january to march 2020 asset and wealth management tax ... · asset and wealth management tax...

TRANSCRIPT

Australia

Asset and Wealth Management Tax Highlights – Asia Pacific

COVID-19 MeasureOn 12 March 2020, the Federal Government announced its first package (AUD17.6 billion) of measures to respond to the current economic challenges confronting the Australian economy as a result of the continued spread of the Coronavirus (COVID-19). This was followed by a second package announced on 22 March 2020 which brought the total relief by all arms of Government to AUD189 billion at that stage. One week later, a further AUD130 billion ‘JobKeeper’ package was announced on 30 March 2020, following a comprehensive health package announced on the previous day.

The focus of the relief package is supporting businesses and employers to keep operating as best and for as long as they can and so as to be in the best-placed position when this crisis has passed to help keep Australians in jobs.

The federal economic stimulus packages to date have a number of components including:

• JobKeeper payments to help businesses keep staff employed and assist business recover once the Covid-19 crisis passes;

• Supporting business capital investment through enhanced tax concessions (asset tax write offs);

• Cash flow assistance for small and medium-sized businesses as well as not-for-profits (NFPs) to help them stay in business and keep their employees in jobs;

• Targeted support for the most severely affected sectors, regions and communities; • Measures to support the flow of credit such as a Government guarantee of 50 per cent to

support new short-term unsecured loans to small and medium enterprises;• Temporary relief for financially stressed business including, among other measures, relief

for directors from any personal liability for trading while insolvent; and• Support for individuals and households in the form of stimulus payments and income

support, temporary measures to allow early access to superannuation and reducing the superannuation minimum drawdown rates.

.

January to March 2020

In this edition’s asset and wealth management tax highlights for the Asia Pacific region, we highlight industry and tax developments from Australia, China, Hong Kong, India, Japan, Malaysia and Singapore, which may impact your asset and wealth management business. We hope you find these updates of interest, and will be pleased to discuss these developments and issues with you further..

January to March 2020 2Asset and Wealth Management Tax Highlights – Asia Pacific

All States and Territories have also been progressively introduced various stimulus measures, including relief for various State based taxes.

ATO’s report on Top 100 Interim Findings

The Australian Taxation Office (ATO) has published its key findings from 80 tax assurance reviews in the ‘Top 100 Program’ which includes public and multinational businesses and superannuation funds that have substantial economic activity related to Australia.

Broadly, most taxpayers reviewed obtained an overall medium assurance rating, with an expectation that many will transition from medium to high assurance. This level of assurance is based on an objective view (having regard to objective evidence) of whether the taxpayer is considered to have paid the right amount of tax. Tax governance is a key focus area under the ‘justified trust’ methodology for large public and multinational businesses, with an effectively operating tax governance framework said to provide the ATO with greater confidence in reported tax outcomes.

The ATO continues to see taxpayers make an investment in tax governance or take steps to improve their tax risk governance and they are using the available ATO guidance. Transfer pricing is a common assurance area with approximately 85 per cent of Top 100 taxpayers reporting related party dealings.

Permanent tax relief for merging superannuation funds

Legislation is now before Federal Parliament to extend the current tax relief (i.e. loss relief and asset roll-over relief) for merging superannuation funds so that it will be made permanent from 1 July 2020. This should remove tax as an impediment to mergers and facilitate industry consolidation.

Expanded concept of significant global entity now before Parliament

The Australian Government has introduced legislation which expands the scope of what is a significant global entity (SGE) and introduces the new concept of a Country by Country Reporting Entity (CbCRE). The new rules are particularly relevant for any groups of entities that would be required to consolidate for accounting purposes as a single group if the members of the group were assumed to be a listed company and were not affected by the accounting exceptions for consolidation or materiality. The consequences of an entity becoming an SGE or a CbCREare significant in terms of the additional compliance burdens and the cost of failing to determine status as an SGE correctly.

Affected entities should review their existing ownership and control structure as soon as possible as the new rules are proposed to apply to income years commencing on or after 1 July 2019.

ATO reviewing arrangements with Australian taxable property

The ATO has noted it has concerns around foreign residents disposing of taxable Australian property (TAP) and that although most foreign residents get it right, it has identified problems whereby foreign residents are claiming assets are not TAP and, as such, are reviewing arrangements where foreign residents are:

• structuring investments in indirect Australian real property interests in such a way that each entity holds an interest of less than 10 per cent (i.e the non-portfolio interest test)

• attributing significant value to non-taxable Australian real property assets (relevant to the principal asset test), and

• dissipating funds by transferring them offshore prior to meeting Australian tax obligations.

January to March 2020 3Asset and Wealth Management Tax Highlights – Asia Pacific

Discounted capital gains and FITO claims

The High Court of Australia has dismissed the taxpayer’s application for special leave to appeal against the decision of the Full Federal Court Burton v Commissioner of Taxation [2019] FCAFC 141. The majority of the Full Federal Court had held that the taxpayer, who derived assessable capital gains from investments made in the United States (US), was not entitled to a full foreign income tax offset (FITO). Specifically, the taxpayer was not entitled to a FITO in respect of that part of the capital gain that was not included in the assessable income due to the capital gains tax discount.

In response to the High Court’s decision, the ATO has released a statement welcoming the decision and encouraging taxpayers to review any prior year FITO claims and make necessary voluntary amendments such that the FITO claim is limited to the extent of the assessable amount of the capital gain in Australia, even though foreign tax may have been paid on the whole of the gain in the foreign jurisdiction. The ATO has indicated that it intends to commence compliance activity on this issue in the near future.

Board of Taxation to review rollovers

The Board of Taxation has been requested by the Government to undertake a review into Australia’s system of capital gains tax rollovers and associated provisions, focusing on considering practical ways to simplify existing rollovers. The Board is to finalise its review and report to the Government by 30 November 2020.

January to March 2020 4Asset and Wealth Management Tax Highlights – Asia Pacific

China

Industry views on the VAT law consultation draft

In our Q4 2019 edition, we highlighted that the Chinese government has introduced the Consultation Draft of the Value-added Tax (VAT) Law of the People’s Republic of China (or the Consultation Draft) on 27 November 2019 and launched a consultation process to collect comments from industry participants. PwC supported an industry group – the China Wealth Management 50 Forum – to prepare a research report to provide various recommendations to address key VAT issues arising in the financial services sector in China and to provide recommendations on China’s VAT legislation.

For more details, please click here (Chinese version) or here (English version).

China releases a series of fiscal and taxation policies to prevent and control the epidemic

In response to the COVID-19 pandemic, Chinese governments at all levels have rapidly issued several policies to control the situation and support the economy. On 5 February 2020, the executive meeting of the State Council decided to launch a series of fiscal and taxation policies in addition to the previously introduced measures to ensure that there are sufficient supplies for epidemic prevention and control work, effective from 1 January 2020.

Asset managers in China are also eligible to enjoy some of the above policies, including a full tax deduction on qualified donations to charitable institutions and/or to hospitals to counter COVID-19, deferral or reduction of employers’ social security contribution, etc.

For more details, please click here.

January to March 2020 5Asset and Wealth Management Tax Highlights – Asia Pacific

Budget 2020

On 26 February, Hong Kong's Financial Secretary Paul Chan Mo-po announced the 2020/21 Budget, outlining the Hong Kong SAR Government's plan for the economy and proposals for tax developments. These included various measures aimed at revitalising Hong Kong's financial service industry, with key ones being:

To develop the securities market in Hong Kong - a proposal to waive stamp duty on stock transfers paid by exchange traded fund market makers in the course of creating and redeeming ETF units listed in Hong Kong.

Clarity on carried interest coming? The Government plans to provide a tax concession for carried interest issued by private equity funds operating in Hong Kong subject to the fulfilment of certain conditions. An industry consultation on the proposal will follow, with target application from 2020-21.

For further analysis on the full Budget and what it means for you, your business, and Hong Kong's economy, please refer to our website and commentary. You can also download our 2020/21 Hong Kong Tax Facts and Figures, which includes the latest tax laws and practices together with the proposals and measures set out in the Budget.

Hong Kong

Hong Kong’s new limited partnership for funds

On 20 March 2020, the Hong Kong SAR Government gazetted the Limited Partnership Fund Bill (the Bill), introducing a new registration regime for limited partnership funds (or LPFs) to be set up and operate in Hong Kong. This Bill has been a long time coming and was alluded to in the 2020/21 Budget delivered by the Financial Secretary in February. With the unified tax exemption and open-ended fund company regime already in place, and the anticipation of the carried interest tax concession coming in 2020/21, the introduction of an LPF regime is another big step towards building a more extensive asset and wealth management ecosystem in Hong Kong. Please click here for our newsflash, which sets out the key features of the LPF regime, and our insights on why it comes at a crucial time.

January to March 2020 6Asset and Wealth Management Tax Highlights – Asia Pacific

India

Tax exemption for SWFs and pension funds for infrastructure investments

On 23 March 2020, the Indian Parliament passed the Finance Bill 2020, which includes a tax exemption for SWFs and pension funds' investments in certain infrastructure projects. Under the proposal:

‒ The SWF exemption has been extended to investments made in InvITs and Category I or Category II Alternative Investment Fund (AIF) which has 100% investment in one or more eligible company or entity (i.e. entities engaged in infrastructure activity). The earlier proposal restricted the benefit of the exemption to income derived from investments in companies or enterprises.

‒ The exemption is granted to income from investments in debt, share capital or units. The term share capital will include income from investments in both equity and preference share capital. This is an extension from the earlier proposal where the exemption was restricted to income from investment in debt or equity only.

‒ It has been clarified that exemption shall only be applicable for investments made on or after 01 April 2020 but on or before 31 March 2024.

‒ The amended provision also provides that if difficulty arises in interpretation or implementation of any provisions of this exemption, the Central Board of Direct Taxes (CBDT) can issue guidelines for removing such ambiguities, after consultation with the Central Government.

Although the definition of eligible investors extended to pension funds, pension funds have different conditions to that of SWFs.

Our news alert presents a snapshot, relevant to the financial services sector, of the changes made to the Bill, as passed by the Lok Sabha, over the original proposals when the Bill was tabled. The Bill was subsequently assented by the President and is now the Finance Act, 2020. For more details, please click here.

January to March 2020 7Asset and Wealth Management Tax Highlights – Asia Pacific

COVID-19 Tax Measures

On 7 April 2020, a package of emergency fiscal measures to mitigate the economic impact of Covid-19 was approved by the Cabinet.

The package includes special tax measures for businesses, such as reductions in fixed asset and property taxes, the deferral of tax payments and social security premiums, and exemptions from National Pension Insurance and National Health Insurance premium payments. The Bill is expected to be submitted to and approved by the Diet by the end of April. For more details, please click here.

Japanese based asset managers should consider whether they may be eligible to apply for any of the measures.

Extension of Deadline for Submission of Securities and Financial Reports

While not a tax measure, it has also been announced on 5 April 2020 that the filing deadline of the securities and financial reports for companies based on the Financial Instruments and Exchange Act will be extended to the end of September this year, to allow companies and audit firms sufficient time to proceed with their account settlement and audit work in light of the COVID-19 situation.

2020 Tax Reforms

At the end of March 2020, the 2020 Japan Tax Reform proposals were passed into law. The reforms discussed below are selected reforms that have more impact and relevance for the asset and wealth management industry.

Scope of Interest under the Earnings Stripping Rules expanded

Under the earnings stripping rules, interest expense which is taxable in Japan in the hands of the income recipient was excluded from these deductibility restrictions.

Following the 2020 tax reforms, where a Japanese corporation pays interest to a Japanese permanent establishment (PE) of a foreign corporation (for example, the Tokyo branch of a foreign bank), and the parties contemplate in advance that the Japanese PE will transfer the interest received to its foreign head office, such interest would be included in the scope of interest subject to restrictions under the earnings stripping rules.

This change will apply to fiscal years beginning on or after 1 April 2020.

Receipt of Dividends from a Subsidiary adjusting base cost of Subsidiary

Under the 2020 tax reforms, where a Japanese parent receives from a subsidiary dividend greater than 10% of the book value of the shares of that subsidiary in a given year, the parent must reduce its basis in the shares of the subsidiary by the amount of dividends subject to the dividend income exclusion. This rule is designed to prevent a Japanese parent from reducing any capital gain (or inflating a loss) arising on a subsequent transfer of the subsidiary’s shares when first receiving (tax exempt) dividends from the subsidiary. Certain exceptions apply to this rule which was introduced following some examples that came in light in practice.

The rule applies to fiscal years beginning on or after 1 April 2020.

Scope of creditable foreign tax payments

Under the 2020 tax reforms, the scope of creditable foreign corporation taxes will be narrowed to exclude foreign taxes paid under the following circumstances:

(i) foreign taxes levied on payments between foreign corporations that were denied relief under treaties on the grounds that such payments were deemed to have been made to the Japanese corporation;1 and

Japan

January to March 2020 8Asset and Wealth Management Tax Highlights – Asia Pacific

(ii) foreign taxes levied on payments from a foreign PE to its Japanese head office or another related party as a result of the foreign tax authorities disallowing a deduction at the local level. 2

These changes will apply to fiscal years beginning on or after 1 April 2021.

Revised Rules on Overseas Used Rental Property for Individuals

New rules have been introduced to restrict the ability of individual permanent resident taxpayers from claiming accelerated depreciation on older rental properties located overseas when applying the ‘simplified method’ election to determine their useful life.

The changes are effective from the 2021 fiscal year (where individuals are assessed on a calendar year basis).

1 An example of foreign taxes ineligible for Japanese tax credit under this section of the provision would be those arising to a taxpayer who was denied tax treaty benefits by a foreign taxing authority in reference to a treaty’s anti-abuse or anti-conduit provisions applicable to back-to-back transactions.2 An example of foreign taxes ineligible for the Japanese tax credit under this section of the provision would be BEAT amounts, where a US branch was required to pay additional tax in the US as a result of application of the BEAT rules.

January to March 2020 9Asset and Wealth Management Tax Highlights – Asia Pacific

Removal of exemption on retail money market fund for corporate investors

Currently, interest income (as stated in paragraph 35A of Schedule 6 of the Act) derived from licensed banks, Islamic banks and development financial institutions is exempted from tax.

The Ministry of Finance has communicated that the tax exemptions available to retail money market funds will no longer apply to corporate investors with effect from 1 July 2020 onwards. This will mean that income which would normally be tax exempted at the unit trust level will no longer be tax exempted if received by corporate investors.

Special tax deduction on rental discount given to SME tenants

Owners of buildings or business premises will be given an additional tax deduction equivalent to the amount of reduction in rent that is given to tenants that are small and medium enterprises (SMEs) for the months of April 2020 to June 2020.

The condition to qualify for the tax deduction claim is that the minimum rental reduction must be at least 30% of the original monthly rental charged to the SME tenant.

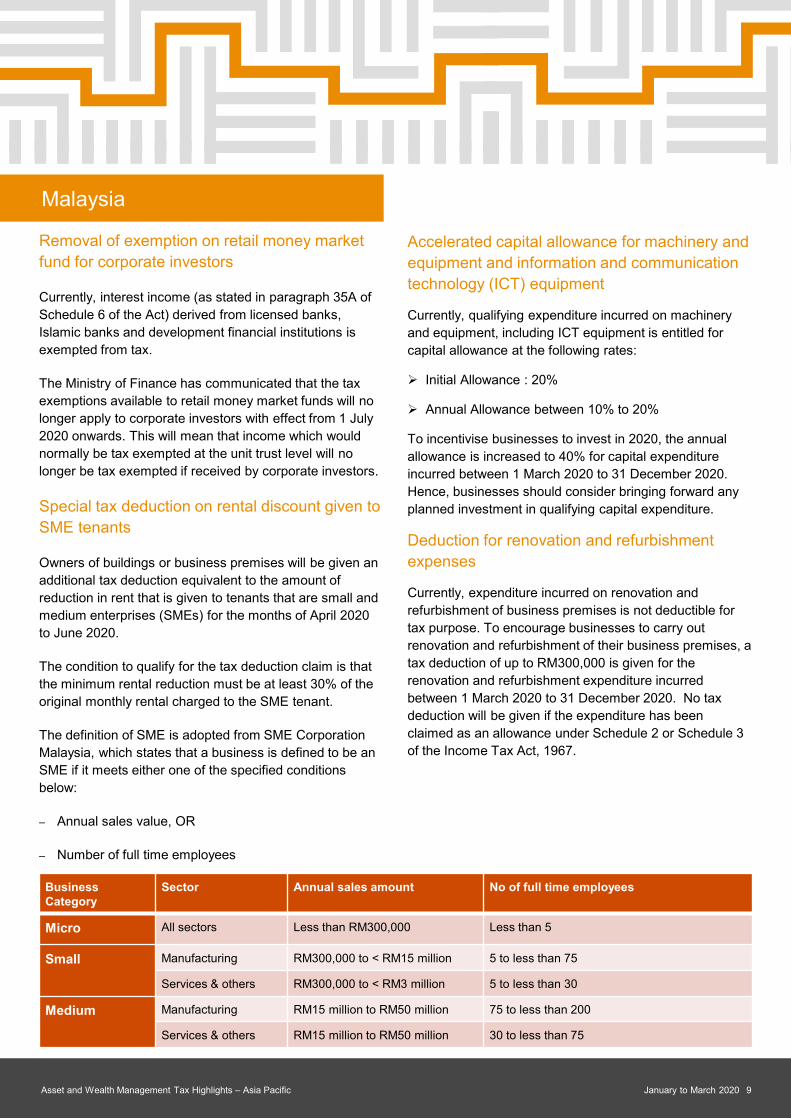

The definition of SME is adopted from SME Corporation Malaysia, which states that a business is defined to be an SME if it meets either one of the specified conditions below:

‒ Annual sales value, OR

‒ Number of full time employees

Accelerated capital allowance for machinery and equipment and information and communication technology (ICT) equipment

Currently, qualifying expenditure incurred on machinery and equipment, including ICT equipment is entitled for capital allowance at the following rates:

Initial Allowance : 20%

Annual Allowance between 10% to 20%

To incentivise businesses to invest in 2020, the annual allowance is increased to 40% for capital expenditure incurred between 1 March 2020 to 31 December 2020. Hence, businesses should consider bringing forward any planned investment in qualifying capital expenditure.

Deduction for renovation and refurbishment expenses

Currently, expenditure incurred on renovation and refurbishment of business premises is not deductible for tax purpose. To encourage businesses to carry out renovation and refurbishment of their business premises, a tax deduction of up to RM300,000 is given for the renovation and refurbishment expenditure incurred between 1 March 2020 to 31 December 2020. No tax deduction will be given if the expenditure has been claimed as an allowance under Schedule 2 or Schedule 3 of the Income Tax Act, 1967.

Malaysia

Business Category

Sector Annual sales amount No of full time employees

Micro All sectors Less than RM300,000 Less than 5

Small Manufacturing RM300,000 to < RM15 million 5 to less than 75

Services & others RM300,000 to < RM3 million 5 to less than 30

Medium Manufacturing RM15 million to RM50 million 75 to less than 200

Services & others RM15 million to RM50 million 30 to less than 75

January to March 2020 10Asset and Wealth Management Tax Highlights – Asia Pacific

Digital Service Tax

Effective 1 January 2020, service tax at 6% will be imposed on digital services provided by both local and foreign service providers. Digital services are defined as services which are delivered or subscribed over the internet or other electronic network and cannot be delivered without the use of IT and the delivery of the service is substantially automated. This could potentially result in certain service providers charging digital service tax to fund management companies, resulting in an increase in cost.

January to March 2020 11Asset and Wealth Management Tax Highlights – Asia Pacific

Singapore Budget 2020

In the Singapore Budget 2020 in February 2020, it was announced that the tax incentive schemes for venture capital funds and venture capital fund management companies will be extended and enhanced. Please refer to the following PwC budget commentary for a synopsis of the changes. Further details of the changes are expected to be released by Enterprise Singapore in May 2020.

For more details on the PwC budget commentary, please click here

COVID-19 support measures and tax guidance

The Inland Revenue Authority of Singapore (IRAS) has implemented a series of relief measures to help businesses and individuals affected by the COVID-19 pandemic. The IRAS has also provided guidance for taxpayers who may be affected by the COVID-19 developments. The guidance seeks to address issues such as impact on tax residence and permanent establishment exposure due to travel restrictions and quarantine requirements imposed.

• Extension of tax filing deadlines

The IRAS will grant an automatic extension of deadlines for tax filing for individuals and businesses. In general, filing deadlines falling in the month of April 2020 will be extended to May 2020. Please refer to the IRAS website for details: click here

• Deferment of tax payments

Corporate income tax payments for companies and income tax payments for self-employed individuals which are due in April, May and June 2020 will be granted an automatic three-month deferment to July, August and September 2020 respectively.

In addition, individuals (employees) may apply for deferment of income tax payments due in May, June and July 2020 to August, September and October 2020 respectively. Unlike the above, this is not an automatic deferment.

• Property tax rebate for non-residential properties

Non-residential properties will be granted property tax rebate for the period 1 January 2020 to 31 December 2020. Commercial properties badly affected by COVID-19 such as hotels, serviced apartments, tourist attractions, shops and restaurants will receive a 100% rebate. Other non-residential properties such as offices and industrial properties will get a 30% rebate. Owners of properties that are granted the property tax rebate are required to pass on the rebate to their tenants.

• Guidance on tax residence status of companies

The tax residency of a company is determined by the place in which its business is controlled and managed. Typically, the location of the company’s Board of Directors (BoD) meetings, during which strategic decisions are made, is a key factor in determining where the control and management is exercised.

Where a company is a Singapore tax resident for Year of Assessment (YA) 2020 (i.e. financial year ending in 2019), and is not able to hold its BoD meetings in Singapore due to the travel restrictions relating to COVID-19, the IRAS is prepared to continue to consider the company as tax resident for the YA 2021, subject to conditions.

Conversely, where a company is not a tax resident of Singapore for YA 2020, and it has to hold its BoDmeetings in Singapore due to the travel restrictions relating to COVID-19, the IRAS is prepared to continue to consider the company as a non-resident for YA 2021, subject to conditions.

• Guidance on permanent establishment

Employees of a foreign company may have to remain in Singapore due to travel restrictions relating to COVID-19. The IRAS will consider such unplanned presence does not result in the creation of a permanent establishment in Singapore for the foreign company, subject to conditions.

Singapore

January to March 2020 12Asset and Wealth Management Tax Highlights – Asia Pacific

However, the employment income derived from the business trip/short-term assignment (prior to the forced extended stay) will be subject to normal tax rules. For example, employment income from a business trip/short-term assignment (not including the extended stay) will be tax exempt if the duration of that trip/assignment is not more than 60 days in a calendar year.

Please refer to the following PwC commentary and IRAS website for further details.

For more details on the PwC commentary, please click here.

For more details on the IRAS website, please click here.

Updated Singapore-Indonesia tax treaty

Singapore signed an updated tax treaty with Indonesia on 4 February 2020. If the tax treaty is ratified and enters into force within 2020, it will become effective from 2021 for all Indonesia taxes and taxes withheld by Singapore, and effective from 2022 for taxes chargeable (other than taxes withheld) by Singapore. The table below summarises the key changes to the tax rates in the updated treaty.

• Tax relief for individuals

Tax relief for returning Singaporeans and Singapore Permanent Residents (“SPRs”)

If Singaporeans or SPRs are working from Singapore remotely for overseas employers after returning from overseas, the IRAS will continue to consider them as not exercising an employment in Singapore for the period from their date of return to 30 September 2020 (date subject to review as the situation evolves) provided all the following conditions are met:

1. There is no change in the contractual terms governing employment overseas before and after their return to Singapore.

2. This is a temporary work arrangement due to COVID-19.

Tax relief for stranded non-resident foreigners

The IRAS will consider non-resident foreigners who are unable to leave Singapore due to travel restrictions, and who have been working remotely from Singapore for their overseas employers during the extended stay in Singapore, as not exercising an employment in Singapore for the period of the extended stay provided all the following conditions are met:

1. The extended stay is for a period of not more than 60 days.

2. The work done during the extended stay is not connected to the individual’s prior business trip/short-term assignment in Singapore, and such work would have been performed overseas if not for COVID-19.

The period of the extended stay starts on the date following the end of the business trip/short-term assignment, and ends on the date of the individual’s departure from Singapore (both dates inclusive).

Type of income Current treaty Updated tax treaty

Dividends 10% (subject to minimum 25% shareholding) or 15%

No change to tax rates

Branch Profits 15% 10% Interest 10% / 0% - certain

instruments e.g. government bonds

10% / 0% - limited to payment to government (as defined)

Royalties 15% 10% / 8% (depending on type of royalties)

For more details on the PwC tax bulletin, please click here.

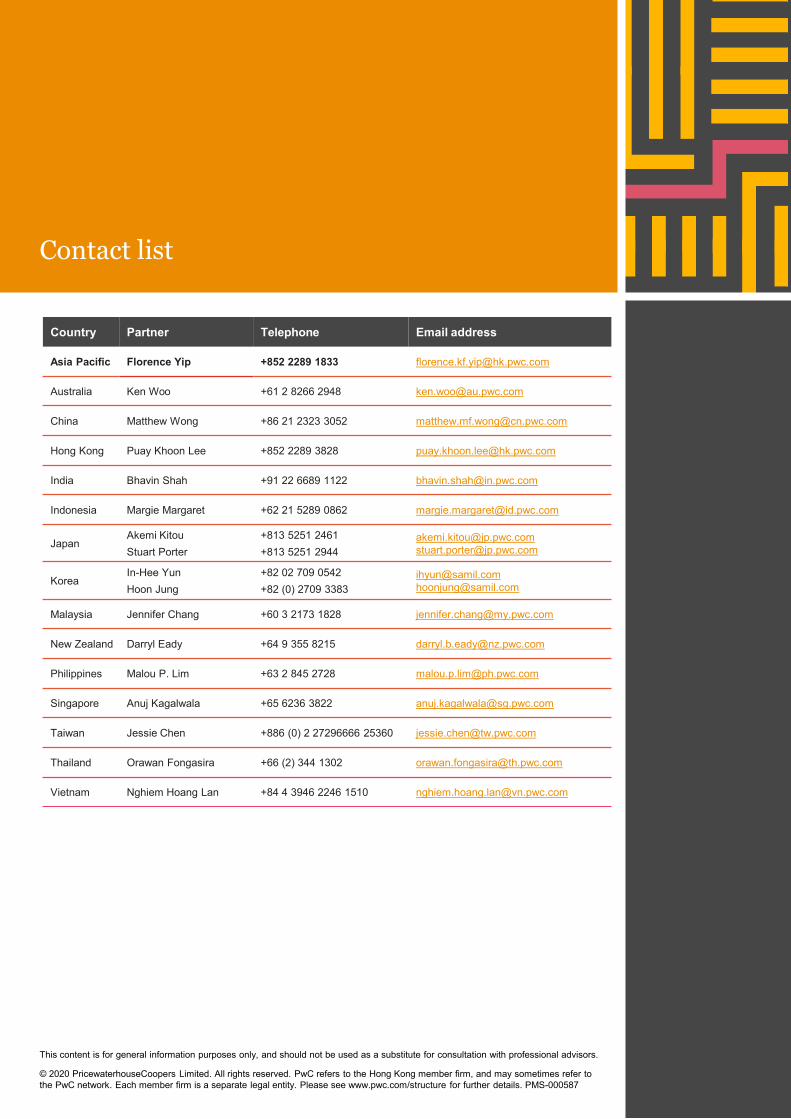

Contact list

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2020 PricewaterhouseCoopers Limited. All rights reserved. PwC refers to the Hong Kong member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. PMS-000587

Country Partner Telephone Email address

Asia Pacific Florence Yip +852 2289 1833 [email protected]

Australia Ken Woo +61 2 8266 2948 [email protected]

China Matthew Wong +86 21 2323 3052 [email protected]

Hong Kong Puay Khoon Lee +852 2289 3828 [email protected]

India Bhavin Shah +91 22 6689 1122 [email protected]

Indonesia Margie Margaret +62 21 5289 0862 [email protected]

JapanAkemi KitouStuart Porter

+813 5251 2461+813 5251 2944

[email protected] [email protected]

KoreaIn-Hee YunHoon Jung

+82 02 709 0542+82 (0) 2709 3383

[email protected] [email protected]

Malaysia Jennifer Chang +60 3 2173 1828 [email protected]

New Zealand Darryl Eady +64 9 355 8215 [email protected]

Philippines Malou P. Lim +63 2 845 2728 [email protected]

Singapore Anuj Kagalwala +65 6236 3822 [email protected]

Taiwan Jessie Chen +886 (0) 2 27296666 25360 [email protected]

Thailand Orawan Fongasira +66 (2) 344 1302 [email protected]

Vietnam Nghiem Hoang Lan +84 4 3946 2246 1510 [email protected]