jaiprakash associates limited (jal) -...

TRANSCRIPT

1

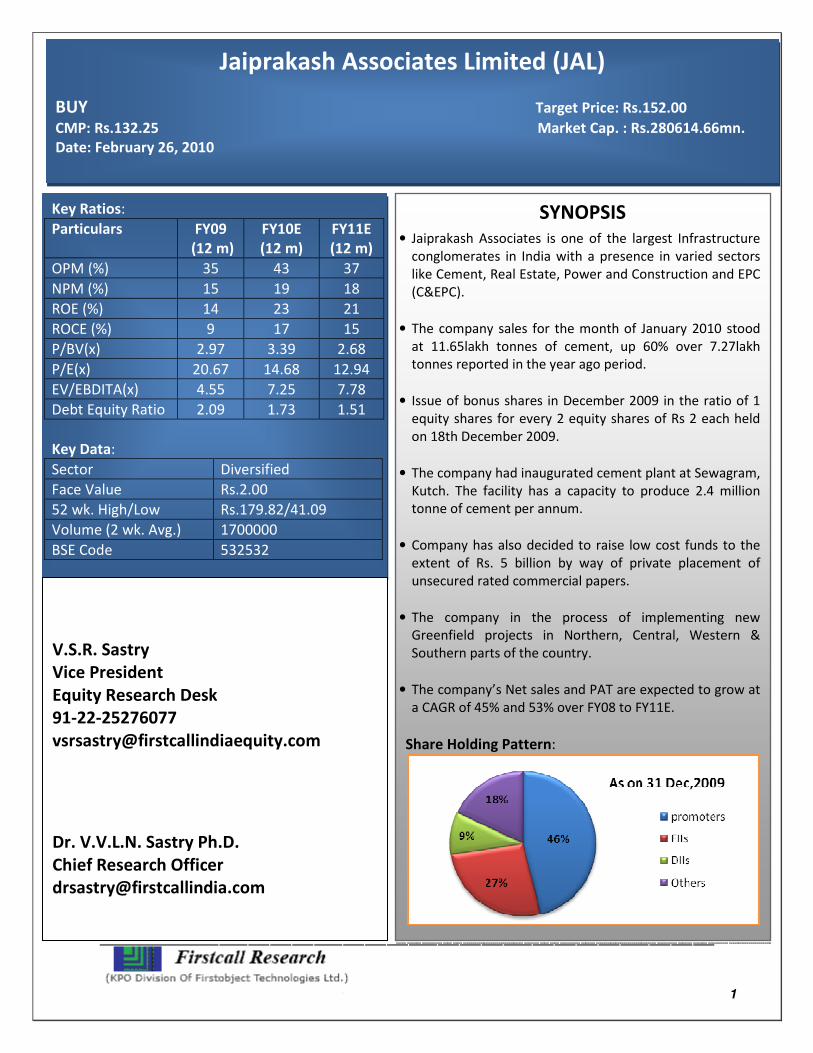

Jaiprakash Associates Limited (JAL)

BUY Target Price: Rs.152.00

CMP: Rs.132.25 Market Cap. : Rs.280614.66mn.

Date: February 26, 2010

Key Ratios:

Particulars FY09

(12 m)

FY10E

(12 m)

FY11E

(12 m)

OPM (%) 35 43 37

NPM (%) 15 19 18

ROE (%) 14 23 21

ROCE (%) 9 17 15

P/BV(x) 2.97 3.39 2.68

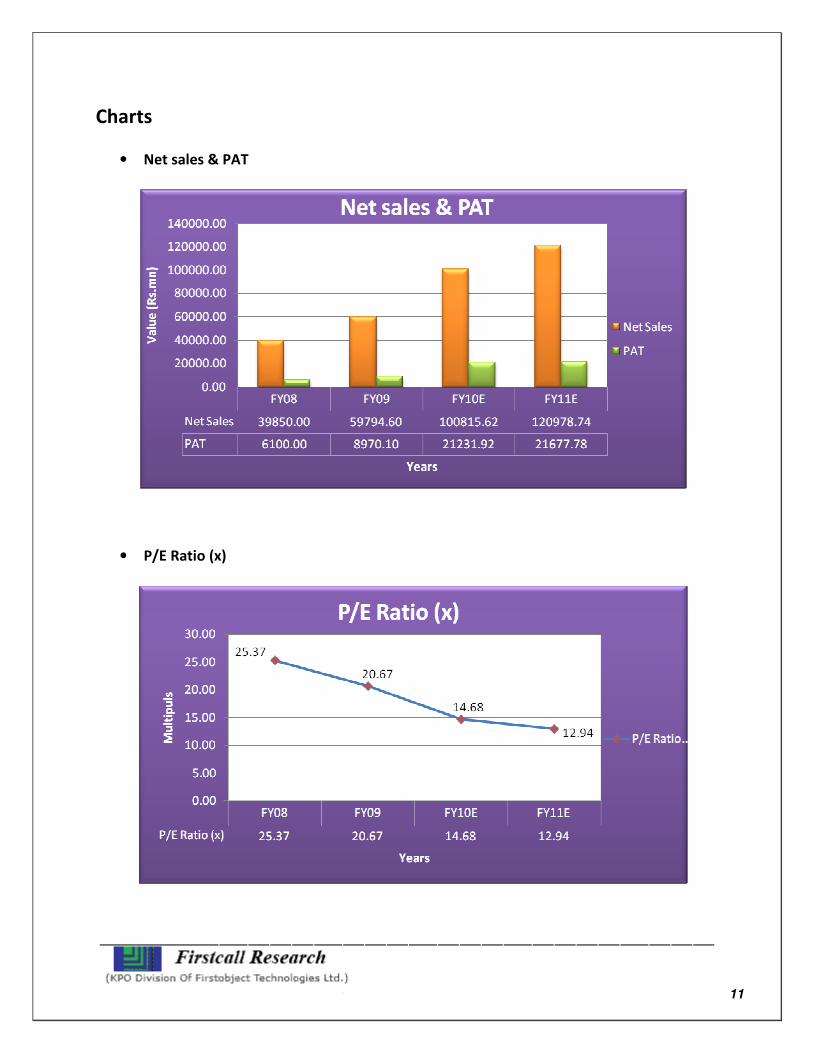

P/E(x) 20.67 14.68 12.94

EV/EBDITA(x) 4.55 7.25 7.78

Debt Equity Ratio 2.09 1.73 1.51

Key Data:

Sector Diversified

Face Value Rs.2.00

52 wk. High/Low Rs.179.82/41.09

Volume (2 wk. Avg.) 1700000

BSE Code 532532

SYNOPSIS

• Jaiprakash Associates is one of the largest Infrastructure

conglomerates in India with a presence in varied sectors

like Cement, Real Estate, Power and Construction and EPC

(C&EPC).

• The company sales for the month of January 2010 stood

at 11.65lakh tonnes of cement, up 60% over 7.27lakh

tonnes reported in the year ago period.

• Issue of bonus shares in December 2009 in the ratio of 1

equity shares for every 2 equity shares of Rs 2 each held

on 18th December 2009.

• The company had inaugurated cement plant at Sewagram,

Kutch. The facility has a capacity to produce 2.4 million

tonne of cement per annum.

• Company has also decided to raise low cost funds to the

extent of Rs. 5 billion by way of private placement of

unsecured rated commercial papers.

• The company in the process of implementing new

Greenfield projects in Northern, Central, Western &

Southern parts of the country.

• The company’s Net sales and PAT are expected to grow at

a CAGR of 45% and 53% over FY08 to FY11E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Peer Group Comparison 08

3. Key Concerns 08

4. Financials 09

5. Charts & Graph 11

6. Outlook and Conclusion 13

7. Industry Overview 14

3

Investment Highlights

• Result Updates Q3 FY10

For the third quarter, the top line of the company increased 115%YoY and stood at

Rs.29638.30mn against Rs.13806.30mn of the same period of the last year. The bottom

line of the company for the quarter stood at Rs.1030.20mn from Rs.1655.10mn of the

corresponding period of the previous year i.e., a decrease of 38%YoY.

EPS of the company for the quarter stood at Rs.0.49 for equity share of Rs.2.00 each.

4

Expenditure for the quarter stood at Rs.20776.10mn, which is around 93% higher than the

corresponding period of the previous year. Direct Construction, Manufacturing & Hotel /

Hospitality &power expenses of the company for the quarter accounts for 50% of the

sales of the company and stood at Rs.14958.90mn. Employee cost of the company for the

quarter accounts for 4% of the sales of the company and stood at Rs.1066.60mn.

OPM and NPM for the quarter stood at 30% and 3% respectively from 27% and 12%

respectively of the same period of the last year.

5

• Segment-Wise revenue for the quarter

Segment Revenue (Rs. million)

Construction 16430.50

Cement & Cement Products 9483.40

Real Estate 3455.50

Unallocated 399.30

Hotel/Hospitality & Golf Course 461.10

Investment 38.50

Wind Power 23.70

Total 30292.00

Less: Inter Segment Revenue -615.20

Net sales/income from Operations 29676.80

Turnover from Cement Division (including cement products) at Rs 948.34 crore v/s Rs

589.63 crore registering growth of 60.83%

The construction segment revenue grew 130% to Rs 1643.05 crore during the quarter

under review, while the cement and the real estate vertical also did phenomenally well.

Cement PBIT increased by 50% to Rs 236.39 crore and the construction segment PBIT

went up by 369% to Rs 410.71 crore.

Turnover from Engineering Division (including Real Estate, Hotels, Wind Power) at Rs

2037.08 crore v/s Rs 830.89crore registering a growth of 145.16%

6

The Company issued Bonus Shares on 19.12.2009 in the ratio of One Equity Share for

every Two Equity Shares of Rs.2/- each held on 18.12.2009. After issue of Bonus Shares,

Earnings per Share has been adjusted for the corresponding period of the previous year

During the quarter under report the Company issued 1,25,00,000 Equity Shares of Rs.2/-

each to a Trust for the employees under the "Jaypee Employee Stock Purchase Scheme,

2009" in accordance with the Scheme approved by the Share-holders. As per SEBI

Guidelines the difference between Market Price and Face Value has been debited to

Employee Compensation Expenses Account.

During the Quarter, FCCBs aggregating USD 10,000 [out of total FCCB-I of USD 100 Million

due on 17.02.2010] have been converted into 9,264 Equity Shares of Rs.2/- each at a

predetermined price of Rs.47.262 per share, thereby increasing the paid-up share capital

of the Company by Rs.18,528/- and Securities Premium by Rs.4,19,307/-.

• January sales

The company sales for the month of January 2010 stood at 11.65 lakh tonnes of cement,

up 60% over 7.27 lakh tonnes reported in the year ago period.

The company’s sales for the April-January period have increased by 40% to 86.17 lakh

tonnes from the corresponding period of the previous fiscal.

• Bonus issue

The Company issued Bonus Shares on 19.12.2009 in the ratio of One Equity Share for

every Two Equity Shares of Rs.2/- each held on 18.12.2009. After issue of Bonus Shares,

Earnings per Share has been adjusted for the corresponding period of the previous year

The company has received shareholders' approval for bonus issue through postal ballot on

December 08, 2009.

• Jaiprakash Associates starts Gujarat facility

Narendra Modi, chief minister of Gujarat inaugurated Jaiprakash Associates’ cement plant

at Sewagram, Kutch. The facility has a capacity to produce 2.4 million tonne of cement per

annum.

This Greenfield facility is expected to help the company to meet the growing demand

from the western region of the country. Following this inauguration, the total cement

capacity of the company has increased to 17.1 million tonne per annum. The company has

spent Rs 1,500 crore on the first phase of this project, which was completed in 33 months

time.

7

Further, the Jaypee Group Company is looking to augment its annual capacity to 35.55

million tonne by the fiscal year 2012.

• Jaiprakash Associates to mop-up Rs. 500 Crores

The company has received its board’s approval for raising low cost funds of up to Rs 500

crore through private placement of unsecured rated commercial papers.

The board has also decided to disinvest/ offer for sale 6 crore equity shares out of 121.50

crore equity shares of Rs 10 each held by the company in its subsidiary - Jaypee Infratech.

• ICRA retains CR1 construction grading of Jaiprakash Associates

Credit rating agency, ICRA has retained the grading assigned to Jaiprakash Associates (JAL)

at CR1 grade. CR1 grading indicates very strong contract Execution Capacity.

• Jaiprakash Associates May Look At Acquisition

The company rose about INR 11.90 billion through sale of treasury shares in bulk deals.

The company plans to use parts of the proceeds for a possible acquisition or setting up of

cement capacity in Maharashtra and overseas. "The funds raised will be used to finance

the proposed 360 mw captive power plants and add more cement capacity. And the fund

will not be used for debt repayment.

• CARE assigns `A+` rating to NCD issue of JP Asso

Credit rating agency, CARE has assigned the `CARE A+` rating to the proposed Long-term

Non Convertible Debentures (NCD) issue aggregating Rs 5,000 million of JAL. This rating is

applicable to facilities having tenure of more than one year.

Facilities with this rating are considered to offer adequate safety for timely servicing of

debt obligations. Such facilities carry low credit risk.

Instrument Amount (Rs. million) Rating

Long-term Debt

programme (proposed) 5000 CARE A+

Total 5000

8

Peer Group Comparison

Name of the

company

CMP(Rs.)

(As on

February

26, 2009)

Market Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E (x) P/BV

(x)

Dividend

(%)

Jaiprakash associates

ltd 132.25 280614.66 8.80 15.03 4.46 50.00

Unitech ltd 71.80 171515.90 1.69 42.49 5.69 5.00

IRB Infrastructure

Developers 252.80 84021.60 1.76 143.64 6.16 15.00

IVRCL Infrastructure

and Projects 321.85 42968.60 15.70 20.50 2.38 70.00

Hindustan

Construction

Company 133.90 40605.10 2.96 45.24 4.08 80.00

Key Concerns

� Slowdown in the economy could impact investment and activity in infrastructure and

adversely affect business.

� Increased competition in Engineering and Construction may put pressure on operating

margins.

� Recession in global economy

� Fluctuations in exchange rates

� Slow execution of orders

� Adverse Govt. policies

9

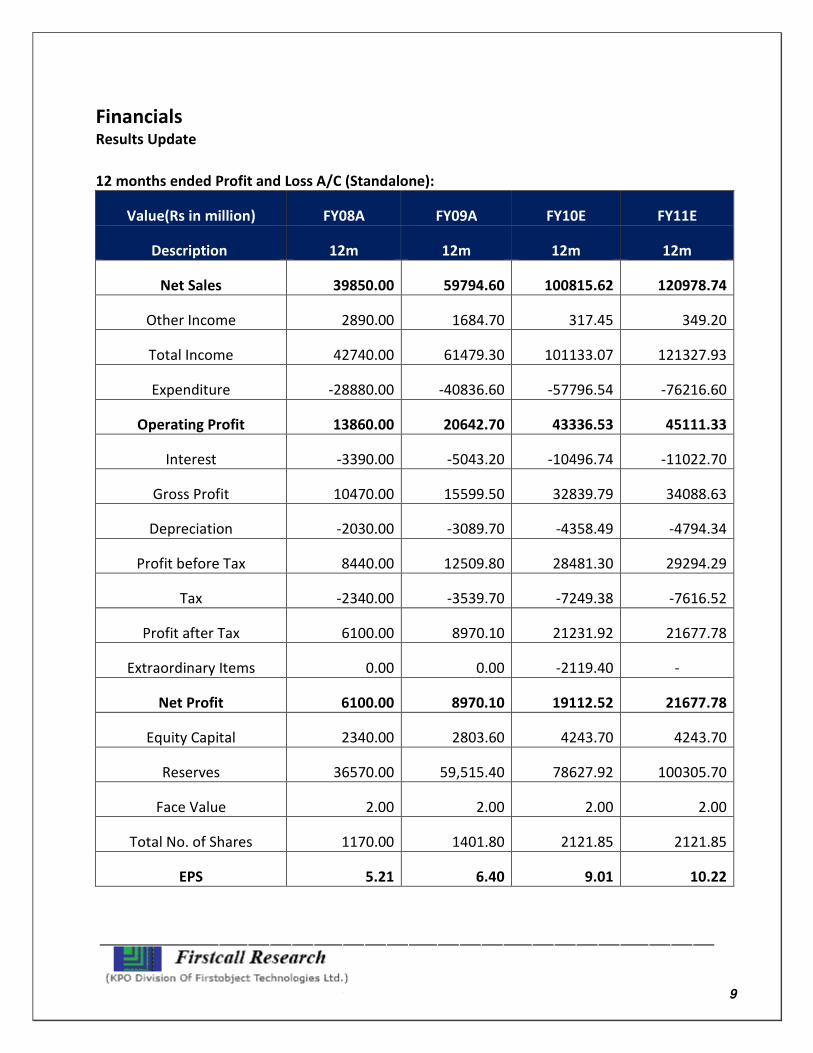

Financials Results Update

12 months ended Profit and Loss A/C (Standalone):

Value(Rs in million) FY08A FY09A FY10E FY11E

Description 12m 12m 12m 12m

Net Sales 39850.00 59794.60 100815.62 120978.74

Other Income 2890.00 1684.70 317.45 349.20

Total Income 42740.00 61479.30 101133.07 121327.93

Expenditure -28880.00 -40836.60 -57796.54 -76216.60

Operating Profit 13860.00 20642.70 43336.53 45111.33

Interest -3390.00 -5043.20 -10496.74 -11022.70

Gross Profit 10470.00 15599.50 32839.79 34088.63

Depreciation -2030.00 -3089.70 -4358.49 -4794.34

Profit before Tax 8440.00 12509.80 28481.30 29294.29

Tax -2340.00 -3539.70 -7249.38 -7616.52

Profit after Tax 6100.00 8970.10 21231.92 21677.78

Extraordinary Items 0.00 0.00 -2119.40 -

Net Profit 6100.00 8970.10 19112.52 21677.78

Equity Capital 2340.00 2803.60 4243.70 4243.70

Reserves 36570.00 59,515.40 78627.92 100305.70

Face Value 2.00 2.00 2.00 2.00

Total No. of Shares 1170.00 1401.80 2121.85 2121.85

EPS 5.21 6.40 9.01 10.22

10

Quarterly ended Profit and Loss A/C (Standalone):

Value(Rs. in million) 30-Jun-09 30-Sep-09 31-Dec-09 31-Mar-10E

Description 3m 3m 3m 3m

Net Sales 21168.60 18888.50 29638.30 31120.22

Other Income - 236.60 38.50 42.35

Total Income 21168.60 19125.10 29676.80 31162.57

Expenditure -12522.80 -4269.50 -20776.10 -20228.14

Operating Profit 8645.80 14855.60 8900.70 10934.43

Interest -2218.90 -2587.50 -2762.30 -2928.04

Gross Profit 6426.90 12268.10 6138.40 8006.39

Depreciation -1017.10 -1100.40 -1109.40 -1131.59

Profit before Tax 5409.80 11167.70 5029.00 6874.80

Tax -498.00 -2465.80 -1879.40 -2406.18

Profit after Tax 4911.80 8701.90 3149.60 4468.62

Extraordinary Items 0.00 0.00 -2119.40 -

Net Profit 4911.80 8701.90 1030.20 4468.62

Equity Capital 2803.60 2804.10 4243.70 4243.70

Face Value 2.00 2.00 2.00 2.00

Total No. of Shares 1401.80 1402.05 2121.85 2121.85

EPS 3.50 6.21 0.49 2.11

11

Charts

• Net sales & PAT

• P/E Ratio (x)

12

• P/BV (X)

• EV/EBITDA(X)

13

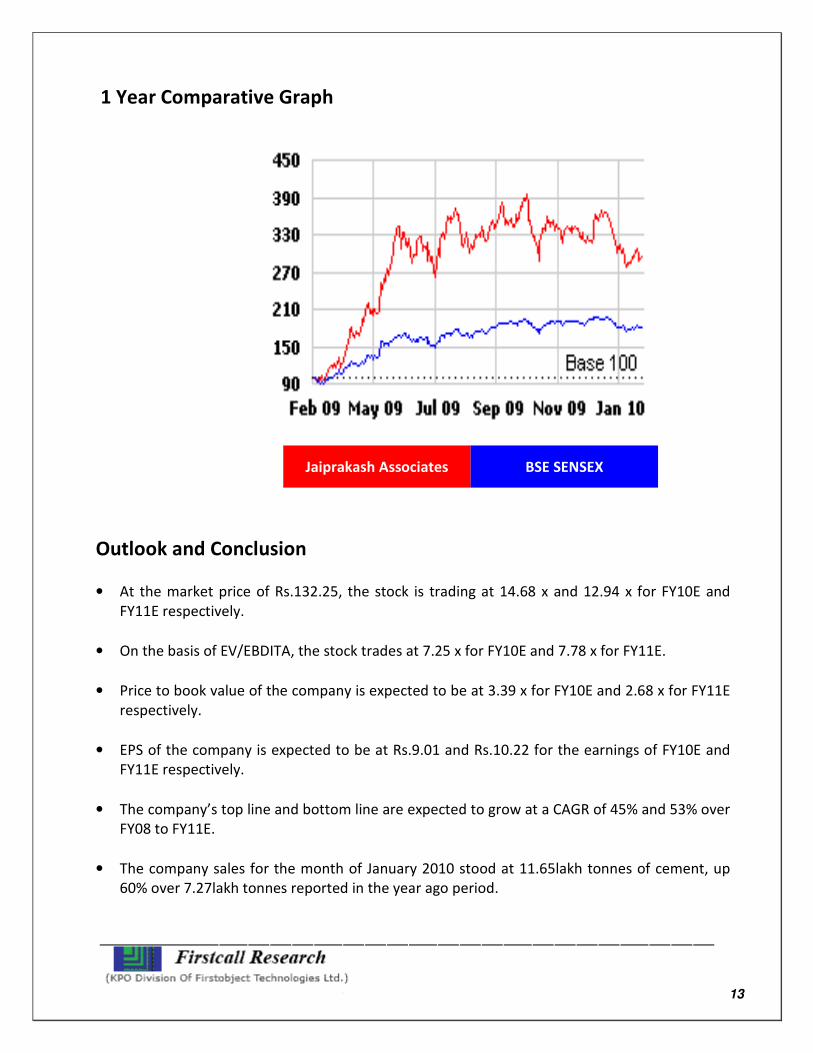

1 Year Comparative Graph

Outlook and Conclusion

• At the market price of Rs.132.25, the stock is trading at 14.68 x and 12.94 x for FY10E and

FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 7.25 x for FY10E and 7.78 x for FY11E.

• Price to book value of the company is expected to be at 3.39 x for FY10E and 2.68 x for FY11E

respectively.

• EPS of the company is expected to be at Rs.9.01 and Rs.10.22 for the earnings of FY10E and

FY11E respectively.

• The company’s top line and bottom line are expected to grow at a CAGR of 45% and 53% over

FY08 to FY11E.

• The company sales for the month of January 2010 stood at 11.65lakh tonnes of cement, up

60% over 7.27lakh tonnes reported in the year ago period.

Jaiprakash Associates BSE SENSEX

14

• The company in the process of implementing new Greenfield projects in Northern, Central,

Western & Southern parts of the country.

• Issue of bonus shares in December 2009 in the ratio of 1 equity shares for every 2 equity

shares of Rs 2 each held on 18th December 2009.

• The company inaugurated cement plant at Sewagram, Kutch. The facility has a capacity to

produce 2.4 million tonne of cement per annum. This Greenfield facility is expected to help

the company to meet the growing demand from the western region of the country. Following

this inauguration, the total cement capacity of the company has increased to 17.1 million

tonne per annum. The company has spent Rs 1,500 crore on the first phase of this project,

which was completed in 33 months time.

• Company has also decided to raise low cost funds to the extent of Rs. 5 billion by way of

private placement of unsecured rated commercial papers.

• We recommend ‘BUY’ with a target price of Rs.152.00 for medium to long term.

Industry Overview

Infrastructure

The country’s infrastructure sector accelerated by 5.3 per cent in November 2009, backed

primarily by growth in steel and cement production in the month. The six core sectors, which

contribute 26.7 per cent to the overall Index for Industrial Production (IIP), had grown 0.8 per

cent in the corresponding month of 2008. Finished (carbon) steel production grew at the highest

rate—11.7 per cent—during the month, against a decline of 6.3 per cent in the corresponding

period of 2008. Cement production also picked up to post a growth rate of 9 per cent in

November, marginally up from 8.7 per cent in the month in 2008. Production of petroleum

refinery products also grew by 4.9 per cent on a year on year basis, as against a contraction of 1.1

per cent in the year ago period.

Infrastructure investment in India is set to grow dramatically. India has become a major

outbound investor and people are engaging with Indians to seek investment into their countries,

said the Minister for Road Transport and Highways, Mr. Kamal Nath, in Davos. According to

investment banking company Goldman Sachs, India's infrastructure sector will require US$ 1.7

trillion investment in the next 10-years. It also added that such investment would come more

from the domestic market than overseas.

Furthermore, India is likely to emerge as a major hub for production of quality steel products,

according to Ratan Jindal, vice-chairman, managing director and CEO of Jindal Stainless Steel

15

(JSL). The International Steel Exhibition ‘Indinox’, to be held at Ahmadabad in January, will

portray India as a major destination for manufacturing steel products. The domestic demand,

especially from the railways, and varied use of stainless steel, will also act as a catalyst in growth

of the steel industry in India.

Notably, truck sales, a key indicator of goods movement, zoomed by an astronomical 201.1 per

cent in December 2009. According to data released by the Indian Foundation for Transport

Research and Training (IFTRT), though April-December truck sales rose by 11.9 per cent, the

normally weak off take month of December belied all calculations by registering a 201.09 per

cent jump in the sales of trucks in the 5-49 tonne range and operating on intra-state,

countersigned inter-state and on national permit routes.

Meanwhile, the public private partnership appraisal committee (PPPAC) has given its nod for the

proposed US$ 806.4 million mega container terminal at the Chennai port. The port trust is likely

to award the project by March 2010. The project would be developed in phases between 2013

and 2018. The Tuticorin Port Trust (TPT) is planning to award projects worth US$ 371 million over

the next two years. The proposed investment would enable the port to increase its cargo

handling capacity by another 20 million tonnes.

Safexpress, one of the largest supply chain and logistics Companies in India, has launched its

ultra-modern logistics park in Pune. This is company’s ninth warehouse in India.

The Rajasthan State Industrial and Investment Corporation Limited (RIICO) has signed a

memorandum of understanding (MoU) with Container Corporation of India Limited (Concor) to

set up a US$ 75.23 million multi-model logistic park (MMLP) in the state. The park would have

facilities for a container yard, a modern container handling system, cargo handling, warehousing,

etc.

Ports

India's logistics sector is witnessing increased activity—the country's major ports have posted a

12.8 percent year-on-year (y-o-y) rise in cargo volumes in November 2009. The Public Private

Partnership Appraisal Committee (PPAC) has approved four projects worth over US$ 897.7 million

to be developed through the public-private partnership (PPP) mode in a move to boost capacity

at the major ports in the country. The four port projects have been cleared by a panel headed by

Mr Ashok Chawla, Finance Secretary. These include projects for development of a mega container

terminal at the Chennai Port, a project to develop a multi-purpose berth at the Paradip Port in

Orissa, development of the second North Cargo Berth at Tuticorin Port in Tamil Nadu and

development of a container terminal at the New Mangalore Port.

The Cabinet Committee on Infrastructure (CCI) has approved a proposal to develop the fourth

container terminal at the Jawaharlal Nehru Port (JNPT), the country's busiest port, at an

estimated cost of US$ 1.44 billion. The government also cleared a proposal to build standalone

16

container handling facility at Mumbai port at a cost of US$ 129.6 million. The project would be

implemented within two years from the date of the award of the project. Meanwhile, cargo

handled by the major ports in the country, a key indicator of economic activity, grew for the fifth

consecutive month at 49.1 million tonnes (MT) compared to 45.3 MT in the corresponding month

last year. According to data from the Indian Ports Association (IPA), for the third quarter ended

December 2009, the major ports have registered cargo growth of 10.7 per cent compared to the

same period last year, while sequential growth has been 9.7 per cent.

Airports

Flying high on strong economic recovery, domestic air travel has made a comeback in 2009, with

traffic registering an increase of 7.9 per cent over the previous year. The increase to 44,510,000

flyers in 2009 came on the strong revival in traffic since July 2009. Jet and Kingfisher operated

over 70 percent of their fleet with budget airlines. The combined market share of IndiGo,

SpiceJet, JetLite and Go Air was 38.5 per cent.

Mumbai Airport posted its highest ever monthly passenger traffic in its history in December 2009.

According to Mumbai International Airport (MIAL), the Chhatrapati Shivaji International Airport

(CSIA) saw a record 2.53 million passengers in December 2009. This number is the highest-ever

passenger volume handled by the airport in its history, with the previous high standing at 2.38

million passengers in January 2008.

The government has mandated MIAL with the task of upgrading and modernising CSIA, which is a

joint venture between the Airports Authority of India and the GVK-SA consortium.

Railroads

Indian Railways' revenue earnings have increased by 8.74 per cent to an estimated US$ 11.97

billion during April-November 2009, compared with US$ 10.29 billion during the same period last

year. Total earnings from goods traffic went up by 8.56 per cent to US$ 8.04 billion during April-

November 2009 from US$ 6.92 billion during April-November 2008. During this period, the

Railways carried 574.38 MT of revenue freight traffic, registering an increase of 7.44 per cent

over the 534.6 MT carried during the corresponding period last year. During the first eight

months of the financial year 2009-10, total passenger revenue earnings increased by 8.01 per

cent to US$ 3.36 billion from US$ 2.91 billion during the same period last year.

According to the Department of Industrial Policy and Promotion (DIPP), the foreign direct

investment (FDI) inflow into railways related components has been US$ 77.49 million from April

2000 to September 2009. A quarterly estimate for Q2, 2009-10 for railways by the Central

Statistical Organisation suggests growth rates at 11.2 per cent and 6.3 per cent for net tonne km

and passenger km, respectively.

Roads

17

The CCI has approved the widening of over 445 km of national highways at an estimated cost of

US$ 950 million, which will be undertaken by the National Highways Authority of India (NHAI) in

the design-build-finance-operate-transfer (DBFOT) mode.

One of the projects is four-laning of 83.85 km Godhra-Gujarat/Madhya Pradesh border section on

National Highways in Gujarat (total project cost is estimated at US$ 156.55 million; concession

period is 27 years, including a construction period of 30 months). Besides, the Government would

also meet the expenditure amounting to US$ 24.5 million for land acquisition and other pre-

construction activities for the project.

The CCI gave its nod to for a six-laning project of 54.83 km stretch on the Chengapalli to start of

Coimbatore bypass section and four-laning of 13 km on the end of Coimbatore bypass to Tamil

Nadu/Kerala border section. The total project cost is estimated at US$ 186.2 million, with a

concession period of 27 years. Another approval was for a project to four lane 155.15 km Indore-

Jhabua-Gujarat/Madhya Pradesh border section. The total project cost is estimated at US$

256.55 million after restructuring under the DBFOT pattern. The concession period is for 25 years,

including a construction period of 30 months, said an official release.

The CCI also gave its nod to implement four-laning of Haridwar-Dehradun on DBFOT basis in

annuity mode. The total project cost is estimated at US$ 104.4 million.

Another project to be implemented is four-laning of 80 km stretch on Muzaffarnagar-Haridwar.

The total project cost is estimated at US$ 164.6 million, with a concession period for 25 years,

including a construction period of 910 days. The sixth project is four-laning 65.07 km long section

of Goa/Karnataka Border to Panaji (Goa). The total project cost is estimated at US$ 102.8 million

under the DBFOT pattern.

Anil Dhirubhai Ambani Group (ADAG)’s flagship company Reliance Infrastructure Ltd (R-Infra)

won a US$ 218.3 million road project from the Gujarat government, within a week after winning

the US$ 380 million Pune-Satara Road project from the National Highway Authority of India

(NHAI). The project is to execute a 71 kilometre four-six lane corridor connecting the ports of

Mundra and Kandla in Gujarat. The project has to be completed by December 2012 on a DBFOT

(toll) basis with a concession period of 25 years.

Recently, the elevated expressway between Silk Board junction and Electronic City junction, built

for US$ 165.5 million, was opened to public use. A consortium comprising Soma Enterprise Ltd,

Nagarjuna Construction Company and Maytas Infra Ltd constructed the 9.985 km long elevated

road project. The project, executed through a special purpose vehicle, Bangalore Elevated

Tollway Ltd, was built on a build operate transfer basis for the National Highways Authority of

India. The consortium has set up a highway traffic management system comprising of CCTV

surveillance of the roads, automatic traffic counters and classifiers, meteorological stations,

variable message signs and emergency call boxes for the road users. The consortium will operate

18

and maintain the roads in the stretch between Silk Board junction and inter-state border for the

next 18 years.

Investments

• Larsen & Toubro (L&T), the country’s largest engineering company, will invest around US$

5.46 billion to build its thermal power business in the next five years. L&T Power, the

wholly-owned subsidiary of L&T, will have a generation capacity of 5,500 MW, including

hydro power, by 2015. Larsen and Toubro Ltd also formed a Joint Venture with Malaysia-

based SapuraCrest Petroleum to install pipelines and construct offshore rigs and platforms

in India, the Middle East and South East Asia.

• Maersk India, part of the A.P. Moller-Maersk Group of Denmark, inaugurated its container

freight station (CFS) at Ponneri, around 25 km north off Chennai. It has invested around

US$ 10 million in the CFS, which will provide storage and ‘stripping' of laden import

containers and consolidation of export cargo, according to Mr Hans-Henrik Skonning

Hansen, South Asia Cluster Manager, Maersk India.

• Corus, a subsidiary of Tata Steel, has decided to invest US$ 50.38 million pounds at its rail

production facility in Hayange, France. The move has come after the Europe's second

largest steel maker secured contract worth US$ 503.79 million from the French railway

operator SNCF.

• York Transport Equipment, the Singapore-based axles/suspensions maker for heavy

commercial vehicles and part of the Tata group, will soon set up a second plant in India. It

already has one in Jamshedpur and is now on the lookout for a site in south-west India to

set up a facility with a capacity of 100,000 units. York was acquired by TRF, a Tata

company specialising in material handling equipment, in 2007. It has units in Singapore,

Australia and China with operations across half a dozen countries.

• Swiss cement company Holcim plans to invest US$ 1 billion in setting up 2-3 greenfield

manufacturing plants in the country in the next five years to serve the rising domestic

demand, according to a senior company executive.

• Tata Power has lined up investments of US$ 5.19 billion for its upcoming plants in

Mundra, Maithon and Jojobera over the next three years. Tata Power and Reliance Power

are coming up with UMPPs with a combined generation capacity of close to 16,000 MW.

Jindal Steel & Power, which has a production capacity of 1,000 MW, plans to add another

4,380 MW thermal power and 6,100 MW hydro power capacity in the next five years.

With this expansion as planned core sector engineers are required for boiler, turbine and

pump operations, and to also take care of the logistics.

According to the Central Electricity Authority (CEA), the country will require manpower of around

800,000 to keep the growth engine running over the next decade. The industry is likely to require

around 40,000 engineers for core sectors such as electrical, mechanical and instrumentation

every year since the average manpower-to-MW ratio here is close to 0.75.

Government Initiatives

19

The Government of India has envisaged capacity addition of 100,000 MW by 2012 to meet its

mission of power to all.

Recently, a ministerial group discussing large power plants with a capacity to generate 4,000 MW

of power has approved, in principle, a proviso requiring such plants that will be awarded in the

future to use local power generation equipment. The move is expected to provide a fillip to

domestic manufacturing. The decision on so-called ultra mega power plants, or UMPPs, will also

benefit domestic power generation equipment manufacturers such as state-owned Bharat Heavy

Electricals Ltd (Bhel) and Larsen and Toubro Ltd (L&T), which has a joint venture with Mitsubishi

Heavy Industries Ltd (MHI) of Japan. At least three joint ventures, between Toshiba Corp. of

Japan and JSW Group; Ansaldo Caldaie SpA of Italy and GB Engineering Enterprises Pvt. Ltd; and

Alstom SA of France and Bharat Forge Ltd are looking to start manufacturing power equipment in

India.

The Uttar Pradesh government has signed memorandum of understanding (MoU) with Lanco

Infratech Limited and Bajaj Hindusthan Limited for generation of 2,400 mega watt (MW) power in

the state. Under the terms and conditions of the MoU, Lanco would generate 1,320 MW and 660

MW power in Fatehpur and Anpara respectively, while Bajaj Hindusthan would generate a total

of 400 MW power at its five sugar mills in the state. Bajaj is the largest sugar producer in the

country and controls 16 mills in UP. The state government is targeting a total power generation

capacity of 25,000 mega watt (MW) by the end of the next 12th Five-Year Plan. The Asian

Development Bank (ADB) has approved a financial assistance for US$ 200 million under the

Assam Power Sector Enhancement Investment Programme. The project has some innovative

features like franchisee-based distribution, off grid electrification with renewable energy,

reduction in CHG emissions through efficiency gains. The road transport and highways ministry

has proposed priority sector status for road development, allowing private highway developers

more funds from banks.

Cement

Sector structure/Market size

India is the world's second largest producer of cement after China, with cement companies

adding nearly 11 million tonnes (MT) capacity during April-September 2009, taking the total

installed capacity to around 231 MT by September 2009.

With the boost given by the government to various infrastructure projects, road networks and

housing facilities, growth in the cement consumption is anticipated in the coming years.

According to Jyotiraditya Scindia, Minister of State, Ministry of Commerce and Industry, cement

production could rise to 236.16 MT in FY11 and touch 262.61 MT in FY12.

20

With almost total capacity utilisation levels in the industry, cement despatches have maintained a

10 per cent growth rate. Total despatches grew to 170 MT during 2007–08 as against 155 MT in

2006–07.

According to the Cement Manufacturer’s Association, cement despatches were 14.13 MT in

December 2009, showing a growth of 13 per cent as compared to 12.48 MT in December 2008.

During December 2009, cement production was 13.91 MT, registering a growth of 13 per cent as

compared to 12.31 MT in December 2008. Between April to December 2009, cement production

totaled 116.01 MT while cement despatches totaled 115.31 MT.

A few of the leading manufacturers are UltraTech/Grasim combine, Dalmia Cements, India

Cements, Holcim etc.

Technological change

Continuous technological upgrading and assimilation of latest technology has been going on in

the cement industry. Presently, 93 per cent of the total capacity in the industry is based on

modern and environment-friendly dry process technology and only 7 per cent of the capacity is

based on old wet and semi-dry process technology. There is tremendous scope for waste heat

recovery in cement plants and thereby reduction in emission level.

New Investments

• Dalmia Cement, South India’s second largest cement maker, will invest over US$ 652.6

million to add 10 MT capacity over the next 2-3 years.

• India Cements Ltd will invest US$ 104 billion to set up two thermal power plants in the

southern states of Tamil Nadu and Andhra Pradesh.

• Anil Ambani Group Company Reliance Infrastructure will invest US$ 2.1 billion to set up

cement plants with a total capacity of 20 mtpa over the next five years.

• Reliance Cementation, an Anil Dhirubhai Ambani Group (ADAG) company, plans to set up

a 5 MT integrated cement plant in Yavatmal district of Maharashtra at a cost of US$ 463.2

million.

• Swiss cement company Holcim plans to invest US$ 1 billion in setting up 2-3 greenfield

manufacturing plants in India in the next five years. The expansion will take the company’s

total cement-making capacity to 60 mtpa from 50 mtpa currently.

• Jaiprakash Associates Ltd will invest US$ 973.07 million to take its cement manufacturing

capacity from 20 mtpa to 33 mtpa by 2012.

• Chettinad Cement, the flagship company of the diversified Chettinad group, has chalked

out an aggressive expansion plan to boost its capacity to 13 mtpa in another four years

from its current capacity of 7.5 mtpa at an investment of US$ 259.42 million.

• Kolkata-based Shree Cement plans to invest US$ 432.38 million to increase its cement

output by two million tonnes to 12 MT by March 2010 and raise power generation

capacity by over four-fold by FY'12.

21

Mergers and Acquistions (M&As)

• Holcim strengthened its position in India by increasing its holding in Ambuja Cement from

22 per cent to 56 per cent through various open market transactions with an open offer

for a total investment of US$ 1.8 billion. Moreover, it also increased its stake in ACC

Cement with US$ 486 million, being the single largest acquirer in the cement sector.

• UltraTech Cement, a unit of conglomerate Aditya Birla Group, is absorbing sister unit

Samruddhi Cement, to form India's biggest cement firm.

• Leading foreign funds like Fidelity, ABN Amro, HSBC, Nomura Asset Management Fund

and Emerging Market Fund have together bought around 7.5 per cent in India's third-

largest cement firm, India Cements (ICL), for US$ 124.91 million.

• Cimpor, the Portugese cement maker, paid US$ 68.10 million for Grasim Industries' 53.63

per cent stake in Shree Digvijay Cement.

• Vicat SA, a French cement maker acquired a 6.67 per cent stake in Hyderabad-based Sagar

Cement for US$ 14.35 million.

• Dalmia Cement has increased its stake in OCL India to 45.4 per cent from 21.7 per cent at

an investment of US$ 38.26 million as part of its plan to expand its footprint in eastern

India.

Government Initiatives

Government initiatives in the infrastructure sector, coupled with the housing sector boom and

urban development, continue being the main drivers of growth for the Indian cement industry.

• Increased infrastructure spending has been a key focus area over the last five years

indicating good times ahead for cement manufacturers.

• The government has increased budgetary allocation for roads under National Highways

Development Project (NHDP).

• Appointing a coal regulator is looked upon as a positive move as it will facilitate timely and

proper allocation of coal (a key raw material) blocks to the core sectors, cement being one

of them.

Keeping in mind the global meltdown which is impacting the cement companies in India, the

government re-imposed the counter-veiling duty (CVD) and special CVD on imported cement in

January. This is likely to provide a level playing field to domestic companies.

Road Ahead

According to a report by the ICRA Industry Monitor, the installed capacity is expected to increase

to 241 MTPA by FY 2010-end. India's cement industry is likely to record an annual growth of 10

per cent in the coming years with higher domestic demand resulting in increased capacity

utilisation.

22

Real estate

The Indian real estate sector plays a significant role in the country's economy. The real estate

sector is second only to agriculture in terms of employment generation and contributes heavily

towards the gross domestic product (GDP). Almost five per cent of the country's GDP is

contributed to by the housing sector. In the next five years, this contribution to the GDP is

expected to rise to 6 per cent.

According to Jones Lang LaSalle, faster economic growth in Brazil, Russia, India and China (BRIC)

could result in the property markets of those nations recovering at a faster rate than the UK and

US real estate markets. It has also been suggested that India's property sector could begin to

improve from late 2009 and may attract up to US$ 12.11 billion in real estate investment over a

five-year period.

Almost 80 per cent of real estate developed in India is residential space, the rest comprises of

offices, shopping malls, hotels and hospitals. According to the Tenth Five Year Plan, there is a

shortage of 22.4 million dwelling units. Thus, over the next 10 to 15 years, 80 to 90 million

housing dwelling units will have to be constructed with a majority of them catering to middle-

and lower-income groups.

Moreover, India leads the pack of top real estate investment markets in Asia for 2010, according

to a study by PricewaterhouseCoopers (PwC) and Urban Land Institute, a global non-profit

education and research institute.

The report, which provides an outlook on Asia-Pacific real estate investment and development

trends, points out that India, particularly Mumbai and Delhi, are good destinations. Residential

properties are viewed as more promising than other sectors and Mumbai, Delhi and Bangalore

top the pack in the hotel ‘buy' prospects as well.

The study is based on the opinions of over 270 international real estate professionals, including

investors, developers, property company representatives, lenders, brokers and consultants.

Apart from the huge demand, India also scores on the construction front. A McKinsey report

reveals that the average profit from construction in India is 18 per cent, which is double the

profitability for a construction project undertaken in the US.

The real estate sector is also likely to get a boost from Real Estate Mutual Funds (REMFs) and Real

Estate Investment Trusts (REITs). In fact, according to a CRISIL paper, the REITs would have the

potential to hold at least 5 per cent share of the total global real estate market by 2010, the size

of which would reach US$ 1,400 billion in the next three years. The paper titled, ‘Indian REITs; Are

We Prepared', says that by 2010, REITs alone would hold a market size of US$ 70 billion of the

total real estate market as its concept is gaining ground in countries like India and other

developing nations.

23

According to the Federation of Indian Chambers of Commerce and Industry (FICCI), the Indian

real estate sector is likely to experience consolidation wherein bigger players may opt for outright

buy of smaller firms or forge joint ventures or business alliances with them.

Foreign direct investment (FDI) into India in the real estate sector for the fiscal year 2008-09 has

been US$ 12.62 billion approximately, according to the latest data given by the Department of

Policy and Promotion (DIPP).

Moreover, buoyed by positive market sentiment and demand revival in housing, four real estate

companies—Emaar MGF Land, Lodha Developers, Sahara Prime City and Ambience Ltd—are

looking to mop-up over US$ 2.35 billion through public offerings.

New Projects

• Zuri Group Global is planning to invest about US$ 247.5 million towards setting up five-

star business hotels and luxury residential properties over the next three years.

• An investment of US$ 627.3 million will be made by industries in the Aeropsace and

Precision Engineering Special Economic Zone at Adibatla, Andhra Pradesh.

• Unitech will invest US$ 853.42 million in construction of up to 30 million sq ft of

residential and commercial spaces to be launched by next year.

• Real estate developer The 3C Company will develop an affordable housing project over 41

acres of land in Noida at an investment of US$ 519.93 million.

• A consortium consisting of the Essel Group and Delhi-based Bhushan Steel and Power will

develop an amusement, theme and knowledge city over 250 acres at Kharghar in Navi

Mumbai. The total value of the transaction is US$ 454.95 million making it, in absolute

terms, one of the largest real estate transactions in India.

• Tata Realty and Infrastructure Limited (TRIL) will develop a US$ 758.47 million IT Special

Economic Zone (SEZ) in Chennai.

Government Initiatives

The government has introduced many progressive reform measures to unlock the potential of

the sector and also meet increasing demand levels. The stimulus package announced by the

government, coupled with the Reserve Bank of India's (RBI) move allowing banks to provide

special treatment to the real estate sector, is likely to impact the Indian real estate sector in a

positive way. RBI has decided to extend exceptional concessional treatment to the commercial

real estate exposure which are restructured, up to June 30, 2009.

• 100 per cent FDI allowed in realty projects through the automatic route.

• In case of integrated townships, the minimum area to be developed has been brought

down to 25 acres from 100 acres.

• Urban Land (Ceiling and Regulation) Act, 1976 (ULCRA) repealed by increasingly larger

number of states.

24

• Minimum capital investment for wholly-owned subsidiaries and joint ventures stands at

US$ 10 million and US$ 5 million, respectively.

• Full repatriation of original investment after three years.

• 51 per cent FDI allowed in single-brand retail outlets and 100 per cent in cash-and-carry

through the automatic route.

The 2009-10 budget has also given sops to the realty sector. Developers of affordable housing

projects (units of 1,000-1,500 sq ft) have been granted a tax holiday on profits from projects

initiated in the financial year 2007-08. Such projects would have to be completed before March 1,

2012.

At the same time, the finance minister allocated US$ 207 million to grant a 1 per cent interest

subsidy on home loans up to US$ 20,691, provided the cost of the home is not more than US$

41,382. This subsidy is expected to give a further boost to the housing sector.

Road Ahead

According to the Confederation of Real Estate Developers' Associations of India (CREDAI), the

affordable housing segment is set to play an important role in India's real estate sector in 2010 on

the back of an uptick in demand.

Moreover, 2010 is expected to be a positive year for the real estate sector. The revival is

expected to be driven by infrastructure growth, which, in turn, can accelerate real estate

activities both in the residential as well as commercial spaces.

____________________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other sources

believed to be reliable but we do not represent that it is accurate or complete and it should

not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s affiliates shall

not be in any way responsible for any loss or damage that may arise to any person from any

inadvertent error in the information contained in this report. This document is provide for

assistance only and is not intended to be and must not alone be taken as the basis for an

investment decision.

25

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

Other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com