japanese financial system at crossroad toshiyuki tsujioka tsuyoshi daito robert early

Post on 21-Dec-2015

220 views

TRANSCRIPT

Japanese Financial System at Crossroad

Toshiyuki Tsujioka

Tsuyoshi Daito

Robert Early

Who are they?

Agenda

Overview of Japanese Financial System

Japan Post – the Last Crusade

The new wave (Shinsei Bank and Ripplewood)

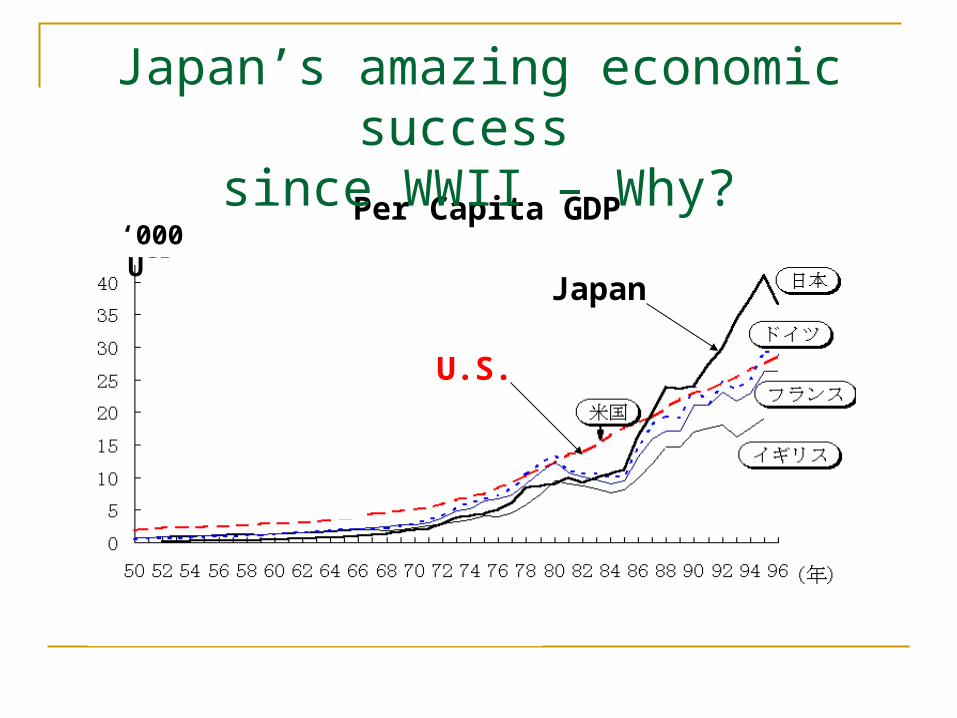

Per Capita GDP‘000 USD

Japan’s amazing economic success

since WWII – Why?

Japan

U.S.

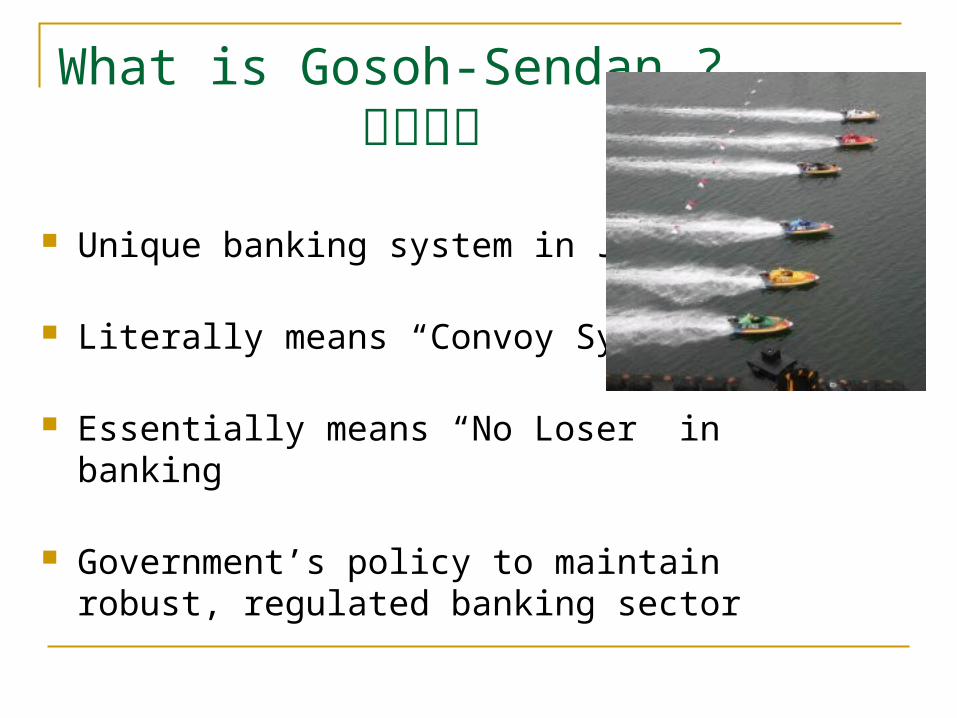

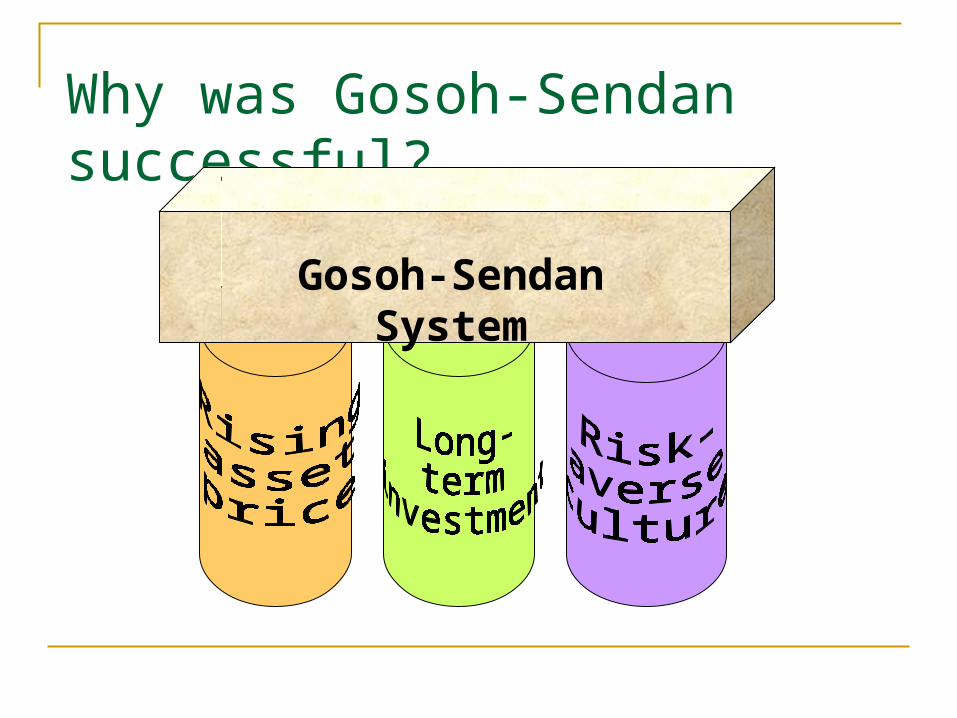

What is Gosoh-Sendan ? 護送船団

Unique banking system in Japan

Literally means “Convoy System”

Essentially means “No Loser” in banking

Government’s policy to maintain robust, regulated banking sector

How did Gosoh-Sendan work until ’80s?

Corporations

Banks

Private

Government

Deposits Loans

Employment

High Regulations

Why was Gosoh-Sendan successful?

Gosoh-Sendan System

What happened in ’90s?

Vicious Cycle of Credit Crunch Asset prices fall Bad loans accumulate Banks become reluctant to lend

Gosoh-Sendan

Globalization Burst of Bubble

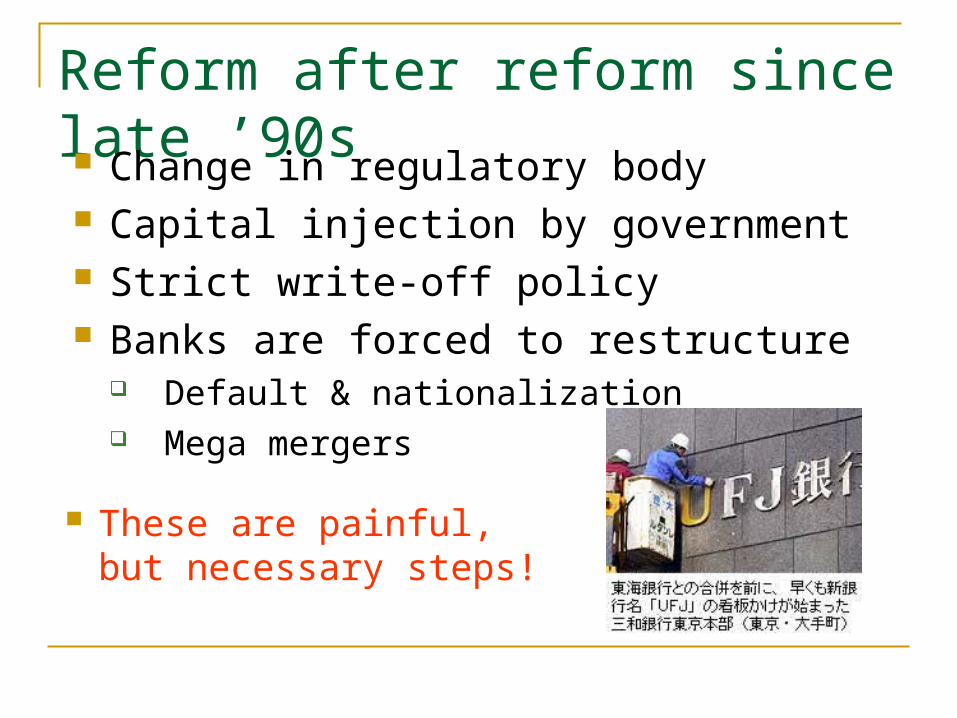

Reform after reform since late ’90s Change in regulatory body Capital injection by government Strict write-off policy Banks are forced to restructure

Default & nationalization Mega mergers

These are painful, but necessary steps!

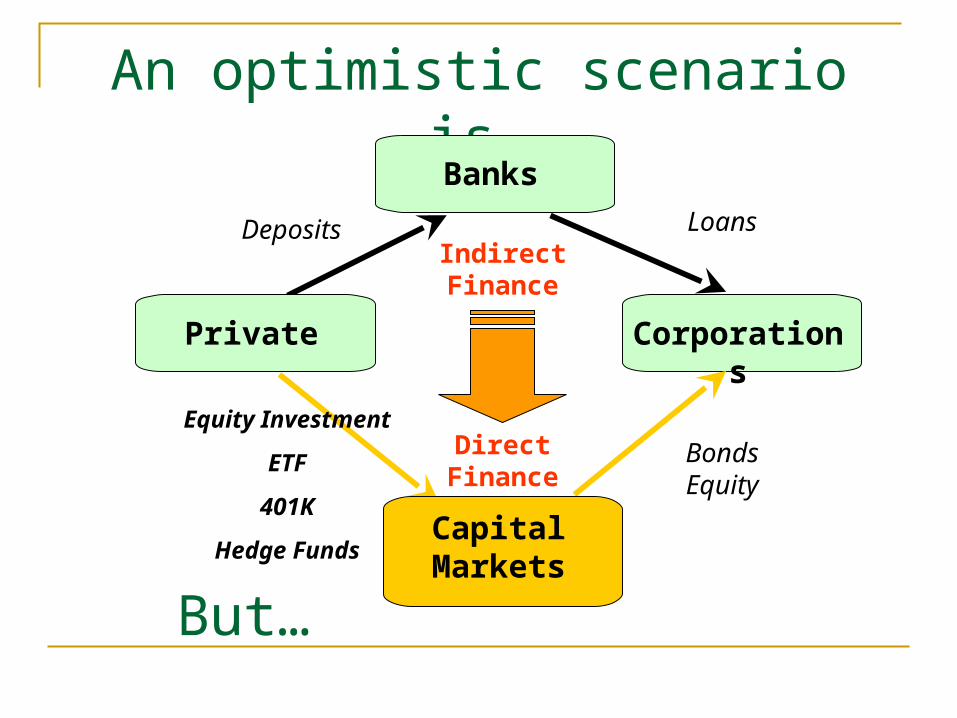

An optimistic scenario is…

But…

Corporations

Banks

Private

Deposits Loans

Capital Markets

Bonds Equity

Equity Investment

ETF

401K

Hedge Funds

Indirect Finance

Direct Finance

0% 20% 40% 60% 80% 100%

Japan

US

Depositary FI Insurance / pensions Other non-depositary

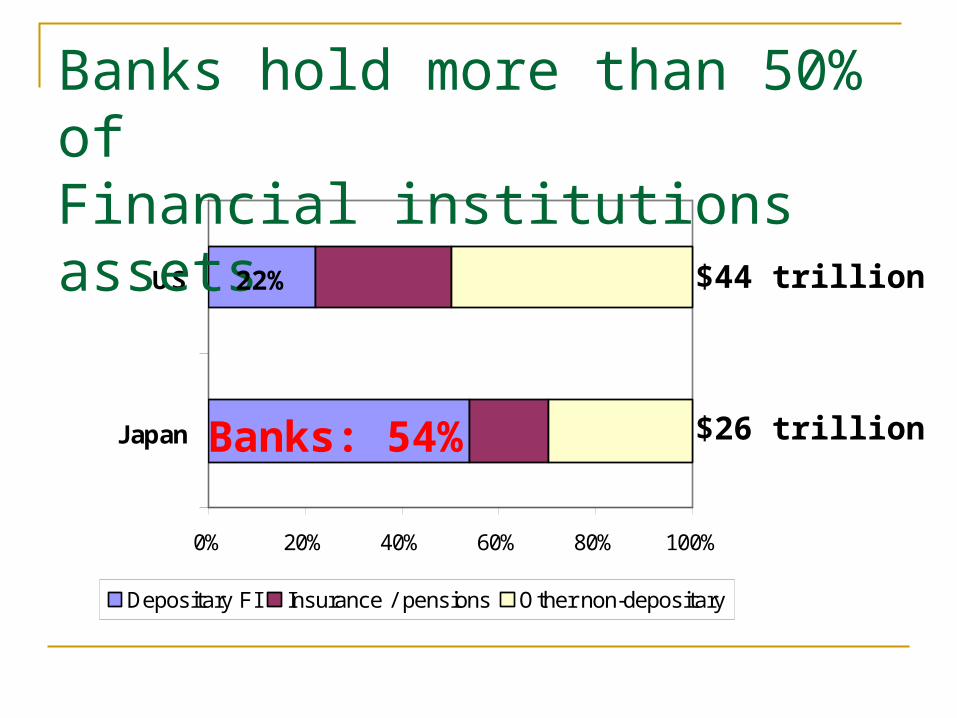

Banks hold more than 50% ofFinancial institutions assets

Banks: 54%

22%

$26 trillion

$44 trillion

0% 20% 40% 60% 80% 100%

Japan

US

Cash / deposits BondsMutual funds StocksInsurance / pensions Others

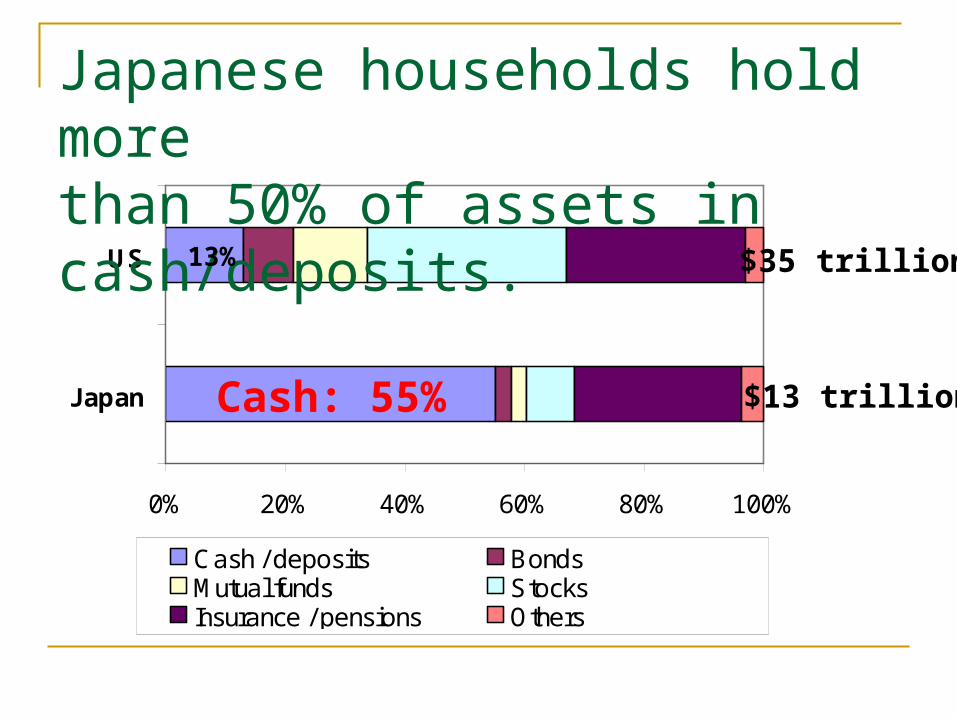

Japanese households hold morethan 50% of assets in cash/deposits.

Cash: 55%

13%

$13 trillion

$35 trillion

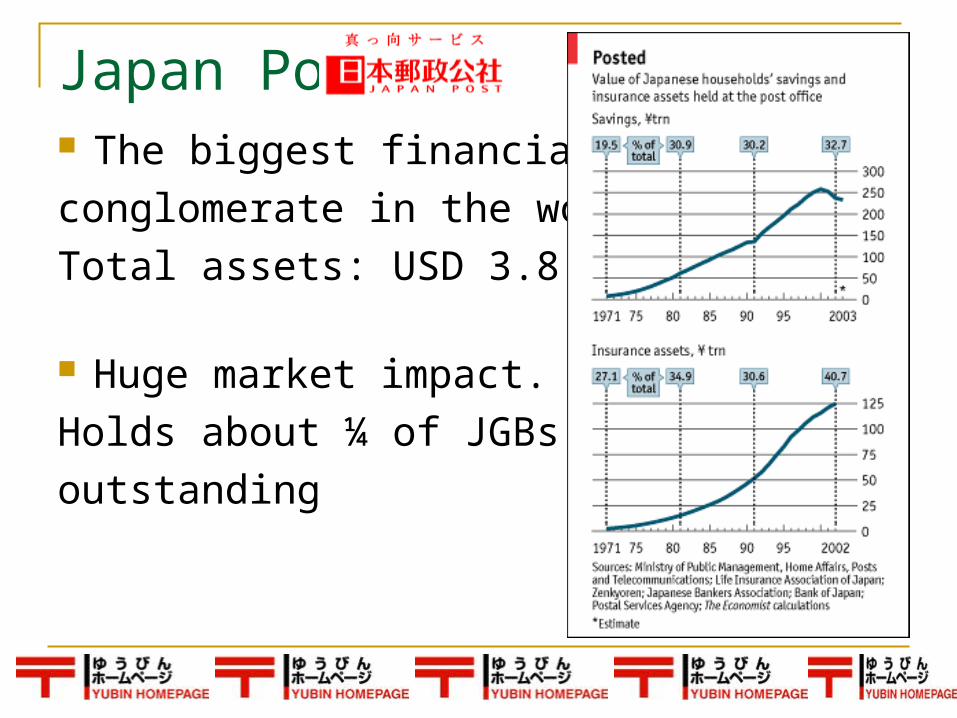

The biggest financial

conglomerate in the world.

Total assets: USD 3.8 trillion

Huge market impact.

Holds about ¼ of JGBs

outstanding

Japan Post

Politicians: need votes

Government: need to sell JGBs

Japan Post

Axis of Evil: Politicians, Government, and Japan Post

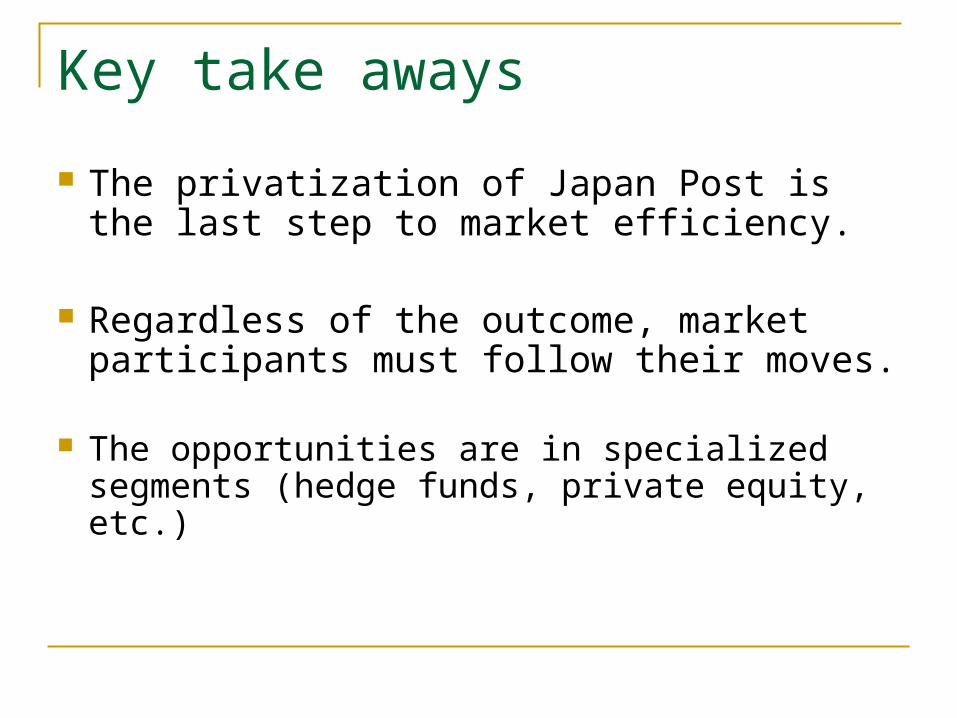

Key take aways

The privatization of Japan Post is the last step to market efficiency.

Regardless of the outcome, market participants must follow their moves.

The opportunities are in specialized segments (hedge funds, private equity, etc.)

Ripplewood and Shinsei Bank

A Major Force for Restructuring

Ripplewood and Shinsei Bank Bought Long Term

Credit Bank from Japanese government and turned it into Shinsei Bank

Total investment of $1.15B in 1999

IPO of 35% for $2.1B Shinsei is valued at over

$6B BIG PROFITS

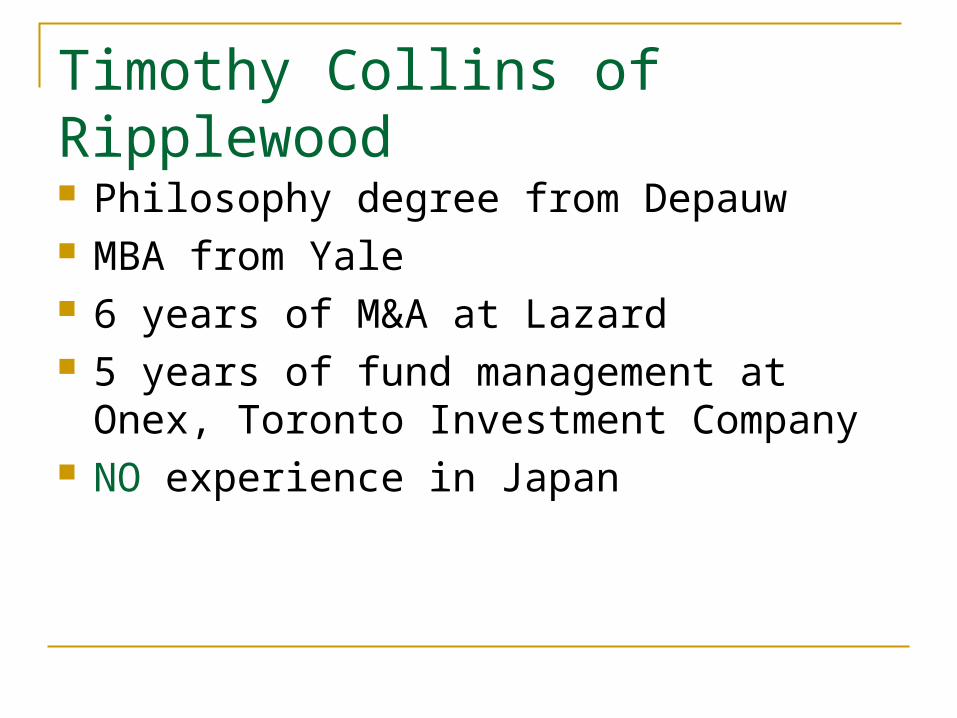

Timothy Collins of Ripplewood Philosophy degree from Depauw MBA from Yale 6 years of M&A at Lazard 5 years of fund management at Onex,

Toronto Investment Company NO experience in Japan

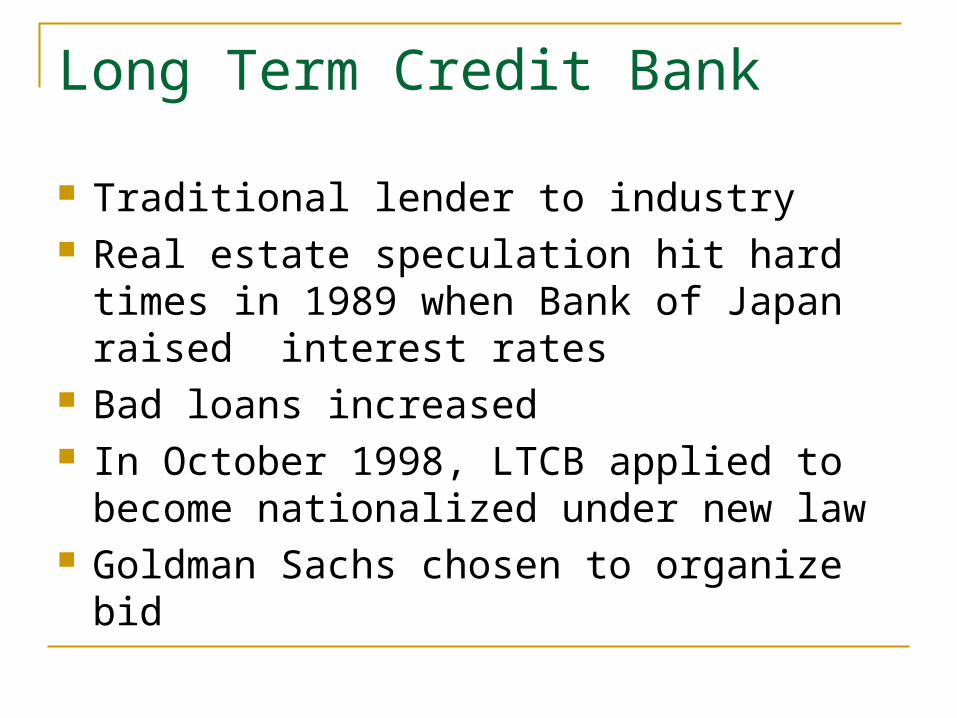

Long Term Credit Bank

Traditional lender to industry Real estate speculation hit hard times in 1989

when Bank of Japan raised interest rates Bad loans increased In October 1998, LTCB applied to become

nationalized under new law Goldman Sachs chosen to organize bid

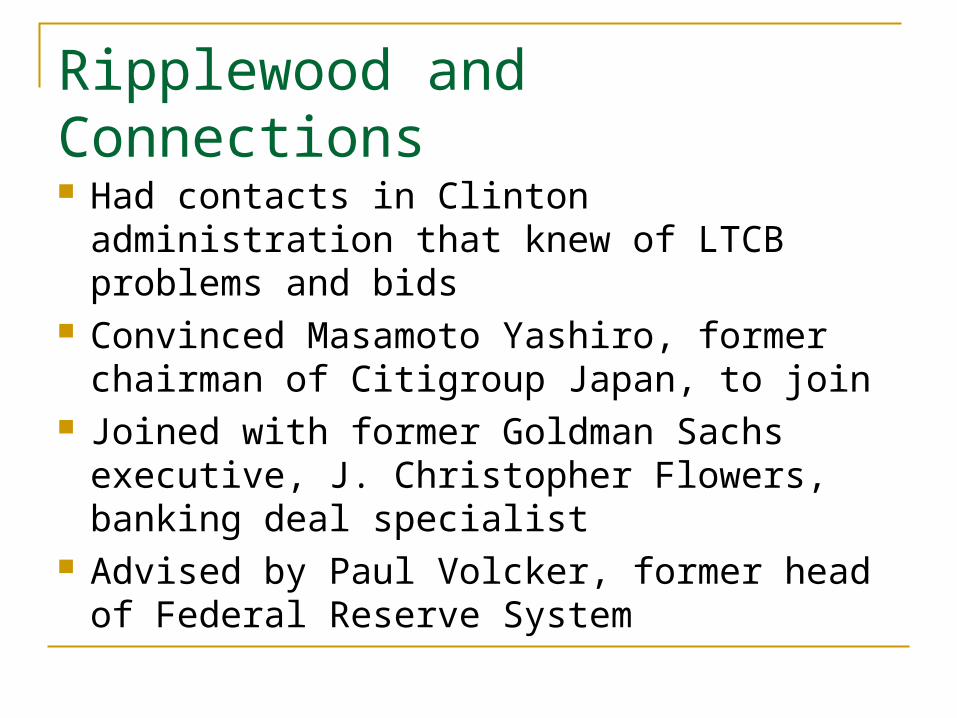

Ripplewood and Connections

Had contacts in Clinton administration that knew of LTCB problems and bids

Convinced Masamoto Yashiro, former chairman of Citigroup Japan, to join

Joined with former Goldman Sachs executive, J. Christopher Flowers, banking deal specialist

Advised by Paul Volcker, former head of Federal Reserve System

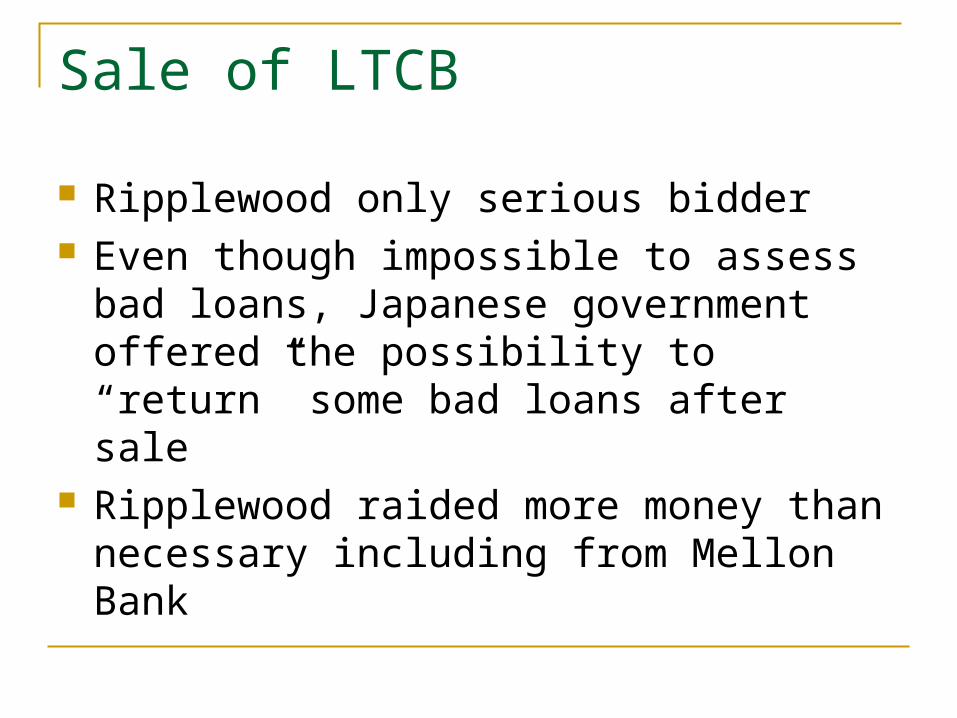

Sale of LTCB

Ripplewood only serious bidder Even though impossible to assess bad loans,

Japanese government offered the possibility to “return” some bad loans after sale

Ripplewood raided more money than necessary including from Mellon Bank

Shinsei Bank

Masamoto Yashiro became CEO Focus on entering retail bank market and deal with

loans On June 28, 2000, returned loans and capital for

Sogo, reputable retailer, forcing bankruptcy IPO in 2004 Current numbers

Total revenue of ¥ 123.5billion Net income of ¥ 66.4billion

The Future: Japanese Activities Japanese private equity investment increasin

g Unison Capital Inc. Nippon Mirai Capital Co.

Japanese banks back private equity groups Mizuho Capital Group Phoenix Capital Co.

Don’t be like this!!!

Back-ups

“Main Bank” System

Cross-Share Holding

Toshiba

Mitsui Bank

Mitsui Chem.

Mitsui Insur.

Mitsui Corp.

Toyota

6 mega banks 3 long-term banks 80 first-level local banks 100 second-level local banks