jc - personal care industry - amazon web services€¦ · · 2017-09-09consumer and through third...

TRANSCRIPT

Consumer SectorPersonal Care IndustrySenior Analyst: Joyce ChanJunior Analysts: Brandon Neimark, Carlota De Villa, Olivia Roman and Adam Martinez

1

2

Agenda§ Industry Definition§ Industry Information§ Revenue Generation§ Industry Revenue § Porter’s Five Forces§ Trend 1: Consumer Willingness to Pay§ Trend 2: Demand for Men’s Grooming§ Trend 3: R&D Tax Credit§ Risks and Sensitivities§ Comparable Companies§ Conclusion

3

Industry Definition

§ The personal care industry prepares, blends, compounds and packages beauty products and cosmetics. Most firms in the industry conduct their own research and development for new products and manufacture them as well. Firms in this industry develop and sell personal care products through retailers, directly to the consumer and through third party distributors. Personal care products include: skin care, make up, hair care, oral care, and fragrances.

§ The largest player in this industry is an international company, L’Oréal, with 13.6% market share in North America.

L’OrealTicker: Or

Market Cap: 92.28 Bn

Revlon IncTicker: Rev

Market Cap: 1.87 Bn

Avon Products, Inc. Ticker: AVP

Market Cap: 2.98 Bn

Estee Lauder Companies Inc.Ticker: EL

Market Cap: 31.33 Bn

Coty, Inc.Ticker: COTY

Market Cap: 13.99 Bn

4

Industry Information

*Percentages based on total personal care industry revenue: $56.63bn

Sources: Statista; S&P Net Advantage; IBIS World

Industry breakdown by Market Cap

Consumer StaplesMarket Cap: $3.6 T

Household & Personal Care Products

Market Cap: $844.4bn

Personal Care

Market Cap: $458.9bn

36.10%

22.90%

17.30%

12.20%

1.10%

2015 Personal Care Product Segmentation

Skincare

Haircare

Make-up

Perfumes

Oral Cosmetics

§ Companies within the personal care industry do not focus on one product, but a mix.

5

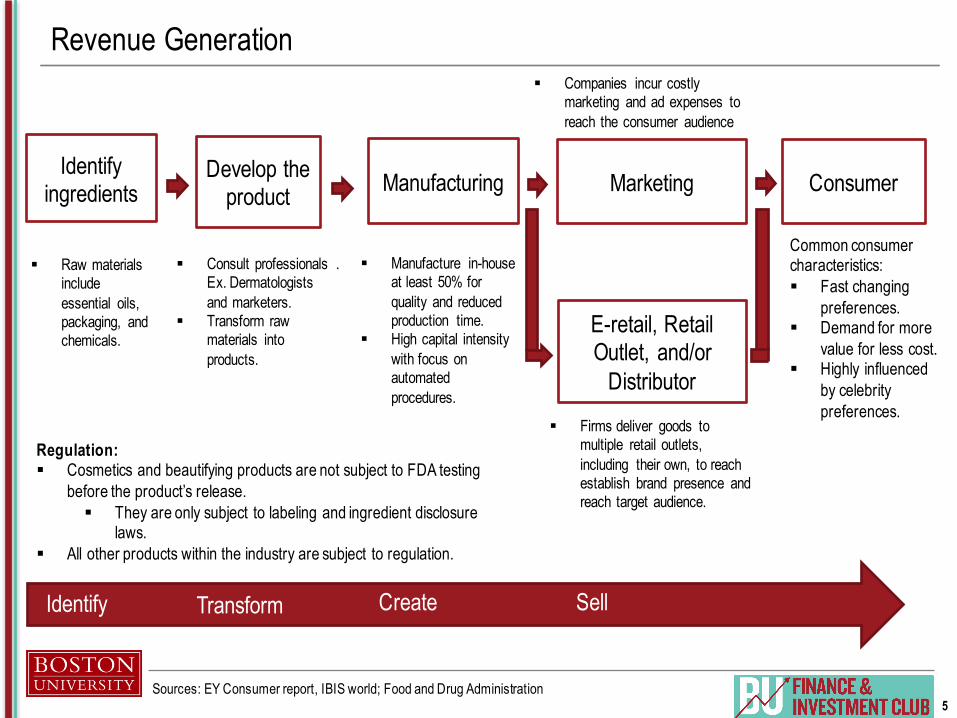

Revenue Generation

Identify ingredients

Develop the product Marketing Consumer

E-retail, Retail Outlet, and/or

Distributor

§ Consult professionals . Ex. Dermatologists and marketers.

§ Transform raw materials into products.

§ Manufacture in-house at least 50% for quality and reduced production time.

§ High capital intensity with focus on automated procedures.

§ Firms deliver goods to multiple retail outlets, including their own, to reach establish brand presence and reach target audience.

Sources: EY Consumer report, IBIS world; Food and Drug Administration

Identify Transform Create Sell

Manufacturing

§ Raw materials include essential oils, packaging, and chemicals.

§ Companies incur costly marketing and ad expenses to reach the consumer audience

Common consumer characteristics:§ Fast changing

preferences.§ Demand for more

value for less cost.§ Highly influenced

by celebrity preferences.

Regulation: § Cosmetics and beautifying products are not subject to FDA testing

before the product’s release.§ They are only subject to labeling and ingredient disclosure

laws. § All other products within the industry are subject to regulation.

6

Industry Revenue

§ Revenue grew at a CAGR of 4.36% between 2007 and 2015.

§ Revenue projected to grow at a CAGR of 5.17% between 2016 and 2021.

§ The Great Recession in 2008 did not have adverse effects on the Personal Care industry. – Largely due to a firm’s diverse brand

lines that include luxury and low-end goods.

– Consumers continue purchasing cosmetics despite reducing budgets.

§ Despite changes in the CCI, the industry revenue has increased steadily.

The revenue earned within this industry has low level of volatility due to diverse

brand lines.

Sources: IBIS World; OECD Data

0

5,000

10,000

15,000

20,000

25,000

30,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

$ in

Milli

ons

Industry Revenue ‘07 – ‘21

CAGR 4.36%

CAGR 5.17%

95

96

97

98

99

100

101

102

0

5,000

10,000

15,000

20,000

25,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

CCI

Indu

stry R

even

ue in

$ M

illion

s

Industry Revenue vs. Consumer Confidence Index ‘07-‘16

Revenue CCI

7

Porter’s Five Forces Analysis

Sources: UK Essay; IBIS World

High

Medium

High

HighLowIndustry Rivalry Customers

New Entrants

Substitutes

Suppliers

§ Competition build brand reputation to stand out from other similar products.

Barriers to Entry§ Established manufacturers

have considerable economies of scale and initial costly investments pose a barrier to entrants.

Barriers to Exit§ No considerable barriers.

§ Suppliers include:§ Inorganic chemicals§ Organic chemicals§ Soap & Cleaning

Compounds

§ Highly swayed by fashion trends, affected by consumer confidence and income.

§ Consumers can easily change from product to product if dissatisfied

§ Many competitors in the cosmetic industry exist to capture one consumer

Firms in the industry are challenged by retaining and attracting consumers who

have fast changing tastes.

8

Trend 1 – Increased Willingness to Pay for Sustainable Goods

R&D Tax Credit

Demand for Men’s

Grooming Products

Consumer Willingness

to Pay

9

Leveraging marketing campaigns to promote sustainability has contributed to a CAGR of 9.8% in the organic personal care industry.

Increased Willingness to Pay for Sustainable Goods§ Consumers are willing to pay 40.29% more for responsible products in 2009.

The willingness to pay has continued to rise.

§ 84% seek responsible products whenever possible.§ 57% of the global population who are willing to pay more for sustainable

products are willing to pay for fresh, natural and organic ingredients.§ Organic personal care market expected to reach $15.98b in 2020.§ Average gross margin: 32.65%

Sources: Nielsen; In-cosmetics Latin America; MITSloan “Does It Pay to be Good?”; Cone Communications Insight Report; Marketing Charts; McKinsey & Co.

62%

59%

57%

45%

43%

41%

41%

31%

0% 10% 20% 30% 40% 50% 60% 70%

Brand I trust

Known for health/wellness beneifts

Fresh, natural, organic ingredients

Environmentally friendly

Known for its social value

Environmentally friendly package

Community commitment

TV ad about social/environmental good

Top Sustainability Purchasing Drivers ‘15

36%

Average % Marketing Expenses of Sales ’10-’15

Marketing Expenses

50%55%

66%

0%

10%

20%

30%

40%

50%

60%

70%

2013 2014 2015

Willingness to Pay a Premium for Sustainable Products

10

Trend 2 – Demand for Men’s Grooming Products

Cosmeceutical Product Growth

Demand for Men’s

Grooming Products

R&D Tax Credit

11

258.94 263.88 267.88 267.91 272.14 273.15 274.62 274.72 275.32

17.318.3 19.3 20.3 21.4 22.6 23.9 25.2 26.6

200

220

240

260

280

300

320

2012 2013 2014 2015 2016 2017 2018 2019 2020

$ in

Billi

ons

Global Share of Men's Grooming in Industry Revenue

Global Industry Men's Grooming

Demand for Men’s Grooming Products

§ Men’s product outlook is positive especially products such as: serum, tinted moisturizers with UV protection, deodorants, and hair molding products

§ Per capita spending is a significant contributor to industry revenue because it is highly correlated.

§ Men’s grooming makes up an average 8.01% of the global personal care industry.

§ Global men’s grooming segment grew at a historical CAGR of 5.52% between 2012 -2016.

§ It will grow at a future CAGR of 5.58% from 2017-2020.

Sources: Bloomberg; R&D Taxsavers; IBIS World; Statista

Men’s grooming products are growing at a historical CAGR of 5.52% indicating a

strong revenue stream for the next 5 years.

52

53

54

55

56

57

58

59

60

61

29 30 31 32 33 34

Indu

stry R

even

ue in

($B)

Spending per Capita on Men's Grooming

U.S. Industry Revenue vs. Men's Grooming ‘11- ‘15

R^2 = 0.8593Y = 1.6593x + 3.6504

6.68% 6.94% 7.20% 7.58% 7.86% 8.27% 8.70% 9.17% 9.66%

12

Trend 3 – R&D Tax Credit

R&D Tax Credit

Demand for Men’s

Grooming Products

Consumer Willingness

to Pay

13

R&D Tax Credit

0

1000

2000

3000

4000

5000

6000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Reve

nue

($ M

illion

)

North American Organic Personal Care Revenue Product

Skin Care Hair Care Oral Care Cosmedic OthersCosmetics

Sources: GMR Insights Report; EY consumer report; R&D Tax savers; Moss Adams LLP; Physicians Committee for Responsible Medicine; Global Market Research

§ President Obama signed a permanent extension to the PATH Act of 2015 allowing businesses to credit $250 000 per year in taxes.

§ Tax credit can be applied if four criteria are met:§ Technical uncertainty, process of experimentation,

technological in nature and qualified process.§ Despite an increase in nonfinancial services profits by a

CAGR of 5.06%, R&D expenditure grows at a CAGR of 1.4%.

§ Areas of research:§ Cosmeceuticals: products that have both functional

and beautifying aspects.§ Nanotechnology embedded cosmetics.§ Organic plant-based cosmetics.

§ A possible alternative to paraben, a commonly found cosmetic product preservative that has links to cancer.

§ Organic personal care products are growing at a CAGR of 9.8%.

§ Corporate non-financial profit increased 18.12% from 2011-2015 and R&D expenditure increased 0.36%.

311.71 319.28 334.72 345.87 345.33

1115.6 1167.9 1235.21358.2 1317.8

0

200

400

600

800

1,000

1,200

1,400

1,600

2011 2012 2013 2014 2015

$ in Billions

R&D Expenditure vs. Nonfinancial Services Corporation Profits

R&D Expenditure Coporate Nonfinancial Profits

Tax credit will help alleviate a personal care company’s pressure to constantly innovate and can offer a

reasonable alternative to paraben.

14

Risks and Sensitivities

Four main risks are evident in the personal care industry:

§ 1) Fast-changing consumer purchasing behavior– Consumers are quick to change their preferences and demands to follow the new trend.– Firms struggle to keep up with their unique demands.

§ 2) Steadily increasing pressure to demonstrate greater value to consumers– 17% of consumer product companies identify bringing innovations as one of the most challenging barriers to executing

strategy.– Branding through advertising social media platforms is vital for consumer engagement and presence.

§ 3) Tailoring products to local markets is costly– Firms remain competitive by interacting with the consumers in order to gain brand loyalty.– Marketing and ad campaigns are significant costs to retain one customer.

§ 4) Limited volume growth– Companies are looking at developing markets to grow since developed markets are maturing.– However, each region is unique and has its own tailored demands making it more difficult and expensive for companies

to expand.

Sources: EY Consumer Insight Report

15

Key Financials

§ Comparable Companies

High 4.70 N/A 5925 78.24 16.75 14.35 7.58 8.50 48.15 294.62 8.53 13.58 309.7 47.84 3.92 197.80Median 2.50 4556 60.30 14.06 10.90 2.09 -3.76 17.79 9.69 1.97 5.11 27.06 15.43 3.63 100.69Low 1.40 1531 49.11 4.37 2.68 -18.65 -15.20 13.00 -10.81 -24.51 1.00 -2.18 12.30 1.85 93.12Mean 2.61 4070 61.03 12.95 10.24 -0.20 -3.55 26.81 60.44 -1.85 7.36 18.45* 21.87 3.24 121.96

Ticker

EquityValue(b)

(11.25)Closing Price EV

(%) Gross Profit Margin

(%) EBITDA Margin

(%) EBIT Margin

Net Income Margin

(%)Revenue CAGR '10-'15

(%) ROIC

(%) ROE

(%) ROA

(%) Leverage P/E

EV/ EBITDA

Inventory Turnover

Days in Inventory

AVP 2.50 5.68 5,203 60.30 4.37 2.68 -18.65 -14.06 14.25 294.62 -24.51 12.59 -2.18 19.34 3.92 93.12

REV 1.52 28.95 3,136 65.15 13.32 9.67 2.04 8.50 13.00 -6.33 1.97 13.58 27.06 12.30 3.63 100.69

NUS 2.94 53.93 4,556 78.24 14.06 10.90 5.92 6.54 40.87 15.05 8.53 1.00 21.83 14.42 1.85 197.80

EPC 4.70 80.93 5,925 49.11 16.26 14.35 7.58 -15.20 17.79 9.69 3.67 5.11 27.07 15.43 3.89 93.83

ELF 1.40 30.97 1,531 52.36 16.75 13.61 2.09 n/a 48.15 -10.81 1.12 4.53 309.7 47.84 2.94 124.34

16

Summary Industry Rating§ Personal care products industry rating:

The industry has a neutral outlook because the personal care industry is mature with possible growth opportunities.

§ 1) Industry Recap– R&D tax credits will help companies reduce the costs they incur when they are pressured to produce more innovative and

useful products.– Men’s grooming is expected to continue growing consistently.– Consumer willingness to pay for premium and ethically sourced products is key to reaping higher margins.

§ 2) Industry Outlook– Opportunities in the men’s grooming segment and producing innovative products offers strong revenue growth.

§ 3) Risk factors– Significant marketing costs caused by rapidly changing consumer preferences will force firms to spend more on marketing

and reducing product cycle time.

Neutral/Overweight

17

Q & A

18

§ Industry Definition§ Industry Information§ Revenue Generation§ Industry Revenue § Porter’s Five Forces§ Trend 1: Consumer Willingness to Pay§ Trend 2: Demand for Men’s Grooming§ Trend 3: R&D Tax Credit§ Risks and Sensitivities§ Comparable Companies§ Conclusion

Appendix

19

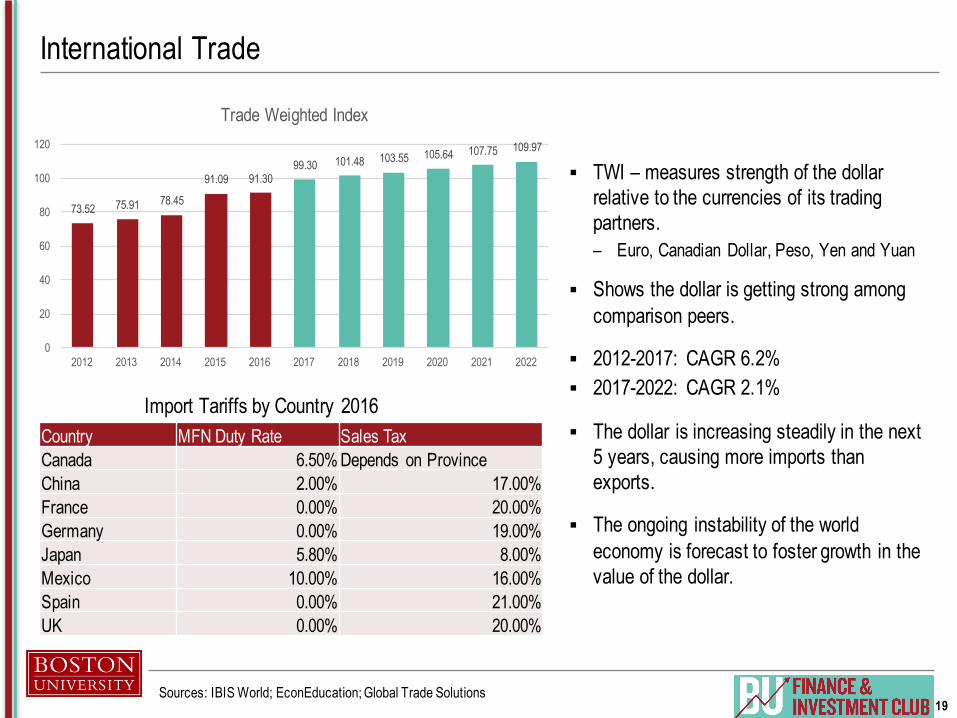

International Trade

§ TWI – measures strength of the dollar relative to the currencies of its trading partners.– Euro, Canadian Dollar, Peso, Yen and Yuan

§ Shows the dollar is getting strong among comparison peers.

§ 2012-2017: CAGR 6.2%§ 2017-2022: CAGR 2.1%

§ The dollar is increasing steadily in the next 5 years, causing more imports than exports.

§ The ongoing instability of the world economy is forecast to foster growth in the value of the dollar.

73.52 75.91 78.45

91.09 91.3099.30 101.48 103.55 105.64 107.75 109.97

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Trade Weighted Index

Sources: IBIS World; EconEducation; Global Trade Solutions

Country MFN Duty Rate Sales TaxCanada 6.50% Depends on ProvinceChina 2.00% 17.00%France 0.00% 20.00%Germany 0.00% 19.00%Japan 5.80% 8.00%Mexico 10.00% 16.00%Spain 0.00% 21.00%UK 0.00% 20.00%

Import Tariffs by Country 2016

20

World Price of Crude Oil

§ Petroleum and mineral oil are basic ingredients in many cosmetic products.– Ex. Foundation, cleanser, moisturizer etc.

§ More specifically propylene glycol is used in shampoo and isopropyl alcohol is disinfectant used in cleansers derived from oil.

§ Parabens – cosmetic preserver allowing a minimum 3 year shelf life contained in lotions, deodorants, and ointments.

§ Less expensive oil means more profits for the cosmetic industry because– Less transportation costs for deliveries.– Lower cost of basic ingredient.

Sources: IBIS World; EconEducation; Organic Make Up; Entrepreneur; IBIS World; Breast Cancer Fund

105.01 104.0796.25

50.7942.47

51.76 54.26 55.64 57.53 58.92 61.05

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

$ pe

r Bar

rel

World Price of Crude Oil