AED 2,387,320,000) had been 1% higher/lower with all other variables held constant, profit forthe year would have been AED 23,873,200 (2015: AED 23,873,200) lower/higher, mainly as aresult of higher/lower fair value of Sukuk borrowing.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(22)

3 Financial risk management (continued)

3.1 Financial risk factors (continued)

(b) Credit risk

Credit risk is the risk that one party to a financial instrument will cause a financial loss to theother party by failing to discharge an obligation. The Group has no significant concentrations ofcredit risk. Credit risk arises from related party receivables, derivative financial instruments,trade receivables including rental receivables from lessees and cash and cash equivalents held atbanks and (Note 8, 9, 10 and 11 respectively). Credit risk is managed on a Group basis. TheGroup has policies in place to ensure that rental contracts are entered into only with lessees withan appropriate credit history. The Group’s maximum exposure to credit risk to customer isdisclosed in Note 10. Derivative assets and bank deposits are limited to high-credit-qualityfinancial institutions. The table below excludes cash on hand as at 31 December 2016 amountingto AED 225,000 (2015: AED 225,000) and presents an analysis of cash and cash equivalents byrating agency designation at the end of reporting period based on Moody's ratings or itsequivalent for the main banking relationships:

2016 2015AED’000 AED’000

A1 61 7,872A2 3,057 169,861A3 19,265 7,933Aa3 86 -B2 - 5,814Ba2 - 1,600Ba3 - 213Baa1 241,138 7,849Baa2 52 80

263,659 201,222

(c) Liquidity risk

Prudent liquidity risk management implies maintaining sufficient cash and the availability offunding through an adequate amount of credit facilities. Due to the dynamic nature of theunderlying business, the Group maintains flexibility in funding by keeping credit lines available.

The table below analyses the Group’s financial liabilities into relevant maturity based on theremaining period at the consolidated balance sheet to the contractual maturity date. The amountsdisclosed in the table are the contractual undiscounted cash flows. Balances due within 12months equal their carrying balances as the impact of discounting is not significant.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(23)

3 Financial risk management (continued)

3.1 Financial risk factors (continued)

(c) Liquidity risk (continued)

Less than1 year

Between1 year and

2 years

Between2 years and

5 years TotalAED’000 AED’000 AED’000 AED’000

At 31 December 2016Sukuk borrowing 167,144 167,144 2,470,892 2,805,180Trade and other payables (excluding

advances from customers) (Note 17) 944,320 - - 944,320Due to related parties (Note 8) 32,226 - - 32,226

1,143,690 167,144 2,470,892 3,781,726

At 31 December 2015Sukuk borrowing 167,144 167,144 2,638,036 2,972,324Trade and other payables (excluding

advances from customers) (Note 17) 896,207 - - 896,207Due to related parties (Note 8) 19,037 - - 19,037

1,082,388 167,144 2,638,036 3,887,568

3.2 Capital management

The Group’s objectives when managing capital are to safeguard the Group’s ability to continueas a going concern in order to provide returns to the shareholder and to maintain an optimalcapital structure to reduce the cost of capital. In order to maintain or adjust the capital structure,the Group may adjust the amount of profit distributable to the shareholder or manage its workingcapital requirements. Consistent with others in the industry, the Group monitors capital on thebasis of the gearing ratio. This ratio is calculated as net debt divided by total capital. Net debt iscalculated as total borrowings (gross of transaction costs) less cash and cash equivalents. Totalcapital is calculated as ‘Total equity’ as shown in the consolidated balance sheet plus net debt.

The gearing ratios at 31 December 2016 and 2015 were as follows:2016 2015

AED’000 AED’000

Sukuk borrowing (Note 14) 2,387,320 2,387,320Less: Cash and cash equivalents (Note 11) (263,884) (201,447)Net debt 2,123,436 2,185,873Total equity 9,092,126 8,670,892Total capital 11,215,562 10,856,765

Gearing ratio 19% 20%

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(24)

3 Financial risk management (continued)

3.3 Fair value estimation

The table below analyses financial instruments carried at fair value, by valuation method. Thedifferent levels have been defined as follows:

Quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1).Inputs other than quoted prices included within level 1 that are observable for the asset orliability, either directly (that is, as prices) or indirectly (that is, derived from prices) (Level2)Inputs for the asset or liability that are not based on observable market data (that is,unobservable inputs) (Level 3).

There are no assets and liabilities measured at fair value at 31 December 2016.

The following table presents the Group’s assets measured at fair value at 31 December 2015.

Level 1 Level 2 Level 3 TotalAED’000 AED’000 AED’000 AED’000

Derivative financial instruments (Note 9) - 1,500 - 1,500

4 Critical accounting estimates and judgements

Estimates and judgements are continually evaluated and are based on historical experience andother factors, including expectations of future events that are believed to be reasonable under thecircumstances.

The Group makes estimates and assumptions concerning the future. The resulting accountingestimates will, by definition, seldom equal the related actual results. The estimates andassumptions that have a significant risk of causing a material adjustment to the carrying amountsof assets and liabilities within the next financial year are addressed below.

Impairment of non-financial assets

Impairment of non-financial assets is a key area involving management judgement, requiringassessment as to whether the carrying value of assets can be supported by the net present valueof future cash flows derived from such assets using cash flow projections which have beendiscounted at an appropriate rate.

In calculating the net present value of the future cash flows for investment properties andinvestment properties under construction of Jafza One project, certain assumptions are requiredto be made in respect of the impairment reviews. The key assumptions on which managementhas based its cash flow projections when determining the recoverable amount of the assets are asfollows:

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(25)

4 Critical accounting estimates and judgements (continued)

For office towers:o Management’s projections have been prepared on the basis of strategic plans,

knowledge of the market, and management’s views on achievable growth inmarket share over the long term period of ten years;

o Completion date for the office towers within February 2017 to October 2017 foran amount capped with contractors;

o Stabilised occupancy for office towers within 24 to 57 months; ando Capitalisation rate of 9%

For other project facilities:o Average delegate and daily rate and ticket price; ando Discount rate of 13% based on the Group’s weighted average cost of capital with a

risk premium reflecting the relative risks in the markets in which the businessesoperate.

At 31 December 2016 and 2015 no impairment has been recognised against investmentproperties under construction (Note 6).

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(26)

5 Property and equipment

Motor andutility

vehiclesFurniture

and fixtures Equipment

Capitalwork-in-progress Total

AED’000 AED’000 AED’000 AED’000 AED’000CostAt 1 January 2015 44 55,842 25,094 - 80,980Additions - - - 1,098 1,098Transfer - 1,795 163 (1,958) -Transfer from a related

party (Note 8) - 9,904 25 860 10,789At 31 December 2015 44 67,541 25,282 - 92,867Additions - 1,409 213 1,623 3,245Transfer - 1,472 151 (1,623) -Disposals - (104) (10) - (114)Transferred from a

related party (Note 8) - 914 110 - 1,024

At 31 December 2016 44 71,232 25,746 - 97,022

Accumulateddepreciation

At 1 January 2015 44 51,080 24,817 - 75,941Charge for the year - 3,626 191 - 3,817Transfer from a related

party (Note 8) - 8,292 17 - 8,309At 31 December 2015 44 62,998 25,025 - 88,067Charge for the year - 2,859 493 - 3,352Disposals - (101) (10) - (111)

At 31 December 2016 44 65,756 25,508 - 91,308

Net book amountAt 31 December 2016 - 5,476 238 - 5,714

At 31 December 2015 - 4,543 257 - 4,800

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(27)

6 Investment properties

Buildings andInfrastructure

Investmentproperties

underconstruction Total

AED’000 AED’000 AED’000CostAt 1 January 2015 3,491,446 966,682 4,458,128Additions - 395,507 395,507Transfers 711,957 (711,957) -At 31 December 2015 4,203,403 650,232 4,853,635Additions - 464,813 464,813Transfer 326,574 (326,574) -Transfer from a related party (Note 8) - 39 39At 31 December 2016 4,529,977 788,510 5,318,487

Accumulated depreciationAt 1 January 2015 998,984 10,269 1,009,253Charge for the year (Note 19) 97,072 - 97,072At 31 December 2015 1,096,056 10,269 1,106,325Charge for the year (Note 19) 108,678 - 108,678At 31 December 2016 1,204,734 10,269 1,215,003

Net book amountAt 31 December 2016 3,325,243 778,241 4,103,484

At 31 December 2015 3,107,347 639,963 3,747,310

The following amounts have been recognised in the consolidated statement of comprehensiveincome in respect of investment properties:

2016 2015AED’000 AED’000

Lease rental income (Note 18) 1,665,476 1,591,006Direct operating expenses 184,864 171,352

At 31 December 2016, the Group had capital commitment of AED 295,339,000 (2015: AED693,741,000).

Management has provided, for each class of property, assumptions made in the determination offair values and other key information on the properties. Management believes that theseinformation are beneficial in evaluating the fair values of the investment properties.

Level 2 TotalAED’000 AED’000

Buildings and infrastructure 6,911,098 6,911,098Investment properties under construction 778,241 778,241Total 7,689,339 7,689,339

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(28)

6 Investment properties (continued)

On an annual basis, the Group engages external, independent and qualified valuers to determinethe fair value of the Group’s investment properties.

The external valuations of the Level 2 investment properties have been performed using incomecapitalisation and residual method of valuation. The external valuers, in discussion with theGroup’s management, have determined these inputs based on the current lease rates, specificconditions and comparable rentals in the corresponding market.

Valuation techniques underlying management’s estimation of fair value

‘Capitalisation/discounted cash flow method’ involves determination of the value of theinvestment property by calculating the net present value of expected future earnings. Thesignificant inputs into this valuation approach are the future rental cash inflows, growth rates,discount rates and capitalisation rates. The valuation method adopted for these properties isbased on inputs that are not based on observable market data (that is, observable inputs - Level2).

‘Residual price method’ involves determination of the net present value of forecasted cashflowsof a project development on the respective plots of land; reduced by the estimated constructionand other costs to completion that would be incurred by a market participant. The significantinputs into this valuation approach are the estimated selling prices, costs to complete anddevelopers’ margins, discount rates and capitalisation rates (that is, observable inputs - Level 2).

The Group’s investment properties are all based in Dubai and a significant portion has beenleased out.

The significant unobservable inputs used in the fair value measurement categorised within Level2 of the fair value hierarchy of the entity's portfolios of investment properties are:

Market rental value (per sqm per annum);Rent growth per annum;Historical and estimated long term occupancy rate; andYields, discount rates and terminal capitalisation rate.

Significant increases/(decreases) in estimated rental value (per sqm per annum) and rent growthper annum in isolation would result in a significantly higher/(lower) fair value measurement.Significant increases/(decreases) in long-term occupancy rate and discount rate in isolationwould result in a significantly lower/(higher) fair value measurement.

At 31 December 2016 and 2015, the Group’s investment properties were fair valued on an openmarket basis by independent professionally-qualified valuers who have recent experience in thelocations and categories of the investment properties valued. Based on such valuation, the fairvalue of the investment properties at 31 December 2016 is AED 7,689,339,000 (2015: AED7,741,189,000) including investment properties under construction of AED 778,241,000 (2015:AED 752,289,000).

For all investment properties the current use of the properties is their highest and best use.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(29)

7 Land use right

2016 2015AED’000 AED’000

CostAt 1 January and 31 December 8,981,867 8,981,867

AmortisationAt 1 January 733,654 642,928Charge for the year (Note 19) 90,726 90,726

At 31 December 824,380 733,654

Net book amount at 31 December 8,157,487 8,248,213

The land use right of the Group is held under a long-term lease arrangement and amortised over theterm of the lease of 99 years.

8 Related party transactions and balances

Related parties include the Parent, the Intermediate parent and the Ultimate parent company, keymanagement personnel and any businesses (other related parties) which are controlled, directlyor indirectly by the shareholders and directors or over which they exercise significantmanagement influence.

During the year the Group entered into the following significant transactions with related partiesin the normal course of business and at prices and terms agreed by the Group’s management.

2016 2015AED’000 AED’000

Income:Revenue generated from other related parties 24,300 35,120

Expenses:Cost recharges from the Parent company 21,522 36,556Cost of sales – other related parties 8,174 58,595Other operating expenses – other related parties 27,540 23,669

57,236 118,820

Key management remuneration:- Salaries and other short term employee benefits 26,754 28,466- Termination and post-employment benefits 2,085 2,091

28,839 30,557

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(30)

8 Related party transactions and balances (continued)

Related party balances include the following:

2016 2015AED’000 AED’000

Due from related parties:Parent company 235,889 643Other related parties 17,100 19,092

252,989 19,735

Due to related parties:Other related parties 32,226 19,037

Due from Parent company of AED 235,889,000 has no minimum contractual term, and theParent is required to repay at any time on demand, even though the Group does not expect torequire repayment in the foreseeable future. As a result, the advance is recognised as an asset forits face value and is classified as a current asset, as the Parent company does not have anunconditional right to defer settlement beyond 12 months.

During the year, property and equipment amounting to net book amount of AED 1,024,000(2015: AED 2,480,000) and investment properties amounting to AED 39,000 (2015: NIL) weretransferred from the Parent company to the Establishment (Note 5 and 6).

9 Derivative financial instruments

In 2013, the Group entered into interest rate swap agreements (“swaptions”) for a notionalamount of AED 1,050,000,000. Under these swaptions, in consideration for a premium, theGroup purchased the right but not the obligation to receive an agreed upon capped 3 monthsEIBOR interest rate. The EIBOR cap rates that can be exercised during the correspondingreference periods as per the terms of the swaptions are as follows:

Reference periods EIBOR cap rateFrom 19 December 2013 to 18 December 2014 1.10%From 19 December 2014 to 18 December 2015 1.45%From 19 December 2015 to 18 December 2016 1.95%

The fair value of the Group’s derivative financial instruments, which represent swaptions that arenot traded in an active market, is determined by using valuation techniques which maximise theuse of observable market data (Mark to Market) where it is available and rely as little as possibleon entity specific estimates. Since significant inputs required to fair value the swaptions areobtained through quotations from banks for new swaptions under similar terms, the instrument isincluded in Level 2. The fair value of swaptions as at 31 December 2015 is AED 1,500 and ispresented as current asset in the consolidated balance sheet. Bank borrowings was settled on 21December 2015.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(31)

9 Derivative financial instruments (continued)

During 2016, the Group received AED 1,436,000 on maturity of swaptions and AED 64,000 ischarged to finance cost as fair value loss on interest rate swaptions.

Also during 2016, all interest rate swap agreements which were entered into in 2013 matured andno new interest rate swap agreements were entered into during 2016 and 2015.

10 Trade and other receivables

2016 2015AED’000 AED’000

Trade receivables 91,759 80,977Less: provision for impairment of receivables (64,895) (62,557)

26,864 18,420Advances to suppliers 20,412 97,661Other receivables and prepayments 3,257 3,277As at 31 December 50,533 119,358

At 31 December 2016 and 2015, the Group had a broad base of customers with no concentration ofcredit risk within trade receivables. The carrying amounts of the Group trade and other receivablesare denominated entirely in AED.

As of 31 December 2016, trade receivables of AED 1,662,000 (2015: AED 34,000) were fullyperforming.

As of 31 December 2016, trade receivables of AED 25,202,000 (2015: AED 18,386,000) were pastdue but not impaired. These relate to a number of independent customers for whom there is norecent history of default. The ageing analysis of these trade receivables is as follows:

2016 2015AED’000 AED’000

1 to 12 months 10,569 2,160Over 12 months 14,633 16,226As at 31 December 25,202 18,386

As of 31 December 2016, trade receivables of AED 64,895,000 (2015: AED 62,557,000) wereimpaired and provided for. The ageing of these receivables is as follows:

2016 2015AED’000 AED’000

1 to 12 months 15,856 10,272Over 12 months 49,039 52,285As at 31 December 64,895 62,557

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(32)

10 Trade and other receivables (continued)

Movements in the Group’s provision for impairment of trade receivables are as follows:

2016 2015AED’000 AED’000

At 1 January 62,557 83,434Provision for impairment of trade receivables (Note 21) 13,043 444Written off during the year (10,705) (21,321)As at 31 December 64,895 62,557

The creation and release of provision for impairment of receivables have been included in “Generaland administrative expenses” (Note 21) in the statement of comprehensive income. Amountscharged to the allowance account are generally written off when there is no expectation ofrecovery.

The other classes within trade and other receivables do not contain impaired assets. The maximumexposure to credit risk at the reporting date is the fair value of each class of receivable mentionedabove. The Group does not hold any collateral as security.

The carrying value less impairment provision of trade receivables is assumed to approximatetheir fair values due to the short-term nature of trade receivables. Other receivables approximatetheir fair values. The fair values are within Level 3 of the fair value hierarchy.

11 Cash and cash equivalents

2016 2015AED’000 AED’000

Cash at banks and on hand 83,739 32,447Fixed deposits 180,145 169,000

263,884 201,447

Current accounts and fixed deposits are placed with domestically-incorporated banks and localbranches of international banks. Fixed deposits earned interest at rates ranging from 1.0% to2.5% per annum (2015: 0.6% to 2.5%).

12 Equity

Share capital

The total authorised, issued and fully paid share capital of the Establishment at 31 December2016 and 2015 comprises 4,268 shares of AED 1,000,000 each.

Dividends per share

On 28 April 2016, the Group declared dividends of AED 734,500,000 (Per share: AED172,094.66). There were no dividends declared or paid during 2015.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(33)

13 Employees’ end of service benefits

2016 2015AED’000 AED’000

At 1 January 24,371 20,955Charge for the year (Note 23) 2,990 3,295Transfer - 2,424Payments during the year (1,411) (2,303)At 31 December 25,950 24,371

In accordance with the provisions of IAS 19, management has carried out an exercise to assessthe present value of its obligations at 31 December 2016, using the projected unit method, inrespect of employees’ end of service benefits payable under the UAE Labour Law. Under thismethod, an assessment has been made of an employee’s expected service life with the Group andthe expected basic salary at the date of leaving the service. Management has assumed averageincrement/promotion cost of 5% (2015: 4%). The expected liability at the date of leaving theservice has been discounted to its net present value using a discount rate of 3.51% (2015:4.16%).

14 Sukuk borrowing

On 19 June 2012, the Group issued through its subsidiary JAFZ Sukuk (2019) Limited, Sukuktrust certificates (“Sukuk”) for a nominal value of AED 2,387,000,000 (AED 2,340,000,000 netof transaction costs of AED 47,000,000) which are listed on Nasdaq Dubai and the Irish StockExchange. The Sukuk matures seven years from the issue date and bears a profit commission at acoupon rate of 7% per annum to be paid semi-annually. The Sukuk are denominated in UnitedStates Dollars (“USD”).

Up to the date of full repayment of bank borrowings (Note 16), Sukuk were secured in parripassu with bank borrowings. After the repayment of bank borrowings on 21 December 2015, thesecurity for Sukuk was released and henceforth Sukuk became unsecured.

The following fair values of Islamic Sukuk are based on quoted market rates and are within Level1 of the fair value hierarchy:

Carrying amount Fair value2016 2015 2016 2015

AED’000 AED’000 AED’000 AED’000

Sukuk borrowing 2,387,320 2,387,320 2,620,060 2,671,435Deferred borrowing costs (20,678) (27,954) - -

2,366,642 2,359,366 2,620,060 2,671,435

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(34)

15 Deferred revenue

2016 2015AED’000 AED’000

At 1 January 347,573 318,547Additions during the year 1,664,185 1,620,032Released during the year (Note 18) (1,665,476) (1,591,006)At 31 December 346,282 347,573

Current portion 309,002 309,403Non-current portion 37,280 38,170

346,282 347,573

16 Bank borrowings

The Group obtained a syndicated loan facility from a consortium of banks which bore interest ata rate of three months EIBOR plus 2.75% per annum and paid on a quarterly basis. Effective 22September 2014, the interest rate on term loan has been revised to EIBOR plus 1.85% per annum.

On 21 December 2015, the Group repaid the full outstanding balance against the term loan bypaying AED 2,135,560,000, which comprised of early repayment of AED 1,904,120,000 andcontractual payments of AED 231,440,000. The Group amortised additional deferred borrowingcosts amounting to AED 26,357,000 due to such early repayment during the year (Note 24).

17 Trade and other payables

2016 2015AED’000 AED’000

Refundable deposits 697,781 663,496Accrued expenses 152,371 145,532Trade payable 51,442 53,745Retention and other payables 42,726 33,434Advances from customers 26,545 24,917

970,865 921,124

The carrying value of trade and other payables is assumed to approximate their fair values due tothe short-term nature of trade and other payables. The fair values are within Level 3 of the fairvalue hierarchy.

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(35)

18 Revenue

2016 2015AED’000 AED’000

Lease rental income:- Plots 735,843 691,921- Warehouses 307,596 316,205- On site residences 292,058 280,437- Offices 272,023 249,857- Others 57,956 52,586

1,665,476 1,591,006Administration service revenue 137,509 140,283License and registration fees 133,534 126,067

1,936,519 1,857,356

19 Cost of sales

Utilities 120,163 118,627Depreciation of investment properties (Note 6) 108,678 97,072Amortisation of land use right (Note 7) 90,726 90,726Repairs and maintenance 76,186 74,280Others 16,162 11,358

411,915 392,063

20 Other operating income

Write-back of liabilities 13,611 5,829Lease transfer, sub-lease income and lease commission 13,390 12,067Facility manager operating fee income 6,415 4,786Sale of property from repossessed facility 3,930 1,181Fines and penalties 2,032 2,509Outdoor advertisement revenue 278 253Others 3,626 5,410

43,282 32,035

21 General and administrative expenses

Staff cost (Note 23) 105,148 108,452Expenses recharged by related parties 40,343 51,676Provision for impairment of trade receivables (Note 10) 13,043 444Security charges 9,543 7,921Depreciation of property and equipment (Note 5) 3,352 3,817Others 10,457 10,239

181,886 182,549

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(36)

22 Selling and marketing expenses

2016 2015AED’000 AED’000

Staff cost (Note 23) 44,918 45,387Advertisements 3,159 4,015Exhibitions 2,878 2,796Events 2,079 1,143Others 5,188 4,383

58,222 57,724

23 Staff cost

2016 2015AED’000 AED’000

Salaries and other staff benefits 120,810 124,420Bonus 17,919 17,465Pension expenses 8,347 8,659End of service benefits (Note 13) 2,990 3,295

150,066 153,839

Included under:

General and administrative expenses (Note 21) 105,148 108,452Selling and marketing expenses (Note 22) 44,918 45,387

150,066 153,839

24 Finance costs - net

2016 2015AED’000 AED’000

Finance income:Interest income on bank deposits 4,593 15,989

Finance costs:Profit commission on Sukuk borrowing (167,144) (167,144)Fair value loss on interest rate swaptions (64) (1,177)Interest on bank borrowing - (52,314)Amortisation of borrowing cost on early repayment of bank

borrowing (Note 16) - (26,357)Other finance charges (9,429) (33,448)

(176,637) (280,440)(172,044) (264,451)

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(37)

25 Financial instruments by category

Derivativeused forhedging

Loans andreceivables

Assets per consolidated balance sheet AED’000 AED’00031 December 2016Due from related parties - 252,989Trade and other receivables (excluding prepayments and

advances to suppliers) - 26,484Cash and cash equivalents - 263,884

- 543,357

31 December 2015Due from related parties - 19,735Derivative financial instruments 1,500 -Trade and other receivables (excluding prepayments andadvances to suppliers) - 18,954Cash and cash equivalents - 201,447

1,500 240,136

Other financialliabilities at

amortised costLiabilities per consolidated balance sheet AED’00031 December 2016Sukuk borrowing 2,366,642Trade and other payables (excluding refundable deposits and

advances from customers) 246,539Due to related parties 32,226

2,645,407

31 December 2015Sukuk borrowing 2,359,366Trade and other payables (excluding refundable deposits and

advances from customers) 232,711Due to related parties 19,037

2,611,114

Jebel Ali Free Zone FZE

Notes to the consolidated financial statements for the year ended 31 December2016 (continued)

(38)

26 Future minimum rental payments receivable under non-cancellableleases